Risk Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

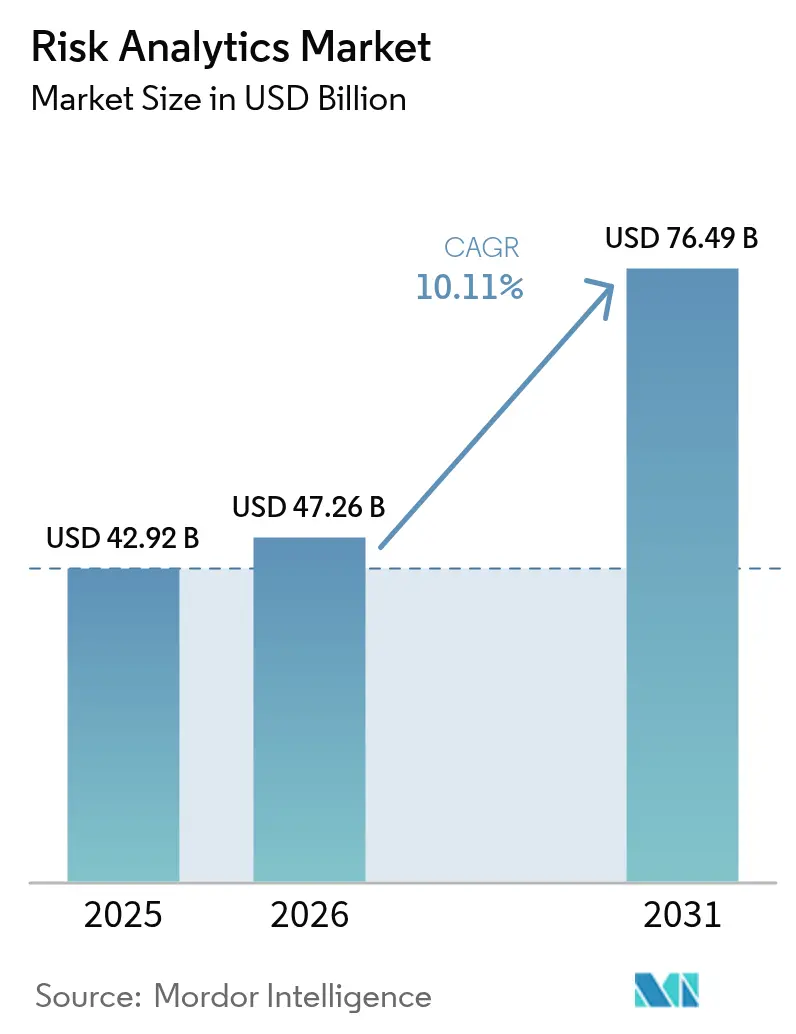

| Market Size (2026) | USD 47.26 Billion |

| Market Size (2031) | USD 76.49 Billion |

| Growth Rate (2026 - 2031) | 10.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Risk Analytics Market Analysis by Mordor Intelligence

The risk analytics market size is expected to grow from USD 42.92 billion in 2025 to USD 47.26 billion in 2026 and is forecast to reach USD 76.49 billion by 2031 at 10.11% CAGR over 2026-2031. Heightened regulatory scrutiny, real-time fraud exposure on instant-payment rails, and mandatory climate-risk disclosure are making advanced analytics a strategic necessity rather than a discretionary IT spend. Financial institutions are phasing out rule-based tools in favor of AI-driven platforms that evaluate millions of data points within milliseconds to support capital optimization, fraud interdiction, and climate scenario modeling. Cloud-native architectures, quantum-resistant algorithms, and unified data fabrics are cutting total cost of ownership while enabling parallel compliance reporting across jurisdictions[1]Google Cloud, “Accelerating Risk Analytics with Secure Data Fabric,” cloud.google.com. The convergence of these forces is reshaping vendor strategies toward platform-as-a-service delivery that merges software, consulting, and managed operations.

Key Report Takeaways

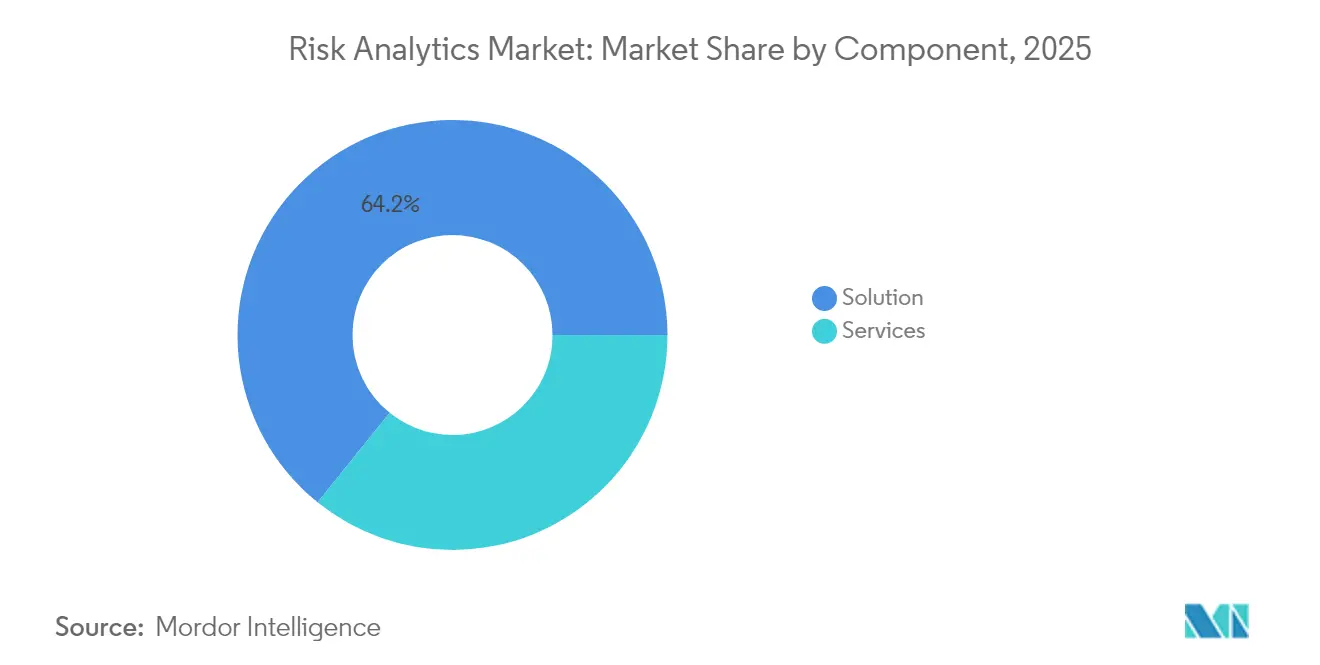

- By component, Solutions led with 64.20% of the risk analytics market share in 2025, while Services are expanding at an 11.62% CAGR to 2031.

- By deployment, On-premises accounted for 66.95% of the risk analytics market size in 2025; Cloud is forecast to grow at 11.92% CAGR through 2031.

- By risk type, Credit risk held 39.85% share of the risk analytics market size in 2025; Climate and ESG risk analytics will expand at an 11.12% CAGR.

- By application, Fraud detection and AML captured 41.05% of the risk analytics market share in 2025; Cyber-risk analytics registers the fastest 10.74% CAGR.

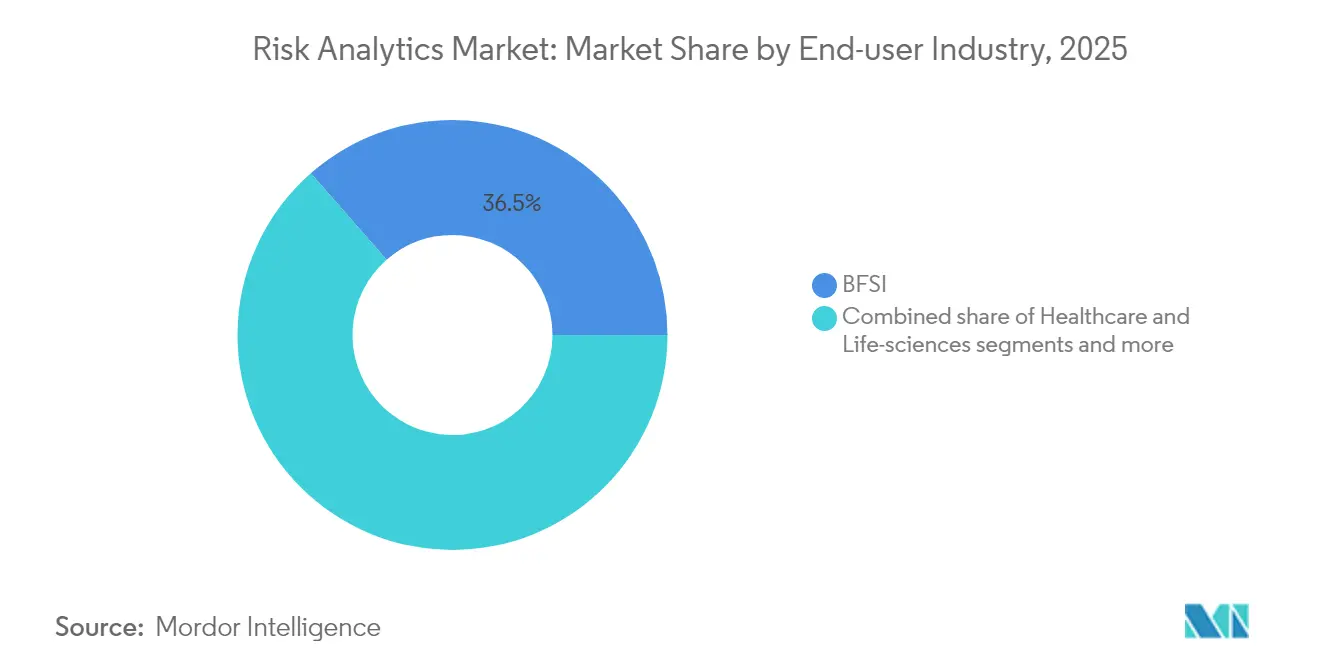

- By end-user industry, BFSI commanded 36.45% of revenue in 2025; Retail and e-commerce will grow at 10.55% CAGR on soaring digital transactions.

- By organisation size, large enterprises represented 68.75% of demand in 2025, but SMEs are advancing at 12.05% CAGR through 2031 on cloud democratization.

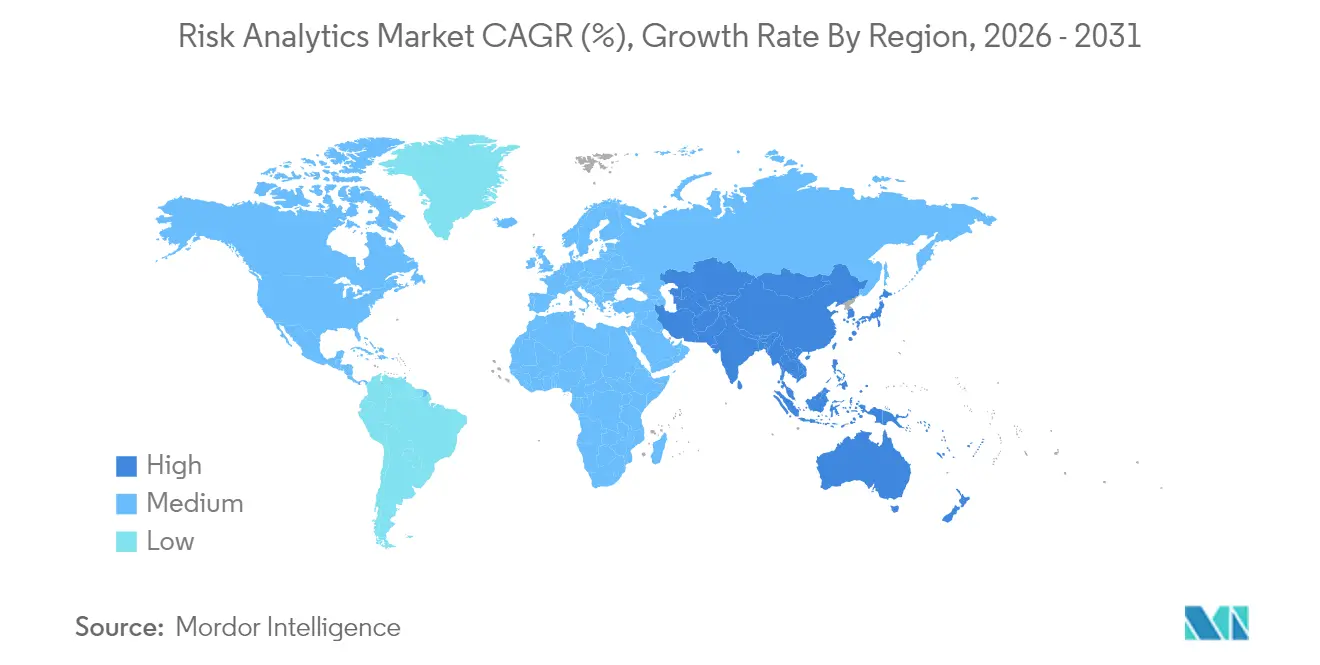

- By geography, North America led with 38.15% revenue share in 2025; Asia-Pacific is projected to expand at an 11.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Risk Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-time fraud surge in instant-payment rails | +2.1% | Global, led by North America and APAC | Short term (≤ 2 years) |

| Heightened post-Basel IV capital-adequacy scrutiny | +1.8% | Global, EU and UK lead | Medium term (2-4 years) |

| Mandatory climate-risk disclosure | +1.5% | Global, EU leads | Long term (≥ 4 years) |

| AI-powered credit scoring for thin-file borrowers | +1.3% | Global, emerging markets focus | Medium term (2-4 years) |

| Multi-cloud risk-data fabrics cut TCO > 25% | +1.1% | North America and EU core, spreading to APAC | Short term (≤ 2 years) |

| Quantum-computing threat to legacy crypto-algos | +0.9% | Global, advanced economies first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Real-time fraud surge in instant-payment rails

Instant settlement environments expose banks to transaction-level attacks that overwhelm batch fraud tools. Global real-time payment volumes are on track to hit 575 billion transactions by 2028, forcing institutions to deploy millisecond analytics that blend behavioral biometrics, device intelligence, and network analytics while maintaining false-positive rates below 1%[2]European Payments Council, “2024 Payment Threats and Fraud Trends Report,” europeanpaymentscouncil.eu. The United Kingdom’s mandatory reimbursement rule for authorized push-payment fraud strengthens the economic case for AI-native platforms that score transactions as they occur. Vendors that can combine streaming data ingestion, graph analytics, and model governance within a single cloud-native stack hold a decisive edge.

Heightened post-Basel IV capital-adequacy scrutiny

The EU’s January 2025 Basel IV rollout and FINMA’s enhanced operational-risk ordinances oblige multinational banks to run several risk-weighted asset calculations in parallel. Cloud-based Monte-Carlo engines allow near real-time capital optimization across diverging rulesets while satisfying BCBS 239 data-aggregation tests. As regulators intensify on-site data audits, demand for unified data lineage, audit trails, and scenario libraries accelerates the migration toward service-rich platforms that embed regulatory logic natively.

Mandatory climate-risk disclosure

Federal Reserve guidance now links climate exposure to safety-and-soundness expectations for large banks. The EU Corporate Sustainability Reporting Directive mandates auditable metrics across scopes and asset classes, redirecting budgets toward geospatial analytics that merge satellite imagery with long-run climate models. Institutions are re-engineering credit and market-risk engines to capture transition-risk factors such as carbon pricing. Vendor offerings that integrate physical and transition risk within existing portfolio-risk views are gaining rapid acceptance.

AI-powered credit scoring for thin-file borrowers

Large language models and multimodal AI engines ingest payment history, telco data, and social signals to identify creditworthy applicants lacking formal bureau files. The Monetary Authority of Singapore’s Veritas consortium sets fairness and transparency benchmarks that shape product designs. Banks in India, Nigeria, and Brazil leverage these models to unlock new lending pools without breaching discrimination rules. Demand concentrates on platforms that embed explainability layers, synthetic data augmentation, and bias-testing modules inside scoring workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute talent shortage in model-risk governance | -1.7% | Global, severe in North America and EU | Medium term (2-4 years) |

| Rising SaaS subscription fatigue among mid-tiers | -1.2% | Global, mid-tier institutions | Short term (≤ 2 years) |

| Vendor-lock-in concerns over proprietary ML stacks | -0.9% | Global, highest in North America and EU | Medium term (2-4 years) |

| Inconsistent ESG taxonomies across jurisdictions | -0.8% | Global, pronounced in EU, US and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute talent shortage in model-risk governance

Fifty-four percent of banks report gaps in quantitative validation skills, delaying model releases and inflating compliance costs. Salary inflation is steepest for specialists who combine statistics, regulatory insight, and AI competence. Institutions are adopting automated validation toolkits that replay production data and issue governance alerts, but supervisors still require human sign-off. Vendors that bundle workflow, documentation, and auto-testing capabilities mitigate the constraint yet cannot fully replace scarce expertise.

Rising SaaS subscription fatigue among mid-tiers

Mid-tier banks juggle dozens of niche tools, creating integration overhead and licensing creep. Many are rationalizing stacks in favor of unified risk analytics market platforms that provide modular capabilities under usage-based pricing. Hybrid-cloud architectures and container orchestration lower exit barriers, alleviating vendor-lock concerns. Providers able to showcase clear payback periods through proof-of-value pilots see quicker renewals despite budget caution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services adoption accelerates as institutions seek specialist expertise

Market share data show Solutions at 64.20% in 2025, yet the Services arm is expanding faster at 11.62% CAGR. The risk analytics market size tied to consulting, implementation, and managed operations grows as banks confront AI governance, climate stress testing, and quantum-risk modeling. Service firms help integrate advanced engines with legacy cores while aligning outputs to jurisdictional templates. In parallel, core software evolves toward low-code configurability, natural language front-ends, and quantum-resistant libraries.

Ongoing regulatory change keeps customers reliant on external specialists for model inventory curation, documentation, and validation. Managed services covering data quality, scenario libraries, and real-time monitoring reduce overhead for mid-tier players. As a result, spending tilts toward recurring service contracts even where perpetual licenses remain in place. Vendors that fuse software upgrades with outcome-based service commitments guard renewals and upsell opportunities.

By Deployment: Cloud uptake rises despite on-premises prevalence

On-premises systems retain 66.95% share in 2025 as institutions guard sensitive data against extraterritorial access. Yet a 11.92% CAGR for cloud indicates decisive migration momentum, raising the risk analytics market value delivered via SaaS and platform-as-a-service models. Cloud deployments support elastic compute bursts for intraday stress testing, real-time fraud scoring, and high-frequency market-risk recalculations. Providers of sovereign-cloud zones ease data-residency objections in Europe, the Middle East, and Asia.

Hybrid architectures dominate transition roadmaps. Legacy credit engines remain on-premises while AI inference layers, visualization dashboards, and batch reporting shift to cloud micro-services. Clients use multi-cloud orchestrators to avoid lock-in and align workloads with latency, cost, and data-localization constraints. Solutions that embed workload-placement logic and cross-cloud cost analytics capture wallet share as institutions refine resource allocation strategies.

By Risk Type: Climate and ESG analytics record fastest advance

Credit risk still anchors 39.85% of 2025 revenue, but climate and ESG models expand at 11.12% CAGR through 2031. The risk analytics market share for climate scenarios grows as disclosure mandates require quantification of floods, wildfires, and transition shocks at obligor level. Integrated platforms overlay physical-risk maps on loan collateral and securities holdings to calculate capital charges consistent with regulator guidelines.

Vendors add transition-risk libraries that model carbon-price pathways and policy shocks, linking them to credit, market, and operational risk exposures. Institutions re-factor stress-testing suites to merge climate outcomes with macroeconomic downturns. Providers that can supply traceable climate data, transparent methodologies, and audit trails win procurement evaluations, especially in Europe where supervisors scrutinize scenario assumptions.

By Application: Cyber-risk analytics surges on digital-first operations

Fraud detection and AML captured 41.05% share in 2025 and continues to evolve toward behavioral and network-based analytics. Cyber-risk analytics however outpaces with a 10.74% CAGR as financial infrastructure digitizes and regulators impose ICT-risk standards. The risk analytics market size for cyber models expands under the Digital Operational Resilience Act that requires threat identification, penetration testing, and service-level orchestration.

Platforms ingest log data, vulnerability scans, and supply-chain intelligence to quantify residual cyber exposure in monetary terms. They connect to security orchestration tools to trigger controls when risk thresholds breach tolerance. Clients prioritize solutions that unify cyber, operational, and third-party risk within enterprise dashboards, enabling boards to compare cyber exposure with credit or liquidity risks on common scales.

By End-user Industry: Retail and e-commerce drive fraud-centric innovation

The BFSI vertical held 36.45% of revenue in 2025 as banks continue to invest in compliance, stress testing, and anti-fraud analytics. Retail and e-commerce, posting a 10.55% CAGR, emerges as a hotbed of real-time fraud and chargeback management. The risk analytics market size for merchants increases as instant payments and buy-now-pay-later plans raise exposure to synthetic identities and refund abuse. Visa research shows over 80% of merchants boosting instant-payment acceptance, escalating fraud management needs.

Online sellers adopt plug-and-play AI fraud engines that flag anomalies at checkout, score customers on risk tiers, and feed results into embedded finance offerings. Telecom and tech providers also increase spend to safeguard digital wallets and embedded lending channels. Vendors supplying verticalized risk content and out-of-the-box connectors shorten time-to-value and penetrate non-financial sectors faster.

By Organisation Size: SMEs close capability gaps via platform democratization

Large enterprises maintain 68.75% share under complex regulatory obligations and sophisticated portfolios. The highest 12.05% CAGR resides in SMEs that leverage subscription models to gain enterprise-grade analytics without heavy CapEx. Cloud service providers and fintech aggregators bundle scoring, fraud, and compliance modules into pay-as-you-grow packages. The risk analytics market democratizes as SME adoption spreads to micro-lenders, regional insurers, and mid-sized retailers.

Ease of integration and outcome-based pricing accelerate SME uptake. Vendors that automate data onboarding, offer pre-trained models, and supply sandbox testing environments reduce implementation cycles from months to weeks. Partner ecosystems distribute these offerings through accounting platforms and vertical SaaS marketplaces, widening reach while containing customer-acquisition costs.

Geography Analysis

North America held 38.15% of revenue in 2025, underpinned by strict supervisory regimes and early hyperscale-cloud adoption. The Federal Reserve’s climate guidance and Basel III endgame rules sustain spending on capital optimization, stress testing, and data lineage solutions. U.S. institutions also pilot quantum-resistant encryption to future-proof payment rails, supported by IBM’s multi-billion dollar quantum roadmap.

Europe commands significant share and shapes regulatory templates worldwide. Implementation of the Digital Operational Resilience Act in 2025 obliges banks to integrate ICT-risk analytics with traditional financial-risk metrics. The bloc’s leadership on ESG rules propels climate-scenario spending, while BCBS 239 compliance pushes real-time data aggregation investments. Fragmented member-state rules raise demand for platforms that map multiple reporting schemas onto consistent data models.

Asia-Pacific is the fastest-growing region at 11.23% CAGR. India’s Unified Payments Interface processes billions of monthly transfers, heightening real-time fraud needs. China deepens supply-chain finance analytics and readies digital currency risk frameworks. Southeast Asian markets accelerate credit-scoring for first-time borrowers using alternative data. Regulators adopt sandbox schemes that speed vendor approvals, fuelling rapid deployment of scalable cloud offerings adapted to local data-localization norms.

Regulatory Landscape

Regulation is tightening around how enterprises govern, document, and disclose risk, shifting risk analytics from periodic reporting toward continuous controls and auditable model operations. In the United States, the SEC cybersecurity disclosure framework (Item 106 under 17 CFR 229.106) requires registrants to describe processes for assessing and managing material cybersecurity risks, which increases demand for platforms that can evidence controls, decisions, and outcomes across enterprise workflows.

In Europe, the EU AI Act (Regulation (EU) 2024/1689) introduces lifecycle-based risk management requirements for high-risk AI systems, including an Article 9 risk management system that must be operational ahead of the August 2, 2026 enforcement milestone. Supervisory expectations are also getting more specific around AI governance and third-party risk, as reflected in IOSCO toolkits for AI supervision in capital markets and national guidance such as BaFin materials on ICT risks when using AI. This reinforces the need for explainability, audit trails, and technically mappable compliance documentation.

Value Chain Analysis

The value chain starts with data inputs and risk content, including internal enterprise data (transactions, customer behavior, operational logs), external intelligence (threat feeds, geospatial and climate layers, regulatory taxonomies), and reference models used for stress testing, fraud, and portfolio risk. Platform vendors then transform these inputs through data management hubs, streaming analytics, scenario engines, dashboards, and model-risk governance tooling, with delivery across on-premises, hybrid, or cloud deployments. System integrators and consulting firms operationalize the technology through implementation, model validation, process redesign, and managed operations, which is especially relevant for mid-tier organizations facing constraints in quantitative validation and governance.

Downstream, enterprises embed risk scores and alerts into business workflows such as payments, lending, trading, procurement, and third-party risk management (TPRM). Evidence from 2026 TPRM-focused industry studies and supply-chain resilience research points to a shift from point-in-time supplier assessments to continuous monitoring across both software and physical supply chains. This increases the importance of connectors to ERP, GRC, and security stacks, while bottlenecks concentrate around data quality and lineage, integration across fragmented toolsets, and access to timely external intelligence. As a result, buyers are prioritizing unified risk data fabrics and interoperable APIs that reduce vendor lock-in and improve auditability.

Competitive Landscape

The risk analytics market features moderate consolidation. Incumbents such as SAS, IBM, Oracle, and SAP leverage broad suites that align with multi-risk governance and regulatory mapping. Specialists like FICO, Moody’s Analytics, and NICE Actimize cultivate deep domain models for credit, climate, or financial crime. Acquisition momentum is strong as vendors seek differentiated data sources and AI engines. Mastercard’s purchase of Recorded Future adds threat intelligence to its fraud shield services.

Cloud hyperscalers intensify competition by embedding analytics APIs into infrastructure layers. Google, Microsoft, and Amazon market low-latency fraud detection, auto-scaling stress-test grids, and managed model-ops. Partnerships between software vendors and cloud providers ensure regulatory certifications and sovereign-cloud options that reassure supervisors. Start-ups focus on quantum-safe algorithms, geospatial climate metrics, and synthetic-data validation tools, targeting niches where incumbents are slower to innovate.

Real-time processing capability is a decisive differentiator. Vendors demonstrate millisecond decision times on peak loads while preserving explainability and audit trails. Offerings that couple streaming analytics with line-of-business dashboards attract buyers who need actionable insights rather than historical reports. Competitive advantage increasingly depends on ecosystem openness, model-risk governance tooling, and transparent licensing that alleviates subscription fatigue.

Risk Analytics Industry Leaders

IBM Corporation

SAP SE

SAS Institute Inc.

Oracle Corporation

Accenture PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is converting new governance and disclosure duties into machine-readable reporting and evidence trails. The SEC has advanced structured cybersecurity disclosure mechanics through its Cybersecurity Disclosure (CYD) taxonomy guidance in March 2026, which increases demand for risk analytics systems that can map controls, incidents, and governance processes into consistent, taggable datasets across business units. Vendors and service providers that package data lineage, policy-to-control mapping, and reporting templates alongside analytics engines can shorten compliance cycles while reducing manual documentation effort.

Another opportunity lies in bringing AI governance, cyber-risk analytics, and third-party risk into a single operating layer as enterprises deploy more AI-enabled decisioning and manage increasingly complex supplier ecosystems. Product direction from large vendors reflects this convergence, for example IBM launching software in June 2025 to unify AI security and governance (combining watsonx.governance with Guardium AI Security and aligning to frameworks such as the EU AI Act and ISO 42001), and SAP showcasing agent-based risk workflows for credit risk on SAP BTP in 2026. With on-premises still representing 66.95% of deployments in 2025, hybrid architectures that keep sensitive datasets local while pushing elastic inference, scenario compute, and cross-jurisdiction reporting to cloud services remain a practical adoption path, particularly where sovereign-cloud options and audit-ready model governance reduce regulator and board concerns.

Recent Industry Developments

- July 2026: IBM and Red Hat expanded Lightwell with new commercial offerings positioned as trust infrastructure for the AI era. The move supports enterprise-grade governance and security capabilities that adjacent risk analytics workflows increasingly depend on when deploying AI at scale across regulated operations.

- October 2025: SAP Fioneer partnered with Asset Impact to integrate forward-looking, asset-level climate transition data into core risk and credit systems. This strengthens climate and ESG risk analytics by embedding transition-risk datasets into reporting pipelines aligned with PCAF, CSRD, and evolving supervisory expectations.

- December 2024: Mastercard closed its USD 2.65 billion acquisition of Recorded Future, bringing threat intelligence deeper into its fraud prevention portfolio. The combination tightens the link between cyber-risk signals and real-time fraud analytics, increasing competitive pressure on risk platforms to unify security telemetry with financial crime decisioning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers software and related services used to identify, measure, monitor, and report risk using analytics, models, and scoring across business workflows. It includes tools used for financial, operational, compliance, cyber, and climate risk use cases.

Scope exclusions: We exclude generic business intelligence suites and stand-alone actuarial modeling tools that are not sold as risk analytics platforms.

Segmentation Overview

- By Component

- Solution

- Risk-calculation engines

- Risk reporting and dashboards

- ETL / Data-management hubs

- Services

- Consulting

- Integration and Implementation

- Managed / BPO Services

- Solution

- By Deployment

- On-premises

- Cloud

- By Risk Type

- Credit

- Operational

- Liquidity

- Compliance / RegTech

- Climate and ESG

- By Application

- Fraud Detection and AML

- Stress Testing and Scenario-Analysis

- Model-Risk Management

- Cyber-Risk Analytics

- Supply-chain / Third-party Risk

- By End-user Industry

- BFSI

- Healthcare and Life-sciences

- Retail and E-commerce

- Energy and Utilities

- IT and Telecom

- Others

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public references that help us pin down the demand pool and the regulatory push behind spending, then moved into what vendors say they are shipping and monetizing. Sources included SEC filings and annual reports, US NIST publications for risk and security guidance, ISO standards documents for risk management language and controls mapping, and IMF and World Bank macro series, along with OECD and national statistical offices for industry output and employment context.

We also reviewed association and regulator sites (such as banking and insurance supervisory guidance) and reputed press coverage, then used product documentation to understand packaging shifts from on-premise licenses to subscriptions. For cross-checks on company revenue splits, M&A notes, and patent activity, we referenced paid database subscriptions for company financial intelligence, news and financials, and patent databases. These desk sources are not exhaustive, and many other public and subscription references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test what gets counted as risk analytics versus adjacent governance or reporting tools, and to validate pricing and adoption patterns by buyer type. We spoke with a mix of solution providers, system integrators, and end users, including risk, compliance, and security teams across APAC, EMEA, and the Americas, which helped us confirm assumptions that were unclear in desk findings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 18% | APAC: 40% |

| Mid tier: 41% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 21% | Managers: 42% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction, where enterprise risk and compliance spending pools were allocated into analytics-specific use cases using adoption indicators gathered from desk sources and then refined through interview feedback. We then corroborated the totals with selective bottom-up approximations, such as sampled vendor revenue splits, service attach rates, and a price times volume sense-check for subscription users, before finalizing the numbers.

Inputs used in the model included cloud versus on-premise mix shifts, average contract value ranges by buyer size, services-to-software ratios for implementation and managed support, regulated-industry intensity (especially BFSI and insurance), and incident and compliance pressure signals that typically pull forward renewals and upgrades. For forecasting, we relied on scenario analysis supported by trend lines from recent adoption and pricing movement, then aligned scenario weights with what experts expect on budget growth, migration pace, and procurement cycles. Where bottom-up revenue signals were incomplete, gaps were handled through conservative normalization using comparable peer splits and region-level demand indicators, then rechecked in follow-up calls.

Data Validation & Update Cycle

Results were triangulated across multiple lenses, including vendor-side monetization signals, buyer-side adoption feedback, and independent indicators like cloud migration pace and regulated-industry spend direction. When outputs showed unusual jumps by year or region, we traced the drivers back to one or two assumptions, then revisited and adjusted them only after additional desk checks or re-contacts.

Before sign-off, the model and written logic go through multi-step analyst reviews so that scope, math, and narrative remain aligned. Reports are refreshed annually, with interim updates when material events occur, such as major regulation changes or large acquisitions that alter market structure. Right before delivery, a final pass is done to ensure the latest public updates are reflected in the numbers and assumptions.

Mordor Intelligence's Risk Analytics Market Size Versus Other Published Estimates

Published market sizes for risk analytics can look far apart even when they use the same label, because the counted products and services are not always the same. Differences also come from how quickly cloud subscription pricing is updated, how services are treated, and whether adjacent categories are blended into the total.

Generic business intelligence suites sit outside Mordor Intelligence's scope for this market, which can reduce totals versus studies that bundle broad analytics platforms together with risk-specific tools. Gaps also show up when some publishers apply aggressive subscription uplift assumptions, include wider governance or compliance platforms, or convert currencies using different timing, which changes the USD view for multi-region revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 42.92 B (2025) | |

| Industry Research Publisher A | USD 44.67 B (2024) | Uses a different base year and may include a broader component mix across software and services without clearly separating risk analytics platforms from adjacent enterprise analytics and governance tooling, which can lift the stated total. |

| Industry Research Publisher B | USD 48.15 B (2024) | Applies a 2024 base with a wider risk-type and vertical framing and does not specify exclusions for adjacent tool categories, which can expand what gets counted along with differences in pricing refresh timing for subscription deals. |

The comparison shows that the spread is mostly explained by scope edges and the timing of the stated base year, rather than by a disagreement on core demand drivers. By keeping inclusions tied to risk analytics platforms and validating key pricing and attach-rate assumptions through interviews, the estimate stays traceable to repeatable inputs that can be rechecked as the market evolves.

Key Questions Answered in the Report

What is the current risk analytics market size and growth outlook?

The risk analytics market is valued at USD 47.26 billion in 2026 and is forecast to reach USD 76.49 billion by 2031, posting a 10.11% CAGR.

Which segment contributes the largest risk analytics market share?

Solutions retain leadership at 64.20% of 2025 revenue, reflecting continued investment in core engines and dashboards.

Why are services growing faster than software in risk analytics?

Institutions need specialized expertise for AI model governance, climate-risk methodology, and multi-jurisdiction compliance, driving an 11.62% CAGR for services to 2031.

How fast is cloud adoption advancing in risk analytics?

Cloud deployments are expanding at 11.92% CAGR as hybrid architectures deliver elastic compute and lower ownership costs while meeting data-residency rules.

Which geographic region will add the most new revenue?

Asia-Pacific leads growth at 11.23% CAGR to 2031 owing to digital-payment proliferation and evolving regulatory frameworks that favor cloud-native analytics.

What technologies define competitive advantage in the risk analytics industry?

Real-time AI engines, quantum-resistant algorithms, sovereign-cloud availability, and automated model-risk governance tools differentiate leading platforms.

Page last updated on: