United Arab Emirates Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

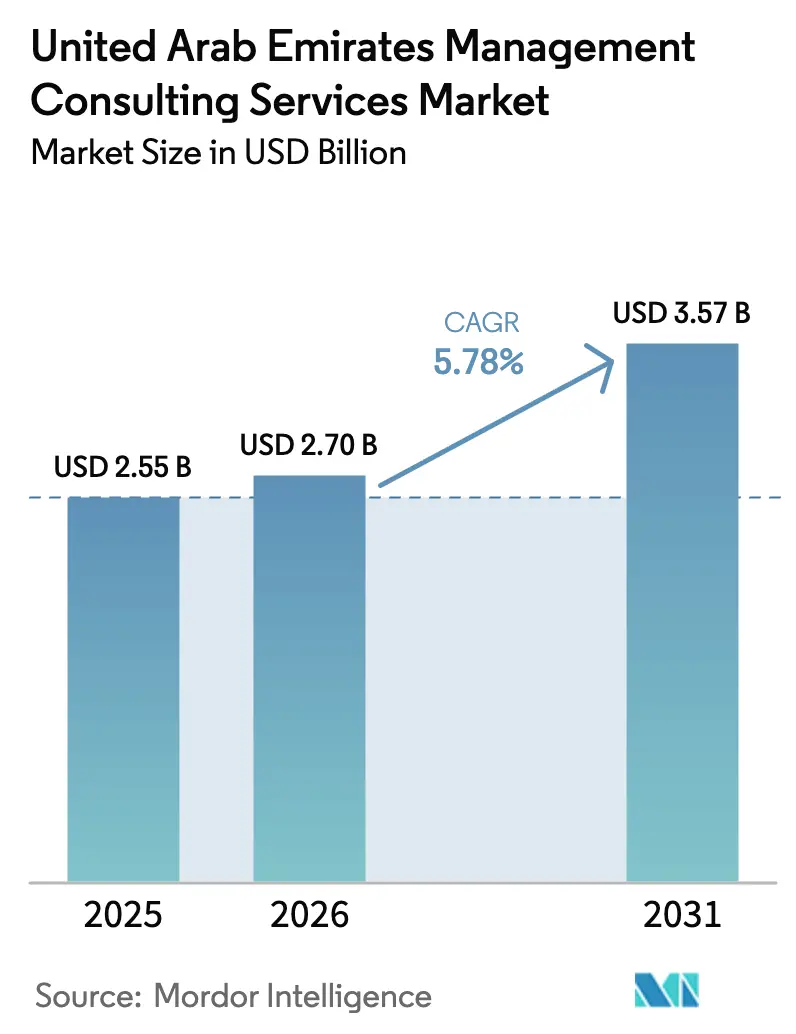

| Base Year Market Size (2025) | USD 2.55 Billion |

| Market Size (2026) | USD 2.7 Billion |

| Market Size (2031) | USD 3.57 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Management Consulting Services Market Analysis by Mordor Intelligence

The United Arab Emirates management consulting services market size was valued at USD 2.55 billion in 2025 and estimated to grow from USD 2.7 billion in 2026 to reach USD 3.57 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). The national diversification agenda powers this market trajectory, mandatory ESG disclosures, and large-scale digital transformation programs that require specialist knowledge in strategy, operations, and cutting-edge technologies. Growing regulatory complexity around data sovereignty and corporate taxation further elevates the need for compliance-oriented consulting solutions, while free-zone incentives attract foreign SMEs that rely on external advisers for efficient market entry. The national green-hydrogen roadmap, targeting 1.4 million tons of annual production by 2031, stimulates demand for project management and sustainability briefs. Large enterprises still account for nearly four-fifths of current spend, yet small and medium-sized enterprises accelerate consulting democratization through digital platforms and hybrid delivery models. Compliance-heavy sectors—including finance, healthcare, and energy—continue to prioritize external experts to meet evolving obligations, driving consistent deal flow in the United Arab Emirates management consulting services market.

Key Report Takeaways

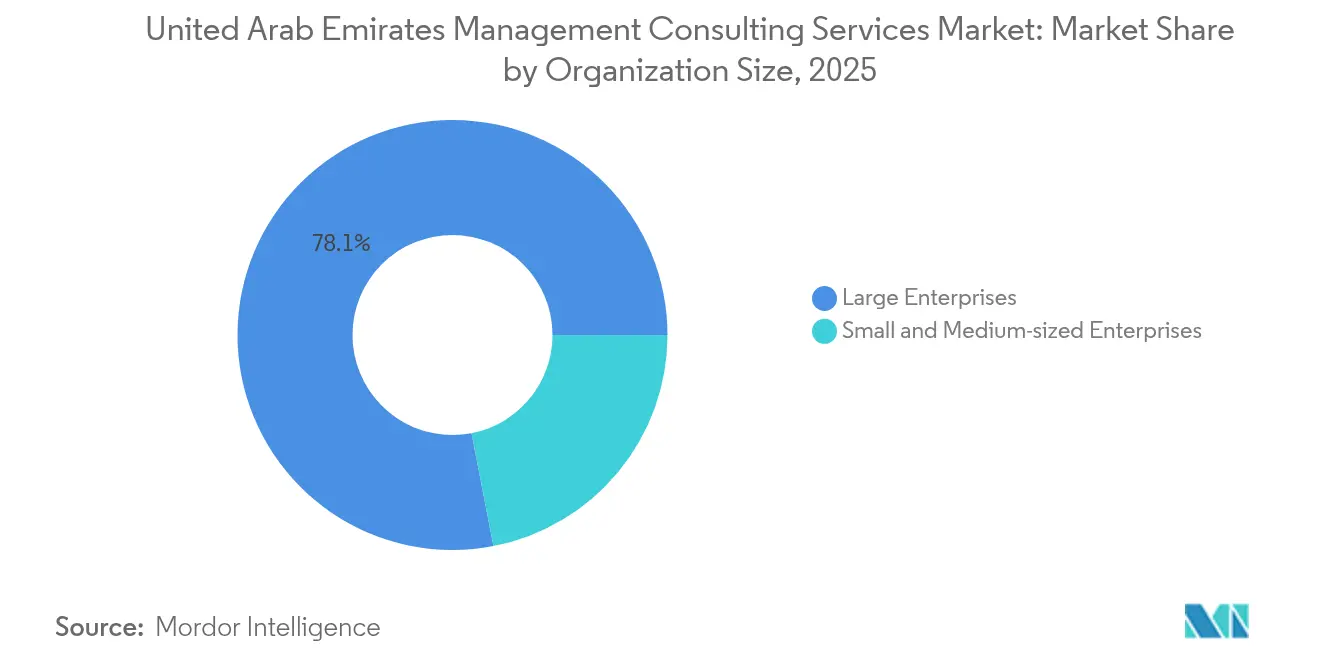

- By organization size, large enterprises dominated with 78.05% United Arab Emirates management consulting services market share in 2025, while SMEs recorded the highest projected CAGR at 7.05% through 2031.

- By service type, operations consulting led with 36.68% of the United Arab Emirates management consulting services market size in 2025, whereas technology consulting is forecast to expand at 9.12% CAGR between 2026-2031.

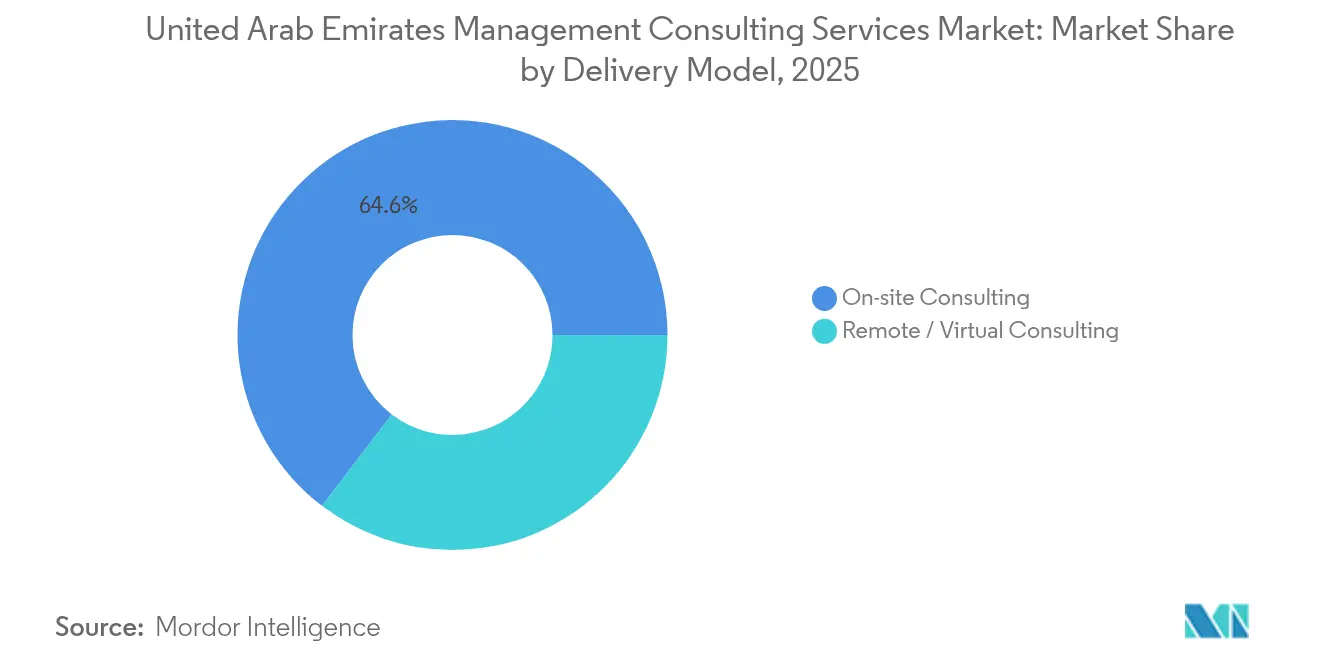

- By delivery model, on-site consulting captured 64.62% United Arab Emirates management consulting services market share in 2025 and remote formats are advancing at a 7.18% CAGR through 2031.

- By end-user industry, financial services held 25.12% of the United Arab Emirates management consulting services market size in 2025, while healthcare and life sciences is progressing at a 14.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2031 national diversification agenda boosts advisory spend | +1.2% | Dubai, Abu Dhabi, federal agencies | Medium term (2-4 years) |

| Mandatory ESG reporting for listed firms | +0.8% | DFM, ADX | Short term (≤ 2 years) |

| Accelerated digital transformation and AI adoption | +1.5% | All emirates, led by government | Medium term (2-4 years) |

| Free-zone incentives attracting foreign SMEs | +0.9% | 40+ free zones | Long term (≥ 4 years) |

| Green-hydrogen and clean-energy megaproject pipeline | +0.7% | Abu Dhabi, Northern Emirates | Long term (≥ 4 years) |

| Growing family-office professionalization | +0.6% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2031 national diversification agenda boosts advisory spend

The federal “We the UAE 2031” roadmap seeks to double GDP to AED 3 trillion and lift non-oil exports to AED 800 billion, prompting enterprises to realign portfolios and governance models, which fuels strategic, operational, and HR advisory contracts across 14 priority sectors. [1]Ministry of Economy, “UAE GDP Growth in First Nine Months of 2024,” MOEC.GOV.AE Early-stage success—non-oil GDP rose 4.5% in the first nine months of 2024—has heightened demand for consultants who can guide market-entry design, supply-chain localization, and Emiratization compliance. Transport and warehousing, expanding 7.9%, and construction, rising 7.4%, are among the most active verticals for process-optimization projects. The industrial sector added USD 54 billion to GDP in 2023, underlining the strong need for continuous productivity improvements. In parallel, rising foreign business registrations swell the client base for incorporation, tax, and regulatory expertise, keeping the United Arab Emirates management consulting services market on an ascending course.

Mandatory ESG reporting for listed firms drives sustainability consulting

Dubai Financial Market and Abu Dhabi Securities Exchange require listed entities to publish granular sustainability metrics, immediately translating into advisory mandates around data capture, materiality mapping, and assurance. [2]SSE Initiative, “Abu Dhabi Securities Exchange ESG Reporting,” SSEINITIATIVE.ORG The rule’s compulsory status removes any budget hesitation, shifting ESG from discretionary to essential. New digital-economy entrants operating inside DIFC must reconcile carbon accounting with corporate-tax compliance, further expanding the consulting remit. National net-zero and renewable-energy pledges, underpinned by up to AED 200 billion of investment, add project-finance and green-bond structuring workstreams. As reporting cycles mature, demand is migrating from framework design to performance benchmarking and value-chain decarbonization, deepening wallet share for sustainability advisers in the United Arab Emirates management consulting services market.

Accelerated digital transformation and AI adoption among UAE corporates

Abu Dhabi’s USD 13 billion program to become the world’s first fully AI-native government by 2027 involves more than 200 solutions across all public services, spawning extensive opportunities in architecture design, change management, and cybersecurity. The federal Digital Economy Strategy aims to raise the digital share of non-oil GDP from 12% to 20% by 2030, compelling companies to integrate cloud, analytics, and automation at pace. Sector-specific pilots—such as AI-driven medical-claims analysis rolled out in Dubai Healthcare City—demonstrate tangible efficiency gains and, by extension, prime pipelines for tech implementation consultancies. Hyperscale data-center expansion supporting the Stargate AI project intensifies advisory work in infrastructure design and data-protection compliance. Together, these undertakings elevate technology consulting to the fastest-growing slice of the United Arab Emirates management consulting services market.

Free-zone incentives attracting foreign SMEs that outsource consulting

More than 40 free zones grant 100% foreign ownership and 0% corporate tax for qualifying income, yet impose rigorous substance tests, transfer-pricing documentation, and evolving e-invoicing rules that SMEs seldom manage internally. The number of active companies in DIFC alone jumped 25% to 7,700 in 2025, translating into sustained demand for setup, legal-structure optimization, and ongoing compliance services. Upcoming Peppol-based e-invoicing deadlines add a technology layer, creating multiyear advisory annuities around ERP integrations and tax-reporting automation. These conditions reinforce SME reliance on external counsel, supporting steady volume growth in the United Arab Emirates management consulting services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortages and visa cost inflation for senior consultants | -0.9% | Nationwide | Short term (≤ 2 years) |

| Intensifying fee pressure from boutique and freelance platforms | -0.7% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Rising data-sovereignty rules limiting remote delivery | -0.5% | Nationwide | Medium term (2-4 years) |

| Heightened compliance scrutiny of public-sector tenders | -0.6% | All emirates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Talent shortages and visa cost inflation for senior consultants

Mandatory Emiratization quotas for companies with 20-49 employees exacerbate competition for qualified nationals, while new green-visa thresholds require minimum AED 15,000 salaries and bachelor’s degrees, raising cost structures for foreign specialists. [3]GDRFA-Dubai, “Green Visa for Skilled Workers,” GDRFAD.GOV.AE Parallel expansion of the domestic ICT sector, valued at USD 39.72 billion in 2023, strains the same talent pool, creating wage inflation for digital and cybersecurity consultants. The United Arab Emirates management consulting services market, therefore, faces delivery-capacity bottlenecks, compelling firms to invest in local talent development and offshore knowledge hubs to maintain margin integrity.

Intensifying fee pressure from boutique and freelance platforms

Low-cost entry via free-zone structures encourages niche boutiques to undercut established players on commoditized engagements such as regulatory filings and basic process audits. Digital marketplaces match freelancers with clients for transactional tasks, pushing price expectations downward. While high-complexity projects still command premium rates, mid-tier assignments experience margin compression, prompting incumbents to differentiate through specialized IP and sector expertise to safeguard share in the United Arab Emirates management consulting services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs drive consulting democratization

Small and medium-sized enterprises contributed a vigorous 7.05% CAGR outlook through 2031 despite large corporates holding a prevailing 78.05% stake in the United Arab Emirates management consulting services market in 2025. Free-zone registrations in Dubai surpassed 70,500 in 2024, and each new entity requires incorporation assistance, tax-compliance roadmaps, and HR frameworks for Emiratization adherence. The democratization trend gains traction as digital consulting platforms offer modular, pay-as-you-go packages that balance cost with expertise. SMEs also tap advisers for Peppol e-invoicing roll-outs, transfer-pricing documentation, and cloud migration, reinforcing their role as a steady pipeline contributor to the United Arab Emirates management consulting services market.

Large enterprises remain primary revenue anchors through multi-year transformations in AI, green energy, and global expansion. Abu Dhabi’s AI-native initiative alone channels consulting fees across more than 200 projects, underscoring the strategic heft of corporate and public mega-clients. Nonetheless, price-sensitive SMEs broaden the market base, making the segment critical for volume growth and service-line innovation such as subscription compliance monitoring. Workforce nationalization targets also foster advisory engagements in talent management and learning platforms, further embedding SMEs within the collective trajectory of the United Arab Emirates management consulting services market.

By Service Type: Technology consulting accelerates digital transformation

Technology engagements are projected to grow at 9.12% CAGR, eclipsing all other categories, while operations consulting preserved a 36.68% leadership share in 2025. AI adoption in government, finance, and healthcare fuels demand for cloud architecture, data governance, and algorithm-bias mitigation guidance, anchoring technology’s outperformance. At the same time, corporate tax and ESG regulations maintain momentum for operations and strategy consultants who optimize processes and pivot operating models toward compliance readiness. AppliedAI’s locally built workflow platform showcases productivity gains exceeding 80% in turnaround times, reinforcing measurable ROI that sustains premium pricing for specialized tech briefs.

Operations consulting continues to dominate because diversification priorities require supply-chain localization, lean manufacturing, and shared-services consolidation across legacy sectors. HR advisory expands on the back of Emiratization quotas and talent-scarcity mitigation programs, while sustainability consulting scales quickly to address mandatory ESG filings. The broadening palette of service lines together cements a comprehensive offering within the United Arab Emirates management consulting services market, allowing providers to cross-sell complementary expertise over longer engagement lifecycles.

By Delivery Model: Remote consulting gains despite data-sovereignty constraints

On-site engagements claimed 64.62% of the United Arab Emirates management consulting services market size in 2025, yet virtual delivery is projected to record 7.18% CAGR through 2031 as firms perfect hybrid models that satisfy privacy statutes. Personal-data transfers now require equivalency assessments, prompting deployment of regional data-processing centers and secure-tunnel architectures that enable consultants to work remotely while keeping data resident in the UAE. Post-pandemic cultures favor video collaboration and asynchronous workflows, enhancing client acceptance of remote advisory for diagnostics, training, and code reviews. Mandatory Peppol e-invoicing enforces cloud connectivity, creating natural pull for virtual technology consultants.

The hybrid approach mitigates travel costs, accelerates talent deployment, and supports 24-hour cycle times while preserving compliance. As large public entities scale AI adoption, they increasingly stipulate local-hosting or sovereign-cloud clauses, further driving investment in UAE-based secure delivery hubs. Thus, remote models expand incrementally, harnessing digital efficiency gains without breaching regulatory thresholds, and enriching service diversity in the United Arab Emirates management consulting services market.

By End-User Industry: Healthcare leads growth amid infrastructure expansion

Healthcare and life sciences show the fastest 14.02% CAGR forecast through 2031, propelled by Dubai’s gap analysis that identified acute-bed and outpatient shortfalls requiring expansive capital programs, operating-model redesign, and revenue-cycle optimization. AI-driven claims analysis initiatives in Dubai Healthcare City exemplify tech-enabled consulting niches with measurable bottom-line impact.

Financial services, holding 25.12% of the United Arab Emirates management consulting services market share in 2025, remains the largest single vertical due to wealth-management inflows and regulatory recalibration within ADGM and DIFC. Manufacturing retains high advisory intensity through Operation 300bn incentives, while energy and utilities demand deep project-management expertise for nuclear, solar, and hydrogen undertakings. Government bodies serve as anchor clients for digital-service redesign and procurement modernization, with Abu Dhabi’s AI program providing a blueprint for national replication. Together, these industries diversify revenue streams and hedge providers against cyclicality within the United Arab Emirates management consulting services market.

Geography Analysis

Dubai and Abu Dhabi jointly absorb the majority of consulting spend, driven by DIFC’s 7,700-company ecosystem and Abu Dhabi’s AI-first public-sector doctrine. DIFC’s active firm count surged 25% in 2025, a magnet for financial-services advisers, compliance specialists, and technology integrators. Abu Dhabi’s USD 13 billion AI program necessitates complex vendor-management and skills-transfer roadmaps, anchoring multi-year contracts for digital strategists. The combined pull from both emirates reinforces a dense project pipeline within the United Arab Emirates management consulting services market.

Northern emirates contribute via industrial diversification and renewable megaprojects, including the Mohammed bin Rashid Solar Park and Al Dhafra PV field, which call for structured-finance advice and supply-chain audits. Sharjah and Ras Al Khaimah deploy free-zone models to attract advanced manufacturing SMEs, expanding regional demand for operational excellence consulting. The federal vision to elevate logistics competitiveness across land, sea, and air corridors encourages network-optimization assignments spanning multiple emirates, ensuring geographically balanced growth in the United Arab Emirates management consulting services market.

Cross-border service provisioning through sovereign-cloud set-ups allows advisers based in one emirate to serve clients elsewhere without violating data-locality rules, enhancing market fluidity. As free zones tailor value propositions—ADGM for finance, DMCC for commodities, KEZAD for industry—consultants align sector playbooks and regulatory toolkits to each locale’s specialization, reinforcing the federated yet integrated character of the United Arab Emirates management consulting services market.

Competitive Landscape

The United Arab Emirates management consulting services market is moderately fragmented, with global firms, regional specialists, and boutique advisers competing on domain expertise, price, and delivery innovation. Technology consulting displays higher fragmentation as AI and cybersecurity niches attract start-ups, while strategy engagements remain concentrated among marquee names leveraging longstanding public-sector relationships. Free-zone incentives have lowered entry barriers, enabling new arrivals such as Primus Partners and Searce to establish regional bases, intensifying bid competition. Meanwhile, Lazard’s expansion underscores opportunities in financial advisory, though premium assignments often migrate to specialists with deep regulatory insight into ADGM and DIFC frameworks.

Differentiation hinges on intellectual property around ESG, corporate tax, and data-sovereignty compliance. Firms offering AI-enabled accelerators like workflow-automation toolkits reduce engagement cycles by up to 80%, setting new efficiency benchmarks. Family-office professionalization introduces a profitable niche for governance and impact-investment advisories, with ultra-wealthy clients valuing long-term, high-touch relationships. Price pressure from freelance platforms persists in commoditized segments, prodding incumbents to pivot toward high-complexity, high-margin projects that anchor their relevance within the United Arab Emirates management consulting services market.

Regulatory shifts act as both hurdles and differentiators. Providers that invest early in sovereign-cloud infrastructure and local talent pools navigate data-residency mandates more smoothly, winning hybrid delivery mandates. Talent shortages nevertheless elevate wage costs, compelling firms to adopt aggressive graduate-hiring and upskilling programs. The combined dynamics underscore a competitive arena that rewards specialization, innovation, and compliance acuity.

United Arab Emirates Management Consulting Services Industry Leaders

Accenture Middle East B.V.

McKinsey & Company, Inc.

Deloitte & Touche (M.E.) LLP

KPMG Lower Gulf Limited

PricewaterhouseCoopers (PWC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Enec and Samsung C&T signed an MoU to explore international nuclear-energy investments, broadening consulting prospects in project management and regulatory approvals.

- July 2025: DIFC reported a 25% jump in active companies to 7,700 and 9% workforce growth to 47,901 professionals, expanding advisory opportunities in finance and fintech.

- July 2025: CVC and Tabreed partnered to acquire a UAE district-cooling business, opening avenues for M&A and operational-efficiency consultants in utilities.

- June 2025: PIMCO joined forces with Aditum Investment Management to launch DFSA-registered feeder funds, creating structuring mandates for asset-management advisers.

United Arab Emirates Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other End-user Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the United Arab Emirates management consulting services market?

The market is valued at USD 2.7 billion in 2026 and is forecast to reach USD 3.57 billion by 2031.

Which service type is growing the fastest across UAE clients?

Technology consulting leads growth with a 9.12% CAGR through 2031, driven by AI and cloud adoption.

How do mandatory ESG rules affect consulting demand?

Compulsory sustainability disclosures at DFM and ADX make ESG advisory a non-negotiable cost for listed companies and spur multi-year consulting contracts.

Why are SMEs important for consulting providers in the UAE?

Free-zone incentives attract foreign SMEs that rely on external advisers for company formation, tax compliance, and digital-process integration, supporting a 7.05% CAGR in SME consulting spend.

What factors limit faster consulting-sector expansion in the UAE?

Talent shortages, rising visa costs, and stringent data-sovereignty laws inflate operating expenses and complicate remote service delivery.

Which emirates generate the most consulting opportunities?

Dubai drives volume through DIFC’s financial cluster, while Abu Dhabi anchors large technology and public-sector programs such as its AI-first government initiative.

Page last updated on: