United Kingdom Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

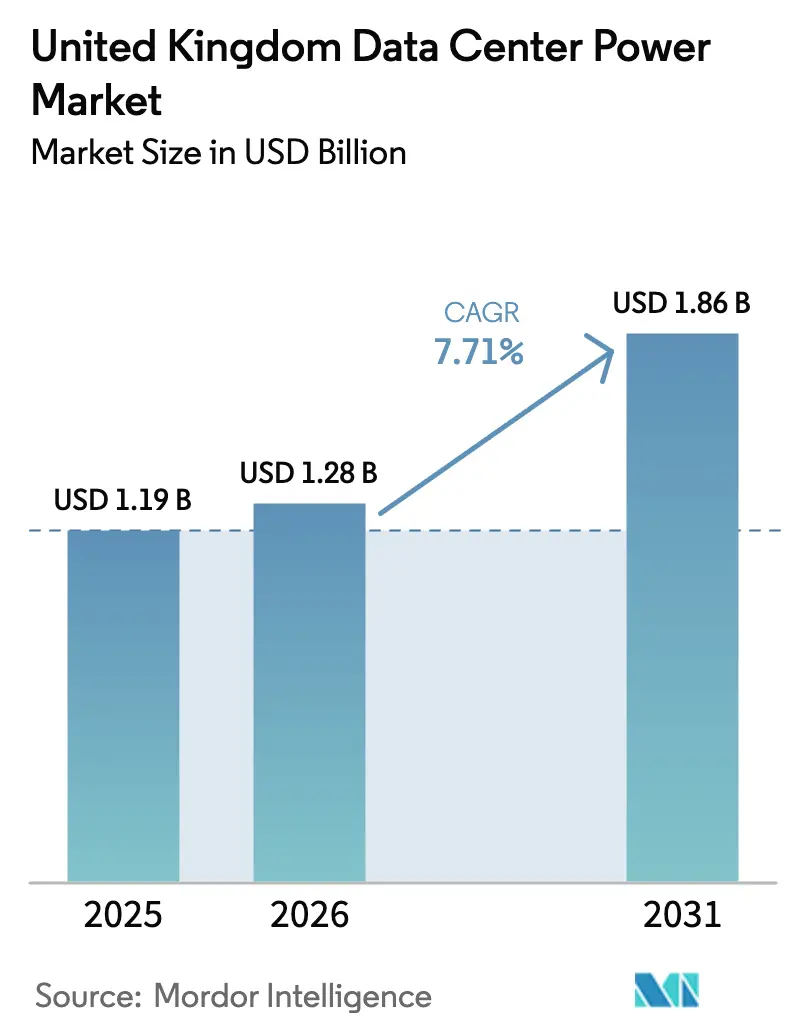

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 7.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Data Center Power Market Analysis by Mordor Intelligence

The United Kingdom data center power market size was valued at USD 1.19 billion in 2025 and estimated to grow from USD 1.28 billion in 2026 to reach USD 1.86 billion by 2031, at a CAGR of 7.71% during the forecast period (2026-2031). Rapid AI adoption is pushing rack densities from 5-10 kW to 30-50 kW, forcing operators to redesign electrical architectures and reinforce grid connections. Government recognition of data centers as Critical National Infrastructure in 2024 has accelerated planning approvals, while sustainability mandates are steering investment toward renewable-ready designs and grid-interactive UPS technology. Colocation still commands the largest share, but hyperscale facilities are scaling faster as they chase AI capacity. Hydrogen-compatible backup systems and busway-based distribution are emerging as key differentiators in the United Kingdom data center power market.

Key Report Takeaways

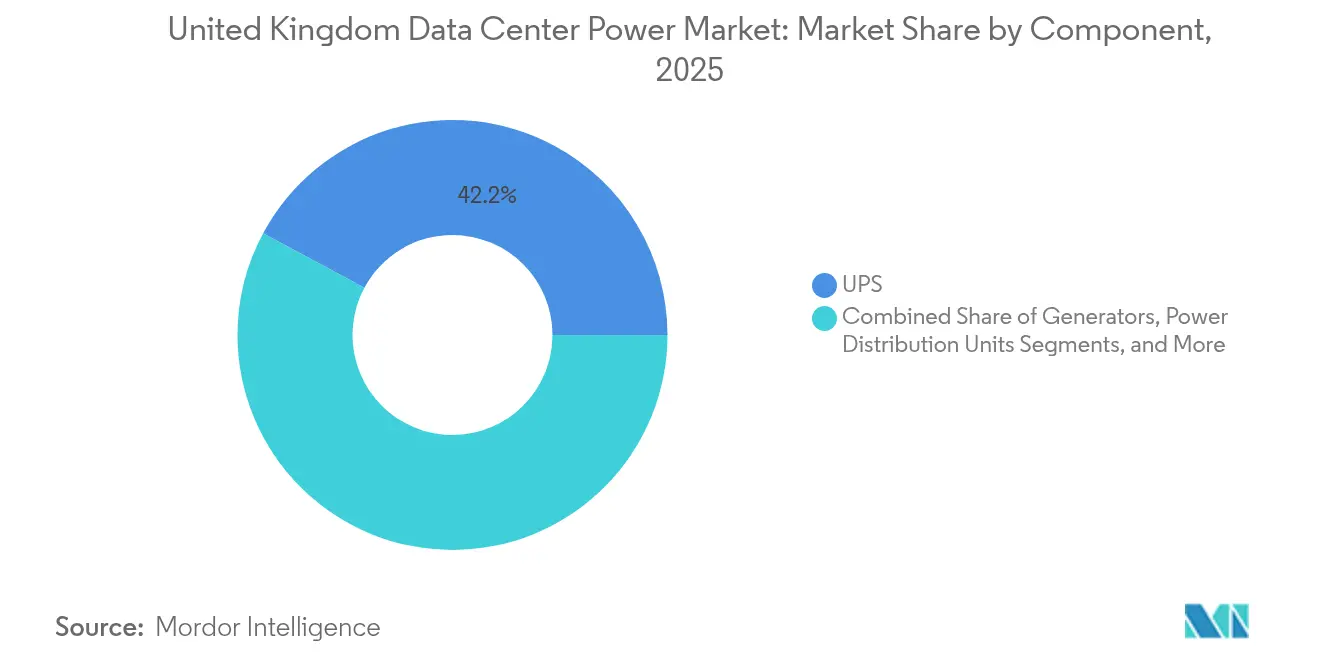

- By component, UPS systems led the United Kingdom data center power market with 42.15% of the market share in 2025; PDUs are forecast to expand at a 9.12% CAGR through 2031.

- By data center type, colocation operators held a 34.85% share of the United Kingdom's data center power market in 2025, while hyperscalers are expected to advance at a 10.31% CAGR through 2031.

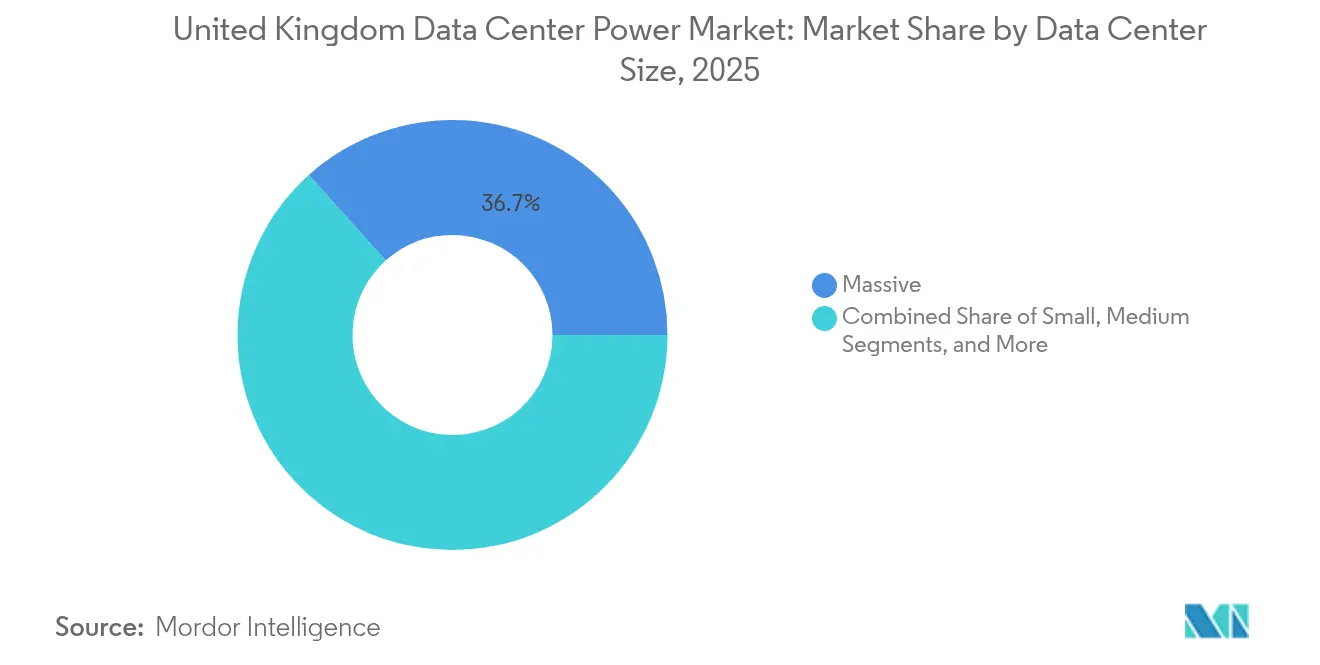

- By size, large facilities accounted for a 36.65% share of the United Kingdom data center power market in 2025; mega sites are projected to post an 11.08% CAGR through 2031.

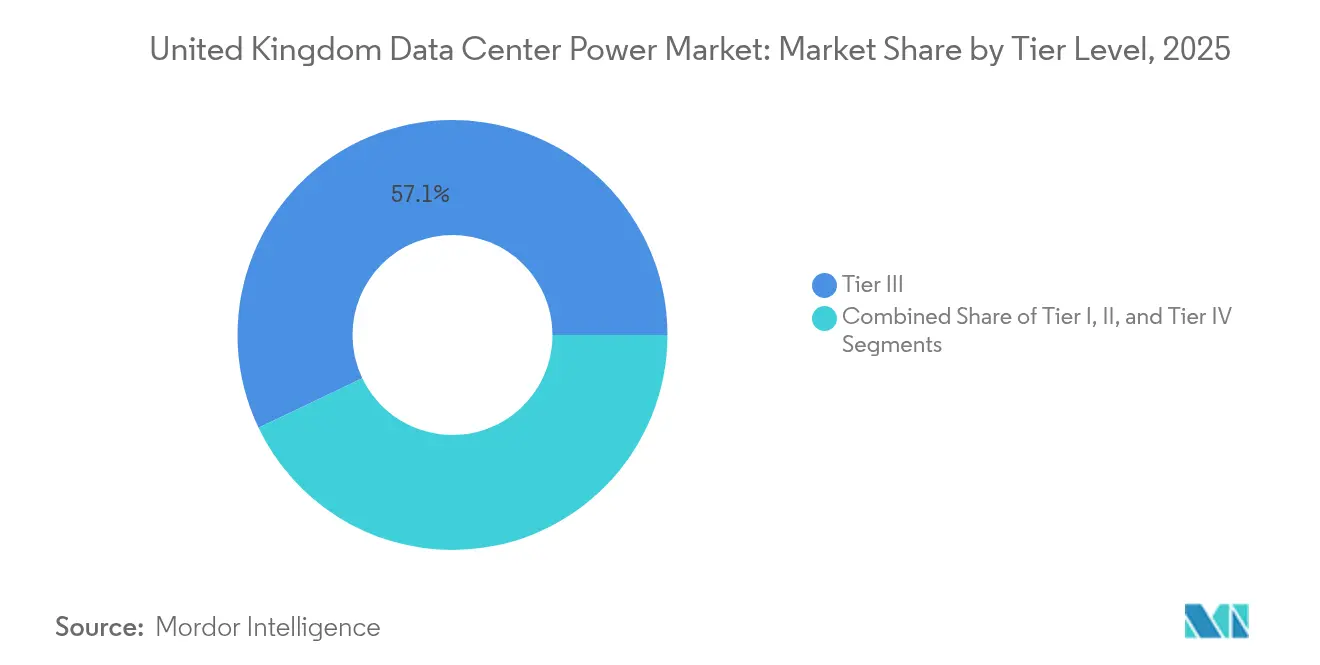

- By tier level, Tier III sites dominated the United Kingdom data center power market with a 57.10% share in 2025; Tier IV facilities are projected to grow at a 9.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of mega and hyperscale facilities | +1.2% | Global, concentrated in South-East England | Medium term (2-4 years) |

| Cloud-first enterprise and AI workload surge | +2.1% | National, with early gains in London, Manchester, Birmingham | Short term (≤ 2 years) |

| Sustainability regulations driving renewable power integration | +0.9% | National, stricter enforcement in London ULEZ zones | Long term (≥ 4 years) |

| Grid-interactive UPS monetisation via National Grid ESO services | +0.7% | National grid-connected facilities | Medium term (2-4 years) |

| Hydrogen-ready backup design ahead of 2030 diesel phase-out | +0.8% | National, pilot projects in industrial regions | Long term (≥ 4 years) |

| AI/ML rack-density growth | +1.8% | Global, concentrated in hyperscale facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising adoption of mega and hyperscale facilities

Mega and hyperscale campuses are reshaping the United Kingdom data center power market as operators secure dedicated substations, install on-site 400 kV connections, and deploy AI-driven energy management platforms that enhance PUE performance. Blackstone’s GBP 13 billion (USD 16.3 billion) Northern England campus, CoreWeave’s GBP 1 billion (USD 1.36 billion) expansion project illustrate this scale shift, each demanding multi-hundred-megawatt footprints and reinforcing grid capacity in underserved regions. These facilities have become magnets for renewable micro-grids and private-wire power purchase agreements, embedding long-term sustainability into the investment thesis. As a result, the UK data center power market is transitioning toward larger, fewer, and more efficient sites that can unlock economies across distribution, cooling, and operations. Suppliers that offer modular substations, intelligent busway, and hydrogen-ready UPS equipment are increasingly favored in project tenders.

Cloud-first enterprise and AI workload surge

Surging AI inference and training workloads drive volatile 30-50 kW rack profiles, compounding instantaneous load swings that challenge legacy PDUs and static switchgear. Enterprises pivoting to public cloud place urgent capacity demands on London and Southeast campuses, prompting hyperscalers to pre-purchase grid capacity five years in advance. Power quality analytics now sit alongside battery-state monitoring in facility dashboards, ensuring GPU clusters operate within strict voltage tolerances. Consequently, the United Kingdom data center power market is witnessing a surge in record orders for lithium-ion battery cabinets, modular rectifiers, and dynamic back-feed protection. The International Energy Agency projects that AI will drive a doubling of global data center electricity demand to approximately 945 TWh by 2030, with AI-optimized facilities expected to quadruple their electricity consumption.[1]International Energy Agency, “AI is set to drive surging electricity demand from data centres while offering the potential to transform how the energy sector works,” iea.org

Sustainability regulations driving renewable power integration

Mandates under the Clean Energy Mission spur operators to sign long-term wind and solar PPAs, install rooftop photovoltaic arrays, and adopt battery-storage peakers to buffer intermittency. Digital Realty alone now holds 1.4 GW of contracted renewable supply, a template increasingly adopted by peers.[2]Digital Realty, “Environmental, Social, and Governance (ESG) report,” digitalrealty.co.ukData centers are deploying AI-driven energy-management software that shifts non-critical workloads to periods with high renewable energy availability, thereby reducing Scope 2 emissions. These strategies broaden the supplier base within the United Kingdom data center power market to include BESS integrators and micro-grid specialists capable of synchronizing multiple renewable feeds, demand-response modules, and hydrogen fuel-cell stacks. As carbon taxes tighten, the financial payback on green-premium UPS designs shortens, propelling further adoption.

Grid-interactive UPS monetization via National Grid ESO services

Operators now regard UPS installations as revenue assets rather than sunk costs. Grid-code-compliant inverters allow facilities to deliver fast-frequency response, demand turn-up, and virtual inertia services. Vertiv’s Liebert EXL S1 is already dispatching spare capacity into National Grid ESO markets without compromising ride-through times.[3]Vertiv, “How to Maximize Revenues from Your Data Center Energy,” vertiv.com Participation offsets TNUoS charges, improving project IRR and accelerating refresh cycles for legacy static UPS fleets. Academic studies confirm that coordinated UPS and chiller thermal inertia can unlock gigawatts of flexible capacity nationwide. Consequently, the United Kingdom data center power market integrates electricity-trading APIs directly into power-management layers, linking facility controls with balancing-mechanism portals and reshaping operator skill-sets toward energy-market trading

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for electrical infrastructure and upgrades | -1.2% | National | Medium term (2-4 years) |

| Lengthy grid-connection lead times in South-East UK | -0.9% | South-East England, particularly London | Short term (≤ 2 years) |

| Ultra-low-emission zones limiting on-site generator testing | -0.4% | Urban centers, particularly London | Medium term (2-4 years) |

| Shortage of HV-certified labour for data-centre builds | -0.7% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX for electrical infrastructure and upgrades

Modern AI nodes require liquid-cooled racks, busways rated to 1,250 A, and lithium-ion UPS strings, which push capital requirements well beyond traditional 2 N diesel-based budgets. Transitioning to hydrogen-ready fuel-cell systems adds a 30-40% cost premium, while busway retrofits often trigger complete switchboard replacements. Operators, therefore, phase builds into 4 MW blocks and favor pay-as-you-grow infrastructure that aligns capital outlay with contracted load. Financing structures now bundle power gear, renewable PPAs, and energy-trading revenues, easing balance-sheet strain but lengthening procurement cycles. These factors temper expansion plans across the United Kingdom data center power market, especially for mid-tier operators lacking hyperscale buying power.

Lengthy grid-connection lead times in South-East UK

Demand in London exceeds local transmission capacity, resulting in connection queues extending to five years. Developers commit to speculative builds in Scotland, Northern Ireland, and Northern England, where capacity is accessible within shorter timelines. UK Power Networks’ Constellation initiative could release 1.98 GVA of headroom; however, many projects will not come online until after 2028. Interim solutions include on-site gas-turbine peakers, battery-storage imports, or peer-to-peer capacity swaps, each adding complexity and cost. The constraint drives a geographic rebalancing of the United Kingdom data center power market, with regional hubs attracting inward investment through expedited substation approvals and renewable-rich microgrids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Dominate While PDUs Accelerate

Uninterruptible power supply units held 42.15% of the United Kingdom's data center power market in 2025, as operators prioritized redundancy and ride-through capability during grid events. Lithium-ion chemistry and silicon-carbide IGBTs now underpin next-generation frames, enabling higher operating temperatures and smaller footprints. Grid-interactive firmware further elevates UPS value by monetising reserve capacity. The United Kingdom data center power market size attributable to UPS installations is projected to expand steadily in line with hyperscale rollouts.

Power distribution units represent the fastest-growing component segment, advancing at a 9.12% CAGR. Intelligent PDUs with per-outlet metering and environmental sensors support AI rack densities, facilitating granular cost allocation in colocation halls. Manufacturers integrate machine-learning algorithms that predict overloads and preempt breaker trips. Adoption is strongest in London’s multi-tenant facilities, but regional builds are quickly following suit as compliance frameworks demand circuit-level energy reporting. Suppliers combining PDU hardware with SaaS analytics are capturing a disproportionate share of incremental spend within the United Kingdom data center power market.

By Data Center Type: Colocation Leads While Hyperscalers Surge

Colocation operators captured 34.85% of the United Kingdom data center power market in 2025, benefiting from enterprises retiring on-premise rooms and seeking flexible contracts. Equinix, Telehouse, and Digital Realty continue to densify London campuses, adding busway retrofit phases that support 20 kW racks without floor reconfiguration. Service differentiation now hinges on smart DCIM suites and renewable matching guarantees that align with corporate ESG goals.

Hyperscalers are the growth engine, recording a 10.31% CAGR as AI-focused cloud services proliferate. Projects exceeding 100 MW commit to direct-to-chip liquid cooling, necessitating new power-to-cooling ratios and dedicated substation loops. These vast campuses attract ecosystem partners such as GPU-leasing start-ups and edge-cache providers, creating self-reinforcing demand clusters. The United Kingdom data center power market size allocated to hyperscale builds is poised to eclipse the colocation share by the end of the decade if current investment trajectories hold.

By Data Center Size: Large Facilities Dominate, Mega Centers Expand Rapidly

Large sites held 36.65% of the United Kingdom data center power market in 2025, striking a balance between scale economies and manageable grid interfaces. Operators deploy modular 4 MW blocks, allowing staged capex and swift customer fit-outs. The segment remains favoured by financial-services tenants that require low-latency metro proximity yet cannot justify hyperscale footprints.

Mega facilities are expanding at an 11.08% CAGR. They leverage private-wire PPAs, on-site battery clusters, and, increasingly, hydrogen-ready backup chains. Centralised utility corridors simplify maintenance and raise load factors. As AI models grow larger, mega campuses attract frontier research programmes, reinforcing their role within the United Kingdom data center power market size growth curve. Suppliers capable of delivering 132 kV primary switchgear, multi-truckload bus duct, and high-capacity liquid-cooling pumps capture the majority of procurement spend in this segment.

By Tier Level: Tier III Dominates While Tier IV Grows for Critical Workloads

Tier III sites accounted for 57.10% of the United Kingdom data center power market in 2025, offering N+1 redundancy that suits most enterprise SLAs at a competitive cost point. Operators optimise energy use through rightsizing generator fleets and employing UPS eco-mode without breaching uptime commitments. These facilities increasingly feature a sectionalised busway to contain fault domains and allow live-phase maintenance.

Tier IV demand is rising at a 9.36% CAGR, driven by algorithmic trading firms, fintechs, and life sciences research that require fault-tolerant power paths. Dual substations, cross-tied switchboards, and 2 N + 1 UPS topologies lift capex but virtually eliminate single points of failure. Hydrogen fuel cells are being piloted in Tier IV annexes, where urban generator testing is subject to air-quality restrictions. The heightened power-density profile positions Tier IV as a pivotal contributor to future United Kingdom data center power market growth, albeit from a smaller base.

Geography Analysis

London and the South-East represented a significant share of the United Kingdom's data center power market in 2025, leveraging dense fibre interconnectivity, proximity to financial services, and established campus ecosystems. Yet transmission-level headroom is shrinking, prompting developers to pre-pay for capacity or accept multi-year delays. Ultra-low-emission zones further complicate diesel-generator testing, accelerating interest in battery-based standby and hydrogen pilots.

Scotland is emerging as a prime alternative. Abundant wind generation, favourable ambient temperatures, and supportive planning councils attract hyperscale commitments. Facilities integrate behind-the-meter wind PPAs that stabilise operating costs and enhance renewable credentials. Northern England follows closely, buoyed by Blackstone’s EUR 13 billion campus, which validates regional viability and catalyzes infrastructure upgrades across Tyneside and Teesside.

Competitive Landscape

The United Kingdom data center power market is moderately concentrated, with Schneider Electric, Vertiv, ABB, and Eaton controlling a large installed base across UPS, switchgear, and busway segments. Schneider Electric recently unveiled the Galaxy VXL UPS, coupled with NVIDIA-validated reference designs that streamline AI rack deployment. Vertiv and Ballard introduced a 400 kW fuel-cell UPS stack that eliminates diesel emissions while enabling fast-frequency response participation.

Merger activity is altering the supplier mix. The union of Anord and Mardix strengthens British-based switchgear competencies, challenging ABB’s e-House offerings in new build tenders. Eaton partnered with Siemens Energy to integrate grid-automation software with modular power rooms, targeting hyperscale campuses that require real-time visibility into sub-second load dynamics.

Innovation themes revolve around grid-interactive firmware, solid-state transfer switches, and hydrogen-compatible generator frames. Vendors able to certify equipment under both Uptime Tier standards and emerging Sustainability Site Facility (SSF) metrics gain an advantage. As AI rack densities increase, thermal-aware power distribution, liquid-cooled busways, and direct current power trunks are emerging as the next battlegrounds in the United Kingdom's data center power market.

United Kingdom Data Center Power Industry Leaders

Schneider Electric SE

Vertiv Group Corp.

ABB Ltd.

Eaton Corporation plc

Caterpillar Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vertiv and Ballard Power Systems launched the industry's first zero-emission UPS for data centers, delivering 400 kW per module, Hydrogen Central.

- March 2025: Blackstone received approval for a GBP 13 billion (USD 17.67 billion) hyperscale data center in Northern England, incorporating 100% renewable energy. Datacenters.com

- March 2025: Schneider Electric unveiled the Galaxy VXL UPS and AI-optimised reference designs at Data Centre World London 2025 Schneider Electric.

- February 2025: Eaton and Siemens Energy announced a strategic partnership to deliver integrated power and grid-automation solutions Siemens Energy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom data center power market as the annual spending on electrical infrastructure, UPS systems, switchgear, PDUs, backup generators, energy storage, and related site-level power management services deployed inside cloud, colocation, enterprise, and edge facilities across the country.

Scope Exclusion: cooling equipment, electricity tariffs, and diesel or gas fuel purchases are kept outside the value pool.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Desk Research

We began by compiling shipment, capacity, and price indicators from publicly accessible tier-1 sources such as the Department for Science, Innovation & Technology, National Grid ESO, Ofgem, Uptime Institute, techUK, and academic journals that track power-use effectiveness trends. Company filings, UK planning portals, and reputable media archived on Dow Jones Factiva added project-level detail, while D&B Hoovers supplied financial splits for major OEMs active in switchgear and UPS. Cross-checking with import statistics, patent abstracts, and EU regulatory releases allowed us to map technology adoption curves and spot regional biases in grid-connection queues. These sources are illustrative; many additional references informed validation and clarifications.

Primary Research

Mordor analysts conducted structured interviews with facility engineers at hyperscale campuses, procurement heads at colocation chains, grid-connection consultants, and OEM sales managers across London, Manchester, Scotland, and the South East. The conversations helped us confirm live rack-density ranges, average sales prices, and commissioning lead times, filling gaps left by desk material and tightening model assumptions.

Market-Sizing & Forecasting

A top-down build starts with DSIT-reported installed IT load (MW), which is linked to typical power-infrastructure cost per megawatt and refreshed with surveyed ASP movements. Results are then balanced against bottom-up checkpoints such as sampled UPS shipments and channel stock rolls. Key drivers in the model include rack-density migration, share of hyperscale square footage, grid-connection lead-time shifts, average PUE, and lithium-ion UPS penetration. Forecasts to 2030 rely on a multivariate regression that blends projected IT load, cloud CAPEX, and GDP growth, with scenario bands agreed by primary-research experts.

Data Validation & Update Cycle

Outputs pass variance tests against government load statistics and OEM revenue disclosures. An analyst peer review resolves anomalies before sign-off. We refresh the dataset annually and issue mid-cycle updates when material events, such as major grid policy changes, arise. A final sense check is performed just before delivery, ensuring clients receive the latest numbers.

Why Mordor's United Kingdom Data Center Power Baseline Stand Firm

Published estimates often diverge because studies select different facility types, component lists, and forecast cadences.

Two common gap drivers are the bundling of mechanical cooling with electrical spend and the use of aggressive CAGR scenarios that stretch historic relationships between IT load and infrastructure outlays.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.19 B (2025) | Mordor Intelligence | |

| USD 2.86 B (2024) | Global Consultancy A | Bundles cooling assets and energy management software, applies regional extrapolation with limited primary checks |

| USD 1.24 B (2023) | Industry Journal B | Focuses only on core hardware sold into on-prem enterprise rooms; omits colocation and hyperscale segments |

| USD 6.13 B (2030) | Global Consultancy C | References a forecast year and assumes 13 % CAGR plus resale of grid services revenue, inflating the baseline |

In summary, Mordor's analysts anchor values to observable MW capacity, clearly defined component spend, and a measured forecast engine, giving decision-makers a dependable, transparent baseline that can be replicated with publicly auditable variables.

Key Questions Answered in the Report

What is the current value of the United Kingdom data center power market?

The market is valued at USD 1.28 billion in 2026 and is set to reach USD 1.86 billion by 2031.

Why are grid-interactive UPS systems gaining traction?

They allow operators to earn revenue from National Grid ESO by providing frequency response while still protecting critical loads.

How are sustainability mandates affecting backup power choices?

Operators are shifting toward hydrogen-ready fuel-cell systems and HVO-compatible generators to meet emissions targets ahead of diesel phase-out deadlines.

What tier level is most prevalent in UK facilities?

Tier III dominates with 57.10% market share, offering N+1 redundancy and 99.982% availability for most enterprise workloads.

Page last updated on: