Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

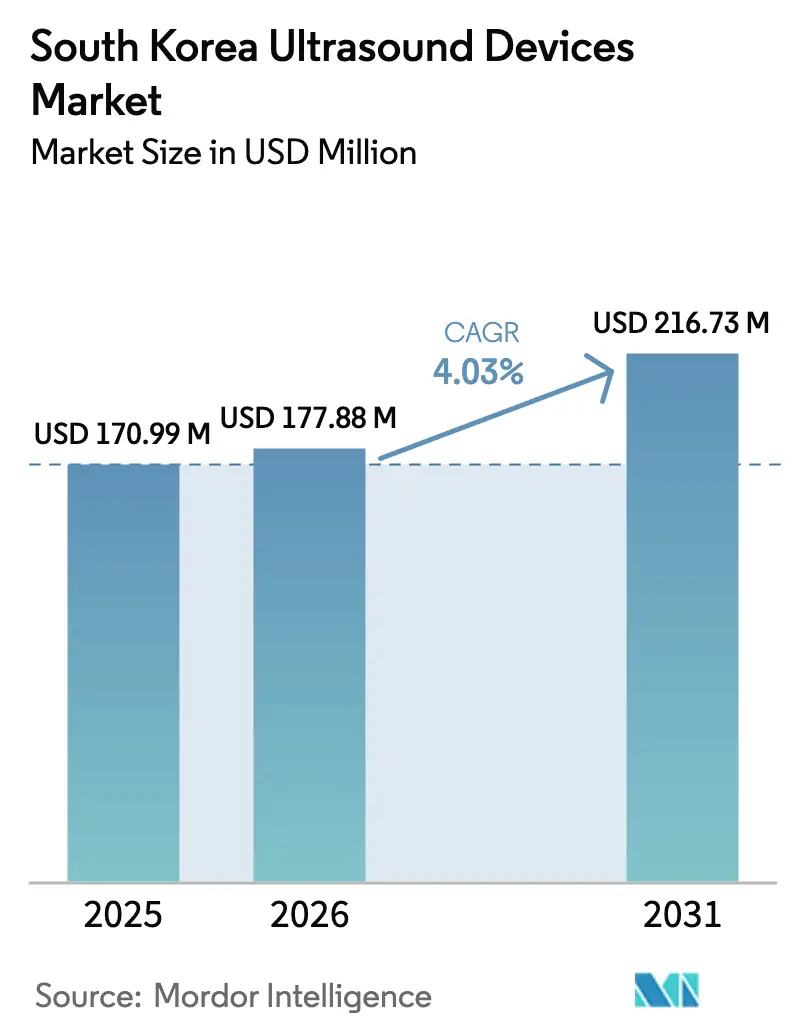

| Base Year Market Size (2025) | USD 170.99 Million |

| Market Size (2026) | USD 177.88 Million |

| Market Size (2031) | USD 216.73 Million |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Ultrasound Devices Market Analysis by Mordor Intelligence

South Korea Ultrasound Devices Market size in 2026 is estimated at USD 177.88 million, growing from 2025 value of USD 170.99 million with 2031 projections showing USD 216.73 million, growing at 4.03% CAGR over 2026-2031.

The projected increase reflects a shift from unit growth toward higher-value technology upgrades, with reimbursement expansion and artificial-intelligence (AI) integration driving demand. Hospitals still lead purchases, yet the wider National Health Insurance (NHI) coverage for seven prenatal scans and for urogenital imaging has bolstered patient access, anchoring revenue in obstetrics and gynecology (OB/GYN). Rapid adoption of 3D/4D systems, handheld devices for critical care, and high-intensity focused ultrasound (HIFU) for therapeutic use underscores a technology-led growth pattern. Corporate competition has pivoted to AI capabilities after Samsung Medison acquired Sonio, while Siemens Healthineers and GE Healthcare added AI toolsets through product launches and acquisitions. South Korea’s population aging past 20% over 65 in 2025 ensures long-term imaging demand, although sonographer shortages and strict regulatory pathways temper near-term growth.

Key Report Takeaways

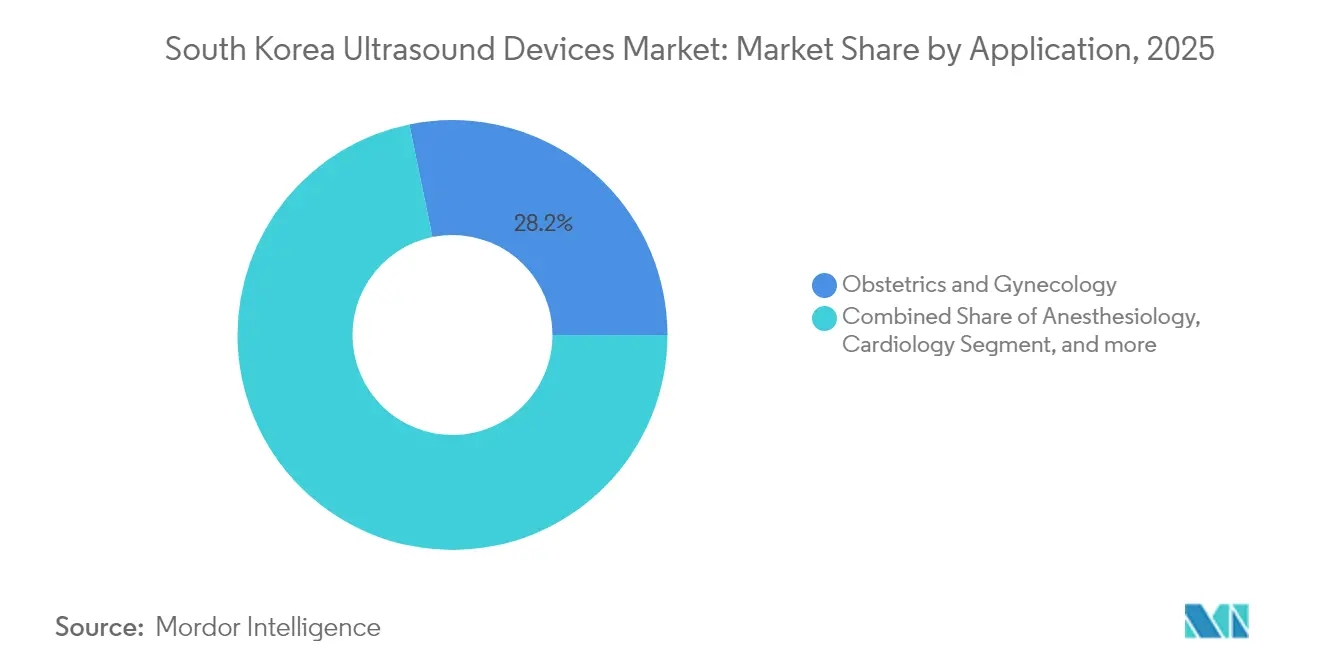

- By application, obstetrics and gynecology led with 28.22% of the South Korea ultrasound devices market share in 2025, while critical care is projected to record the fastest 5.27% CAGR through 2031.

- By technology, 3D & 4D ultrasound accounted for 39.52% of the South Korea ultrasound devices market size in 2025, whereas high-intensity focused ultrasound is anticipated to advance at a 4.85% CAGR to 2031.

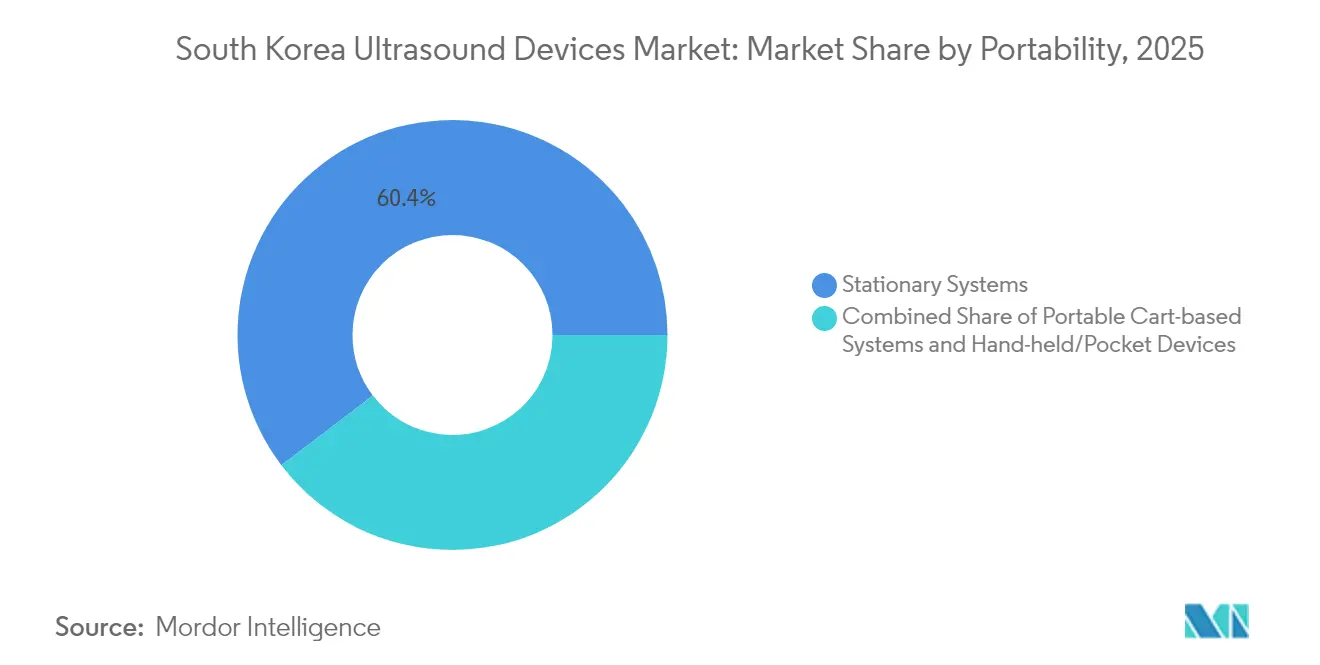

- By portability, stationary systems held 60.35% revenue share in 2025, while hand-held or pocket devices are expected to expand at a 6.52% CAGR over the forecast horizon.

- By end user, hospitals captured 47.86% of sales in 2025, yet ambulatory surgical centers are set to grow the fastest at 6.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric population & imaging demand | +1.2% | National, higher impact in rural regions | Long term (≥ 4 years) |

| Government reimbursement expansion for point-of-care ultrasound | +1.0% | Nationwide | Medium term (2-4 years) |

| Technological advancements in transducer miniaturization | +0.6% | Global technology, local uptake | Short term (≤ 2 years) |

| Integration with AI-based diagnostic algorithms | +0.7% | Technology hubs and leading hospitals | Short term (≤ 2 years) |

| Increasing burden of chronic diseases | +0.8% | Metropolitan concentration | Medium term (2-4 years) |

| Growth of precision medicine & image-guided interventions | +0.4% | Tertiary centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population & Imaging Demand

By 2025 one in five South Koreans is at least 65, creating sustained ultrasound demand for liver, gallbladder and cardiovascular assessments.[1]Bibek Giri et al., “Aging Population in South Korea: Burden or Opportunity?,” IJS Global Health, ijsgh.com Community-care pilots now reimburse in-home scans, encouraging providers to deploy portable units. Rural clinics increasingly rely on pocket devices for chronic-disease monitoring, widening geographic adoption. Hospital administrators report higher sonography workloads, spurring investment in workflow-optimizing AI. While the demographic trend secures volume growth, it tightens budgets and heightens workforce shortages, requiring training incentives for regional technologists.

Government Reimbursement Expansion for Point-of-Care Ultrasound

The NHI cut patient out-of-pocket costs for abdominal and kidney scans by as much as 70%, boosting examination volumes across outpatient sites. Coverage now extends to automated breast ultrasound and musculoskeletal exams, broadening clinical indications. Expanded reimbursement secures predictable cash-flows that justify capital purchases at ASCs. Yet quality-assurance audits reveal variable accuracy when scans are performed by non-physicians, prompting new certification guidelines.

Technological Advancements in Transducer Miniaturization

Next-generation piezo-composite arrays have lifted center frequencies above 15 MHz, enabling high-resolution imaging for dermatology, thyroid and micro-vascular studies.[2]Hae Gyun Lim, “Recent Advancements in High-Frequency Ultrasound Applications,” MDPI, mdpi.com Handheld probes paired with smartphones allow emergency physicians to triage trauma at the bedside. Miniaturization also supports catheter-based ultrasound for intravascular procedures, diversifying revenue sources. Manufacturers bundle AI-driven auto-measurement to offset operator variability, improving diagnostic consistency. Nevertheless, rapid hardware cycles compel buyers to upgrade sooner, raising life-cycle costs and pressuring smaller centers.

Integration With AI-Based Diagnostic Algorithms

Samsung Medison’s 2024 purchase of Sonio accelerated AI fetal-anomaly screening, decreasing manual measurement time by 30%. Similar advances such as RealCAC-Net produce 0.96 classification accuracy for carotid compressibility during CPR, elevating ultrasound from imaging tool to real-time triage aid. Regulatory certainty following the Digital Medical Products Act of January 2025 has shortened approval cycles for AI-embedded devices, encouraging rapid software iteration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited skilled sonographers outside tertiary hospitals | -0.7% | Rural regions | Long term (≥ 4 years) |

| Stringent regulatory approval timelines | -0.5% | National | Medium term (2-4 years) |

| High upfront cost of advanced ultrasound platforms | -0.4% | Small and mid-size facilities | Short term (≤ 2 years) |

| Reimbursement caps on outpatient ultrasound services | -0.3% | Ambulatory care settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Skilled Sonographers Outside Tertiary Hospitals

A workforce study found 19 labs lacked echocardiography technologists and 18 lacked transcranial Doppler specialists, exposing regional service gaps.[3]Hyung-Joon Bae et al., “Workforce Estimation of Clinical Technologists in Ultrasonic Inspection,” Biomedical Science Letters, bslonline.org Concentration of talent in Seoul tertiary centers restricts ultrasound penetration into community hospitals and ASCs. Pain-management clinics report delays in adopting musculoskeletal scans because physicians must first complete society-run workshops. Unless training capacity scales, device vendors will face uneven regional demand and under-utilized equipment.

Stringent Regulatory Approval Timelines

The Digital Medical Products Act, enforced in January 2025, introduced software-as-a-medical-device (SaMD) pathways but also lengthened dossier review for AI algorithms, delaying market entry by up to nine months. Small innovators struggle to meet post-market performance reporting, curbing domestic start-ups’ speed. Added compliance costs discourage niche therapeutic ultrasound manufacturers, limiting technology diversity. While harmonization talks with the FDA aim to streamline reviews, current timelines continue to hinder rapid product refresh cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: OB/GYN Dominance Driven by Policy Support

Obstetrics & gynecology contributed 28.22% to the South Korea ultrasound devices market size in 2025 after NHI funding for seven prenatal scans cemented routine fetal imaging. AI-enabled anomaly detection, unlocked through Samsung’s Sonio deal, elevates diagnostic yield and cements long-term OEM revenue. Over the forecast, critical care posts the fastest 5.27% CAGR as handheld probes become standard in emergency and intensive-care units. Rising trauma and shock cases in regional centers prompt bulk purchases of pocket scanners. Cardiovascular ultrasound adoption accelerates as Siemens’ Acuson Origin captures 5,000 real-time measurements with 99% accuracy, streamlining echo workflows. Musculoskeletal and urology volumes benefit from newly reimbursed spinal and urinary scans, although uptake depends on training expansion. HIFU-based vascular closure achieves greater than 95% success in varicose-vein treatment, nurturing a therapeutics niche.

Continuous policy backing ensures OB/GYN retains scale, yet competitive intensity rises as GE integrates ScanNav labor analyses, and Philips eyes AI obstetric workflows. Critical care penetration hinges on device ruggedness and infection-control design. Cardiology buyers weigh AI-bundled premium systems against budget limits, delaying replacement decisions. Musculoskeletal growth could falter without credentialing reforms. Vendors targeting vascular and oncology HIFU must navigate separate procedure codes, limiting short-term revenue, but long-term therapeutic diversification remains attractive.

By Technology: 3D/4D Leadership Challenged by HIFU Innovation

3D & 4D platforms held 39.52% of the South Korea ultrasound devices market share in 2025, propelled by enhanced fetal visualization and real-time cardiac volumetrics. Progressive hospitals now adopt AI abdomen tools for automatic liver and kidney sizing, cutting scan time 36%. HIFU records the highest 4.85% CAGR, driven by prostate, thyroid and aesthetic procedures showing fewer side effects than conventional surgery. 2D imaging remains indispensable for first-line abdominal screening due to lower cost and operator familiarity. Doppler modules gain traction in carotid and peripheral arterial clinics, assisted by AI flow quantification.

Regulatory clarity for therapeutic ultrasound is still evolving, but early adopters leverage MFDS fast-track for novel cancer ablation devices. Local OEMs such as Classis ramp global publications to validate HIFU efficacy. Cost-sensitive clinics continue to prefer versatile 3D/4D consoles over procedure-specific HIFU rigs until reimbursement widens. Deep learning upgrades extend usable life of installed 2D systems, slowing replacement. Technology suppliers balancing advanced features with modular upgrades can defend share while monetizing AI subscriptions.

By Portability: Handheld Growth Challenges Stationary Dominance

Stationary consoles captured 60.35% of the South Korea ultrasound devices market size in 2025 because high-resolution radiology and cardiac imaging still require large transducer arrays and GPU processing. Yet handheld devices register the swiftest 6.52% CAGR, as perioperative and ambulance teams demand pocket scanners for immediate triage. Cart-based units fulfill general-ward mobility and remain popular among diagnostic centers that need mid-tier pricing.

Emerging smartphone-tethered probes, typified by Healcerion’s SONON, enable remote consultations and tele-training. AI edge-processing now boosts image clarity on handheld devices, narrowing performance gaps. Infection-control covers and single-use sheaths accelerate adoption in ICUs. Still, battery life, heat management and limited deep penetration constrain handheld use in obese or complex cases. Premium stationary consoles retain relevance through integrated AI and multimodality fusion, securing high-margin service contracts.

By End User: Hospital Dominance Faces ASC Challenge

Hospitals generated 47.86% of 2025 revenue and continue ordering flagship consoles for cardiology, radiology and interventional suites where advanced features justify price. ASCs, however, post a leading 6.06% CAGR as more urological and orthopedic procedures shift outpatient, driven by 134.9% transurethral surgery growth. Diagnostic imaging centers benefit from automated breast ultrasound coverage, attracting high-volume screenings.

Hospital buyers prioritize AI workflow to mitigate sonographer shortages, adopting auto-captioning and cloud reporting. ASCs favor portable carts that balance price with procedure versatility. Community clinics leverage government grants to procure handheld devices for chronic-disease management programs. Vendor financing models gain traction among small providers facing capital constraints. Mixed public-private ownership dynamics create diverse procurement rules, requiring flexible commercial strategies.

Geography Analysis

South Korea ultrasound devices market concentration is highest in Seoul-Incheon, where tertiary hospitals undertake complex imaging. The capital region accounts for the bulk of high-end console installations, underpinned by a 90% electronic medical record adoption rate that simplifies AI integration. Southern provinces experience faster handheld uptake as rural outreach teams lean on portable probes for liver and gallbladder monitoring. Government integrated-community-care pilots fund ultrasound in county clinics, reducing travel burden for elderly patients.

Regulation shapes regional roll-outs: MFDS collaborates with 19 agencies including the FDA to harmonize AI standards, positioning Korea as a preferred pilot market for multinationals. Digital Medical Products Act compliance is mandatory nationwide, but approval support centers in Daegu and Osong speed local applications. Broadband 5G coverage enables real-time tele-mentoring between urban specialists and rural generalists, boosting exam accuracy.

Private-sector hospital chains in Busan and Daejeon increasingly source mid-range consoles from domestic OEMs to minimize service downtime. Provincial funding incentives covering up to 30% of capital costs for AI imaging spur adoption beyond the Seoul corridor. Nevertheless, sonographer shortages are acute in Gangwon and Jeju, limiting utilization rates despite installed capacity. Targeted workforce expansion remains essential to fully translate equipment penetration into scan volume.

Competitive Landscape

Samsung Medison’s USD 93 million purchase of Sonio in 2024 exemplifies home-grown leadership in AI obstetric imaging, cementing the firm’s stronghold within the South Korea ultrasound devices market. GE Healthcare counters via a USD 51 million buy-out of Intelligent Ultrasound’s clinical AI unit, integrating ScanNav tools that guide sonographers during fetal exams. Siemens Healthineers quickly achieved FDA clearance for Acuson Origin, an AI-rich cardiovascular platform yielding 5,000 measurements per echo, reinforcing premium positioning.

White-space opportunities arise for niche companies: Healcerion leverages smartphone connectivity for rural deployments, while Classis amplifies HIFU aesthetics with a 51.5% jump in supporting publications. Canon Medical’s partnership with Olympus for endoscopic ultrasound marries imaging and scopes, tapping gastrointestinal specialists. Philips pivots to point-of-care by debuting a versatile portable suite in June 2025, targeting multi-department use.

Competition is shifting from probes and pixels to proprietary algorithms and workflow ecosystems. Vendors adding subscription-based AI modules and cloud analytics lock customers into recurring revenue streams. Domestic start-ups face scale challenges against multinational R&D budgets but benefit from MFDS innovation vouchers and K-Bio lab space subsidies. Market share reshuffles will hinge on each player’s capacity to bundle hardware, AI, and service at cost points matching varied provider segments.

South Korea Ultrasound Devices Industry Leaders

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Siemens Healthineers received FDA clearance for its Acuson Origin cardiovascular ultrasound system, featuring advanced AI capabilities that can capture over 5,000 measurements during echocardiography exams with 99% diagnostic accuracy. The system includes real-time cardiac view recognition and the AcuNav Lumos 4D ICE catheter for enhanced imaging during complex heart procedures

- July 2024: GE Healthcare announced its acquisition of the clinical AI business from Intelligent Ultrasound for USD 51 million, adding AI-driven ultrasound tools designed to improve scan efficiency and workflow for clinicians. The acquisition includes products like ScanNav Anatomy and ScanNav Assist, which support sonographers during OB-GYN examinations

South Korea Ultrasound Devices Market Report Scope

As per the scope of the report, a diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. They assess various kidney, liver, and other abdominal conditions. They are also widely used to treat chronic illnesses, including diabetes, asthma, cancer, and heart disease. As a result, these devices have a variety of uses in the medical area, including diagnostic imaging and therapeutic modality. South Korea Ultrasound Devices Market Is Segmented by Application (Anesthesiology, Cardiology, Gynecology/Obstetrics, Musculoskeletal, Radiology, Critical Care, and Other Applications), Technology (2D Ultrasound Imaging, 3D and 4D Ultrasound Imaging, Doppler Imaging, and High-intensity Focused Ultrasound) Type (Stationary Ultrasound and Portable Ultrasound). The report offers the value (USD) for all the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Obstetrics and Gynecology |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Other End Users |

| By Application | Anesthesiology |

| Cardiology | |

| Obstetrics and Gynecology | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Ambulatory Surgical Centers | |

| Other End Users |

Key Questions Answered in the Report

What is the 2026 value of the South Korea ultrasound devices market?

It stands at USD 177.88 million, with a projected 4.03% CAGR to 2031.

Which application generates the most revenue?

Obstetrics & gynecology, supported by NHI coverage for seven prenatal scans.

Which segment is growing fastest?

Critical care imaging, expanding at a 5.27% CAGR to 2031.

How are AI tools influencing purchasing decisions?

Hospitals and ASCs favor consoles bundled with AI that automate measurements, improve accuracy and cut scan time.

Why are handheld devices gaining popularity?

Rural outreach, emergency medicine and home-care programs need portable, low-cost imaging with adequate diagnostic quality.

What regulatory change took effect in 2025?

The Digital Medical Products Act, requiring MFDS authorization for AI-based ultrasound devices, now governs software and hardware approvals.

Page last updated on: