Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

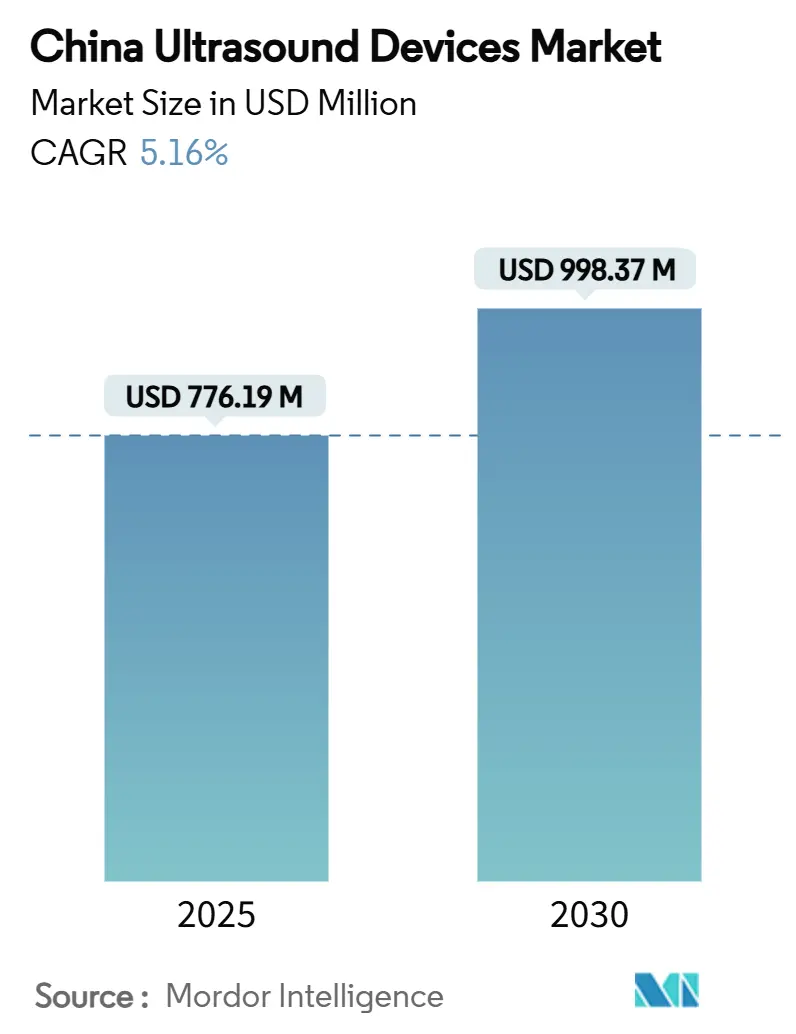

| Market Size (2025) | USD 776.19 Million |

| Market Size (2030) | USD 998.37 Million |

| Growth Rate (2025 - 2030) | 5.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Ultrasound Devices Market Analysis by Mordor Intelligence

The China Ultrasound Devices Market size is estimated at USD 776.19 million in 2025, and is expected to reach USD 998.37 million by 2030, at a CAGR of 5.16% during the forecast period (2025-2030).

Rising chronic disease prevalence, government-funded imaging upgrades, and the mandatory ≥85% local-content rule are strengthening domestic manufacturing capacity. At the same time, point-of-care adoption, rapid AI approvals, and sustained rural health spending continue to widen the clinical footprint of the China ultrasound devices market. Price erosion triggered by volume-based procurement and tighter post-market surveillance act as checks on margins, yet well-capitalized vendors are exploiting acquisition and partnership openings to secure long-term growth. Competitive positioning now hinges on AI-driven workflow tools, integrated service contracts, and the ability to localize production while meeting evolving NMPA standards.

Key Report Takeaways

- By technology, 3D & 4D equipment led with 39.33% of China ultrasound devices market share in 2024, while high-intensity focused ultrasound is projected to expand at a 6.68% CAGR to 2030.

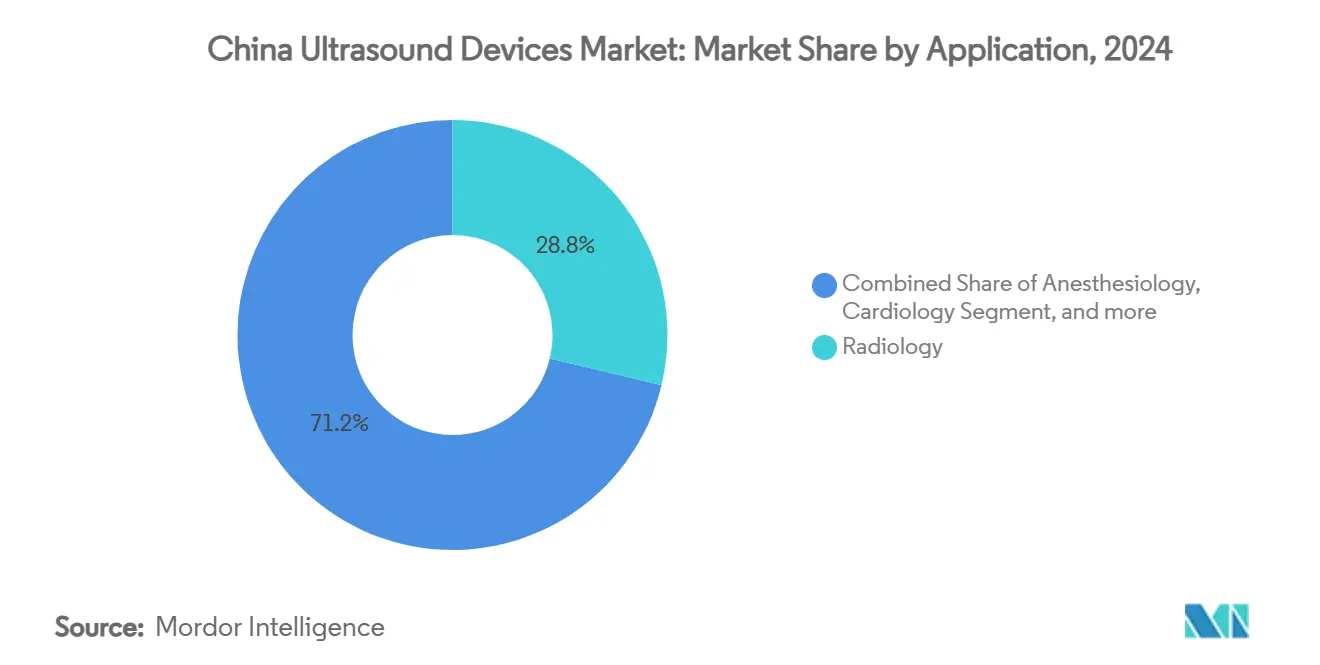

- By application, radiology accounted for 28.76% of the China ultrasound devices market size in 2024 and critical care is advancing at a 7.31% CAGR through 2030.

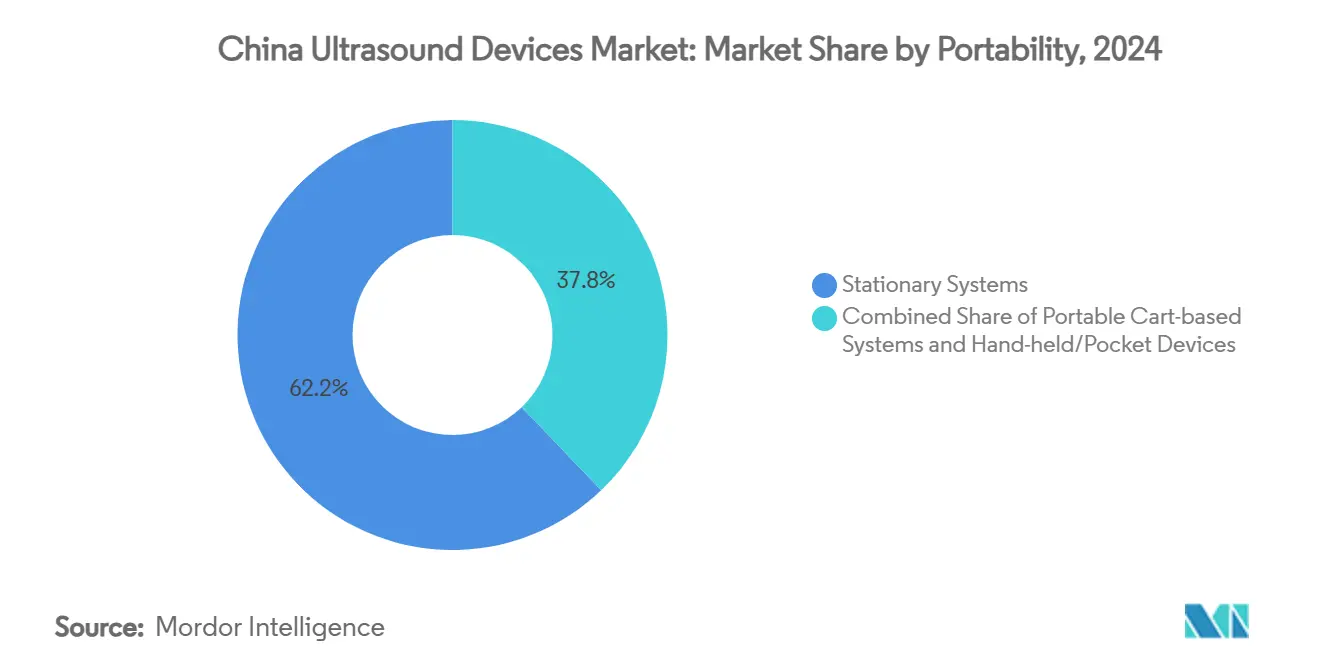

- By portability, stationary systems commanded 62.16% revenue share of the China ultrasound devices market in 2024, whereas handheld devices post the fastest 9.11% CAGR to 2030.

- By end user, hospitals represented 48.25% of the China ultrasound devices market size in 2024, while ambulatory and day-care centers record an 8.37% CAGR to 2030.

China Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Chronic & Lifestyle Diseases | +1.2% | National, with higher concentration in urban areas | Long term (≥ 4 years) |

| Government-Funded Imaging Equipment Upgrades | +0.9% | National, with priority focus on county hospitals and rural areas | Medium term (2-4 years) |

| Rapid Adoption of Point-of-Care & Handheld Ultrasound | +0.8% | National, with early adoption in tier-1 cities expanding to lower tiers | Short term (≤ 2 years) |

| AI-Enabled Image Reconstruction & Workflow Automation | +0.7% | National, with concentration in major medical centers | Medium term (2-4 years) |

| Mandatory ≥85% Local-Content Policy Favoring Domestic OEMs | +0.6% | National policy with uniform implementation | Long term (≥ 4 years) |

| Expansion of Healthcare Infrastructure | +0.5% | National, with emphasis on western and central regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic & Lifestyle Diseases

China’s population aged ≥65 years is expected to reach 400 million by 2050, driving ultrasound demand in cardiology, oncology, and diabetes management. Per-capita health spending ranged from RMB 460.1 in Tibet to RMB 3,274.5 in Beijing in 2024, illustrating regional gaps addressed by the Healthy China 2030 plan that caps out-of-pocket costs at 25%.[1]National Health Commission, “China Health Statistical Yearbook 2025,” nhc.gov.cn Hospital planners now favor high-throughput consoles that preserve image quality under heavier workloads. Tele-ultrasound, backed by 5G pilots, has proven effective for remote diagnostics in county hospitals.[2]Frontiers in Public Health, “5G-Based Robot-Assisted Ultrasound in Rural China,” frontiersin.org The demographic shift secures a durable case load for the China ultrasound devices market, prompting OEMs to integrate ergonomics and AI triage that cut scan times.

Government-Funded Imaging Equipment Upgrades

Central subsidies support ultrasound replacement cycles across 2,000 county hospitals, prioritizing local OEMs in tender awards.[3]National Healthcare Security Administration, “Volume-Based Procurement Update 2024,” nhsa.gov.cn The National Health Commission has also seeded 14 medical-imaging data-lake projects to improve algorithm training. Western and central provinces receive preferential capital budgets, encouraging hospitals to purchase modular platforms that lower lifetime costs. Procurement teams now require bundled service contracts covering software upgrades, which steers buyers toward scalable systems. These factors provide tailwinds for the China ultrasound devices market, particularly for vendors offering local manufacturing footprints.

Rapid Adoption of Point-of-Care & Handheld Ultrasound

The pandemic highlighted the infection-control benefits of handheld scanners, which performed lung and abdominal exams in isolation wards using the BLUE protocol. Mission Harmony showed handheld durability with 3,126 remote-site examinations onboard the PLA (N) Peace Ark hospital ship. Emergency physicians now rely on wireless probes that pair with smartphones to shorten triage times. Provincial trauma networks are equipping ambulances with pocket devices, expanding the China ultrasound devices market beyond hospital walls. OEMs answer this need with ruggedized, battery-efficient models and companion cloud platforms for image archiving.

AI-Enabled Image Reconstruction & Workflow Automation

NMPA cleared 70 imaging-AI products by 2024, and the Chinese Radiology Society formed an AI subgroup to formalize adoption pathways. In ultrasound departments, the physician-to-patient ratio slipped from 1.05:10,000 in 2017 to 0.96:10,000 in 2024, fueling algorithmic assistance. Solutions such as the Dr.J breast-cancer workflow allow nurses to capture standardized scans, lowering skill barriers. Robotic arms further improve reproducibility and dataset quality for AI training. As a result, diagnostic turnaround shrinks, making AI a centerpiece of the China ultrasound devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CFDA Approval Timelines & Post-Market Surveillance Tightening | -0.8% | National, affecting all manufacturers equally | Short term (≤ 2 years) |

| GPO-Driven Price Cuts Squeezing OEM Margins | -1.1% | National, with varying intensity by province | Medium term (2-4 years) |

| High Cost of Premium 3D/4D & CEUS Platforms | -0.6% | National, with higher impact in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Shortage of Skilled Sonographers in Lower-Tier Cities | -0.7% | Central and western regions, rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CFDA Approval Timelines & Post-Market Surveillance Tightening

Class II registrations now average 155 working days and USD 28,850 in fees, while Class III processes approach 185 days, increasing compliance costs. The 2024 Standards Catalogue update mandates in-country clinical data, extending pilot timelines. Post-market oversight calls for real-time adverse-event tracking, pushing OEMs to invest in digital vigilance systems. Although “green channel” reviews exist for breakthrough devices, smaller firms lack resources to exploit them, tempering innovation momentum in the China ultrasound devices market.

Group Purchasing-Organization Price Cuts

Centralized volume tenders shaved nearly 70% off median prices for high-value consumables and more than 60% in Shanghai’s pilot device tender. A monopsony dynamic forces OEMs to revise cost structures and shift engagement from clinicians to procurement bureaus. Domestic suppliers, backed by tax credits and land incentives, hold an edge in bid scoring, squeezing multinational margins further. Companies must now bundle service warranties and AI add-ons to defend pricing in the China ultrasound devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Critical Care Drives Specialized Growth

Radiology retained 28.76% of China ultrasound devices market share in 2024, underpinned by its central role in comprehensive diagnostic pathways. Portable consoles equipped with AI lesion quantification enable radiology units to handle growing chronic-disease screening volumes efficiently. Critical care logged a 7.31% CAGR, propelled by intensivists adopting bedside echo and lung protocols during ventilator management. Cardiology applications benefit from 3D strain imaging that guides transcatheter procedures, while gynecology/obstetrics maintains stable demand through universal prenatal screening.

The China ultrasound devices market size attributable to critical care reflecting expanded emergency-department budgets and reimbursement of point-of-care scans. Musculoskeletal and urology segments also rise as sports-injury clinics and nephrology centers digitize records for AI analytics. National clinical-practice guidelines now list ultrasound as first-line for deep-vein thrombosis evaluation, boosting vascular workload. Across applications, vendors localize user interfaces in Mandarin and regional dialects to shorten training times.

By Technology: HIFU Innovation Reshapes Treatment Paradigms

3D & 4D platforms hold 39.33% of China ultrasound devices market whereas high-intensity focused ultrasound (HIFU) commands the fastest 6.68% CAGR as Chinese firms scale non-invasive oncology and fibroid therapies. Treatment volumes tripled between 2018 and 2024 in tertiary oncology centers, where HIFU shortens bed stays and lowers infection risk. The China ultrasound devices market size for 3D & 4D units reached driven by fetal anomaly screening and valve-repair planning.

AI-augmented Doppler modules now auto-grade stenosis and generate structured vascular reports, cutting scan times by 30%. Meanwhile, 2D systems stay relevant in rural clinics due to affordability, especially when bundled with cloud PACS subscriptions. Software-defined architectures allow hospitals to unlock contrast-enhanced ultrasound (CEUS) via license keys instead of hardware swaps, extending asset life and smoothing capital allocation within the China ultrasound devices market.

By Portability: Handheld Revolution Transforms Care Delivery

Stationary consoles accounted for 62.16% of China ultrasound devices market revenue in 2024, retaining primacy in cardiac cath labs and oncology suites where image fidelity is paramount. Yet handheld scanners exhibited a 9.11% CAGR, empowered by smartphone connectivity and enterprise encryption that satisfies hospital cybersecurity rules.

Cart-based mobile units occupy the middle ground, featuring trolley designs with battery packs for ward rounds. Field medics and telemedicine hubs in Xinjiang now deploy pocket probes linked via 5G to urban specialists, widening clinical reach. Proprietary app stores host AI plugins for bladder volume and nerve-block guidance, supporting anesthesia departments. Collectively, portability innovations diversify the China ultrasound devices market and reinforce its resilience against procurement cycles.

By End User: Ambulatory Care Expansion Accelerates

Hospitals held 48.25% of China ultrasound devices market size in 2024, reflecting their concentration of high-acuity cases and financing capacity. However, ambulatory and day-care centers posted an 8.37% CAGR as payment reforms steered elective surgeries to outpatient settings. Diagnostic imaging chains now acquire mid-range scanners in bulk, leveraging economies of scale.

Primary-care clinics integrate handheld devices to confirm gallstones or obstetric viability, avoiding costly referrals. Government-backed county hospital upgrades foster tiered referral systems where lower-level facilities perform preliminary scans and transmit images upstream. This redistribution of service points sustains equipment demand across all tiers of the China ultrasound devices market.

Geography Analysis

Eastern municipalities such as Beijing, Shanghai, and Guangdong cluster the majority of high-end installations, buoyed by per-capita healthcare spending of RMB 3,274.5 in Beijing versus RMB 460.1 in Tibet. Tertiary centers procure 3D/4D consoles with AI fetal screening modules, driving premium growth in the China ultrasound devices market. The number of Class III-A hospitals rose from 647 in 2006 to 1,580 in 2024, yet distribution remains uneven, prompting policy to rebalance resources.

Central provinces receive higher capital-equipment subsidies, spurring procurement of modular mid-range systems that can upgrade to CEUS via software unlocks. Western regions, prioritizing maternal-infant initiatives, favor portable probes compatible with tele-consultation. Guangxi data show imaging assets clustered in Nanning, Guilin, and Liuzhou, leaving rural counties reliant on outreach clinics.

Tele-ultrasound pilots using robotic arms and 5G links connect Sichuan’s township clinics with Chengdu radiologists, shrinking diagnostic delays. AI decision support compensates for skill deficits, boosting scan confidence in understaffed facilities. As provincial budgets rise, the China ultrasound devices market finds fresh openings for AI-ready, entry-level consoles that bridge urban-rural care gaps.

Competitive Landscape

Domestic manufacturers grew their diagnostic, powered by the ≥85% local-content mandate. Mindray set a regulatory benchmark in 2024 when its Resona 7 earned EU MDR certification, the first Chinese ultrasound platform to do so. Market concentration intensified after volume-based procurement cut average prices for coronary stents by 93% and pressured device vendors to streamline distribution.

International firms face direct competition from localized production lines and provincial incentives favoring domestic bids. In response, several multinationals have inked technology-transfer deals with state-owned enterprises to secure tender eligibility. Product differentiation now revolves around AI-driven ergonomics and remote-service diagnostics that minimize downtime.

Focused ultrasound therapy remains a white-space segment, with Chongqing Haifu exporting systems to 30 countries and expanding domestic installations in oncology centers. Robotic ultrasound startups attract venture capital by automating obstetric scans, an approach that could disrupt mid-tier console demand. Overall, strategic M&A and joint ventures shape the hierarchy within the China ultrasound devices market.

China Ultrasound Devices Industry Leaders

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Canon Medical Systems Corporation

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The State Council issued comprehensive reform guidelines for drug and medical device regulation, targeting establishment of a modernized regulatory framework by 2027 with enhanced review processes for innovative devices and improved support for R&D activities

- October 2024: GE Healthcare signed a cooperation agreement to establish its Greater China ultrasound headquarters in Wuxi New District, enhancing innovation and research capabilities with a comprehensive ultrasound business ecosystem including innovation center, service center, and customer experience center

China Ultrasound Devices Market Report Scope

Sonography, another name for diagnostic ultrasonography, is an imaging method that creates images of various body structures using high-frequency sound waves. They are used to evaluate a variety of disorders relating to the liver, kidneys, and other abdominal conditions. They are also widely used to treat chronic illnesses, which include ailments including diabetes, asthma, cancer, and heart disease.

The China ultrasound devices market is segmented by application, technology, and type. By application, the market is segmented into anesthesiology, cardiology, gynecology/obstetrics, musculoskeletal, radiology, critical care, and other applications. By technology, the market is segmented into 2D ultrasound imaging, 3D and 4D ultrasound imaging, doppler imaging, and high-intensity focused ultrasound. By type, the market is segmented into stationary ultrasound and portable ultrasound. The report offers the value (in USD) for all the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology / Obstetrics |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Hospitals |

| Diagnostic Imaging Centres |

| Ambulatory & Day-Care Centres |

| Other End Users |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology / Obstetrics | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Hospitals |

| Diagnostic Imaging Centres | |

| Ambulatory & Day-Care Centres | |

| Other End Users |

Key Questions Answered in the Report

How large is the China ultrasound devices market in 2025?

The China ultrasound devices market size is USD 776.19 million in 2025.

What is the forecast CAGR for China ultrasound equipment through 2030?

The market is projected to grow at a 5.16% CAGR from 2025 to 2030.

Which technology segment is expanding fastest?

High-intensity focused ultrasound records the highest 6.68% CAGR through 2030.

Why are handheld scanners gaining popularity?

Handheld devices offer infection-control benefits, smartphone connectivity, and improve bedside diagnostics, supporting a 9.11% CAGR.

How do volume-based procurements impact prices?

Centralized tenders have trimmed ultrasound-related device prices by up to 60%, pressuring OEM margins yet broadening access.

Which regions present untapped growth potential?

Central and western provinces, where infrastructure upgrades and tele-ultrasound pilots meet underserved populations, represent high-growth corridors.

Page last updated on: