High Intensity Focused Ultrasound (HIFU) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

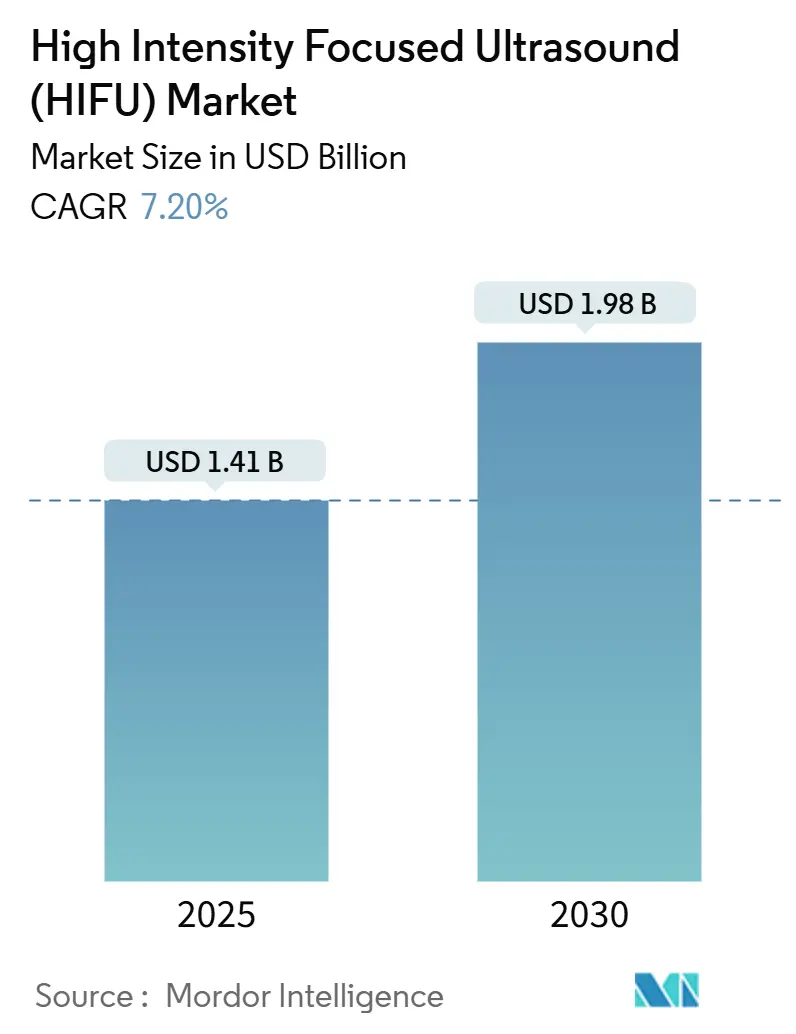

| Market Size (2025) | USD 1.41 Billion |

| Market Size (2030) | USD 1.98 Billion |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

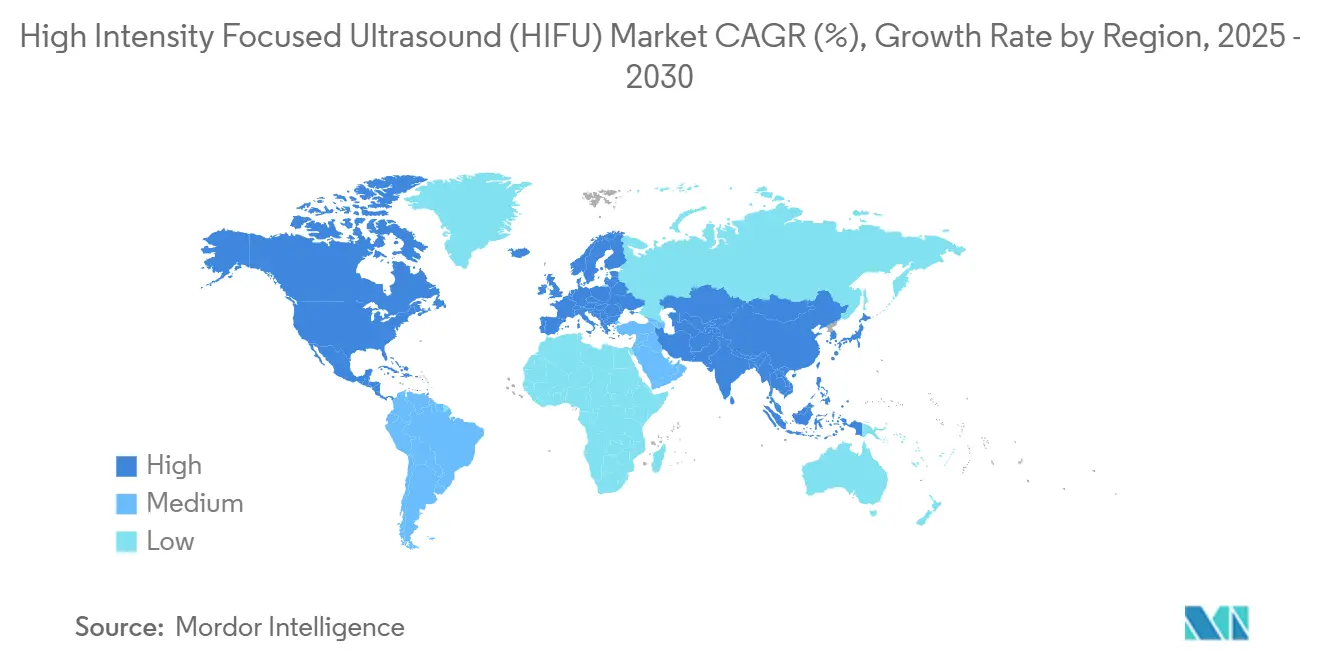

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Intensity Focused Ultrasound (HIFU) Market Analysis by Mordor Intelligence

The high-intensity focused ultrasound market size stands at USD 1.41 billion in 2025 and is projected to reach USD 1.98 billion by 2030, advancing at a 7.20% CAGR. The expansion reflects a structural shift from experimental use toward routine clinical adoption as reimbursement, regulatory, and imaging-precision milestones converge. Adoption accelerates where value-based care priorities reward procedures that shorten recovery, reduce infection risks, and cut overall spending. Real-time targeting enhancements, artificial-intelligence treatment planning, and the steady migration of cases to outpatient sites strengthen pricing power for operators while broadening patient access. Amid these conditions, industry leaders combine AI, robotics, and cloud connectivity to close skills gaps and standardize results, positioning platforms for wider deployment even in community settings.

Key Report Takeaways

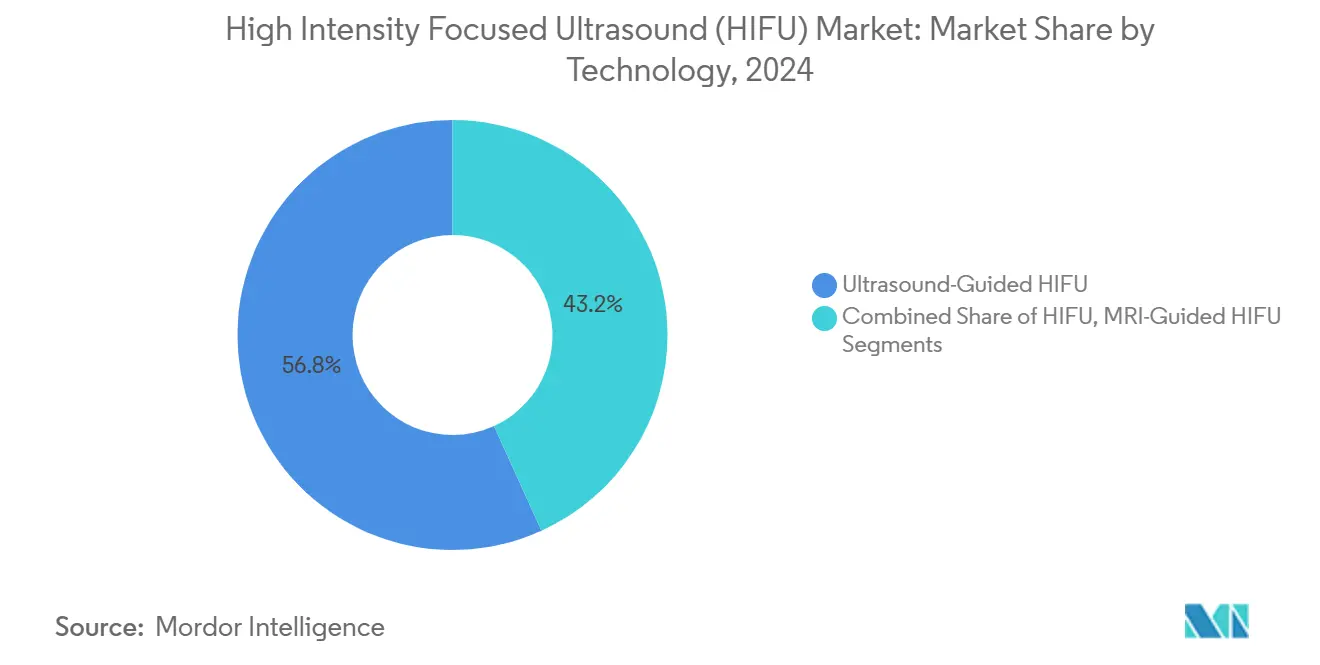

- By technology, ultrasound-guided systems led with 56.8% revenue share in 2024; MRI-guided platforms are forecast to expand at a 14.8% CAGR through 2030.

- By application, oncology held 38.5% of the High-Intensity Focused Ultrasound market share in 2024, while neurology is poised for the fastest 18.2% CAGR to 2030.

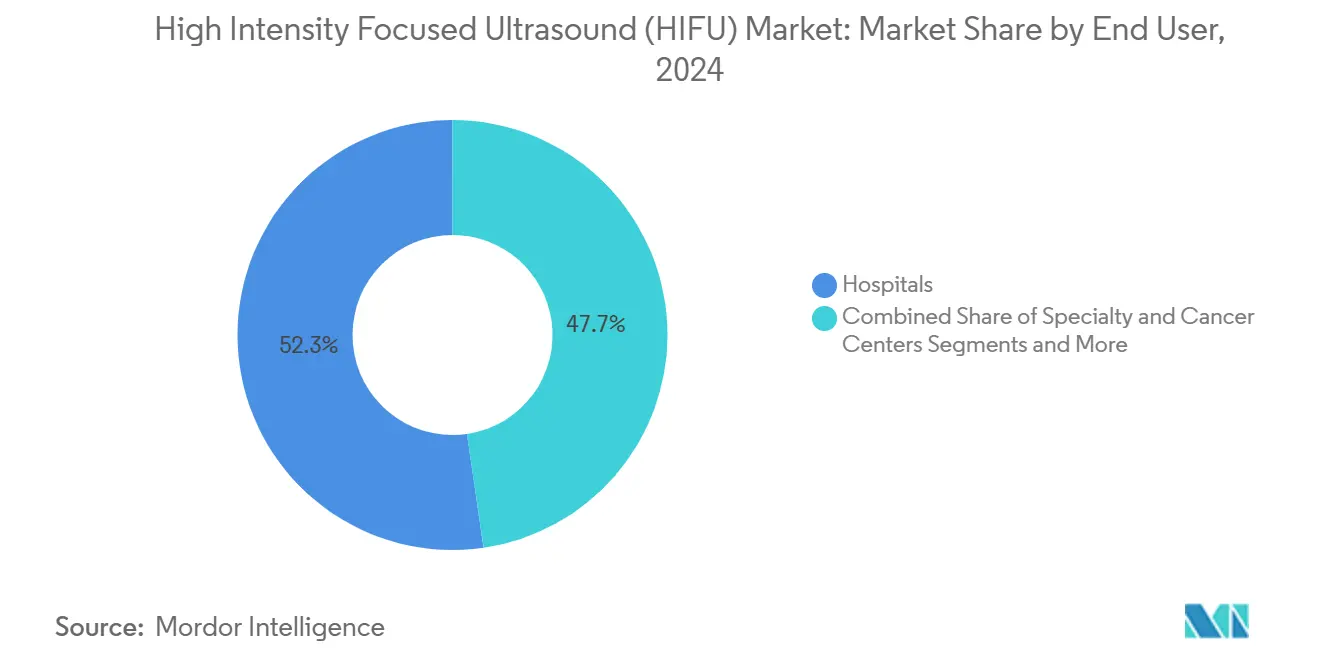

- By end user, hospitals accounted for 52.3% of 2024 revenue, yet ambulatory surgical centers are projected to post a 13.1% CAGR to 2030.

- By geography, North America maintained 33.7% share in 2024 and Asia Pacific is tracking a 12.8% CAGR through 2030.

Global High Intensity Focused Ultrasound (HIFU) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of prostate and uterine-fibroid cases | +1.80% | North America, Europe, Global | Medium term (2-4 years) |

| Growing demand for non-invasive oncology treatments | +2.10% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Advancements in real-time imaging and targeting precision | +1.50% | North America, Europe, Asia Pacific | Long term (≥ 4 years) |

| Favorable reimbursement codes in US and EU | +1.20% | North America, Europe | Short term (≤ 2 years) |

| Integration of AI-powered treatment-planning algorithms | +0.90% | North America, Europe | Medium term (2-4 years) |

| Emergence of outpatient HIFU centers in retail hubs | +0.70% | North America, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Prostate & Uterine-Fibroid Cases

The growing global incidence of prostate cancer and symptomatic fibroids sustains demand for organ-sparing alternatives. Uterine fibroids affect up to 80% of women by age 50, and HIFU preserves fertility while delivering high post-treatment natural conception rates with miscarriage rates comparable to surgery.[1]Zhao M. et al., “Evaluating pregnancy outcomes in women with uterine fibroids treated with high-intensity focused ultrasound,” Reproductive Health, reproductive-health-journal.biomedcentral.com Prostate patients increasingly favor focal therapy that minimizes sexual and urinary side effects, positioning HIFU as a strategic choice in early-stage disease management. These epidemiological and quality-of-life factors jointly elevate procedure volumes across high-income regions.

Growing Demand for Non-Invasive Oncology Treatments

Value-based purchasing drives hospitals to favor modalities that cut infection risk and shorten inpatient stays. HIFU ablates tumors without incisions, lowering postoperative costs that influence reimbursement metrics. Combined HIFU-brachytherapy protocols signal life-quality gains for inoperable cohorts, broadening the addressable market beyond curative oncology into palliative care.[2]Liu Y. et al., “Repeated high intensity focused ultrasound combined with iodine-125 seed brachytherapy offers improved quality of life,” Oncology Letters, spandidos-publications.com

Advancements in Real-Time Imaging & Targeting Precision

AI-assisted imaging now automates contouring and dosage calculations, lowering operator variability. Systems integrate algorithms that shorten planning cycles while improving accuracy, making procedures viable in centers without extensive subspecialist staffing. Contrast-enhanced ultrasound visualizes perfusion shifts during sonication, allowing real-time energy adjustment. Efficiency gains translate to higher daily procedure volumes, ease learning curves, and improved therapeutic confidence in varied anatomical territories.

Favorable Reimbursement Codes in US & EU

Dedicated CPT codes and Medicare payments align financial incentives with clinical value.[3]Gilyard B., “HistoSonics expanding Plymouth HQ,” startribune.com European CE-mark pathways consolidate multistate approvals, slashing regulatory timelines for updated platforms. U.S. facility fees for ambulatory settings encourage outpatient migration that lifts capacity without straining hospital theaters. Incremental annual payment uplifts underscore policy momentum backing minimally invasive therapies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of HIFU systems | −1.4% | Global, emerging markets most affected | Long term (≥ 4 years) |

| Limited skilled operators and training gaps | −1.1% | Global, sharper in Asia Pacific and emerging regions | Medium term (2-4 years) |

| Radio-frequency ablation price competition | −0.8% | North America, Europe | Short term (≤ 2 years) |

| Acoustic-thermometry regulatory gaps | −0.6% | FDA and EMA jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Ultrasound-Guided Systems Drive Market Leadership

Ultrasound-guided platforms captured 56.8% of revenue in 2024, reflecting favorable capital cost and streamlined workflow advantages. This segment underpins the High-Intensity Focused Ultrasound market size leadership position, while MRI-guided technology is projected to grow at a 14.8% CAGR through 2030 as imaging expectations rise for deep-seated lesions. Hospitals select modality based on anatomical complexity; superficial fibroid or prostate targets suit ultrasound, whereas neurological and pancreatic cases rely on MRI thermometry. Remote guidance over 5G demonstrated safe delivery by merging expert oversight with real-time imaging, illustrating future hybrid pathways. Component miniaturization and AI-enabled presets aim to close cost gaps, potentially narrowing the adoption divide over the forecast horizon.

Ultrasound systems boost procedural throughput, an advantage for ambulatory centers where turnover drives profitability. Conversely, MRI guidance improves margin capture in tertiary centers that bill premium imaging packages. Suppliers now explore dual-mode consoles, allowing operators to switch imaging paradigms within a single chassis, a strategy that could consolidate footprints and broaden asset utilization. Such innovation anchors technology segmentation forecasts in the High-Intensity Focused Ultrasound market.

By Application: Oncology Dominance Faces Neurology Disruption

Oncology retained 38.5% revenue in 2024 and still anchors the High-Intensity Focused Ultrasound market, yet neurology procedures for essential tremor are climbing faster at an 18.2% CAGR to 2030. Essential tremor success stories spur payors to review coverage, while Parkinson’s and obsessive-compulsive disorder trials progress. Uterine-fibroid and endometriosis pathways diversify gynecologic use cases, expanding female patient appeal. Cosmetic dermatology, though still a niche, generates attractive cash-pay margins, enticing aesthetic clinics into the modality’s orbit.

Clinical data underline oncology’s resilience: focal prostate therapy demonstrates functional preservation, and palliative bone-metastasis protocols relieve pain without opioid dependence. Nonetheless, neurology’s momentum could overtake oncology beyond the forecast if multi-target indication approvals accelerate. Application-specific software packages hint at this shift, embedding workflow nuances that shorten learning curves and deepen end-user loyalty within each disease area, further segmenting the High-Intensity Focused Ultrasound market.

By End User: Hospital Dominance Challenged by ASC Growth

Hospitals controlled 52.3% of 2024 revenue, leveraging established imaging suites and multidisciplinary teams. The segment anchors early adoption for complex cases and generates referral streams that stabilize asset utilization. However, ambulatory surgical centers (ASCs) are forecast to grow at a 13.1% CAGR to 2030, pivoting on same-day discharge and lower overhead. ASC economics benefit from facility fees near USD 4,280, a model aligning neatly with routine fibroid or prostate cases. High-throughput protocols and compact console footprints further tip the scales toward outpatient settings for less complex anatomy.

Specialty cancer institutes integrate HIFU alongside radiation and systemic therapy, delivering multidisciplinary care under one roof. Dermatology clinics leverage compact transducers for skin tightening, illustrating new customer classes. Training institutions and research hospitals round out the customer mix, generating early-stage evidence that informs reimbursement submissions and procedure guidelines, collectively enriching the High-Intensity Focused Ultrasound industry knowledge base.

Geography Analysis

North America maintained a 33.7% revenue share in 2024, supported by dedicated CPT codes and Medicare payments up to USD 17,500 per procedure. Structured operator certification, academic-industry collaboration, and AI-enabled workflow tools together create a robust ecosystem. Private insurers increasingly mirror Medicare’s coverage, further widening patient pools. Multi-institution centers of excellence showcase outcome data that underpin guideline inclusion, embedding HIFU into standard-of-care pathways. Device makers also exploit the region’s vibrant outpatient sector to pilot subscription leasing models that lower capital hurdles for independent ASCs.

Asia Pacific registers the highest 12.8% CAGR outlook through 2030, lifted by demographic aging, rising cancer incidence, and expanding middle-class spending. China’s domestic manufacturing base drives cost efficiency, with local producers scaling exports that broaden adoption. South Korea recorded double-digit growth in aesthetic HIFU sales, with domestic vendors controlling more than half of unit shipments. Regional regulators pursue mutual-recognition schemes that shorten approval cycles, and government procurement initiatives prioritize localized equipment, accelerating volume ramps in public hospitals. Cross-border tele-mentoring networks emerge, extending expert oversight to rural centers and reinforcing uptake across the High-Intensity Focused Ultrasound market.

Europe benefits from CE-mark harmonization, allowing single-file approvals across member states. Reimbursement gains for essential tremor in the Netherlands and Germany prove pivotal, prompting neighboring payors to reevaluate coverage. Academic consortia publish multi-center fibroid outcomes with notable quality-of-life gains and minimal adverse events. Though adoption tempo is tempered by rigorous health-technology assessments, once evaluations conclude positively, uptake accelerates within tax-funded systems. These pathways reinforce Europe’s position as a stable, evidence-led adopter poised for steady share growth.

Competitive Landscape

The High-Intensity Focused Ultrasound market features moderate fragmentation, with top players leveraging AI, robotic assistance, and cloud analytics to differentiate. EDAP TMS integrated Avenda Health software to automate focal-zone planning, lowering operator dependency. InSightec launched Exablate Prime with automated dosage and an upgraded UI to streamline workflow. HistoSonics’ histotripsy platform secured USD 102 million to commercialize liver tumor applications, signaling investor confidence in emerging cavitation-based ultrasonic therapy.

Strategic consolidation shapes the landscape: Cynosure merged with Lutronic to expand aesthetic energy devices, broadening cross-selling potential via combined distribution networks. Equipment vendors deploy outcome-based financing models and bundled maintenance to lock in multi-year revenue. Emerging players concentrate on single-organ targets or low-cost portable units, aiming to penetrate price-sensitive markets. Competitive intensity now hinges on securing post-sale service contracts and clinical-data leadership, factors that directly influence purchasing committees evaluating long-term partnership value.

High Intensity Focused Ultrasound (HIFU) Industry Leaders

Chongqing Haifu Medical Technology

EDAP TMS S.A.

InSightec Ltd.

Profound Medical Corp.

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The U.K.’s National Health Service became Europe’s first healthcare system to roll out the Edison histotripsy device, giving liver-cancer patients access to incision-free tumor ablation and signaling the NHS’s intent to fast-track novel focused-ultrasound therapies

- March 2025: Chongqing Haifu Medical completed the first international 5G-remote HIFU surgery, underscoring the viability of tele-mentoring.

- December 2024: VCU Health’s Massey Cancer Center launched Virginia’s first robotic-focused ultrasound program for prostate cancer care, highlighting the growing geographic reach of HIFU technology across U.S. academic medical centers.

Global High Intensity Focused Ultrasound (HIFU) Market Report Scope

| Ultrasound-Guided HIFU |

| MRI-Guided HIFU |

| Oncology |

| Gynecology |

| Neurology |

| Cosmetic Dermatology & Aesthetics |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty & Cancer Centers |

| Dermatology Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Ultrasound-Guided HIFU | |

| MRI-Guided HIFU | ||

| By Application | Oncology | |

| Gynecology | ||

| Neurology | ||

| Cosmetic Dermatology & Aesthetics | ||

| Others | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty & Cancer Centers | ||

| Dermatology Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2025 value of the High-Intensity Focused Ultrasound market?

USD 1.41 billion with a 7.20% CAGR toward 2030.

Which technology currently leads unit sales?

Ultrasound-guided systems captured 56.8% share in 2024.

Which medical specialty is growing fastest for HIFU?

Neurology applications for essential tremor are advancing at an 18.2% CAGR.

Why are ambulatory surgical centers important for growth?

ASC facility fees and same-day discharge align with HIFUs non-invasive profile, supporting a 13.1% CAGR to 2030.

Which region offers the highest future expansion potential?

Asia Pacific, forecast at a 12.8% CAGR, driven by healthcare modernization and domestic manufacturing.

Page last updated on: