Cinema Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

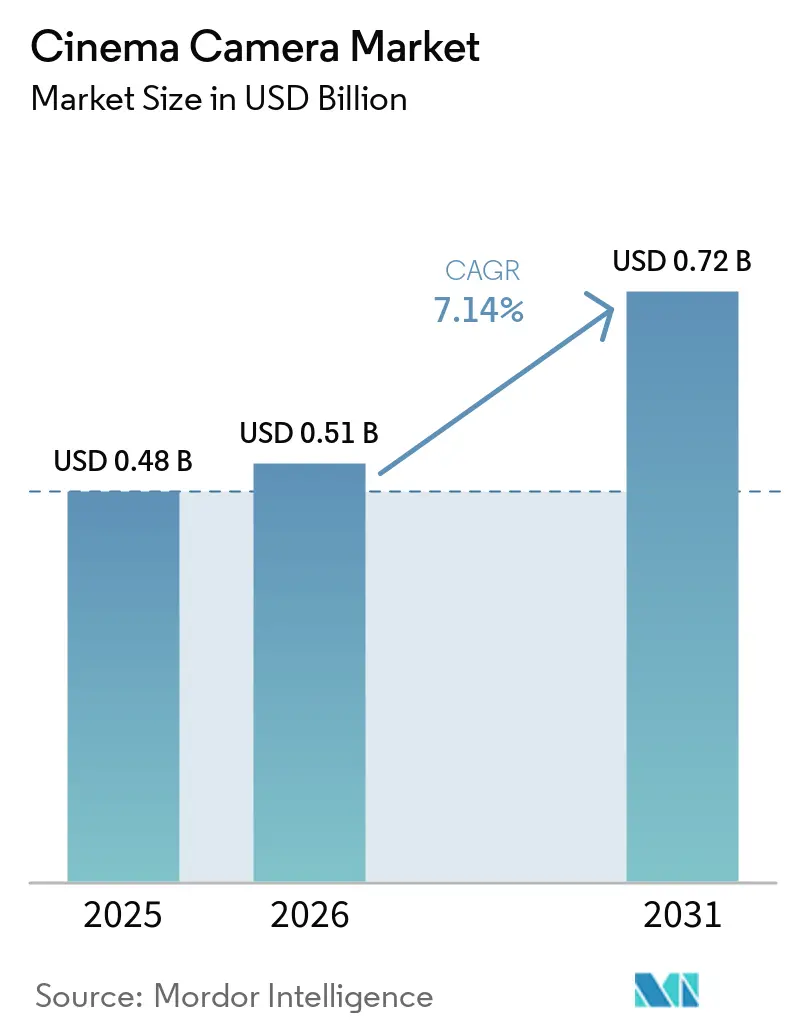

| Market Size (2026) | USD 0.51 Billion |

| Market Size (2031) | USD 0.72 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

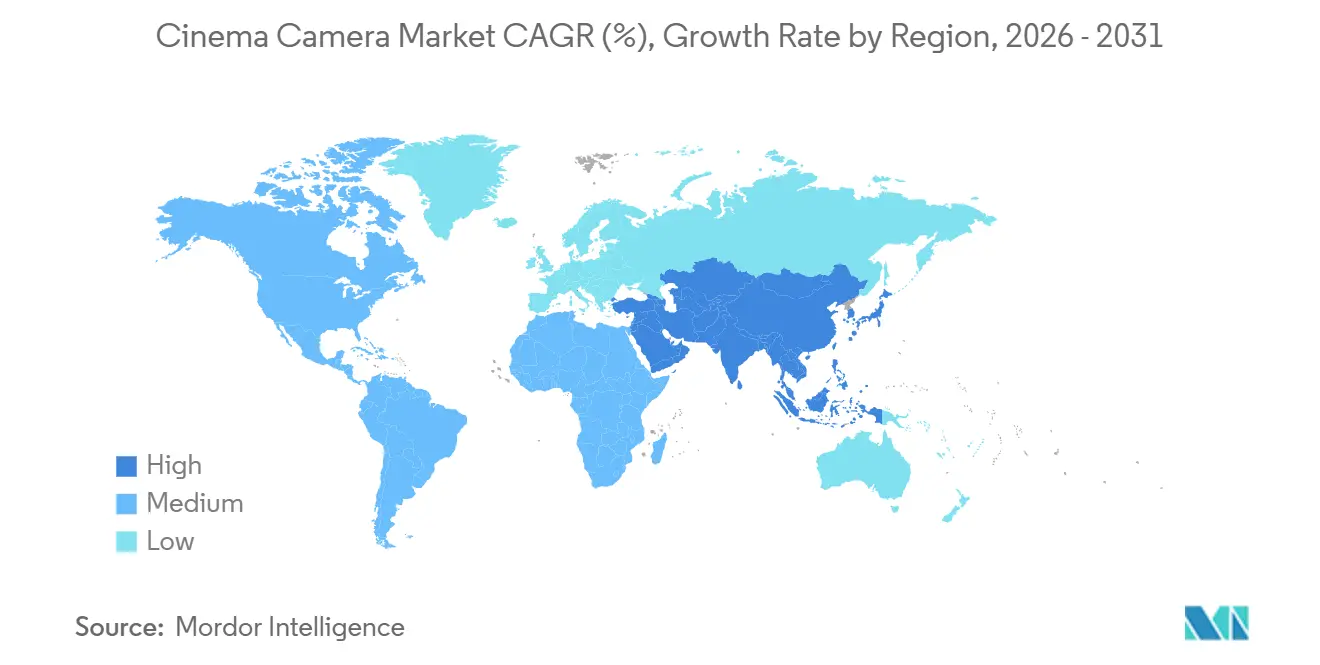

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

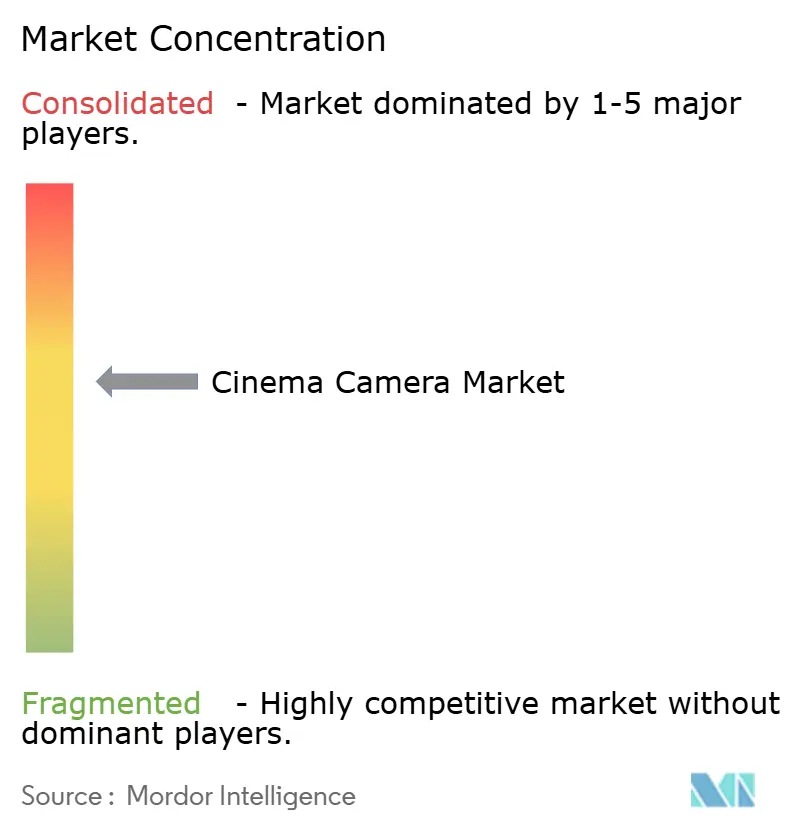

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cinema Camera Market Analysis by Mordor Intelligence

The cinema camera market size is expected to increase from USD 0.48 billion in 2025 to USD 0.51 billion in 2026 and reach USD 0.72 billion by 2031, growing at a CAGR of 7.14% over 2026-2031. Rising demand for 4K-plus native capture on streaming originals, shorter replacement cycles triggered by virtual production, and aggressive sub-USD 10,000 full-frame launches are redrawing purchasing criteria across studios, rental houses, and independent creators. Capital is flowing toward bodies that embed gen-lock, low-latency metadata, and AI-assisted autofocus so that on-set image decisions migrate upstream and compress post timetables. Simultaneously, high-budget features are shifting lens budgets to large-format glass in pursuit of depth-of-field aesthetics that differentiate premium content on home displays, while cost-sensitive segments lean on oversampling and proxy workflows to contain data-rate overheads.

Key Report Takeaways

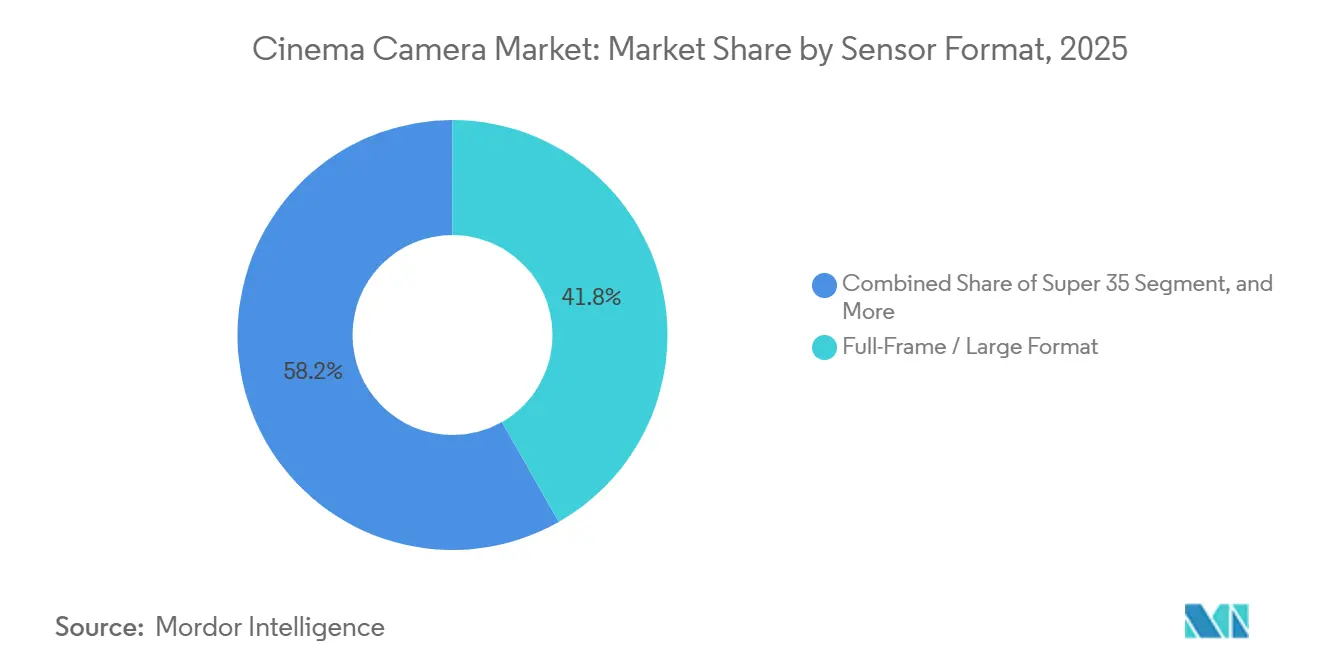

- By sensor format, full-frame and large-format models held 41.78% of the cinema camera market in 2025, and the segment is projected to expand at a 7.94% CAGR through 2031.

- By resolution, 8K and above is the fastest-growing tier, advancing at a 7.88% CAGR through 2031, whereas 4K captured 48.13% of revenue share in 2025.

- By camera type, virtual-production-integrated bodies are forecast to grow at 7.63%, while traditional digital cinema cameras are forecast to hold a 66.43% revenue share in 2025.

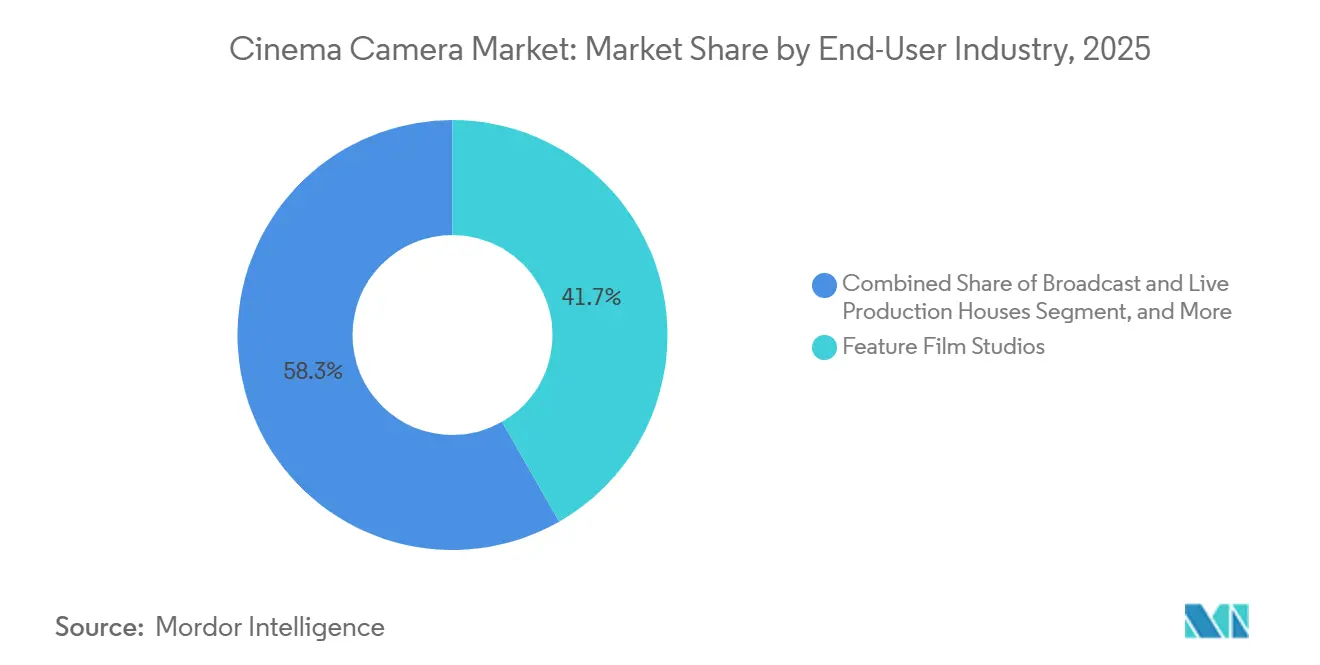

- By end user, feature film studios commanded 41.74% of 2025 demand, while independent and documentary filmmakers are expanding at 8.01% through 2031.

- By distribution channel, direct sales and rental houses accounted for 54.31% of 2025 turnover, yet online retail is projected to grow by 7.73% through 2031.

- By geography, Asia-Pacific led with 33.12% of 2025 revenue, whereas the Middle East is forecast to post the fastest pace at 8.14% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cinema Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for 4K and Higher Cinematic Content | +1.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid Image-Sensor Innovations (Stacked CMOS, Global Shutter) | +1.5% | Global, led by Japan and South Korea sensor fabrication hubs | Long term (≥ 4 years) |

| Full-Frame and Large-Format Adoption in High-Budget Features | +1.3% | North America and Europe, spillover to Middle East | Medium term (2-4 years) |

| Virtual-Production Volumes Needing Gen-Lock Capable Cameras | +1.2% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| AI-Powered Autofocus and On-Sensor Processing for Indie Workflows | +0.9% | Global, with rapid uptake in Asia-Pacific and South America | Medium term (2-4 years) |

| Emerging-Market Film Industries Boosting Rental Demand | +0.8% | Middle East, India, South Korea, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for 4K and Higher Cinematic Content

Streaming platforms now mandate 4K as a baseline deliverable and actively encourage 6K or 8K origination to keep libraries future-proof. Episodic series budgeting above USD 5 million per episode increasingly specifies 8K bodies even when output remains 4K, because higher native resolution allows digital stabilization and reframing headroom without visual penalties. Rental houses are retiring 2K-only stock ahead of depreciation schedules, creating steep secondary-market discounts that lower entry barriers for emerging filmmakers.[1]Association of Independent Commercial Producers, “2025 Production Formats Survey,” aicp.com Commercial producers have joined the shift, with 63% of North American and European spots captured at 6K in 2025 to support social media repurposing without reshoots. The resolution race, therefore, pulls new capital toward sensors capable of high-speed oversampling and robust heat dissipation, while lifting throughput requirements across media cards, on-set DIT carts, and cloud archives.

Rapid Image-Sensor Innovations (Stacked CMOS, Global Shutter)

Sony released three global-shutter stacked CMOS parts in 2024 that cut readout to below 1 ms and remove rolling-shutter skew during whip pans and drone moves. Canon embedded deep-learning autofocus directly on-sensor, pushing subject-tracking accuracy to 96% and reducing dependence on dedicated focus pullers on sub-USD 10 million shows. Prototype sensors from Forza reached 1,100 fps at 4K, proving that high-speed capture can move beyond ultra-specialized systems priced above USD 150,000. These breakthroughs compress the performance gap between cinema and broadcast gear, forcing manufacturers to differentiate with color science and metadata richness rather than basic sensitivity specs. Supply risk nevertheless lingers because global-shutter wafer output is concentrated in two Japanese fabs, meaning any disruption could choke supply for a full production year.

Full-Frame and Large-Format Adoption in High-Budget Features

Full-frame rigs accounted for 41.78% of revenue in 2025 and are on track for a 7.94% CAGR as cinematographers chase shallow depth-of-field, which signals premium positioning to viewers. Streaming originals allocate up to 22% of an episode’s budget to camera and lighting, compared with 15% in legacy broadcast, underscoring how visual differentiation has become a subscriber-retention lever. Large-format sensors also broaden the field of view at identical focal lengths, reducing lens swaps and boosting daily page counts by as much as 15%. Lens costs remain a barrier, running roughly 50% above Super 35 glass, and the thinner focus plane raises retake counts, yet rental houses still charge 25%-30% daily premiums because demand remains strong. The result is a two-tier lens ecosystem in which high-budget shows use premium optics, while cost-sensitive shoots stick with legacy PL-mount sets.

Virtual-Production Volumes Needing Gen-Lock Capable Cameras

More than 300 permanent virtual-production volumes were operational worldwide by 2025, up from fewer than 50 in 2020, and every wall demands cameras that can gen-lock to LED refresh cycles to avoid banding. Sony VENICE 2 and ARRI Alexa 35 both stream low-latency lens metadata over SMPTE ST 2110 to real-time engines, ensuring parallax and lighting match live backgrounds. Rental houses accelerated refresh timelines by 18 months to stock gen-lock-ready kits because productions using LED stages cut post schedules by roughly 30% and shave 15%-20% off overall budgets. Cameras designed primarily for virtual production now ship with integrated wireless lens control and on-sensor distortion maps, features previously sold as bolt-on modules. Manufacturers that lag on these capabilities risk obsolescence as virtual production becomes a default for effects-heavy series.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Costs and TCO of Professional Cine Cameras | -1.4% | Global, acute in emerging markets | Medium term (2-4 years) |

| Data-Intensive 6K-12K Workflows Strain Storage and Post Budgets | -1.1% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Supply-Chain Tightness for Global-Shutter Sensor Wafers | -0.7% | Global, with bottlenecks in Japan and South Korea | Short term (≤ 2 years) |

| Eco-Regulations on Hazardous Electronics Components | -0.4% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs and TCO of Professional Cine Cameras

An ARRI Alexa 35 package exceeds USD 150,000 once lenses, wireless follow focus, monitors, and proprietary media are added. Annual maintenance averages 10% of the acquisition cost, while Codex Media still invoices at triple the consumer SSD rate. Consequently, only major rental houses or continuously producing studios can justify ownership; smaller teams gravitate toward mirrorless hybrids that meet Netflix 4K criteria for one-fifth the outlay. ShareGrid data show that breakeven on a flagship body occurs after roughly 80 rental days, a duration only long-running series typically hit. Emerging markets face steeper hurdles, as a USD 150,000 spend equates to nearly two years of senior cinematographer wages in India or Brazil.

Data-Intensive 6K-12K Workflows Strain Storage and Post Budgets

Recording 8K RAW yields 2.6 TB per hour, ballooning cloud archival costs to USD 0.023 per GB per month and pushing the annual storage for a 10-hour feature to USD 7,200. Real-time 8K color grading requires dual Ada GPUs, adding USD 25,000 per bay.[2]NVIDIA, “RTX 6000 Ada GPU Datasheet,” nvidia.com Proxy generation multiplies transcoding labor, stretching post schedules by 2-3 weeks and inflating facility invoices by up to USD 25,000 per title. India’s facility gap is glaring; only 12% of shops can process 8K, forcing offshoring at 60% cost premiums. Productions therefore adopt a hybrid capture approach, 8K for effects plates and 4K for dialog, to balance quality and budget, though format juggling increases conform risks during final assembly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Format: Full-Frame Rewrites Rental Economics

Full-frame and large-format units accounted for 41.78% of 2025 revenue, and their share of the cinema camera market is projected to widen as the tier posts a 7.94% CAGR through 2031. High-end dramas and franchise films rely on the format’s shallow depth of field to distinguish streaming originals from traditional television. Rental houses report full-frame kits earning 25% daily rate premiums over Super 35, while still posting 90% utilization during peak production months. Super 35 remains indispensable for documentaries and run-and-gun features because its deeper focus plane lowers retake counts, and decades of PL glass reduce lens-budget pressure. Micro Four Thirds fills drones and gimbals, where sub-1.2 kg payloads are mandatory. Super 16 and 35 mm film persists for auteur projects but faces lab scarcity. Manufacturers now ship modular bodies that accept multiple sensor blocks so crews can pivot between full-frame and Super 35 on the same chassis, though this flexibility adds 15% weight and complicates cooling.

The cinema camera market is increasingly orienting R&D toward maintaining color-science parity across interchangeable blocks so that editors can intercut formats seamlessly. Full-frame adoption forces lens suppliers to reissue vintage focal lengths in new mounts, and average weekly lens rental revenue has risen 18% since 2024 as a result. Super 35’s resilience stems from global broadcast workflows that still rely on BB4-mount adapters and ENG zoom ranges unheard of in full-frame glass. Meanwhile, Micro Four Thirds growth plateaued once full-frame bodies like Sony FX3 hit equivalent weight classes. Film’s two-digit growth in 2025 stemmed mostly from music videos chasing grain aesthetics, not mainstream narrative production. As a result, inventory managers allocate capex toward full-frame while sweating existing Super 35 stock, reinforcing a dual-format equilibrium that should underpin cinema camera market share dynamics for the next five years.

By Resolution Capability: 8K Momentum Versus Workflow Drag

4K held 48.13% of 2025 revenue, yet 8K is forecast to post a 7.88% CAGR, and the cinema camera market size for 8K rigs is moving faster than infrastructure readiness. Sony indicated that 72% of VENICE 2 shipments in 2025 were 8K-enabled, signifying demand that outstrips immediate distribution need. Visual effects and action genres appreciate the oversized canvas for stabilization, while marketing teams value the ability to pull high-resolution stills from motion frames. Cloud storage firms report 320% year-over-year growth in 8K ingest volumes. By contrast, 6K sits in a Goldilocks slot, delivering 50% more pixels than 4K but halving the data load of 8K, making it the sweet spot for mid-budget scripted work and commercial shoots.

Despite the hype, less than 15% of finished titles in 2025 were mastered at 4K or higher because post-facility access lags behind capture ambitions. Productions often down-res 8K RAW to 4K OpenEXR during visual-effects handoff to manage file weight. The cinema camera industry counters workflow drag by embedding H.265 and Apple ProRes record options at capture so that lower-bitrate mezzanine files coexist on the same card. Future demand hinges on cost declines in SSDs and public-cloud egress fees. Meanwhile, 2K cameras are used only in live broadcasts, where bandwidth throttles resolution. As streaming platforms roll out 8K front-end apps in Japan and South Korea, adoption should accelerate, yet economic feasibility will depend on broader reductions in data-center power draw and network transit costs.

By Camera Type: Virtual-Production-Ready Bodies Gain Ground

Traditional digital cinema cameras contributed 66.43% of 2025 revenue, but virtual-production-integrated bodies are growing at 7.63% as LED-stage usage explodes. The cinema camera market share for these purpose-built units is expected to cross 30% by 2031. Gen-lock input, low-latency lens-data streaming, and wireless focus are now table stakes for marquee episodic contracts. Sony VENICE 2 and ARRI Alexa 35 lead bookings on stages in Los Angeles, London, and Seoul, driven by latency budgets under 6 ms for real-time parallax correction. Film cameras cling to an artist niche below 2% share, whereas 3D and VR rigs stall because headset adoption cooled in 2025.

Manufacturers are increasingly down-cascade virtual production features into sub-USD 10,000 bodies. Blackmagic’s PYXIS 6K streams metadata over Ethernet, while Canon C80 supports RF lens mapping, letting indie crews link directly to Unreal Engine in prosumer budgets. This democratization could cannibalize premium tiers if image-quality deltas narrow, prompting vendors to wrap cloud-collaboration ecosystems around flagships to defend margins. Hybrid mirrorless models dominate documentary festivals because their autofocus and compact size enable single-operator shoots, underlining disparate priorities across segments of the cinema camera market.

By End-User Industry: Indies Propel Volume, Studios Anchor Value

Feature film studios accounted for 41.74% of 2025 demand in dollar terms, purchasing or renting top-tier packages regardless of cost, while independents and documentarians posted the highest unit growth at 8.01% CAGR. Indie directors increasingly exploit sub-USD 6,000 Netflix-approved bodies that negate the need for dedicated digital imaging technicians. At the 2026 Sundance Festival, Sony FX3 and FX6 appeared in over half of documentary entries, confirming that affordability plus autofocus can displace heavier rigs on verité shoots.

Broadcasters upgraded faster than expected once the Olympics and NFL rights holders mandated 4K workflows, pushing newsroom orders for ENG-style cinema hybrids.[3]European Broadcasting Union, “4K Deployment Survey,” ebu.ch Commercial production firms, which turn projects in under two weeks, now own rather than rent bodies so they can amortize across 15 shoots annually. Government film-fund incentives in Saudi Arabia and South Korea, coupled with rebate rules that favor local equipment spend, further diversify the cinema camera market. Studios will continue commanding premium rental packages, but independents set the volume trend that guides product-line breadth and firmware cadence.

By Distribution Channel: Online Financing Transforms Ownership

Direct sales and rental houses accounted for 54.31% of 2025 revenue; yet online retail is projected to expand by 7.73%, aided by 0% APR installment plans that cut upfront capital by 70%. B and H Photo Video disclosed that 42% of cinema camera receipts in 2025 involved third-party financing, illustrating how payment flexibility unlocks ownership for freelance cinematographers and boutique agencies. Sub-USD 10,000 price points make online checkout viable without hands-on demos, although bodies above USD 50,000 still flow through rental networks that bundle insurance and 24-hour swaps.

Manufacturers establish regional service hubs and virtual configurators to replicate the consultative value of brick-and-mortar dealers. Specialty stores now account for only 14% of the market share and are repositioning toward educational workshops and sensor cleaning services to stay differentiated. The cinema camera industry expects online platforms to capture most incremental unit growth, while high-value studio orders continue rotating through legacy dealer relationships anchored by production insurance requirements.

Geography Analysis

Asia-Pacific delivered 33.12% of 2025 revenue and remains the strategic growth engine of the cinema camera market. China’s USD 7.45 billion box-office rebound in 2025 funneled capex into 6K and 8K bodies for science-fiction tentpoles, and the country’s subsidy matrix favors domestic equipment purchases. South Korea earmarked KRW 150 billion (USD 108 million) for a Busan virtual-production complex that will house 12 LED volumes, guaranteeing a local customer base for gen-lock-ready cameras. India certified 3,455 features in FY 2024-25 and logged a USD 1.23 billion visual-effects sector, yet only 12% of its post facilities can process 8K, sending high-res masters to North American vendors at 60% premiums.

The Middle East is projected to post the fastest regional CAGR of 8.14% through 2031, as Saudi Arabia’s 40% cash rebate scheme aims to reach 100 features by 2030. PlayMaker Studios and Jax Film Studios collectively invested USD 500 million in LED-equipped stages, though only six rental houses carry multi-million-dollar inventories, forcing productions to air-freight kits from Europe at 30% extra cost. The United Arab Emirates maintains a zero-tax regime on film services; Dubai hosted 47 international shoots in 2025, up 52% from 2023, reinforcing Gulf demand for large-format packages that impress global producers.

North America and Europe together accounted for 52% of 2025 spending, supported by dense infrastructure and proximity to streaming headquarters in Los Angeles and London. The United States alone operates more than 180 LED stages, and episodic budgets allocate up to 22% for cameras and lighting. Europe remains fragmented by national incentives and customs paperwork, but ARRI’s Munich base secures a 58% share of high-budget European titles. South America trails because import tariffs lift camera prices by up to 50%, though Brazil’s 312 domestic features in 2025 highlight latent demand once fiscal barriers ease.[4]Brazilian Film Agency, “National Production Numbers 2025,” ancine.gov.br

Competitive Landscape

Competition is moderate consolidated. The top five vendors, ARRI, Sony, Canon, Nikon-RED, and Blackmagic Design, captured roughly 68% of 2025 revenue, giving the cinema camera market a mid-level concentration. ARRI leverages proprietary color science plus a USD 2.8 billion installed lens ecosystem to keep Alexa 35 on 68% of Sundance 2026 features. Sony’s dual-base ISO VENICE 2 slashes lighting truck needs by 40%, winning episodic bids that shoot four-company moves per day. Nikon’s purchase of RED folds autofocus IP into cinema bodies, foreshadowing computational imaging features that could close the gap between stills and moving-image devices.

Chinese challengers attack on price, Kinefinity grabs 8% Asia-Pacific share with USD 10,000 8K bodies, and Z CAM sells virtual-production-ready models at half Western prices, though limited service networks constrain take-up outside China. Vendors increasingly compete on software, AI-driven focus, noise reduction, and cloud-pipeline hooks now headline product launches. SMPTE ST 2110 has standardized metadata flow, reducing vendor lock-in and turning hardware into a commodity layer where price and delivery lead times dominate. Established brands respond by compressing refresh cycles to 24 months and bundling cloud grading or remote monitoring to keep customers in proprietary ecosystems.

Looking ahead, entry-level Netflix-approved camera bodies priced below USD 5,000 present a significant untapped opportunity in the market. Currently, Blackmagic’s PYXIS 6K is the only product occupying this space. However, it is expected to face increasing competition from major players such as Canon and Sony, which are likely to enter this segment once they address concerns about margin cannibalization. Additionally, Chinese manufacturers are anticipated to target Western rental houses by establishing service depots in key locations such as Los Angeles and London. In response, existing market leaders may adopt innovative strategies, such as introducing firmware subscription models. These models would shift costs from capital expenditure (capex) to operational expenditure (opex), potentially transforming rental firms' fleet planning strategies.

Cinema Camera Industry Leaders

Arnold & Richter Cine Technik GmbH & Co. Betriebs KG (ARRI)

Red Digital Cinema, LLC

Blackmagic Design Pty Ltd.

Canon Inc.

Sony Group Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Canon issued firmware enabling 6K 120 fps Canon RAW Light on C400 and C80, cutting high-frame-rate file sizes by 35%.

- March 2026: Sony launched the FX9 Mark II, adding dual-base ISO 800/4000 to attract documentary crews working in low light.

- February 2026: ARRI unveiled Alexa 35 Live with built-in fiber transmission for multi-camera sports and concert coverage.

- January 2026: Blackmagic introduced URSA Cine 17K, a 17K large-format body at USD 30,000, pricing 60% under flagship rivals.

Global Cinema Camera Market Report Scope

The Cinema Camera Market refers to the global industry that designs, manufactures, distributes, and sells professional-grade cameras specifically built for motion picture production. These cameras are engineered to deliver high-resolution video, advanced color science, wide dynamic range, and cinematic image quality required for films, television, advertising, and digital content creation.

The Cinema Camera Market Report is Segmented by Sensor Format (Full-Frame/Large Format, Super 35, Micro Four Thirds, and Super 16 and Film), Resolution Capability (4K, 6K, 8K and Above, and Less Than or Equal to 2K HD), Camera Type (Digital Cinema Cameras, Film Cameras, Virtual-Production Integrated Cameras, and 3-D/VR Cinema Cameras), End-User Industry (Feature Film Studios, Independent and Documentary Filmmakers, Broadcast and Live Production Houses, and Advertising and Commercial Production Companies), Distribution Channel (Direct Sales and Rental Houses, Online Retail/E-Commerce, Specialty Camera Stores, and Authorized Resellers and System Integrators), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Full-Frame / Large Format |

| Super 35 |

| Micro Four Thirds |

| Super 16 and Film |

| 4K |

| 6K |

| 8K and Above |

| Less Than or Equal to 2K HD |

| Digital Cinema Cameras |

| Film Cameras |

| Virtual-Production Integrated Cameras |

| 3-D/VR Cinema Cameras |

| Feature Film Studios |

| Independent and Documentary Filmmakers |

| Broadcast and Live Production Houses |

| Advertising and Commercial Production Companies |

| Direct Sales and Rental Houses |

| Online Retail/E-Commerce |

| Specialty Camera Stores |

| Authorised Resellers and System Integrators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Sensor Format | Full-Frame / Large Format | ||

| Super 35 | |||

| Micro Four Thirds | |||

| Super 16 and Film | |||

| By Resolution Capability | 4K | ||

| 6K | |||

| 8K and Above | |||

| Less Than or Equal to 2K HD | |||

| By Camera Type | Digital Cinema Cameras | ||

| Film Cameras | |||

| Virtual-Production Integrated Cameras | |||

| 3-D/VR Cinema Cameras | |||

| By End-User Industry | Feature Film Studios | ||

| Independent and Documentary Filmmakers | |||

| Broadcast and Live Production Houses | |||

| Advertising and Commercial Production Companies | |||

| By Distribution Channel | Direct Sales and Rental Houses | ||

| Online Retail/E-Commerce | |||

| Specialty Camera Stores | |||

| Authorised Resellers and System Integrators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current cinema camera market size and projected CAGR to 2031?

The cinema camera market stands at USD 0.51 billion in 2026 and is forecast to reach USD 0.72 billion by 2031, registering a 7.14% CAGR.

Which geographic region is expected to post the fastest growth through 2031?

The Middle East is projected to advance at an 8.14% CAGR to 2031, driven by Saudi Arabia's 40% cash-rebate scheme and large virtual-production investments.

Why are full-frame and large-format sensors gaining share over Super 35?

Full-frame and large-format sensors already hold 41.78% of revenue and are expanding at 7.94% CAGR because their shallow depth-of-field look helps streaming originals stand out.

What is the main operational hurdle slowing 8K adoption?

8K RAW produces 2.6 TB of data per hour, inflating cloud storage and workstation costs, which strains post-production budgets despite a 7.88% forecast growth rate.

How concentrated is the competitive landscape among camera makers?

The top five vendors, ARRI, Sony, Canon, Nikon-RED, and Blackmagic Design, capture about 68% of revenue, giving the space a mid-level concentration score of 6.

How is virtual production influencing new camera purchases?

More than 300 LED volumes now operate worldwide, so studios demand gen-lock-ready bodies that cut post schedules by up to 30%, accelerating replacement cycles.

Page last updated on: