Camera Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 43.03 Billion |

| Market Size (2031) | USD 52.91 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Fastest Growing Market | Middle East |

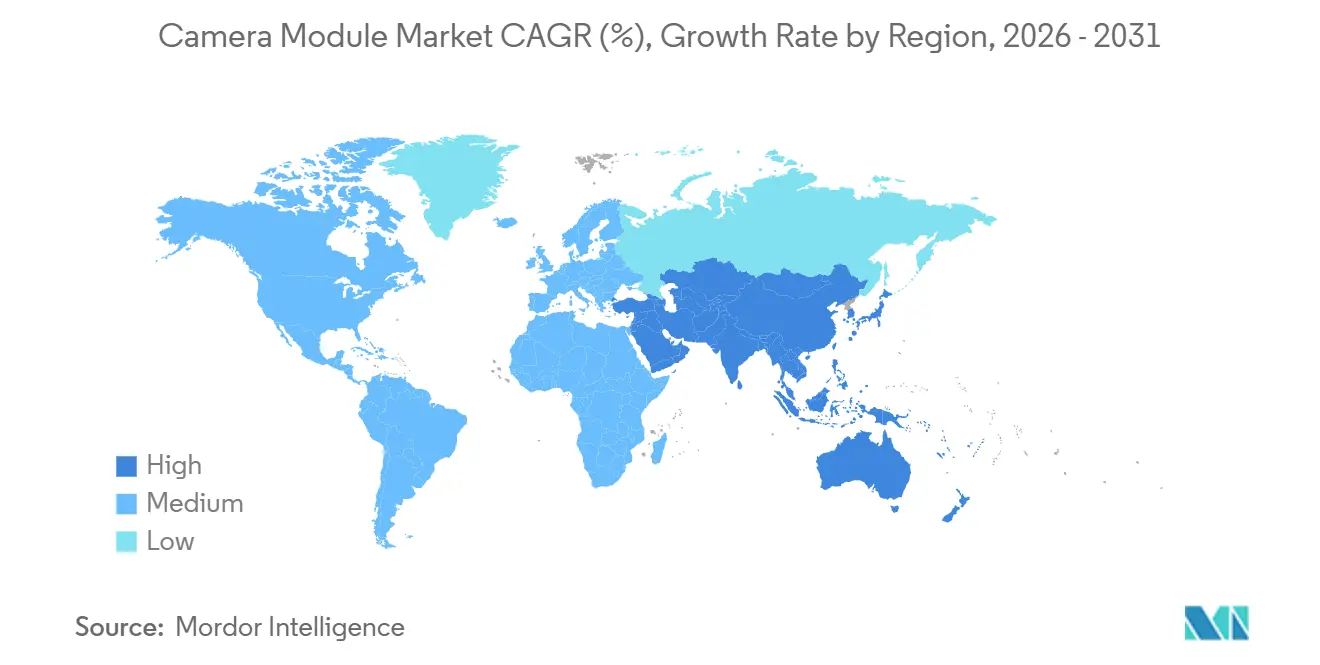

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Camera Module Market Analysis by Mordor Intelligence

The camera module market size is expected to grow from USD 41.12 billion in 2025 to USD 43.03 billion in 2026 and is forecast to reach USD 52.91 billion by 2031 at 4.22% CAGR over 2026-2031. This modest headline growth masks a shift from smartphone replacement cycles toward safety-driven automotive demand and edge analytics surveillance installations that carry richer bill-of-materials and longer design-in horizons. Consumer electronics still anchor volumes, but tier-one vehicle suppliers and smart-city contractors now set the technology roadmap. Vertically integrated players are winning design awards by bundling sensors, lenses, and actuators under one roof, while pure-play assemblers struggle with eroding gross margins. Sovereign industrial policies in Asia and the Middle East are localizing assembly, shortening lead times, and adding geopolitical complexity to an already stretched supply chain. At the same time, packaging advances such as flip-chip and wafer-level optics are shrinking z-height, opening the door to under-display and folded-optics form factors that command above-average selling prices.

Key Report Takeaways

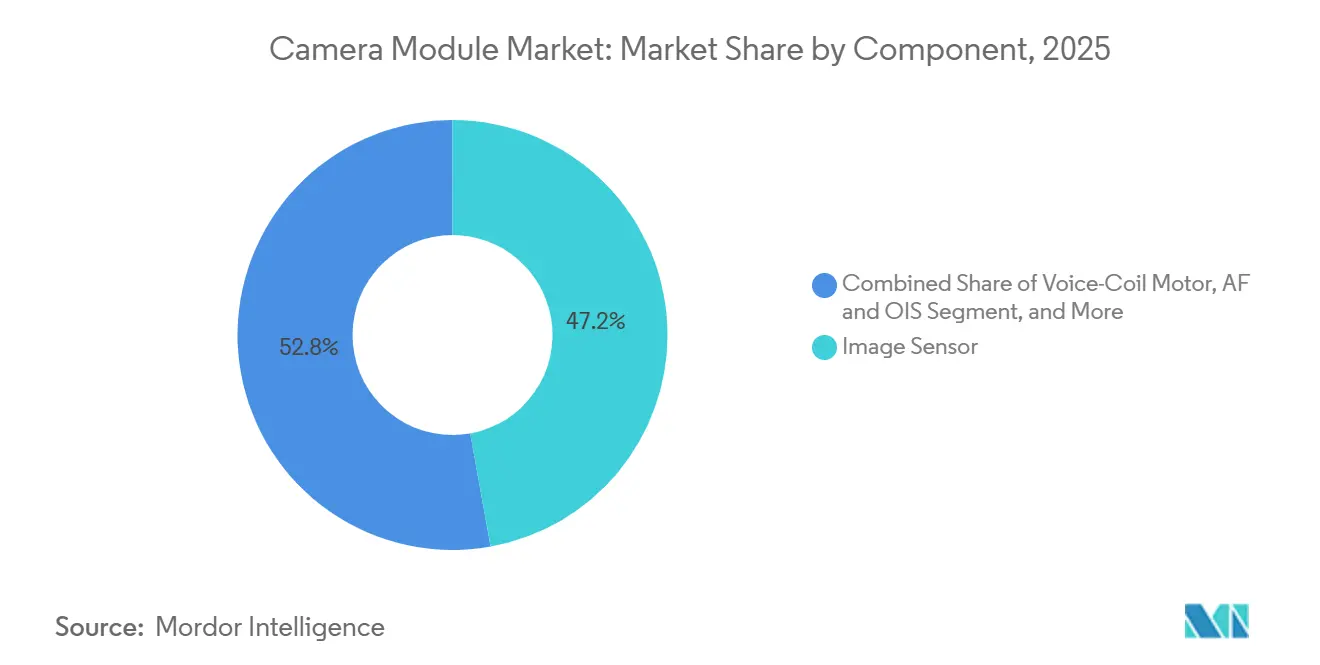

- By component, image sensors led with 47.17% revenue share in 2025, while voice-coil motor and optical image stabilization assemblies are projected to grow at a 5.07% CAGR to 2031.

- By sensor type, CMOS sensors commanded 89.22% of the camera module market share in 2025 and are expected to grow at a 4.73% CAGR over the forecast period.

- By resolution, the 8–13-megapixel segment accounted for 48.54% of the camera module market share in 2025, whereas modules above 13 megapixels are set to expand at a 4.83% CAGR through 2031.

- By focus type, autofocus modules held 61.32% of the camera module market share in 2025 and are on track for a 4.69% CAGR across the period.

- By manufacturing process, flip-chip and wafer-level packaging captured 56.91% share in 2025, with the same segment forecast to register the quickest 4.62% CAGR.

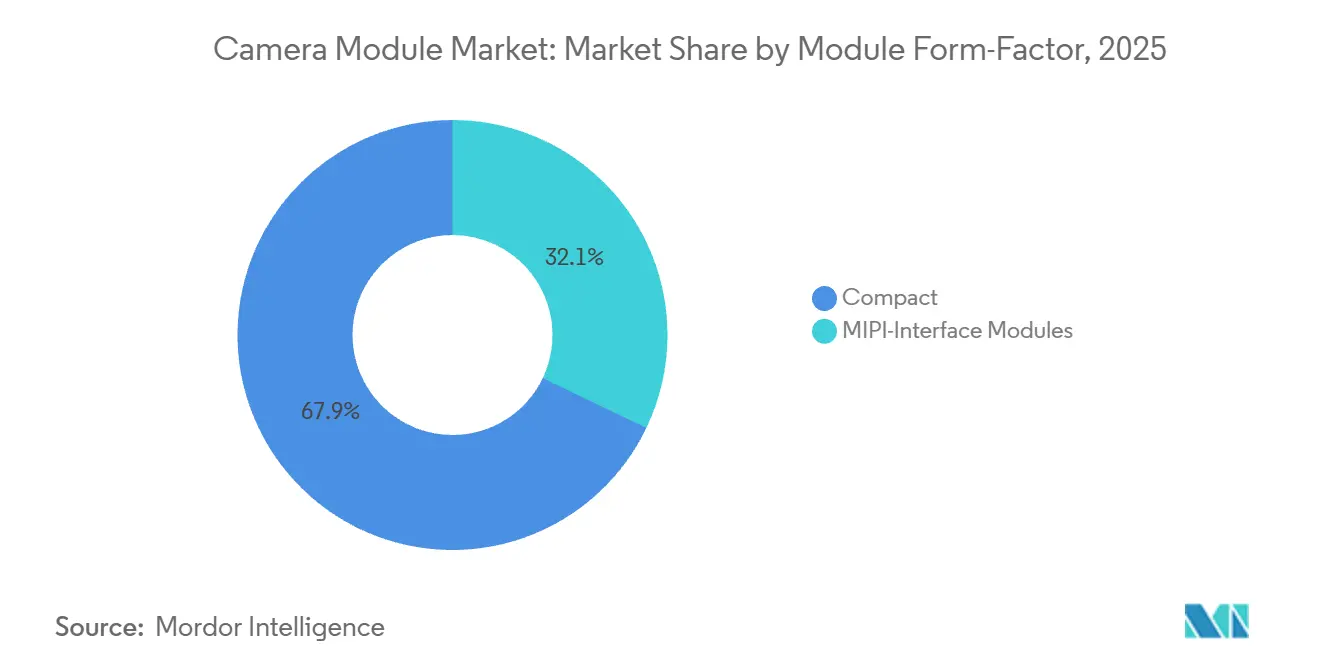

- By module form-factor, compact modules comprised 67.89% of revenue in 2025, while MIPI-interface modules are poised for a 4.67% CAGR.

- By application, consumer electronics accounted for 58.83% of the market in 2025, yet automotive modules are projected to record the highest CAGR of 5.46% through 2031.

- By geography, Asia-Pacific secured a 42.37% share in 2025, whereas the Middle East is expected to post the fastest CAGR of 5.21% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Camera Module Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-Camera Smartphone Adoption Exceeding Three Lenses in Chinese Flagships | +0.8% | Asia-Pacific core, spillover to Europe and Middle East | Medium term (2-4 years) |

| Rear-Visibility and ADAS Camera Mandates, FMVSS-111 and EU-GSR | +0.9% | North America and Europe, early adoption in Japan and South Korea | Long term (≥ 4 years) |

| AI-Enabled Edge-Analytics Surveillance Roll-outs in Middle-East Smart-City Projects | +0.6% | Middle East, with pilot expansions in Southeast Asia and Africa | Medium term (2-4 years) |

| Periscope or Folded-Optics Boom Elevating Lens Count per Module | +0.7% | Global, led by premium smartphone segments in Asia-Pacific and North America | Short term (≤ 2 years) |

| PLI Scheme-Driven Local Assembly of Modules in India | +0.5% | India, with secondary effects on South Asia supply chains | Medium term (2-4 years) |

| 3D or Depth-Sensing Demand for XR Headsets in United States and Korea | +0.4% | North America and Asia-Pacific, concentrated in consumer electronics hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Multi-Camera Smartphone Adoption Exceeding Three Lenses

Chinese flagship devices now integrate four or more discrete cameras, adding roughly 1.3 modules per handset. Xiaomi’s 17 Ultra debuted a 200-megapixel periscope alongside ultra-wide, wide, and macro units, each with its own autofocus chain.[1]Xiaomi Corporation, “Xiaomi 17 Ultra Product Specifications,” mi.com OPPO and vivo mirrored this approach in the Find X8 and X200 Pro series, raising average selling prices while maintaining shipment volumes. Depth-sensing time-of-flight modules, once confined to halo products, are now standard above USD 400 retail, unlocking new augmented-reality shopping features. The cumulative effect is incremental module demand despite a plateau in global smartphone replacements. Samsung’s All Lenses on Prism design shaved 22% off periscope z-height, enabling competitors to embed folded optics without sacrificing battery capacity.

Rear-Visibility and ADAS Camera Mandates

Safety regulations are transforming optional camera systems into base-grade hardware. In the United States, FMVSS-111 requires rear-view cameras on all light vehicles from model year 2026.[2]National Highway Traffic Safety Administration, “Federal Motor Vehicle Safety Standard 111 Rear Visibility,” nhtsa.gov The European Union General Safety Regulation applies similar pressure, mandating forward-facing cameras for lane-keeping and speed-limit assistance on new vehicle types from July 2024. Tier-one suppliers now integrate three to four cameras per vehicle, bundled with radar and lidar, raising module content to a forecast 3.8 units by 2030. Lexus models sold in North America will feature at least four cameras from 2026, accelerating the qualification cycle for automotive-grade components.

AI-Enabled Edge-Analytics Surveillance Rollouts

Smart-city programs in Saudi Arabia and the United Arab Emirates specify cameras with on-device neural processing to lower bandwidth and latency. NEOM’s greenfield buildout covers 26,500 sq km and has awarded early procurement to Hikvision and Dahua.[3]NEOM, “NEOM Smart City Infrastructure,” neom.com Dubai requires all cameras installed after January 2025 to support local object recognition in compliance with data-residency rules. Hardware that can execute convolutional neural networks at the edge carries a 40-60% cost premium over legacy analog devices, buoying the camera module market.

Periscope or Folded-Optics Boom

Folded optics deliver greater than 5× optical zoom in a sub-9 mm chassis. Samsung’s All Lenses on Prism architecture reduced the module height to 5.6 mm in the Galaxy S24 Ultra, prompting Apple to adopt a tetraprism in the iPhone 16 Pro Max with a 200 mm focal length. In Q3 2025, Largan Precision's shipments of periscope units surged by 68% year-over-year, fueled by a rising demand for camera stacks that are both thinner and more powerful.

Restraints Impact Analysis of Camera Module Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VCM Actuator Supply Constraints Post-2024 Earthquake in Taiwan | -0.5% | Global, with acute shortages in Asia-Pacific and North America | Short term (≤ 2 years) |

| Wafer-Level Optics Yield Loss in Under-Display Camera Modules | -0.3% | Asia-Pacific, concentrated in premium smartphone manufacturing hubs | Medium term (2-4 years) |

| Escalating Patent Litigation on Stacked CIS Architectures | -0.2% | Global, with litigation concentrated in United States, Europe, and Japan | Long term (≥ 4 years) |

| EN 303645 Cyber-Security Compliance Delays for Networked Modules in EU | -0.3% | Europe, with spillover effects on global IoT camera certifications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

VCM Actuator Supply Constraints Post-2024 Earthquake

The April 2024 Hualien earthquake damaged clean rooms at key Taiwanese actuator suppliers, doubling lead times for autofocus and optical image stabilization voice-coil motors. Samsung Electro-Mechanics and LG Innotek reported a 12% sequential decline in module shipments as they paid premium logistics costs to secure limited parts. Restoration reached 85% by late 2025, but OEMs have since dual-sourced from Japanese vendors to mitigate future shocks.

Wafer-Level Optics Yield Loss in Under-Display Modules

Under-display cameras achieve 62% pilot yields, compared with 92% for conventional modules, inflating costs by 2.3 times and limiting adoption to ultra-premium phones priced above USD 1,000. LG Innotek’s investor deck cited photolithography defects and die-singulation misalignment as persistent hurdles. Samsung's Galaxy Z Fold 6 showcased a compromise: its external camera produced softer selfies, which impacted the overall image quality and tempered consumer enthusiasm. This trade-off highlighted the challenges of balancing innovative design with performance expectations in the foldable smartphone market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Camera Module Market Segment Analysis

By Component:

Actuators Close the Value GapThe camera module market size for image sensors accounted for 47.17% of revenue in 2025, while actuators captured a smaller share but posted the strongest 5.07% CAGR through 2031. Sony’s stacked CMOS parts fetch premium pricing, but demand for dual-axis optical image stabilization actuators in periscope modules is narrowing the gap. Voice-coil motor volumes rose as every additional lens now ships with its own autofocus drive, and automotive programs specify ruggedized actuators rated for −40 °C to 105 °C. Lens sets remained the second-largest element, with glass-molded aspherics replacing plastic in high-temperature environments. Assembly services, though the smallest component share, deliver value in long-life automotive platforms where vibration damping and hermetic sealing outstrip consumer-grade requirements.

A shift in mix is visible across applications. Automotive cameras pay a 30% premium for high-dynamic-range sensors and global shutters, while consumer electronics gravitate toward pixel-binned back-side illuminated chips. STMicroelectronics and ON Semiconductor released 0.1 lux sensors for night-time driver assistance, raising average selling prices even when unit volumes stay modest. Meanwhile, pure-play assemblers face commoditization as flagship smartphone brands bring design in-house.

By Sensor Type:

CMOS Entrenches LeadershipCMOS technology accounted for 89.22% of 2025 sales and is forecast to grow at a 4.73% CAGR, crowding out charge-coupled devices in scientific niches. Deep-trench isolation, pinned photodiodes, and on-chip analog-to-digital conversion lifted sensitivity while cutting power draw, sealing CMOS dominance. Samsung’s 108-megapixel ISOCELL sensors and OmniVision’s staggered-HDR OV50K captured automotive awards, displacing legacy CCD units. In contrast, Teledyne’s ultra-low-noise CCDs survive in astronomy and lab instruments where pixel purity trumps frame rate.

Next-generation CMOS parts, now boasting global shutters and 16-bit dual-gain output—features that were once the hallmark of CCD—are poised to further erode the market share of CCD in the camera module arena. OEMs are increasingly favoring alternatives over CCDs, reserving the latter primarily for specialty imaging. This shift is driven by the compounded cost advantages and technological advancements that enhance both efficiency and performance.

By Pixel or Resolution:

High-Megapixel Growth Outpaces Mid-TierModules above 13 megapixels are expanding at a 4.83% CAGR, supported by periscope telephoto lenses and pervasive 4K video capture. Xiaomi’s 200-megapixel sensor bins to 12.5 megapixels for low-light shots yet retains full resolution for digital zoom, bridging marketing specs with real-world usability. The entrenched 8-13-megapixel class still accounts for 48.54% of revenue but faces erosion as entry-level smartphones leapfrog to higher resolutions. Security cameras are also being upgraded to 4K to meet municipal procurement rules for facial recognition, retiring 2-megapixel analog inventory.

Optical physics sets boundaries: f/1.8 lenses with 1.0 µm pixels hit diffraction limits past 108 megapixels, making further increases in resolution less practical without compromising image quality. Sony's IMX989, boasting a 1.6 µm pixel pitch at 50 megapixels, emphasizes per-pixel sensitivity over sheer pixel count, ensuring better performance in low-light conditions and enhanced image clarity. In the automotive realm, 8-megapixel sensors strike a balance between cost efficiency and functionality, offering sufficient resolution to recognize license plates from 50 meters. This configuration establishes a practical limit for mainstream vehicles, where affordability and performance must align.

By Focus Type:

Autofocus Extends LeadAutofocus systems held a 61.32% share in 2025 and are set to grow at a 4.69% CAGR as users expect instant focus across every lens. Closed-loop voice-coil motors with Hall sensors achieve sub-0.3-second locks, critical for video and burst photography. Corning's liquid-lens solutions offer a robust, solid-state focus for industrial applications, providing enhanced durability and precision. However, these solutions currently cater to a relatively small market segment, limiting their broader adoption.

Cost-sensitive or fixed-distance applications continue to rely on fixed-focus modules due to their simplicity and cost-effectiveness. Video doorbells, equipped with extended depth-of-field optics, achieve consistent clarity from the doorstep to the street without requiring any moving parts, ensuring durability and reliability. Similarly, driver-monitor cameras are designed to operate at a fixed distance of 0.8 meters, providing accurate monitoring without the need for adjustments. A minimal price difference of just USD 1.50-2.00 per unit further enhances the appeal of fixed-focus modules, making them a preferred choice for low-margin IoT devices where affordability and functionality are critical.

By Manufacturing Process:

Flip-Chip Shrinks Z-HeightFlip-chip and wafer-level packaging accounted for 56.91% of the market in 2025 and are expected to grow at a 4.62% CAGR as smartphones chase thinner profiles. Solder bumps replace bond wires, reducing module height by 0.5 mm and boosting signal integrity. Samsung Electro-Mechanics now co-packages the image signal processor and DRAM buffer, trimming board footprint by 30%. Wafer-level optics push size even lower but carry yield penalties that restrain scale-up.

Chip-on-board, at 43.09% share in 2025, remains preferred in vehicles where proven wire-bond reliability under extreme vibration wins over incremental space savings. STMicroelectronics showcased a remarkable one-million-hour mean time between failures for its automotive COB (Chip-on-Board) assemblies. This achievement highlights the company's commitment to reliability and innovation in automotive applications. The benchmark flip-chip, which represents a significant advancement in technology, is currently undergoing qualification to ensure its performance and durability.

By Module Form-Factor:

Compact Dominates, MIPI Gains in CarsCompact units captured 67.89% of 2025 shipments, embedded in almost every smartphone and tablet. They bundle the sensor, lens, and connector into a 10 mm-square package and meet handset makers’ integration requirements. The camera module market size for MIPI-interface modules was 32.11% in 2025 and will grow at a 4.67% CAGR as automakers standardize on the MIPI CSI-2 link, enabling 4K streams over 2-meter cables. Remote mounting lets cameras sit in mirrors or grilles while central processors reside in trunks, simplifying harness weight and cost.

Consumer electronics use compact modules for absolute thinness, whereas industrial vision alternates between the two depending on the robot arm's reach. Canon has unveiled a compact module, measuring just 8.5 mm square, that boasts a 48-megapixel sensor, all while keeping its height to a mere 5.2 mm. This development underscores the industry's ongoing push to minimize z-height, catering to the growing demand for smaller, high-performance imaging solutions in devices such as smartphones, drones, and other compact electronics.

By Application:

Automotive Becomes Growth EngineConsumer electronics accounted for 58.83% of 2025 revenue, but value growth now eclipses volume growth as brands add periscope and ultra-wide lenses to justify device upgrades. Automotive, starting from a smaller base, enjoys the fastest 5.46% CAGR as safety mandates lock in multi-camera arrays per vehicle. Security and surveillance benefit from analog-to-IP retrofits anchored in Middle Eastern smart-city builds. Medical imaging shifts to 4K endoscopes, while industrial robots adopt 3D depth modules for bin picking and safety zoning.

Tier-one suppliers, such as Bosch, have begun integrating forward-collision and traffic-sign recognition cameras into single modules. This innovation has enabled OEMs to reduce costs by 40% compared to using discrete units. Meanwhile, in the smartphone arena, average selling prices for modules under 13 megapixels dropped by 8% in 2025. This decline was driven by intense competition among Chinese assemblers vying for orders, which in turn squeezed margins for pure-play manufacturers to below 15%.

Geography Analysis

APAC Camera Module Market

Asia-Pacific commanded 42.37% of the camera module market share in 2025, powered by China’s clustering of sensor fabs, lens grinders, and assembly lines that condense design cycles. Sunny Optical, O-Film, and LuxVisions shipped more than 60% of global smartphone modules from plants within 500 kilometers of final assembly sites. India’s INR 73,000 crore Production-Linked Incentive scheme (USD 8.77 billion) is redirecting capacity to domestic players Dixon Technologies and Bhagwati Products, giving regional brands faster access to modules. Japan pivots toward automotive-grade sensors, while South Korea leverages vertical integration to bundle sensors and lenses for premium vehicle contracts.

GCC Camera Module Market

The Middle East, though small, is the fastest-growing region, with a 5.21% CAGR. NEOM and Dubai smart-city mandates for AI-ready surveillance hardware propel high-margin shipments. As Gulf states enhance surveillance at stadiums, transport hubs, and major public venues, the adoption of 4K, 120-fps facial recognition cameras will drive a surge in tender volumes. This expansion is part of broader efforts to strengthen security infrastructure and ensure public safety in high-traffic and sensitive areas.

The Americas, Europe and Africa Camera Module Market

North America leans heavily towards automotive and industrial sectors, driven by robust demand and innovation, while smartphone production has been offshored to other regions. In Europe, growth faces challenges as EN 303645 cybersecurity regulations delay IoT camera certifications, pushing certain rollouts to 2027 and impacting the pace of technological adoption. South America witnesses a rebound, supported by the recovery of vehicle production in Brazil and Argentina, which is further bolstered by improving economic conditions. Meanwhile, Africa, still a niche market, focuses primarily on the automation of South African mining operations, leveraging advancements in technology to enhance efficiency and productivity.

Regulatory Landscape

Regulation for camera modules is increasingly shaped by safety mandates, cybersecurity requirements, and trade controls that affect component sourcing and certification timelines. In automotive, the United States FMVSS-111 rear-visibility requirement applies to all light vehicles from model year 2026, while the EU General Safety Regulation (EU-GSR) mandates camera-enabled ADAS functions on new vehicle types from July 2024, raising the importance of automotive-grade validation, traceability, and long-term supply assurance.

For networked and surveillance endpoints, India’s MeitY STQC requirements for CCTV introduce hardware security and firmware integrity expectations that flow down to module vendors and ODMs selling into public-sector and smart-city deployments. In parallel, US compliance pressure spans procurement restrictions under NDAA Section 889 for certain camera suppliers and tighter supply-chain scrutiny under Section 5949. The US BIS also updated Export Administration Regulations in 2024 for specific cameras and imaging systems, adding licensing friction for cross-border shipments. Standards activity affects design and qualification as well, including China’s SAC GB/T 43063-2023 test methods for CMOS image sensors (effective since January 2024) and ongoing EU RoHS updates via amendments to Annex III exemptions that influence material selection and documentation for EEE shipments into Europe.

Value Chain Analysis

The camera module value chain runs from upstream silicon and optics through precision assembly and qualification, then into OEM integration across smartphones, vehicles, IoT, industrial vision, and medical devices. Image sensors remain the pivotal cost and performance driver, with supply power concentrated in a small set of advanced CIS vendors. Lenses and actuators (VCM, AF, OIS) add differentiation in periscope and ruggedized automotive designs, while flip-chip and wafer-level packaging shift more value toward advanced interconnect and optical alignment capabilities. Assembly and test are still highly concentrated in East Asia, typically colocated with handset and electronics manufacturing clusters to compress iteration cycles and manage yield.

Downstream, buying power varies by end market: smartphone OEMs push aggressive cost, lead-time, and form-factor targets, while automotive programs impose longer qualification cycles and tighter reliability specs. That raises the importance of process control, traceability, and stable multi-year sourcing. Recent supply-chain disruptions and capacity constraints have pushed more dual-sourcing and regionalization, with India’s PLI supporting local module assembly and global OEMs asking suppliers to diversify production footprints across Southeast Asia. Bottlenecks persist in high-precision alignment labor, actuator availability, and access to advanced sensor substrates and packaging lines, making vertically integrated suppliers and partners with proven manufacturing execution systems more competitive for automotive and AI-enabled surveillance bids.

Competitive Landscape

The top five suppliers, LG Innotek, Samsung Electro-Mechanics, Sunny Optical, O-Film, and Hon Hai Precision, held about a 55% share in 2025. Vertically integrated firms that master sensors, lenses, and actuators win automotive bids by offering turnkey stacks with guaranteed supply continuity. Patent estates around stacked CMOS and back-side illumination underpin royalty income and deter new entrants. Sony and Samsung cross-license to OmniVision and ON Semiconductor, avoiding litigation that could stall shipments in major jurisdictions.

Chinese assemblers face falling gross margins in the 8-13-megapixel segment as two-week lead-time commitments and price wars take their toll. Consolidation is likely among sub-scale firms that lack the capital for wafer-level optics or automotive qualification. Meanwhile, Bosch and Continental are backward-integrating camera lines to secure ADAS volumes, challenging traditional module vendors. White space remains in ruggedized subsea and aerospace imaging, where Teledyne and FLIR operate relatively unopposed.

In the tech arena, suppliers achieving near-punch-hole camera quality with under-display technology, or those offering sub-6 mm periscope modules and 140-dB HDR automotive sensors, are securing multi-year contracts at premium rates. These advancements cater to the growing demand for high-performance components in industries such as consumer electronics and automotive. Without continuous innovation, suppliers face the risk of being pushed down to the commoditized, low-resolution market, where competition is intense, and profit margins are significantly lower.

Camera Module Industry Leaders

LG Innotek Co. Ltd

Sunny Optical Technology Group Co. Ltd

Chicony Electronics Co. Ltd

Sony Group Corporation

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Camera Module Market Companies Covered in this Report

- LG Innotek Co. Ltd

- Samsung Electro-Mechanics Co. Ltd

- Sunny Optical Technology Group Co. Ltd

- O-Film Group Co. Ltd

- Hon Hai Precision Industry Co., Ltd.

- Chicony Electronics Co. Ltd

- LuxVisions Innovation Ltd, Lite-On

- Cowell E Holdings Inc.

- Sony Group Corporation

- OmniVision Technologies Inc.

- STMicroelectronics N.V.

- AMS Osram AG

- ON Semiconductor Corp.

- Panasonic Corp.

- Largan Precision Co. Ltd

- MINEBEA MITSUMI Inc.

- Canon Inc.

- Robert Bosch GmbH

- Continental AG

- Magna International Inc.

- Valeo SA

- e-con Systems Pvt Ltd

Market Opportunities and Future Outlook

Opportunities are emerging where camera modules combine higher bill-of-materials content with longer design-in cycles, particularly in regulated automotive sensing and in AI-capable surveillance tied to smart-city requirements. Automotive demand is reinforced by EU-GSR (from July 2024 for new vehicle types) and US FMVSS-111 (model year 2026), which elevate demand for qualified camera stacks, including higher dynamic range sensors, robust actuators, and standardized high-bandwidth interfaces such as MIPI CSI-2 for multi-camera architectures. In the Middle East, smart-city procurement is pulling in edge-analytics capable cameras, reinforced by Dubai requirements for cameras installed after January 2025 to support local object recognition aligned with data-residency rules.

On the supply side, assembly diversification and capacity additions outside China create whitespace for module vendors and EMS partners that can deliver stable yield and traceability for mixed consumer and automotive portfolios. Evidence of this shift includes Goertek Vina expanding camera production capacity at its Bac Ninh, Vietnam facility in April 2026, increasing output by 20 million units per year and scaling production lines from eight to 21. At the component level, continued sensor innovation supports module ASP resilience in premium tiers and multi-camera designs; Sony Semiconductor Solutions, for instance, announced the LYTIA 610 64-effective megapixel mobile CIS in June 2026, targeting autofocus and spatial-resolution improvements that translate into differentiated module designs in flagship devices.

Recent Industry Developments in Camera Module Market

- June 2026: Sony Semiconductor Solutions announced the LYTIA 610, a 1/2-type 64-effective megapixel CMOS image sensor for mobile devices featuring the RB2x2 On Chip Lens pixel structure. The release supports higher-performance smartphone camera modules by improving autofocus behavior and spatial resolution, reinforcing the premium sensor roadmap that anchors multi-camera handset stacks.

- December 2025: LG Innotek announced development of a next-generation under-display camera module for driver monitoring systems designed to be integrated behind a vehicle instrument cluster. Hiding the camera while maintaining driver monitoring functionality expands design options for OEM interiors and strengthens LG Innotek positioning in higher-value automotive sensing programs.

- February 2024: LG Innotek developed a high-performance heating camera module aimed at autonomous-vehicle applications, addressing performance degradation from condensation, frost, and low-temperature operation. Thermal management at the module level improves camera uptime in harsh conditions, which is a key requirement for ADAS and automated driving validation programs.

Camera Module Market Report Scope and Research Methodology

Market Definition and Coverage

The camera module market is counted as the revenue earned from complete camera modules that combine image sensors, lenses, and related parts into a ready-to-integrate unit shipped to device makers across end uses.

Scope exclusions: Standalone image sensors, loose lenses, and downstream image signal processors are excluded. We also avoid counting refurbished modules to keep the market view aligned with new device production cycles.

Segments Covered in This Report

- By Component

- Image Sensor

- Lens Set

- Camera Module Assembly

- Voice-Coil Motor, AF and OIS

- By Sensor Type

- CMOS

- CCD

- By Pixel or Resolution

- Up to 7 MP

- 8 - 13 MP

- Above 13 MP

- By Focus Type

- Fixed-Focus

- Autofocus

- By Manufacturing Process

- Chip-on-Board

- Flip-Chip/Wafer-Level Packaging

- By Module Form-Factor

- Compact

- MIPI-Interface Modules

- By Application

- Mobile and Smartphones

- Consumer Electronics

- Automotive

- Healthcare and Medical Imaging

- Security and Surveillance

- Industrial and Robotics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with setting the demand context and technology limits, then it is used to anchor the model to real shipment and adoption signals. We review public materials such as UN Comtrade trade flows for camera parts, International Telecommunication Union indicators for connected-device growth, and national statistics releases (including US Census Bureau and Statistics Korea publications) that help explain electronics output cycles.

To keep assumptions grounded, we also use sources such as IEEE and other peer-reviewed optics and imaging journals, patent databases for lens and actuator innovation trends, and industry association publications that discuss camera specifications and module integration. Company annual reports, investor presentations, and reputable business press are used to cross-check mix shifts across smartphones, automotive, and industrial uses. For gap areas like supplier footprint mapping or long-run financial ratios, we selectively reference paid subscriptions focused on company financials, patent analytics, and shipment-level import-export intelligence. These examples are not exhaustive, and many other public sources were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary conversations are used to test what the desk signals cannot fully explain, especially pricing movement, module content per device, and near-term ordering behavior. We spoke with stakeholders across the value chain, including component suppliers, module assemblers, device OEM teams, and distribution or channel participants, covering major producing and consuming regions so our assumptions are not shaped by a single geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 47% |

| Mid tier: 47% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 17% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where device production, installed base refresh, and trade-linked supply signals are reconstructed into module demand pools, then translated into value using realistic price bands. After that structure is in place, we corroborate it with selective bottom-up checks such as sampled supplier revenue splits, channel conversations on unit volumes, and ASP times volume spot checks by key end uses.

Key inputs that shape the model include smartphone shipments and camera count per handset, passenger-vehicle production and ADAS or surround-view penetration, industrial and security camera adoption indicators, average selling price changes by resolution and autofocus type, and regional manufacturing concentration that affects the shipment pathway. Where a clean roll-up is not possible, such as private suppliers that report limited detail, we handle the gaps using peer benchmarking, capacity-utilization signals, and conservative share ranges that are re-tested during interviews.

Forecasting uses scenario analysis supported by regression-style sensitivity checks, where variables like device shipment outlook, camera count trends, and ASP erosion rates are flexed together. The final forecast path is kept realistic by aligning inputs to what industry experts view as implementable within the next product cycles.

Data Validation & Update Cycle

Validation is done through stepwise checks that compare the model output against independent signals such as trade values, device shipment totals, and publicly discussed specification trends. When a region or end use shows an unusual jump, the drivers are revisited, assumptions are tightened, and targeted re-contacts are triggered to confirm whether a real shift occurred or the input was overstated.

Before sign-off, the work goes through internal analyst review so the arithmetic, unit conversions, and year-to-year logic are consistent. The report is refreshed annually, and interim updates are made when material events occur, such as major demand shocks or supply constraints. Right before delivery, we do a fresh pass to ensure the latest public indicators and interview learnings are reflected.

Mordor Intelligence's Camera Module Market Size Compared Against Other Published Estimates

Published market values for camera modules can look far apart because the scope lines are drawn differently and the pricing math is not always consistent across end uses. Differences usually come from what is counted as a module, which year is treated as the anchor, and whether the estimate is tied back to practical unit and mix checks.

In this market, the biggest gap drivers are whether standalone sensors and lenses are added into the same bucket, whether factory-gate pricing is used versus retail-linked values, and how fast ASP decline is assumed as resolution rises. Currency timing and refresh cadence also matter, since fast-moving smartphone cycles can change the mix within a year. A narrower count that stays at factory-gate revenue and keeps image signal processors outside the scope explains the lower 2026 value in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 43.03 B (2026) | |

| Industry Publisher A | USD 47.74 B (2024) | Uses a 2024 base year with a faster growth outlook, and the component scope appears broader, which can pull in adjacent camera part value beyond complete module assemblies. |

| Global Consultancy B | USD 58.84 B (2026) | Shows a higher 2026 value that likely reflects more aggressive end-use expansion and ASP assumptions, and may include wider component definitions or bundled content per device without tight unit-level cross-checks. |

The spread in the table is mostly explained by scope boundaries and how units and prices are connected to real device demand. Our approach stays traceable because the value is built from device-linked demand pools, checked with supply and trade signals, and then adjusted only when the interview evidence supports a change.

Key Questions Answered in the Report

What is the current size of the camera module market?

The camera module market size is USD 43.03 billion in 2026 and is projected to reach USD 52.91 billion by 2031.

Which segment is growing fastest in value terms?

Automotive camera modules show the quickest expansion, advancing at a 5.46% CAGR through 2031, fueled by safety regulations.

How dominant is CMOS technology over CCD in camera modules?

CMOS sensors hold about 89% share and are expanding, while CCDs remain confined to specialized scientific imaging niches.

Why are periscope modules important for smartphones?

Periscope or folded-optic designs provide ≥5× optical zoom without increasing handset thickness, supporting premium pricing.

Which region offers the highest growth potential after Asia-Pacific?

The Middle East is the fastest growing geography, forecast at a 5.21% CAGR due to large smart-city surveillance projects.

How are supply-chain risks being mitigated post the 2024 Taiwan earthquake?

OEMs are dual-sourcing voice-coil motor actuators and expanding capacity in Japan and India to dilute geographic concentration.

Page last updated on: