Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

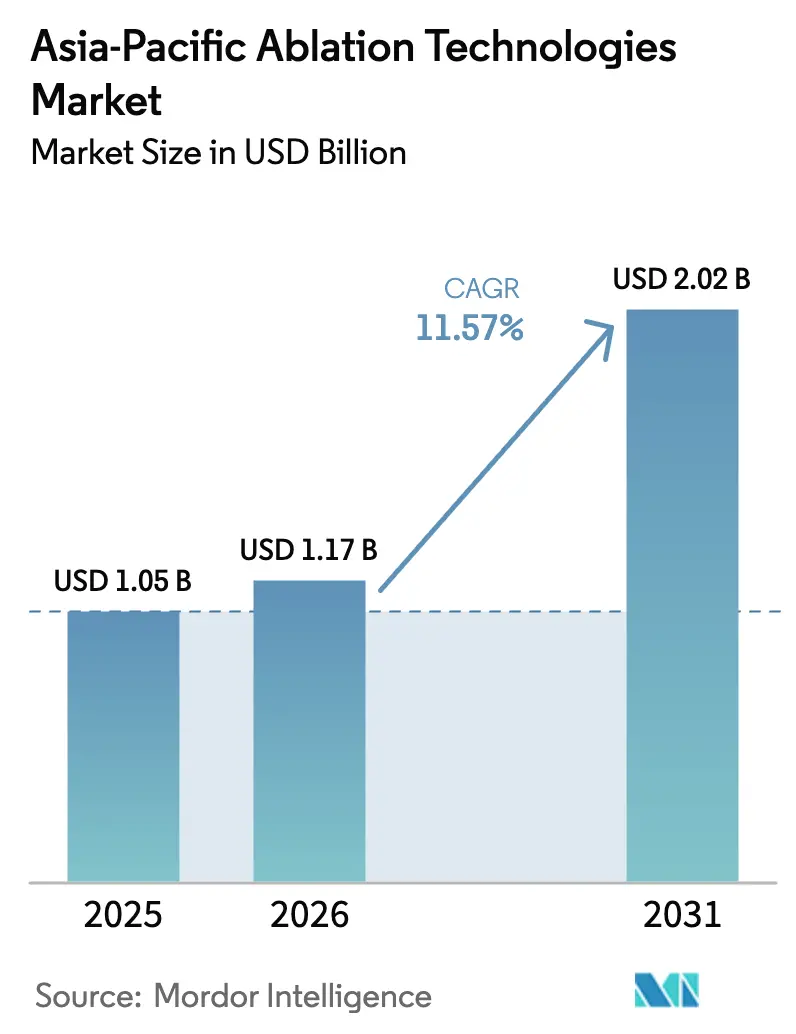

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 11.57% CAGR |

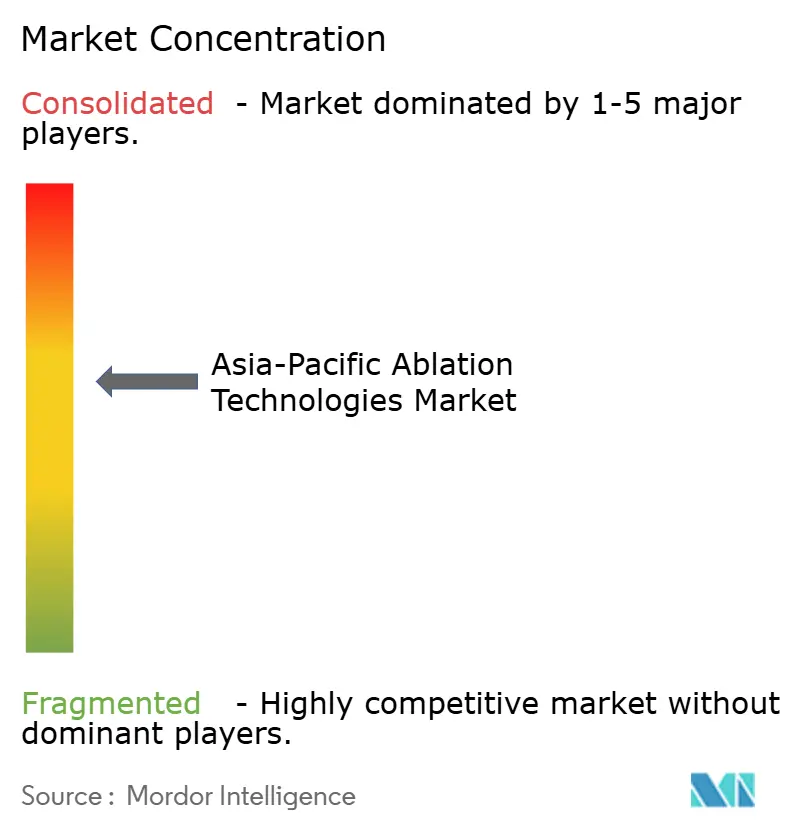

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Ablation Technologies Market Analysis by Mordor Intelligence

The Asia-Pacific Ablation Technologies Market size is expected to grow from USD 1.05 billion in 2025 to USD 1.17 billion in 2026 and is forecast to reach USD 2.02 billion by 2031 at 11.57% CAGR over 2026-2031.

Demand is escalating as cancer, cardiovascular disease, and benign prostatic hyperplasia reshape treatment algorithms across China, India, and Southeast Asia. Shorter recovery windows and lower complication rates than with open surgery position energy-based ablation make it a preferred option when hospital bed capacity is constrained. The Asia-Pacific ablation technologies market benefits from rising health budgets that equip second-tier cities with interventional radiology suites. Localization of manufacturing is trimming landed costs for consumables, while payers steer elective cases toward ambulatory centers to curb inpatient spending. Competitive intensity is rising as multinationals add factories in China and India that meet local-content rules, even as regional firms exploit clinical networks to win tenders.

Key Report Takeaways

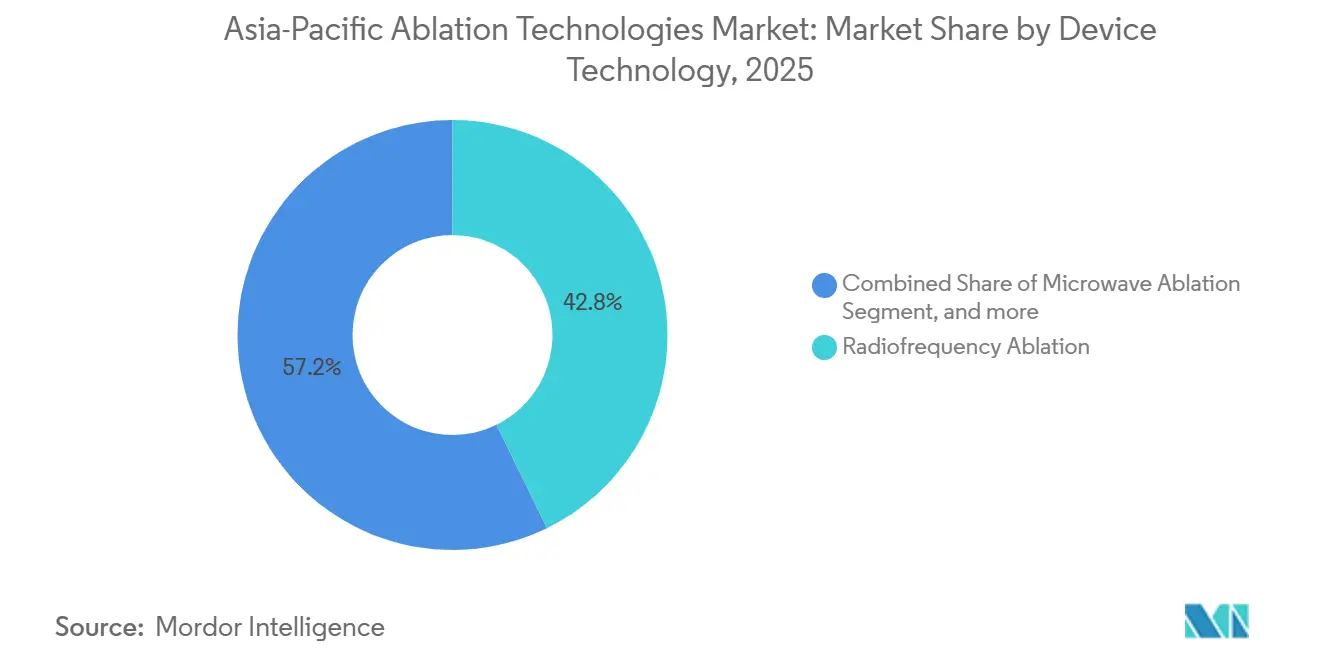

- By device technology, radiofrequency ablation led with a 42.76% share of the Asia-Pacific ablation technologies market in 2025. Microwave ablation is forecast to record the fastest growth, advancing at a 13.65% CAGR through 2031.

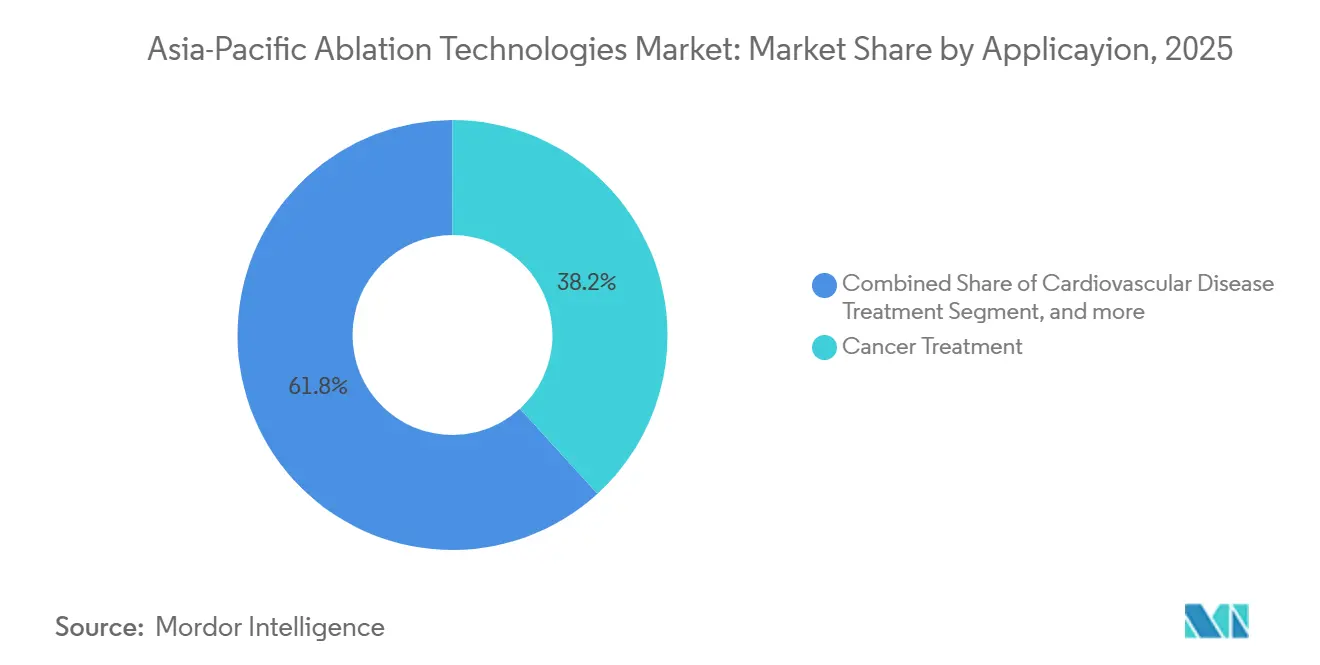

- By application, cancer treatment accounted for 38.22% of revenue in 2025, whereas urological procedures are projected to expand at a 13.43% CAGR through 2031.

- By end user, hospitals held 55.35% of spending in 2025, while ambulatory surgical centers are on track for a 14.22% CAGR through 2031.

- By country, China commanded 34.32% of 2025 regional sales, and India is set to post a 12.54% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Ablation Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Chronic Diseases | +3.2% | China, India, Southeast Asia | Long term (≥ 4 years) |

| Patient Preference For Minimally Invasive Therapy | +2.8% | Japan, Australia, South Korea | Medium term (2-4 years) |

| Continuous Technology Advancements | +2.5% | China, Japan, South Korea | Medium term (2-4 years) |

| Expanding Healthcare Expenditure | +2.1% | India, Indonesia, Vietnam, Philippines | Long term (≥ 4 years) |

| Localization Of Manufacturing | +1.6% | China, India | Short term (≤ 2 years) |

| AI-Enabled Real-Time Guidance | +1.1% | Japan, South Korea, Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic Diseases

Cancer incidence across Asia-Pacific is projected to jump 59% between 2022 and 2045, lifting demand for percutaneous radiofrequency and microwave ablation in liver, lung, and gastric malignancies. Cardiovascular disease caused 10.8 million regional deaths in 2019, fueling catheter-based ablation for atrial fibrillation and ventricular tachycardia. China recorded a 12% year-on-year increase in electrophysiology procedures in 2024, following expanded reimbursement for ablation[1]National Health Commission of China, “2024 Electrophysiology Procedure Report,” NHC.GOV.CN. Diabetes prevalence above 11% in India and Indonesia increases diabetic retinopathy cases that rely on laser photocoagulation. Benign prostatic hyperplasia affects nearly half of Japanese men over 60, sustaining demand for transurethral radiofrequency and water-vapor therapies.

Patient Preference for Minimally Invasive Therapy

A 2024 survey of 1,200 Japanese cardiac patients found 78% favored catheter ablation over antiarrhythmic drugs to manage atrial fibrillation, citing quality-of-life gains. South Korea’s insurance data showed a 19% jump in same-day discharge ablation procedures during 2023-2025 as hospitals adopted enhanced recovery pathways. Australian private insurers lowered co-pays for microwave ablation of varicose veins and thyroid nodules, cutting average episode costs by 32% in 2025. Across high out-of-pocket markets, patients weigh the direct costs of hospital stays against income lost to prolonged recovery, accelerating outpatient adoption.

Continuous Technology Advancements

Pulsed-field ablation delivers non-thermal energy that reduces esophageal and phrenic nerve injury during atrial fibrillation therapy. Boston Scientific’s FARAPULSE system recorded a 2.1% esophageal injury rate, compared with 5.8% for radiofrequency, in a 1,200-patient registry that began clinical use in Japan and Australia in 2024. Medtronic’s PulseSelect platform obtained Chinese clearance in February 2025, eliminating tariffs on imported consoles. Microwave generators now feature temperature feedback and power modulation, which reduce incomplete tumor necrosis rates in liver and lung lesions[2]Journal of Vascular and Interventional Radiology, “Meta-analysis of Microwave vs Radiofrequency Ablation,” JVIR.ORG. Cryoablation platforms integrate ultrasound guidance to monitor ice-ball formation, trimming procedure time by 18 minutes in a 2025 Australian cohort.

Expanding Healthcare Expenditure

China’s health spending grew 7.5% annually from 2020-2025, funding tier-two oncology and cardiology centers equipped with ablation suites. India’s 2025-2026 Union Budget raised health allocations by 12%, earmarking funds for district hospital radiofrequency and microwave systems. Indonesia’s BPJS Kesehatan added percutaneous ablation for hepatocellular carcinoma to its coverage in January 2025, benefiting 230 million enrollees. Vietnam secured a USD 500 million Asian Development Bank loan in mid-2025 to upgrade 50 provincial hospitals with interventional radiology hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Consumable Costs | -0.8% | Asia-Pacific Tier-1 & Tier-2 urban centers | Short term (≤ 2 years) |

| Limited Skilled Workforce Outside Major Cities | -0.6% | Secondary and tertiary cities across Asia-Pacific | Medium term (2-4 years) |

| Fragmented Regulatory Approval Pathways Across Asia-Pacific | -0.7% | Multi-country Asia-Pacific | Long term (≥ 4 years) |

| Concerns Over Long-Term Efficacy Data In Non-Oncologic Indications | -0.5% | Global, with heightened scrutiny in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs

Radiofrequency generators cost USD 80,000-120,000, while single-use catheters add USD 1,500-3,000 per case, stretching public-hospital budgets in India, Indonesia, and the Philippines that rely on capitated reimbursement models. Indonesia reimburses liver ablation at IDR 25 million (USD 1,600), below the USD 2,200 antenna cost, forcing hospitals to absorb losses or cap volumes. Pay-per-use leasing trims upfront outlays by 70% but lifts per-case costs by 15% over five years.

Limited Skilled Workforce Outside Major Cities

China’s tier-one cities house 68% of board-certified electrophysiologists, yet only 12% of the population[3]Chinese Medical Association, “Electrophysiologist Workforce Survey 2025,” CMA.ORG.CN. India produced 320 interventional radiology fellows in 2024, well below the 1,200 needed to staff new ablation suites. ASEAN averages 4.2 electrophysiologists per million residents, compared with 12.8 in Japan and South Korea. Remote proctoring cut complication rates by 28% in an 85-procedure Chinese pilot where Shanghai experts guided Chengdu physicians via Abbott’s tele-navigation platform.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Technology: Microwave Extends Reach

Microwave ablation registered a 13.65% CAGR outlook through 2031, gaining on the 42.76% 2025 lead held by radiofrequency. The Asia-Pacific ablation technologies market size for microwave systems is projected to widen as oncologists value larger ablation zones and shorter procedure times in hepatocellular carcinoma and lung metastases. A 2024 meta-analysis covering 3,200 patients showed complete necrosis in 91% of sub-3 cm liver lesions with microwave versus 84% for radiofrequency, and required 19% fewer sessions. Medtronic’s Emprint system, approved in China in 2024 with thermosphere stabilization, resonated with cirrhotic patient cohorts in which radiofrequency efficacy declines due to ascites.

Radiofrequency remains dominant in electrophysiology because contact-force sensing allows real-time lesion assessment during atrial fibrillation procedures. Cryoablation owns a niche in renal tumors and atrial fibrillation, with Medtronic’s Arctic Front Advance capturing 18% of Japan’s 2025 AF ablation market by simplifying pulmonary vein isolation. Ultrasound-based ablation, led by Chongqing Haifu, is widely installed for uterine fibroids at 2,400 Chinese hospitals, although cross-specialty adoption is slower due to lengthy treatment times. Pulsed-field ablation commands a premium price 30% above standard radiofrequency yet is winning early adopters in Japan and Australia on safety gains.

By Application: Urology Accelerates on Aging Demographics

Cancer therapy represented 38.22% of 2025 revenue, but urological procedures are growing 13.43% per year as small renal masses and benign prostatic hyperplasia migrate to minimally invasive care. The Asia-Pacific population aged ≥65 will reach 630 million by 2030, with benign prostatic hyperplasia affecting 50% of the cohort and driving transurethral radiofrequency and water-vapor therapy volumes. Boston Scientific’s Rezum water-vapor therapy cut the International Prostate Symptom Score by 68% at 12 months for 420 Japanese patients, avoiding surgery in 89% of cases. Cryoablation for T1a renal carcinoma delivered 97% five-year cancer-specific survival in a 2025 Australian cohort while halving complications versus partial nephrectomy.

Cardiovascular care is the second-largest application, with China surpassing 180,000 atrial fibrillation ablation cases in 2025 after reimbursement expanded to include pulsed-field technology. Ophthalmology remains stable in mature economies, yet scales in India, where 450 district hospitals acquired retinal lasers during 2024-2025. Cosmetic ablation for skin resurfacing and body contouring boosted South Korean device sales to USD 1.2 billion in 2025.

By End User: Ambulatory Centers Take Elective Case Mix

Hospitals accounted for 55.35% of 2025 revenue, but ambulatory surgical centers (ASCs) are projected to grow at a 14.22% CAGR through 2031 as payers migrate elective ablation procedures out of costly inpatient wards. China’s 2024 guidelines allowed standalone ASCs to perform radiofrequency ablation for varicose veins and thyroid nodules, sparking private-equity investment. India’s ASC landscape expanded by 23% in 2025, with chains like Pristyn Care operating 50+ centers targeting digitally sourced self-pay patients. Australian insurers waived co-pays for varicose vein ablation performed in day-surgery facilities, lowering average costs from AUD 8,500 (USD 5,500) in hospitals to AUD 4,200 (USD 2,700) in ASCs.

Complex oncologic and cardiac cases still cluster at tertiary hospitals that possess hybrid operating rooms and onsite surgical bail-out. Specialty clinics and pain centers are carving niches in spinal facet ablation and dermatology laser procedures, supported by aging populations in Singapore and South Korea.

Geography Analysis

China held 34.32% of 2025 sales, underpinned by accelerated device approvals and Healthy China 2030 infrastructure spending that channels USD 12 billion into oncology centers. Volume-based procurement reduced ablation catheter prices by 38% in 2024, broadening access yet squeezing margins for importers lacking local plants. The Asia-Pacific ablation technologies market in India is poised for a 12.54% CAGR, driven by tariff cuts via production-linked incentives and doubled training seats for interventional radiology fellows. Japan and South Korea expand cryoablation on the back of aging demographics, while Australia integrates laser systems across private networks, with insurers steering patients to outpatient settings.

The rest of Asia-Pacific leverages ASEAN mutual recognition, which reduces device registration time from 24 to 9 months. Indonesia’s reimbursement unlocks access for 230 million citizens, yet pays 35% under the procedure cost, prompting high-volume supplier discounts. Vietnam’s ADB-backed upgrades aim to double ablation capacity by 2028.

Competitive Landscape

The Asia-Pacific ablation technologies market remains moderately fragmented. Multinationals — Boston Scientific, Abbott, Medtronic, and Johnson & Johnson — collectively hold roughly 55% of revenue thanks to diversified cardiac, oncologic, and urologic portfolios. Regional firms such as Chongqing Haifu, STARmed, and RF Medical leverage cost advantages and local distribution to win tenders in China and South Korea. Boston Scientific gained 23% of new Japanese AF accounts in 2025 with FARAPULSE, which delivers non-thermal pulsed-field energy and lowers collateral injury. Medtronic’s February 2025 Chinese PulseSelect clearance positions it to challenge incumbents in a 180,000-procedure electrophysiology market. Abbott’s Bangalore-built TactiFlex catheter undercuts imports by 25% in Indian tenders.

Patent filings for AI-guided navigation climbed 34% in 2024-2025, led by Johnson & Johnson’s Carto 3 mapping that shaved 22 minutes from procedure time in Korea. White-space potential exists in urological ablation, where Boston Scientific’s Rezum and Olympus’ transurethral systems tap aging male populations in Japan and South Korea. Consolidation is gathering pace as Stryker’s 2024 Vocera acquisition embeds workflow software into ablation suites, and private equity groups roll up ASC chains to enhance purchasing power.

Asia-Pacific Ablation Technologies Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic PLC

Conmed Corporation

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: MicroPort EP launched PulseMagic TrueForce, a single-use pressure-sensing pulsed-field ablation (PFA) catheter, in China, according to the China’s National Medical Products Administration (NMPA).

- July 2025: Johnson & Johnson MedTech, one of the global leaders in cardiac arrhythmia treatment, launched the VARIPULSE Platform in the Asia-Pacific. The platform is used to perform catheter ablation procedures for atrial fibrillation (AFib), an irregular and often rapid heartbeat caused by extra, uncoordinated electrical signals in the atria.

- May 2024: Medtronic launched the PulseSelect pulsed field ablation (PFA) system in Japan, broadening the global reach of the proven safe and effective technology for the treatment of paroxysmal and persistent atrial fibrillation (AFib) patients.

Asia-Pacific Ablation Technologies Market Report Scope

As per the scope of the report, ablation generally refers to the surgical removal of a part of biological tissue. Ablation devices offer a minimally invasive alternative to traditional surgical treatment of liver, prostate, kidney, and lung cancers.

The Asia-Pacific Ablation Technologies Market is Segmented by Device Technology (Radiofrequency Devices, Laser/Light Ablation, Ultrasound Devices, Cryoablation Devices, and Other Devices), Application (General Surgery, Cardiovascular Disease Treatment, Cancer Treatment, Ophthalmological Treatment, Gynecological Treatment, Urological Treatment, Cosmetic Surgery, and Other Applications), End User (Hospitals, Ambulatory Surgical Centers, and Other End Users), and Geography (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific). The report offers the value (in USD million) for the above segments.

By Device Technology

| Radiofrequency Ablation |

| Microwave Ablation |

| Laser/Light Ablation |

| Ultrasound-Based |

| Cryoablation |

| Other Devices |

By Application

| Cancer Treatment |

| Cardiovascular Disease Treatment |

| Ophthalmologic Treatment |

| Gynecological Treatment |

| Urological Treatment |

| Cosmetic Surgery |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgical Centers |

| Other End Users |

Geography

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest Of Asia-Pacific |

| By Device Technology | Radiofrequency Ablation |

| Microwave Ablation | |

| Laser/Light Ablation | |

| Ultrasound-Based | |

| Cryoablation | |

| Other Devices | |

| By Application | Cancer Treatment |

| Cardiovascular Disease Treatment | |

| Ophthalmologic Treatment | |

| Gynecological Treatment | |

| Urological Treatment | |

| Cosmetic Surgery | |

| Other Applications | |

| By End User | Hospitals |

| Ambulatory Surgical Centers | |

| Other End Users | |

| Geography | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest Of Asia-Pacific |

Key Questions Answered in the Report

What revenue is forecast for Asia-Pacific ablation technologies by 2031?

Sales are projected to reach USD 2.02 billion by 2031, growing at a 13.33% CAGR from 2026.

Which device technology is expected to grow the fastest through 2031?

Microwave ablation is set to expand at a 13.65% CAGR, outpacing radiofrequency systems.

How large was China's share of regional ablation sales in 2025?

China accounted for 34.32% of Asia-Pacific revenue in 2025.

Why are ambulatory surgical centers gaining procedure volumes?

Payers and patients seek lower costs and quicker recovery, driving a 14.22% CAGR for ASC ablation volumes through 2031.

Which clinical application currently generates the most revenue?

Cancer treatment leads, contributing 38.22% of 2025 sales.

What main barrier slows adoption in lower-income Southeast Asian hospitals?

High capital equipment and consumable costs strain budgets under capitated reimbursement schemes.

Page last updated on: