Wavefront Aberrometer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

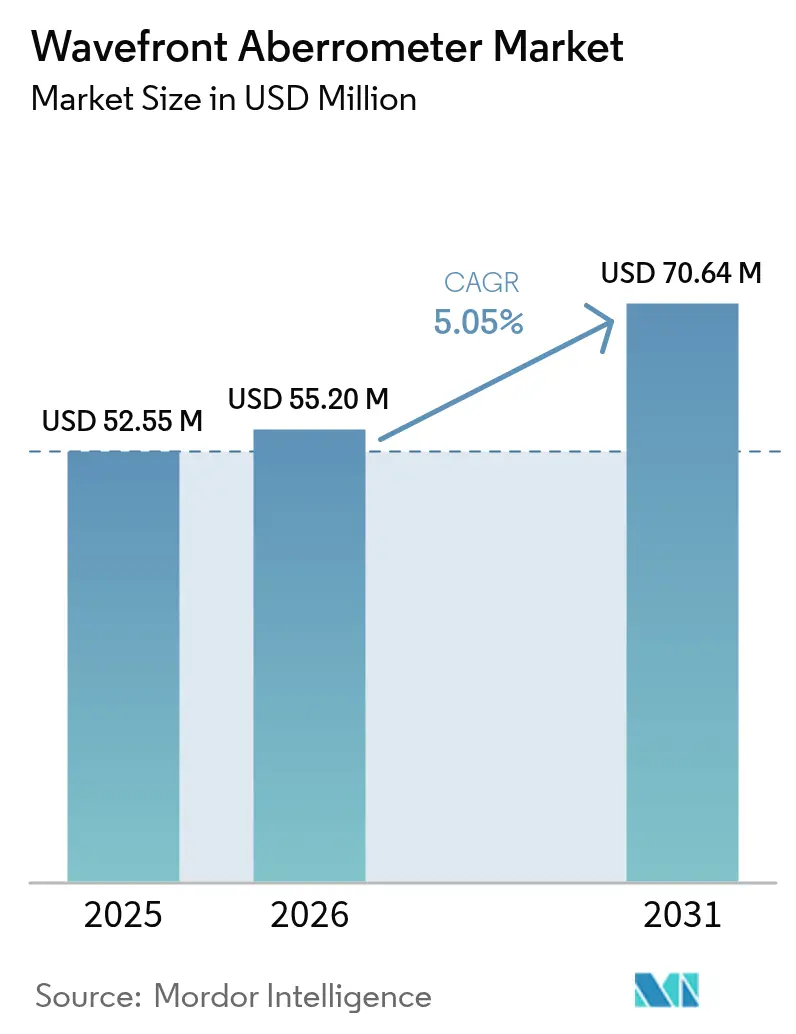

| Market Size (2026) | USD 55.2 Million |

| Market Size (2031) | USD 70.64 Million |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wavefront Aberrometer Market Analysis by Mordor Intelligence

The Wavefront Aberrometer market size is expected to grow from USD 52.55 million in 2025 to USD 55.2 million in 2026 and is forecast to reach USD 70.64 million by 2031 at 5.05% CAGR over 2026-2031.

Adoption is propelled by artificial-intelligence diagnostics, wider intra-operative aberrometry use in premium intraocular lens (IOL) procedures, and the convergence of wavefront-guided LASIK with topography-integrated systems, which together expand diagnostic scope beyond simple refraction. Accelerated uptake of portable units for outreach screening, rising procedure volumes in ambulatory settings, and consolidation moves by leading manufacturers also underpin growth. Countervailing pressures include Medicare’s 2.93% payment reduction for 2025 and shortages of technicians skilled in advanced diagnostics.

Key Report Takeaways

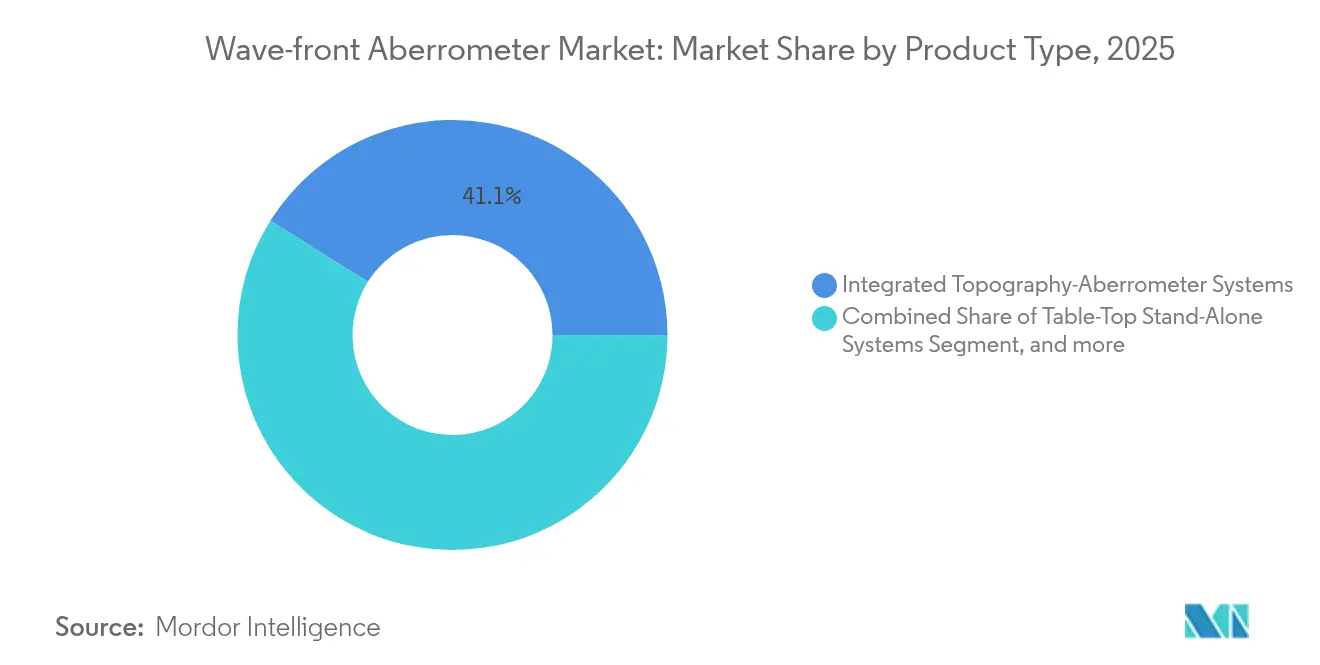

- By product type, integrated topography-aberrometer systems led with 41.08% revenue share in 2025, while intra-operative aberrometers are advancing at a 7.02% CAGR through 2031.

- By application, myopia correction held 55.10% of the wavefront aberrometer market share in 2025, whereas presbyopia applications are set to expand at 6.65% CAGR to 2031.

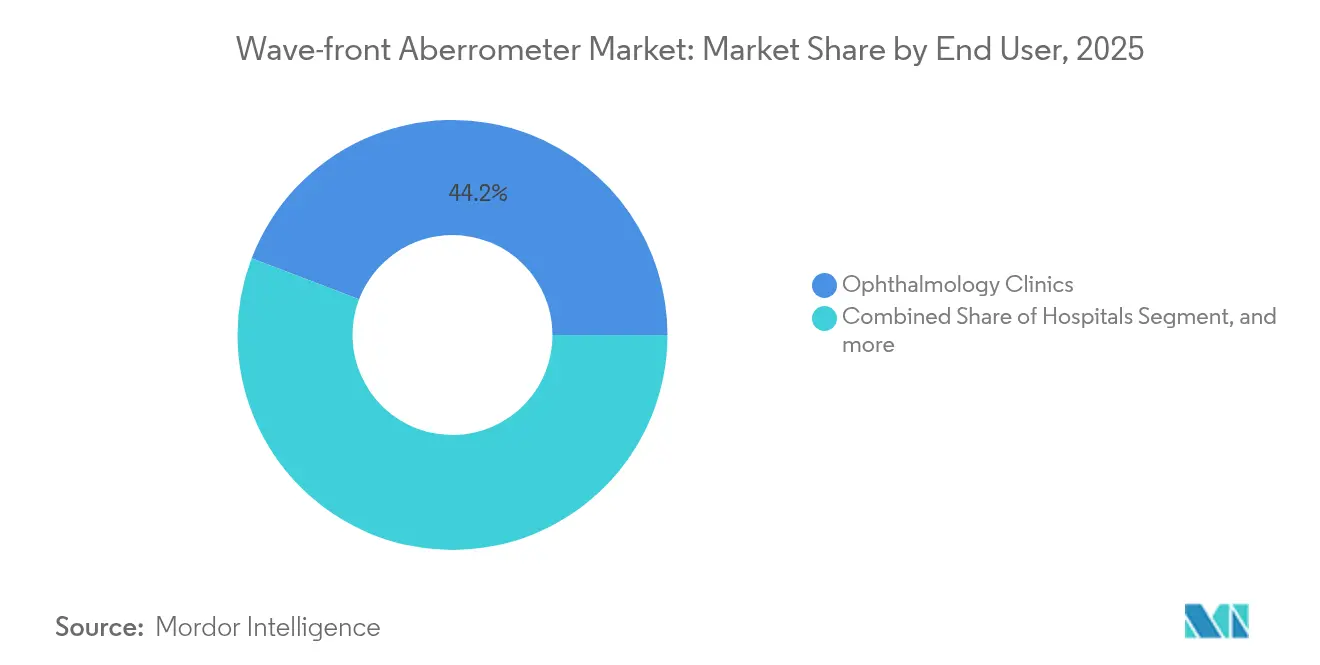

- By end user, ophthalmology clinics maintained a 44.20% share of the wavefront aberrometer market in 2025; ambulatory surgery centers showed the fastest growth at a 6.31% CAGR.

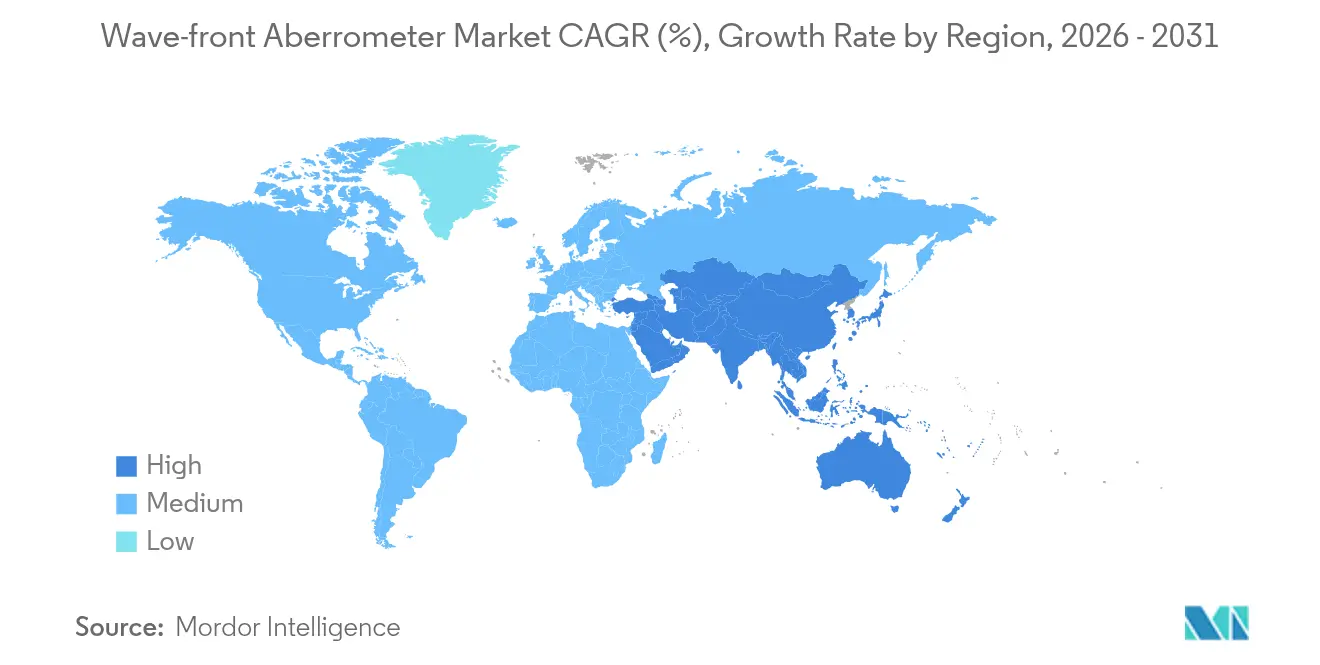

- By geography, North America captured 35.40% of the wavefront aberrometer market in 2025, while Asia-Pacific is poised for 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wavefront Aberrometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Prevalence of Uncorrected Refractive Errors | +1.2% | Global, with concentrated impact in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Surge In Adoption of Wavefront-Guided LASIK And Premium Cataract Procedures | +1.8% | North America & Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advancements in AI-Powered, Topography-Integrated Aberrometers | +0.9% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Rising Use of Intra-Operative Aberrometry to Optimize Intraocular Lens (IOL) | +1.1% | North America & Europe, selective adoption in Asia-Pacific | Medium term (2-4 years) |

| Expansion of Portable Aberrometer Solutions Enabling Remote Diagnostics | +0.7% | Global, with pronounced impact in underserved regions | Medium term (2-4 years) |

| Increased Demand for Precise Ocular Calibration In AR/VR Headsets | +0.4% | North America & Asia-Pacific, emerging in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Prevalence of Uncorrected Refractive Errors

Half of the world population may be myopic by 2030, with Asia-Pacific carrying the greatest burden.[1]Maria Raposo-Mocholi et al., “Global Prevalence of Myopia: 2025 Update,” MDPI, mdpi.com Governments respond by funding early-screening drives where portable devices such as handheld aberrometers identify refractive errors in schools and rural clinics. AI modules now deliver 88% sensitivity and 94% specificity in flagging abnormal wavefront profiles, trimming chair-time, and widening access. Population-level productivity gains further justify public investment, enlarging the wavefront aberrometer market. Vendors that bundle cloud analytics with low-footprint hardware gain an edge in mass-screening contracts.

Surge in Adoption of Wavefront-Guided LASIK and Premium Cataract Procedures

Wavefront-guided refractive surgery routinely delivers 20/40 vision or better in 99.7% of patients, outperforming conventional techniques. Patient willingness to pay for quality upgrades boosts demand for high-accuracy diagnostics. FDA clearance of Bausch + Lomb’s TENEO laser in late 2023 renewed competitive intensity, spotlighting systems that seamlessly integrate aberrometry, eye tracking, and topography. In the wavefront aberrometer market, this translates into higher per-procedure throughput because real-time wavefront data speeds lens-power confirmation. Premium IOL packages, often paid out-of-pocket, thus finance device upgrades despite tighter insurer reimbursements.

Advancements in AI-Powered, Topography-Integrated Aberrometers

Machine-learning models now predict corneal ectasia in subclinical stages, achieving an area-under-curve score of 0.945 in multicenter trials. Software suites such as iTrace Prime generate new indices that quantify quality of vision, giving surgeons richer decision support. Cloud processing reduces workstation hardware costs and permits remote second opinions, letting regional clinics access tertiary-level analytics. In the near term, these capabilities differentiate high-tier products; over time they will become table stakes across the wavefront aberrometer market.

Rising Use of Intra-Operative Aberrometry to Optimize IOL Choice

Systems like ORA and HOLOS deliver live readings that cut postoperative residual astigmatism ≤ 0.50 D in 92.8% of eyes, versus 58.3% when surgeons rely on pre-operative formulas alone. The benefit is greatest in toric, multifocal, and post-LASIK cases where conventional calculations fail. Real-time feedback also shortens revision rates, supporting outpatient cataract pathways that are central to ambulatory-surgery growth in the wavefront aberrometer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment and Per-Procedure Costs | -0.8% | Global, with pronounced impact in emerging markets | Long term (≥ 4 years) |

| Shortage of Skilled Ophthalmic Technicians Trained in Wavefront Diagnostics | -0.6% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Reimbursement Ambiguity Surrounding Intra-Operative Aberrometry Codes | -0.5% | North America & Europe, limited impact in Asia-Pacific | Short term (≤ 2 years) |

| Lack of Standardized Data Formats Impedes Seamless Integration | -0.3% | Global, with varying impact across healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Per-Procedure Costs

Integrated topography-aberrometers list above USD 200,000, while consumables add USD 50–100 per measurement.[2]American Academy of Ophthalmology, “Economic Considerations in Diagnostic Equipment Purchasing,” aao.org Small clinics in cost-sensitive regions struggle to justify these outlays, delaying refresh cycles even as technology leaps ahead. Leasing and pay-per-use models mitigate the hurdle, but margin compression remains real, especially after a 2.93% Medicare cut in 2025.[3]Centers for Medicare & Medicaid Services, “CY 2025 Physician Fee Schedule Final Rule,” cms.gov Until device prices fall or reimbursement improves, spending restraint will temper the wavefront aberrometer market trajectory.

Shortage of Skilled Ophthalmic Technicians Trained in Wavefront Diagnostics

Advanced aberrometry demands operators competent in aligning patients, interpreting higher-order aberrations, and troubleshooting AI workflows. Few accredited programs offer the 700-plus clinical hours needed for certification, creating a talent bottleneck. Clinics often cross-train staff, but the learning curve slows throughput and may discourage equipment investment. Vendors respond with guided user interfaces, yet human expertise remains critical to realize full diagnostic value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Integrated Systems Drive Innovation

Integrated topography-aberrometer systems accounted for 41.08% of the wavefront aberrometer market in 2025, reflecting clinician preference for single-platform corneal mapping and wavefront measurement. These units bundle Placido-disc topography with Hartmann-Shack sensors, letting surgeons refine ablation profiles and IOL power selections without switching devices. Table-top standalone systems still serve high-volume refractive practices where workflow efficiency outweighs multi-modality. Intra-operative aberrometers, although currently smaller in revenue, register a 7.02% CAGR because premium cataract surgeons require live feedback. The handheld sub-segment remains nascent but attracts telehealth programs and military medicine, particularly since forthcoming devices promise sub-USD 15,000 entry pricing that broadens the wavefront aberrometer industry customer base.

In competitive terms, integrated platforms now compete on software depth more than optical hardware. Firms adding biomechanics analytics or predictive AI secure premium price points. Meanwhile, modular architectures let clinics begin with diagnostics and later bolt on surgical guidance tools, easing capital budgeting. As cloud processing offloads computation, lightweight consoles could democratize advanced aberrometry across secondary-tier hospitals, raising the ceiling for the wavefront aberrometer market.

By Application: Presbyopia Acceleration Reshapes Demand

Myopia correction held 55.10% of the wavefront aberrometer market share in 2025. However, presbyopia is the fastest-rising application, advancing 6.65% annually as aging populations seek spectacle-free vision. Extended-depth-of-focus IOLs rely on precise spherical aberration management; thus, presbyopia’s rise directly boosts the wavefront aberrometer market. Astigmatism correction benefits from toric IOL precision, and keratoconus screening leverages higher-order maps coupled with biomechanical indices. Hyperopia remains a stable niche but gains from enhanced energy-profile algorithms embedded in next-generation platforms.

Diagnostic breadth also expands into virtual-reality headset calibration, sports vision, and occupational safety testing. These adjacent uses may not yet move headline numbers, but they diversify revenue and mitigate reliance on elective surgery cycles. Vendors that pre-configure application-specific software kits strengthen stickiness and generate recurring license fees, a pattern likely to persist across the wavefront aberrometer industry.

By End User: Ambulatory Centers Gain Momentum

Ophthalmology clinics generated 44.20% of the wavefront aberrometer market size in 2025. They remain anchors for pre-operative assessment and long-term follow-up, explaining their durability. Yet ambulatory surgery centers (ASCs) show 6.31% CAGR as outpatient refractive and cataract volumes migrate to cost-efficient settings. ASCs favor compact intra-operative units that slot into streamlined OR workflows and minimise patient transfer delays. Hospitals continue to purchase comprehensive suites for complex revisions and teaching labs, but growth is modest. Academic and research institutes, while small in revenue, drive breakthrough features that later filter into commercial models, sustaining the innovation cycle inside the wavefront aberrometer market.

Tele-optometry networks increasingly contract mobile technicians equipped with portable aberrometers, introducing a service-based revenue layer. Software as a Service (SaaS) dashboards enable multi-site practices to benchmark outcomes, nudging clinics toward standardised equipment ecosystems. Collectively, these trends re-shape purchasing criteria from pure hardware specs to total-cost-of-ownership evaluations that integrate maintenance, analytics, and staff training.

Geography Analysis

North America retained 35.40% of global revenue in 2025, or nearly USD 18.6 million of the wavefront aberrometer market size, thanks to entrenched reimbursement codes and high patient willingness to pay for premium IOLs. The region’s regulatory clarity, illustrated by smooth FDA clearance pathways for new excimer lasers, supports continual product refresh. Headwinds include Medicare’s 2025 rate cut, which pressures smaller practices to seek leasing over outright purchase. Consolidation among corporate practice groups may offset some strain by pooling capital for fleet upgrades.

Asia-Pacific posts the fastest regional expansion at 8.78% CAGR, adding USD 7.05 million incremental revenue by 2031. China’s streamlined National Medical Products Administration timelines and the Boao Lecheng fast-track zone slash approval lags, letting overseas-cleared aberrometers reach market early. India’s fresh device-marketing code, coupled with rising private-equity investment in eye-care chains, unlocks buying power. Japan and South Korea, already technologically advanced, lead AI module adoption, reinforcing the premium tier of the wavefront aberrometer market.

Europe shows mature yet steady demand, buoyed by evidence-based practice standards and national health insurance that reimburse functional improvements for cataract and refractive patients. EssilorLuxottica’s regional roll-up of clinics and Heidelberg Engineering assets deepens integration between diagnostics and therapy, potentially moving procurement toward closed-platform ecosystems . Emerging regions Middle East & Africa plus South America offer upside as private hospitals upgrade imaging suites; however, currency volatility and limited reimbursement temper near-term scale.

Competitive Landscape

The wavefront aberrometer market is moderately consolidated. Alcon, Carl Zeiss Meditec, Johnson & Johnson Vision, and EssilorLuxottica collectively exceed a higher revenue share. Each pairs hardware with proprietary software, locking in service contracts. Alcon’s USD 430 million acquisition of LENSAR extends its femtosecond laser franchise and folds intra-operative aberrometry deeper into its cataract platform. EssilorLuxottica’s buying spree, including Heidelberg Engineering, Optegra clinics, and Cellview Imaging, builds a vertically integrated eye-care ecosystem from retail to OR, tightening competitive pressure on stand-alone device makers.

Second-tier players innovate in portability and AI. Tracey Technologies’ iTrace line introduces cloud dashboards that small practices can deploy without hefty servers. Chinese manufacturers push value-priced handhelds tailored to school-screening programs, widening the geographic reach of the wavefront aberrometer market. Software-only entrants craft algorithms that retrofit onto existing cameras, threatening to commoditise optical hardware. In response, incumbents embed biomechanics analytics and machine-learning-driven surgical guidance to sustain differentiation.

Strategic alliances multiply: equipment vendors partner with tele-health platforms to offer integrated screening suites, while data-analytics firms bundle outcome benchmarking tools. Intellectual-property litigation remains rare but could rise as AI models become core competitive assets. Overall, rivalry is set to intensify yet remain innovation-led, preserving attractive gross margins for differentiated products.

Wavefront Aberrometer Industry Leaders

Luneau Technology

Carl Zeiss Meditec

NIDEK

EssilorLuxottica

Alcon

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is opening around higher-precision, workflow-integrated aberrometry that reduces dependence on subjective refraction and supports premium refractive outcomes across cataract and corneal procedures. Clinical work in 2026 evaluating open-field aberrometry designs (for example, CSO's OFA-Osiris) points to continued demand for objective refraction approaches that better manage accommodation-related measurement artifacts, while also keeping subjective refraction as the clinical backstop when discrepancies arise. This creates room for vendors to differentiate through measurement protocols, repeatability tooling, and decision-support layers, rather than focusing only on optical hardware.

A separate opportunity is deepening intra-operative aberrometry for premium and complex IOL selection as more evidence accumulates through real-world cohorts and prospective studies. A 2024 study in Frontiers in Medicine reported ORA VLynk outperforming standard biometry-based formulas for IOL power selection in long eyes with monofocal IOLs, and 2026 clinical research continues to validate ORA performance in toric IOL implantation using direct aphakic measurement. Parallel clinical evaluation activity, including the ongoing NCT07146828 study (initiated in 2025) assessing a binocular wavefront optometry machine with 0.05 D refraction increments for SMILE and FS-LASIK patients, highlights the push toward finer refractive steps and measurable quality-of-vision endpoints. That activity supports upgrades of integrated topography-aberrometer systems in surgical settings and high-volume ambulatory pathways.

Recent Industry Developments

- April 2026: Carl Zeiss Meditec highlighted digital and surgical refractive workflow solutions at ASCRS 2026 in Washington, D.C. The focus on connected diagnostics and surgical planning reinforces the shift toward platform-style purchasing where aberometry and related measurements sit inside a unified refractive workflow. This signals deeper integration of diagnostic and surgical data streams, enabling bundled offerings and cross-sell across imaging, planning, and intraoperative measurement modules.

- February 2026: Advance Medical announced the integration of the WaveDȳn aberrometer into the FocalPoints enVisus platform to support higher-order aberration correction in specialty lens manufacturing. Bringing wavefront measurement into an automated manufacturing workflow extends aberrometry demand beyond clinic-only diagnostics into lens production and customization.

- December 2025: Eaglet Eye partnered with OVITZ to distribute the xwave aberrometer in Europe for scleral lens fitting. The agreement expands access to wavefront-guided specialty contact lens workflows and strengthens the role of aberrometry in non-surgical vision correction pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues from new wavefront aberrometer systems used to measure ocular wavefront errors for diagnostic and preoperative planning, mainly in refractive and cataract workflows, and for advanced contact lens fitting.

Scope exclusions: Conventional autorefractors, corneal topographers without wavefront capability, and refurbished or rental units are excluded from this sizing.

Segmentation Overview

- By Product Type

- Table-Top Stand-Alone Systems

- Integrated Topography–Aberrometer Systems

- Intra-Operative Aberrometers

- Hand-Held / Portable Aberrometers

- By Application

- Myopia

- Hyperopia

- Astigmatism

- Presbyopia

- Keratoconus & Ectasia

- Others

- By End User

- Hospitals

- Ophthalmology Clinics

- Ambulatory Surgery Centres

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we first collect base demand signals tied to eye care procedures and device adoption, then align those signals to the specific wavefront measurement use case. Public sources such as the US FDA device databases, CDC and NIH publications, WHO eye health materials, and OECD health statistics are used to frame procedure volumes, care settings, and technology diffusion. We also review customs and trade statistics portals where available to sense-check cross-border flows of ophthalmic diagnostic equipment, and we review peer-reviewed ophthalmology and optometry journals to understand how aberrometry is used in routine practice.

On the supply side, we review company filings, investor presentations, and product documentation to map installed base signals, product positioning, and replacement cycles. We then use reputed press and association websites for regulatory and reimbursement context. Select paid subscriptions for company financials and news intelligence, along with patent databases, are used to verify timelines, product launches, and ownership changes that can affect year-to-year revenue. These sources are illustrative, and additional public materials were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to convert broad eye care activity into a realistic purchase and upgrade pool for wavefront aberrometers, since usage intensity differs by clinic type and procedure mix. We speak with hospital administrators, specialty clinic owners, ambulatory surgical center teams, distributors, and service partners across major regions so assumptions on pricing, replacement timing, and attachment to refractive and cataract workflows can be checked and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | APAC: 46% |

| Mid tier: 53% | Functional/Unit leaders: 23% | EMEA: 30% |

| Smaller Players: 20% | Managers: 60% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where procedure volumes and eye care capacity indicators are used to reconstruct realistic addressable demand for wavefront measurement, then convert that pool into device revenues using adoption and refresh assumptions. Results are then corroborated using selective bottom-up approximations, such as sampled average selling price by device class multiplied by estimated unit shipments through key channels, followed by adjustments where gaps appear.

Key inputs used in the model include refractive surgery and cataract surgery volumes, the share of surgeries and fittings where aberrometry is used, the mix of standalone versus integrated topography-aberrometer systems, typical replacement cycles for diagnostic capital equipment, and ASP movement by configuration and service bundling (when hardware is sold with bundled software). When respondent inputs differ by care setting, we apply setting-level weights so large hospital procurement is not treated the same as specialty clinic purchasing.

For forecasting, scenario analysis is used around procedure growth, adoption rates, and pricing bands, then smoothed into year-by-year outputs so short-term spikes do not distort the trend. Where bottom-up inputs are incomplete for smaller countries, we use proxy indicators such as ophthalmology center counts and procedure intensity per capita, and then re-check the implied revenue per facility with interviews before finalizing totals.

Data Validation & Update Cycle

Validation is done through multiple checks that compare model outputs against independent signals, including procedure trends, trade movement direction, and implied device spend per relevant care site. Large variances are flagged, and the assumptions behind adoption, refresh, and ASP are revisited until the numbers reconcile in a sensible way.

Before sign-off, the work is reviewed in steps, starting with peer checks on the input table, then a second pass on calculations and year-over-year movements. Reports are refreshed annually, and interim updates are triggered when material events occur, such as regulatory changes, major product launches, or meaningful pricing shifts. Right before delivery, we perform a final refresh pass to ensure the output reflects the latest available information.

Mordor Intelligence's Wavefront Aberrometer Market Size Compared With Other Published Estimates

Published market sizes for wavefront aberrometers can look far apart, even when the growth story sounds similar. Differences usually come from how each study treats product boundaries, which base year is used, and how pricing and replacement timing are handled in the model.

By tracking bundled versus unbundled software revenue rules and refreshing the inclusion tests for integrated topography-aberrometer systems, Mordor Intelligence keeps the wavefront aberrometer total tied to new equipment sales and avoids mixing in adjacent diagnostic categories that inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 55.20 M (2026) | |

| Global Consultancy A | USD 43.02 M (2024) | Uses an earlier base year and may apply different conversion from indication-level demand to equipment revenue, which can understate near-term sales if replacement cycles and integrated systems are weighted lower. |

| Regional Consultancy B | USD 37.40 M (2023) | Starts from a 2023 base and follows a slower growth path, and the scope appears to rely more on broad segmentation without clearly separating new equipment revenues from adjacent optical diagnostic tools. |

Across the three estimates, the spread is mainly explained by base-year choice, how tightly the product scope is drawn, and how pricing and replacement assumptions are updated over time. Our approach stays traceable because each step is linked to procedure activity, care-site adoption, and a clear equipment revenue definition, which can be rechecked when new signals emerge.

Key Questions Answered in the Report

What is the current value of the wavefront aberrometer market?

The wavefront aberrometer market is valued at USD 55.2 million in 2026 and is projected to reach USD 70.64 million by 2031.

Which product segment is growing fastest?

Intra-Operative Aberrometers record the highest growth at a 7.02% CAGR through 2031, driven by demand for real-time IOL power confirmation during cataract surgery.

Why is Asia-Pacific considered the most attractive growth region?

Regulatory streamlining, rising private healthcare investment, and high myopia prevalence push Asia-Pacific to a 8.78% CAGR, outpacing all other regions.

How do artificial-intelligence upgrades influence buying decisions?

AI modules enhance ectasia risk prediction and surgical planning accuracy, making integrated systems more compelling and encouraging clinics to refresh older equipment.

What are the main barriers to wider adoption of wavefront aberrometers?

High upfront costs, per-procedure consumable expenses, and a shortage of technicians skilled in advanced diagnostics remain key restraints.

How have reimbursement changes affected the market?

The 2.93% reduction in Medicare payments for 2025 pressures U.S. practices, prompting greater reliance on leasing and service-based procurement models to manage cash flow.

Page last updated on: