AI Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.08 Billion |

| Market Size (2031) | USD 29.23 Billion |

| Growth Rate (2026 - 2031) | 17.45% CAGR |

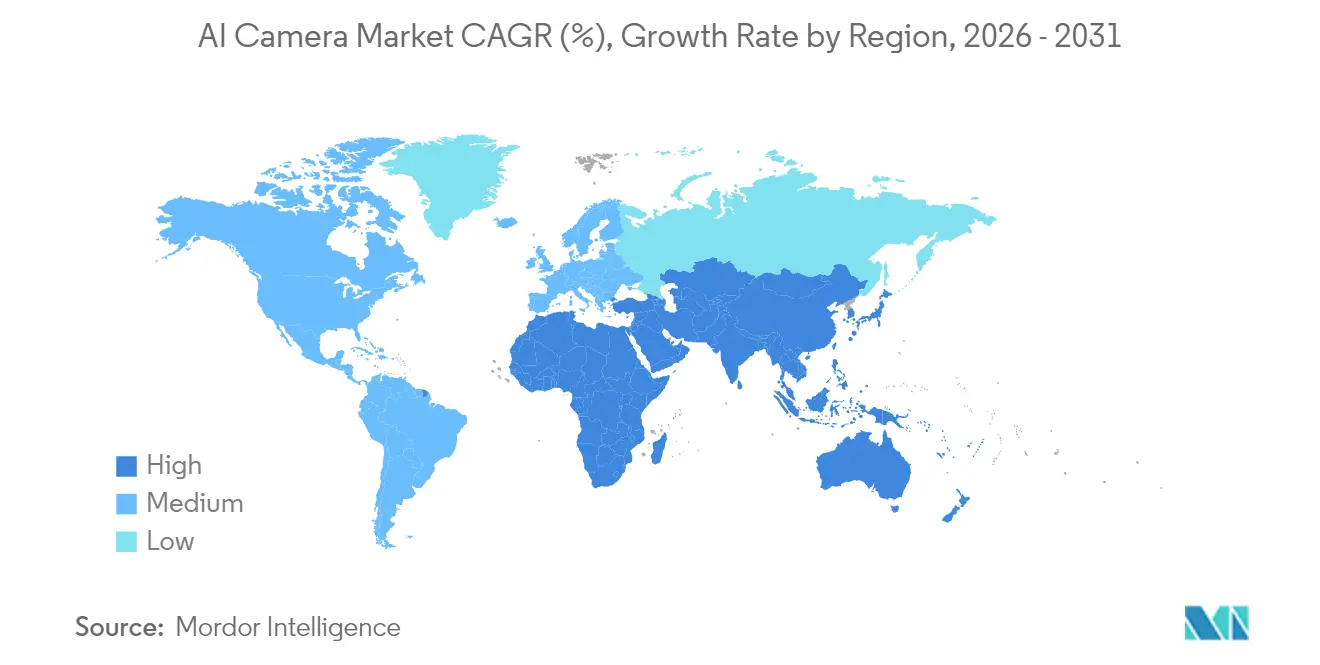

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Camera Market Analysis by Mordor Intelligence

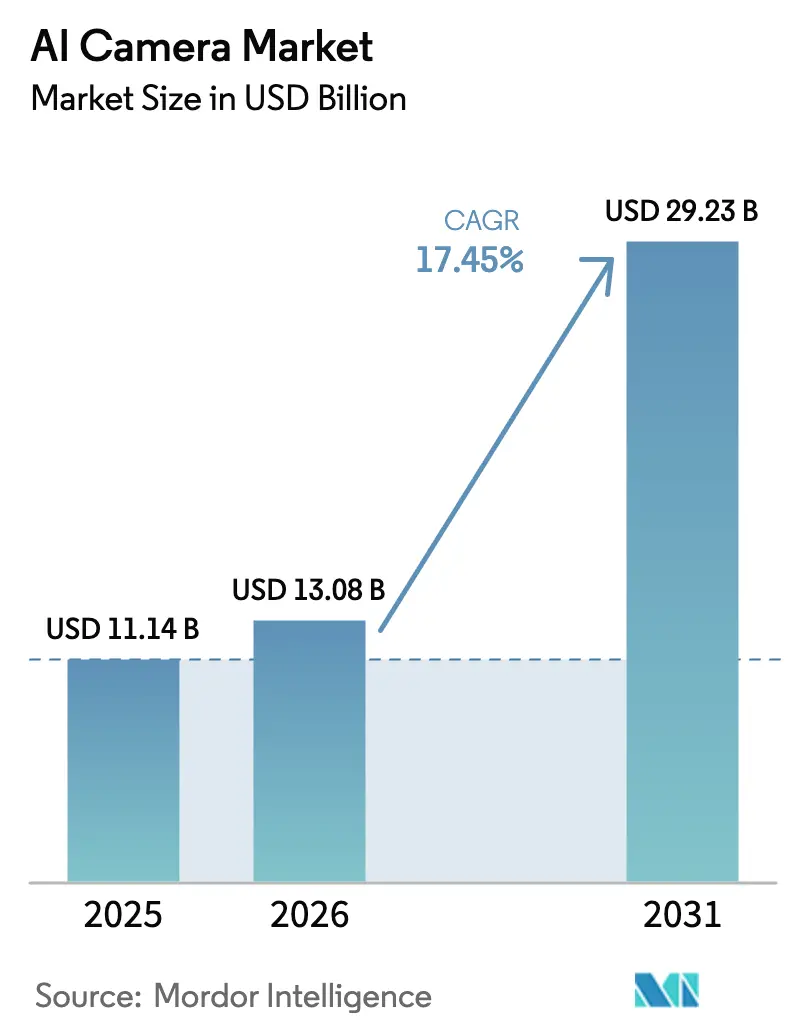

AI Camera Market size in 2026 is estimated at USD 13.08 billion, growing from 2025 value of USD 11.14 billion with 2031 projections showing USD 29.23 billion, growing at 17.45% CAGR over 2026-2031.

Demand is broad-based: intelligent surveillance, autonomous driving, retail analytics, and contact-free patient monitoring are all scaling, helped by maturing edge processors that reduce cloud dependency. Regulatory mandates such as the EU General Safety Regulation, privacy legislation that favours on-device learning, and 5G/Wi-Fi 6 roll-outs are synchronising to shorten deployment cycles. Vendors that pair proprietary AI chips with advanced optics are commanding price premiums while trimming total cost of ownership through bandwidth-sparing architectures.

Key Report Takeaways

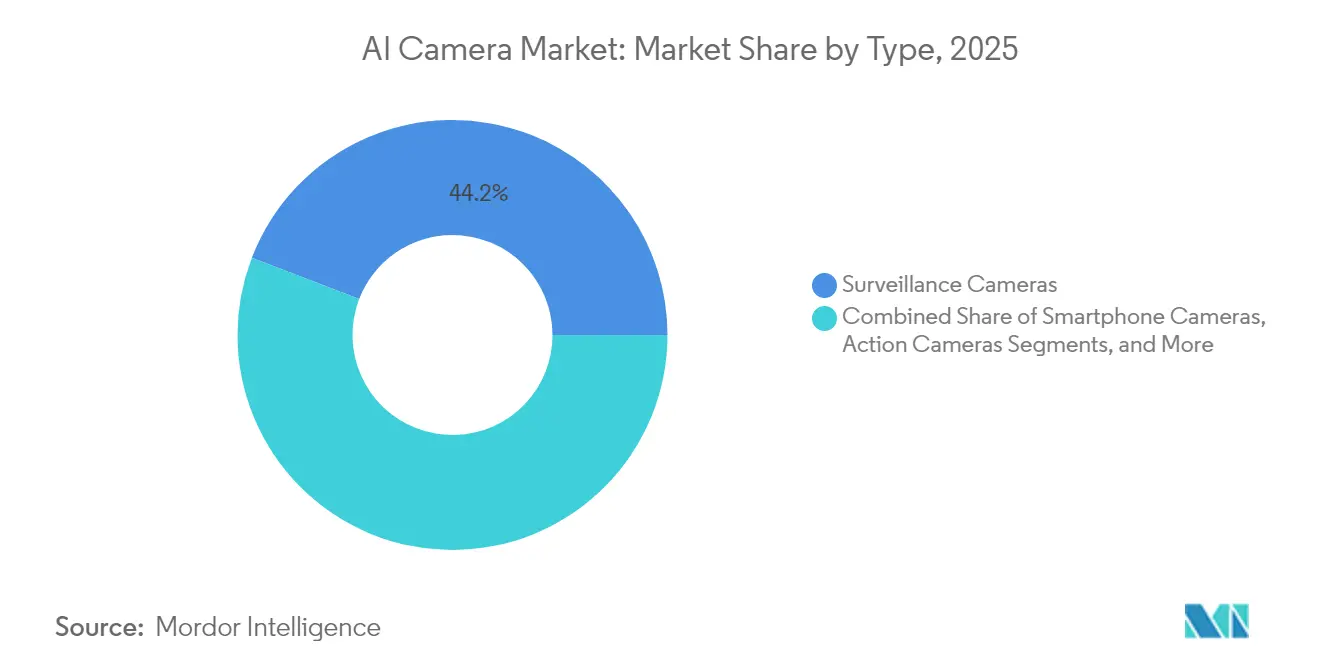

- By type, surveillance cameras led with 44.15% revenue share in 2025, while automotive cameras are projected to grow at 18.92% CAGR to 2031.

- By offering, hardware captured 58.85% of the AI camera market share in 2025; software is advancing at 17.66% CAGR through 2031.

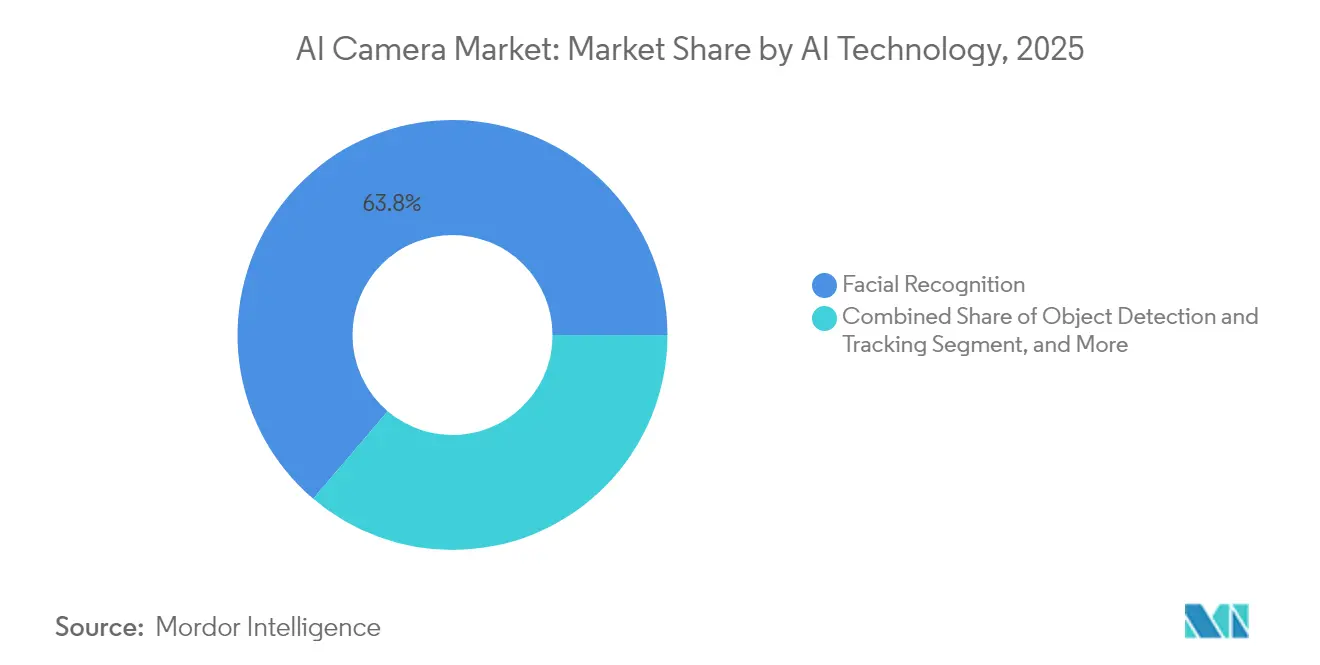

- By AI technology, facial recognition accounted for 63.78% share of the AI camera market size in 2025; gesture & emotion recognition is poised for a 21.92% CAGR to 2031.

- By deployment, indoor environments commanded a 76.92% share in 2025; outdoor deployments are on track for a 22.85% CAGR to 2031.

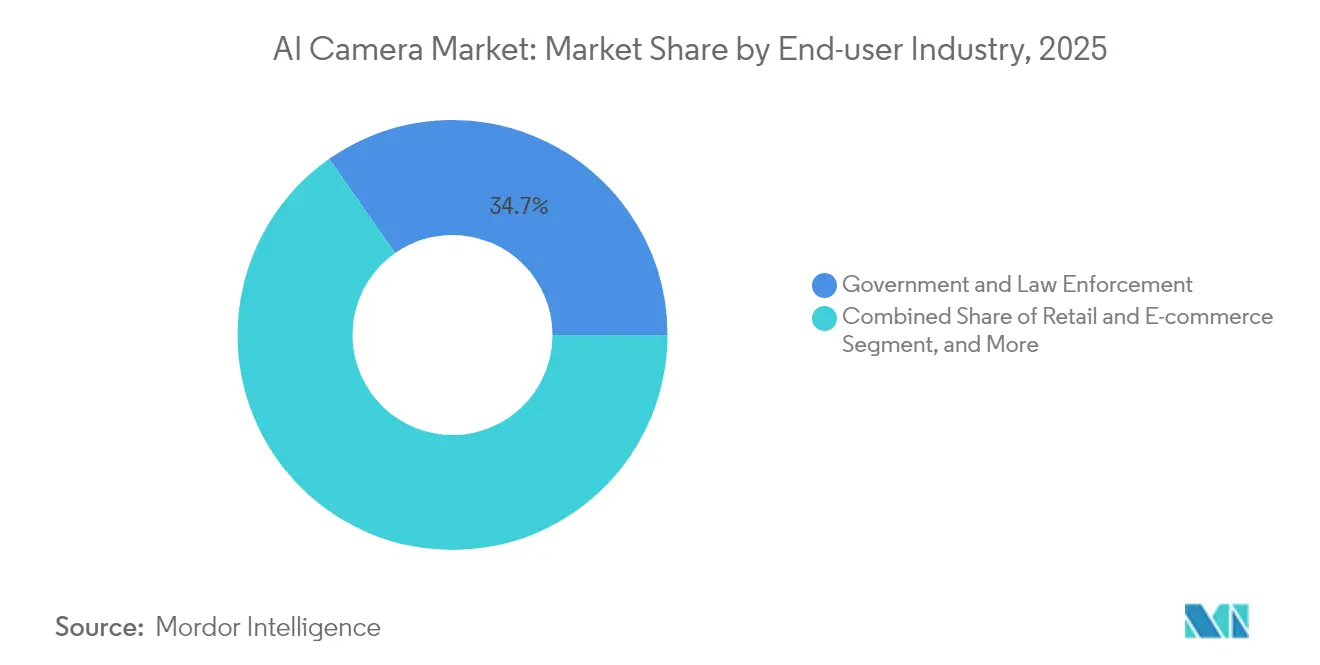

- By end-user, government and law enforcement held a 34.72% share in 2025, while healthcare is set to expand at a 19.76% CAGR to 2031.

- By geography, Asia-Pacific led with a 27.45% share in 2025; the Middle East and Africa region is projected for a 20.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge-AI processing cuts smart-city bandwidth costs | +3.2% | China, UAE, Singapore, global spillover | Medium term (2–4 years) |

| Retail video analytics for real-time shopper insight | +2.8% | North America, EU, expanding to APAC | Short term (≤ 2 years) |

| ADAS mandates push OEM AI camera integration | +4.1% | EU, China, spillover to North America | Short term (≤ 2 years) |

| 5G/Wi-Fi 6 backbone enables ultra-HD industrial vision | +2.5% | APAC, Germany, US | Medium term (2–4 years) |

| Post-COVID hospital demand for remote monitoring | +1.9% | Developed health-care systems worldwide | Long term (≥ 4 years) |

| Privacy-centric on-device learning drives upgrades | +2.1% | EU, California, other privacy-focused regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Edge-AI processing cuts smart-city bandwidth costs

Municipal programmes that move analytics to the camera have reported video backhaul savings up to 90%, allowing thousands of feeds to run on existing fibre without congestion. Lenovo’s validated design shows that only alerts and metadata need transmission, reducing latency and maintaining situational awareness during network outages.[1]Lenovo, “Lenovo Validated Design for Smart Cities,” lenovopress.lenovo.com Pilot cities in China and the UAE have logged productivity gains of 52%–245% in emergency coordination, strengthening the ROI case.[2]UK Government, “Review of the 5G Ecosystem,” assets.publishing.service.gov.uk

Retail video analytics for real-time shopper insight

Global retail AI spending is expected to be around USD 14 billion in 2025, driven by computer-vision checkout and heat-mapping for shelf optimisation. Annual smart-checkout transactions climbed from 42 million in 2019 to more than 1.4 billion in 2023, led by Chinese supermarket chains. Retailers also deploy occupancy analytics to curb shrinkage and refine staffing schedules, although compliance with EU GDPR and California CPRA restricts face-matching functions.

ADAS mandates push OEM AI camera integration

From July 2024, every new car sold in the EU must carry driver-monitoring cameras that track eye closure, gaze, and head angle in real time. Chinese regulators are following with parallel standards, giving the automotive segment a 19.4% forecast CAGR. Automakers now embed AI vision into vehicle electrical architectures instead of offering it as optional hardware, assuring volume demand for Tier-1 suppliers through 2030.

5G/Wi-Fi 6 backbone enables ultra-HD industrial vision

The Cognex In-Sight L38 system illustrates how 5G’s millisecond latency lets cameras trigger line-stop commands before defects propagate. High-throughput wireless removes the need for proprietary cabling in brownfield plants across South Korea and Germany, unlocking AI inspection for small-batch manufacturers that could not justify fibre roll-outs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR / CPRA restrict public facial-recognition roll-outs | -2.3% | EU, California, spreading elsewhere | Short term (≤ 2 years) |

| High total cost of ownership for SMEs in emerging markets | -1.8% | Latin America, Africa, SE Asia, Eastern Europe | Long term (≥ 4 years) |

| Proprietary analytics platforms create ecosystem lock-in | -1.5% | Enterprise and government worldwide | Medium term (2–4 years) |

| Chip shortages delay advanced sensors and ASICs | -2.1% | Global, acute in automotive and industrial | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GDPR / CPRA restrict public facial-recognition roll-outs

The EU AI Act ranks biometric identification as high-risk, demanding stringent risk assessments, bias audits, and cyber-resilience that raise compliance costs. Real-time face matching by police is effectively banned without a court order, forcing cities to pivot towards behavioural analytics. California’s CPRA adds similar obligations, creating fragmented rulebooks that slow multi-jurisdiction projects.

High total cost of ownership for SMEs in emerging markets

OECD polling of 840 firms found that fewer than 25% of small enterprises have adopted AI, citing capital outlays, maintenance fees, and skills gaps as prime barriers. Currency swings and import duties further inflate hardware prices in Latin America and parts of Africa, limiting AI camera uptake outside state-funded safe-city projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Surveillance Dominance Faces Automotive Disruption

Surveillance cameras commanded 44.15% of the AI camera market size in 2025, anchored by city security budgets and corporate loss-prevention programmes. Their installed base delivers recurring software revenue as analytics licences migrate to subscription models. Automotive cameras are growing faster at 18.92% CAGR as ADAS regulations shift demand from optional accessories to mandatory safety equipment, setting the stage for cross-industry component shortages.

Over the forecast horizon, surveillance growth will moderate as penetration in public networks approaches saturation, while automotive settings absorb higher-resolution sensors and in-cabin driver-monitoring units. Action and drone cameras are diversifying into industrial inspection and mapping, adding long-tail upside. Body-worn cameras for law enforcement integrate auto-redaction to comply with privacy statutes, a differentiator in procurement tenders.

By Offering: Hardware Leadership Challenged by Software Growth

Hardware captured 58.85% AI camera market share in 2025, buoyed by ASP premiums on global-shutter sensors, stacked DRAM, and low-power ASICs. Yet software is pacing at 17.66% CAGR, reflecting demand for real-time object classification, traffic-flow analytics, and AI tuning services. Surveillance vendors embed license fees into the camera SKU, transferring margin from silicon to code.

On-device SDKs compress inferencing models to run inside 3-W power envelopes, reducing backend costs and sidestepping GDPR data-transfer triggers. Cloud platforms still matter for heavy batch analytics, especially loss-prevention re-checks across multi-site retail estates, but bandwidth charges create a ceiling. The software pivot is prompting chip suppliers like Ambarella to launch CV-series SoCs with integrated neural network accelerators that support generative reconstruction.

By AI Technology: Facial Recognition Leads Despite Privacy Constraints

Facial recognition held a 63.78% share of the AI camera market size in 2025. Commercial landlords and stadium operators value rapid VIP and threat screening even as municipal deployments slow. Gesture and emotion recognition is the fastest-growing slice at 21.92% CAGR, feeding infotainment dashboards in vehicles and wellness kiosks in offices.

Multi-modal systems that blend face, gait, and object analysis reduce single-algorithm failure risk and improve accuracy in poor lighting. Privacy-preserving frameworks now hash facial templates inside secure enclaves, keeping raw images off networks. Behavioural analytics - such as dwell-time deviation alerts - offer a regulatory-friendly route for public venues wary of biometric scrutiny.

By Deployment Environment: Indoor Applications Drive Current Adoption

Indoor sites constitute 76.92% of 2025 revenue, benefiting from controlled lighting and stable power. Retail, hospitals, and office campuses install ceiling-mount PTZ cameras coupled with Wi-Fi 6 access points that backhaul metadata every few seconds.

Outdoor deployments are projected to rise at 22.85% CAGR as IP67-rated enclosures, vanadium-oxide thermal sensors, and edge AI chips withstand temperature swings. Smart-highway agencies in Japan and the UAE install solar-powered roadside units that stream only traffic-violation clips, cutting data backhaul by over 70%.

By End-user Industry: Government Leadership Faces Healthcare Challenge

Government and law-enforcement agencies accounted for 34.72% of the 2025 demand, driven by safe-city programmes and corrections-facility modernisation. Procurement frameworks increasingly bundle multi-year analytics licences, smoothing revenue for vendors. Healthcare is accelerating at 19.76% CAGR as hospitals retrofit ICU beds with contactless vitals monitoring that flags patient deterioration in under 30 seconds.

Retail chains deploy shelf-stocking robots guided by ceiling cameras that detect out-of-stock gaps. Manufacturing plants leverage AI vision to grade weld quality and spot PPE compliance. Banking lobbies employ behaviour analysis to deter queue-jump fraud and tailgating into restricted areas.

Geography Analysis

Asia-Pacific leads the AI camera market with 27.45% revenue share and benefits from vertically integrated supply chains spanning sensors to finished cameras. China’s provincial safe-city contracts routinely exceed 50,000-camera lots, and Japanese OEMs pre-install driver-monitoring units across entire 2025 model year production runs. South Korea leverages nationwide 5G to deliver 4K feeds for automated tolling, while India’s smart-mobility corridors under the Digital India programme stimulate demand in tier-1 metros.

The Middle East and Africa posts the fastest CAGR at 20.88%. Abu Dhabi’s Ghadan 21 stimulus channels funding into AI start-ups that localise analytics for Arabic scripts on road signage, and Saudi Aramco pilots oil-rig flare-stack monitoring using thermal AI cameras that withstand 60 °C ambient heat. The GCC surveillance spending trajectory aligns with mandatory video laws enacted in 2024, ensuring baseline demand even if crude prices fluctuate.

North America combines mature enterprise budgets with experimental pilots such as Amazon’s Just Walk Out stores that rely on hundreds of ceiling cameras per site. Privacy pressure from CPRA accelerates the shift toward on-device encryption inside camera ASICs. Europe’s cautious stance on biometrics tempers public deployment volumes, but compulsory ADAS will roll more than 15 million driver-monitoring cameras onto roads by 2026, partially offsetting surveillance drag in city centres.

Competitive Landscape

The AI camera market is moderately fragmented. Hikvision and Dahua still top shipment volume, but semiconductor houses like Ambarella and NVIDIA pull margin through silicon differentiation. Axis Communications pursues open-platform alliances, allowing third-party analytics to run on its cameras, while Verkada and Meraki continue closed-ecosystem models that lock customers into subscription renewals.

Strategic partnerships are reshaping power balances. Vicon’s tie-up with Hailo integrates 20-TOPS inference inside a modular housing, cutting latency to 5 ms for person-counting at retail entrances. Cognex pairs proprietary laser optics with deep-learning software to detect sub-millimetre defects on electronics lines, and Motorola Solutions’ Silent Sentinel acquisition adds 20-mile thermal coverage for critical-infrastructure clients.

Price competition at the low end remains fierce, but premium tiers justify MSRP uplifts via predictive maintenance analytics and zero-trust cyber-hardening. Vendors offering full-stack control - from ISP firmware to cloud dashboard - capture recurring ARR, insulating revenue against hardware down-cycles.

AI Camera Industry Leaders

Sony Corporation

Panasonic Corporation

Canon Inc.

Honeywell International Inc.

Hangzhou Hikvision Digital Technology Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Deep Sentinel launched a “Bring Your Own Camera” programme that links third-party cameras to its AI monitoring cloud, lowering replacement costs for legacy estates.

- February 2025: Motorola Solutions acquired Silent Sentinel, adding long-range thermal imaging to its portfolio.

- December 2024: Vicon Industries and Hailo began shipping the NEXT Modular Camera with Hailo-15 edge AI processing.

- August 2024: Actuate raised USD 11.5 million to expand its video analytics suite focused on remote management.

Global AI Camera Market Report Scope

AI camera is a security device with advanced technology, enabling it to interpret its surroundings. Leveraging technologies like machine learning (ML), these cameras analyse visuals, cross-referencing them with databases and other data sources to enhance users' insights. AI cameras enhance business security and promote informed decision-making. By introducing services like video alarms, AI cameras enable owners to detect events promptly, validate alarms, and transmit real-time footage to emergency responders.

The study tracks the revenue accrued through the sale of AI camera types by various players globally. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The AI Camera Market is Segmented by type (surveillance cameras, DSLR cameras, smartphone cameras, and others), offering (image sensors, memory and storage, processors, and others), technology (object detection and recognition, facial recognition, night vision, motion detection, and others), end-user industry (law enforcement and public sector, healthcare, retail, automotive, industrial, BFSI, and others), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Surveillance Cameras |

| Smartphone Cameras |

| Digital Still Cameras (DSLR and Mirrorless) |

| Automotive Cameras |

| Body-worn Cameras |

| Action Cameras |

| Drone and Aerial Cameras |

| Hardware | Image Sensors |

| Processors (ASIC/SoC) | |

| Memory and Storage | |

| Lens and Optics | |

| Software | On-device AI Software/SDK |

| Cloud-based Video Analytics | |

| Services | Integration and Installation |

| Maintenance and Support |

| Facial Recognition |

| Object Detection and Tracking |

| Gesture and Emotion Recognition |

| Scene Recognition and Auto-Exposure |

| Low-light/Night Vision |

| Motion Detection |

| Indoor |

| Outdoor |

| Government and Law Enforcement |

| Retail and E-commerce |

| Transportation and Mobility |

| Healthcare and Hospitals |

| Industrial and Manufacturing |

| Banking and Financial Services |

| Residential/Smart Homes |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Surveillance Cameras | ||

| Smartphone Cameras | |||

| Digital Still Cameras (DSLR and Mirrorless) | |||

| Automotive Cameras | |||

| Body-worn Cameras | |||

| Action Cameras | |||

| Drone and Aerial Cameras | |||

| By Offering | Hardware | Image Sensors | |

| Processors (ASIC/SoC) | |||

| Memory and Storage | |||

| Lens and Optics | |||

| Software | On-device AI Software/SDK | ||

| Cloud-based Video Analytics | |||

| Services | Integration and Installation | ||

| Maintenance and Support | |||

| By AI Technology | Facial Recognition | ||

| Object Detection and Tracking | |||

| Gesture and Emotion Recognition | |||

| Scene Recognition and Auto-Exposure | |||

| Low-light/Night Vision | |||

| Motion Detection | |||

| By Deployment Environment | Indoor | ||

| Outdoor | |||

| By End-user Industry | Government and Law Enforcement | ||

| Retail and E-commerce | |||

| Transportation and Mobility | |||

| Healthcare and Hospitals | |||

| Industrial and Manufacturing | |||

| Banking and Financial Services | |||

| Residential/Smart Homes | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the AI camera market?

The AI camera market is valued at USD 13.08 billion in 2026 and is projected to rise to USD 29.23 billion by 2031.

Which camera type holds the largest share?

Surveillance cameras hold the largest share at 44.15% of 2025 revenue, reflecting entrenched demand in public-safety and enterprise security networks.

Which end-user segment is growing quickest?

Healthcare shows the fastest expansion at a 19.76% CAGR to 2031 as hospitals adopt contactless patient-monitoring solutions.

Why are automotive cameras gaining momentum?

EU and Chinese safety regulations now mandate driver-monitoring and other ADAS functions, pushing OEMs to integrate AI vision across all new vehicles by 2026.

How do privacy laws affect AI camera deployments?

GDPR and CPRA classify facial recognition as high-risk, compelling on-device processing and privacy-preserving analytics that avoid storing personally identifiable imagery.

Which region is expected to grow the fastest through 2031?

The Middle East & Africa region is projected for a 20.88% CAGR, driven by sovereign AI roadmaps and large-scale infrastructure diversification projects.

Page last updated on: