Underwater Camera Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

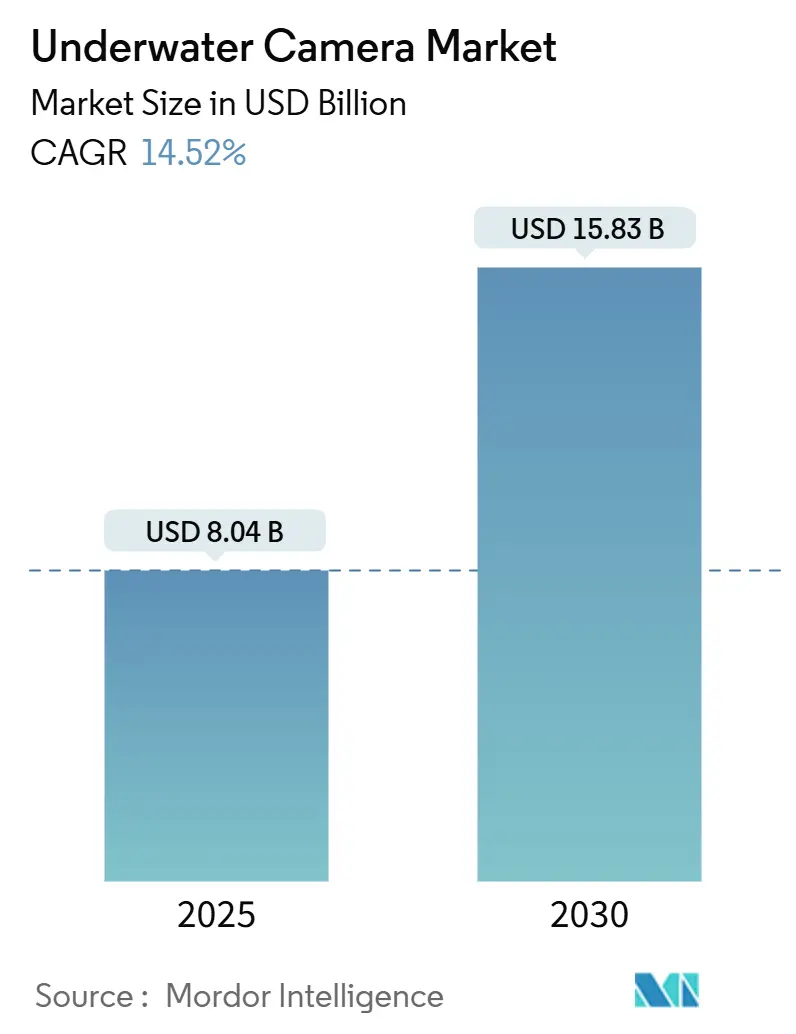

| Market Size (2025) | USD 8.04 Billion |

| Market Size (2030) | USD 15.83 Billion |

| Growth Rate (2025 - 2030) | 14.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Underwater Camera Market Analysis by Mordor Intelligence

The Underwater Camera Market size is estimated at USD 8.04 billion in 2025, and is expected to reach USD 15.83 billion by 2030, at a CAGR of 14.52% during the forecast period (2025-2030).

Growth is propelled by three reinforcing dynamics: consumer enthusiasm for adventure-sports content on social platforms, industrial demand for real-time aquaculture monitoring, and steady sensor miniaturization that delivers professional image quality in compact form factors. Asia Pacific delivers the largest revenue contribution and the quickest regional expansion, buoyed by dense marine-tourism corridors and intensive fish-farming activity. Technological leaps such as BSI-CMOS sensors and AI-enabled color correction reduce traditional barriers tied to illumination, post-processing, and operator skill, widening participation across expertise levels. Meanwhile, online retail ecosystems, amplified by niche underwater photography communities, shorten discovery-to-purchase cycles and allow manufacturers to control margins and brand narrative directly. Supply-chain strains around specialty optical glass and germanium illustrate, however, that component bottlenecks can temper production agility even for market leaders.

Key Report Takeaways

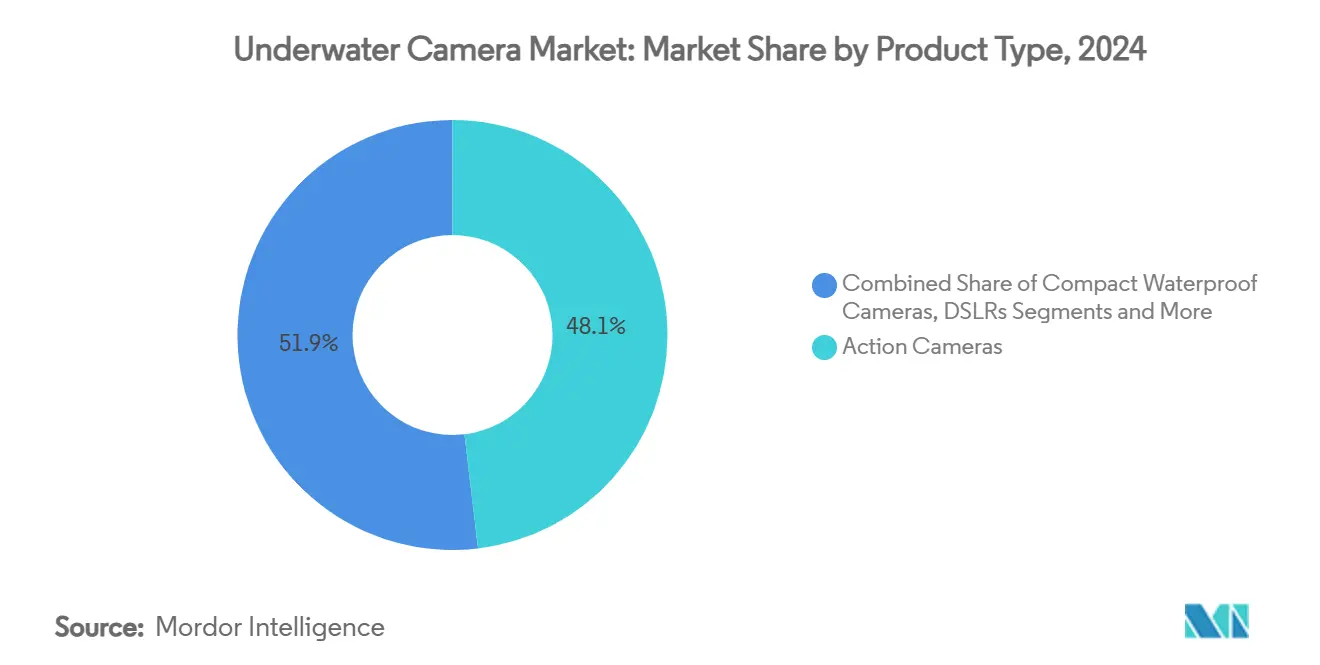

- By product type, action cameras captured 48.1% of the underwater camera market share in 2024, while industrial/ROV-integrated cameras are advancing at a 14.8% CAGR through 2030.

- By application, recreational snorkeling and diving accounted for 32.3% of the underwater camera market size in 2024, whereas fishing and aquaculture monitoring is projected to expand at a 15.6% CAGR between 2025 and 2030.

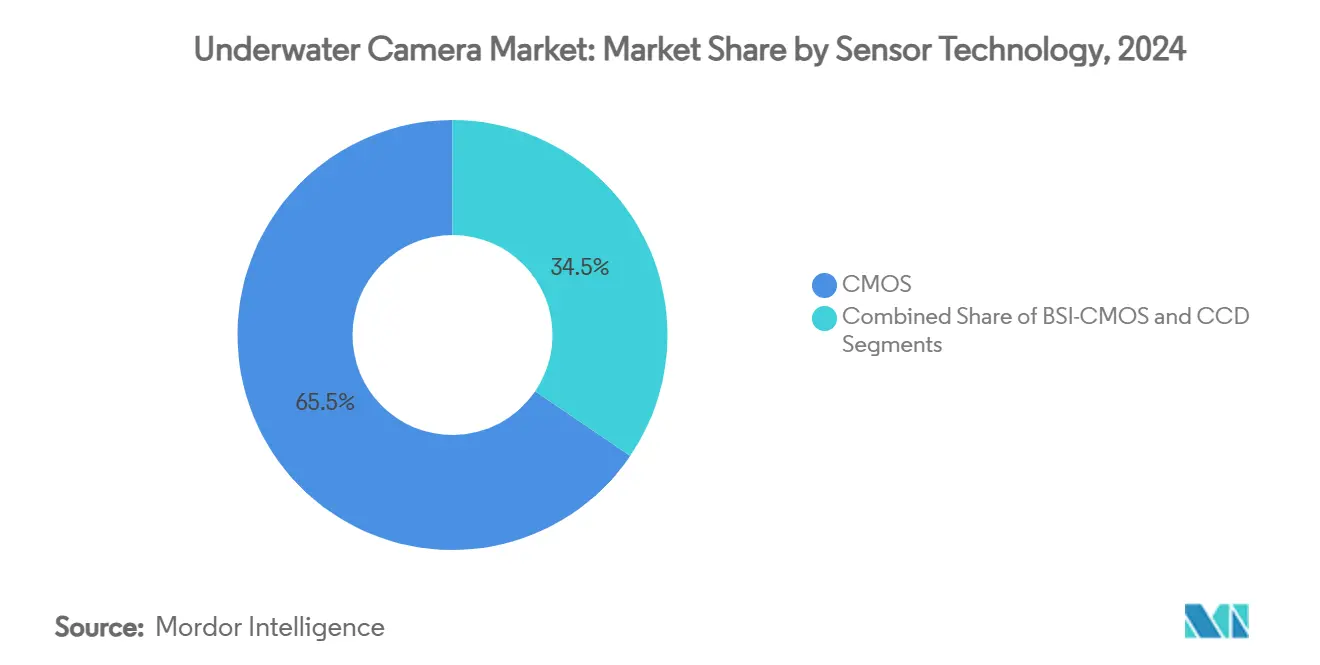

- By sensor technology, CMOS held 65.5% of the worldwide revenue in 2024, and BSI-CMOS leads growth at a 15.1% CAGR over the outlook period.

- By sales channel, online retail commanded 54.7% of global revenues in 2024 and remains the fastest-growing route at a 15.4% CAGR to 2030.

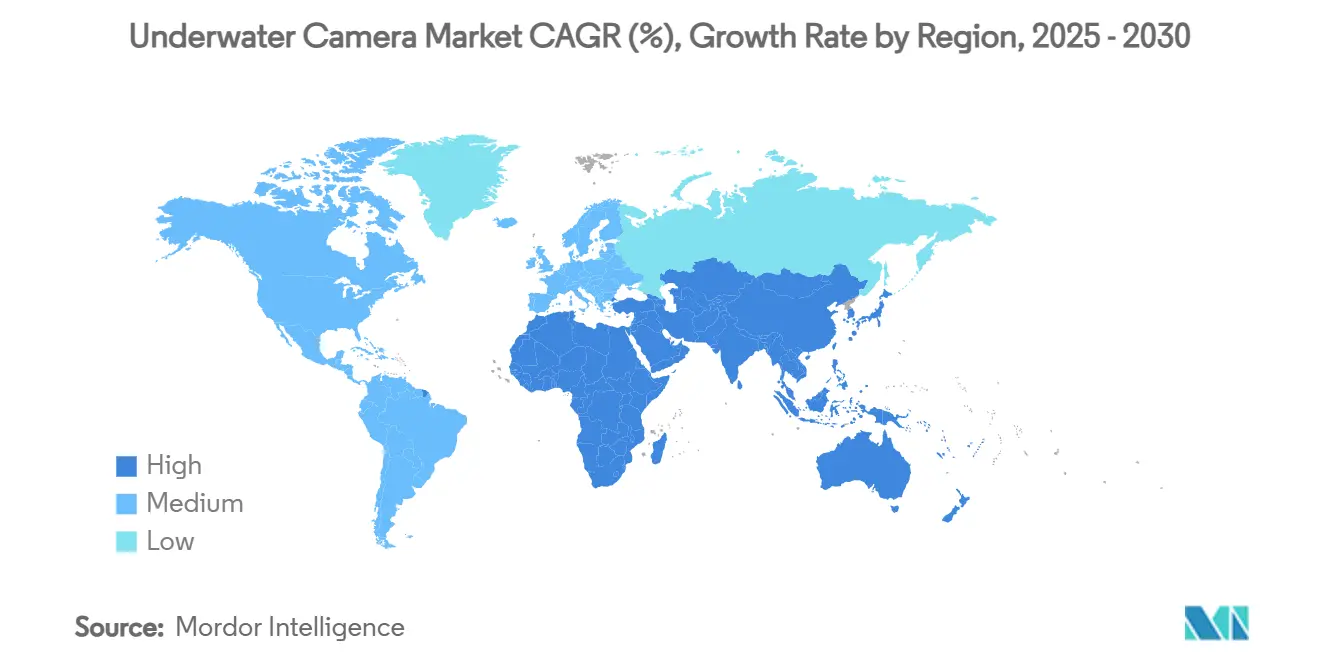

- By geography, Asia Pacific contributed 41.9% of 2024 turnover and is forecast to accelerate at a 14.9% CAGR through 2030.

Global Underwater Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social-media-fuelled adventure-sports content boom | +2.8% | North America, Europe | Short term (≤ 2 years) |

| Rising marine tourism and recreational diving activity | +3.2% | Asia Pacific, MEA, South America | Medium term (2-4 years) |

| Rapid sensor miniaturization and cost decline | +2.1% | Global | Long term (≥ 4 years) |

| AI-based in-camera color correction and metadata tagging | +1.9% | North America, EU, Asia Pacific | Medium term (2-4 years) |

| Precision-aquaculture demand for real-time stock monitoring | +2.4% | Asia Pacific, Nordics, Chile | Long term (≥ 4 years) |

| Growing demand for 360°/VR underwater content experiences | +1.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Social-media-fuelled Adventure-sports Content Boom

Widespread posting of underwater clips on Instagram, TikTok, and YouTube has converted dive footage from a hobbyist niche into a mainstream storytelling format. Content creators increasingly view cameras as core gear alongside fins and regulators, and they demand zero-overheat performance for hour-long 4K sessions. The GoPro HERO 13’s revised thermal layout and filter-stack flexibility exemplify how vendors now treat social media filmmakers as a professional tier. European water-sports tourism is rising at 16.9% annually, creating a broader base of potential buyers who expect broadcast-grade footage from pocket-sized devices. [1]CBI, “The European Market Potential for Water Sports Tourism,” cbi.euSponsorship income further sustains replacement cycles as creators chase incremental image-quality gains. Collectively, these factors give the underwater camera market an immediate sales pulse that is unlikely to fade over the next two seasons.

Rising Marine Tourism and Recreational Diving Activity

International dive resorts report visitor counts surpassing 2019 peaks as border restrictions ease. United States scuba participation rebounded to 3 million people in 2023, revealing a sizeable equipment refresh opportunity. Coastal governments from Indonesia to Egypt invest in artificial reefs and dedicated snorkeling trails, which raise first-time diver curiosity and push entry-level camera bundles. Nordic Blue Parks initiatives showcase underwater heritage trails that blend conservation with tourism, driving interest in visual documentation of submerged cultural assets.[2]Nordic Council of Ministers, “Nordic Blue Parks,” norden.diva-portal.org Demand patterns thus favor rugged designs that can transition from shallow snorkeling to advanced wreck exploration without requiring multiple systems.

Rapid Sensor Miniaturization and Cost Decline

Backside-illuminated CMOS wafers now deliver frame rates beyond 76,000 fps while maintaining high quantum efficiency. Manufacturers consequently embed professional sensors into houseless action cams, slashing the acquisition cost that previously deterred casual users. Compact modules prove especially beneficial for ROVs, where every gram saved extends mission endurance. Yet, Hurricane-related downtime at critical quartz mines reinforces how a single upstream material can constrain final unit availability, nudging firms to develop multi-sourcing strategies. Over the long term, cost/performance curves are still expected to drift favorably, enabling sub-USD 300 units with features once reserved for cinema rigs.

AI-based In-camera Color-correction and Metadata Tagging

Algorithms that compensate in real time for water’s color absorption now negate the need for labor-intensive post-processing. Canon’s EOS R5 Mark II refines autofocus using machine learning to maintain focus even when subjects dart behind coral heads. Sony’s global-shutter architecture synchronizes high-power strobes at previously unattainable speeds, letting shooters balance ambient and artificial light more naturally. For researchers, automatic species recognition and depth tagging embed actionable data into each frame, streamlining analytics workflows. Such AI-centric benefits help the underwater camera market broaden appeal among teams that lack specialist editors but still require expedition-grade outputs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of professional housings and lighting | -1.8% | Global, especially emerging markets | Medium term (2-4 years) |

| Battery-heat constraints during high-resolution recording | -1.2% | Global, more acute in tropical waters | Short term (≤ 2 years) |

| Stricter filming permits in marine-protected areas | -0.9% | Biodiversity hotspots worldwide | Long term (≥ 4 years) |

| Supply-chain disruptions for specialty optical glass & chips | -2.1% | Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Professional Housings and Lighting

Full-frame mirrorless bodies demand aluminum alloy housings that can exceed USD 4,000, while dual-strobe rigs add another USD 2,000-5,000. Such totals surpass many dive travelers’ annual gear budgets, limiting professional-grade imaging adoption in countries where tourism is just maturing. Conservation projects and universities share the same budget pain despite the acute need for documentary footage. In response, manufacturers ship integrated waterproof cameras rated to 15 m that bypass housings for snorkel-depth assignments, gradually softening cost barriers without cannibalizing flagship sales.

Battery-heat Constraints During High-resolution Recording

Heat buildup forces 8K-capable cameras to throttle or shut down after minutes, frustrating scientific transects that must roll continuously. Water removes heat more effectively than air, yet sealed housings block convection, trapping processor waste energy. GoPro’s latest firmware that spreads processing loads proves incremental relief. Longer-term remedies lie in next-gen battery chemistry and ASIC-level video encoders, but until such solutions mature, filmmakers schedule forced cool-down intervals that add operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial ROVs Drive Professional Adoption

Action cameras generated the highest revenue in 2024 by seizing 48.1% of the underwater camera market, yet industrial-grade ROV cameras are pacing the segment with a 14.8% CAGR to 2030. This split underscores how consumer excitement funds volume while mission-critical inspection and survey tasks unlock premium price elasticity.

The underwater camera market size for ROV-integrated systems is expanding as offshore wind farms, oil pipelines, and harbor authorities adopt compact drones for hull inspection and environmental compliance. QYSEA’s FIFISH E-MASTER bundles AI-supported measurement and autonomous navigation in a briefcase-sized platform, signaling a design shift from standalone imagers toward turnkey robotic packages. Meanwhile, compact waterproof models such as OM SYSTEM’s Tough TG-7 cater to casual snorkelers who need ruggedness over optical extremes. Disposable single-use cameras persist in adventure resorts where equipment loss risk is high, but they occupy a shrinking revenue sliver.

By Application: Aquaculture Monitoring Accelerates Commercial Adoption

Recreational snorkeling and diving retained the largest slice of the underwater camera market size at 32.3% in 2024, yet fishing and aquaculture monitoring is accelerating fastest at 15.6% CAGR. Farming operators require 24/7 visual feeds to optimize feed cycles, spot disease and satisfy welfare auditors, turning cameras from optional sensors into core productivity levers.

Photonis’ Nocturn low-light module enables farms to monitor pens overnight without artificial illumination, reducing stress on stock while supplying continuous behavioral data. Adventure sports and vlogging remain vibrant as monetization pathways thicken, but industrial inspection of offshore turbines and subsea cables is rising as a parallel growth engine. Scientific teams capitalize on AI-embedded metadata to automate species counts, freeing field time for hypothesis-driven tasks rather than annotation.

By Sensor Technology: BSI-CMOS Advances Low-light Performance

CMOS technology dominated the underwater camera market share with 65.5% in 2024, and BSI-CMOS is expanding at a 15.1% CAGR on the strength of superior photon collection at depth. Back-illumination positions wiring behind the photodiode layer, yielding cleaner signals under the blue-green wavelengths that prevail below 10 m.

CCD remains entrenched in labs where color fidelity edges out battery life, yet CMOS cost curves and integration ease continue to erode its niche. Emerging SPAD arrays promise single-photon sensitivity for lidar-based depth mapping but await mass-market economics.[3]Sensors Journal, “SPAD Linear Detector Array for Underwater Depth Imaging,” mdpi.comFor now, vendors exploit BSI-CMOS to bring professional noise floors into sub-USD 500 bodies, expanding addressable hobbyist populations.

By Sales Channel: Online Retail Dominates Distribution Evolution

Online marketplaces secured 54.7% of global revenue in 2024 and led growth at a 15.4% CAGR, reflecting how the underwater camera market rewards direct-to-consumer outreach. Manufacturer-hosted storefronts bundle tutorials, firmware updates, and community forums that foster brand stickiness and ease of upgrade.

Physical sports-and-dive shops survive by offering hands-on demos and local water-condition advice, but their average order size tilts toward accessories. OEM/B2B contracts rise in parallel as industrial clients request integrated imaging-robotics bundles plus on-site maintenance. Hybrid models, where buyers pick specs online then collect preassembled kits in store, illustrate how channel boundaries blur in practice.

Geography Analysis

Asia Pacific commanded 41.9% of 2024 revenue and is set to grow at 14.9% CAGR, fueled by China’s manufacturing depth and Southeast Asia’s dive-tourism corridors. Domestic innovators such as India’s EyeROV offer cost-optimized inspection drones that align with regional infrastructure budgets. Expanding middle classes allocate rising discretionary income to reef excursions, while salmon, shrimp, and seaweed farms across China, Vietnam, and Indonesia scale video-centric monitoring to safeguard output.

North America presents a mature but resilient buyer base anchored by 3 million active divers in 2023 and robust demand from offshore energy and scientific institutions. Strategic deals like Kraken Robotics’ USD 17 million acquisition of 3D at Depth illustrate regional appetite for LiDAR-enhanced subsea imaging packages. Regulatory clarity around drone deployment in US ports further stimulates replacement cycles toward AI-augmented systems.

Europe capitalizes on its dual identity as a tourist magnet and environmental research hub. Water-sports tourism is heading toward USD 845.8 billion by 2032 at 16.9% CAGR, ensuring a steady pipeline of first-time camera purchasers. Nordic aquaculture farms pioneer data-rich welfare regimes, while Mediterranean dive operators refresh fleets to comply with updated safety guidelines. EU conservation funds co-finance VR documentation of submerged heritage sites, sustaining high-spec demand even outside traditional summer high seasons.

Competitive Landscape

Market structure remains moderately fragmented: GoPro, Sony, and Canon headline the consumer tier, whereas Teledyne Marine, SubC Imaging, and QYSEA address industrial niches with sealed or ROV-embedded systems. Brand differentiation pivots on low-light performance, AI automation, and thermal stability rather than megapixel races alone. Consumer incumbents defend share by upgrading firmware-level color science and integrating livestream features that appeal to vlogging communities.

Industrial consolidation is intensifying. Kraken Robotics’ purchase of 3D at Depth secures vertically integrated LiDAR plus imaging payloads, while BlueHalo’s acquisition of VideoRay folds mini-ROV expertise into a defense-oriented suite. General Oceans’ buyout of RS Aqua adds fish-tracking sensors that complement its existing subsea imaging line, signaling ecosystem plays over single-product bets. Emerging entrants leverage regional cost advantages; EyeROV in India and several Shenzhen-based OEMs scale rapidly by supplying white-label modules to Western brands.

Future rivalry will likely hinge on software ecosystems that process and monetize captured data. Nauticus Robotics positions its AUVs as multifunction nodes that gather imagery, manipulate tools and transmit analytics in one pass.[4]SEC, “Nauticus Robotics, Inc. Form 10-K,” sec.govVendors able to bundle such end-to-end value can command subscription revenue streams on top of hardware sales, tilting competitive power toward integrated platform owners.

Underwater Camera Industry Leaders

GoPro Inc.

SZ DJI Technology Co., Ltd.

Sony Corporation

SeaLife Cameras

OM Digital Solutions Corporation (Olympus)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kraken Robotics closed the USD 17 million acquisition of 3D at Depth, adding subsea LiDAR technology and more than 450 completed offshore projects to its portfolio

- November 2024: BlueHalo acquired VideoRay, strengthening its unmanned maritime division with Defender-class micro-ROVs aimed at commercial and defense customers

- November 2024: General Oceans bought UK-based RS Aqua, integrating over 40 years of sensor distribution expertise into its GBP 62 million revenue base.

- October 2024: QYSEA Technology unveiled the FIFISH E-MASTER compact ROV with AI-powered measurement and 3D seabed mapping functions, targeting offshore energy inspections.

Global Underwater Camera Market Report Scope

| Action Cameras |

| Compact Waterproof Cameras |

| DSLR and Mirrorless with Housing |

| Professional Cinema Systems |

| Industrial/ROV Integrated Cameras |

| Disposable Waterproof Cameras |

| Recreational Snorkelling and Diving |

| Adventure Sports and Vlogging |

| Professional Photo and Cinematography |

| Commercial Inspection and Maintenance |

| Fishing and Aquaculture Monitoring |

| Scientific and Environmental Research |

| Military and Security Surveillance |

| CMOS |

| BSI-CMOS |

| CCD |

| Online Retail |

| Specialty Camera Stores |

| Sports and Dive Shops |

| OEM/B2B Direct |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Action Cameras | ||

| Compact Waterproof Cameras | |||

| DSLR and Mirrorless with Housing | |||

| Professional Cinema Systems | |||

| Industrial/ROV Integrated Cameras | |||

| Disposable Waterproof Cameras | |||

| By Application | Recreational Snorkelling and Diving | ||

| Adventure Sports and Vlogging | |||

| Professional Photo and Cinematography | |||

| Commercial Inspection and Maintenance | |||

| Fishing and Aquaculture Monitoring | |||

| Scientific and Environmental Research | |||

| Military and Security Surveillance | |||

| By Sensor Technology | CMOS | ||

| BSI-CMOS | |||

| CCD | |||

| By Sales Channel | Online Retail | ||

| Specialty Camera Stores | |||

| Sports and Dive Shops | |||

| OEM/B2B Direct | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the underwater camera market?

The underwater camera market size is USD 8.04 billion in 2025 and is projected to grow rapidly through 2030.

Which region leads global demand?

Asia Pacific holds 41.9% of 2024 revenue and exhibits the fastest 14.9% CAGR on the back of vibrant dive tourism and aquaculture expansion.

What segment is growing fastest?

Industrial/ROV-integrated cameras outpace all other product classes with a 14.8% CAGR as inspection, energy and farming users invest in autonomous imaging platforms.

Why are BSI-CMOS sensors important underwater?

BSI-CMOS sensors collect more light in low-illumination blue-green environments, yielding cleaner images at depth and driving a 15.1% CAGR in the sensor-technology category.

How are online channels affecting sales?

Online retail already commands 54.7% of global turnover and is rising at 15.4% CAGR because direct-to-consumer storefronts allow faster releases, lower prices and richer tutorial content.

What restrains broader professional adoption?

High housing and lighting costs, thermal limits during extended 8K recording and sporadic shortages of specialty optics curb uptake, though integrated waterproof designs are narrowing the gap.

Page last updated on: