United Arab Emirates Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

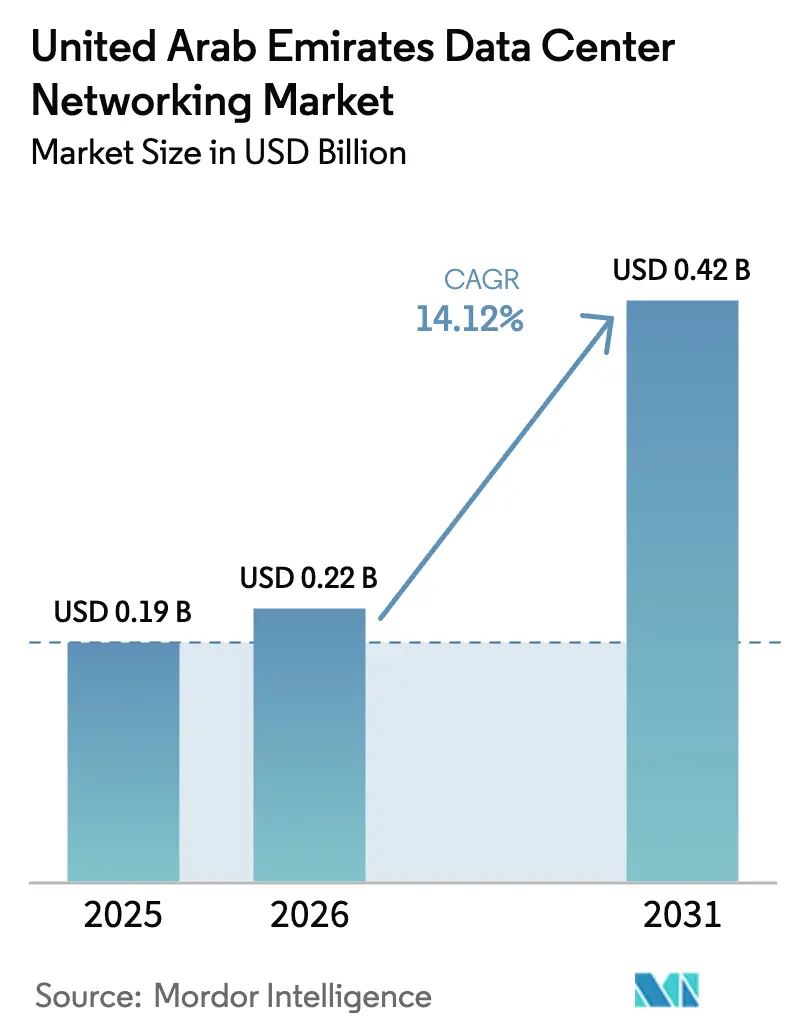

| Base Year Market Size (2025) | USD 0.19 Billion |

| Market Size (2026) | USD 0.22 Billion |

| Market Size (2031) | USD 0.42 Billion |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Data Center Networking Market Analysis by Mordor Intelligence

The UAE data center networking market size was valued at USD 0.19 billion in 2025 and estimated to grow from USD 0.22 billion in 2026 to reach USD 0.42 billion by 2031, at a CAGR of 14.12% during the forecast period (2026-2031). This rapid expansion stems from AI‐centric infrastructure projects, government digital-transformation programs, and the country’s role as a Middle East connectivity gateway. Hyperscale investors are committing multi-billion-dollar budgets to build large-footprint, AI-ready campuses, while nationwide 5G coverage accelerates edge-to-core traffic growth. Public-sector modernization mandates spur cloud migration and software-defined networking adoption, and the arrival of new submarine cables at Fujairah reinforces ultra-low-latency international routes. Strong demand for 400 G and 800 G switching fabrics, coupled with liquid-cooling innovations that address the desert climate, further amplifies capital spending across the UAE data center networking market. Strategic vendor alliances—such as G42’s Stargate UAE collaboration with Nvidia, Oracle, Cisco, and OpenAI—signal a sustained pipeline of large projects that will keep competitive pressure high through the forecast window.

Key Report Takeaways

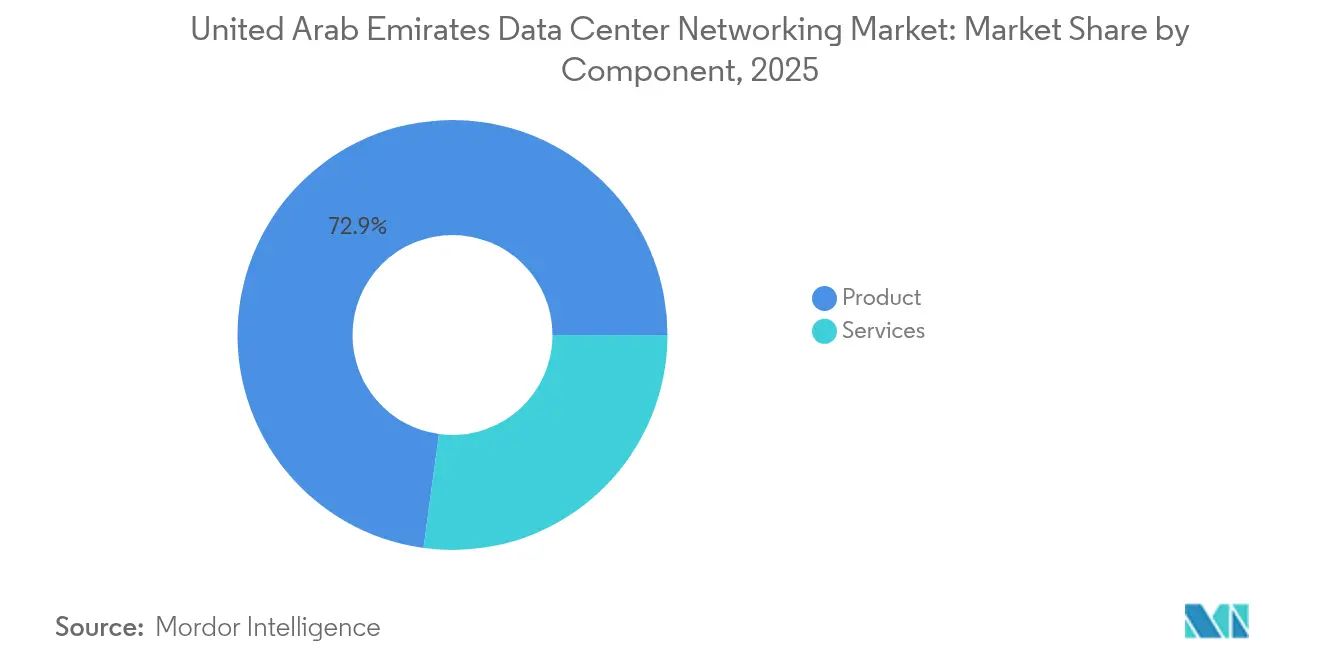

- By component, products led with 72.85% of the UAE data center networking market share in 2025, while services are projected to grow at a 14.32% CAGR through 2031.

- By end-user, IT and telecommunications accounted for 35.05% revenue share in 2025; manufacturing and industrial applications are forecast to expand at a 14.72% CAGR to 2031.

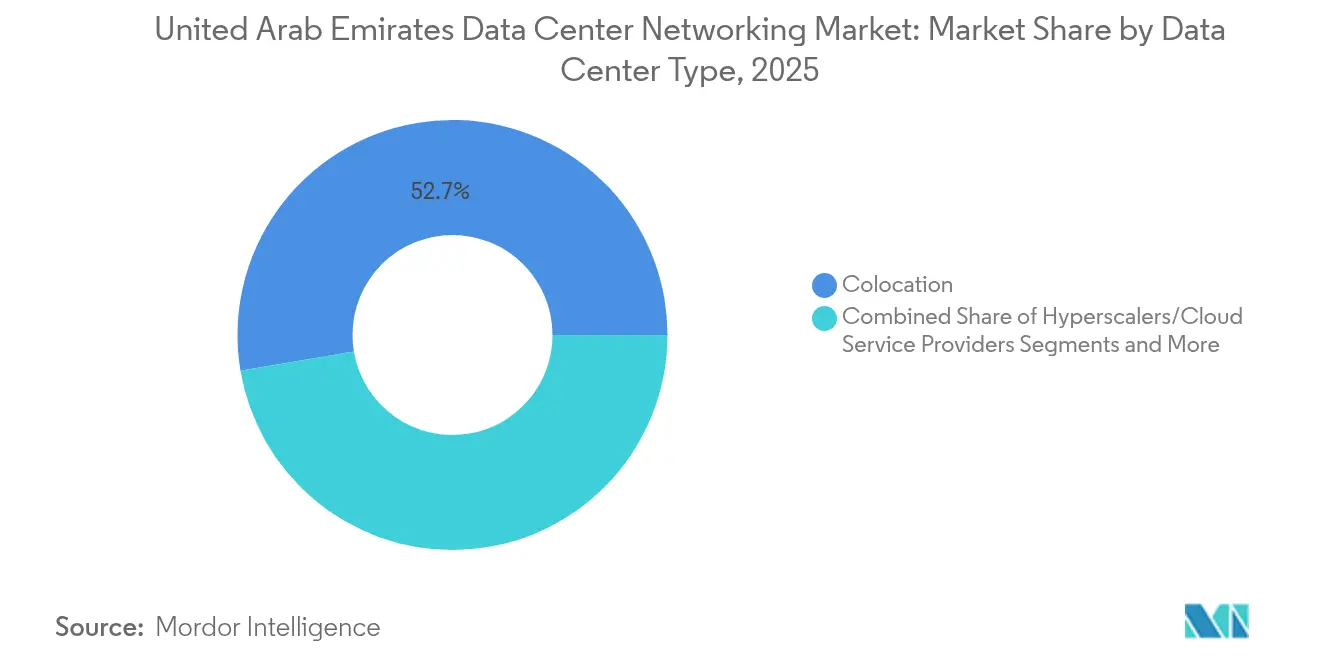

- By data-center type, colocation facilities held 52.65% of the UAE data center networking market size in 2025, whereas hyperscaler deployments are set to grow at a 15.88% CAGR during the same period.

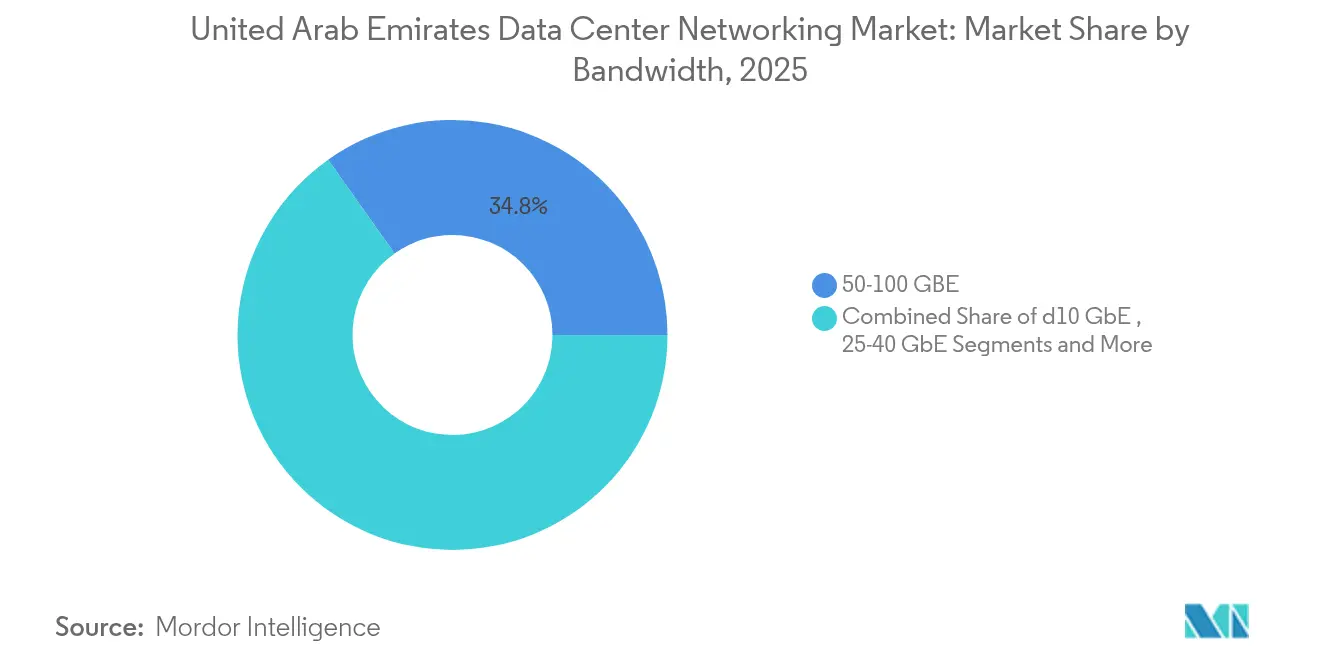

- By bandwidth, 50-100 GbE implementations captured 34.82% of the UAE data center networking market size in 2025; the >100 GbE segment is advancing at a 15.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing hyperscale data-center build-outs | +4.2% | Dubai, Abu Dhabi core with spillover to Northern Emirates | Medium term (2-4 years) |

| Rapid 5G roll-outs boosting edge-data-center interconnect demand | +3.1% | Nationwide, earliest in Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Government-led digital-transformation programs | +2.8% | National, concentrated in major emirates | Long term (≥ 4 years) |

| Shift toward software-defined and virtualised networking | +2.3% | Global adoption with UAE early implementation | Medium term (2-4 years) |

| New submarine-cable landings at Fujairah | +1.1% | Fujairah core with nationwide benefits | Long term (≥ 4 years) |

| Adoption of liquid-cooling-ready switching hardware | +0.8% | National, notably Abu Dhabi and Dubai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing hyperscale data-center build-outs in Dubai and Abu Dhabi

Intensive capital flows into hyperscale campuses are driving the most substantial uplift in network equipment demand. Khazna Data Centers—majority-owned by G42—announced a 100-megawatt AI-ready site in Ajman, while Microsoft partnered with du on a USD 544 million hyperscale facility that expands du’s five-site footprint. International investors, including Silver Lake and MGX, acquired a 40% stake in Khazna for USD 2.2 billion, validating the growth outlook. Large-scale deployments require ultra-dense switching fabrics, 400 G optics, and robust interconnection to regional Internet exchanges, reinforcing the adoption of advanced data-center networking topologies.

Rapid 5G roll-outs boosting edge-data-center interconnect demand

Nationwide 5G coverage fuels edge-computing uptake and prompts operators to deploy regional micro-data centers. e& achieved record 5G throughput of 30.5 Gbps via carrier aggregation, showcasing the network’s ability to sustain data-intensive applications e&. du activated a commercial 5G Standalone network with slicing capability for differentiated enterprise workloads. These milestones propel demand for low-latency backhaul links between far-edge locations and core facilities, accelerating the shift toward software-defined wide-area networking across the UAE data center networking market.

Government-led digital-transformation programs (Smart Dubai, UAE Vision 2031)

Public-sector strategies require near-universal digital service availability, leading ministries and municipalities to refresh underlying network fabrics. Smart Dubai’s portfolio of 130 digital initiatives, including Dubai Pulse, generates persistent demand for scalable, secure connectivity.[1]Digital Dubai, “Smart Dubai Initiatives,” digitaldubai.ae The UAE Ministry of Health deployed Fortinet SD-WAN across 160 sites to unify clinical data exchange, illustrating how agency-level roll-outs cascade into multi-million-dollar infrastructure contracts. Commitments to net-zero emissions by 2050 also incentivize energy-efficient switches and liquid-cooling solutions.

Adoption of liquid-cooling-ready switching hardware for desert-climate efficiency

Ambient temperatures surpassing 45 °C make air-only cooling impractical for high-density racks. Immersion techniques can cut energy consumption by 50% and raise rack power budgets above 250 kW, ensuring reliable operation for AI clusters.[2]IEEE Spectrum, “Immersion Cooling Cuts Datacenter Energy,” spectrum.ieee.org Vendors designing switches with integrated liquid manifolds gain a competitive edge as operators pursue aggressive power-usage-effectiveness (PUE) targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified data-center network engineers | -1.8% | Nationwide, acute in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| High upfront capex for next-gen 400 G+ switching fabrics | -1.4% | Global impact with UAE early adoption challenges | Medium term (2-4 years) |

| Import duties and long lead-times for specialised networking gear | -1.1% | National, all emirates | Medium term (2-4 years) |

| Data-localisation and cyber-residency rules delaying public-cloud fabrics | -0.9% | National, DIFC, and ADGM exemptions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import duties and long lead-times for specialised networking gear

Customs clearance adds administrative steps for AI-optimized switches, and semiconductor shortages extend delivery windows beyond six months for certain line cards. Operators consequently maintain larger inventory buffers, which ties up capital and increases total cost of ownership.

Data-localisation and cyber-residency rules delaying public-cloud fabrics

Federal Decree-Law 45 of 2021 mandates in-country storage of sensitive datasets, compelling cloud providers to re-architect global footprints.[3]Federal Decree-Law 45 (2021) Text, u.ae Certification of multi-zone regions under differing free-zone regulations lengthens deployment roadmaps and tempers near-term equipment imports, though the regulation simultaneously creates domestic build-out opportunities in the longer term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Product-centric spending remains dominant

Products accounted for 72.85% of the UAE data center networking market in 2025 as operators raced to install high-capacity switches, routers, and optical links needed for AI cluster backbones. Ethernet switches alone consumed a major portion of capex, particularly 400 G leaf-spine designs that reduce east-west latency. Optical interconnects have also advanced, driven by nationwide backbones interlinking hyperscale sites in Dubai and Abu Dhabi. Services, although smaller, are growing at a 14.32% CAGR. Integration, optimization, and managed SDN offerings gain traction as enterprises outsource complex configuration tasks to specialist partners equipped with AI-aware network analytics.

Service growth reflects a shortage of in-house network engineers and the need for continuous tuning of AI pipelines. Managed service providers bundle software updates, telemetry, and remote troubleshooting, converting one-time hardware engagements into recurring revenue streams. This evolution increases lifetime customer value in the UAE data center networking market and fosters ecosystem partnerships between global OEMs and local integrators.

By End-User: Manufacturing emerges as fastest riser

IT and telecommunications retained 35.05% of the UAE data center networking market share in 2025, mirroring telco core upgrades and cloud availability-zone roll-outs. Banking, financial services, and insurance segments follow, investing in low-latency fabrics to secure trading and payment platforms. Manufacturing and industrial enterprises, however, pace the CAGR leaderboard at 14.72% through 2031. Emirates Global Aluminium’s Industry 4.0 lighthouse designation highlights the heavy-industry shift toward real-time analytics and predictive maintenance, which require deterministic networking inside smart factories. Healthcare also accelerates, as the Malaffi Health Information Exchange links 1.7 billion records across clinical sites.

Cross-vertical dynamics underscore a broader pivot toward distributed intelligence at the plant floor and in hospitals. As each sector digitizes workflows, demand cascades down the stack for secure, high-bandwidth connections into centralized analytics clusters. These trends reinforce the multi-tenant growth story of the UAE data center networking market.

By Data-Center Type: Hyperscalers narrow the gap

Colocation providers commanded 52.65% of the UAE data center networking market size in 2025 thanks to carrier-neutral neutrality and rapid provisioning. Yet hyperscaler self-builds are growing at a 15.88% CAGR, shifting share as global cloud giants prioritize sovereign capacity. Dedicated campuses such as Microsoft’s facility offer deterministic performance for AI training while satisfying data-residency rules. Edge and micro centers add another layer, supplying base-station proximity for 5G network slicing.

Operators design hybrid interconnect fabrics that stitch edge locations to metro core nodes and on to hyperscale regions. Liquid-cooled switches inside AI pods feed high-density GPUs, while SD-WAN overlays extend policy control into micro-edge enclosures the size of a shipping container. The architecture diversification supports continued expansion of the UAE data center networking market.

By Bandwidth: 100 G+ becomes the new mainstream

Deployments in the 50-100 GbE tier held 34.82% of 2025 shipments as enterprises refreshed long-lived 10/25 G links. Nevertheless, >100 GbE installations are climbing at a 15.02% CAGR as operators embrace 400 G and beyond for AI cluster interconnect. Trials of 1.6 Tbps optical lanes by e& foreshadow a future where bandwidth doubles every hardware cycle. Edge nodes still leverage ≤10 GbE for sensor traffic, while 25-40 GbE uplinks bridge legacy server racks to new leaf fabrics.

Steady price declines in PAM4 optics narrow the cost delta between 100 G and 400 G ports, encouraging early adopters to leapfrog intermediate speeds. Disaggregated chassis with modular line cards allow gradual scale-out, limiting stranded capacity risks and bolstering the long-run outlook for the UAE data center networking market.

Geography Analysis

Dubai and Abu Dhabi anchor the nation’s 52 operational data centers, jointly delivering most of the 235 MW live capacity. Expansion plans add 343 MW, with Ajman emerging as a supplementary AI cluster location. Dubai’s early foundation—set by Dubai Internet City—offers dense carrier ecosystems and favorable free-zone incentives. Abu Dhabi leverages sovereign wealth backing and abundant land for mega-campuses such as Stargate UAE, slated for 5 GW over multiple phases. Fujairah’s cable-landing stations integrate international traffic, routing east-west fiber paths that lower latency for cross-continental workloads.

Northern emirates witness spill-over as power-price differentials and land-bank availability attract secondary builds. The national energy mix, featuring nuclear at Barakah and solar at Mohammed bin Rashid Al Maktoum Solar Park, helps operators meet carbon targets while containing operating costs. Federal data-sovereignty laws create a must-build environment for multinational clouds, cementing domestic capacity additions rather than remote serving. The ascending capital curve in neighboring Saudi Arabia and Qatar intensifies regional rivalry, but the UAE’s regulatory clarity and diversified power sources sustain its competitive edge.

Competitive Landscape

The vendor arena blends global switch and router manufacturers, regional integrators, and emerging cloud-native software suppliers. G42 and Etisalat formed Khazna Data Centers, consolidating carrier-neutral colocation assets and elevating domestic scale. Silver Lake and MGX’s USD 2.2 billion minority stake underscores international appetite for UAE digital infrastructure. Arista Networks surpassed Cisco in global data-center switch share in Q4 2023, a signal that open-standards platforms resonate with AI-focused operators. Broadcom’s merchant silicon roadmap and Nvidia’s Mellanox interconnect technologies penetrate switching line-cards destined for AI clusters.

Strategic moves include Nokia’s acquisition of Infinera to fortify an optical super-division with SDN-ready coherent pluggables, and Qualcomm’s partnership with e& to seed edge-AI gateways. Local system integrators bolt specialized services onto hardware from these majors, filling skills gaps in deployment and supporting the UAE data center networking industry shift toward automation. Vendors that can combine energy-efficient designs, desert-rated cooling, and AI flow-aware telemetry are positioned to win upcoming tenders.

United Arab Emirates Data Center Networking Industry Leaders

Cisco Systems Inc.

VMware Inc.

Fujitsu Ltd.

Schneider Electric

Eaton Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: G42 unveiled Stargate UAE, a 5 GW AI campus in Abu Dhabi in partnership with Nvidia, Oracle, Cisco, and OpenAI.

- May 2025: Qualcomm and e& launched a joint engineering center in Abu Dhabi to develop 5G edge-AI gateways.

- April 2025: Microsoft and du closed a USD 544 million hyperscale data-center agreement in the UAE.

- March 2025: Nokia finalized a USD 2.3 billion acquisition of Infinera, expanding its optical networks portfolio.

United Arab Emirates Data Center Networking Market Report Scope

Data center networking refers to the set of technologies, protocols, and hardware used to connect physical and network-based devices and manage the network infrastructure, storage, and processing of applications and data. Data center networking is very critical for 100% uptime of data centers. In the current web-connected world, business workloads are executed on single computers, hence leading to the need for data center networking. Networks provide servers, clients, applications, and middleware with a standard plan to stage the execution of workloads and also to manage access to the data produced.

The South Korean data center networking market is segmented by product (ethernet switches, routers, storage area network (SAN), application delivery controllers (ADC), and other networking equipment), by services (installation & integration, training & consulting, and support & maintenance), and by end-user (IT & telecommunication, BFSI, government, media & entertainment, and other end users).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Products | Ethernet Switches |

| Routers | |

| Storage Area Network (SAN) | |

| Application Delivery Controllers (ADC) | |

| Network Security Appliances | |

| Software-Defined Networking (SDN) Controllers | |

| Optical Interconnects | |

| Services | Installation and Integration |

| Training and Consulting | |

| Support and Maintenance | |

| Managed Network Services |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Defense |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Other End-Users |

| Colocation |

| Hyperscalers/Cloud Service Providers |

| Edge/Micro Data Centers |

| Less than or equal to 10 GbE |

| 25-40 GbE |

| 50-100 GbE |

| Greater than 100 GbE |

| By Component | Products | Ethernet Switches |

| Routers | ||

| Storage Area Network (SAN) | ||

| Application Delivery Controllers (ADC) | ||

| Network Security Appliances | ||

| Software-Defined Networking (SDN) Controllers | ||

| Optical Interconnects | ||

| Services | Installation and Integration | |

| Training and Consulting | ||

| Support and Maintenance | ||

| Managed Network Services | ||

| By End-User | IT and Telecommunications | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Defense | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial | ||

| Other End-Users | ||

| By Data-Center Type | Colocation | |

| Hyperscalers/Cloud Service Providers | ||

| Edge/Micro Data Centers | ||

| By Bandwidth | Less than or equal to 10 GbE | |

| 25-40 GbE | ||

| 50-100 GbE | ||

| Greater than 100 GbE | ||

Key Questions Answered in the Report

What is the current value of the UAE data center networking market?

The market stands at USD 0.22 billion in 2026 and is projected to double to USD 0.42 billion by 2031.

Which segment is expanding fastest within the UAE data center networking market?

Hyperscaler data-center deployments are growing at a 15.88% CAGR, outpacing other facility types through 2031.

How are 5G roll-outs influencing UAE data center networking investments?

Nationwide 5G coverage drives demand for edge micro-data centers and low-latency interconnects, accelerating purchases of software-defined wide-area networking solutions and higher-bandwidth backhaul links.

What are the main challenges confronting operators in the UAE data center networking industry?

Skill shortages in certified network engineers, high upfront costs for 400 G+ equipment, import lead-times, and compliance with data-localization laws are the primary hurdles.

Page last updated on: