Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

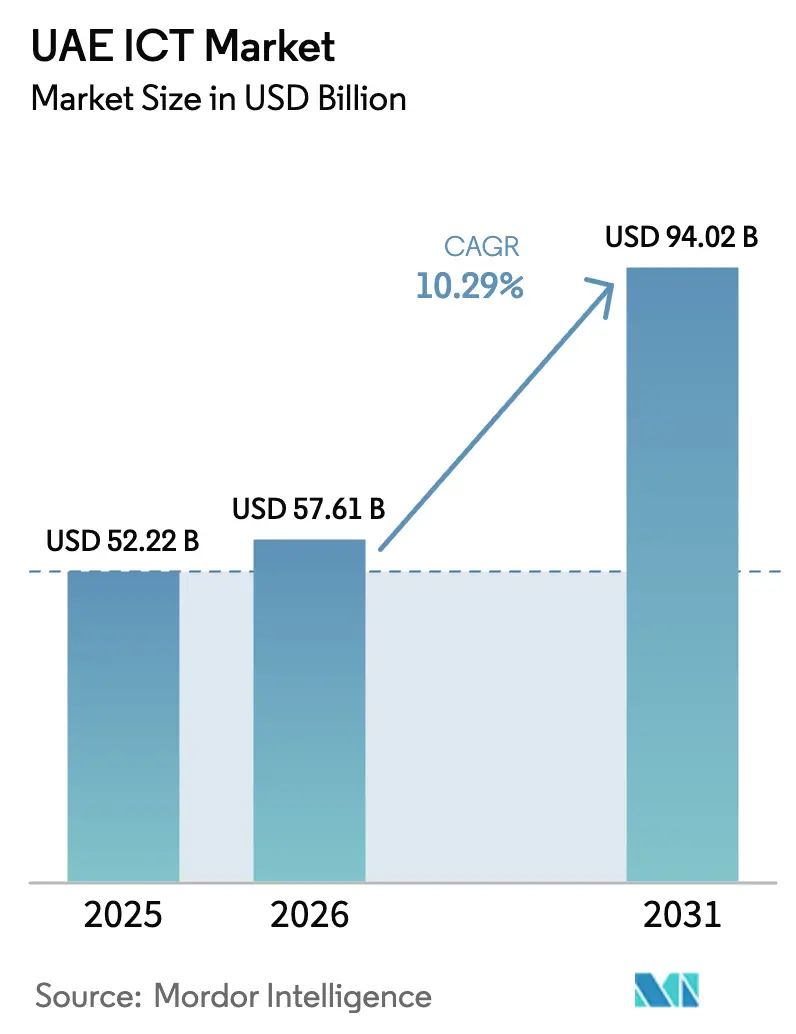

| Base Year Market Size (2025) | USD 52.22 Billion |

| Market Size (2026) | USD 57.61 Billion |

| Market Size (2031) | USD 94.02 Billion |

| Growth Rate (2026 - 2031) | 10.29% CAGR |

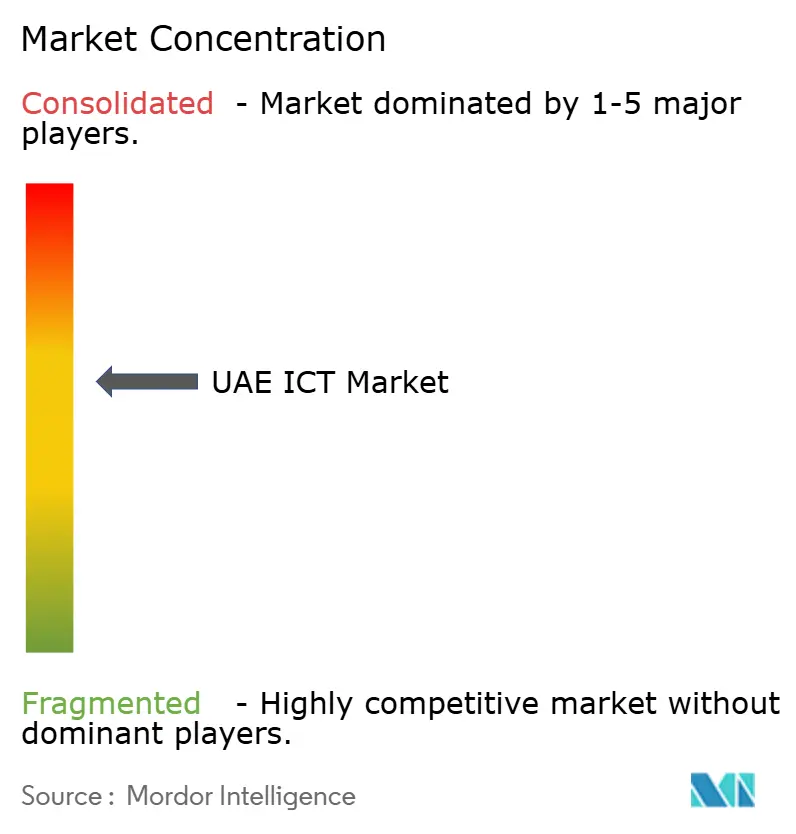

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE ICT Market Analysis by Mordor Intelligence

The UAE ICT Market size is projected to expand from USD 52.22 billion in 2025 and USD 57.61 billion in 2026 to USD 94.02 billion by 2031, registering a CAGR of 10.29% between 2026 to 2031. The current growth momentum is fueled by sovereign-cloud mandates, AED 13 billion (USD 3.54 billion) in federal digital-infrastructure funding, and a hyperscaler pipeline already exceeding USD 1.5 billion in committed capital. Enterprise demand now pivots on data-residency compliance, 5G-enabled edge workloads, and the National AI Strategy 2031 goal of AED 335 billion (USD 91.2 billion) in annual economic impact. Accelerated rollouts of cloud-native ERP systems, tighter cybersecurity regulations, and a corporate-tax regime that rewards digitized bookkeeping further amplify spending momentum. Competitive rivalry is intensifying as telecom incumbents reposition as platform players and hyperscalers localize capacity to meet strict sovereignty rules, creating a two-tier vendor landscape across public-sector and SME domains.

Key Report Takeaways

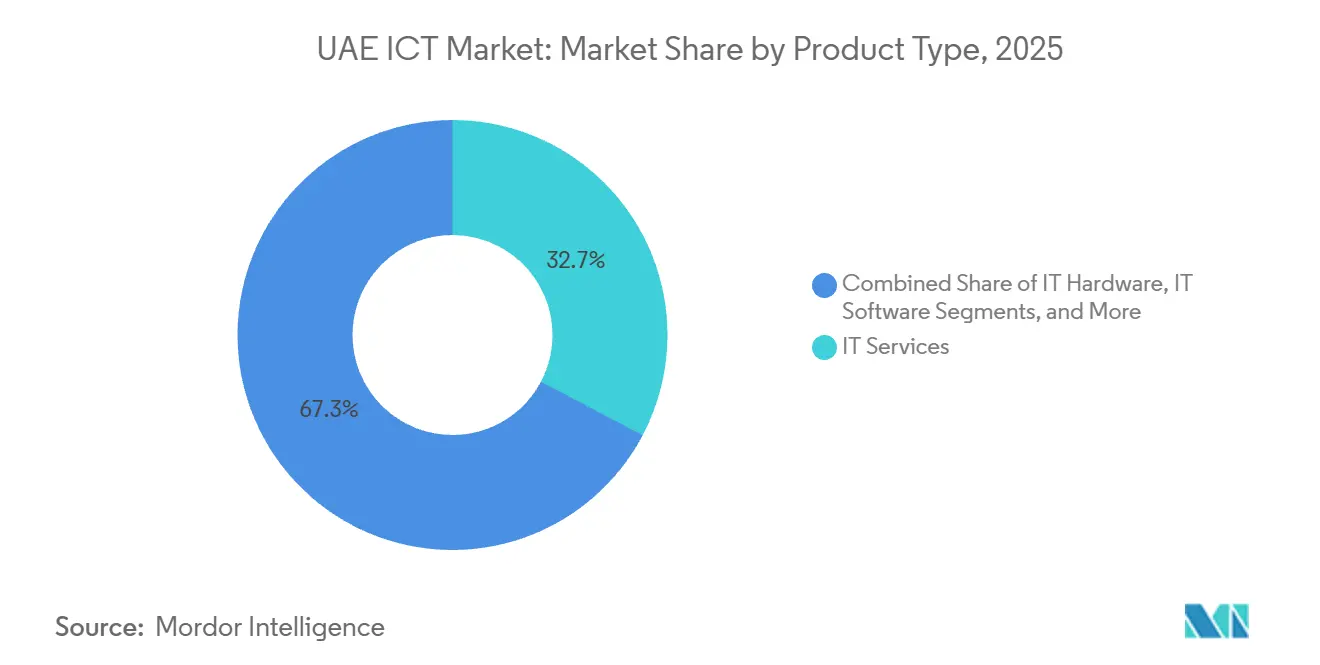

- By product type, IT services led with a 32.73% revenue share in 2025 of the UAE ICT market, while IT security and cybersecurity are advancing at an 11.11% CAGR through 2031.

- By enterprise size, large enterprises held 62.84% of the UAE ICT market share in 2025, yet SMEs are forecast to record a 12.04% CAGR to 2031.

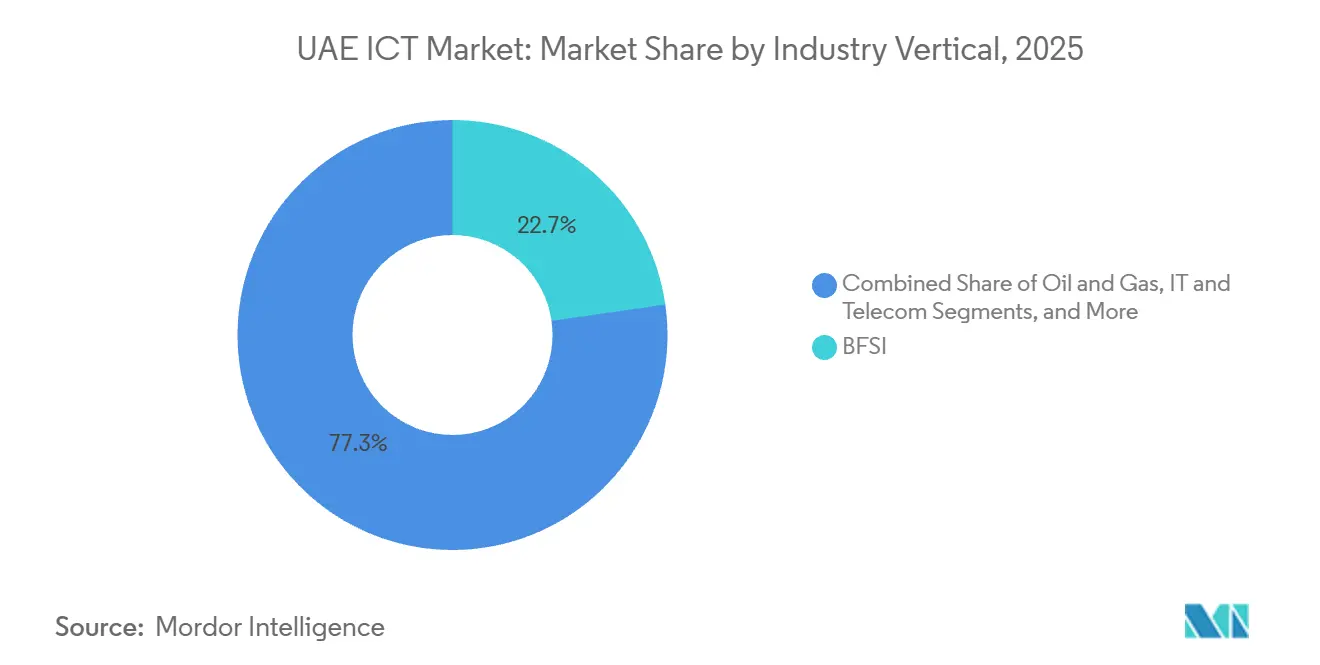

- By vertical, BFSI commanded 22.74% of spending in 2025 of the UAE ICT market; healthcare is expanding at an 11.46% CAGR through 2031.

- By deployment model, cloud models captured 46.83% of the UAE ICT market size in 2025 and are growing at an 11.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-City and 5G Infrastructure Build-Out | +2.3% | National, concentrated in Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Cloud-First Federal Mandates and Digital-Transformation Programs | +2.1% | National, cascading to emirate-level entities | Short term (≤ 2 years) |

| Hyperscaler Expansion Driven by In-Country Data-Residency Rules | +1.8% | National, anchored in Abu Dhabi and Dubai free zones | Medium term (2-4 years) |

| National AI Strategy 2031 Accelerating Enterprise AI Adoption | +1.6% | National, early gains in BFSI, government, healthcare | Long term (≥ 4 years) |

| Corporate-Tax Rollout Spurring ERP Upgrades | +1.2% | National, SME and mid-market segments | Short term (≤ 2 years) |

| COP28 Net-Zero Goals Driving Green ICT Procurement | +0.9% | National, pilot projects in Abu Dhabi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smart-City and 5G Infrastructure Build-Out

Nationwide 5G coverage already reaches 99.5% of populated areas, yet private-network adoption among factories and ports still sits below 15%. Municipal sensor grids, intelligent traffic systems, and edge-compute nodes require ultra-low latency, pulling new investment into radio-access upgrades and metro fiber rings. Systems integrators are bundling spectrum coordination, network design, and managed services to capture recurring revenue as industrial campuses digitize. ISO 27001 certification is now compulsory for vendors in many smart-city procurements, raising entry barriers but assuring baseline resilience. The combination of ubiquitous coverage and under-penetrated enterprise use cases provides a multi-year runway for network equipment makers, cybersecurity providers, and application developers.

Cloud-First Federal Mandates and Digital-Transformation Programs

The federal cloud-first directive obliges agencies to default to public or hybrid cloud, reserving on-premise builds for legacy systems under active modernization plans.[1]Government of the UAE, “Cloud-First Policy,” u.ae Abu Dhabi’s Digital Strategy allocates AED 13 billion (USD 3.54 billion) to migrate 80% of services to cloud platforms by 2027. Preference now skews toward hyperscalers with UAE sovereign-cloud attestations, squeezing mid-sized providers without local regions. Compliance with the National Cloud Security Policy further narrows the eligible vendor pool, favoring platforms that deliver native encryption, access logging, and incident response at UAE data-classification tiers. This consolidation reshapes procurement cycles, shortens proof-of-concept phases, and accelerates time-to-production for new digital services.

Hyperscaler Expansion Driven by In-Country Data-Residency Rules

Oracle’s second UAE region, operational in 2024, joins Microsoft Azure and AWS in providing multi-region redundancy without cross-border data flows. Google Cloud’s planned launch will further pressure pricing as enterprises adopt multi-cloud bargaining tactics. Capital intensity climbs while margin headroom shrinks, pushing hyperscalers to upsell advanced analytics, AI accelerators, and industry clouds to defend average revenue per account. Financial services and healthcare entities are piloting sovereign-cloud models that keep encryption keys under domestic control, a pattern likely to extend to oil and gas workloads by 2027.

National AI Strategy 2031 Accelerating Enterprise AI Adoption

The AED 335 billion (USD 91.2 billion) economic target under the AI Strategy is spurring BFSI chatbots, healthcare diagnostics, and smart-city analytics. GPU scarcity inside UAE regions, however, constrains model-training capacity, prompting demand for edge AI servers and on-device inference. Government ethics frameworks now require vendors to document datasets, bias-mitigation steps, and audit logs, adding compliance overhead yet differentiating the UAE ICT market as a regulated AI environment attractive to multinational corporates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security Talent Shortage and Rising Attack Frequency | -1.4% | National, acute in cybersecurity and cloud-engineering roles | Short term (≤ 2 years) |

| High Expatriate Turnover Inflating OPEX | -1.1% | National, IT services and consulting segments | Medium term (2-4 years) |

| Tougher Data-Sovereignty Penalties Under Draft PDPL | -0.8% | National, higher impact on multinationals | Medium term (2-4 years) |

| SME ICT Budgets Diverted to Sovereign Mega-Projects | -0.7% | National, spillover in retail, hospitality, education | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Talent Shortage and Rising Attack Frequency

Demand for certified security professionals outstrips supply by roughly 30%, elevating wage pressure and driving enterprises toward managed security services.[2]Telecommunications and Digital Government Regulatory Authority, “UAE Telecommunications Infrastructure Report 2025,” tdra.gov.ae Mandatory 24/7 monitoring for critical infrastructure adds cost layers that can exceed AED 1 million (USD 272,000) annually for mid-sized firms. Vendors now pitch outcome-based contracts that guarantee detection and response metrics, transferring risk away from customers but concentrating market power among global providers with deep threat-intelligence feeds.

High Expatriate Turnover Inflating OPEX

Annual churn above 20% among expatriate IT workers raises recruitment and knowledge-transfer costs by up to 25% per project. Firms respond with offshore delivery centers and Emiratization initiatives, yet these tactics introduce latency and prolonged ramp-up schedules. Vendors offering workforce-stability perks such as family relocation support and structured career paths gain an edge in multi-year managed-service bids, especially within the UAE ICT market segments that demand on-site presence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cybersecurity Pulls Ahead of Services

IT services accounted for 32.73% of the UAE ICT market in 2025, spanning consulting, implementation, and managed operations. In parallel, cybersecurity revenue is expanding at an 11.11% CAGR, outpacing the overall UAE ICT market by nearly one percentage point. Cloud security, identity and access management, and zero-trust networking dominate budget allocations as critical-infrastructure operators harden defenses against escalating ransomware threats. Hardware sales moderate amid cloud migration, yet AI-optimized servers and edge gateways offer new lanes for equipment vendors.

Unified security platforms are eclipsing point solutions as enterprises seek operational simplicity and integrated analytics. Palo Alto Networks’ Prisma and Fortinet’s Security Fabric exemplify bundle strategies that embed endpoint, cloud, and network defenses in one pane of glass. Regulatory frameworks mandate quarterly vulnerability assessments, reinforcing a compliance-driven buying cycle that favors vendors with in-country security operations centers. The result is a reshaped supplier hierarchy in which platform breadth, rather than niche-feature depth, determines wallet share in the UAE ICT market.

By Enterprise Size: SMEs Narrow the Digital Gap

Large enterprises accounted for 62.84% of the UAE ICT market in 2025, driven by hybrid-cloud blueprints and complex integration needs. Yet SMEs are slated for a 12.04% CAGR as government subsidies and cloud-native software dismantle cost barriers. Tax-compliance deadlines under the 9% corporate levy accelerate ERP rollouts, pushing adoption of Microsoft Business Central, Oracle NetSuite, and SAP Business One.

SMEs favor standardized SaaS stacks that bundle productivity, accounting, and CRM, while large enterprises negotiate bespoke integrations across multi-cloud estates. Khalifa Fund grants that reimburse up to 50% of cloud subscriptions reduce capital strain for smaller firms. This bifurcation produces a two-tier channel model: global integrators court large-enterprise transformation programs, whereas local resellers and ISVs service SMEs through marketplace portals, broadening access to the UAE ICT market without inflating sales overhead.

By End-User Industry Vertical: Healthcare Moves Fastest

BFSI sustained a 22.74% share of 2025 spending, but healthcare posts the swiftest trajectory at an 11.46% CAGR through 2031. Unified electronic health record mandates and AI-enabled diagnostics catalyze new procurement cycles among hospitals and clinics.[3]Ministry of Health and Prevention, “Digital Health Initiatives,” mohap.gov.ae Government and public-sector bodies remain pivotal, exemplified by Abu Dhabi’s AED 13 billion (USD 3.54 billion) cloud migration program.

Oil and gas deploy edge analytics and digital twins to curb downtime, while retail and logistics invest in omnichannel platforms and warehouse automation. Education and hospitality add incremental volumes through e-learning and contactless guest systems. Across every vertical, compliance with data-residency rules and zero-trust guidelines anchors technology evaluation, guiding supplier selection within the UAE ICT market.

By Deployment Model: Cloud and Hybrid Gain Dominance

Cloud models captured 46.83% of the UAE ICT market share in 2025 and will grow at an 11.78% CAGR, powered by local hyperscaler regions and sovereign-cloud certifications. Hybrid architectures earn the fastest sub-segment growth as highly regulated workloads balance latency, sovereignty, and cost considerations.

Hardware vendors pivot to as-a-service models, and software publishers shift from perpetual licenses to subscriptions, improving revenue visibility but requiring higher customer success spend. Systems integrators expand assessment-to-runway services that span migration, optimization, and managed operations, unlocking recurring fees that outlast one-time implementation revenue. Multi-cloud orchestration skills evolve into table stakes for capturing large transformation mandates across the UAE ICT market.

Geography Analysis

The UAE ICT market spending concentrates in Abu Dhabi, Dubai, and Sharjah, which together contribute more than 85% of enterprise outlays. Abu Dhabi’s AED 13 billion (USD 3.54 billion) digital-infrastructure budget from 2025 to 2027 underpins sovereign-cloud clustering and public-sector workload migrations. Dubai remains the fintech and smart-city nerve center, with its AI Blueprint targeting AED 100 billion (USD 27.23 billion) yearly value creation. Sharjah and the northern emirates emerge as manufacturing and logistics digitization corridors, yet must backhaul traffic to southern data-center hubs, introducing latency premiums.

Cross-emirate initiatives such as UAE Pass and the federal e-procurement portal harmonize standards, enabling solution scalability across jurisdictions. Nonetheless, overlapping data-protection regimes at Dubai International Financial Centre and Abu Dhabi Global Market oblige multinationals to juggle nuanced compliance matrices. Vendors with dual-office footprints in Abu Dhabi and Dubai secure bid advantages through local support capacity, while cloud-native ISVs target under-served SMEs in northern emirates.

Latency asymmetry emphasizes the importance of edge nodes and content-delivery clusters outside the two primary hyperscaler corridors. The UAE ICT market therefore presents a geographic white space in which regional data-hubs and managed-edge platforms can differentiate on proximity, especially for real-time analytics in manufacturing and logistics.

Competitive Landscape

The UAE ICT market is moderately concentrated. Etisalat by e&, du, Microsoft, AWS, Oracle, and IBM jointly account for roughly 35-40% of total spending. Telecom incumbents are repackaging connectivity, cloud, IoT, and security into integrated solutions to mitigate over-the-top erosion. Hyperscalers compete on in-country regions, multi-region redundancy, and compliance badges, with Oracle’s USD 1.5 billion Abu Dhabi expansion illustrating the escalating capital bar.

Global systems integrators such as Accenture and Tata Consultancy Services leverage vertical accelerators and outcome-based pricing to secure government mega-projects. Local champion Injazat capitalizes on sovereign data centers and Emirati talent programs to anchor public-sector contracts. Cybersecurity specialists Palo Alto Networks and Fortinet ride zero-trust mandates but face price compression as buyers gravitate to platform bundles. Niche players like Digital 14 carve space in sovereign-cloud security tailored to Gulf risk profiles, underscoring that regional context and compliance acumen increasingly trump global scale.

Edge computing, AI infrastructure tuned for data-sovereignty constraints, and vertical SaaS for healthcare, education, and hospitality remain nascent. Vendors investing in domestic R&D, Emirati workforce development, and long-term partnerships with regulators obtain preferential consideration under economic-diversification and Emiratization policies, tightening the loop between public-policy objectives and private-sector success within the UAE ICT market.

UAE ICT Industry Leaders

e& (Etisalat Group)

Emirates Integrated Telecommunications Company PJSC (du)

Microsoft Corporation

Amazon Web Services, Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The UAE government launched the 6G Initiative targeting speeds 500 times faster than 5G, positioning the country as a wireless testbed.

- October 2025: Microsoft expanded its Azure footprint with new availability zones in Abu Dhabi for enhanced disaster-recovery architectures.

- September 2025: Abu Dhabi agencies completed migration of more than 60% of digital services to cloud, exceeding interim targets.

- August 2025: Oracle’s second UAE cloud region entered service, delivering multi-region redundancy inside national borders.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the UAE ICT market as all spending within the country on IT hardware, software, infrastructure, managed and professional IT services, cybersecurity solutions, and fixed-plus-mobile communication services purchased by enterprises and public agencies. Consumer electronics, media content, and pure connectivity ARPU are excluded.

Scope Exclusion: handset retail sales are deliberately left outside the baseline so the model focuses on enterprise-led digital transformation.

Segmentation Overview

- By Product Type

- IT Hardware

- Computer Hardware

- Networking Equipment

- Peripherals

- IT Software

- IT Services

- IT Consulting and Implementation

- IT Outsourcing (ITO)

- Business Process Outsourcing (BPO)

- Managed Security Services

- Cloud and Platform Services

- IT Infrastructure

- IT Security / Cybersecurity

- Application Security

- Cloud Security

- Data Security

- Network Security

- Endpoint Security

- Infrastructure Protection

- Integrated Risk Management

- Identity and Access Management (IAM)

- Communication Services

- IT Hardware

- By Enterprise Size

- Small and Medium-sized Enterprises

- Large Enterprises

- By End-user Industry Vertical

- BFSI

- Government and Public Sector

- Oil and Gas

- IT and Telecom

- Retail, E-commerce and Consumers

- Manufacturing and Industrial

- Energy and Utilities

- Healthcare

- Other End-user Industry Verticals (Transportation, Logistics, Education, Hospitality)

- By Deployment Model

- On-premise

- Cloud

- Hybrid

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with CIOs of utilities, banks, and government entities in Dubai and Abu Dhabi, alongside regional system integrators and carrier product heads. These discussions clarified cloud migration rates, average service-level prices, and the pace at which SMEs adopt cybersecurity bundles, tightening the assumptions drawn from the desk work.

Desk Research

We first reviewed quantitative datasets from bodies such as the UAE Federal Competitiveness & Statistics Center, the Telecommunications and Digital Government Regulatory Authority, the International Telecommunication Union, and UN Comtrade, which reveal hardware imports, data-center capacity additions, spectrum fees, and broadband adoption. Company filings, government budget papers, and reputable dailies complement these statistics with contract values and policy timelines.

Subscription databases, including D&B Hoovers for vendor revenue splits and Dow Jones Factiva for deal flow, give our analysts historic benchmarks and price points. These illustrative sources are not exhaustive; several additional open records were mined to validate volumes, values, and growth signals.

Market-Sizing & Forecasting

A top-down reconstruction links national ICT expenditure lines from budget and trade data to enterprise demand pools, followed by selective bottom-up supplier roll-ups that test the totals. Key variables like data-center white-space builds, 5G subscriber penetration, average managed-service contract value, import duties on networking gear, and public-cloud price declines drive year-on-year adjustments. Forecasts employ multivariate regression with scenario checks that our primary respondents vet; gaps in vendor billing estimates are bridged by channel checks and sampled ASP × volume proxies.

Data Validation & Update Cycle

Model outputs pass three layers of analyst review where abnormal year swings are compared with macro indicators and sector KPIs. Reports refresh every twelve months, and material policy or capex announcements trigger interim updates so clients receive the latest vetted view before download.

Why Mordor's UAE ICT Baseline Earns Executive Trust

Published figures often differ because firms select dissimilar service baskets, convert currencies at varied dates, and refresh models on uneven cadences.

Key gap drivers include contrasting inclusion of cybersecurity and cloud services, varying treatment of telecom capex versus opex, and differing base years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 52.23 B (2025) | Mordor Intelligence | |

| USD 41.36 B (2023) | Regional Consultancy A | Omits security services and public-cloud spend, older currency baseline |

| USD 43.93 B (2025) | Industry Journal B | Double counts telecom capex and folds consumer electronics into ICT totals |

The comparison shows that when the right scope, timely exchange rates, and dual-path validation are used, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the forecast value of the UAE ICT market by 2031?

The market is projected to reach USD 94.02 billion by 2031.

Which segment is growing fastest within UAE ICT spending?

Cybersecurity leads with an 11.11% CAGR through 2031.

How large is cloud deployment in the UAE ICT market?

Cloud models already capture 46.83% of spending and are rising at an 11.78% CAGR.

Why are SMEs accelerating ICT investment in the UAE?

Corporate-tax compliance and subsidized cloud programs are driving a 12.04% CAGR for SME ICT outlays.

What geographic areas dominate ICT spending in the UAE?

Abu Dhabi and Dubai together account for more than 85% of enterprise ICT expenditure.

Which constraint most threatens UAE ICT growth?

A 30% shortfall in certified cybersecurity professionals is the single biggest drag on near-term expansion.

Page last updated on: