Middle East Data Center Power Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

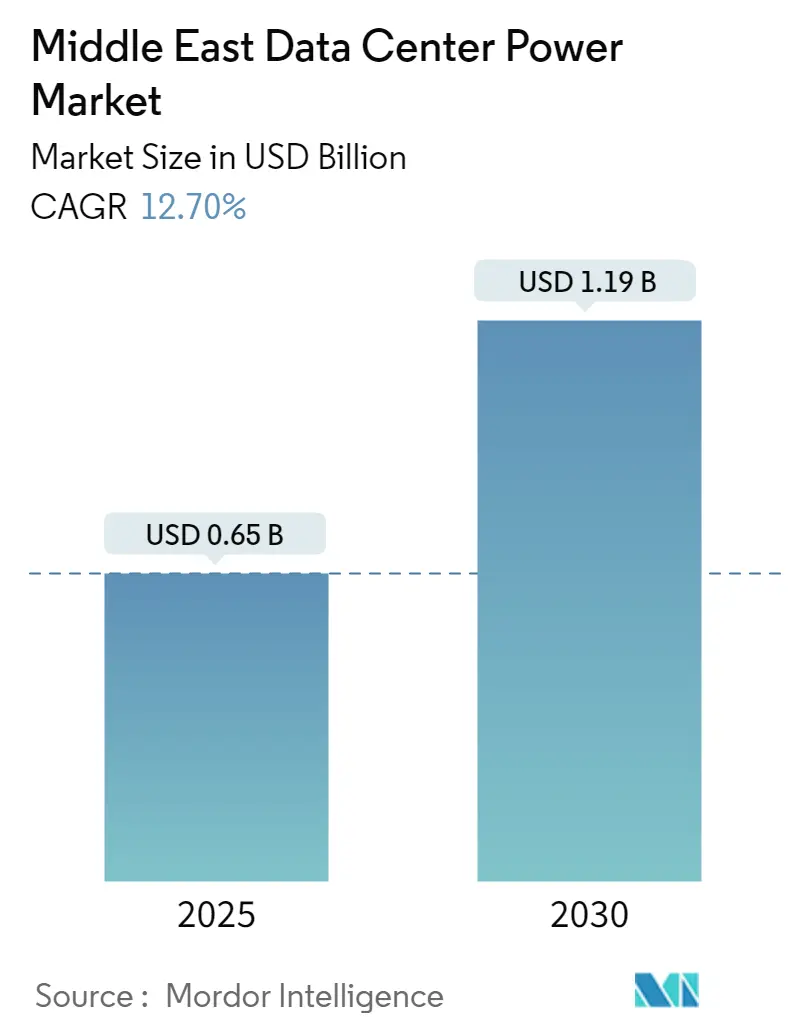

| Market Size (2025) | USD 0.65 Billion |

| Market Size (2030) | USD 1.19 Billion |

| Growth Rate (2025 - 2030) | 12.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Data Center Power Market Analysis by Mordor Intelligence

The Middle East data center power market is valued at USD 0.65 billion in 2025 and is projected to reach USD 1.19 billion by 2030, advancing at a 12.7% CAGR. Rapid hyperscale investments, sovereign AI programs and national digital-economy agendas are amplifying demand for resilient power infrastructure. Forward-looking operators are pairing renewable generation with battery storage to comply with clean-energy mandates, while liquid-cooling adoption is pushing rack densities from 10 kW toward 150 kW, reshaping UPS and PDU specifications. Vendor-financed, pay-as-you-go power blocks are also compressing project timelines, allowing cloud leaders to synchronize facility builds with ramping AI workloads. These shifts ensure that the Middle East data center power market remains central to Gulf governments’ diversification strategies as they pivot from hydrocarbons toward digital services.

Key Report Takeaways

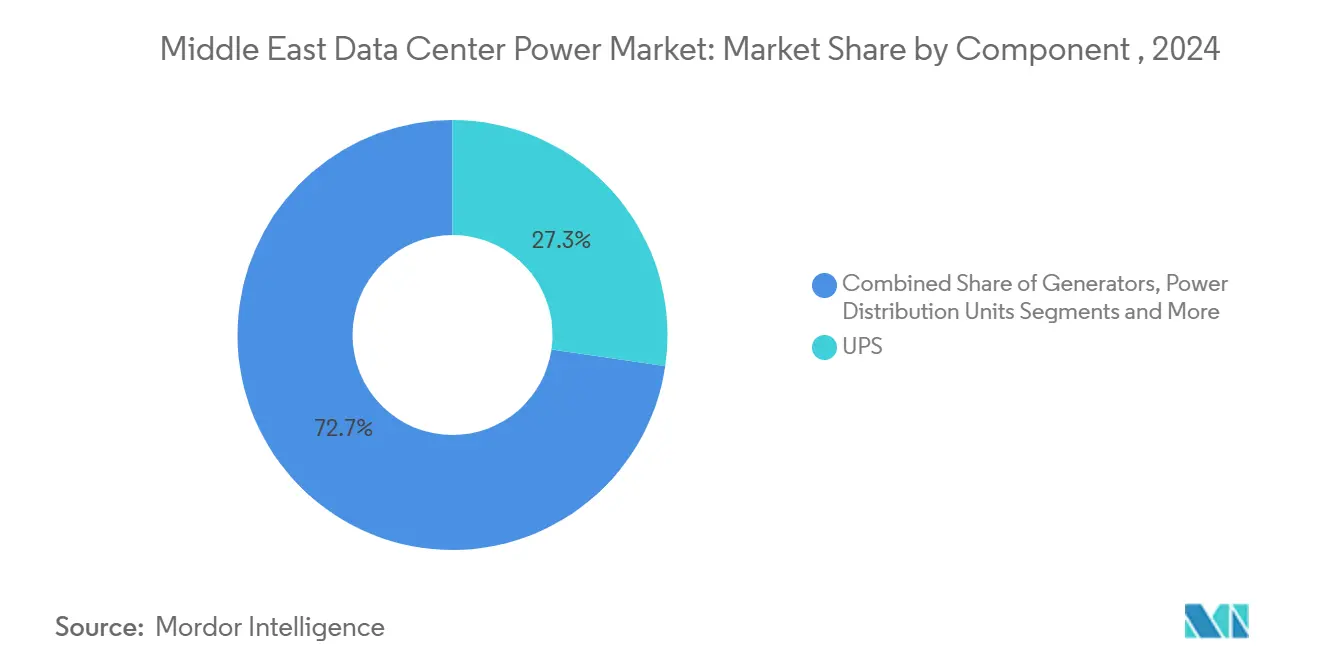

- By component, UPS systems led with 27.3% revenue share in 2024; Power Distribution Units are forecast to expand at a 13.3% CAGR to 2030.

- By data-center type, colocation held 46.6% of the Middle East data center power market share in 2024, while hyperscale operators are advancing at a 14.8% CAGR through 2030.

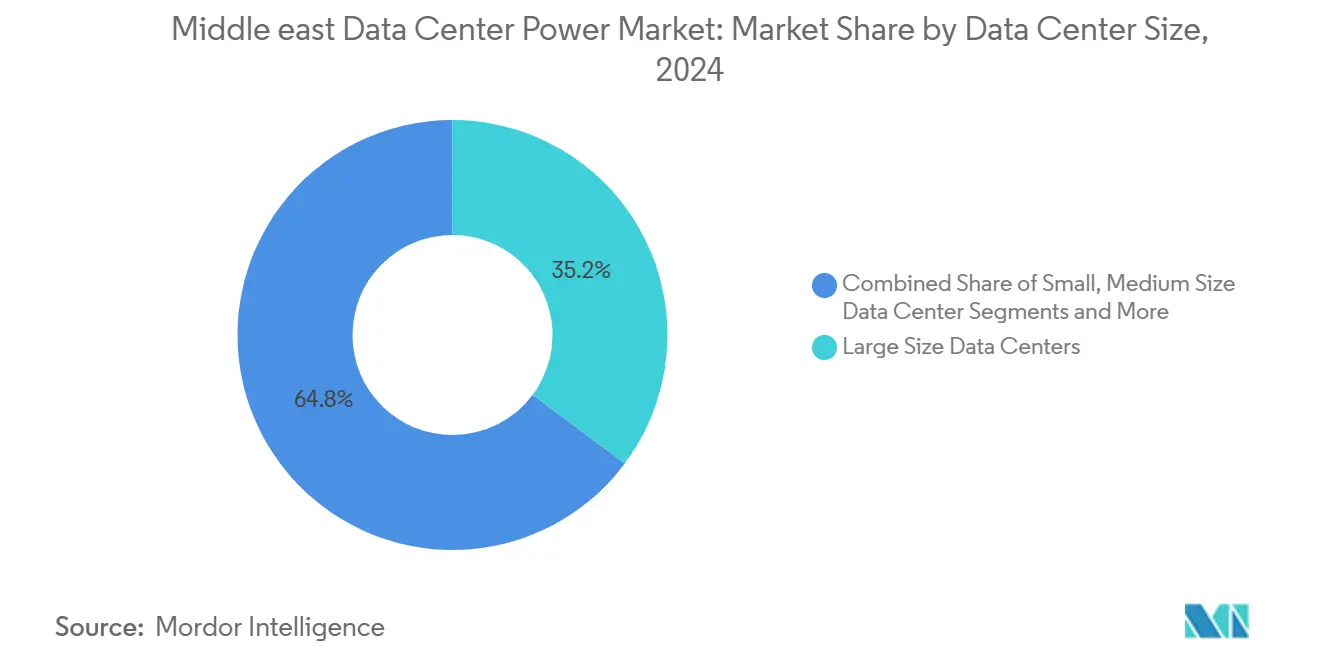

- By facility size, large data centers accounted for a 35.2% share of the Middle East data center power market size in 2024, and mega sites are projected to grow at a 13.9% CAGR to 2030.

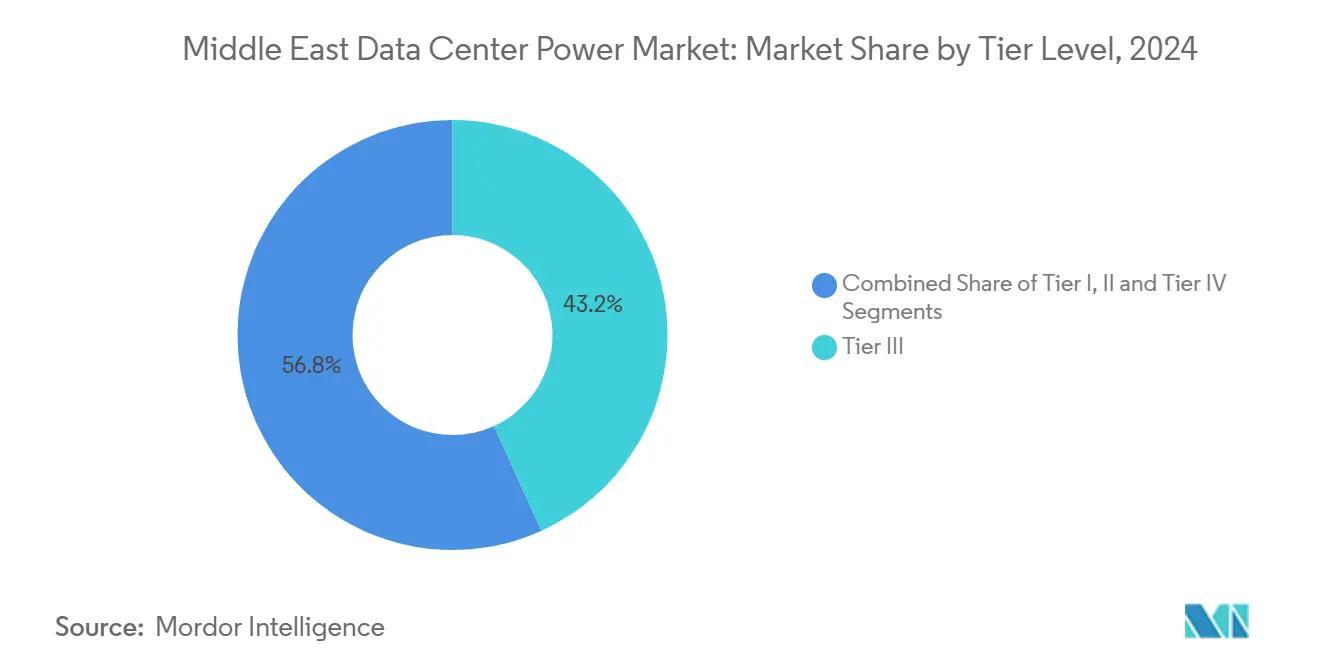

- By tier level, Tier III configurations dominated with 43.2% market share in 2024; Tier IV is expanding at a 15.1% CAGR through 2030.

- By country, Saudi Arabia commanded a 31.7% share in 2024, whereas the UAE shows the fastest growth at 14.3% CAGR to 2030.

Middle East Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud and AI-led hyperscale pipeline explosion | +3.2% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Government-backed digital-economy visions | +2.8% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Colocation shift toward renewable-ready power | +2.1% | Global; UAE & Saudi Arabia leadership | Medium term (2-4 years) |

| Tariff incentives for on-site solar + battery | +1.9% | Saudi Arabia, UAE, Oman | Short term (≤ 2 years) |

| Liquid-cooling adoption | +1.7% | Global; accelerated in harsh-climate regions | Short term (≤ 2 years) |

| Vendor financing models | +1.3% | GCC countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud and AI-led Hyperscale Pipeline Explosion

Rising AI workloads are forcing a leap in rack-level power density, triggering a wholesale redesign of electrical back-bones. NEOM’s USD 5 billion 1.5 GW AI campus showcases 400 V DC distribution and Silicon-Carbide e-switching that deliver 98% conversion efficiency. Microsoft and du have committed USD 544.5 million to a hyperscale build in the UAE that will run high-density training clusters while keeping latency below 20 ms to Europe. These builds anchor submarine-cable landings and attract ancillary colocation spend, driving a regional cascade of power-equipment orders. Suppliers able to pre-fabricate 50 MW blocks now win contracts on speed, tilting the competitive field toward modular UPS and generator pods.

Government-backed Digital-Economy Visions

Saudi Vision 2030 targets 130 GW of renewables by 2030, designating data centers as anchor offtakers that can soak up midday solar peaks.[1]Ministry of Energy, Saudi Arabia, “National Renewable Energy Program targets 130 GW by 2030,” energy.gov.saDubai’s D33 roadmap layers a USD 1.9 billion AI-infused smart grid that trims line losses to 2%, creating a near-perfect environment for grid-interactive UPS fleets. These policies weave clean-power targets with data-sovereignty rules, compelling operators to co-locate solar farms, BESS arrays and Tier IV halls. Local-content clauses meanwhile, incubate regional switchgear assemblers and battery-rack OEMs, widening the supplier base and compressing import lead times

Colocation Shift Toward Renewable-Ready “Green” Power Architectures

Enterprise ESG mandates push colocation landlords to guarantee 24/7 renewable electricity. Equinix’s DX3 Dubai site already sources 100% clean power, using BESS to arbitrage tariff peaks and feed grid-stability markets.[2]Mercom Capital Group, “Scaling Energy Storage in the MENA Region Amidst Renewables Boom,” mercomindia.com Grid-interactive UPS units pioneered in Europe are now qualifying for Gulf frequency-containment contracts, unlocking new revenue streams and shortening payback to under six years. Region-specific hardware, such as GSL Energy’s liquid-cooled 125 kW/418 kWh pack, withstands 50 °C ambient without derating, making green power viable even in desert edge nodes.

Liquid-Cooling Adoption Boosting Rack-level Power Density

Immersion and cold-plate systems cut cooling energy by up to 40% and bring PUE below 1.1. Schneider Electric’s 75% stake in Motivear signals a supply-chain pivot toward sealed coolant loops optimized for 30 kW-plus racks. In Riyadh, indirect-evaporative designs achieve 82% free-cooling hours annually, proving that advanced thermal schemes can thrive despite harsh climates. Liquid cooling also eliminates water use, vital in water-scarce Gulf states, and opens previously unsuitable inland sites for big-footprint campuses.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-connection bottlenecks and curtailment risk | -2.3% | Regional, particularly UAE and Saudi Arabia | Medium term (2-4 years) |

| High TCO of Tier III/IV redundancy in harsh climates | -1.8% | Desert regions, extreme climate zones | Long term (≥ 4 years) |

| Skilled-labor deficit for critical-power OandM | -1.5% | Regional, with acute shortages in Saudi Arabia and UAE | Long term (≥ 4 years) |

| Natural-gas price volatility impacting genset economics | -1.2% | Global, with regional exposure through backup power systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Bottlenecks and Curtailment Risk

Utility queues add 18-24 months to project timelines as system operators demand costly impact studies and synchronous-condensing hardware. Voltage-dip events recorded by Gulf grids mirror incidents cited by NERC’s Large-Load Task Force, underscoring the stakes for regional reliability. Although the GCC interconnection eases cross-border trades, it lacks the capacity for multi-GW hyperscale pulls without fast-track substation builds. Developers often resort to temporary gas turbines to cover commissioning windows, inflating capex, and complicating emissions targets.

High TCO of Tier III/IV Redundancy in Harsh Climates

Ambient temperatures above 40 °C derate diesel generators by 10-15%, forcing oversizing and raising fuel burn. [3]Cummins, “Generator rating guidelines for high-temperature environments,” cummins.comCooling can absorb 40% of site energy in traditional air-cooled halls, and sand ingress accelerates filter replacement cycles, adding OPEX. Operators respond with sealed liquid-cool loops, vertical heat-exchangers and AI-driven fault prediction, yet the cost delta over a temperate-climate build still hovers around 18%. Advanced hydrogen-ready turbines promise relief but remain capex-heavy until regional fuel logistics mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Lead Amid PDU Innovation

UPS platforms generated 27.3% of 2024 revenue thanks to escalating reliability targets and modular topologies that parallel AI capacity rollouts. Lithium-ion and nickel-zinc chemistries shrink footprint by 40% and slash maintenance visits, advantages that resonate with labor-scarce Gulf operators. Generators follow as the second-largest slice, yet hydrogen-capable turbines and gas-engine hybrids are gradually nudging diesel toward niche standby roles. Intelligent PDUs represent the fastest-growing niche at a 13.3% CAGR, propelled by outlet-level metering that helps cloud tenants right-size breaker ratings and avoid stranded capacity.

Edge sites and containerised nodes favour integrated Remote Power Panels and static-switch boards that can be swapped in minutes, an approach echoed by Vertiv’s prefabricated enclosures. Energy-storage systems, meanwhile, mark the newest frontier, unlocked by tariff structures rewarding peak-shaving. The convergence of telemetry-rich hardware and DC bus architectures is expected to lift the Middle East data center power market size for advanced PDUs to USD 0.23 billion by 2030, underscoring a shift from pure backup toward active grid support.

By Data Center Type: Hyperscale Growth Challenges Colocation Dominance

Colocation retained 46.6% of 2024 spending as enterprises outsourced capital-intensive power rooms, yet hyperscalers are expanding at 14.8% CAGR, narrowing the gap each quarter. AI-training farms require contiguous 100 MW blocks, prompting cloud majors to secure multi-site power purchase agreements that lock in 24/7 renewable coverage. Edge and enterprise camps form a tertiary layer, demanding micro-UPS and fan-less switchgear that can ride through logistics delays.

The hyperscale surge boosts the Middle East data center power market as sovereign-cloud frameworks compel global providers to build in-country. Colocation incumbents counter by layering liquid-cool pods and 400 V DC aisles into existing halls, extending asset life and upselling high-density footprints. Partnerships such as KKR with Gulf Data Hub promise USD 5 billion in build-out, combining global capital with local permits to accelerate project velocity.

By Data Center Size: Mega Facilities Drive Power Density Evolution

Large campuses captured 35.2% of 2024 revenue, balancing granular leasing with scale economies. However, mega facilities registering 13.9% CAGR are redrawing supply chains by pre-ordering 150 MW GIS substations and 2 km cable corridors years in advance. These complexes often embed 20 MWh BESS farms that monetize frequency-response markets within months of energization.

Smaller edge nodes still matter: 5 MW prefabricated blocks co-located with 5G towers provide content caching and sensor aggregation in oilfields. Modular switchgear and air-independent cooling make them deployable in 12 weeks. Nonetheless, mega-site momentum means the Middle East data center power market share of campus-scale builds could cross 40% by 2030 as AI demand concentrates compute footprints.

By Tier Level: Tier IV Expansion Reflects Mission-Critical Demands

Tier III holds a 43.2% share in 2024, yet Tier IV is clocking a 15.1% CAGR as fintechs, exchanges, and sovereign-AI labs demand 99.995% availability. N+1 redundancy now extends to lithium-ion strings and coolant pumps, creating intricate supervision needs.

Environmental severity pushes some operators to adopt Tier IV solely for cooling fault tolerance, even when power circuits run N+N. This raises capex but lessens revenue risk from thermal excursions, especially during peak summer. The Middle East data center power industry now sees consultants modeling Tier IV uptake alongside hydrogen backup as a route to both uptime and decarbonization.

Geography Analysis

Saudi Arabia secured 31.7% of 2024 revenue on the back of low electricity tariffs and 62 live data centers. The kingdom’s USD 5 billion NEOM-DataVolt deal cements its giga-scale ambition. Conversely, the UAE records a 14.3% CAGR, benefiting from Dubai’s carrier-dense ecosystems and Abu Dhabi’s 5 GW AI campus plan.

Israel leverages deep-tech talent to market sovereign-cloud zones, while Qatar’s post-World-Cup digitization and Kuwait’s 2035 plan ignite greenfield builds. Oman and Bahrain position themselves as disaster-recovery hubs, citing seismic stability and subsea cable redundancy. These trajectories ensure a geographically diverse funnel that keeps the Middle East data center power market resilient to single-country policy swings.

Competitive Landscape

Global OEMs such as ABB, Schneider Electric, and Vertiv expand Gulf factories to sidestep logistics constraints and meet localization quotas. Their portfolios now bundle Silicon-Carbide UPS, lithium and nickel-zinc battery strings, switchgear, monitoring and five-year O&M wraps, enabling single-purchase contracts that de-risk project schedules. Schneider’s Motivear buy gives it a head-start in sealed liquid-coolant loops, while ABB layers FACTS devices to mitigate harmonic injection at high-density AI halls ABB. These moves tighten integration and raise switching costs for customers.

Regional challengers emerge. GSL Energy deploys ruggedized BESS tailored for 50 °C environments, winning utility-interactive pilots in Oman. Gulf Data Hub leverages KKR capital to build carrier-neutral parks, standardizing 2.5 MW power blocks that snap together as demand scales. Meanwhile, GE Vernova offers H2-blendable turbines as diesel exit ramps, and ZincFive positions nickel-zinc as a safer alternative to lithium in fire-code-sensitive metros.

Middle East Data Center Power Industry Leaders

ABB

Schneider Electric

Vertiv

Eaton

Caterpillar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Eaton and Siemens Energy formed a partnership to deliver modular 500 MW onsite power plants for data centers, targeting a two-year reduction in time-to-market.

- May 2025: Khazna Data Centers announced two AI-ready Abu Dhabi facilities totaling 60 MW that feature high-density liquid cooling.

- April 2025: du and Microsoft confirmed a USD 544.5 million hyperscale build in Dubai, with phased delivery supporting Gulf AI services.

- March 2025: ADQ and ECP launched a USD 5 billion venture to develop 25 GW of renewable projects dedicated to regional data centers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Middle East data center power market as the total yearly revenue earned from uninterruptible power supplies, diesel or gas generators, power distribution units, switchgear, transfer switches, remote power panels, and on-site energy-storage systems that feed purpose-built cloud, colocation, enterprise, and edge facilities across Saudi Arabia, the United Arab Emirates, Israel, Qatar, Kuwait, and neighboring states. These values are captured at ex-factory pricing that neutralizes import duties and channel mark-ups.

Scope Exclusions. We exclude cooling equipment, IT hardware, building and fit-out services, and grid-scale renewables that are not contractually tied to data-center loads.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

- By Country

- United Arab Emirates

- Saudi Arabia

- Israel

- Qatar

- Kuwait

- Rest of Middle East

Detailed Research Methodology and Data Validation

Primary Research

Analysts interviewed construction contractors, facility operators, utility planners, and equipment distributors across the Gulf and Levant. These conversations clarified on-ground commissioning dates, typical price cushions on Tier III versus Tier IV builds, and expected swing factors such as hydrogen backup pilots, letting us refine utilization curves and stress-test our assumptions.

Desk Research

We began by mapping every live and announced data-center site using public filings, national electricity authority connection registers, and trade association digests such as GCCIA grid statistics, OFV data flow bulletins, and Arab ICT Union yearbooks. Our team then pulled tariff schedules, generator import records, and customs codes from UN Comtrade to size hardware flows by country. Company 10-Ks, investor decks, and news feeds hosted on Dow Jones Factiva enriched capacity timelines, while D&B Hoovers supplied revenue splits that anchor supplier ASPs. This information created the foundational demand pool.

Additional indicators, including regional AI workload estimates in IEEE journals and patent trends accessed via Questel, helped us validate power-density shifts and redundancy preferences. The sources named illustrate the breadth of materials consulted; many other public and paid inputs fed our desk research.

Market-Sizing & Forecasting

We built a top-down model that starts with installed and announced IT load (MW) and multiplies it by average electrical CAPEX per MW, which is cross-checked with sampled ASP × volume roll-ups from supplier disclosures. Key variables include new hyperscale MW pipeline, rack density trend, utility tariff outlook, UPS replacement cycles, and average generator runtime hours. We forecast each driver through multivariate regression, blended with scenario analysis for grid-constraint risk, and then reconcile outputs with bottom-up facility counts to close gaps created by edge sites that publish limited data.

Data Validation & Update Cycle

Model outputs undergo variance checks against historical customs inflows and independent MW announcements. Senior analysts review anomalies, request clarifications from primary contacts, and approve only when discrepancies fall within set tolerance bands. Reports refresh once a year, and we trigger interim updates whenever major capacity or policy shocks emerge.

Why Mordor's Middle East Data Center Power Baseline Commands Reliability

Published estimates often diverge because firms pick different geographic cut-offs, treat backup capacity inconsistently, or apply one-size price curves to every tier.

Key gap drivers include whether Africa is bundled with the Gulf, if edge facilities under 3 MW are ignored, and how aggressively battery-based UPS adoption is assumed. Mordor Intelligence narrows the scope to the Middle East only, prices hardware by redundancy class, and refreshes its inputs every twelve months, which curbs drift from outdated tariffs or phased project delays.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.65 B (2025) | Mordor Intelligence | - |

| USD 0.54 B (2024) | Regional Consultancy A | Bundles Africa, applies single facility count multiplier, lacks tier differentiation |

| USD 0.59 B (2024) | Global Consultancy B | Omits edge sites under 3 MW and prices only installed UPS capacity, linear projection without scenario checks |

These comparisons show that Mordor's disciplined scope selection, variable tracking, and annual refresh cadence deliver a balanced, transparent baseline that decision-makers can reproduce and trust.

Key Questions Answered in the Report

How big is the Middle East Data Center Power Market?

The Middle East Data Center Power Market size is expected to reach USD 0.65 billion in 2025 and grow at a CAGR of 12.70% to reach USD 1.19 billion by 2030.

What is the current Middle East Data Center Power Market size?

In 2025, the Middle East Data Center Power Market size is expected to reach USD 0.65 billion.

Who are the key players in Middle East Data Center Power Market?

Vertiv Group Corp., Eaton Corporation, ABB Ltd, Legrand Group and Schneider Electric SE are the major companies operating in the Middle East Data Center Power Market.

What years does this Middle East Data Center Power Market cover, and what was the market size in 2024?

In 2024, the Middle East Data Center Power Market size was estimated at USD 0.57 billion. The report covers the Middle East Data Center Power Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Middle East Data Center Power Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: