Space Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 6.32 Billion |

| Growth Rate (2026 - 2031) | 15.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Space Camera Market Analysis by Mordor Intelligence

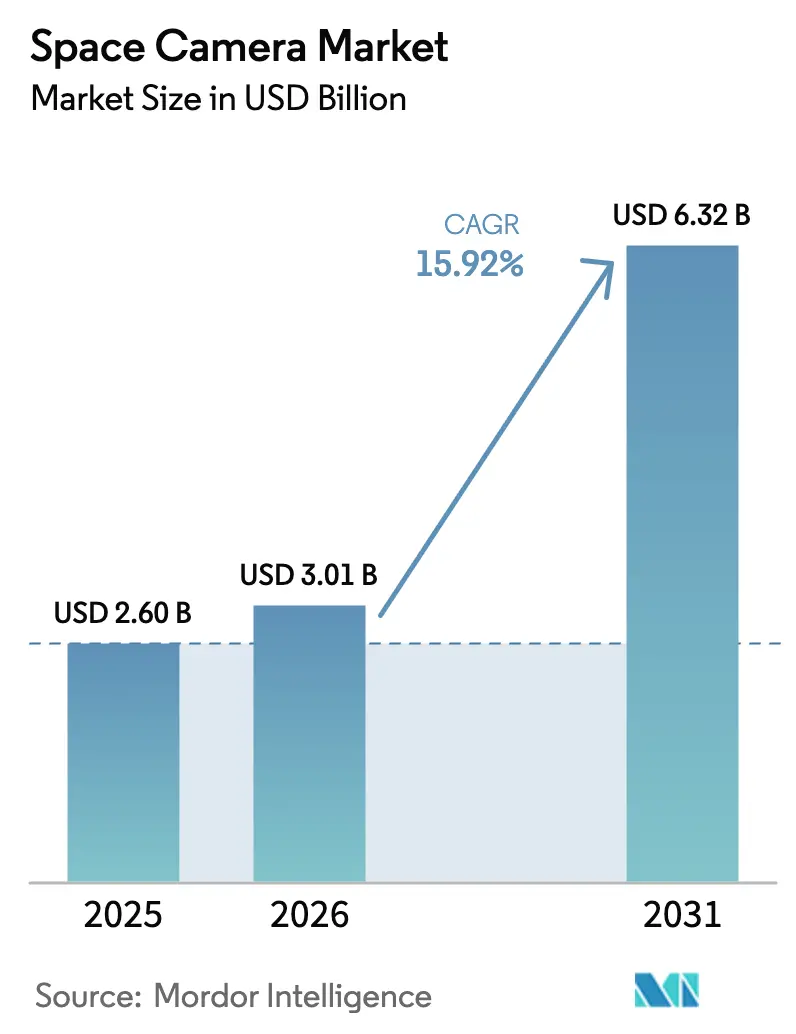

The space camera market size in 2026 is estimated at USD 3.01 billion, growing from 2025 value of USD 2.6 billion with 2031 projections showing USD 6.32 billion, growing at 15.92% CAGR over 2026-2031. Continued miniaturization, defense spending on orbital intelligence, and the scale-up of commercial constellations have converged to accelerate demand for higher-performance yet lighter imaging payloads. Venture investors poured more than USD 50 million into NewSpace camera start-ups in 2024, validating the commercial opportunity and shortening innovation cycles. Government programs added further lift by prioritizing persistent surveillance architectures that rely on multi-sensor satellites. At the same time, radiation-hardened CMOS advances, notably delta-doped designs and 4H-Silicon Carbide packaging, have tightened the cost-to-performance ratio while extending sensor longevity. Together, these forces keep the space camera market on a steep growth path despite export-control friction and on-orbit thermal constraints.

Key Report Takeaways

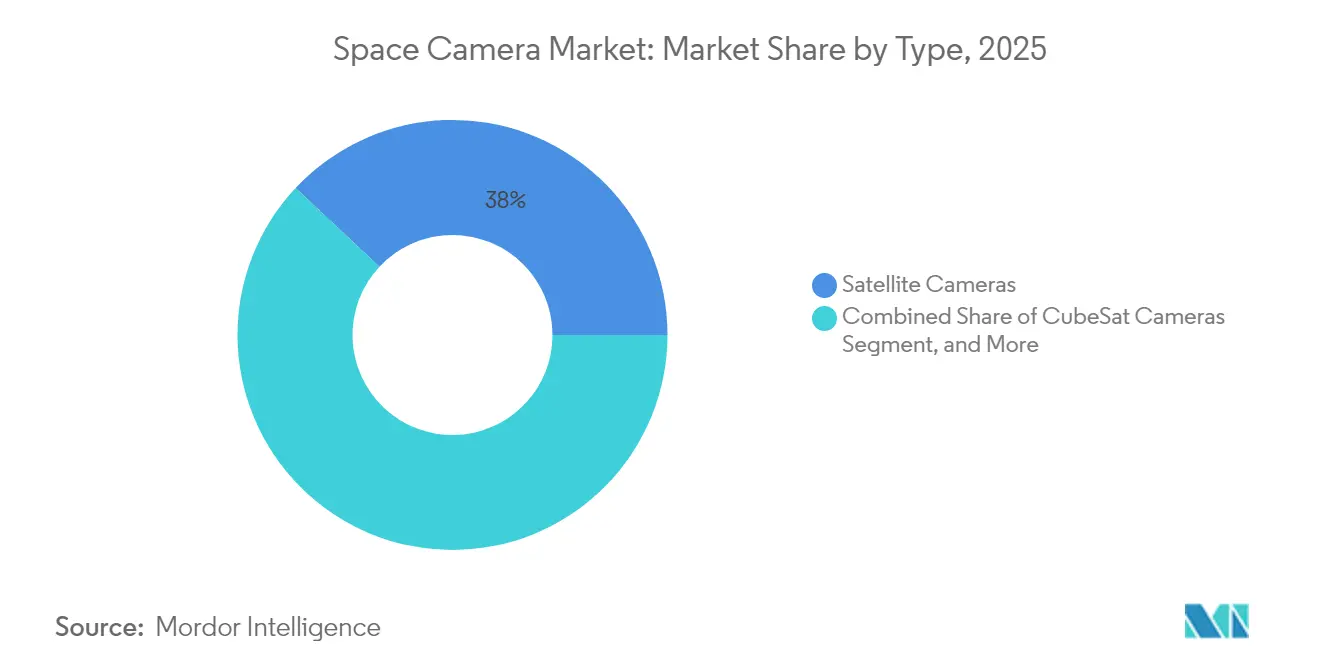

- By type, satellite cameras led with 38.02% revenue share in 2025 while CubeSat cameras recorded the fastest 17.54% CAGR through 2031.

- By technology, electro-optical systems held 40.62% share in 2025; hyperspectral cameras are forecast to advance at 16.21% CAGR to 2031.

- By sensor, CMOS accounted for 64.80% of the space camera market size in 2025 and is expected to expand at 16.74% CAGR through 2031.

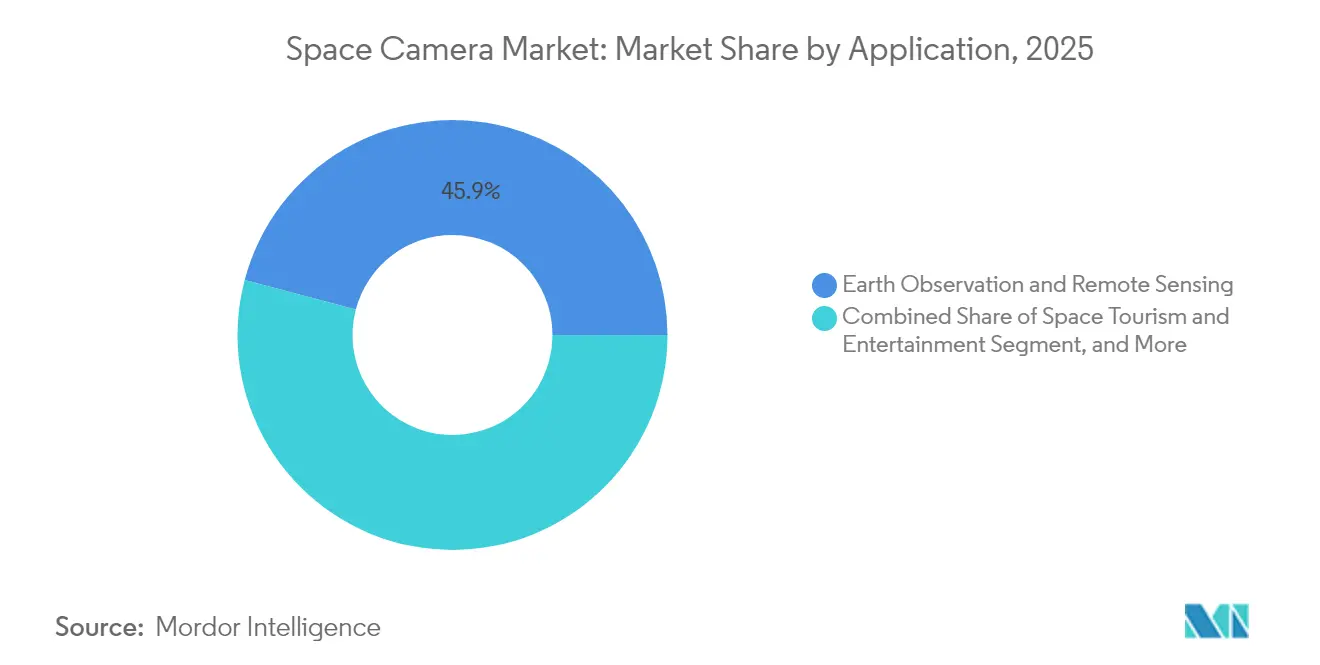

- By application, earth observation captured 45.88% share in 2025, whereas space tourism cameras are set to grow at 16.33% CAGR over the forecast horizon.

- By end use, government and military users commanded 52.10% share in 2025, while commercial enterprises will post an 17.88% CAGR through 2031.

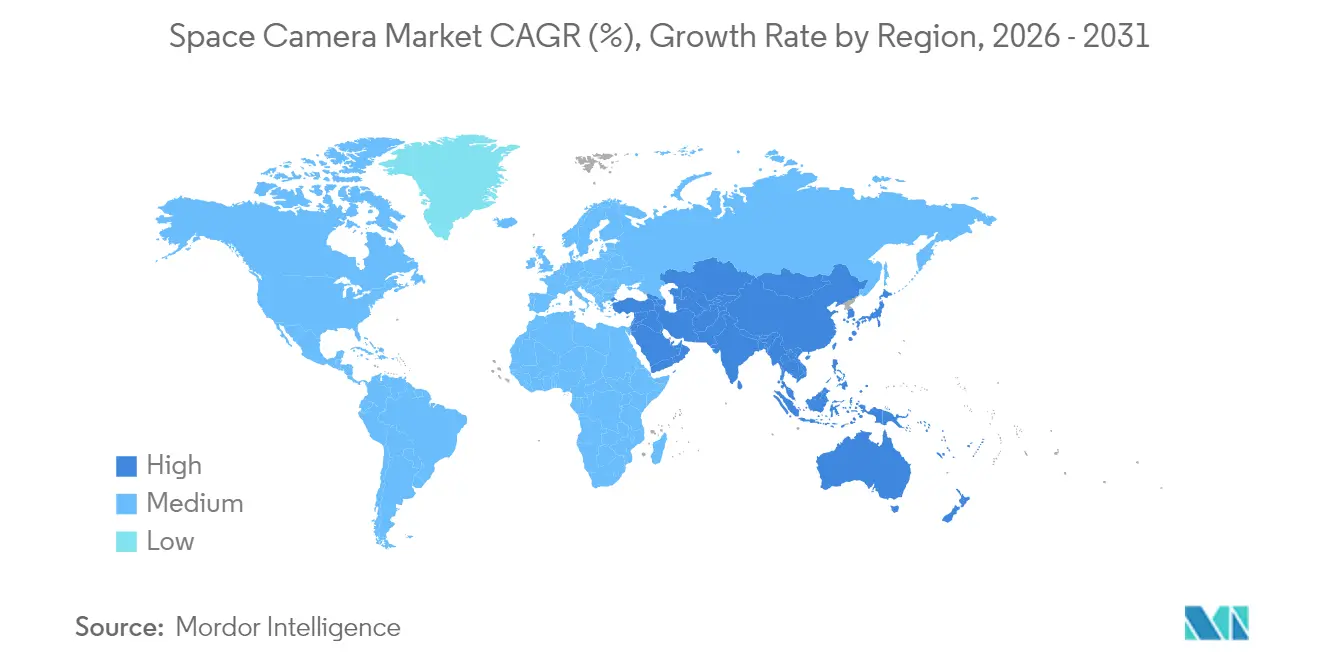

- By geography, North America led with 37.42% revenue share in 2025, while Asia-Pacific is forecast to expand at an 18.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Space Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid miniaturisation of satellite payloads reducing camera cost-to-performance ratio | +3.20% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing demand for real-time Earth analytics supporting high-refresh optical payload adoption | +2.80% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Defence urgency for space-based persistent ISR boosting high-resolution imaging payloads | +3.50% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Commercial constellations' shift to multi-sensor integration (EO-IR-MSI) amplifying replacement cycles | +2.10% | Global, led by North America and Europe | Long term (≥ 4 years) |

| NewSpace venture funding unlocking novel CubeSat camera form-factors | +2.30% | North America, Europe, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Low-orbit in-situ servicing missions creating demand for radiation-hardened onboard inspection cameras | +1.80% | North America and Europe primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Miniaturization of Satellite Payloads Reducing Camera Cost to Performance Ratio

Breakthroughs in component density now place 4K video sensors inside 3U CubeSat frames, slashing payload mass and launch fees by roughly 40% while keeping sub-meter resolution intact. Radiation-tolerant CMOS stacks built with delta-doped layers withstand harsh proton bombardment, extending in-orbit duty cycles without heavy shielding. The better economics encouraged operators to widen constellation footprints rather than raise individual pixel counts, unlocking new revisit-rate business models. Simera Sense’s EUR 13.5 million (USD 14.6 million) Series A in 2024 epitomized the capital flow into miniaturized hyperspectral cameras geared for mass deployment.[1]SpaceNews Staff, “NewSpace Venture Funding Trends in Satellite Imaging,” SpaceNews, spacenews.com Streamlined FCC approvals for standardized small satellites further lower entry barriers and keep the space camera market expanding at double-digit speed.

Growing Demand for Real-Time Earth Analytics Supporting High-Refresh Optical Payload Adoption

Commercial users in agriculture, logistics, and disaster management increasingly require sub-hour revisit rates, a target unreachable with legacy store-and-forward systems. Planet Labs scaled its fleet past 200 active satellites by 2024, each mounting a multispectral imager plus onboard processors that compress data and conduct edge analytics before downlink. Camera suppliers have responded with designs that embed AI accelerators close to the detector, reducing bandwidth by priority-flagging only the most valuable frames. ISO 19115 metadata alignment now guides procurement to ensure every image can flow into cross-platform analytics workflows. These upgrades shorten satellite replacement intervals from seven years to nearer three, lifting recurring revenues for space camera manufacturers.

Defense Urgency for Space-Based Persistent ISR Boosting High-Resolution Imaging Payloads

U.S. and allied militaries fast-tracked orbital ISR budgets after recent regional conflicts highlighted the value of wide-area, always-on monitoring. L3Harris won a USD 90 million order in 2024 to provide multi-sensor cameras for the next surveillance layer of the National Defense Space Architecture.[2]Defense News Staff, “L3Harris Secures Space Camera Contracts,” Defense News, defensenews.com Procurement rules specify sub-meter visible and thermal bands plus low-light imaging, driving unit prices higher than commercial counterparts yet locking in generous margins. Separate European and Indo-Pacific initiatives aim to cut dependence on foreign data feeds, fostering new sovereign opportunities for regional suppliers. Because platforms fall under ITAR, U.S. prime contractors retain an edge on domestic work, whereas European firms benefit from lighter export hurdles.

Commercial Constellations’ Shift to Multi-Sensor Integration (EO-IR-MSI) Amplifying Replacement Cycles

Maxar and others increasingly demand satellites that fuse electro-optical, infrared, and multispectral sensors into a single optical bench, maximizing data richness per kilogram. Retrofits on legacy spacecraft can only go so far, prompting aggressive upgrades across operational fleets between 2025 and 2028. Integrating multiple sensor stacks adds thermal load and complexity, but sophisticated fusion algorithms now offset those challenges with higher-margin analytics products. Constellation owners view the capex uptick as justified by the ability to cross-sell agricultural vigor indices, urban heat maps, and nighttime light economic proxies from one platform. ESA calibration frameworks for multi-sensor packages standardize procurement specs and accelerate adoption.[3]ESA Media, “Calibration Standards for Multi-Sensor Space Payloads,” European Space Agency, esa.int

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited on-orbit camera thermal management window constraining sensor longevity | -1.90% | Global, particularly affecting low-orbit missions | Medium term (2-4 years) |

| Export-control regimes (ITAR, EAR) delaying international camera supply chains | -2.30% | Global, with strongest impact on North America-Europe trade | Short term (≤ 2 years) |

| Space debris proliferation raising risk-adjusted insurance premiums for optical payloads | -1.40% | Global, concentrated in heavily trafficked orbital zones | Long term (≥ 4 years) |

| Persistent downlink bandwidth bottlenecks capping ultra-high-definition video adoption | -1.70% | Global, affecting all regions equally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited On-Orbit Camera Thermal Management Window Constraining Sensor Longevity

Spacecraft in low-earth orbit cycle through temperature swings near 200°C every 90 minutes, degrading sensor dark current and distorting optics over time. Active cooling devices, such as pumped-fluid loops or Stirling cryocoolers, mitigate heat but add mass and draw power that small buses cannot spare. Ball Aerospace delivered custom thermal regulators on the USD 498 million GOES-U payload in 2024, illustrating the cost premium attached to extended-life solutions.[4]Ball Aerospace Team, “GOES-U Payload Thermal Design,” Ball Aerospace, ball.com Mission planners now budget for shorter refresh intervals or accept periodic image-quality decay, both of which temper but do not derail the pace of space camera market growth.

Export-Control Regimes (ITAR, EAR) Delaying International Camera Supply Chains

The July 2024 U.S. rule change widened ITAR coverage to include select hyperspectral imagers, stretching license cycles by up to 12 months for foreign buyers. European and Asian programs increasingly seek non-U.S. alternatives to avoid uncertainty, fragmenting scale economies that could otherwise lower unit costs. For American vendors, domestic defense contracts offset lost export volumes, yet the net effect is slower topline progress than technical capability alone would permit. Conversely, European suppliers like Thales Alenia Space gain share on projects free of U.S. content. The policy landscape therefore shapes competitive positioning as strongly as sensor innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: CubeSat Cameras Drive Miniaturization Revolution

Satellite cameras held the highest 38.02% space camera market share in 2025, reflecting entrenched use in earth observation and defense programs. Nevertheless, the space camera market size for CubeSat platforms is on an 17.54% CAGR path to 2031 as launch rideshare economics reward lighter payloads. Miniature imagers now offer sub-meter ground sampling in 3U frames, spurring universities, start-ups, and even established primes to adopt distributed architectures.

CubeSat demand also benefits from faster refresh cycles: operators retire small units every three to four years, refreshing fleets with next-generation sensors that tack on infrared or hyperspectral channels. Meanwhile, fixed ground-based cameras and onboard spacecraft inspection systems remain niche but stable subsegments, catering to space-station maintenance and orbital-servicing robotics. Together these shifts keep the space camera market diversified across legacy geostationary missions and agile small-sat constellations.

By Technology: Hyperspectral Cameras Accelerate Agricultural Applications

Electro-optical units led with 40.62% share in 2025, underpinning most military and commercial mapping missions. Yet hyperspectral payloads will post the fastest 16.21% CAGR as farmers, miners, and carbon auditors require spectral fingerprints well beyond RGB. The space camera market size for hyperspectral platforms stood at a modest base but is anticipated to reach high-triple-digit million-dollar levels by 2031, capturing double-digit revenue slices in several verticals.

Recent sensor fabrication breakthroughs have shrunk 100-plus-band detectors into single-wafer CMOS stacks, cutting power draw by one-third. Edge-resident machine learning then parses vegetation stress or mineral composition before downlink, alleviating bandwidth choke points. Infrared and multispectral cameras continue to serve wildfire response and water-quality audits, yet hyperspectral’s richer data cube promises premium pricing for analytics-driven services.

By Sensor Type: CMOS Sensors Dominate Through Radiation Hardening

CMOS devices delivered 64.80% of the space camera market in 2025, up sharply from historical CCD dominance. Innovations including delta-doped epitaxy and 4H-Silicon Carbide covers have lifted total ionizing dose tolerance past 150 krad, closing the performance gap with specialized CCDs while keeping power budgets low. The space camera market size tied to CMOS sensors is forecast to advance at 16.74% CAGR, ensuring the architecture remains the default for small-sat fleets.

CCD imagers still serve astronomy or deep-space science where ultra-low noise overrides cost parameters, but volumes are comparatively minor. Over the mid-term, commercial semiconductor fabs are exploring 3D-stacked pixel arrays that promise further gains in dynamic range. As such, CMOS will likely own more than two-thirds of the space camera market share by decade-end.

By Application: Space Tourism Emerges as Growth Driver

Earth observation preserved 45.88% share in 2025 thanks to steady demand from agriculture, insurance, and environmental agencies. However, the rising cadence of commercial suborbital journeys has carved out a fresh revenue pocket. Blue Origin and Virgin Galactic now embed multiple 4K cameras inside crew cabins to livestream panoramic views for paying passengers. That niche is small today, but the 16.33% CAGR projected through 2031 turns it into a meaningful contributor as flight volumes climb.

Exploration missions still call for specialized imagers able to withstand lunar or Martian dust, while astronomy uses ultra-sensitive sensors to study faint cosmic phenomena. Military ISR, another evergreen pillar, maintains a mid-teens growth arc that balances cyclical defense budgets with ongoing geopolitical tension.

By End Use: Commercial Enterprises Accelerate Constellation Deployment

Government and military agencies held 52.10% of 2025 revenue, yet private-sector operators will expand faster at 17.88% CAGR. Companies such as Planet Labs, Maxar, and HawkEye 360 refresh fleets every few years to integrate multi-sensor packages and onboard AI, shortening camera replacement cycles. The resulting demand shift means suppliers must balance bespoke defense specs with volume-oriented commercial requirements.

Space agencies, universities, and research institutes together form a vibrant secondary market, leveraging lower launch costs to conduct targeted climate or astrophysics missions. Their collective share may remain below 15%, but their appetite for cutting-edge sensors spurs continuous R and D, indirectly benefiting broader commercial segments.

Geography Analysis

North America accounted for 37.42% of 2025 revenue, powered by sizeable Pentagon outlays and a deep bench of aerospace primes capable of end-to-end camera payload delivery. The region’s suppliers benefit from long-term ID/IQ contracts that lock in multiyear production runs, stabilizing cash flow amid cyclical procurement cycles. U.S. export regulations do curb overseas sales, yet domestic opportunities spanning defense, civil science, and the nascent space tourism sector provide ample headroom for growth.

Asia-Pacific will generate the fastest 18.20% CAGR as China, India, and Japan allocate larger budgets to commercial remote sensing and national security missions. Beijing-backed start-ups launched several 100-plus-satellite constellations in 2024, while ISRO’s commercial arm green-lit multiple public-private imaging ventures. These moves seed demand for both imported optics and home-grown sensors, positioning the region to rival North American output by the early 2030s.

Europe maintains a balanced profile, with ESA-coordinated programs reducing duplicative investments across member states. Companies like Thales Alenia Space, OHB, and Airbus Defence and Space leverage cooperative funding to deliver electro-optical and hyperspectral systems without ITAR strings, making them preferred suppliers to the Middle East, Africa, and parts of Asia. Although South America and Africa contribute modest volumes today, localized programs in Brazil, Argentina, and South Africa underscore a gradual broadening of geographic demand.

Competitive Landscape

The space camera market shows moderate concentration: the top five vendors L3Harris, Ball Aerospace, Teledyne, Thales Alenia Space, and Airbus Defence and Space collectively control just below 60% of global revenue. These incumbents leverage deep system-engineering expertise and established security credentials to secure high-value defense work. Yet NewSpace entrants such as Simera Sense, Kuva Space, and GOMSpace are scaling quickly on the strength of miniaturized products and agile production cycles.

Strategically, market leaders are pushing vertical integration by bundling optics, onboard processing, and downlink solutions under one contract, thereby capturing more of the project budget. L3Harris, for instance, clinched multiple >USD 90 million deals in 2024 for integrated EO-IR-MSI payloads, illustrating how comprehensive offerings command premium pricing. Emerging firms counter by specializing in narrow niches such as ultra-compact hyperspectral modules that legacy vendors cannot cost-effectively pursue.

Intellectual-property filings in radiation-hardened CMOS designs, thermal management innovations, and AI-on-edge firmware have risen markedly since 2024, indicating a race to secure technological moats. Export-control compliance remains a differentiator: U.S. suppliers enjoy home-market protection but face licensing drag abroad, while European counterparts use lighter regulations as a sales lever in third-country bids.

Space Camera Industry Leaders

Teledyne Technologies Incorporated .

Hamamatsu Photonics K.K.

Canon Inc.

L3Harris Technologies Inc.

Raytheon Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Canon Inc. signed an agreement with a European launch provider to supply modular cameras optimized for lunar surface logistics missions.

- October 2024: L3Harris Technologies received a USD 90 million contract from the U.S. Space Force for next-generation multi-sensor payloads supporting persistent surveillance.

- September 2024: Ball Aerospace completed delivery of imaging systems for the USD 498 million GOES-U weather satellite program.

- August 2024: Simera Sense closed EUR 13.5 million (USD 14.6 million) in Series A funding aimed at scaling production of CubeSat hyperspectral cameras.

Global Space Camera Market Report Scope

The Space Camera Market Report is Segmented by Type (Satellite Cameras, CubeSat Cameras, Onboard Spacecraft Cameras, Fixed Cameras, Portable Cameras, Others), Technology (Electro-Optical Cameras, Infrared Cameras, Multispectral Cameras, Hyperspectral Cameras, Others), Sensor Type (CMOS Sensors, CCD Sensors, Others), Application (Earth Observation and Remote Sensing, Space Exploration, Astronomy and Cosmic Studies, Space Tourism and Entertainment, Scientific Research, Military and Defense, Others), End Use (Government and Military, Commercial Enterprises, Space Agencies, Research Institutions), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Satellite Cameras |

| CubeSat Cameras |

| Onboard Spacecraft Cameras |

| Fixed Cameras |

| Portable Cameras |

| Other Types |

| Electro-Optical (EO) Cameras |

| Infrared (IR) Cameras |

| Multispectral Cameras |

| Hyperspectral Cameras |

| Other Technologies |

| CMOS Sensors |

| CCD Sensors |

| Other Sensor Types |

| Earth Observation And Remote Sensing |

| Space Exploration |

| Astronomy And Cosmic Studies |

| Space Tourism And Entertainment |

| Scientific Research |

| Military And Defense |

| Other Applications |

| Government And Military |

| Commercial Enterprises (Including Private Satellite Operators) |

| Space Agencies |

| Research Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Satellite Cameras | |

| CubeSat Cameras | ||

| Onboard Spacecraft Cameras | ||

| Fixed Cameras | ||

| Portable Cameras | ||

| Other Types | ||

| By Technology | Electro-Optical (EO) Cameras | |

| Infrared (IR) Cameras | ||

| Multispectral Cameras | ||

| Hyperspectral Cameras | ||

| Other Technologies | ||

| By Sensor Type | CMOS Sensors | |

| CCD Sensors | ||

| Other Sensor Types | ||

| By Application | Earth Observation And Remote Sensing | |

| Space Exploration | ||

| Astronomy And Cosmic Studies | ||

| Space Tourism And Entertainment | ||

| Scientific Research | ||

| Military And Defense | ||

| Other Applications | ||

| By End Use | Government And Military | |

| Commercial Enterprises (Including Private Satellite Operators) | ||

| Space Agencies | ||

| Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the space camera market in 2026?

The space camera market size reached USD 3.01 billion in 2026 and is projected to reach USD 6.32 billion by 2031, growing at a 15.92% CAGR during 2026-2031.

Which camera type is growing fastest?

CubeSat cameras exhibit the highest growth, expanding at an 17.54% CAGR thanks to miniaturization and lower launch costs.

Why are hyperspectral cameras gaining traction?

Hyperspectral sensors deliver detailed spectral data useful in agriculture, mining, and carbon monitoring, driving a 16.21% CAGR through 2031.

Which region grows the quickest?

Asia-Pacific leads with an 18.20% CAGR, fueled by major programs in China, India, and Japan.

Who holds leadership in defense imaging contracts?

North American primes such as L3Harris and Ball Aerospace dominate high-value defense deals owing to established security clearances.

What limits camera lifespan in orbit?

Severe thermal cycling in low-earth orbit degrades sensors, requiring expensive cooling solutions or more frequent satellite replacement.

Page last updated on: