Construction Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

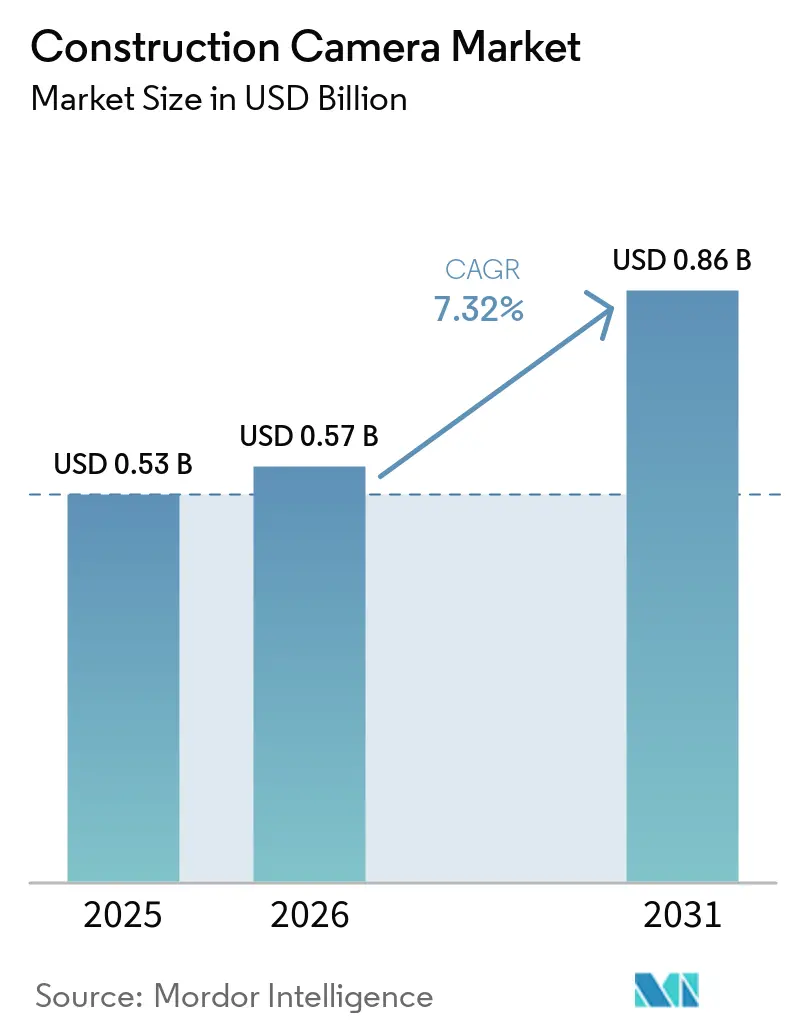

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 0.86 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

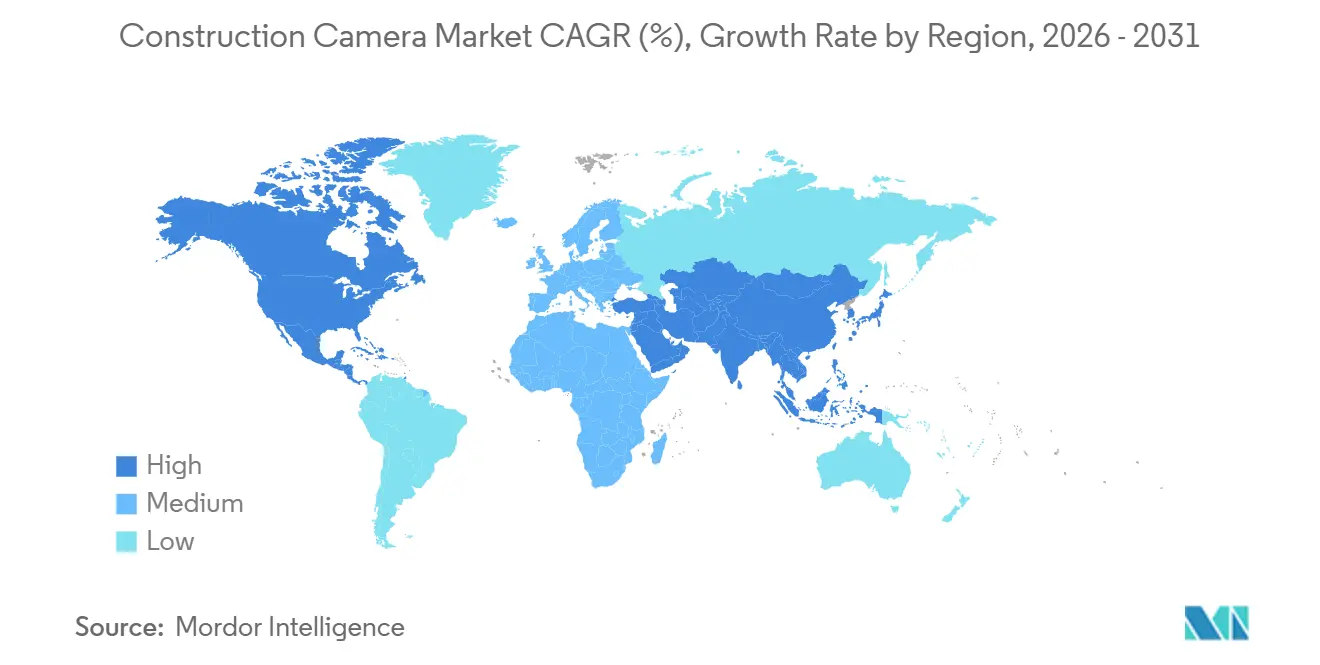

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Camera Market Analysis by Mordor Intelligence

The construction camera market size is expected to increase from USD 0.53 billion in 2025 to USD 0.57 billion in 2026 and reach USD 0.86 billion by 2031, growing at a CAGR of 7.32% over 2026-2031. Demand is rising because owners and insurers now treat continuous video archives as mandatory evidence of schedule adherence, safety compliance, and workmanship quality. Solar-powered rigs that run for weeks without grid access dominate power-source adoption, while 4G- and 5G-enabled units are displacing Wi-Fi meshes that once needed on-site routers. Camera vendors are shifting to software-as-a-service pricing, embedding feeds inside construction management platforms so field teams review imagery in the same workspace used for RFIs and change orders. Edge artificial intelligence that spots missing hard hats or fall risks is moving cameras from passive recorders to real-time safety guardians, and premium discounts offered by US insurers are shortening payback periods for most mid-size projects. Although higher hardware costs and stricter privacy rules temper adoption in some regions, ongoing megaproject funding across Asia-Pacific keeps the construction camera market on a double-digit growth trajectory.

Key Report Takeaways

- By power source, solar-powered systems accounted for 51.33% of the construction camera market share in 2025, and they are projected to expand at 9.53% CAGR through 2031.

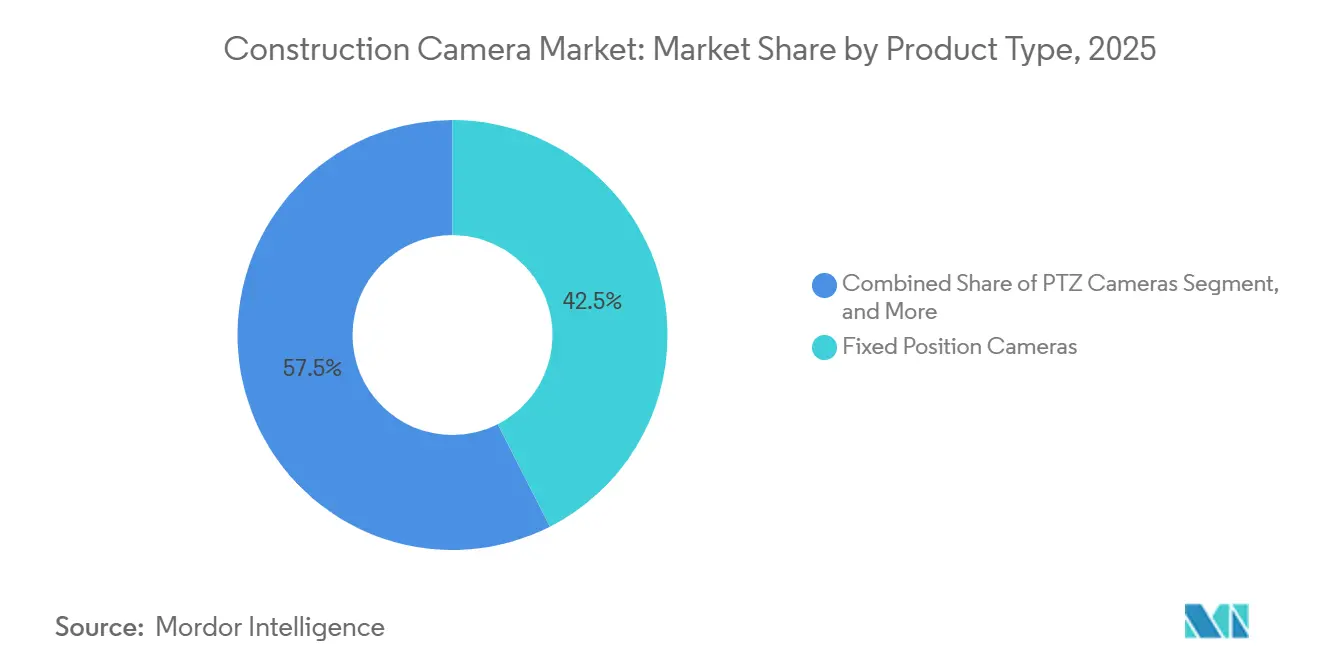

- By product type, mobile trailers and crane-mounted rigs are advancing at a 9.37% CAGR over 2026-2031, outpacing fixed-position cameras, which held 42.51% of revenue in 2025.

- By connectivity, 4G/5G solutions captured 57.39% of 2025 revenue and are forecast to grow at 9.76% annually, reflecting contractors’ move away from Wi-Fi.

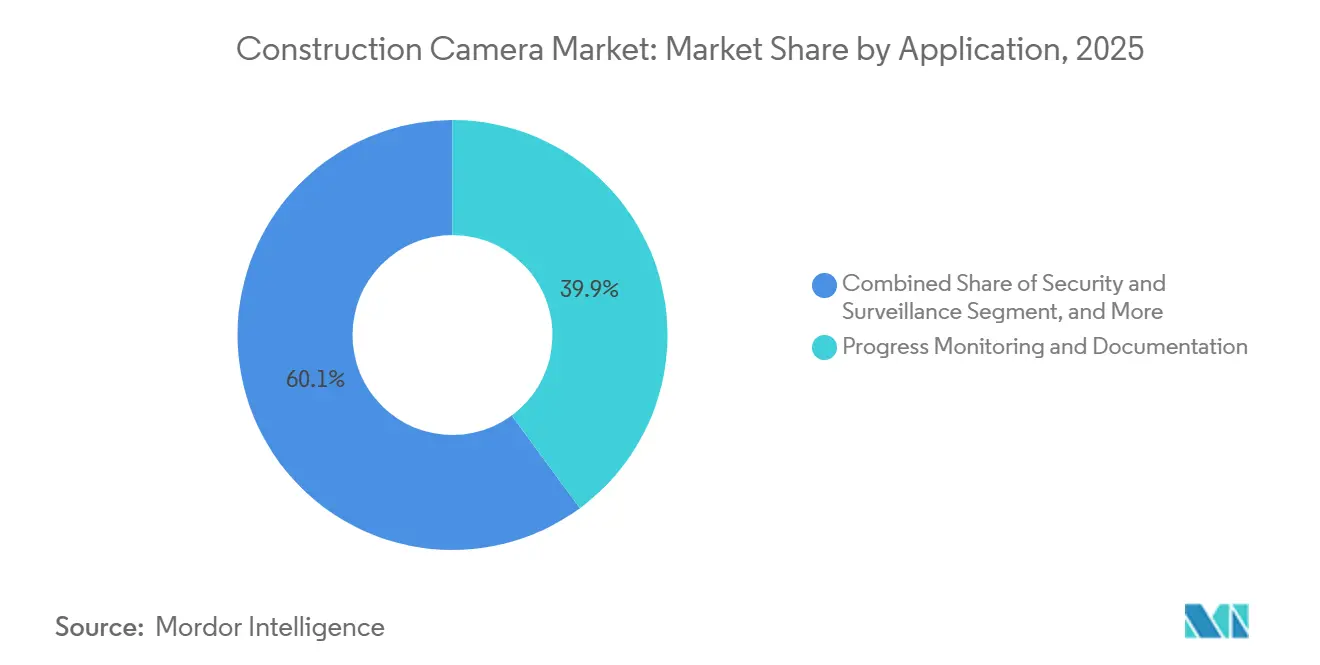

- By application, progress monitoring led with 38.13% of 2025 spending, while safety and compliance analytics is expected to deliver a 9.17% CAGR to 2031.

- By end user, general contractors accounted for 45.98% of 2025 sales, yet industrial EPC and energy firms are the fastest-growing segment, with a 9.39% CAGR during the forecast period.

- By geography, North America retained 38.83% of global revenue in 2025, whereas Asia-Pacific is poised for the quickest regional rise at 9.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Construction Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge AI Safety-Compliance Analytics | +1.8% | Global, early traction in North America and Europe | Medium term (2-4 years) |

| Integration with Procore and Autodesk BIM | +1.5% | North America and Europe, spreading to Asia-Pacific | Short term (≤ 2 years) |

| Solar-Powered Autonomous Deployments | +1.3% | Remote sites in Asia-Pacific, Middle East, and South America | Long term (≥ 4 years) |

| Growing Adoption of Remote Project Platforms | +1.2% | Global | Short term (≤ 2 years) |

| Insurance Premium Discounts | +0.9% | North America and Europe | Medium term (2-4 years) |

| High-Resolution Time-Lapse Marketing | +0.7% | Global with emphasis on North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Edge AI Safety-Compliance Analytics

Edge processors in cameras now flag missing PPE, proximity hazards, and restricted-zone intrusions in under 200 milliseconds. Early adopters cut OSHA-recordable incidents by 34% in 2025, helping contractors negotiate lower workers’ compensation premiums. Local inference preserves privacy because only incident metadata leaves the jobsite, satisfying California Assembly Bill 1221 and GDPR mandates. Uptake remains concentrated among steel erection and electrical trades that face higher severity risks, but declining chipset prices should extend the benefits to general trades within three years.

Integration with Procore and Autodesk BIM Workflows

Plug-and-play application programming interfaces allow superintendents to open a daily log, click a timestamp, and call up synchronized imagery without leaving their project dashboard. Construction firms using such integrations reported 23% lower rework costs and 18% fewer schedule overruns in 2026, according to Procore’s ROI study. As field crews align as-built imagery with federated BIM models, designers receive near-real-time alerts when installations deviate from tolerances, closing feedback loops that once spanned weeks.

Solar-Powered Autonomous Deployments

A 100-watt monocrystalline panel matched with lithium iron phosphate batteries now powers a 4G camera for up to 14 overcast days. The hardware eliminates the need for fuel deliveries and generator maintenance, cutting carbon emissions during remote road and bridge builds. Utility companies charge USD 15,000-30,000 per mile for temporary grid drops, so payback on solar rigs is often realized within a single construction season.[1]Michael Lee, “Solar PV Advances for Remote Construction,” energy.gov Government mandates on Saudi Arabia’s NEOM and other Middle Eastern gigaprojects institutionalize solar cameras for the next decade.

Growing Adoption of Remote Project-Management Platforms

Cloud suites such as Procore and Autodesk BIM 360 have become the dominant operating systems for large contractors. Embedding camera feeds inside those platforms halves project review meeting durations and reduces the separate photo-deck chore that drains superintendent time. As mid-market builders chase public bids that require digital handovers, vendors bundling ready-made integrations gain a critical edge in the construction camera market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Multi-Site Hardware Costs | -1.4% | Global, most severe in South America and Africa | Short term (≤ 2 years) |

| Stricter Privacy and Worker-Surveillance Rules | -1.1% | North America (California, New York) and GDPR-regulated Europe | Medium term (2-4 years) |

| Bandwidth and Cloud-Storage Expenditures | -0.8% | Regions with limited cellular infrastructure | Medium term (2-4 years) |

| Electronics-Tariff Volatility | -0.6% | North America with spillovers into Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Multi-Site Hardware Costs

Mid-size contractors managing 10-20 projects are required to allocate a significant investment of USD 50,000-150,000 to deploy multi-camera systems. While subscription-based models provide a more accessible entry point by reducing upfront costs, they often bind firms into long-term commitments, typically 36-month contracts. These contracts can add up to a total cost of USD 10,800 per unit, posing challenges for contractors if their project workloads decrease during the contract period. Additionally, external factors, such as the 16% import duty on imaging equipment in Brazil, further inflate costs, making procurement more expensive. In several African nations, limited access to equipment financing options, often available at high 12% APR rates, adds another layer of difficulty, delaying purchase decisions and hindering the adoption of advanced camera systems in these regions.

Stricter Privacy and Worker-Surveillance Regulations

California Assembly Bill 1221 and the European Union’s GDPR impose stringent requirements on the collection, storage, and use of images, mandating explicit consent, retention policies, and disclosure obligations for every image captured. To ensure compliance, contractors incur annual costs of USD 20,000 to 50,000 for legal reviews, workforce training, and the implementation of necessary protocols. Additionally, insurers continue to mandate the maintenance of five-year archives, compelling firms to adopt solutions such as anonymization techniques or on-premises data vaults. These measures introduce additional layers of complexity, which can delay procurement decisions and slow down the adoption of imaging technologies, even in regions that are otherwise prepared for camera deployments.[2]European Commission, “Guidelines on GDPR Video Compliance,” ec.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobility Drives Adoption on Vertical Builds

The construction camera market size is by product type, with fixed-position units accounting for 42.51% of revenue. Contractors choose these low-cost models for highways and flat industrial sites where a single vantage point covers months of work. Yet on skyscrapers and bridge pylons, crews reposition cranes weekly, and fixed units lose sightlines. Mobile trailer and crane-mounted rigs, therefore, grow at 9.37% annually, outpacing the overall construction camera market. One mobile PTZ can replace several static units, reducing data plan usage and truck rolls. However, increased motor complexity raises maintenance, especially in dusty Gulf deserts or Arctic winds.

Mobile solutions also unlock premium pricing through advanced analytics. Vendors bundle pan-tilt-zoom robotics with edge AI modules that recognize formwork progression floor by floor, feeding earned-value metrics into scheduling software. Rental fleets expand because owners prefer off-balance-sheet equipment that arrives pre-configured with cellular packages. As megaproject pipelines thicken in Asia-Pacific and the Middle East, demand for easily relocated rigs cements the product-type shift over the forecast horizon.

By Power Source: Solar Systems Consolidate Majority Control

Solar installations commanded 51.33% of the power-source segment in 2025, giving the category the highest construction camera market share at present. Rising conversion efficiencies now reach 22%, and lithium iron phosphate batteries lengthen runtime, driving a 9.53% CAGR projection that outstrips AC-powered alternatives. Extending grid service still costs USD 15,000-30,000 per mile, so the total cost of ownership favors solar when jobsites move every six months. Cellular throttling tech patented in 2025 cuts image bitrate under low-battery states, preserving uptime without new panels.

Battery-only and hybrid systems are suitable for demolition and site prep contracts lasting under 90 days, where panel amortization is unrealistic. In urban infill, AC-powered PoE cameras remain viable because temporary service already exists for trailers and tower cranes. Overall, solar’s expanding reliability and compliance with carbon-reduction targets in public bids assure its position as the long-term backbone of the construction camera market.

By Connectivity: Cellular Becomes the Default Uplink

The connectivity segment illustrates how reliability trumps pure bandwidth cost. Cellular links accounted for 57.39% of revenue in 2025 and are forecast to accelerate at a 9.76% CAGR through 2031. Verizon and AT&T now sell construction-specific plans with guaranteed uplinks and priority access during emergencies, eliminating the IT overhead of monitoring routers or mesh nodes. PoE and Ethernet remain the cheapest per gigabyte but rely on permanent fiber trunks, rarely installed during early earthworks.

Wi-Fi mesh networks are declining as contractors recognize that interference within steel frames erodes video quality. Private 5G has emerged as an enterprise differentiator. It supports real-time safety analytics with latency under 20 milliseconds, letting AI algorithms halt lifts when workers enter exclusion zones. Although initial carrier setup fees are steep, large general contractors amortize the spend across dozens of active projects, confirming cellular as the strategic option in the construction camera market.

By Application: Safety Analytics Rises From Niche to Necessity

Progress monitoring accounted for 38.13% of spending in 2025, as it remains essential for owners to maintain a chronological archive of project developments. This segment remains a critical component for tracking construction progress and ensuring transparency in project timelines. However, safety and compliance analytics emerged as the fastest-growing segment, with a 9.17% CAGR, driven by increasing regulatory requirements for proactive hazard mitigation. The adoption of Edge AI technology that anonymizes faces has enabled continuous monitoring without violating privacy regulations. Additionally, insurers now recognize metadata alerts as valid evidence of near-miss interventions, further supporting the segment's growth. Security applications also remain significant, particularly in scenarios where copper theft and vandalism pose risks to project schedules. Furthermore, value-added marketing videos have gained traction as an additional use case for construction cameras.

Developers are increasingly embedding high-resolution time-lapse videos into investor dashboards, reducing inquiry overhead and enhancing presales efforts. These time-lapse videos provide stakeholders with a clear and engaging visual representation of project progress, fostering greater confidence and interest among potential investors. As cameras evolve into multifunctional devices, the construction camera market is benefiting from broader budget allocations across various departments, including safety, quality assurance, and sales. This diversification of use cases has further solidified the importance of construction cameras in modern project management.

By End User: Industrial EPC and Energy Firms Spur Future Growth

General contractors captured 45.98% of sales in 2025 because they write most purchase orders, making them the primary decision-makers in the procurement process. Industrial EPC (Engineering, Procurement, and Construction) firms and energy developers, however, are experiencing the highest growth, with a 9.39% CAGR. This growth is driven by the increasing complexity and scale of projects such as LNG terminals, solar farms, and offshore wind arrays, which require strict adherence to multiple regulatory oversight regimes. Operators in these sectors must visually document critical processes, including weld procedures, hydrostatic tests, and commissioning steps, to ensure compliance and accountability.

In addition, owners in the higher education and healthcare segments are increasingly mandating the use of cameras as a prerequisite for bidding on projects. This requirement shifts the cost burden upstream to contractors but ensures deeper market penetration for camera vendors. Furthermore, government agencies, such as the California Department of Transportation, have implemented specific mandates requiring 4K time-lapse evidence for all projects exceeding USD 50 million. These regulatory and institutional requirements are solidifying construction cameras' role as essential tools, embedding them as non-negotiable line items in project budgets. This trend is driving a sustained and durable adoption curve in the construction camera market.

Geography Analysis

North America accounted for 38.83% of global revenue in 2025, sustained by insurer premium credits that cut builders’ liability costs by up to 25%. US megaprojects like the USD 5.9 billion Gordie Howe International Bridge deploy dozens of mobile PTZ rigs and benefit from private 5G backbones for real-time feed delivery. Canada’s Trade Diversification Corridors Fund requires time-lapse documentation on federally financed roads and ports, creating a pipeline of camera tenders. Mexico follows with near-shoring industrial plants that must meet US export-control audits and, therefore, install continuous visual monitoring from day one.

Asia-Pacific is forecast to post the highest CAGR of 9.57% as governments allocate multibillion-dollar budgets for transport corridors, underwater tunnels, and smart-city districts. China’s USD 42 billion urban modernization program ties funding to visual proof of anti-corruption safeguards. India’s Brahmaputra tunnel and Dhubri-Phulbari Bridge embed camera clauses into EPC contracts to satisfy National Highways Authority quality protocols.[3]National Highways Authority of India, “Quality-Assurance Protocols,” nhai.gov.in Japan’s earthquake reconstruction guidelines mandate cameras on all seismic retrofits, while South Korea pilots BIM-linked video overlays that shorten punch-list cycles. These policies embed long-term demand into the construction camera market.

Europe balances opportunity with compliance friction. GDPR rules limit footage retention to 30 days unless tagged to incidents, pushing vendors to offer anonymization services. The United Kingdom’s Building Safety Act requires digital twins for high-rise assets, turning cameras into lifelong facility management tools. In the Middle East, sovereign-funded cities like NEOM require solar-powered cameras across thousands of square kilometers. Etihad Rail’s USD 11 billion network mounted 60 units along remote desert trackage, demonstrating how thermal extremes accelerate demand for ruggedized rigs. South America and Africa trail because of import tariffs and high borrowing costs, yet concession models for toll roads are beginning to state camera deliverables, planting early seeds for growth.

Competitive Landscape

The top five suppliers, EarthCam, OxBlue, Sensera, TrueLook, and Evercam, dominate the market, making the field moderately concentrated. EarthCam’s ninth-generation platform integrates seamlessly with Procore, tagging photos by work breakdown codes, which strengthens vendor lock-in for large enterprise accounts. Sensera’s adaptive bitrate patent significantly reduces solar downtime by 40%, while OxBlue markets crane-mounted rigs that move vertically as cores rise, catering to high-rise construction projects.[4]OxBlue Corporation, “Crane-Mounted Camera Systems,” oxblue.com Evercam, on the other hand, provides GDPR-compliant storage solutions that automatically blank faces and erase footage after 30 days, a critical feature for compliance in continental Europe.

Emerging startups such as Forsight AI and Digital Eagle are introducing edge-compute modules that can attach to any camera body, enabling local detection of PPE infractions. While hardware remains relatively commoditized, the development of robust software ecosystems and carrier relationships demands multi-million-dollar investments, creating significant barriers to entry for new players. Vendors are shifting their focus from merely selling camera feeds to delivering measurable outcomes, such as reducing injuries and minimizing project delays, with pricing models now aligned to the savings realized by clients.

Regional specialists are carving out niches to address specific needs, further diversifying the construction camera market. For instance, ultra-low-power Arctic kits are tailored for extreme cold environments, while autonomous trailer fleets are designed to serve remote Australian mining camps. These specialized solutions highlight the growing demand for customized offerings that address unique operational challenges, ensuring the market continues to evolve and expand to meet diverse requirements.

Construction Camera Industry Leaders

EarthCam, Inc.

OxBlue Corporation

Sensera Systems, Inc.

TrueLook, Inc.

Evercam Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Verizon added millimeter-wave 5G coverage to three US megaproject corridors, lifting guaranteed uplink speeds to 100 Mbps for real-time AI video analytics.

- February 2026: Evercam released a GDPR-ready auto-redaction tool that blurs faces on-device before footage reaches the cloud, easing compliance audits in EU member states.

- October 2025: EarthCam introduced its ninth-generation Procore integration, cutting image sorting time by 70% for enterprise contractors.

- September 2025: Verizon expanded its private 5G construction network to 12 additional US metro areas.

Global Construction Camera Market Report Scope

The Construction Camera Market comprises the global ecosystem of hardware, software, and services dedicated to capturing, transmitting, storing, and analyzing visual data from construction sites through fixed and mobile camera systems. These solutions are designed to enable continuous or periodic site monitoring, improve project transparency, enhance security, and support data-driven decision-making across the construction lifecycle.

The Construction Camera Market Report is Segmented by Product Type (Fixed Position Cameras, PTZ Cameras, 360°/Panoramic Cameras, and Mobile Trailer and Crane-Mounted Cameras), Power Source (AC-Powered Systems, Solar-Powered Systems, and Battery-Only/Hybrid Systems), Connectivity (4G/5G Cellular, Wi-Fi/Mesh, and Wired Ethernet/PoE), Application (Progress Monitoring and Documentation, Security and Surveillance, and Marketing and Stakeholder Engagement), End-User Industry (General Contractors, Owners/Developers, Government and Infrastructure Agencies, and Industrial EPC and Energy Firms), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fixed Position Cameras |

| PTZ Cameras |

| 360°/Panoramic Cameras |

| Mobile Trailer and Crane-Mounted Cameras |

| AC-Powered Systems |

| Solar-Powered Systems |

| Battery-Only/Hybrid Systems |

| 4G/5G Cellular |

| Wi-Fi / Mesh |

| Wired Ethernet/PoE |

| Progress Monitoring and Documentation |

| Security and Surveillance |

| Marketing and Stakeholder Engagement |

| General Contractors |

| Owners / Developers |

| Government and Infrastructure Agencies |

| Industrial EPC and Energy Firms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Fixed Position Cameras | ||

| PTZ Cameras | |||

| 360°/Panoramic Cameras | |||

| Mobile Trailer and Crane-Mounted Cameras | |||

| By Power Source | AC-Powered Systems | ||

| Solar-Powered Systems | |||

| Battery-Only/Hybrid Systems | |||

| By Connectivity | 4G/5G Cellular | ||

| Wi-Fi / Mesh | |||

| Wired Ethernet/PoE | |||

| By Application | Progress Monitoring and Documentation | ||

| Security and Surveillance | |||

| Marketing and Stakeholder Engagement | |||

| By End-User Industry | General Contractors | ||

| Owners / Developers | |||

| Government and Infrastructure Agencies | |||

| Industrial EPC and Energy Firms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global construction camera market in 2026?

The market is valued at USD 0.57 billion in 2026, and is expected to reach USD 0.86 billion by 2031.

What compound annual growth rate is projected for construction cameras between 2026 and 2031?

The market is forecast to expand at an 7.32% CAGR over that period.

Which geography is expected to record the quickest sales expansion through 2031?

Asia-Pacific is projected to post the fastest regional rise, advancing at a 9.57% CAGR.

What is driving the rapid adoption of solar-powered camera systems on jobsites?

Solar rigs cut the cost and delay of extending grid service, provide up to 14 days of autonomous runtime, and align with carbon-reduction mandates on megaprojects.

How is edge artificial intelligence changing job-site safety monitoring?

Embedded processors now identify missing PPE or proximity hazards in milliseconds, letting supervisors intervene instantly and reducing OSHA-recordable incidents by roughly one-third.

How concentrated is the vendor landscape for construction cameras?

The top five suppliers account for about 40-45% of global revenue, indicating moderate concentration with ample room for regional specialists.

Page last updated on: