Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

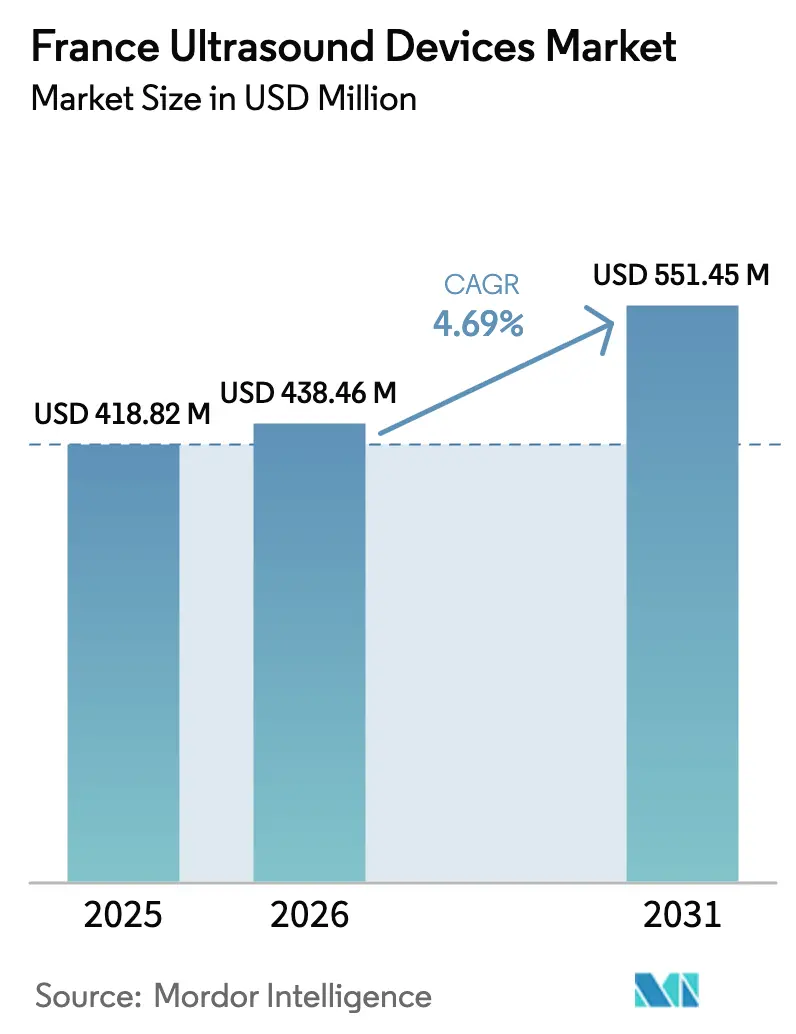

| Base Year Market Size (2025) | USD 418.82 Million |

| Market Size (2026) | USD 438.46 Million |

| Market Size (2031) | USD 551.45 Million |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Ultrasound Devices Market Analysis by Mordor Intelligence

The France Ultrasound Devices Market size is expected to grow from USD 418.82 million in 2025 to USD 438.46 million in 2026 and is forecast to reach USD 551.45 million by 2031 at 4.69% CAGR over 2026-2031.

Current growth reflects steady capital investment, rising point-of-care deployment, and therapeutic innovations that keep ultrasound central to hospital and home-care diagnostics. Aging demographics lift demand for echocardiography and musculoskeletal imaging, while the shift toward portable devices reduces infrastructure strain on provincial hospitals. EU MDR compliance costs reshape vendor strategy toward high-volume, cost-efficient platforms, and purchasing consortia channel spending into devices that demonstrate measurable workflow gains. Intensifying AI integration and reimbursement support for tele-ultrasound underpin the market’s resilience and open opportunities in underserved rural regions.

Key Report Takeaways

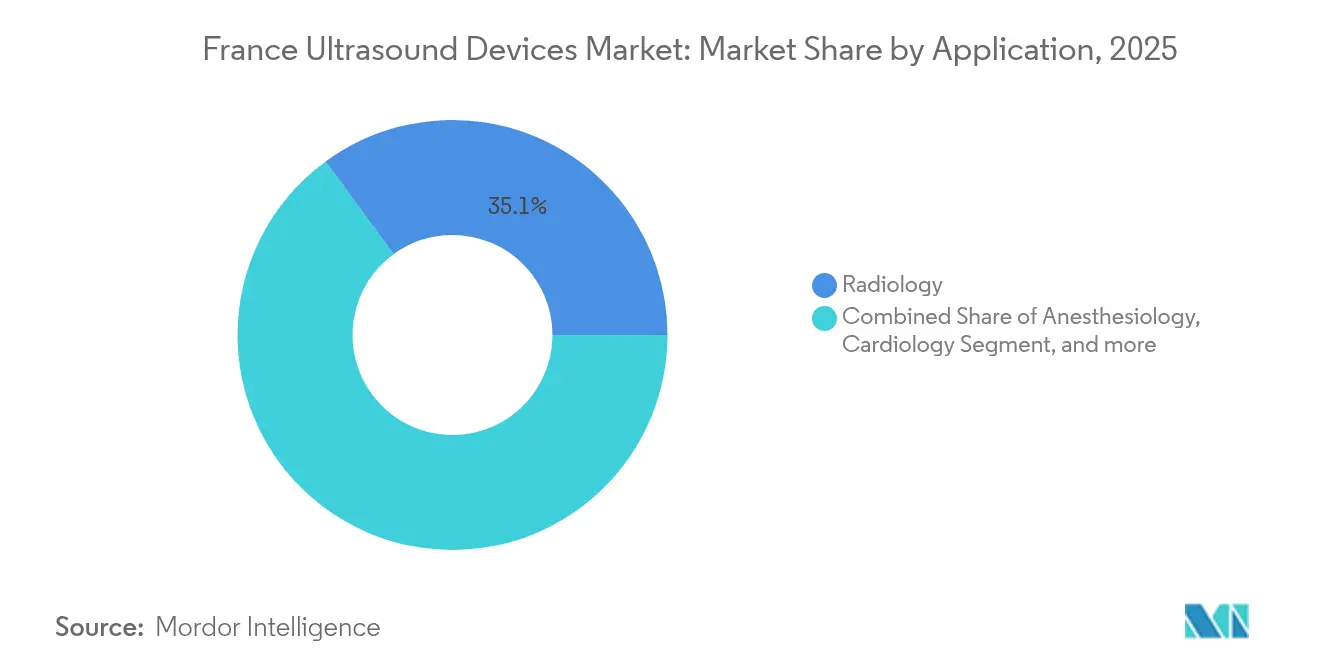

- By application, critical care expanded at a 6.02% CAGR through 2031, outpacing radiology, which held 35.05% of the France ultrasound devices market share in 2025.

- By technology, 3D & 4D systems commanded 39.41% of the France ultrasound devices market size in 2025, whereas high-intensity focused ultrasound (HIFU) is projected to grow at 5.56% CAGR to 2031.

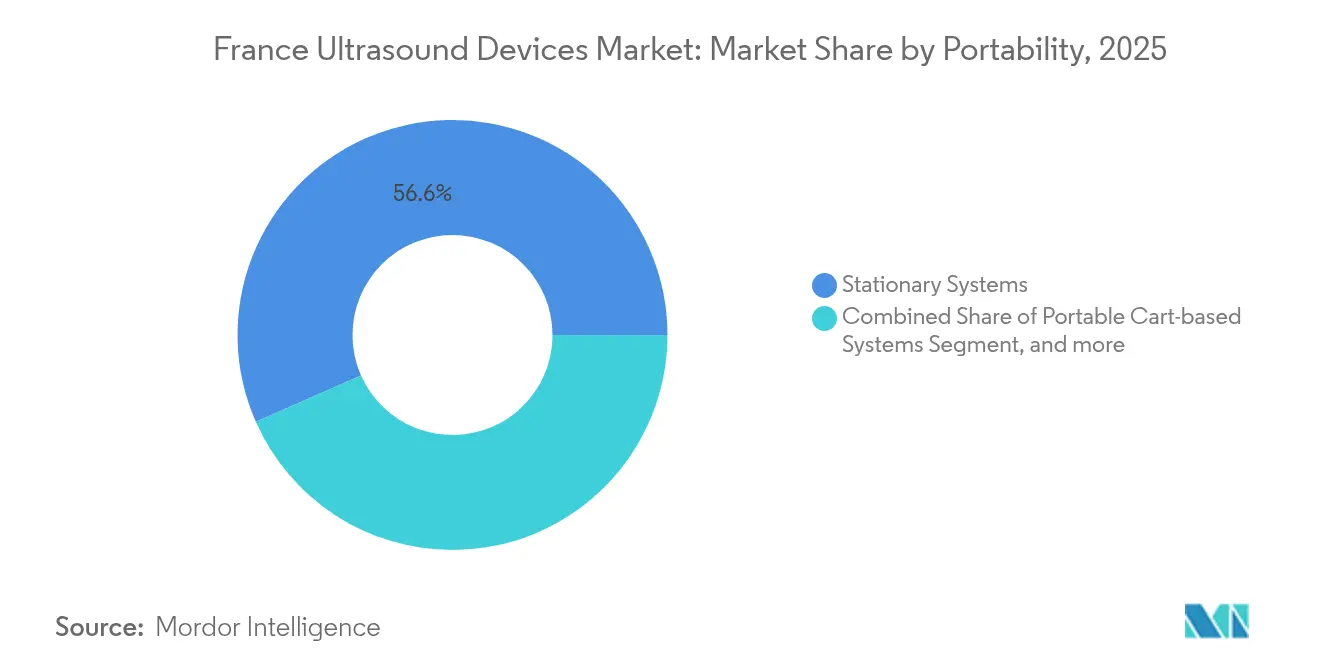

- By portability, stationary consoles retained 56.62% revenue share in 2025, while handheld units recorded the fastest trajectory at 7.35% CAGR.

- By end user, hospitals generated 53.94% of 2025 sales, but home-healthcare settings are poised to rise with a 6.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Chronic Disease Burden | +1.8% | National, concentrated in rural regions | Long term (≥ 4 years) |

| Rapid Adoption of Point-of-Care Ultrasound in Emergency Departments | +1.2% | National, urban hospitals leading | Medium term (2-4 years) |

| Continuous Upgrades in 2D/3D/4D & AI-Enabled Imaging | +0.9% | National, private sector early adoption | Medium term (2-4 years) |

| Government Push to Reduce Radiation Exposure | +0.7% | National, regulatory compliance driven | Short term (≤ 2 years) |

| Expansion of Tele-Ultrasound Reimbursement for Rural Care | +0.6% | Rural regions, overseas territories | Long term (≥ 4 years) |

| GP Ultrasound Training Initiatives Broadening Primary Care Use | +0.5% | National, primary care networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Chronic Disease Burden

The share of residents aged 65 and above reached 21.8% in 2025, and higher life expectancy has pushed cardiovascular and musculoskeletal case loads that rely on non-ionizing imaging.[1]INSEE, “Répartition de la population par âge,” insee.fr Echocardiography volumes continue to grow in community clinics as general practitioners incorporate ultrasound into chronic-care pathways to limit hospital readmissions. Peripheral joint evaluation needs also expand because the same demographic supports a rise in osteoarthritis interventions. Although physician numbers rose 1.7% year-on-year, specialist appointments remain scarce outside metropolitan areas, amplifying ultrasound’s value as a gatekeeper modality in primary care. This demographic reality anchors a long-term driver that offsets intermittent budget tightening.

Rapid Adoption of Point-of-Care Ultrasound in Emergency Departments

French hospitals increased emergency-department (ED) ultrasound availability, validating bedside imaging as a clinical standard. Prospective studies show point-of-care ultrasound (POCUS) alters diagnostic decisions in 82% of ED visits and therapeutic plans in 47% of cases, building a compelling evidence base for continued procurement. The national emergency-medicine society has set competency frameworks that mandate supervised scanning milestones, ensuring uniform skill development across regions.[2]SFMU, “Compétences en échographie d’urgence,” sfmu.org Field research by French defense forces underscores the technique’s adaptability, with untrained nurses reporting 96% willingness to pursue instruction for combat support. Together, these findings explain why the France ultrasound devices market continues to pivot toward compact, battery-operated scanners that meet tight ED turnaround times.

Continuous Upgrades in 2D/3D/4D & AI-Enabled Imaging

Vendor M&A has accelerated algorithmic imaging breakthroughs. Samsung acquired Paris-based Sonio for USD 92.4 million in 2024 to automate prenatal exams. GE HealthCare paid USD 51 million for Intelligent Ultrasound, a move that dovetails with its NVIDIA alliance to automate probe positioning. Clarius and ThinkSono debuted guided systems that overlay AI contouring on live B-mode to shorten novice learning curves. French labs contribute to frontier research such as airborne ultrasound surface-motion cameras for contact-free respiratory diagnostics. These upgrades improve image quality, cut exam times, and reduce reliance on scarce sonographers, especially in provincial facilities.

Government Push to Reduce Radiation Exposure

Regulatory authorities updated CCAM coding in 2025 to include enhanced liver and pediatric protocols, broadening reimbursement and underscoring ultrasound as the first-line alternative where ionizing modalities pose risk. Defense medical guidelines show that frontline ultrasound reduces CT utilization for thoracoabdominal trauma, a practice transferable to civilian settings. The European Space Agency funds tele-robotic echography initiatives such as AdEchoTech’s Melody, highlighting multilevel institutional commitment to radiation-free diagnostics.[3]European Space Agency, “Tele-echography in remote medicine,” esa.int These policy currents foster early-stage adoption among pediatrics and obstetrics departments, supporting short-term volume expansion despite hospital deficit pressures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU MDR Re-Certification Costs & Delays | -1.4% | EU-wide, affecting all manufacturers | Short term (≤ 2 years) |

| High Capital & Maintenance Costs of Advanced Systems | -0.8% | National, budget-constrained hospitals | Medium term (2-4 years) |

| Shortage of Certified Sonographers in Provincial Hospitals | -0.6% | Rural regions, provincial healthcare facilities | Long term (≥ 4 years) |

| Purchasing Group Consolidation Squeezing Vendor Margins | -0.4% | National, hospital procurement networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU MDR Re-Certification Costs & Delays

Manufacturers contend with expanded technical-file audits, post-market surveillance, and rising notified-body fees as deadlines move toward 2028. The burden is acute for smaller suppliers that lack dedicated regulatory staff, raising the risk of product withdrawal and tightening hospital supply options. French GMED’s queue times elongate purchasing cycles, driving hospitals to extend asset life instead of refreshing fleets, which suppresses near-term market uptake.

High Capital & Maintenance Costs of Advanced Systems

Public-sector hospitals reported a EUR 2.4 (USD 2.7) billion deficit in 2023, while a central directive seeks EUR 300 (USD 348) million in imaging savings by 2027. Premium consoles equipped with AI and 4D functionality often exceed EUR 150,000 (USD 165,000) and carry annual service contracts topping EUR 12,000 (USD 13,200). These commitments are untenable for many regional centers, delaying replacement cycles and pushing demand toward hand-carried units priced below USD 4,000. Vendor margins narrow under group-purchasing bids, limiting reinvestment capacity in R&D and potentially slowing next-generation feature rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Critical Care Drives Emergency Expansion

Critical care applications grew at a 6.02% CAGR, a pace that positions them as the most dynamic slice of the France ultrasound devices market. Intensivists increasingly favor handheld scanners for bedside evaluations that shorten average sepsis diagnosis time by 18 minutes. At the same time, radiology retains 35.05% of 2025 revenue because it remains the central imaging gatekeeper in large academic centers. Cardiology growth aligns with AI-enhanced fetal and adult echo protocols introduced after Samsung’s Sonio buyout. Conversely, the gynecology/obstetrics sub-segment faces headwinds from the decline to 663,000 births in 2024. Musculoskeletal demand rises on the back of arthroplasty volume growth, and vascular assessments exploit HIFU guidance for chronic venous disease therapy. Together these dynamics maintain a balanced demand structure that underpins a diverse end-user base.

Critical care’s larger addressable patient turnover, amplified by ED POCUS programs, ensures persistent capital flow into cart-based and portable platforms. Hospitals invest in AI-driven workflow tools that auto-measure ejection fraction, reducing exam variability and catering to the chronic heart-failure cohort.

By Technology: HIFU Innovation Accelerates Therapeutic Applications

HIFU is projected to grow 5.56% annually, benefiting from prostate-cancer studies reporting 90% salvage-free survival at three years. While 3D & 4D imaging maintained a 39.41% share in 2025, catheter-based procedures increasingly incorporate 4D fusion guidance. Open-architecture scanners capable of software upgrades allow hospitals to avoid complete console replacement, sustaining loyalty to incumbent brands.

The France ultrasound devices market share for 3D & 4D systems is expected to remain dominant through 2031, yet HIFU’s procedural reimbursement expansions hint at accelerating penetration. The Focused Ultrasound Foundation logs 171 active indications globally, with oncology, vascular, and aesthetics driving clinical pipeline diversification. That breadth of therapeutic application secures downstream demand for disposables and service contracts long after equipment installation.

By Portability: Handheld Devices Transform Point-of-Care Access

Stationary systems held 56.62% of 2025 sales, underlining their necessity for complex exams, but handheld devices surged at 7.35% CAGR. Butterfly Network’s CE-marked iQ3 melds Ultrasound-on-Chip architecture with 3D rendering to deliver entry-level tomography in a smartphone form factor. Comparative testing found Vscan Air best for user interface and Butterfly iQ strongest for prostate volume reliability. Provincial hospitals and private home-care agencies embrace these sub-USD-4,000 tools for daily wound monitoring and heart-failure follow-ups, reducing outpatient travel burdens.

The France ultrasound devices market size attributed to handhelds is projected to exceed reflecting tele-health program funding that reimburses rural examinations. Meanwhile, cart-based portables maintain demand for ABUS breast screening and interventional suites where multi-probe flexibility remains vital. Innovation in wearable ultrasonic patches, such as Novosound’s IP filing, foreshadows a new sub-segment for continuous monitoring that may further disrupt the stationary-console paradigm.

By End User: Home Healthcare Emergence Reshapes Service Delivery

Hospitals accounted for 53.94% of 2025 turnover, leveraging bulk-buy power and specialty depth, yet home-healthcare settings are slated for a 6.86% CAGR. National tele-consult infrastructure, scaled during COVID-19, now supports remote ultrasound where a nurse positions the probe and a radiologist guides interpretation in real time. AdEchoTech’s Melody has already been deployed across 15 institutions, underlining technical maturity. Diagnostic centers preserve a second-line niche by offering advanced Doppler and interventional services offloaded from saturated hospital schedules. In contrast, ambulatory surgical centers integrate real-time imaging for needle-guided analgesia.

The France ultrasound devices market size for home healthcare is still small but highly elastic, aided by reimbursement frameworks that compensate for domiciliary echo follow-ups. With cardiology appointment wait times surpassing 42 days in several départements, portable solutions in the home shorten patient pathways and free tertiary capacity for complex cases.

Geography Analysis

Paris, Lyon, and Marseille anchor demand concentration, each hosting university hospitals that run multi-vendor fleets. Yet rural Occitanie and Nouvelle-Aquitaine suffer lower specialist density, prompting regional health agencies to subsidize tele-ultrasound hubs. Group purchasing organizations negotiate on behalf of entire regions, trimming per-unit pricing by 11% in 2024 contracts and nudging procurement toward budget-friendly handhelds. Overseas territories such as Réunion adopt portable scanners paired with satellite connectivity for obstetric outreach, an approach supported by European Space Agency funding.

National health‐expenditure growth of 3.3% for 2025 covers essential device upgrades, but the parallel EUR 300 million imaging-savings target forces administrators to demonstrate utilization thresholds before approving console replacements. Consequently, facilities with usage below 2,000 scans per year shift to pay-per-scan leasing or shared-ownership pools. Cross-border agreements let Alsace clinics send complex fetal cases to German centers while retaining follow-up echography locally, optimizing resource allocation inside the Schengen health corridor.

Manufacturing corridors around Île-de-France and Pays de la Loire foster supplier–research ecosystems; AdEchoTech, EDAP TMS, and Theraclion benefit from local tax incentives and engineering talent. EU research consortia secure Horizon Europe grants for AI-enabled ultrasound, ensuring continuous technology inflow that sustains the France ultrasound devices market.

Regulatory Landscape

Ultrasound systems marketed in France are regulated as medical devices under the EU Medical Device Regulation (EU) 2017/745 (MDR) and require conformity assessment by a notified body prior to CE marking. In-country oversight sits with the Agence nationale de securite du medicament et des produits de sante (ANSM), supported by the Haute Autorite de Sante (HAS) guidance on the practical pathway for medical devices in France, including clinical evidence expectations and post-market obligations.

Post-market control is reinforced through ANSM market surveillance and vigilance activities, including technical-documentation review and inspections of economic operators. France also runs coordinated surveillance actions with DGCCRF and DGDDI, tightening control across distribution and import channels and raising the compliance bar for manufacturers and distributors operating ultrasound portfolios.

Competitive Landscape

The market remains moderately consolidated: GE HealthCare, Philips, Siemens Healthineers, Samsung Medison, and Canon Medical collectively exceed a significant share, while domestic innovators occupy specific niches. GE HealthCare’s 2024 acquisition of Intelligent Ultrasound accelerates its analytics roadmap, protecting its leading 30% global share. Siemens has slipped to sixth globally and weighs divestiture options amid pricing pressure. Samsung’s Sonio purchase underscores strategic emphasis on AI, especially in fetal care. EDAP TMS commands the national HIFU segment for prostate and breast applications, while Theraclion leads in venous disease ablation.

Handheld disruptors vie for hospital outpatient departments and home-health agencies; Butterfly Network raised USD 76 million in 2025 public equity to fund European rollouts. Clarius pairs with ThinkSono to embed DVT detection algorithms, and Philips markets Lumify with subscription-based app updates. EU MDR compliance insulates entrenched brands because new entrants face prolonged certification timelines. Vendor alliances with cloud PACS providers diversify service models toward software-as-a-service, tightening customer lock-in via data analytics packages.

France Ultrasound Devices Industry Leaders

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Two near-term whitespace areas stand out in France: expanding point-of-care and home-based ultrasound where specialist density is low, and rolling out workflow automation that helps offset throughput delays tied to sonographer constraints. The first set of opportunities is supported by mature tele-ultrasound deployments (for example, AdEchoTechs Melody used across multiple institutions) and by the market shift toward sub-USD 4,000 handheld units adopted by provincial hospitals and home-care agencies, which reduces the infrastructure burden compared with replacing high-cost consoles.

On the supply and innovation side, public industrial policy provides another lever for localization and software-defined differentiation in imaging. France 2030 earmarked EUR 400 million for the medical device sector, and SNITEM reported that 36% of industrial medical device firms established new production sites within the last five years, supporting expansion of local manufacturing and integration partners for probes, software, and service. This combines with MDR-driven recertification pressure, which favors vendors that can pair compliant hardware with AI-enabled upgrades, subscription software, and service models that help hospitals manage imaging-savings mandates while maintaining utilization and quality targets.

Recent Industry Developments

- June 2026: Cardiawave: First routine clinical treatments using Valvosoft after CE mark approval, deployment across France, the Netherlands, and Germany. The rollout expands therapeutic ultrasound indications and accelerates regional commercialization in France and neighboring markets. The deployment demonstrates rapid market uptake and validates CE marked indications for Valvosoft.

- June 2026: Canon Medical Systems Europe: Strategic collaboration with Fraiya to introduce AI-powered prenatal ultrasound workflow support. The collaboration enhances AI-enabled workflow for prenatal imaging on premium Canon platforms. It strengthens the integration of AI driven diagnostics within Canon's ultrasound ecosystem in Europe.

- June 2026: Canon Medical Systems Europe - Announced a strategic collaboration with Fraiya to introduce AI-powered prenatal ultrasound workflow support. The announcement underscores Canon’s continued investment in AI assisted prenatal imaging across its product line. It reinforces the premium portfolio with enhanced workflow automation for fetal assessment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, we define the France ultrasound devices market as revenues earned from ultrasound imaging systems sold for clinical diagnosis in France across public and private healthcare settings, including related probes that are sold with or for these systems.

Scope exclusions: We exclude ultrasound service contracts, consumables like gel, and imaging procedures billed by hospitals or clinics.

Segmentation Overview

- By Application

- Anesthesiology

- Cardiology

- Gynecology / Obstetrics

- Musculoskeletal

- Radiology

- Critical Care

- Urology

- Vascular

- Other Applications

- By Technology

- 2D Ultrasound Imaging

- 3D & 4D Ultrasound Imaging

- Doppler Imaging

- High-Intensity Focused Ultrasound

- Other Technologies

- By Portability

- Stationary Systems

- Portable Cart-based Systems

- Hand-held / Pocket Devices

- By End User

- Hospitals

- Diagnostic Centers

- Ambulatory Surgical Centers

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model to real healthcare activity in France, and to build the first set of volumes and price ranges before interviews. Public sources such as OECD Health Statistics, Eurostat, and the World Bank helped us sanity check healthcare spend direction, demographics, and hospital capacity signals that influence imaging procurement.

We also reviewed sources such as the French Ministry of Health publications, the National Institute of Statistics and Economic Studies (INSEE), and open materials from medical imaging and radiology societies in France to understand equipment renewal patterns and where ultrasound is being used more often. Alongside these, we used company annual reports, investor presentations, and reputed press coverage, and then validated select company financial splits using paid subscriptions focused on company financials, news, and patent databases. The sources listed here are illustrative, and many other public and paid references were used to collect data, cross-check assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on checking what desk research cannot show clearly, such as realistic selling prices after discounts, typical upgrade cycles, and mix shifts between cart-based and portable systems in France. We spoke with a spread of stakeholders, including distributors, hospital procurement teams, imaging department users, and service partners across France, and then used their feedback to tighten assumptions and resolve conflicting signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | |

| Mid tier: 45% | Functional/Unit leaders: 25% | |

| Smaller Players: 22% | Managers: 59% |

Market-Sizing & Forecasting

The sizing started from a top-down approach where procedure demand signals and installed base replacement needs were translated into annual unit demand, which was then valued using France-relevant average selling prices. To keep the totals grounded, we also ran selective bottom-up approximations using supplier and channel checks, and then adjusted the final number when the two views showed a meaningful gap.

Key inputs used in the model included the estimated installed base by care setting, typical replacement and upgrade cycles, the share shift toward portable systems, average system pricing by portability class, and the annual throughput pressure created by aging population and chronic disease imaging needs in France. Where information was missing for smaller sites, we filled gaps using bounded ranges from interviews and then applied conservative adoption curves that were later rechecked.

For forecasting, scenario analysis was used with a base case tied to expected hospital capital spending discipline, continued outpatient growth, and steady technology refresh in France. Assumptions on price movement were kept practical, with gradual ASP changes based on mix (portable versus cart-based) rather than a single flat inflation factor.

Data Validation & Update Cycle

Model outputs were validated by comparing results against independent signals such as healthcare spending direction, public hospital investment cues, and the implied unit volumes that would be required to support the value totals for France. When an outlier appeared, we revisited the driver behind it, and then rechecked the underlying assumptions with additional calls or follow-up questions.

Before sign-off, the work is reviewed in steps, starting from variable checks and moving to a full read-through of logic, math, and narrative consistency. Reports are refreshed annually, and we also update sooner when a material event changes pricing, procurement timing, or supply conditions. Right before delivery, an analyst runs a final pass so clients receive the latest updated view.

Mordor Intelligence's France Ultrasound Devices Market Estimate Compared With Other Published Estimates

Published market values for ultrasound devices in France can look far apart because teams do not always count the same revenues, time their currency conversions in the same way, or apply the same price logic when portable systems gain share. Differences also show up when one estimate leans more on shipment assumptions, while another is tied closer to replacement cycles and hospital procurement behavior in France.

A refresh-led difference matters here because device ASPs move with discounting, tender timing, and mix shifts, so a model that updates FX timing and rechecks price bands with fresh interviews can land in a different place even if unit demand looks similar. Those update and validation steps, along with a practical ASP-by-mix approach, are key reasons the 2025 market size used in Mordor Intelligence differs from some other published figures.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 418.82 M (2025) | |

| Trade Journal A | USD 402.00 M (2025) | Uses a fixed average price for all systems and applies a single-year procurement snapshot, which can understate mix-driven ASP changes when portable systems expand. |

| Regional Consultancy B | USD 455.00 M (2025) | Appears to include service and extended warranty revenues in the same total and uses earlier-year currency conversion timing, which can lift the reported value versus device-only counting. |

The spread in the table is mostly explained by what is counted as revenue, and by how pricing is kept current when product mix shifts across care settings in France. By keeping scope limited to device revenues and tying price and replacement assumptions to repeatable checks, we get a practical number that can be traced back to clear demand and ASP drivers.

Key Questions Answered in the Report

How large is the France ultrasound devices market in 2026?

It is valued at USD 438.46 million and is projected to grow to USD 551.45 million by 2031 at a 4.69% CAGR.

Which application shows the fastest revenue growth?

Critical care leads with a 6.02% CAGR through 2031, propelled by expanding emergency-department POCUS programs.

What technology segment is gaining traction beyond diagnostics?

High-intensity focused ultrasound accelerates at 5.56% CAGR as therapeutic prostate and vascular uses scale.

Why are handheld ultrasound devices popular in France?

Their sub-USD 4,000 price, CE compliance, and plug-and-play cloud connectivity suit budget-limited rural and home-care settings.

How does EU MDR influence market dynamics?

Lengthy recertification timelines and higher notified-body fees favor established brands, tightening near-term product pipelines.

Which factor most limits capital purchases in public hospitals?

Persistent operating deficits and a government mandate to save EUR 300 (USD 348) million on imaging from 2025-2027 constrain high-cost console replacements.

Page last updated on: