Underwater Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

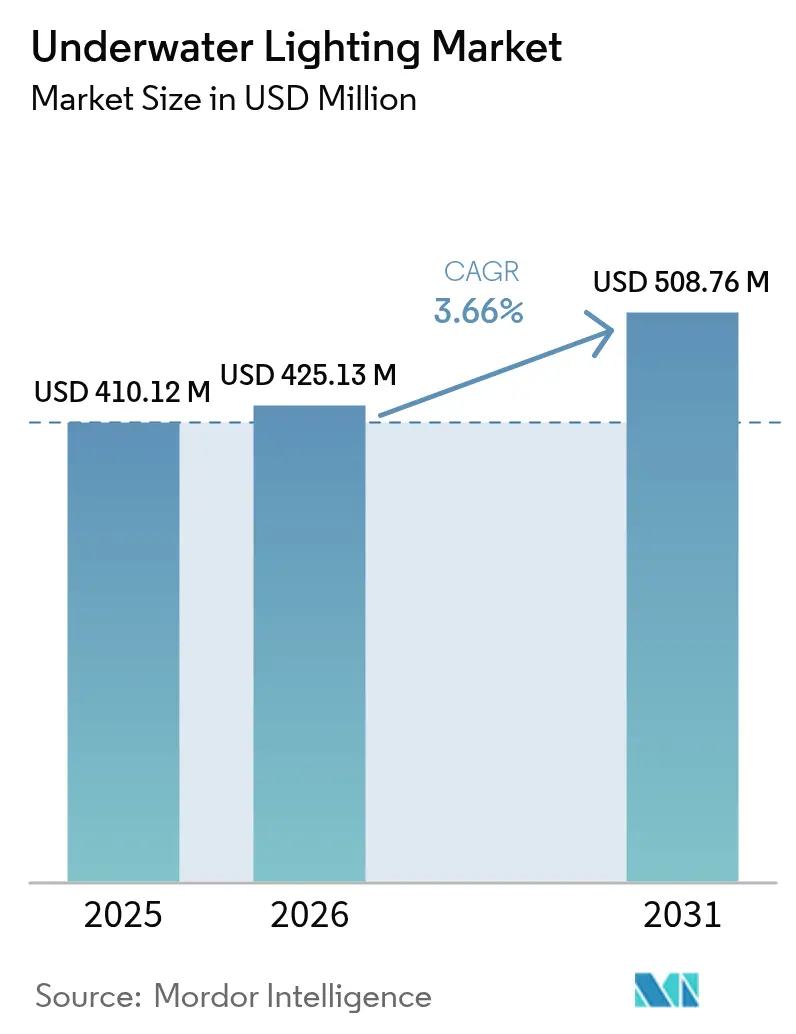

| Market Size (2026) | USD 425.13 Million |

| Market Size (2031) | USD 508.76 Million |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

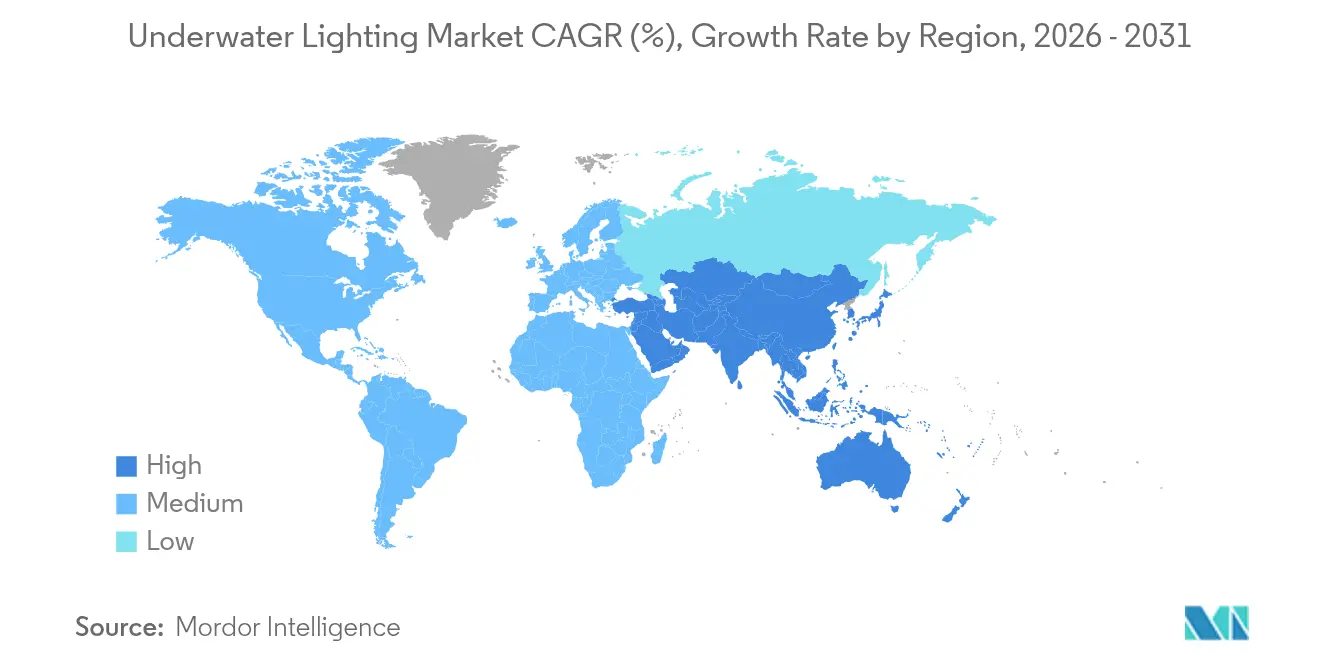

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Underwater Lighting Market Analysis by Mordor Intelligence

The underwater lighting market size in 2026 is estimated at USD 425.13 million, growing from 2025 value of USD 410.12 million with 2031 projections showing USD 508.76 million, growing at 3.66% CAGR over 2026-2031. Demand pivots toward high-efficacy LEDs as the technology secures 79.22% underwater lighting market share in 2024, displacing halogen and metal-halide systems across pools, marinas, and aquaculture sites. RGB and smart-enabled LEDs are expanding fastest because they integrate with chartplotters, building-management software, and aquaculture control platforms, creating additive revenue streams for software-as-a-service offerings. Flush and thru-hull fixtures gain traction in new-build vessels where hull integration during fabrication trims labor and improves hydrodynamics, while spectrally tuned luminaires for salmon and trout farms open biologically oriented niches. Geographic momentum shifts to Asia-Pacific as coastal tourism hubs fund marinas and waterfront resorts, yet Europe maintains leadership through energy-efficiency mandates and early compliance with fluorescent phase-outs, sustaining retrofit volumes that protect established suppliers.

Key Report Takeaways

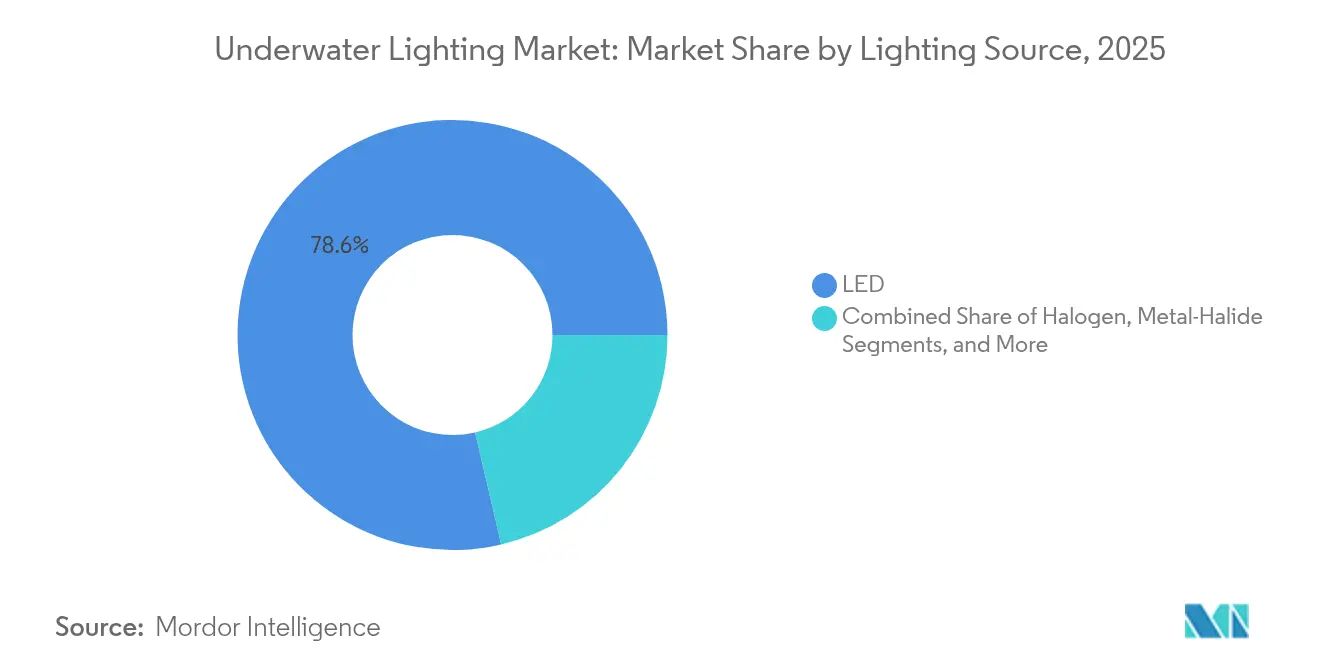

- By lighting source, LEDs accounted for 78.64 of % underwater lighting market share in 2025, and RGB plus smart-enabled LEDs are projected to advance at a 5.32% CAGR through 2031.

- By mounting type, surface-mounted fixtures captured 64.12% revenue in 2025, whereas flush and thru-hull systems are poised to grow at a 6.02% CAGR to 2031.

- By application, swimming pools represented 55.63% of the underwater lighting market size in 2025, but boats and yachts are forecast to climb at a 6.21% CAGR during the outlook period.

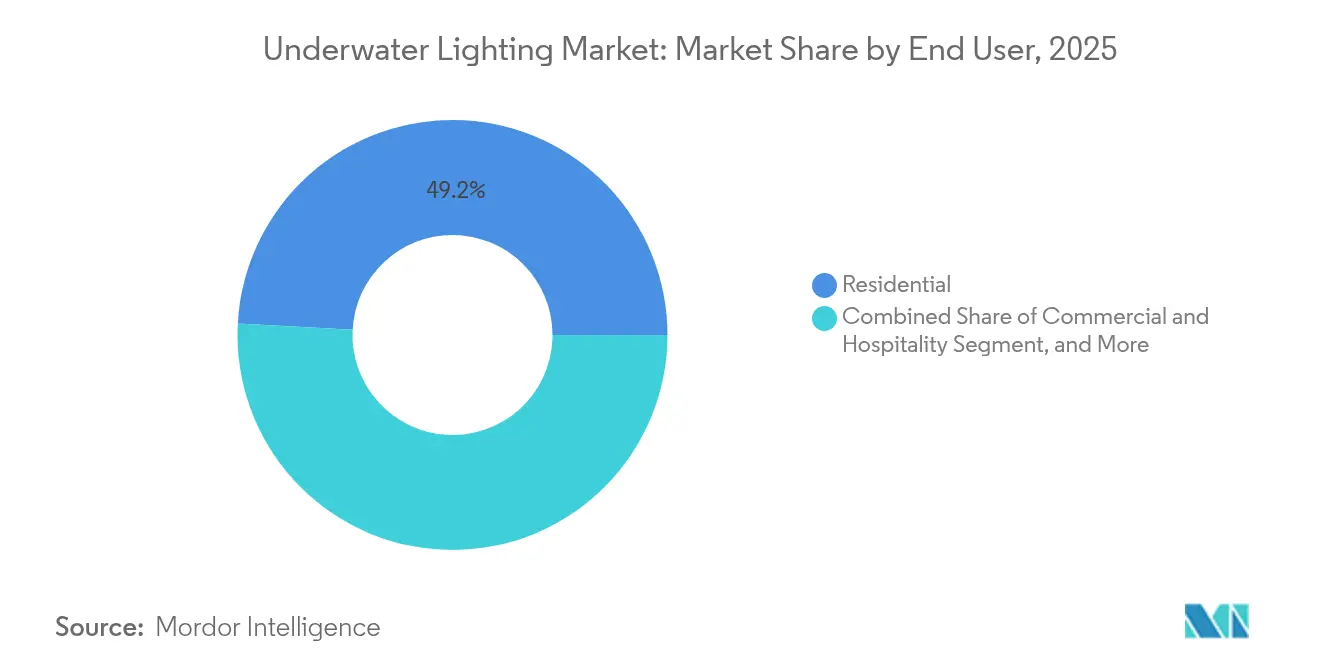

- By end user, residential installations held 49.15% revenue share in 2025, while commercial and hospitality projects are expected to expand at 5.55% CAGR to 2031.

- By sales channel, Aftermarket channels comprised 54.32% revenue in 2025, and online storefronts will grow at 4.81% CAGR to 2031 as distributors digitize catalogs and offer direct shipping.

- By geography, Europe led with 31.88% revenue share in 2025, and Asia-Pacific is set to register the fastest 5.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Underwater Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for underwater lights in pools and aesthetic water-featured landscaping | +0.9% | North America, Europe, Middle East | Medium term (2-4 years) |

| Government incentives accelerating LED adoption in lighting retrofits | +0.7% | Europe, North America | Short term (≤ 2 years) |

| Increasing construction of luxury hotels, resorts and water parks | +0.6% | Middle East, Asia-Pacific | Medium term (2-4 years) |

| Growing recreational boating and yachting activities | +0.8% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Emergence of smart/IoT-enabled underwater lighting systems | +0.5% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Deep-sea aquaculture's need for spectrally tuned submersible LEDs | +0.4% | Norway, Chile, Australia, Scotland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Underwater Lights in Pools and Aesthetic Landscaping

Residential and municipal pool permits in the United States rose 8.9% in 2024, stimulating LED retrofits that cut energy use by 85% versus halogen and stretch lifespans to 50,000 hours. Fluidra noted that products carrying sustainability credentials, including LED fixtures, contributed 51% of its 2023 sales, confirming the pull from eco-conscious buyers. Middle-Eastern resorts now specify multi-zone RGB packages controlled via DMX512 to synchronize fountains with façade lighting, elevating lights from basic safety gear to key design elements. Higher fixture counts per project lift average sales values, while IEC 60598-2-18 compliance and voluntary ENERGY STAR labels support procurement decisions. Together, these factors reinforce an upgrade cycle that keeps the underwater lighting market growing even as pool construction moderates.

Government Incentives Accelerating LED Adoption in Retrofits

The US EECBG voucher program funds LED upgrades in public aquatic centers, compressing payback periods to under three years.[1]U.S. Department of Energy, “Energy Efficiency and Conservation Block Grant Program,” energy.gov EU Directive 2024/1275 obliges automatic lighting controls in non-residential buildings by 2027, pushing commercial pool operators toward networked LEDs. Norway’s Innovation Norway financed Havlandet’s pilot salmon farm, proving that grant support can de-risk early use of spectrally tuned luminaires. Mowi Feed’s 2024 factory retrofit with Glamox LEDs slashed electricity consumption by 60% after RoHS restrictions removed fluorescent tubes from the market. Public-sector funding thus accelerates the baseline shift to LEDs across both civic and industrial venues.

Increasing Construction of Luxury Hotels, Resorts and Water Parks

Saudi Arabia’s Red Sea Project, UAE’s Dubai Creek Harbour, and Qatar’s Lusail Marina all embed underwater LEDs in marinas and lagoons to impress high-net-worth visitor. Singapore’s Sentosa expansions and Australia’s Gold Coast marina upgrades link submerged lighting to centralized BMS dashboards, proving out energy-monitoring and scheduling benefits. Water parks in China specify high-output fixtures that withstand 5 ppm chlorine during 12-hour daily cycles, widening industrial specifications beyond leisure yachts. These commercial builds prefer flush-mount or thru-hull units that sit flush with pool walls, reducing patron injury risk while easing maintenance from equipment rooms. As hospitality chains pursue social-media-ready aesthetics, color-changing lights become essential décor, accelerating growth in the underwater lighting market.

Increasing Construction of Luxury Hotels, Resorts and Water Parks

Saudi Arabia’s Red Sea Project, UAE’s Dubai Creek Harbour, and Qatar’s Lusail Marina all embed underwater LEDs in marinas and lagoons to impress high-net-worth visitors. Singapore’s Sentosa expansions and Australia’s Gold Coast marina upgrades link submerged lighting to centralized BMS dashboards, proving out energy-monitoring and scheduling benefits. Water parks in China specify high-output fixtures that withstand 5 ppm chlorine during 12-hour daily cycles, widening industrial specifications beyond leisure yachts. These commercial builds prefer flush-mount or thru-hull units that sit flush with pool walls, reducing patron injury risk while easing maintenance from equipment rooms. As hospitality chains pursue social-media-ready aesthetics, color-changing lights become essential décor, accelerating growth in the underwater lighting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital cost of marine-grade LED fixtures | -0.6% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Challenging maintenance in corrosive saltwater environments | -0.4% | Coastal regions, tropical latitudes | Long term (≥ 4 years) |

| Lack of harmonized global safety standards increasing certification costs | -0.3% | Global, exporters face highest burden | Medium term (2-4 years) |

| Light pollution regulations limiting illumination in sensitive marine habitats | -0.2% | North America coastal zones, Europe marine protected areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Cost of Marine-Grade LED Fixtures

Premium housings in aluminum-bronze and borosilicate glass push retail prices to USD 1,200 for flush-fit lights and USD 2,850 for high-output thru-hull units.[2]Atlantic Marine Inc., “TIX202 Flush-Fit Thru-Hull LED Light,” atlanticmarineinc.com Although life-cycle analysis favors LEDs thanks to 50,000-hour ratings and 85% energy savings, sticker shock slows adoption among small boat owners and budget-focused municipalities. Financing options are scarce because lenders view lighting as discretionary, leaving customers to fund upgrades up front. This cost hurdle weighs heaviest in emerging coastal economies where discretionary boating budgets remain tight, tempering short-term expansion of the underwater lighting market.

Challenging Maintenance in Corrosive Saltwater Environments

Salt-fog ingress, galvanic corrosion, and biofouling degrade seals and coatings, cutting field life below laboratory IP69K test results. Correct anode selection zinc for saltwater, aluminum for brackish, magnesium for freshwater mitigates but does not eliminate pitting. OceanLED specifies Delrin isolators and Tritonium coatings to slow marine growth, yet thru-hull replacements still demand haul-outs or dive crews, inflating total cost of ownership. Operators in remote cruising regions risk extended downtime waiting for spares, encouraging some buyers to favor surface-mount fixtures with simpler above-water servicing. These maintenance realities cap long-term growth, especially for high-output gear installed in warm, high-salinity waters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lighting Source: LED Dominance Driven by Control and Efficacy

LEDs controlled 78.64% of the underwater lighting market size in 2025, and their share continues rising as RGB and smart variants post a 5.32% CAGR. Multi-chip arrays match or exceed metal-halide brightness while eliminating 10-minute restrike delays. Halogen lingers almost solely in legacy pool niches where transformers and wiring resist LED retrofits, yet accelerating regulatory bans should push halogen toward single-digit presence by 2030. Spectrally tuned LEDs tailored to salmon photoreceptors illustrate the technology’s biological versatility, opening revenue far from traditional leisure markets. Meanwhile, phosphor-converted packages such as Signify’s SeaCage hit 150 lm/W, and lab prototypes reveal scope for further efficiency gains. As connectivity platforms improve, fixture firmware updates and color-scene libraries create post-sale revenue, strengthening supplier margins and anchoring customers in proprietary ecosystems. Collectively, these factors secure LEDs as the undisputed engine of the underwater lighting market.

Flush-mounts and thru-hulls increasingly bundle intelligent thermal throttling that protects diode junctions during stagnant water events, sharply reducing failure rates. While halogen replacement bulbs still sell into existing niches, distributors report steady decline in unit volumes. Metal-halide fixtures defend a final stronghold among operators demanding extreme lumen density in tight envelopes, but continual LED advances in chip density and cooling threaten even this bastion. Consequently, investors continue to funnel capital into LED-specific R&D rather than prolonging legacy lamp life-cycles. The underwater lighting industry therefore aligns its product roadmaps almost exclusively around LED architectures.

By Mounting Type: Flush and Thru-Hull Adoption Gains Momentum

Surface-mounted lights retained 64.12% revenue in 2025 because do-it-yourself owners favor bolt-on simplicity. Yet flush and thru-hull units will grow 6.02% annually as boatbuilders install them during lay-up, embedding wiring before gelcoat and avoiding future penetrations. OceanLED’s Explore TH series supports wet-maintenance, letting crews swap lenses without hauling out, a feature that neutralizes historic service drawbacks. Flush profiles slash drag and reduce entanglement risks for fishing nets and mooring lines, appealing to performance-oriented skippers. Builders also value the through-hull’s clean exterior aesthetic that supports premium vessel branding.

Retrofit complexity keeps surface-mount fixtures dominant in the aftermarket because owners can fit lights with basic hand tools. Conversely, new yachts integrate flush units to avoid warranty disputes over drilled hulls. Clip-on and portable lights address photographers and dive-tour operators who need brief, battery-powered luminance, but their low lumen output limits broader growth. As more OEMs pre-wire hulls for lights, an increasing portion of the underwater lighting market revenue will shift to factory channels and away from retail DIY installations.

By Application: Boats and Yachts Accelerate Beyond Pools

Swimming pools generated 55.63% revenue in 2025, yet boats and yachts are expanding at a 6.21% CAGR through 2031 as factory-installed LEDs become standard on new craft. Chartplotter-synced controllers now allow single-touch scene changes, broadening appeal among mid-market boat owners. The underwater lighting market size for boating applications will therefore overtake incremental pool growth mid-decade. Fountain and architectural water-feature projects remain cyclical but lucrative, especially in Gulf resorts where synchronized RGB shows attract evening crowds. In aquaculture, downward-facing LEDs reduce sea-lice infestation by 50%, proving economic gains beyond mere illumination.

Municipal pool operators lean heavily on LED retrofits for energy compliance, while residential owners adopt app-based scheduling that integrates with broader smart-home ecosystems. Yacht refits take place during winter lay-ups, generating seasonal spikes for service yards. Fishing crews employ dual-color systems, toggling white during docking and green at anchor to lure baitfish. These diverse use cases ensure that no single vertical dominates long-term, insulating the underwater lighting market from downturns in any one segment.

By End User: Commercial and Hospitality Demand Strengthens

Residential installations held 49.15% revenue share in 2025, but commercial and hospitality clients will expand at 5.55% CAGR through 2031 as resorts seek Instagram-ready nightscapes. Luxury properties in the Middle East now integrate multi-zone RGB arrays managed from building-management dashboards, enabling daily theme switches that differentiate guest experiences. Connected-pool counts hit 877,000 worldwide by late 2023, and Fluidra targets 1 million by 2025, underscoring rapid digital adoption. Industrial ports employ rugged white LEDs for safety perimeters, prioritizing high lumen density rather than aesthetics.

Defense procurement cycles create smaller but stable orders for ruggedized fixtures on naval craft and remotely operated vehicles. Commercial aquaculture farms remain an emerging but high-value niche because biological gains offer fast return on investment. Residential buyers continue frequent light replacements due to exposure and pool-chemical stress, keeping aftermarket volumes high. As hotels and water parks bundle lighting with broader entertainment systems, suppliers able to integrate DMX512 and IoT protocols stand to capture rising commercial wallet share across the underwater lighting market.

By Sales Channel: Online Aftermarket Platforms Expand Reach

Aftermarket channels comprised 54.32% revenue in 2025, and online storefronts will grow at 4.81% CAGR to 2031 as distributors digitize catalogs and offer direct shipping. E-commerce sites such as Atlantic Marine Inc. permit filter-based searches by lumen output, housing material, and control protocol, empowering informed buying decisions. OEM channels dominate large-volume orders to boatyards and pool contractors, capturing 45.68% of revenue thanks to design-phase engagement that locks fixtures into specifications. Traditional brick-and-mortar marine stores counter by bundling installation and warranty services, adding value beyond parts sales.

Regions with mature parcel networks, like North America and Western Europe, experience faster online conversion, while high import duties slow uptake in parts of Asia and Latin America. Fluidra’s hybrid Fluidra PRO model combines web ordering with 84 local PRO Centres, blending speed with hands-on support, and illustrating a winning omnichannel formula. As consumers grow accustomed to digital shopping, the underwater lighting industry will increasingly treat direct-to-consumer fulfillment as a baseline expectation.

Geography Analysis

Europe led the underwater lighting market in 2025 with 31.88% revenue share, driven by EU Directive 2024/1275 energy mandates and the RoHS-enforced fluorescent phase-out that fueled retrofit demand. Norway’s 1.3 million-ton salmon output underpins steady orders for spectrally tuned LEDs, as evidenced by Signify’s Salmon Evolution win. Italy’s EUR 8.33 billion yacht sector supports winter refit activity, while Germany and France tighten pool efficiency standards, spurring domestic pool upgrades. The UK’s Lumishore, now under Garmin, exports high-value RGB fixtures, highlighting Europe’s innovation role.

Asia-Pacific is projected to record a 5.62% CAGR through 2031, propelled by China’s coastal tourism investments, Singapore’s Sentosa developments, and Australia’s AUD 10.12 billion boating industry. Chinese Tier-2 cities fund wave pools and lazy rivers that require chlorine-resistant LEDs, while Singapore links submerged lights to BMS dashboards for energy analytics. Australia’s remote cruising routes elevate reliability requirements, pushing buyers toward IP68-rated hardware. Japan’s flat residential construction limits pool growth, but land-based fish farms adopt LEDs for yellowtail and sea bream. India’s leisure-boating niche remains cost-sensitive, yet luxury resorts in Goa and Kerala specify RGB systems to compete globally.

North America generated roughly 27.74% of global revenue in 2025. US pool permits climbed 8.9%, and NMMA-reported spending kept after-sales lights moving despite a slight dip in new-boat units. DOE vouchers encourage municipal pool retrofits, while Florida sea-turtle ordinances require amber or red spectra during nesting season, prompting tunable products, Canada’s shorter boating season compresses installation windows, making inventory forecasting critical. Mexico’s Cancún resorts demand color-changing lagoon lighting to attract U.S. tourists. Collectively, these regional nuances keep suppliers agile and diversified, reinforcing long-run stability for the underwater lighting market.

Regulatory Landscape

Underwater lighting suppliers have to account for overlapping safety, ingress-protection, and marine-navigation requirements that differ by application (pools and fountains vs vessels vs subsea infrastructure). For fixed luminaires used in water, IEC 60598-2-18:2022 anchors construction and test requirements, while ingress protection testing aligns with IEC 60529 (commonly specified to IP68 for continuous immersion). In North America, UL 676:2021 (ANSI approval noted in Sept 2025) is a key product safety reference for underwater luminaires and submersible junction boxes, and US vessel installations also intersect with U.S. Coast Guard requirements under 46 CFR.

On the marine side, navigation-light performance is standardized through the International Maritime Organization (IMO) performance standards (MSC.253(83)), shaping optical and reliability expectations on vessels that incorporate underwater lighting as part of broader exterior-lighting packages. In January 2026, the U.S. Coast Guard Marine Safety Center published an updated Plan Review Guide E2-23 for small passenger vessels, expanding acceptance of additional lighting standards (including UL 924 for emergency lighting and EN 14744/ABYC C-5 for navigation lights), which can reduce design and plan-review friction for builders and refit yards sourcing compliant lighting systems.

Value Chain Analysis

The underwater lighting value chain begins with LED emitters and optical components (lenses, diffusers), power electronics (drivers, controls, wireless modules), and marine-grade mechanical inputs (aluminum-bronze or stainless housings, borosilicate windows, seals, and cable penetrators). Design and engineering translate application needs into photometrics, thermal management, and corrosion control, then move into qualification against relevant safety and immersion standards (for example, IEC 60598-2-18 for in-water luminaires and UL 676 for North America).

For higher-stakes subsea and defense applications, suppliers also coordinate specialized connector and penetrator integration and the associated test regimes, with certification footprints becoming a gating factor for market access. Manufacturing and assembly are often vertically integrated to manage sealing processes, coating quality, and final test, and multiple players run in-house facilities for both standard and custom builds. Underwater Lights Limited highlights in-house manufacturing for bespoke marine and yacht lighting, DeepSea Power & Light operates an in-house factory model with quick-ship configurations, and Outland Technology manufactures subsea cameras and lights from its 13,500 sq ft facility. Distribution splits between OEM channels (boatbuilders, pool contractors, system integrators) and aftermarket networks (marine retailers, installers, e-commerce), with service partners and yards supporting installation, troubleshooting, and replacement cycles in corrosive saltwater environments.

Competitive Landscape

Market concentration is moderate: the top five vendors control about 35–40% combined revenue, leaving room for regional specialists. Garmin’s 2024 acquisition of Lumishore embeds lighting within its chartplotter ecosystem, offering helm-based control that may set an integration benchmark. Signify leverages a 1,748-patent portfolio to dominate aquaculture, landing Salmon Evolution and Australis Seafoods contracts that showcase biodiversity benefits ONCE.LIGHTING. Fluidra’s 13% share of the global pool-equipment space feeds cross-sales through its 84 PRO Centres and connected-pool app, converting hardware buyers into platform subscribers.

Differentiation centers on wet-maintenance designs, thermal-management algorithms, and DMX512 or NMEA 2000 compatibility. Emerging disruptors offer lighting-as-a-service subscriptions paired with cloud control and energy analytics, though uptake remains nascent. Certification complexity across UL 676, CE, and IEC 60598-2-18 favors capital-rich incumbents, creating barriers for entrants that lack multi-region compliance budgets. Still, agile regional firms win business by bundling installation and service in locales like Australia’s Gold Coast or the US Gulf Coast. The underwater lighting market therefore balances scale advantages with localized service plays, fostering steady innovation without tipping into monopoly.

Underwater Lighting Industry Leaders

Eaton Corporation

Signify Holding (Koninklijke Philips N.V.)

Acuity Brands Inc.

Hayward Industries Inc.

Lumitec LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product differentiation is creating whitespace around lower-maintenance operation in harsh marine environments, particularly where biofouling and condensation raise service costs. Metro Marine Lighting introduced an F-Series full spectrum line in April 2026 that incorporates anti-biofouling and anti-condensation approaches (including UVC emitters), pointing to a premium positioning opportunity in marinas, yachts, and waterfront hospitality projects where uptime and visual consistency are emphasized. Lumitec also started production and distribution of its SeaBlazeX3 surface-mount underwater light in June 2026, focusing on thermal management and leak protection, which supports demand for longer-life fixtures intended to reduce callbacks for installers and service yards.

A second opportunity band is the convergence of lighting with sensing and imaging workflows in subsea operations, where illumination quality directly affects photogrammetry, inspection output, and mission efficiency. Technical specifications are increasingly centered on high-lumen, flicker-free, digitally controlled arrays that integrate with ROV/AUV telemetry (e.g., RS-485, PWM) and support synchronization with multi-camera setups, creating applications beyond leisure such as marine infrastructure inspection, research, and industrial subsea work. On the channel side, distributor expansions into dock and marine lineups, including DRSA - Light It Up broadening its 2026 dock lighting assortment to include SeaBlaze X3, reflect ongoing shelf-space competition and a scaling path for manufacturers through installer-friendly SKUs and upgrade cycles.

Recent Industry Developments

- June 2026: Lumitec commenced production and distribution of the SeaBlazeX3 surface-mount underwater light, featuring DryLock thermal management and leak-protection features. The shift strengthens its surface-mount portfolio for boats, docks, and marina applications where installers prioritize reduced failure risk and simplified servicing.

- August 2025: Eaton launched CEAG VLL Series Ex lights for hazardous and marine environments, with manufacturing referenced at its Chennai facility. This adds capacity and localization for marine-adjacent lighting programs where ruggedization and compliance requirements shape procurement in industrial waterfront and offshore settings.

- April 2024: Acuity Brands (Hydrel) expanded its 4426 series underwater luminaires for fountains and water features by adding new low-voltage options. The update supports safer, more flexible specifications for architectural water features and can lower operating and maintenance complexity for contractors and municipalities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The underwater lighting market is defined as the revenue generated from lighting products designed to operate fully submerged, along with related driver/control hardware, across pool, fountain, marine, industrial, and specialty underwater use cases.

Scope exclusions: We exclude topside landscape lighting, general marine deck lighting that is not submersible, and standalone installation labor unless it is bundled within the product sale price.

Segmentation Overview

- By Lighting Source

- LED

- Halogen

- Metal-Halide / Others

- By Mounting Type

- Surface-Mounted

- Flush / Thru-Hull

- Portable / Clip-On

- By Application

- Swimming Pools

- Fountains and Water Features

- Boats and Yachts

- Aquaculture and Research

- By End User

- Residential

- Commercial and Hospitality

- Industrial / Marine Infrastructure

- Defense and Government

- By Sales Channel

- OEM

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the basic demand and supply picture before detailed sizing was attempted. We relied on public materials such as US Census Bureau trade and production statistics, UN Comtrade import and export series, USITC tariff schedules and HS code notes, and energy-efficiency standards and guidance from the US Department of Energy.

To keep assumptions realistic, additional context was taken from product certification and safety references (such as UL and IEC published guidance), marine and pool industry association updates, and company filings and investor presentations to understand pricing logic and channel mix. Where available, patent database screening helped us see the pace of LED and control feature innovation and the application areas being prioritized. A paid subscription focused on company financials and a shipment-level trade database were also used selectively to cross-check scale and routing patterns. The sources mentioned here are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on speaking with manufacturers, distributors, installers, and large buyers across marine, pool, and water-feature applications to confirm pricing, replacement cycles, and channel shares. We also used expert input from different regions to align on adoption timing for LED upgrades, retrofit pull, and the practical impact of safety and energy rules, which helped close gaps left by public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 22% | APAC: 41% |

| Mid tier: 46% | Functional/Unit leaders: 22% | EMEA: 34% |

| Smaller Players: 22% | Managers: 56% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where demand pools were reconstructed from visible installation bases and renewal behavior, then converted into value using typical price ladders. For example, pool and water-feature counts, boat and yacht build and retrofit activity, and the share of LED and smart/RGB fixtures were translated into annual unit needs, then priced using region-appropriate average selling prices.

To keep the output grounded, the totals were corroborated with selective bottom-up approximations such as sampled SKU price checks, distributor channel checks, and manufacturer revenue splits for underwater product lines, and adjusted when clear mismatches showed up. Inputs used in the model included LED penetration, retrofit versus new installation mix, average fixture count per installation, replacement cycles for harsh-water use, and OEM versus aftermarket shares, along with trade flow signals where product classification allowed.

Forecasting was then run using scenario analysis supported by simple regression checks on drivers like discretionary marine spending and construction-linked pool activity, with assumptions reviewed against expert expectations. When bottom-up information was incomplete for a niche application, we used conservative proxy ratios from similar end uses and then validated the reasonableness through follow-up calls.

Data Validation & Update Cycle

Validation was done in several passes so that errors do not slip through. Model outputs were checked against independent signals such as trade movement, announced product launches, and channel feedback on pricing and lead times, and large variances were reviewed by another analyst before sign-off.

If an assumption moved the total more than expected, re-contact was triggered with a different respondent type, for example switching from a supplier view to an installer or distributor view, to confirm the practical reality. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp raw material changes affecting fixture pricing or sudden shifts in marine demand. Before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Underwater Lighting Market Size Versus Other Published Estimates

Published market sizes for underwater lighting often do not match because firms pick different base years, include different application edges, and apply different price progression logic across regions. Currency timing and how retrofit demand is treated also create noticeable spreads, even when the product list sounds similar.

The main gap drivers are scope and how value is constructed from units and pricing. Some estimates fold in adjacent marine lighting categories or include services and software value more broadly, while others apply faster LED upgrade curves and higher average selling price lift without checking channel discounting, which can inflate totals. In this study, OEM and aftermarket splits are treated separately and LED share is tied to observable replacement and retrofit cycles, a narrower counting choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 425.13 M (2026) | |

| Trade Journal A | USD 361.97 M (2025) | Uses an earlier base year and a different forecast window, and it appears to apply a broader growth assumption for LED upgrades without clearly separating OEM versus aftermarket price realization. |

| Global Consultancy B | USD 363.66 M (2025) | Anchors sizing to 2025 and may emphasize a tighter application list, which can reduce totals if aquaculture, research, or industrial marine infrastructure demand is treated as minor or excluded. |

The table shows that most of the spread is explained by base-year selection and the way adjacent applications and channels are counted. By keeping the demand pool tied to installation bases, replacement timing, and realistic price ladders by channel, the resulting market value remains easy to trace and repeat across updates.

Key Questions Answered in the Report

How large is the underwater lighting market in 2026?

The underwater lighting market size is USD 425.13 million in 2026.

What is the expected growth rate for underwater lighting through 2031?

The market is projected to expand at a 3.66% CAGR to reach USD 508.76 million by 2031.

Which lighting source dominates sales?

LEDs command 78.64% underwater lighting market share due to high efficacy, smart control, and long life.

Which application is growing fastest?

Boats and yachts are forecast to increase at a 6.21% CAGR as chartplotter integration fuels demand.

Why are flush and thru-hull fixtures gaining traction?

Builders embed flush and thru-hull lights during hull fabrication, cutting labor and improving hydrodynamics, which drives a 6.02% CAGR for this mounting style.

What regions will lead future growth?

Asia-Pacific is set to grow at 5.62% CAGR through 2031, driven by coastal tourism infrastructure in China, Singapore, and Australia.

Page last updated on: