Israel Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

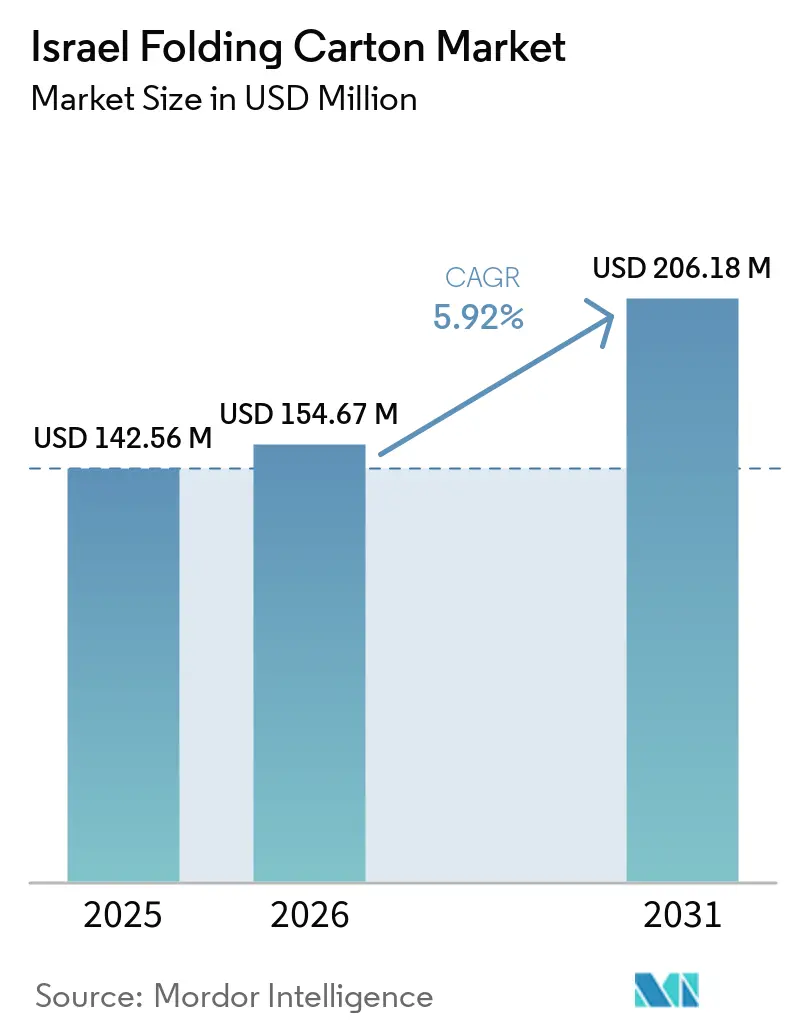

| Base Year Market Size (2025) | USD 142.56 Million |

| Market Size (2026) | USD 154.67 Million |

| Market Size (2031) | USD 206.18 Million |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

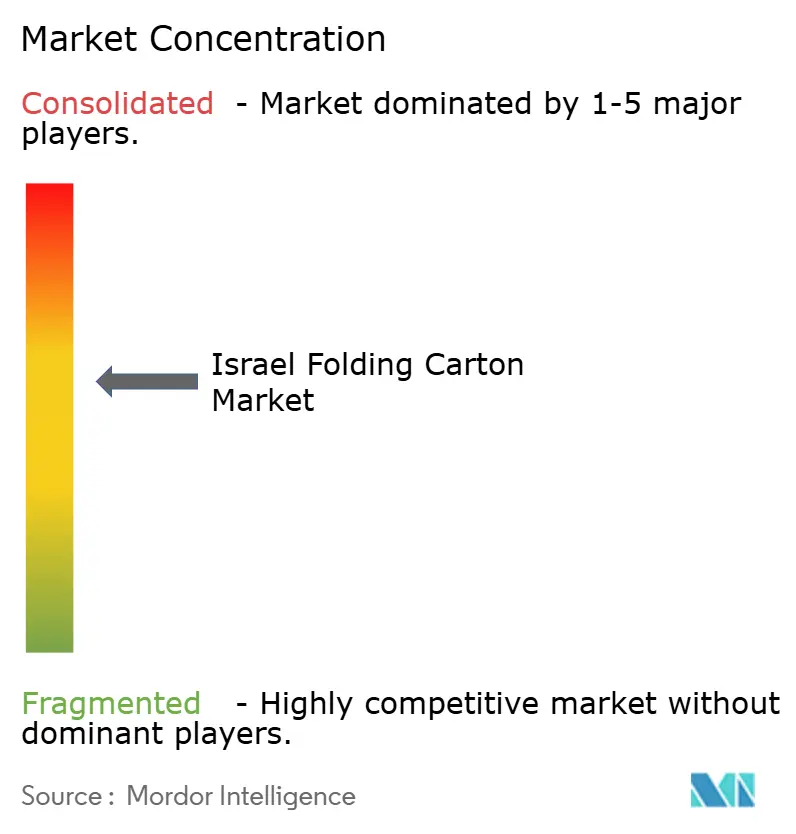

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Folding Carton Market Analysis by Mordor Intelligence

The Israel Folding Carton Market size is projected to be USD 142.56 million in 2025, USD 154.67 million in 2026, and reach USD 206.18 million by 2031, growing at a CAGR of 5.92% from 2026 to 2031. The headline numbers reflect structural shifts more than cyclical swings, as government-backed e-commerce programs, quick-service restaurant delivery demand, and pharmaceutical export compliance realign packaging specifications. Brand owners are gravitating toward barrier-grade-coated substrates for chilled and ambient foods, while converters are turning to digital printing for kosher and bilingual SKU personalization. Constrained domestic virgin-pulp supply has elevated the strategic value of recycled-fiber capacity, while regulatory alignment with European Union norms is reducing import-testing friction while tightening recyclability rules. Competitive intensity is rising as larger converters pivot into flexible and technical packaging, leaving the commodity folding-carton supply to smaller regional players.

Key Report Takeaways

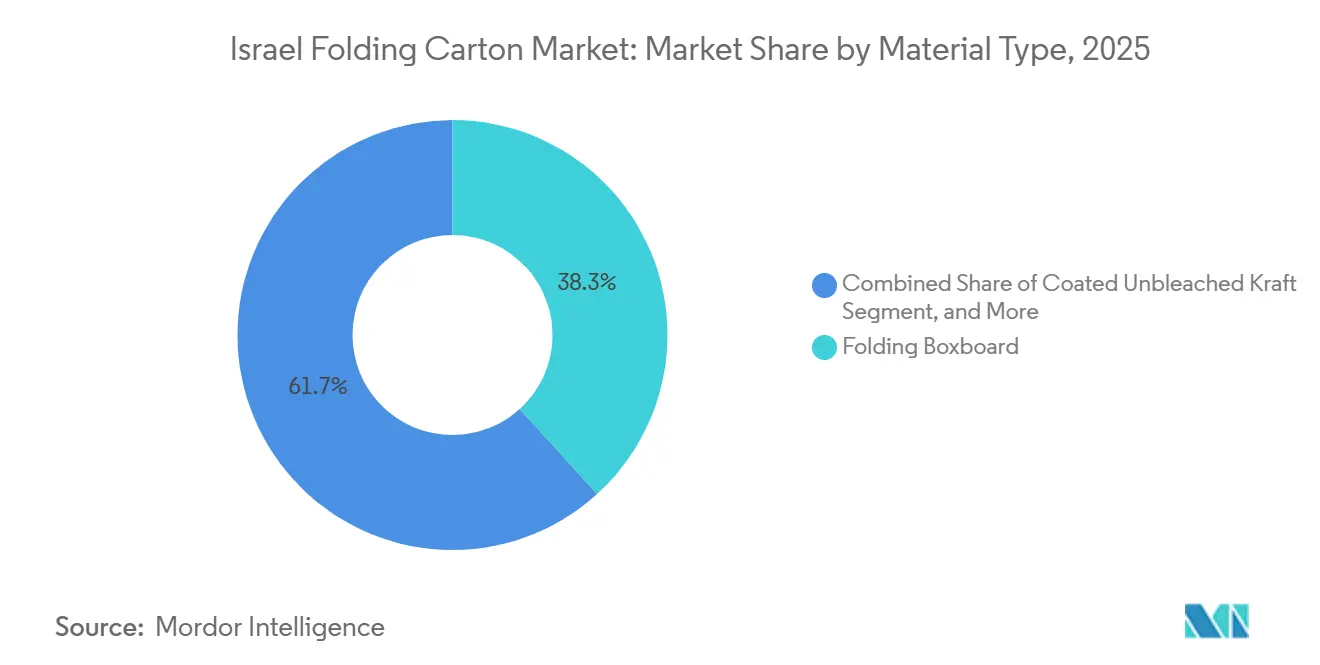

- By material type, folding boxboard captured with 38.26% of the Israel folding carton market share in 2025.

- By printing technology, the Israel folding carton market size for digital printing is projected to grow at a 6.59% CAGR to 2031.

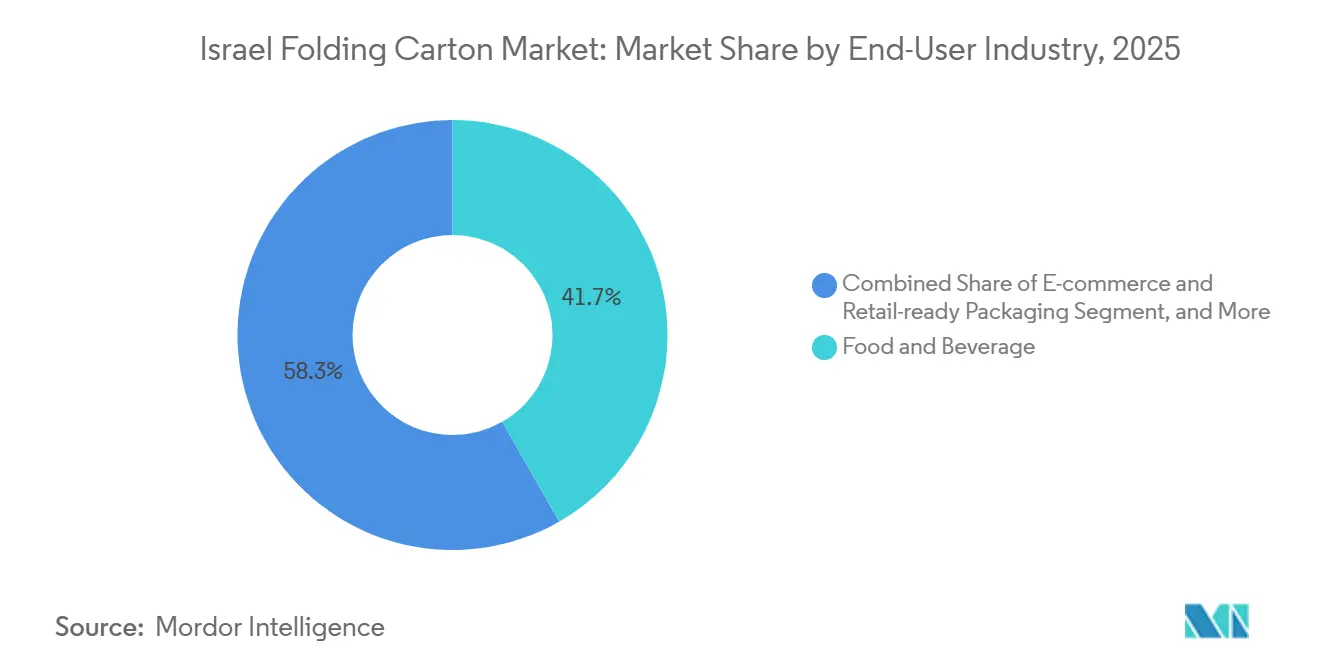

- By end-user industry, the food and beverage industry captured 41.73% of the Israel folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Israel Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Recyclable Packaging Among Israeli Food Brands | +1.2% | National, Central District and Haifa Bay hubs | Medium term (2-4 years) |

| Expansion of Quick-Service Restaurant Delivery Channels | +0.9% | Tel Aviv, Jerusalem, Haifa metros | Short term (≤ 2 years) |

| Rising E-commerce Penetration in Peripheral Regions | +1.1% | Negev, Galilee, Southern District | Medium term (2-4 years) |

| Integration of Digital Print for SKU-Level Personalization | +0.7% | National HP Indigo ecosystems | Long term (≥ 4 years) |

| Government Tax Incentives for Lightweight Paperboard Substitutes | +0.5% | National | Long term (≥ 4 years) |

| Mainstream Shift Toward Low-Migration Inks in Pharmaceuticals | +0.6% | Modi'in and Rehovot clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Recyclable Packaging Among Israeli Food Brands

Food majors have elevated recyclability from marketing promise to supplier prerequisite. Strauss Group achieved an 86% packaging-recyclability rate in 2023 and targets 100% by 2030, prompting converters to develop FSC-certified, high-recycled-content board and low-migration ink systems. Tnuva invested NIS 135 million (USD 37 million) in seven milk-carton lines over five years, locking in demand for coated grades built around thinner, recycled substrates. Israel’s Packaging Law, enforced by Tamir Corporation, mandates 60% recycling for paper and board, and since July 2024, class-action certifications have emerged against non-compliant firms, forcing converters to audit material flows.

Expansion of Quick-Service Restaurant Delivery Channels

Third-party delivery apps and ghost kitchens are reshaping performance specs for food cartons. Google Israel’s Shopping IL workshops onboarded nearly 3,000 small firms to digital sales, boosting carton demand that survives condensation, grease, and motorcycle transit. The Ministry of Economy’s NIS 600 million (USD 160 million) support package channels contracts to domestic converters, although a 17% skilled-technical vacancy in Rishon LeZion slows capacity expansion. Cartons must now deliver barrier integrity equivalent to that of flexible formats, spurring the uptake of coated unbleached kraft in hot-food segments.

Rising E-commerce Penetration in Peripheral Regions

Israel’s online revenue is forecast to climb from USD 7.70 billion in 2025 to USD 11.03 billion by 2029, and peripheral regions will supply a disproportionate share of incremental orders. Retail-ready cartons optimized for automated fulfillment must meet forthcoming EU rules requiring a maximum 50% empty space, so converters invest in wraparound and display-ready designs that can reduce board use by up to 15%.[1]T.M.I.R. Corporation, “The Packaging Law,” tmir.org.il Trade-facilitation reforms cut distance-related costs by 9%, shortening lead times for imported coated board.

Integration of Digital Print for SKU-Level Personalization

HP Indigo’s Israeli R&D hub enables converters to print kosher, bilingual, or seasonal runs without litho plate changes. In February 2026, a USD 50 million HP Indigo 200K deal with ePac signaled that AI-driven defect detection and real-time color management were reaching industrial scale. The technology supports pharmaceutical low-migration ink requirements under EU Regulation 1935/2004, lowering compliance risk for export-oriented drugmakers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Imported Virgin Pulp Prices | -0.8% | National | Short term (≤ 2 years) |

| Competition From Flexible Stand-Up Pouches in Snacks | -0.7% | National snack and confectionery segments | Medium term (2-4 years) |

| Chronic Skilled-Labor Shortage in Israeli Converting Plants | -0.6% | Central District, Haifa Bay | Medium term (2-4 years) |

| Stringent Solid-Waste Landfill Levies | -0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Imported Virgin Pulp Prices

Eucalyptus pulp now trades at USD 560-590 per tonne and NBSK near USD 1,710, squeezing converters without recycled-fiber assets. Infinya Containerboard’s 1,080 tons/day OCC line in Hadera mitigates risk by supplying recycled fluting and linerboard. Smaller plants lack similar hedges, cannot lock long-term pulp contracts, and face shekel-currency exposure that erodes margins.

Competition From Flexible Stand-Up Pouches in Snacks

Mono-material pouches with resealable zippers are migrating snack and confectionery volumes away from cartons. Aran Group’s MonoFlex pouch earned a 2026 Star of Israel award and passes European recyclability tests, demonstrating that flexibles can meet barrier and sustainability targets. Tadbik’s polyolefin shrink sleeves weigh 20-30% less than PET variants and integrate with existing PET recycling streams, underscoring the performance-plus-eco advantage that cartons must counter through graphics, tamper-evidence, and on-shelf display value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Coated Grades Target Barrier-Sensitive Foods

Folding boxboard delivered 38.26% Israel folding carton market share in 2025 on the strength of dry-food and confectionery demand. Coated unbleached kraft shows a forecast 7.35% CAGR because chilled, moist, and greasy products require moisture and grease resistance, a trend validated by Tnuva’s latest milk-carton line. Solid bleached sulfate serves export-oriented pharmaceuticals and cosmetics that need high brightness and certified low-migration coatings. White-lined chipboard loses traction as food brands mandate higher recycled-content thresholds under Tamir enforcement.

Domestic supply is evolving. Stora Enso’s EUR 1 billion (USD 1.1 billion) Oulu line adds 750,000 tons of folding boxboard and coated unbleached kraft, cutting lead times for Israeli importers.[2]PrintIndustry.News, “Stora Enso Launches New Containerboard Line,” printindustry.news Mondi’s multi-site EUR 1.2 billion (USD 1.3 billion) expansion delivers 500,000 tons of virgin and recycled containerboard, improving access to certified recycled content. January 2025 regulatory harmonization with the EU removes duplicate testing, accelerating qualification of these imports. As a result, Israel's folding carton market for barrier-grade coated boards is set to expand more quickly than overall volume growth.

By Printing Technology: Digital Gains on Short-Run Economics

Lithographic printing accounted for 44.59% Israel folding carton market size in 2025 because it balances unit cost and color fidelity on long runs. Digital printing, however, is forecast to grow 6.59% annually, as HP Indigo presses enable kosher and bilingual SKUs without plate changes. Flexographic printing sits between the two, covering cost-sensitive mid-volume jobs and corrugated hybrids; FlexiPack’s Hontec FlexiCon460-7C installation illustrates LED-UV energy savings. Gravure remains confined to ultra-long export runs where cylinder amortization is justified.

Digital’s higher per-unit cost limits penetration to premium or variable-data cartons, yet its AI-based defect analytics trim waste and bolster brand sustainability goals. EU low-migration ink rules drive water-based and soy-based digital ink adoption, a compliance advantage that litho platforms struggle to match. Consequently, Israel's folding carton market share for digital presses will continue to expand across pharmaceuticals, nutraceuticals, and limited-edition food SKUs.

By End-User Industry: E-commerce Packaging Outpaces Staples

Food and beverage retained 41.73% of the Israel folding carton market share in 2025, underpinned by demand from Tnuva and Strauss Group. Yet e-commerce and retail-ready cartons will expand at 7.18% CAGR as Shopping IL and government procurement integrate small businesses into direct-to-consumer channels. These packs must be right-sized for automated fulfillment and comply with EU empty-space restrictions, driving innovation in wraparound and shelf-ready formats.

Pharmaceuticals, personal care, and electronics require premium boards, tamper-evident packaging, and serialized barcodes, which sustain higher average selling prices even at lower volumes. Tobacco and household goods remain flat, pressured by flexible pouch substitution and landfill-levy costs. Israel's folding carton industry players that can serve both high-volume e-commerce shippers and low-volume regulated exporters are best positioned for balanced growth.

Geography Analysis

Central District and Haifa Bay dominate consumption due to their dense populations, proximity to ports, and clustering of large food processors. Automation investments totaling NIS 180 million (USD 50 million) have modernized lines, but a 17% skilled-technician vacancy and 94-day time-to-fill delay new capacity.[3]KiTalent, “Automation Created a Harder Hiring Problem,” kitalent.com Infinya’s Hadera OCC mill secures recycled fluting for nearby converters, reinforcing circular-economy credentials.

Peripheral regions, Negev, Galilee, and the Southern District, exhibit faster e-commerce growth as logistics networks mature. Government procurement rules that favor Israeli-sourced cartons and a NIS 600 million (USD 160 million) support fund stimulate converter contracts, yet limited collection infrastructure constrains local recycled-fiber feedstock, increasing reliance on imported board. January 2025 EU-alignment reforms have shortened testing cycles, enabling quicker import substitution where domestic supply falters.

Trade-facilitation measures shaved 9% off distance-related costs, reducing port clearance times and fostering cross-border cartons shipped to EU markets. However, the impending EU Packaging and Packaging Waste Regulation standards, the 50% maximum empty space requirement, and select plastic bans force converters to redesign boxes for export clients by 2027. Kosher certification, still obligatory for most packaged foods, adds cost and labeling complexity, anchoring demand for variable-data printing and multilingual packaging.

Competitive Landscape

The Israel folding carton market competition is moderately concentrated. Plasto-Kargal commands around 25% of domestic packaging turnover yet focuses on flexible and semi-rigid formats, leaving folding-carton capacity dispersed among regional players. Tadbik, with USD 200 million revenue, is investing in U.S. flexible-packaging sites, indicating a strategic shift away from commodity cartons toward higher-margin retort pouches.

Infinya’s recycled-fiber integration strengthens its cost position during pulp volatility. Technology is the main differentiator. HP Indigo’s local R&D pipeline delivered a record Shutterfly fleet-upgrade deal worth hundreds of millions of shekels in March 2026, underscoring global demand for Israeli digital-print know-how. Converters adopting automation, such as Tadbik’s 20-kits-per-minute medical tray line, gain labor savings critical in a tight talent market.

Compliance capabilities further separate leaders: firms with in-house migration testing or Tamir partnerships secure preferred-vendor status under stricter Packaging Law enforcement.[4]JD Supra, “Israel: Increased Enforcement of Packaging Law,” jdsupra.com Emerging disruptors like Polyflex/Milpol are reducing platemaking times to 30 minutes and developing smart plates that integrate live QC data into digital presses, expected to be commercially available in 2026. This innovation is expected to significantly enhance operational efficiency in the printing industry.

Israel Folding Carton Industry Leaders

Shefi Packaging Ltd.

Ducart Packaging Industries Ltd.

al-ahlia boxes industry co

Best Carton Ltd.

Yamaton Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: HP Indigo signed its largest agreement with Shutterfly to replace all B2 presses with fifth-generation HP Indigo 120K units, plus three-year consumables and service.

- March 2026: ProAmpac finalised the acquisition of TC Transcontinental Packaging, adding 80+ global sites and 11,000 employees focused on barrier films that compete with cartons in flexible applications.

- February 2026: HP Indigo and ePac concluded a USD 50 million deal covering more than ten HP Indigo 200K presses and multi-year service commitments.

- October 2025: Rengo’s Thai Containers Group agreed to acquire 60% of PT Prokemas Adhikari Kreasi, adding twelve Indonesian corrugated plants to its network.

Israel Folding Carton Market Report Scope

The report provides an in-depth analysis of the folding carton market in Israel, focusing on its current trends, growth drivers, challenges, and opportunities. It examines the market's scope, including the production, consumption, and applications of folding cartons across various industries. The study also evaluates the competitive landscape, supply chain dynamics, and key market players, providing insights into market performance during the forecast period.

The Israel Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Israel folding carton market?

The Israel Folding Carton Market size is projected to be USD 142.56 million in 2025, USD 154.67 million in 2026, and reach USD 206.18 million by 2031, growing at a CAGR of 5.92% from 2026 to 2031.

Which material segment is expanding the fastest?

Coated unbleached kraft is forecast to grow at 7.35% CAGR over 2026-2031 due to rising demand for moisture- and grease-resistant food packaging.

How are digital printing impacting converters?

Digital presses enable SKU-level personalization for kosher and bilingual labels, and the segment is growing at a 6.59% CAGR as converters adopt HP Indigo platforms.

Why are flexible pouches a threat to folding cartons?

Flexible stand-up pouches weigh less, extend shelf life, and comply with recyclability targets, drawing snack and confectionery volumes from cartons.

What role does Israel’s Packaging Law play in market dynamics?

The law mandates 60% recycling for paper and board, and stricter 2024 enforcement favours converters with audited recycled-content supply chains.

Which geography inside Israel is driving e-commerce carton demand?

Negev, Galilee, and the Southern District are expanding fast as last-mile logistics improve and government programs push small businesses online.

Page last updated on: