United Arab Emirates Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

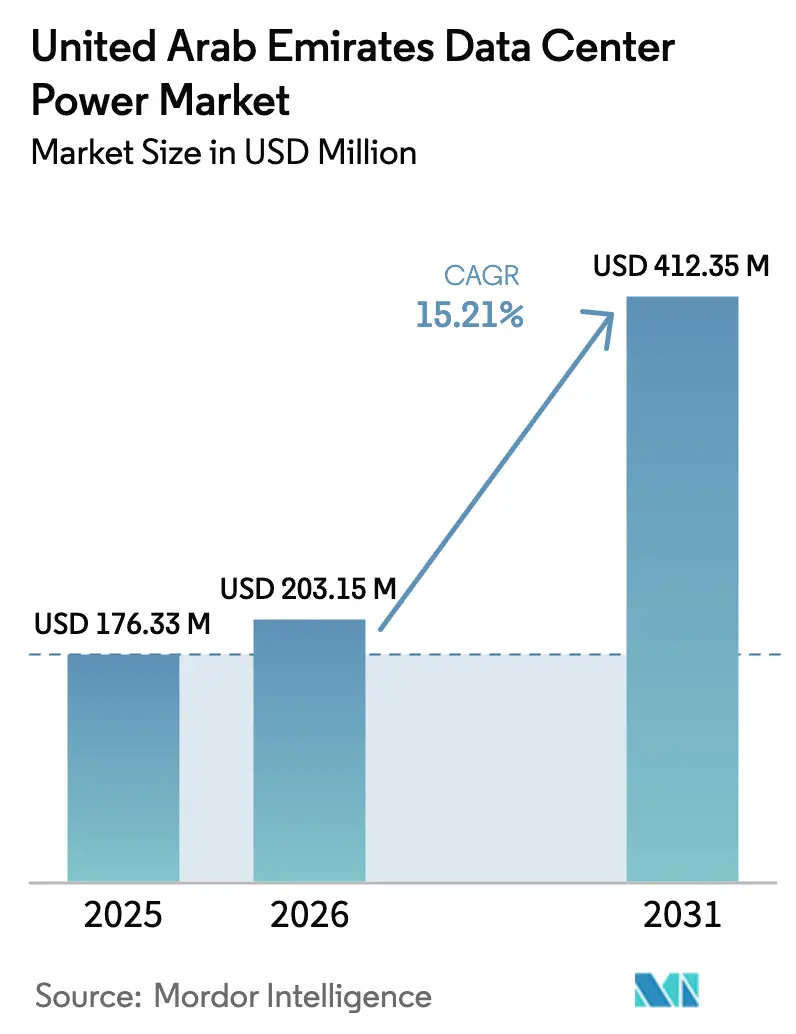

| Base Year Market Size (2025) | USD 176.33 Million |

| Market Size (2026) | USD 203.15 Million |

| Market Size (2031) | USD 412.35 Million |

| Growth Rate (2026 - 2031) | 15.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Data Center Power Market Analysis by Mordor Intelligence

The UAE data center power market size is expected to grow from USD 176.33 million in 2025 to USD 203.15 million in 2026 and is forecast to reach USD 412.35 million by 2031 at 15.21% CAGR over 2026-2031. Sustained government spending on digital-economy infrastructure, the energizing impact of the Barakah nuclear plant’s 25% contribution to national electricity supply, and attractive renewable-energy purchase agreements combine to underpin steady demand for robust, efficient power systems. Hyperscale operators building 100 MW-plus campuses accelerate technology upgrades such as liquid-cooling-ready PDUs and 132-kV substation connections, while smart-city programs boost adoption of distributed microgrids and battery storage. Rising electricity tariffs, short technician supply, and peak-demand levies drive immediate cost-containment measures, reinforcing the business case for high-efficiency UPS platforms and predictive energy-management software. Competition remains moderate as global power majors vie with regional specialists and fast-moving startups that focus on AI-optimized power integration.

Key Report Takeaways

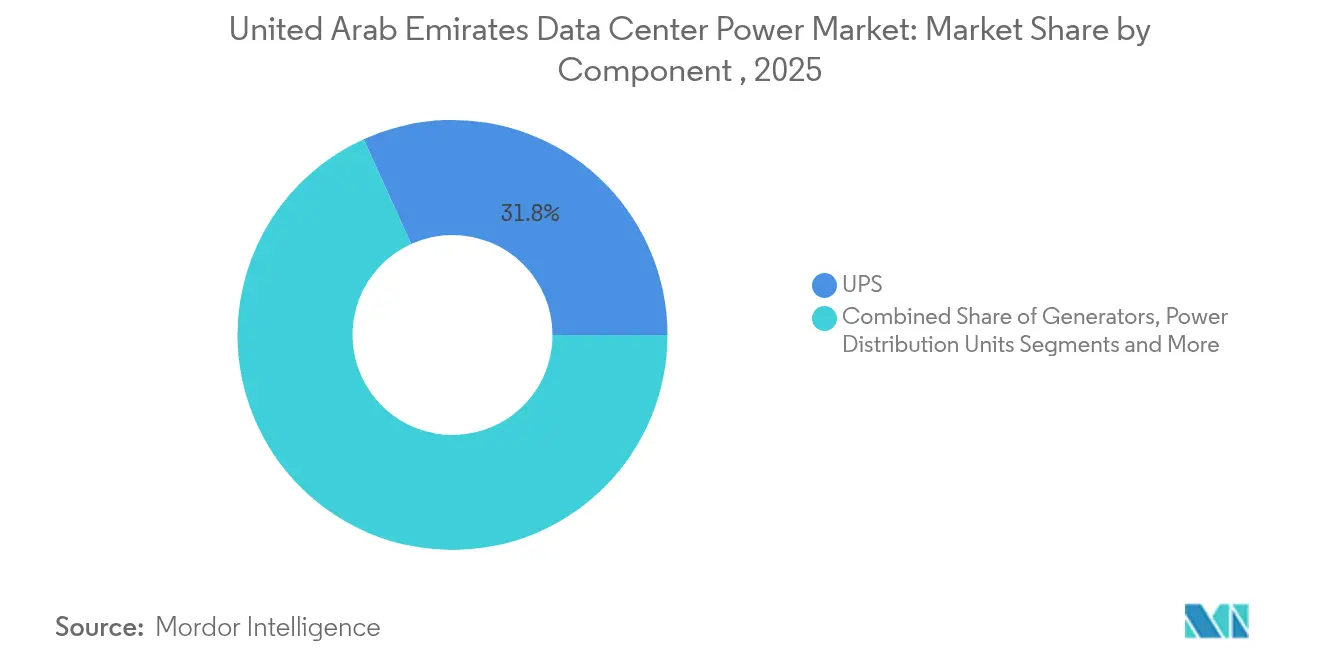

- By component, UPS systems led with 31.78% revenue share in 2025; power distribution units are expanding at a 16.07% CAGR through 2031.

- By data-center type, colocation providers held 44.72% of the UAE data center power market share in 2025, while hyperscale/cloud service providers are projected to grow at 16.86% CAGR.

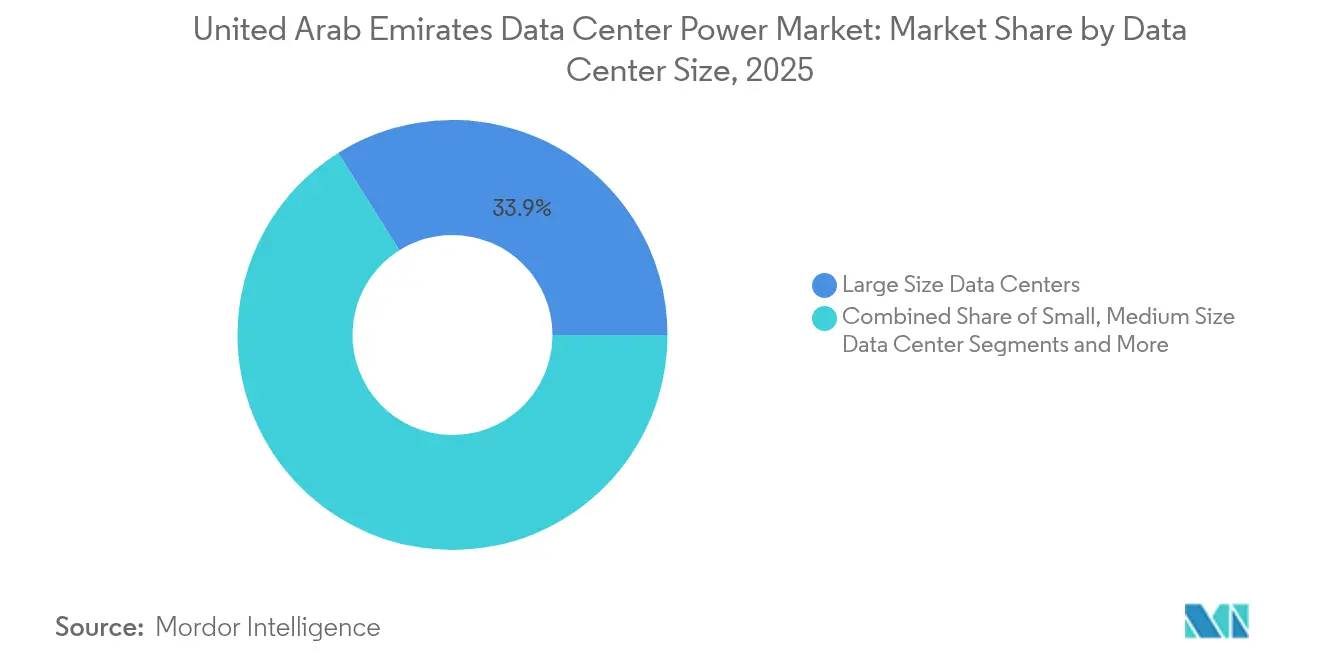

- By size, large data centers accounted for 33.92% of the UAE data center power market size in 2025; mega data centers are forecast to advance at a 15.48% CAGR between 2026-2031.

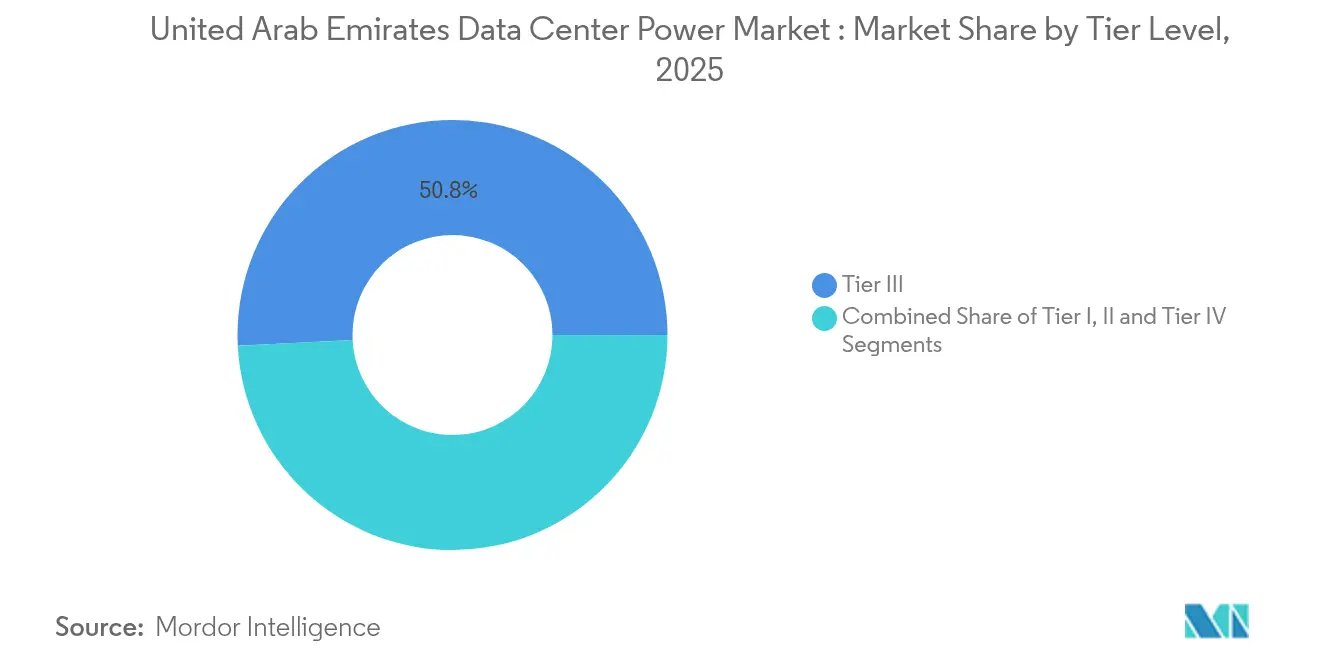

- By tier level, Tier III facilities commanded 50.80% share in 2025, yet Tier IV deployments exhibit the highest projected CAGR at 15.89% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of mega data centers & cloud computing | +3.2% | UAE-wide, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Increasing demand to reduce operational costs | +2.8% | National, with early gains in Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Government smart-city & digital-transformation push | +2.1% | UAE-wide, led by Dubai 2040 and Abu Dhabi Vision 2071 | Long term (≥ 4 years) |

| On-site renewable microgrids & waste-to-energy uptake | +1.9% | Abu Dhabi and Dubai focus, expanding to Northern Emirates | Medium term (2-4 years) |

| AI hyperscale campuses driving 132-kV substation build-outs | +2.4% | Dubai Silicon Oasis, Abu Dhabi’s Masdar City, ADGM | Short term (≤ 2 years) |

| Sustainability regulations driving renewable power integration | +1.8% | National, stricter enforcement in Abu Dhabi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Mega Data Centers & Cloud Computing

Khazna’s 100 MW AI-ready campus in Ajman illustrates how facilities over 100 MW reshape power-infrastructure blueprints, requiring multiple redundant 132-kV feeds and ultra-efficient UPS designs. Gulf Data Hub’s plan to scale to 240 MW prompted the deployment of 99%-efficient UPS lines that sharpen PUE targets.[1]Vertiv Group, “Liebert EXL S1 UPS Powers Gulf Data Hub Expansion,” vertiv.comLiquid-to-liquid cooling that supports 150 kW per rack mandates high-amperage PDUs capable of continuous thermal and power monitoring. Cloud-service operators increasingly bundle renewable PPAs, as seen in AWS’s USD 1 billion deal with e&, compelling vendors to integrate energy-storage modules and grid-tie software. Collectively, these factors deepen demand for turnkey power ecosystems that can be expanded in modular blocks without operational disruption.

Operators face DEWA’s tiered tariffs reaching 38 fils/kWh plus 6 fils/kWh fuel surcharge, compelling a pivot toward efficiency-first power architectures. Schneider Electric’s EcoStruxure deployments demonstrate 15-20% energy savings through predictive analytics that rebalance live loads. [2]Schneider Electric, “EcoStruxure for Data Centers: Energy Efficiency Case Studies,” se.comIntelligent PDUs reveal phantom loads equaling up to 8% of facility consumption, unlocking rapid payback opportunities. Lithium-ion battery systems paired with EMS platforms facilitate peak-shaving strategies able to dodge EWEC’s demand charges. Incremental, modular UPS blocks enable operators to match new capacity to actual demand, trimming stranded-asset risk and capital overhead.

Government Smart-City & Digital-Transformation Push

Dubai’s Smart City 2025 and Abu Dhabi Vision 2071 programs compel public agencies and private partners to consolidate IT workloads in certified facilities that meet strict uptime and cybersecurity benchmarks. ADNOC’s policy favoring in-country value creation drives supplier localization and nurtures local service ecosystems supporting power-infrastructure rollouts. Centralized government data hubs spanning 40 agencies in Abu Dhabi generate scale demand for enterprise-grade power chains equipped with duplicated generators, STS, and battery banks. Mandatory adherence to Tier IV for fintech and public-safety platforms increases preference for dual-feeder configurations with continuous fuel supplies. Federal energy-management rules released in 2024 widen interest in EMS dashboards that verify compliance metrics in real time.

Sustainability Regulations Driving Renewable Power Integration

The Third Nationally Determined Contribution obliges all large energy consumers to track and trim greenhouse-gas intensity by 47% by 2035. [3]Ministry of Climate Change & Environment, “Third Nationally Determined Contribution,” moccae.gov.aeEWEC’s upcoming 400 MW/400 MWh BESS will stabilize intermittency, ensuring data centers can commit to high solar fractions without risking outages a. Operators adopt hybrid natural-gas plus hydrogen gensets, echoing Caterpillar’s field trials with Microsoft that meet near-zero methane targets. The Mohammed bin Rashid Al Maktoum Solar Park’s 5 GW roadmap gives long-term visibility for renewable PPAs at competitive rates. Newly issued green-building codes enforce minimum UPS efficiency levels and continuous energy-metering provisions for facilities commissioned after 2024.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation & maintenance costs | -1.8% | UAE-wide, particularly affecting smaller operators | Short term (≤ 2 years) |

| Grid transmission losses & substation land scarcity | -1.4% | Dubai and Abu Dhabi prime locations | Medium term (2-4 years) |

| Upcoming EWEC peak-demand levies on data centers | -1.1% | Abu Dhabi emirate, potential expansion to other emirates | Short term (≤ 2 years) |

| Shortage of HV-UPS & battery-service technicians | -0.9% | National, acute shortages in Northern Emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Installation & Maintenance Costs

Complete UPS trains for 10 MW halls run USD 2-4 million, depending on redundancy tiers and efficiency specs, straining budgets of new entrants. Delta’s 99%-efficient DPH Series UPS exemplifies a premium kit that lifts capex yet remains essential for hyperscale PUE targets. Annual service contracts consume up to 12% of the outlay, while lithium-ion battery replacements shorten under 40 °C ambient conditions. Import duties on specialist switchgear inflate landed prices by as much as 25% for buyers without volume leverage. Vendor-financed leasing and modular build approaches mitigate exposure but cannot erase the fundamental capital barrier confronting smaller operators.

Grid Transmission Losses & Substation Land Scarcity

Average 7-9% transmission losses worsen to double-digit figures in projects more than 50 km from main substations, eroding operating margins for UAE data center power market participants. Land in Dubai Silicon Oasis exceeds USD 500/m², deterring single-tenant substations for facilities below 50 MW. EWEC’s 1.5 GW turbine build in Madinat Zayed will cover reserve generation but still needs new lines to northern emirates . Grid congestion during evening peaks elevates connection-fee quotes and may delay energization schedules. On-site generation offers relief yet demands additional permitting and fuel-logistics arrangements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Dominance Faces PDU Innovation

UPS systems generated 31.78% of 2025 revenue, reflecting their non-negotiable role in safeguarding IT loads. The UAE data center power market size for UPS-driven architectures equaled USD 56.03 million in 2025, underscoring sustained enterprise reliance on double-conversion units. Growth continues as lithium-ion chemistries displace VRLA banks, shrinking footprint and improving round-trip efficiency. Parallel UPS frames permit hot-scaling in 500 kW blocks, aligning capex with incremental capacity.

Power distribution units post the fastest 16.07% CAGR as AI racks approach 60-150 kW. High-amperage intelligent PDUs deliver branch-circuit-level telemetry, enabling automated load-shedding that trims operating cost. Generators and transfer switches maintain steady demand, though hydrogen and biofuel variants draw heightened interest for net-zero roadmaps. Remote power panels gain traction at the edge, where micro-modular deployments demand compact distribution. Energy-storage systems emerge as a high-growth adjunct, supporting peak-shaving and bridging functions during extended outages.

By Data Center Type: Hyperscale Velocity Challenges Colocation Leadership

Colocation providers accounted for 44.72% of UAE data center power market revenue in 2025, buoyed by enterprises outsourcing to avoid capex. They optimize shared UPS strings across mixed-tenant halls, often reaching 99% internal UPS efficiency. However, hyperscale/cloud operators clock the highest 16.86% CAGR, powered by AI training expansion requiring integrated substation builds and direct renewable PPAs.

Enterprises maintain private on-premise sites for data-sovereignty workloads yet increasingly adopt software-defined power layers to mirror hyperscale efficiency. Edge facilities under 500 kW proliferate along 5G corridors, prioritizing ruggedized UPS modules and lithium-iron-phosphate batteries for remote reliability. This blend of site types fosters vendor differentiation between modular, quick-deploy kits and mega-scale turnkey infrastructures.

By Size: Mega Facilities Drive Infrastructure Evolution

Large data centers held 33.92% revenue share in 2025, balancing capex and manageability for most regional operators. UAE data center power market share for mega facilities, while smaller today, will surge as 100 MW campuses accelerate at 15.48% CAGR through 2031. Mega-site economics prize high-voltage inputs, looped MV distribution, and synchronized gensets rated for extended fuel autonomy.

Massive and small-to-medium sites form complementary niches—massive sites as expansion phases for successful campuses, and smaller footprints for latency-critical or regulatory workloads. Modular electrical rooms in ISO containers enable small sites to deploy in 24 weeks, giving telcos and fintechs an agile expansion path. Conversely, mega campuses anchor utility grid upgrades, often negotiating special tariff structures in exchange for demand guarantees.

By Tier Level: Tier IV Growth Reflects Mission-Critical Demands

Tier III dominated with 50.80% share during 2025, delivering 99.982% uptime at an attainable capex. The UAE data center power market size allocated to Tier IV, though smaller, is projected to outpace others thanks to a 15.89% CAGR driven by financial trading, healthcare diagnostics, and AI training clusters. Dual-cord power to every rack, concurrent maintainability, and fault-tolerant distribution impose 40-60% capex premiums yet meet 99.995% uptime mandates.

Tier I and II retain relevance for non-critical dev-test or archival workloads that can tolerate brief interruptions. The gradual tightening of compliance frameworks in fintech, crypto custody, and smart-health sectors nudges operators toward higher-tier designs with full generator redundancy and triple-conversion UPS topologies. Tier-upgrades often entail live-site retrofits, reinforcing demand for modularized power walls and hot-swap static transfer switches.

Geography Analysis

Dubai offers streamlined permitting at Dubai Silicon Oasis, where operators secure 132-kV dual feeds within six months. Abu Dhabi’s Barakah nuclear plant and Masdar’s solar parks anchor firm baseload and green PPAs that appeal to hyperscale clouds pursuing corporate net-zero mandates.

Northern Emirates—Sharjah, Ajman, Ras Al Khaimah, and Umm Al Quwain emerge as cost-effective alternatives, advertising land discounts of 15-25% and favorable grid-connection fees. Sharjah’s wholesale-and-retail trade contributions create edge-computing demand supporting distributed UPS clusters. Fujairah, sitting on the Arabian Sea outside the Strait of Hormuz, is winning subsea-cable landings and recently welcomed e&’s fourth data center, strengthening east-west latency pathways.

Inter-emirate harmonization gained traction when the federal energy-efficiency code standardized power-quality metrics country-wide in 2024. The UAE data center power market now benefits from unified grid-protection schemes and expedited customs clearance for imported switchgear. High-voltage corridor investments linking Barakah and Al Dhafra PV fields to Dubai reduce congestion risk for planned AI campuses. Yet site selection still hinges on local land-use rules: Dubai Silicon Oasis restricts diesel runtime hours, while Masdar City offers green-energy subsidies conditional on certified PUE benchmarks.

Competitive Landscape

The UAE data center power market supports a moderately fragmented vendor mix. Their global R&D budgets and multi-year service contracts strengthen stickiness with large operators. Schneider Electric’s 2024 acquisition of Motivair adds liquid-cooling capability that dovetails with AI power requirements; ABB fields EcoFlex MV switchgear optimized for 132-kV builds, and Vertiv partners with NVIDIA on GB200 NVL72-ready power layouts.

Regional specialists such as Hyper Intelligent Data Center Technology (HiDCT) and Saudi-based Al Fanar target rapid-deployment packages and 24-hour field response, winning small-to-medium projects seeking high localization. Energy-storage integrators like Ampt and Tesvolt court the same clients with turnkey battery containers suitable for peak-shave applications. Startups emphasize AI-driven energy-optimization SaaS that overlays existing SCADA frameworks, extracting further efficiency gains without hardware swaps.

United Arab Emirates Data Center Power Industry Leaders

ABB Ltd

Schneider Electric SE

Vertiv Group Corp.

Eaton Corporation plc

Caterpillar Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Khazna welcomed MGX and Silver Lake as minority shareholders alongside G42, funding global AI expansion strategies.

- February 2025: Eni inked deals with Masdar and Taqa to power Italian data centers up to 1 GW IT load via 3 GW renewable offtake.

- February 2025: A UAE telecom group sold a USD 2.2 billion stake in Khazna Data Centre, signaling investor confidence and ongoing consolidation.

- January 2025: ADNOC Distribution and Emerge launched phase-two solar rollouts across service stations, generating 30,000 MWh per year and cutting CO₂ by 13,000 tons.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Arab Emirates data center power market as the revenue generated in the country from new and replacement electrical infrastructure that provides, conditions, distributes, and monitors power inside colocation, enterprise, hyperscale, and edge data centers. Included equipment spans uninterruptible power supply (UPS) systems, generators, switchgear, transfer switches, power distribution units, remote power panels, busways, and the associated monitoring software and services. We, therefore, model spend linked directly to the racks that host processing and storage workloads, not the broader building envelope.

Scope exclusion: Cooling systems, IT hardware, real-estate construction, and facility management services lie outside our market boundary.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview equipment vendors, engineering contractors, and colocation operators across Dubai, Abu Dhabi, Sharjah, and Fujairah. These discussions validate typical megawatt sizing, procurement lead times, service margins, and renewable integration plans that cannot be captured through desk work alone, helping us close data gaps and cross-check assumptions.

Desk Research

We begin by mapping the local install base using publicly available sources such as the UAE Telecommunications and Digital Government Authority statistics, Dubai Electricity and Water Authority tariff filings, Emirates Customs import codes for HS 8504 and 8502, and disclosures from regional trade associations like the Middle East Data Center Alliance. Company 10-Ks, sustainability reports, and investor decks supply shipment, pricing, and project pipeline clues, which are then complemented by D&B Hoovers financial snapshots and Factiva news archives available in Mordor's paid tool kit. Government energy outlook papers and peer-reviewed journals on Gulf grid stability complete the secondary foundation. The sources cited above are illustrative; many additional documents inform our desk analysis.

Market-Sizing & Forecasting

We employ a top-down demand pool build anchored on national data center IT load (MW) and expected power density per rack, which is cross-verified with selective bottom-up checks such as sampled UPS shipments and channel ASP × volume estimates. Key variables include edge traffic growth, hyperscale campus announcements, Tier III versus Tier IV mix shift, average diesel price for backup sets, renewable penetration targets, and utility tariff trajectories. Multivariate regression links these drivers to historical spend, while a scenario analysis layer tests upside and downside cases. Where bottom-up evidence underrepresents emerging segments, interpolation is applied yet capped by primary feedback to prevent overstatement.

Data Validation & Update Cycle

Outputs pass through anomaly screens and senior reviewer sign-off. Discrepancies beyond a five percent tolerance trigger re-engagement with respondents. Reports refresh each year, and extraordinary events, policy shifts, mega-facility awards, or force majeure outages prompt interim model updates so clients always receive the latest view.

Why Our United Arab Emirates Data Center Power Baseline Commands Reliability

Published estimates often diverge because each publisher chooses its own equipment slate, pricing curve, and refresh cadence. Our disciplined scope, consistent currency conversion, and annual recalibration provide a stable reference.

Key gap drivers versus other studies include: some track only UPS and generators while we capture PDUs and switchgear; a few inflate totals by applying global average selling prices instead of UAE-specific contract prices; others forecast aggressively by assuming immediate realization of all announced capacity, whereas Mordor phases builds based on construction milestones and grid tie-in timelines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 176.3 million (2025) | Mordor Intelligence | - |

| USD 141.9 million (2024) | Regional Consultancy A | Uses broader Middle East price benchmarks and excludes PDUs |

| USD 162.4 million (2024) | Analyst House B | Counts renewable micro-grid capex and assumes full Tier IV penetration |

Taken together, the comparison shows that Mordor's measured equipment scope, UAE-specific pricing, and phased build-out logic yield a balanced, transparent baseline that decision-makers can trace back to clear variables and repeat the next cycle.

Key Questions Answered in the Report

What is the current value of the UAE data center power market?

It reached USD 203.15 million in 2026 and is forecast to grow to USD 412.35 million by 2031.

Which component segment leads spending?

UPS systems led with 31.78% revenue share in 2025, due to their vital role in uptime assurance.

How fast are hyperscale data centers growing?

Hyperscale/cloud service providers are expanding at a 16.86% CAGR through 2031, the fastest among data-center types.

Why are peak-demand levies a concern?

EWEC’s proposed charges could raise electricity costs by up to 30% during peak periods, pressuring operators to install energy-storage or peak-shaving solutions.

Page last updated on: