3D Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

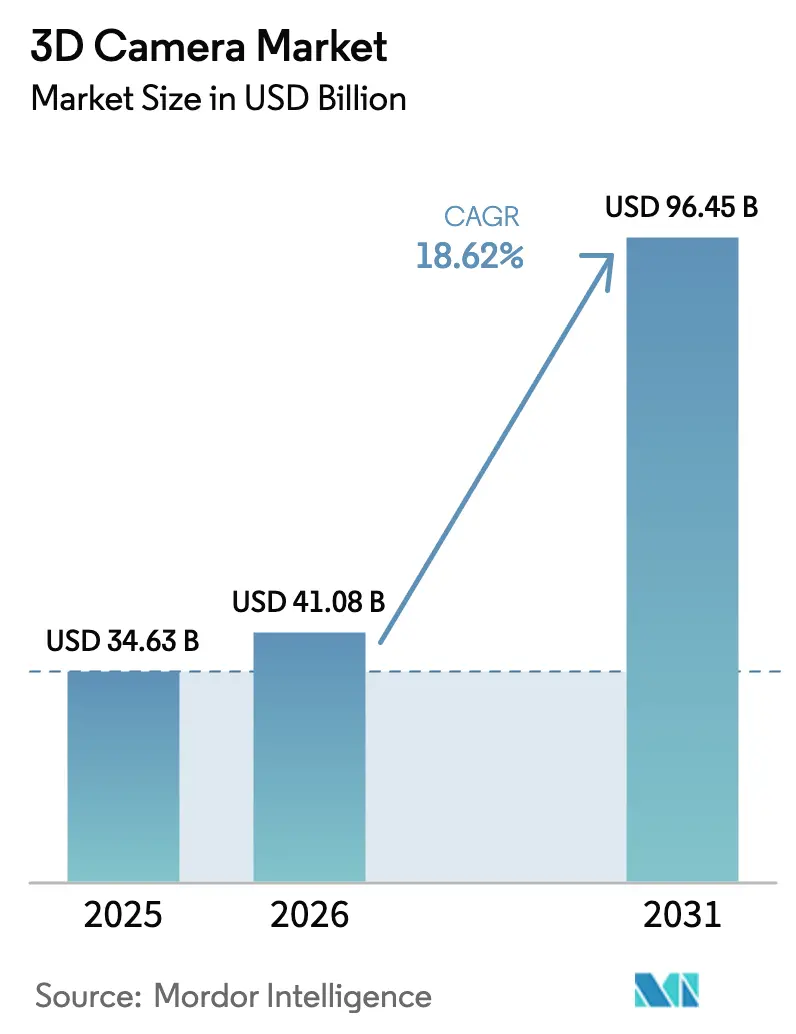

| Market Size (2026) | USD 41.08 Billion |

| Market Size (2031) | USD 96.45 Billion |

| Growth Rate (2026 - 2031) | 18.62% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Camera Market Analysis by Mordor Intelligence

The 3D camera market size is expected to grow from USD 34.63 billion in 2025 to USD 41.08 billion in 2026 and is forecast to reach USD 96.45 billion by 2031 at 18.62% CAGR over 2026-2031. Momentum stems from smartphone LiDAR integration, stricter European driver-monitoring rules, and factory automation that demands fast, precise depth capture. Asia-Pacific handset makers are embedding Time-of-Flight (ToF) sensors across premium tiers, while Gulf smart-city programmes order high-resolution 3D surveillance units. Falling bill-of-materials costs below USD 4 bring advanced depth modules into mid-priced devices, and industrial GigE interfaces unlock higher bandwidth for real-time quality checks. Competitive dynamics remain in flux as Sony tightens vertical integration, Intel spins out RealSense, and Orbbec scales service-robot supply.

Key Report Takeaways

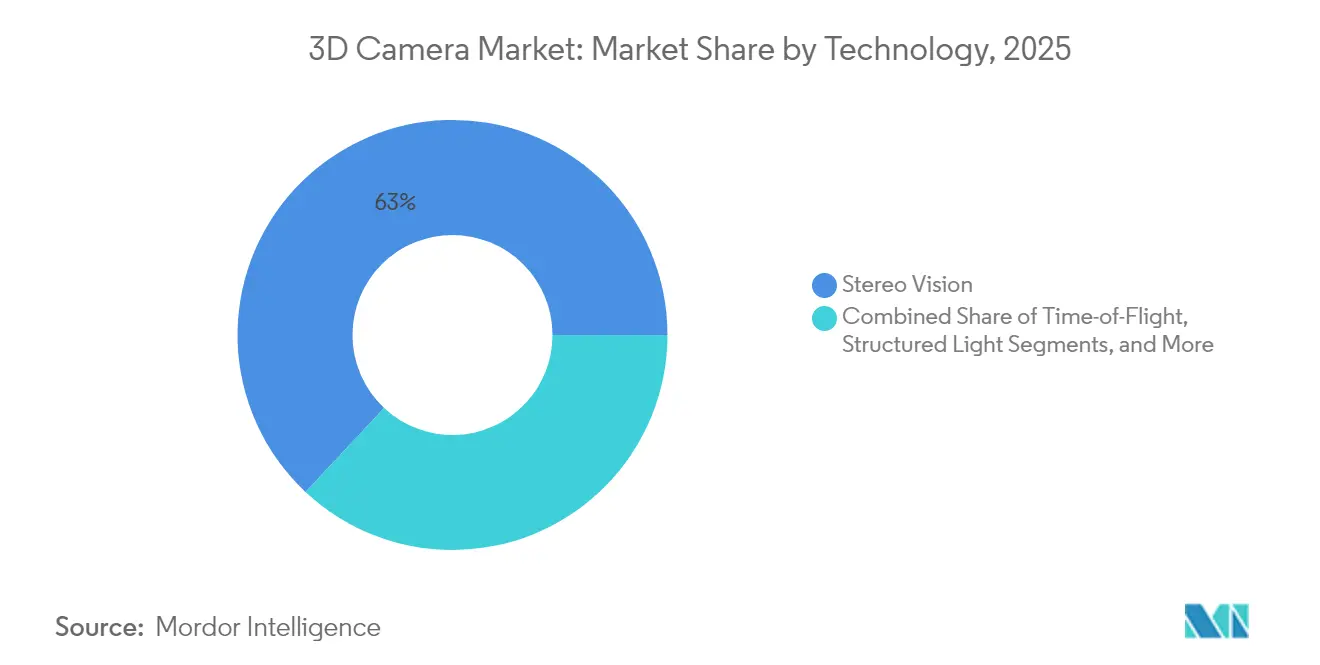

- By technology, Stereo Vision led with 63.02% of 3D camera market share in 2025, whereas Time-of-Flight is projected to expand at a 21.95% CAGR through 2031.

- By type, target-free systems captured 53.88% of the 3D camera market in 2025; the same category is forecast to advance at a 18.96% CAGR to 2031.

- By resolution, 8–16 MP sensors held 58.92% share of the 3D camera market size in 2025, while above-16 MP devices are forecast to grow at a 23.12% CAGR.

- By interface, USB/CSI accounted for 39.34% of the 3D camera market in 2025; GigE exhibits the highest projected CAGR at 23.75% through 2031.

- By application, professional cameras controlled 63.05% of the 3D camera market in 2025, yet smartphones and tablets show a 23.32% CAGR outlook.

- By end-use industry, consumer electronics led with 44.62% share of the 3D camera market size in 2025; automotive is set to climb at a 19.62% CAGR.

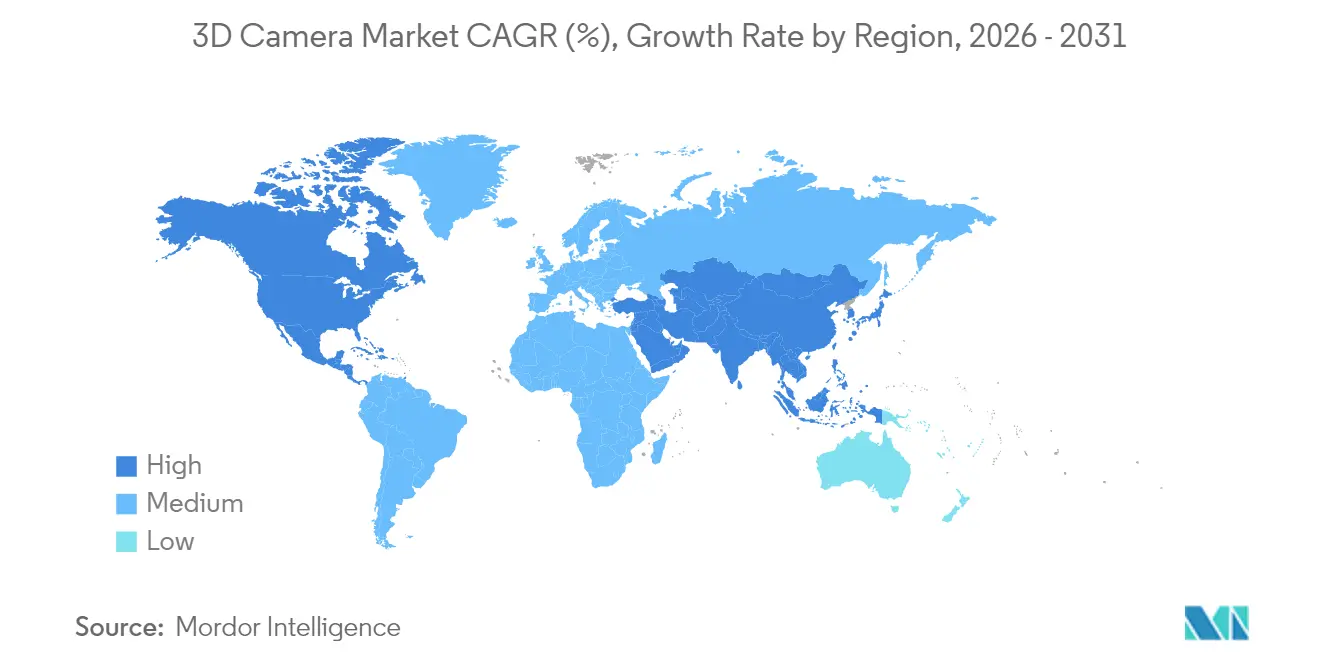

- By geography, Asia-Pacific commanded 38.07% of the 3D camera market in 2025, while North America is expected to post a 21.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of LiDAR-based ToF sensors into flagship smartphones | +2.1% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Automotive OEM mandates for in-cabin driver monitoring | +1.8% | Europe primary, expanding to North America | Short term (≤ 2 years) |

| Smart-manufacturing QA demand for 3D vision | +1.6% | China primary, expanding to APAC | Medium term (2-4 years) |

| Volumetric content production for XR headsets | +1.4% | North America primary, global expansion | Long term (≥ 4 years) |

| Gulf smart-city budgets for 3D surveillance cameras | +1.2% | GCC countries | Short term (≤ 2 years) |

| Falling BOM cost of CMOS depth modules | +0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration of LiDAR-based ToF Sensors into Flagship Smartphones

Apple’s LiDAR debut on the iPhone 12 Pro catalysed depth-sensing uptake, and the iPhone 15 series refines power efficiency for augmented-reality (AR) tasks.[1]Anita Chandran, “Lidar Innovations for a New Reality,” Electro Optics, electrooptics.com Samsung’s System LSI unit now supplies 200-MP image sensors to multiple brands, accelerating Asian OEM adoption. Depth data elevates autofocus and portrait modes, making computational photography a chief differentiator. Supply-chain realignment that shifts VCSEL sourcing from Coherent to Sony underscores vendor volatility. Balancing thermal limits and component costs in sub-premium phones will dictate medium-term penetration.

Automotive OEM Mandates for In-Cabin Driver Monitoring

Euro NCAP rules require driver-state sensing, pushing carmakers to integrate 3D cameras that detect distraction and impairment. Sony forecasts six-fold growth in automotive CMOS imagers, expecting 12 cameras per vehicle by FY 2028 compared with eight in 2024. Niche suppliers such as Smart Eye and Seeing Machines layer AI analytics onto depth input, creating a captive market despite economic cycles. Europe leads compliance, but U.S. regulatory alignment is likely, reinforcing short-term demand.

Smart-Manufacturing QA Demand for 3D Vision

China’s push for zero-defect factories strengthens demand for long-range, high-frame-rate ToF modules. onsemi’s Hyperlux ID captures objects at 30 m and 60 fps, meeting automotive and electronics assembly tolerances.[2]onsemi, “onsemi Debuts Advanced Depth Sensor for Industrial Applications,” investor.onsemi.com Operators gain cost savings by replacing manual inspection with automated defect detection. STMicroelectronics’ stacked-wafer VD55H1 sensor adds 200 MHz modulation for fast conveyor lines.[3]STMicroelectronics, “VD55H1 Product Page,” st.com Adoption follows a medium-term curve as plants retrofit lines and retrain staff.

Volumetric Content Production for XR Headsets

North American studios invest in volumetric stages as spatial-video revenues approach USD 22.5 billion by 2024.[4]Yili Jin et al., “From Capture to Display: A Survey on Volumetric Video,” arxiv.org Camera arrays must synchronise multiple 3D feeds with sub-millisecond latency, spurring demand for high-resolution, calibration-friendly systems. Neural-radiance-field rendering raises data-rate needs, linking hardware sellers with cloud GPUs. The timeline stretches long-term while compression standards and headset adoption mature.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of mass-market 3D content standards | -1.1% | Europe primary, global implications | Long term (≥ 4 years) |

| Thermal and power limits in sub-USD 300 phones | -0.8% | Global, especially emerging markets | Medium term (2-4 years) |

| Export-control curbs on optical chips | -0.7% | China primary, supply-chain spillover | Short term (≤ 2 years) |

| Stereo-vision re-calibration downtime | -0.5% | Nordic countries, industrial automation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Mass-Market 3D Content Standards

Fragmented EU technical protocols force creators to encode multiple volumetric formats, inflating production budgets and stalling investment in capture hardware. Dual-use export rules further slow knowledge exchange among developers. Without unified testing metrics, buyers hesitate, trimming the long-term growth outlook for the 3D camera market.

Thermal and Power Limits in Sub-USD 300 Phones

Budget handsets struggle to dissipate heat from continuous ToF operation. High current draw reduces battery life, compelling OEMs to throttle depth functions or omit them entirely. While silicon advances improve efficiency, cost-constrained designs will retain performance gaps, tempering mainstream uptake through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: ToF Sensors Challenge Stereo Vision Dominance

Stereo Vision held 63.02% of 3D camera market share in 2025 on the strength of low-cost dual-lens rigs. The segment suits professional DSLRs and industrial pick-and-place arms that prefer passive depth estimation. Time-of-Flight, however, is growing at 21.95% CAGR, enlarging the 3D camera market size for smartphones and driver-monitoring modules. Superior low-light performance and single-lens packaging underpin ToF’s rapid uptake. Structured-light remains essential for facial unlock and dental scanning, while emerging hybrid stacks blend ToF with stereo feeds for redundancy.

Manufacturers such as Infineon and pmdtechnologies showcase under-display ToF imagers that preserve bezel-less designs. onsemi’s indirect ToF roadmap extends maximum range to factory-floor distances, expanding industrial prospects. Stereo solutions still appeal in static-scene robotics thanks to lower power draw, yet the performance gap narrows each product cycle.

By Type: Target-Free Systems Enable Broader Applications

Target-free designs captured 53.88% of 3D camera market share in 2025 and are projected to log a 18.96% CAGR as plug-and-play expectations dominate consumer electronics. Eliminating calibration markers simplifies installation in smartphones, robots and smart-home devices, enlarging overall 3D camera market size. Target-based rigs survive in precision metrology, where reference patterns secure micron-level accuracy.

Roborock’s Qrevo Slim robot uses Infineon’s hybrid ToF imager to navigate tight furniture clearances without environmental stickers. Industrial adopters weigh the higher upfront accuracy of target-cameras against downtime from marker alignment. Advances in AI-driven self-calibration are set to narrow that trade-off.

By Resolution: High-Resolution Sensors Drive Premium Applications

Sensors in the 8–16 MP band controlled 58.92% of 3D camera market size in 2025, balancing throughput with detail. Above-16 MP devices are forecast to surge at a 23.12% CAGR as handset brands chase multi-camera computational photography. Samsung’s 200-MP supply deals illustrate the arms race to capture fine textures for AR overlays. Sub-8 MP modules persist in budget IoT units where cost and low bandwidth trump fidelity.

Higher pixel counts inflate raw data rates, spurring adoption of GigE and PCIe interfaces and on-device compression. STMicroelectronics employs stacked wafers and proprietary ISPs to curb die size while lifting frame rates. Industrial users embrace mid-tier resolutions to avoid bandwidth bottlenecks yet still meet tolerance specs.

By Interface: GigE Gains Ground in Industrial Applications

USB/CSI remained the top interface with 39.34% share of the 3D camera market in 2025, prized for plug-and-play links in tablets and embedded boards. GigE, however, is accelerating at 23.75% CAGR, propelled by smart-factory retrofits that require 100 m cable runs and deterministic transfer. CameraLink endures in ultra-high-speed inspection, while proprietary connectors serve niche robotics lines.

Factory engineers choose GigE Vision to harness existing Ethernet switches, slashing integration costs. Rising sensor resolutions and multi-camera arrays elevate throughput needs, driving the move from 5 Gb/s USB to 10 Gb/s and 25 Gb/s Ethernet. Consumer gadgets continue to rely on USB-C ports for cost efficiency.

By Application: Smartphones Disrupt Professional Camera Leadership

Professional rigs held 63.05% of 3D camera market share in 2025, essential for survey-grade mapping, VFX and metrology. Yet smartphones and tablets are expanding at a 23.32% CAGR, democratising depth sensing and growing the reachable 3D camera market size. Apple’s shift to Sony VCSELs underscores premium-tier dependence on reliable supply.

AR/VR headsets add volume as Meta, Sony and HTC refresh devices with inside-out tracking arrays. Robotics and drones embed depth units for autonomous navigation, and laptops include IR-based facial login for zero-trust security. Mass-market demand spurs component scale economies that reverberate into industrial sectors.

By End-Use Industry: Automotive Acceleration Challenges Consumer Electronics

Consumer electronics represented 44.62% of 3D camera market size in 2025 via handsets, tablets and gaming peripherals. Automotive demand is gaining at a 19.62% CAGR as driver-monitoring and parking assistance become standard. Sony plans to capture 43% of in-vehicle CMOS imager sales by 2026.

Industrial plants install 3D vision for surface-defect checks and pick-and-place robots, while security integrators deploy depth cameras to lower false alarms. Healthcare trials depth modules for patient fall detection, and entertainment houses capture volumetric actors for virtual production.

Geography Analysis

Asia-Pacific commanded 38.07% of 3D camera market share in 2025 thanks to China’s factory automation, Japan’s robotics and Korea’s handset giants. Government incentives drive local sensor fabs, though export controls on germanium and gallium raise price volatility. Orbbec’s 70% stake in China’s service-robot cameras shows the depth of regional specialisation.

North America is set to record 21.28% CAGR, buoyed by Euro-aligned safety mandates and XR content studios. Intel’s RealSense spin-off reveals a commitment to dedicated go-to-market models. Canada exploits mining automation, while Mexico’s vehicle exports incorporate driver-monitoring cams.

Europe grows steadily on the back of strong automotive tier-ones and industrial machine builders. Middle East & Africa adopt 3D vision in GCC smart-city grids, focusing on crowd analytics, whereas South America leans toward security and mining use cases amid fiscal constraints.

Competitive Landscape

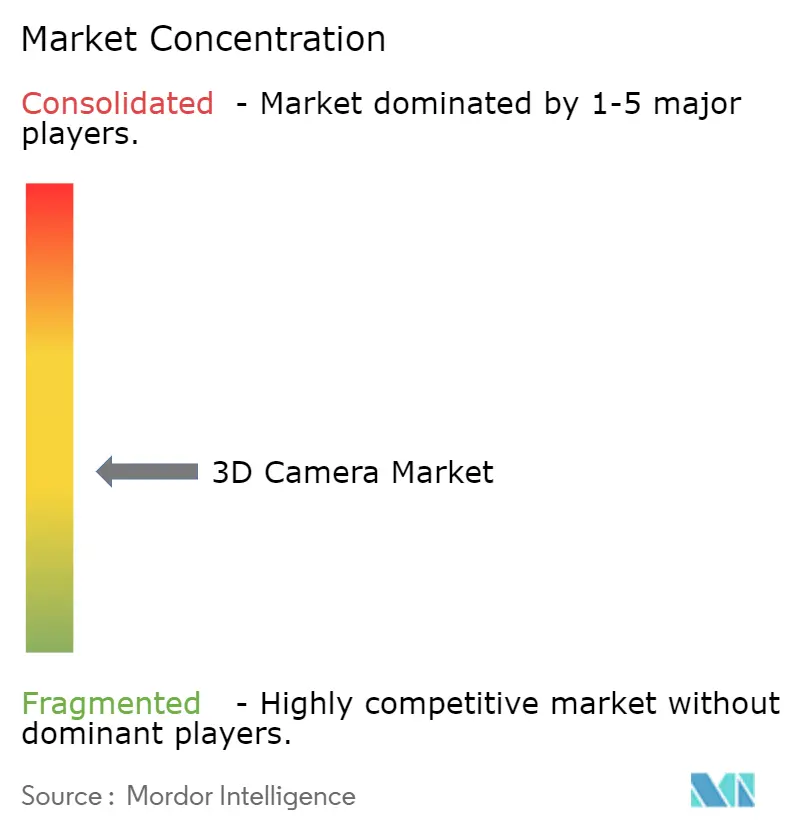

The 3D camera market is moderately fragmented. Sony’s Imaging & Sensing Solutions unit lifted FY 2024 revenue 14% and pairs proprietary CMOS arrays with AI edge chips for automotive clients. Canon funnels imaging IP into machine-vision modules for factories, and Apple integrates depth sensors across its device stack for ecosystem control.

Intel’s RealSense autonomy allows focused R&D while retaining Intel Capital funding, aiming at robotics and logistics verticals. Orbbec dominates Chinese service robots through price-performance optimisation and local support. Infineon and pmdtechnologies bundle sensors with ArcSoft middleware, lowering integration overhead for handset OEMs.

Strategic moves include onsemi’s iToF launch for long-range QA, Samsung’s push into 200-MP depth-ready imagers, and STMicroelectronics’ investment in stacked-wafer production to balance cost and throughput. White-space opportunities lie in ultra-low-power IoT, harsh-environment mining rigs and sub-USD 100 smart-home devices.

3D Camera Industry Leaders

Canon Inc.

Nikon Corporation

Fujifilm Holdings Corporation

Samsung Electronics Co., Ltd.

Sony Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: onsemi unveiled Hyperlux ID, a 30-m indirect ToF sensor for industrial automation.

- January 2025: Intel confirmed plans to spin off RealSense as a standalone company by mid-2025.

- January 2025: STMicroelectronics reported Q4 2024 revenue of USD 3.32 billion and outlined restructuring.

- September 2023: Roborock introduced the Qrevo Slim robot using Infineon’s REAL3 ToF imager.

Global 3D Camera Market Report Scope

3D camera is an imaging device that allows the perception of depth in images to replicate three dimensions as experienced through human binocular vision.

The 3D camera market is segmented by technology (time of flight, stereo vision, structured light), by end-users (consumer electronics, automotive, security and surveillance, aerospace and defense, media and entertainment, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (usd) for all the above segments.

| Time-of-Flight |

| Stereo Vision |

| Structured Light |

| Hybrid Multi-Sensor |

| Target Camera |

| Target-Free Camera |

| Less than 8 MP |

| 8 - 16 MP |

| Above 16 MP |

| GigE |

| CameraLink |

| USB and CSI |

| Other Interfaces |

| Professional Cameras |

| Smartphones and Tablets |

| Computers and Laptops |

| AR/VR Headsets |

| Robotics and Drones |

| Other Applications/Devices |

| Consumer Electronics |

| Automotive |

| Security and Surveillance |

| Industrial and Manufacturing |

| Media and Entertainment |

| Healthcare |

| Aerospace and Defense |

| Other End-use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South East Asia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Technology | Time-of-Flight | ||

| Stereo Vision | |||

| Structured Light | |||

| Hybrid Multi-Sensor | |||

| By Type | Target Camera | ||

| Target-Free Camera | |||

| By Resolution | Less than 8 MP | ||

| 8 - 16 MP | |||

| Above 16 MP | |||

| By Interface | GigE | ||

| CameraLink | |||

| USB and CSI | |||

| Other Interfaces | |||

| By Application/Device | Professional Cameras | ||

| Smartphones and Tablets | |||

| Computers and Laptops | |||

| AR/VR Headsets | |||

| Robotics and Drones | |||

| Other Applications/Devices | |||

| By End-use Industry | Consumer Electronics | ||

| Automotive | |||

| Security and Surveillance | |||

| Industrial and Manufacturing | |||

| Media and Entertainment | |||

| Healthcare | |||

| Aerospace and Defense | |||

| Other End-use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South East Asia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the 3D camera market?

The 3D camera market stands at USD 41.08 billion in 2026 and is projected to grow to USD 96.45 billion by 2031.

Which technology segment is expanding the fastest?

Time-of-Flight sensors are forecast to post a 21.95% CAGR, outpacing other depth-sensing approaches.

Why are automotive firms adopting 3D cameras?

Euro NCAP mandates driver-monitoring systems, pushing carmakers to fit 3D cameras that track distraction and drowsiness, thereby ensuring regulatory compliance.

How are falling component costs affecting adoption?

Sub-USD 4 depth modules lower the price barrier, enabling mid-range phones and smart-home devices to integrate 3D vision features.

Which region is expected to grow fastest through 2031?

North America shows the highest regional CAGR at 21.28%, driven by XR content production and automotive safety regulations.

What are the main restraints on market growth?

Lack of unified content standards, thermal limits in budget phones, and supply-chain risks from export controls are the primary hurdles identified for the next five years.

Page last updated on: