Plenoptic Camera Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

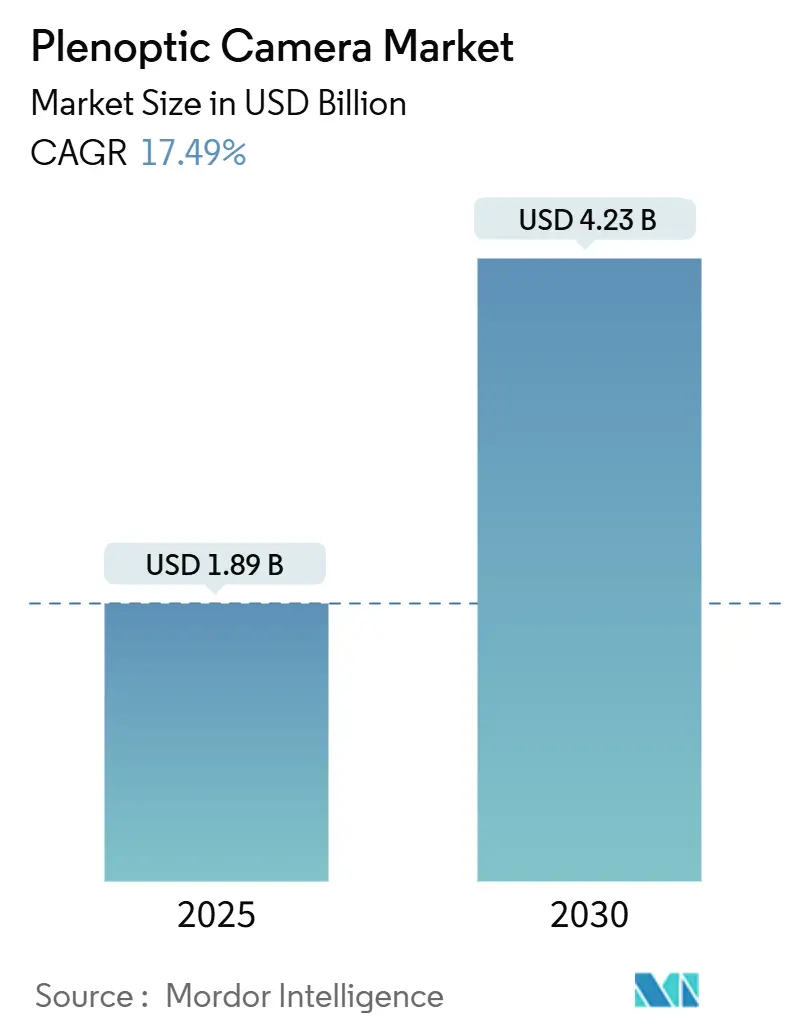

| Market Size (2025) | USD 1.89 Billion |

| Market Size (2030) | USD 4.23 Billion |

| Growth Rate (2025 - 2030) | 17.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plenoptic Camera Market Analysis by Mordor Intelligence

The plenoptic camera market size stands at USD 1.89 billion in 2025 and is projected to expand to USD 4.23 billion by 2030, advancing at a 17.49% CAGR during the forecast period. Surging demand for real-time refocusing, rapid AR/VR content growth, and the maturation of micro-lens array fabrication jointly elevate adoption across consumer, industrial, and medical domains. Defense programs in North America, fresh semiconductor capacity in Asia-Pacific, and the arrival of edge-AI image processors shorten innovation cycles, while software-defined capture kits nurture a developer ecosystem that lowers entry barriers. Unit-level cost declines, achieved through high-volume nano-imprint lithography, further democratize access; meanwhile, professional creators favor medium-format sensors that preserve detail without compromising depth cues. The rising need for dynamic depth mapping in robotics, coupled with privacy-preserving volumetric analytics in healthcare, widens the total addressable opportunity for the light field camera market.

Key Report Takeaways

- By product type, standalone plenoptic cameras led with 47.2% revenue share in 2024; software-defined kits are forecast to expand at a 20.9% CAGR to 2030.

- By application, AR/VR and metaverse creation commanded a 32.2% share of the plenoptic camera market size in 2024, while medical imaging records the highest projected CAGR at 21.5% through 2030.

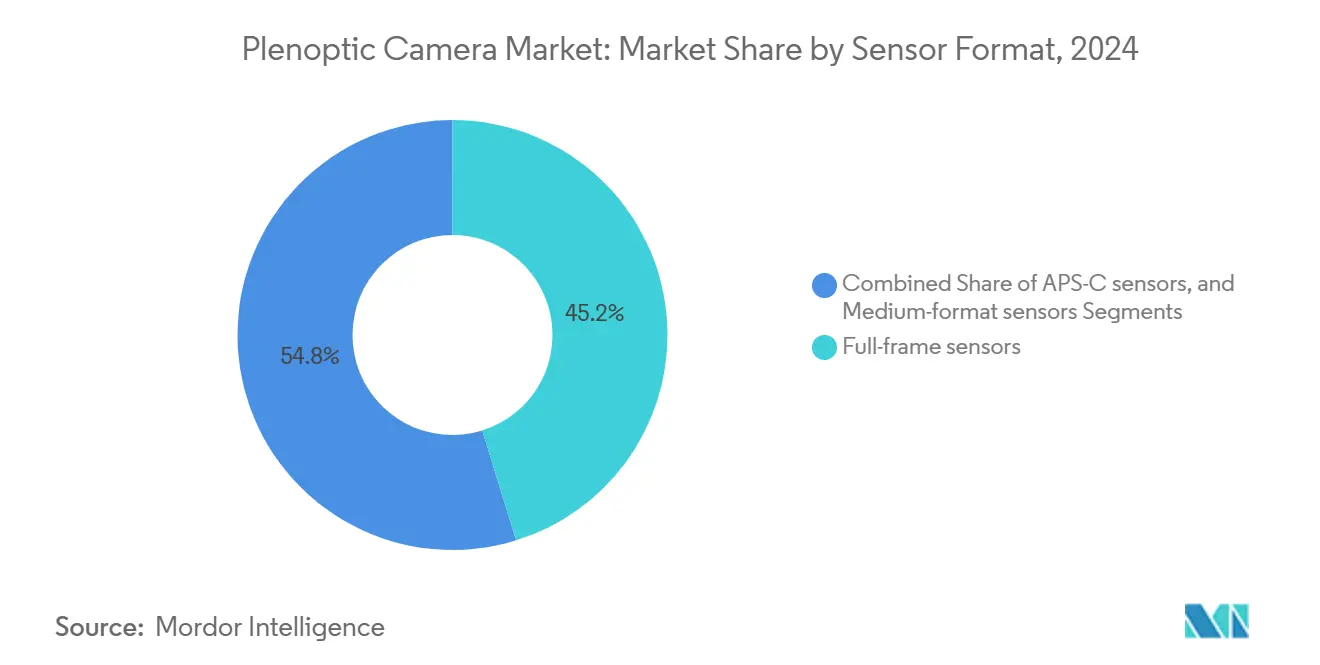

- By sensor format, full-frame sensors accounted for 45.2% of the plenoptic camera market share in 2024, and medium-format sensors are advancing at an 18.9% CAGR through 2030.

- By end-user industry, media and entertainment retained a 34.2% share in 2024; healthcare revenue is set to rise at a 20.2% CAGR between 2025 and 2030.

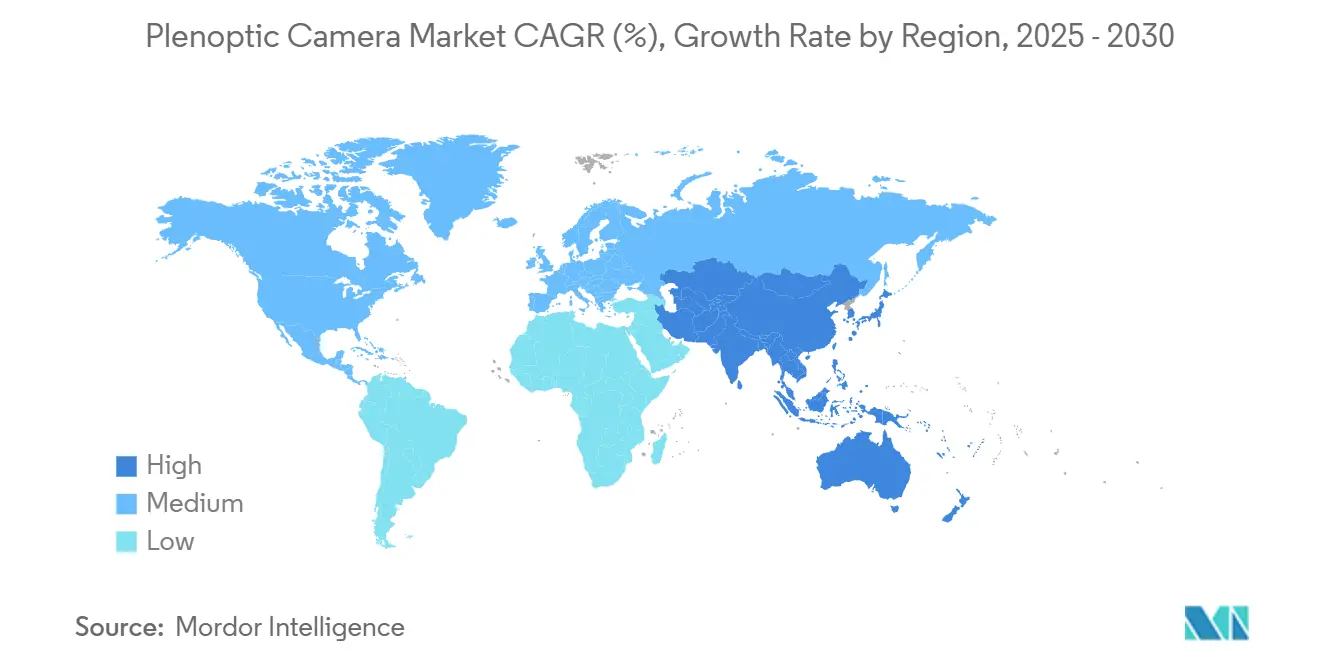

- By geography, North America contributed 38.7% of 2024 revenue, whereas Asia-Pacific is projected to post an 18.7% CAGR, the fastest among all regions.

Global Plenoptic Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for post-capture refocusing | +3.2% | Global, with a concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid penetration in AR/VR and 3-D workflows | +4.1% | North America and the EU leading, Asia-Pacific accelerating | Short term (≤ 2 years) |

| Advances in micro-lens array manufacturing | +2.8% | Asia-Pacific manufacturing hubs, global impact | Long term (≥ 4 years) |

| Integration into robotic vision systems | +2.3% | Germany, Japan, China, the US Midwest | Medium term (2-4 years) |

| Adoption in ophthalmic diagnostic devices | +1.9% | Developed healthcare markets | Long term (≥ 4 years) |

| Edge-AI processors for real-time video | +3.7% | Silicon Valley, Shenzhen, Tel Aviv | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Post-Capture Refocusing in Consumer Imaging

Consumers increasingly expect creative control after the shutter press. Post-capture refocusing lets users shift focus planes in portraits or action scenes without retakes, reducing missed shots and editing time. Canon’s RF-S7.8 mm F4 STM Dual lens adapts light-field principles to a mainstream mirrorless system, illustrating how legacy brands bridge conventional optics with computational depth capture.[1]Canon Inc., “RF-S7.8 mm F4 STM Dual Lens Announcement,” canon.com The feature’s appeal widens the addressable base from enthusiasts to casual smartphone shooters once cost thresholds fall. Developers see monetization in app-based refocus tools, further driving feature standardization across mid-tier devices.

Rapid Penetration in AR/VR and 3-D Imaging Workflows

Immersive content hinges on accurate per-pixel depth and multi-view parallax. Interactive training, location-based entertainment, and virtual production pipelines therefore prioritize plenoptic capture. Holographic headset prototypes demonstrated by NVIDIA combine light-field imagery with eye-tracked foveated rendering to yield lighter form factors without sacrificing realism. These advances shorten production timelines and reduce post-render workloads, anchoring light-field rigs as the preferred on-set cameras for volumetric stages.

Advances in Micro-Lens Array Manufacturing Lowering Costs

Yield improvements in nano-imprint lithography elevate wafer-scale uniformity while trimming defect densities, enabling 25% cost reductions versus projection lithography. NSG Group’s hybrid glass-polymer substrates withstand 300 °C processing yet retain lenslet fidelity, unlocking eight-inch panel production. Such scale economies allow OEMs to embed micro-lens arrays into entry-level devices, accelerating volumes that lower costs further and spur mass-market acceptance.

Integration into Robotic Vision Systems for Dynamic Depth Mapping

Robots operating in unstructured settings require dense, low-latency depth maps. Intrinsic’s plenoptic sensor fuses RGB, infrared, and polarization data to build point clouds that remain accurate under variable lighting.[2]Intrinsic, “AI-Enabled 3-D Vision for Robotics,” intrinsic.ai Automotive and warehouse robots adopting similar architectures eliminate spinning LiDAR units, trimming the bill of materials and maintenance. Rich depth semantics improve grasp success rates, reduce cycle times, and support safer human-robot collaboration, favorably influencing procurement decisions in industrial automation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit price versus conventional systems | -2.4% | Price-sensitive emerging economies | Medium term (2-4 years) |

| Spatial-angular resolution trade-off | -1.8% | Professional imaging markets globally | Short term (≤ 2 years) |

| Lack of an open-source software ecosystem | -1.3% | Developer communities worldwide | Long term (≥ 4 years) |

| Regulatory uncertainty on volumetric privacy | -0.9% | EU (GDPR), California (CCPA), expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit Price Versus Conventional Camera Systems

Precision optics, bespoke sensors, and multi-axis calibration inflate the bill-of-materials, keeping average selling prices well above traditional DSLRs. Although economies of scale and software-defined kits narrow the gap, initial capital still deters adoption in budget-constrained segments. Entry-level users often favor computational bokeh on smartphones, delaying migration until price premiums drop below perceived value thresholds.

Spatial-Angular Resolution Trade-Off Limiting Image Quality

Allocating finite sensor pixels between spatial fidelity and angular sampling inherently reduces per-view resolution. Critical applications such as product macro-photography or defect inspection thus hesitate to replace high-megapixel RGB cameras. Adaptive super-resolution and event-based microsaccade techniques from academic labs raise effective clarity, yet a fundamental ceiling persists until new sensor architectures emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Programmable Kits Reshape Adoption Pathways

Software-defined capture kits contribute the fastest 20.9% CAGR by 2030 as developers leverage CPU-GPU pipelines to emulate plenoptic arrays on commodity sensors. The plenoptic camera market size for standalone plenoptic cameras remains significant, reflecting entrenched demand among studios and defense integrators.

Traditional units keep a 47.2% share by harnessing mature optics and turn-key workflows, particularly in environments where plug-and-play reliability outweighs customization. Modular add-on lens assemblies provide an intermediary step, letting creative professionals retrofit existing bodies without abandoning native glass. Collectively, the tri-modal portfolio broadens channel coverage and hedges vendor risk against architectural shifts.

By Application: Medical Imaging Surges Ahead of AR/VR Entrenchment

AR/VR retains 32.2% of 2024 revenue as studios, game publishers, and training providers scale volumetric pipelines. Nevertheless, medical and life-science use cases exhibit the highest 21.5% CAGR, propelling the light field camera market.

Surgeons exploit intraoperative depth cues to delineate vascular structures, while cytopathology platforms speed large-area scans with micro-camera arrays. Consumer photo-video niches gain convenience through tap-to-refocus outputs, and industrial inspection benefits from sub-millimeter depth accuracy that outperforms stereo pairs under specular glare. Diversified use cases mitigate cyclicality tied to entertainment spending.

By Sensor Format: Growing Preference for Medium-Format Resolution

Full-frame designs held 45.2% revenue in 2024, appealing to cinematographers requiring shallow depth of field for artistic control. Medium-format shipments grow at an 18.9% CAGR as price declines make 53 mm-class sensors attainable for commercial studios seeking billboard-grade detail, expanding the plenoptic camera market share for premium tiers.

APS-C maintains a pragmatic niche, balancing body weight with pixel density for field robotics and drone mapping. Meta-optic stacks that replace thick glass with nanophotonic layers shrink flange distances and facilitate larger sensors in compact bodies.

By End-User Industry: Healthcare Accelerates, Media Holds Pole Position

Media and Entertainment preserved a 34.2% share on the back of streaming original content and live XR events. Yet hospitals, research institutes, and device OEMs push healthcare toward a 20.2% CAGR, elevating the light field camera market.

Smartglasses using multi-focus projection improve reading speeds for macular degeneration patients, showcasing therapeutic dividends. Manufacturing pursues error-free assembly, while defense agencies deploy plenoptic sensors in contested environments for passive ranging under electronic warfare constraints.

Geography Analysis

North America contributed 38.7% of 2024 revenue, anchored by the U.S. Department of Defense’s USD 100 million photonics program that seeds dual-use camera innovations. Silicon Valley’s chiplets and Israel’s vision IP cores accelerate edge inference, ensuring low-latency volumetric pipelines suitable for battlefield and studio alike. Canada’s optics clusters in Ontario supply precision glass, while Mexico’s maquiladoras assemble modules for regional consumption.

Asia-Pacific approaches an 18.7% CAGR through 2030, the highest globally. China’s micro-lens array foundries and Japan’s energy-efficient EUV steppers drive component self-sufficiency.[3]Okinawa Institute of Science and Technology, “Energy-Efficient EUV Lithography,” oist.jp India’s smart-manufacturing incentives lure OEMs to relocate assembly, and Australia pilots plenoptic surveillance along critical infrastructure corridors. Regional policy support for 3-D displays in automotive cockpits further catalyzes demand, widening the light field camera market.

Europe posts steady expansion driven by Germany’s Industry 4.0 upgrades and France’s aerospace imaging programs. GDPR compliance costs initially slowed public-sector deployment, yet harmonized privacy-by-design frameworks now expedite procurement. Nordic research labs explore light-field-enabled environmental modeling, positioning the continent as a testbed for sustainable optics. Eastern European hubs contribute algorithm talent that integrates into open-source SDKs, filling ecosystem gaps.

Competitive Landscape

The market remains moderately fragmented: the top five vendors control a majority of global receipts, leaving space for specialist challengers. Canon integrates dual-fisheye modules into R-mount bodies, blending optical heritage with spatial video toolchains. Sony prototypes stacked time-of-flight sensors that dovetail with plenoptic overlays, while Raytrix focuses on industrial 3-D inspection rigs.

Emergent software firms differentiate through AI-first pipelines. Leia’s cross-platform SDK abstracts depth extraction, enabling developers to embed refocus features without hardware changes.[4]Leia Inc., “Developer Documentation,” leiainc.com Intrinsic, an Alphabet subsidiary, packages plenoptic perception for robot arms, selling subscription-based autonomy stacks. Semiconductor houses such as NVIDIA supply tensor cores optimized for multi-view disparity, monetizing every camera seat through accelerated libraries.

Strategic investment continues: OPEX-friendly kits attract venture funding as they shift revenue from one-time hardware to recurring software. Joint ventures between lens makers and foundries aim to secure micro-lens capacity, hedging against supply volatility. Intellectual-property filings cluster around adaptive sensor readouts and photonic metasurfaces, signaling an impending flip from bulky glass to flat optics that may reset competitive moats.

Plenoptic Camera Industry Leaders

Raytrix GmbH

Light Labs Inc.

Lytro, Inc.

Pelican Imaging Corporation

Kandao Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NVIDIA unveiled AI-enhanced holographic modules for XR glasses, promising dynamic eye-box rendering.

- February 2025: University of Houston researchers introduced photon-counting detectors enabling multi-energy X-ray depth imaging.

- January 2025: CREAL closed a USD 8.9 million round to miniaturize light-field displays for consumer AR eyewear.

- December 2024: Light Field Lab began shipping SolidLight holographic walls for enterprise showrooms.

Global Plenoptic Camera Market Report Scope

| Standalone plenoptic cameras |

| Add-on plenoptic lens modules |

| Software-defined light-field capture kits |

| Consumer photography and videography |

| AR/VR and metaverse content creation |

| Industrial inspection and robotics |

| Medical and life-science imaging |

| Full-frame sensors |

| APS-C sensors |

| Medium-format sensors |

| Media and Entertainment |

| Healthcare |

| Industrial and Manufacturing |

| Defense and Security |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Standalone plenoptic cameras | ||

| Add-on plenoptic lens modules | |||

| Software-defined light-field capture kits | |||

| By Application | Consumer photography and videography | ||

| AR/VR and metaverse content creation | |||

| Industrial inspection and robotics | |||

| Medical and life-science imaging | |||

| By Sensor Format | Full-frame sensors | ||

| APS-C sensors | |||

| Medium-format sensors | |||

| By End-user Industry | Media and Entertainment | ||

| Healthcare | |||

| Industrial and Manufacturing | |||

| Defense and Security | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the light field camera market?

The market is valued at USD 1.89 billion in 2025, with a forecast CAGR of 17.49% through 2030.

Which region grows fastest for light-field cameras?

Asia-Pacific posts the highest regional CAGR at 18.7% owing to strong manufacturing capacity and rising AR/VR adoption.

Which application segment shows the strongest growth outlook?

Medical and life-science imaging is projected to grow at a 21.5% CAGR, the fastest among all applications.

How do software-defined kits influence adoption?

Programmable kits cut hardware costs and let developers retrofit existing cameras, propelling a 20.9% CAGR for this product class.

What limits image quality in current systems?

The spatial-angular trade-off allocates sensor pixels between resolution and depth sampling, reducing per-view clarity in high-detail tasks.

Who are notable technology providers shaping the field?

Canon, NVIDIA, Intrinsic, NSG Group, and Leia Inc. advance optics, processors, vision software, and developer ecosystems, respectively.

Page last updated on: