United Arab Emirates Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

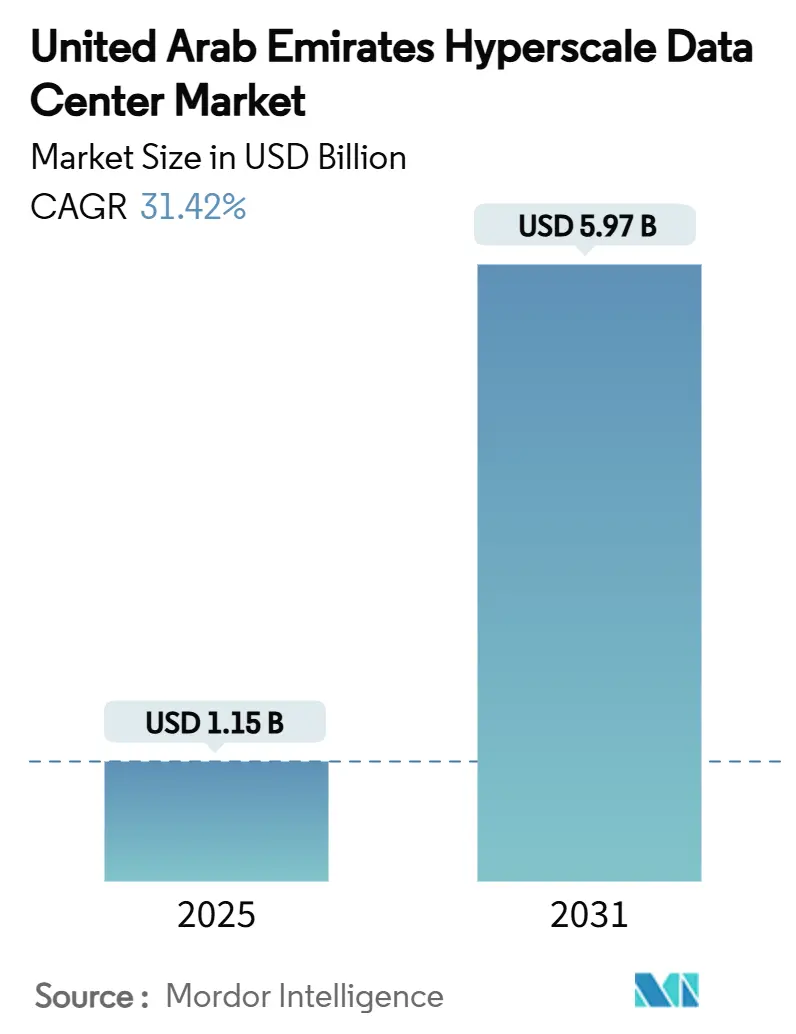

| Market Size (2025) | USD 1.15 Billion |

| Market Size (2031) | USD 5.97 Billion |

| Growth Rate (2025 - 2031) | 31.42% CAGR |

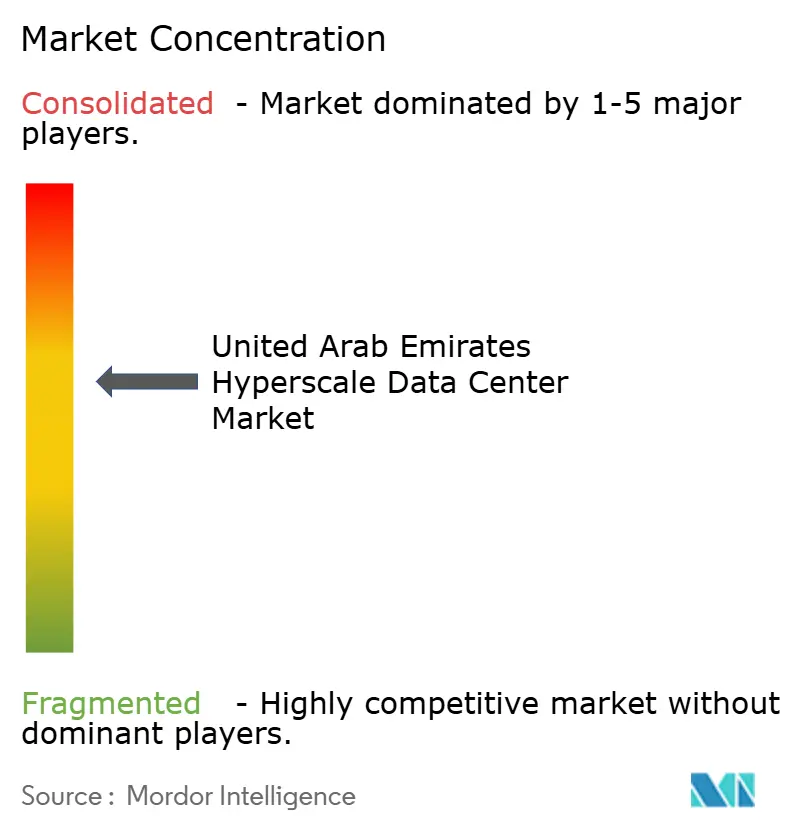

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Hyperscale Data Center Market Analysis by Mordor Intelligence

The United Arab Emirates hyperscale data center market size stood at USD 1.15 billion in 2025 and is forecast to reach USD 5.97 billion by 2031, reflecting a powerful 31.42% CAGR. Accelerated sovereign-cloud mandates, surging artificial-intelligence workloads and competitive renewable-power tariffs are jointly positioning the United Arab Emirates hyperscale data center market as the Middle East’s primary AI infrastructure hub. Power demand is projected to jump from 597.0 MW in 2025 to 1,507.9 MW by 2031, underpinned by rack densities surpassing 100 kW and rapid adoption of liquid-cooling architectures. Government capital commitments exceeding AED 13 billion, strategic alliances such as Microsoft–G42 and a pipeline of nuclear and solar generation projects are further broadening the addressable opportunity. At the same time, workforce shortages and water-use constraints are forcing operators to deploy automation, heat-recovery and non-potable-water systems to preserve margins and meet sustainability targets. Competitive intensity is escalating as international cloud providers shift from hub-and-spoke Gulf models to dedicated Emirates regions, reshaping price–performance dynamics across the United Arab Emirates hyperscale data center market.

Key Report Takeaways

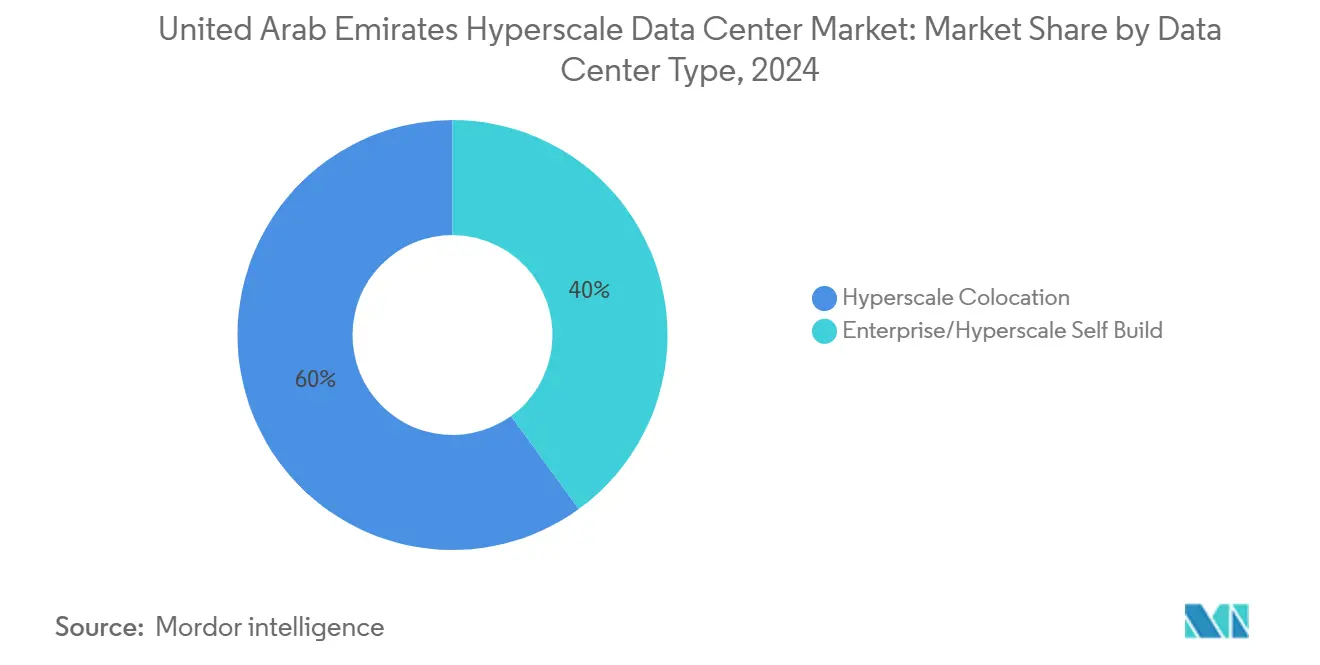

- By data center type, hyperscale colocation led with 60% of the United Arab Emirates hyperscale data center market share in 2024, while hyperscaler self-build deployments are advancing at a 31.6% CAGR through 2030.

- By component, IT infrastructure commanded a 41% share of the United Arab Emirates hyperscale data center market size in 2024, with liquid-cooling systems expanding at a 32.6% CAGR to 2030.

- By tier standard, Tier IV facilities are projected to record the highest growth at a 31.8% CAGR to 2030, although Tier III maintains a 71% share of the 2024 United Arab Emirates hyperscale data center market size.

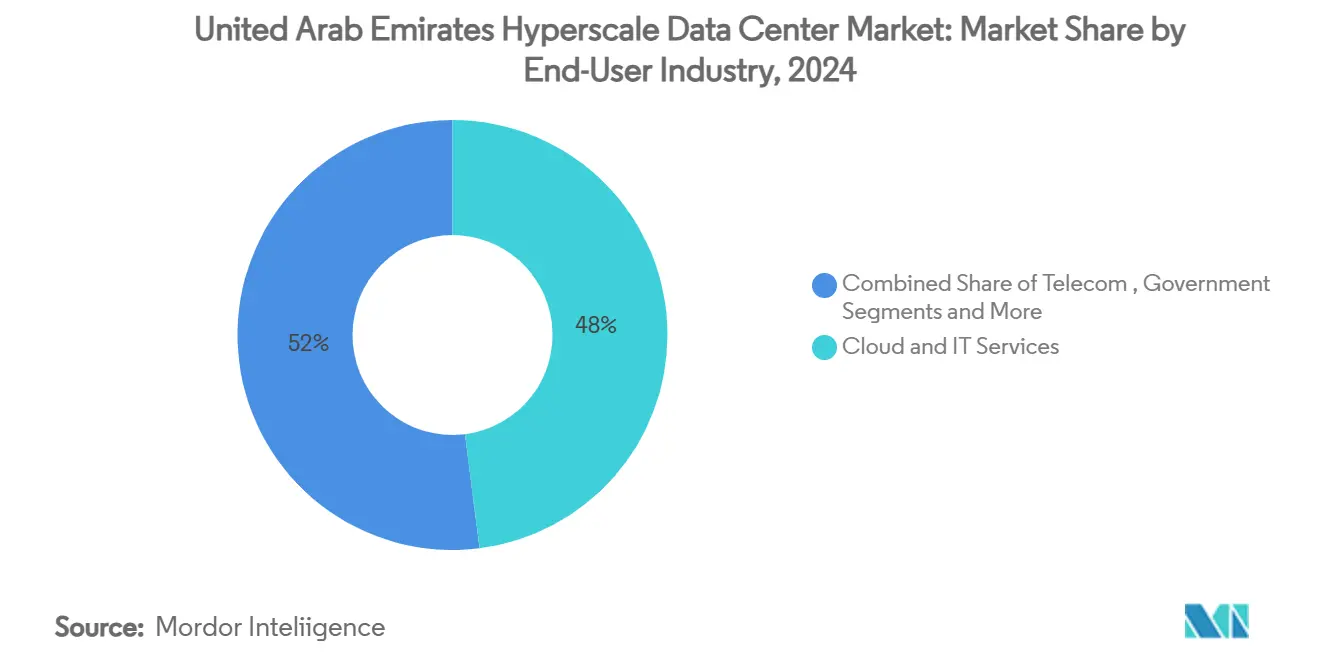

- By end-user industry, cloud and IT services retained a 48% share of the United Arab Emirates hyperscale data center market size in 2024; AI cloud providers are on course for a 32.4% CAGR growth to 2030.

- By data center size, mega facilities are expanding fastest at a 33.1% CAGR, even as massive facilities held 44% of the United Arab Emirates hyperscale data center market size in 2024.

United Arab Emirates Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sovereign-cloud mandates under UAE Digital Government Policy | +8.2% | National, heightened in Abu Dhabi | Medium term (2-4 years) |

| AI/ML rack densities in public and BFSI workloads | +7.8% | National hub for regional AI | Short term (≤2 years) |

| Data-localization rules in DIFC / ADGM | +5.4% | Dubai and Abu Dhabi financial zones | Medium term (2-4 years) |

| Competitive green-energy tariffs via EWEC / DEWA PPAs | +4.1% | Dubai and Abu Dhabi | Long term (≥4 years) |

| District-cooling heat-reuse agreements | +3.2% | Urban centers | Medium term (2-4 years) |

| Barakah SMR pilot blocks for campuses | +2.8% | National, pilot in Abu Dhabi | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Sovereign-Cloud Mandates Under UAE Digital Government Policy

Government entities now require local processing of sensitive workloads, pushing hyperscalers to launch dedicated Emirates regions instead of serving customers from neighboring hubs. Abu Dhabi has budgeted AED 13 billion to become the first fully AI-native public administration by 2027, driving demand for high-density GPU clusters and specialized liquid-cooling systems.[1]Technology Magazine Staff, “Abu Dhabi, Microsoft, G42 Forge Sovereign Cloud Deal,” technologymagazine.com The policy accelerates capacity build-outs because compliance covers both data residency and AI model training, effectively locking in the United Arab Emirates hyperscale data center market for the medium term. International operators are transferring know-how to local partners as illustrated by the Microsoft–G42 sovereign region collaboration, deepening the strategic value chain.

AI/ML Rack Densities Exceeding 100 kW in Public and BFSI Workloads

GPU-rich clusters supporting natural-language inference and fraud-detection algorithms require per-rack power five to ten times higher than legacy enterprise cabinets. Khazna’s 100 MW Ajman campus is optimised for >100 kW racks and employs direct-to-chip cooling to maintain 1.25 PUE targets.[2]G42 Press Office, “Khazna Announces UAE’s First AI-Optimised Data Center,” g42.aiBFSI adoption of AI has likewise accelerated: Emirates NBD’s USD 270 million transformation shifted 1,000+ containerised apps onto private cloud, underscoring hyperscale demand. These workloads compel operators to redesign floorplans, busways and aisle containment, sustaining premium pricing within the United Arab Emirates hyperscale data center market.

Data-Localisation Rules in DIFC / ADGM Boosting In-Country Builds

Strict directives stipulate that finance, health and public data remain onshore, deterring cross-border replication. Multinationals must therefore contract capacity inside Dubai or Abu Dhabi zones, effectively guaranteeing baseline utilisation for new halls. Clifford Chance notes that non-compliance carries civil fines and licence suspension, elevating the risk calculus for foreign cloud-only strategies.[3]Clifford Chance LLP, “Data Transfers in the UAE and the KSA,” cliffordchance.com Regulatory complexity favours incumbents who already field compliance officers, giving the United Arab Emirates hyperscale data center market a protective moat against oversupply.

District-Cooling Heat-Reuse Agreements Enabling Downtown Sites

Municipal district-cooling enables operators to offload waste heat into city networks, freeing valuable urban real estate where conventional chillers would breach noise or emission limits. In Dubai’s Business Bay, heat-reuse trials have allowed 25 MW of incremental capacity without additional substation permits, proving a template for future urban densification. Energy integration projects shorten delivery schedules and give operators near-zero water-use options, matching long-term ESG targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Uptime-accredited O and M workforce inflating labour cost | -4.7% | UAE National, acute in Abu Dhabi and Dubai | Short term (≤ 2 years) |

| Limited freshwater supply curbing evaporative cooling adoption | -3.8% | UAE National, critical in Northern Emirates | Medium term (2-4 years) |

| Airport drone-corridor height limits delaying metro builds | -2.9% | Dubai and Abu Dhabi, proximity to international airports | Medium term (2-4 years) |

| Fibre-landing licence caps restricting new hyperscale entrants | -2.1% | UAE National, concentrated in Dubai and Abu Dhabi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Uptime-Accredited Operations and Maintenance Workforce

The United Arab Emirates hyperscale data center market is adding hundreds of megawatts per year, yet only a few dozen engineers graduate annually with Tier III/IV credentials. Uptime Institute reports starting salaries for accredited technicians in the Gulf have climbed 40% since 2023, compressing EBITDA margins. Operators now co-fund vocational academies and automate routine maintenance to de-risk staffing bottlenecks. International hyperscalers require dual security clearance plus liquid-cooling expertise, making recruitment cycles longer than build cycles and occasionally delaying hall energisation.

Limited Freshwater Supply Curbing Evaporative Cooling Adoption

Evaporative or adiabatic coolers offer low energy intensity but can consume 5-8 litres/kWh, conflicting with the state’s water conservation priorities. MDPI case studies show that condensing-unit retrofits in Dubai saved 25% electricity yet tripled water demand, driving regulators to cap make-up water allocations. Consequently, hyperscale operators are pivoting to closed-loop liquid-immersion and district-cooling hybrids, even at higher capex. Non-potable-water reuse remains under-regulated, injecting planning risk into Northern Emirates projects where desalination infrastructure is modest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: From Colocation Dominance to Self-Build Expansion

Colocation providers supplied 60% of 2024 installed IT load within the United Arab Emirates hyperscale data center market, leveraging mature carrier-hotels and modular hall designs that suited early cloud arrival. The segment benefited from tenant diversity and rapid onboarding, translating into average rack utilisation above 80%. Yet hyperscaler self-build projects are scaling at 31.6% CAGR and are expected to overtake colocation by value before 2030 as AI workloads require bespoke power busways, liquid manifolds and sovereign-control zones. Microsoft’s AED 2 billion self-build in Jebel Ali exemplifies this pivot, incorporating dual 100 MVA feeders and 35 MW of lithium-ion UPS blocks. The United Arab Emirates hyperscale data center market size for hyperscaler self-build facilities is projected to add more than USD 3 billion between 2025-2031, transforming developer-tenant relationships while crowding-out generic multi-tenant designs.

Self-build economics hinge on greater capex but lower long-run TCO, with energy contracts aligned directly to hyperscaler risk absorptions. Local partners such as du and Khazna provide land, permits and dark-fibre loops, shortening time-to-market from 24 months to roughly 14 months. Colocation incumbents are reacting by creating AI-ready suites with 90 kW liquid-ready racks and variable PUE targets, preserving relevance for regulated BFSI and enterprise spill-over workloads. Talent sharing agreements and build-operate-transfer models are also emerging, allowing colocation operators to capture development fees while transferring day-two risk back to hyperscalers.

By Component: Liquid-Cooling Systems Redefine Infrastructure Mix

IT infrastructure accounted for 41% of aggregate 2024 spend in the United Arab Emirates hyperscale data center market, covering high-bandwidth memory GPUs, NVMe fabrics and cloud-native storage arrays. However, liquid-cooling systems are pacing the fastest expansion at 32.6% CAGR. Cold-plate loops, rear-door heat exchangers and full immersion tanks are now standard in new AI halls, permitting densities above 100 kW while limiting PUE drift. The United Arab Emirates hyperscale data center market size for liquid-cooling hardware is forecast to exceed USD 600 million by 2030, outstripping mechanical chillers and CRAC units combined.

Electrical infrastructure is simultaneously evolving: 415 V busways are giving way to 240 V DC micro-grids and static bypass switchgear optimised for fast AI burst cycles. Operators budget nearly USD 150 million per 100 MW block for redundant transformers, generator farms and STATCOM stabilisers. Mechanical infrastructure still captures 25-30% of capex, yet the share is shifting from commodity chillers to bespoke CDU skids and dielectric-fluid purification plants. Meanwhile, general construction costs are rising on account of taller clear-heights, slab thickening and seismic bracing needed to support immersion tanks.

By Tier Standard: Mission-Critical AI Accelerates Tier IV Adoption

Tier III halls provide fault-tolerant N+1 redundancy and dominated 71% of 2024 build stock, aligning with enterprise cost-sensitivity. Nonetheless, Tier IV deployments—offering concurrently maintainable 2N architecture—are scaling at 31.8% CAGR, reflective of the United Arab Emirates hyperscale data center market emphasis on AI research, digital-banking and governmental e-services. Abu Dhabi Municipality’s Tier IV certified recovery site registered zero downtime during the 2024 summer grid-events, reinforcing ROI narratives. United Arab Emirates hyperscale data center market size for Tier IV capacity is projected to approach USD 2.3 billion by 2030, representing roughly one-third of aggregate investment.

Achieving Tier IV in the desert involves triple-fed utility substations plus independent solar or SMR micro-grids, boosting construction lead time but unlocking preferred-supplier accords with hyperscalers that price downtime at over USD 10 million/hour. Tier III will remain relevant for test, development and non-critical log aggregation, yet premium AI training clusters, trading platforms and sovereign workloads will gravitate to Tier IV or Tier IV-equivalent frameworks.

By End-User Industry: AI Cloud Providers Reshape Demand Patterns

Cloud and IT services retained 48% of 2024 demand, reflecting continued lift-and-shift migrations. However, AI cloud providers—entities whose primary revenue stems from model-as-a-service offerings—are expanding fastest at 32.4% CAGR. The United Arab Emirates hyperscale data center market size attributable to AI platforms is on course to eclipse USD 2 billion by 2030 as organisations outsource multimodal model training. OpenAI’s five-gigawatt Stargate cluster underscores the magnitude of single-tenant AI campuses now anchoring Emirates infrastructure strategy.

Government projects form the second fastest-growing vertical, propelled by smart-city and defence analytics. BFSI demand remains solid: payment-switch latency and algorithmic trading are driving 50 μs round-trip benchmarks. Telecom operators invest in MEC (multi-access edge compute) to monetise 5G, while manufacturing and e-commerce verticals accelerate IoT analytics and last-mile logistics optimisation. Combined, these create a granular utilisation profile, blending constant baseline workloads with high-burst AI inference peaks that favour elastic campus designs.

By Data Center Size: Mega Facilities Power Scale Economics

Massive facilities commanded 44% of load in 2024, offering economies of scale without outsized grid impact. Yet mega campuses above 60 MW are growing at 33.1% CAGR and will account for more than half of cumulative United Arab Emirates hyperscale data center market size additions by 2031. Stargate UAE’s 1 GW phase-one anchor and Vantage’s 100 MW announcements epitomise the scale shift. Mega designs centralised chillers, pumps, and transformers, yielding up to 12% capex savings per kW. They also unlock direct nuclear or solar farm interconnects, locking in <0.02 USD/kWh tariffs on 20-year PPAs.

However, mega projects introduce concentration risk; failure modes scale proportionally. Risk mitigation now includes on-site 200 MWh battery arrays and sectionalised busbars that isolate faults to 20 MW blocks. Smaller large sites (≤25 MW) still appeal for edge latency and staging, serving Dubai’s finance district and media corridors. Developers increasingly employ hub-and-edge topology where mega campuses in Abu Dhabi backhaul cognitive workloads, and satellite pods in Dubai handle latency-sensitive traffic.

Geography Analysis

The UAE hyperscale data center market exhibits moderate consolidation with intense competition among established international operators and emerging local players leveraging government partnerships and regional expertise. Market leadership is distributed among hyperscalers pursuing self-build strategies, established colocation providers expanding regional presence, and local operators with strategic government relationships. G42's merger with Etisalat to form Khazna Data Centers, creating the UAE's largest data center provider with 300 MW capacity, demonstrates how local consolidation is reshaping competitive dynamics. The competitive intensity has escalated with international operators establishing dedicated UAE regions rather than serving the market from neighboring countries, driven by data localization requirements and sovereign cloud mandates that favor local infrastructure.

White-space opportunities are emerging in specialized AI infrastructure, edge computing deployments, and sustainable data center technologies that leverage the UAE's renewable energy advantages. Chinese cloud providers, including Alibaba and Huawei, are gaining market share through competitive pricing and strategic partnerships with regional telecommunications operators, challenging established Western hyperscalers' dominance. Technology differentiation is increasingly focused on cooling efficiency, power utilization effectiveness, and AI-optimized infrastructure configurations, with operators investing in liquid cooling systems and advanced power distribution to support high-density workloads. The competitive landscape is being reshaped by massive capital commitments, with Vantage Data Centers securing USD 13 billion in funding for global expansion and Digital Realty sourcing over USD 12 billion in capital commitments from hyperscale partners, indicating the scale of investment required to compete effectively in the evolving market.

Competitive Landscape

Khazna Data Centers leads the UAE hyperscale data center market with 45.8% revenue share and the broadest project pipeline. Its early adoption of 100% renewable PPAs gives tenants price certainty and helps international firms satisfy ESG mandates. Global hyperscalers—AWS, Microsoft, Oracle, and Google Cloud—blend self-built campuses with long-term colocation blocks, ensuring rapid scaling while retaining control over proprietary chipsets and networking fabrics.

Investment activity accelerated in 2025 when KKR committed USD 5 billion to Gulf Data Hub, signaling deep private-equity confidence. Infrastructure funds target yields above 11% by underwriting liquid-cooling retrofits that lift per-rack densities without expanding real estate footprints. e& leverages its carrier network to bundle submarine access, cross-connects, and managed security around its Fujairah campus, targeting media publishers that value one-stop-shop solutions.

Technology differentiation focuses on thermal management. Partners such as Intel and Johnson Controls prototype immersion baths that use biodegradable dielectric fluids, reducing water consumption by 80% and trimming electricity bills. Operators that can certify facility PUE below 1.2 secure premium pricing. Sovereign-cloud variants of popular hyperscale services also proliferate; ADGM compliance packages now include data-loss-prevention templates tuned to local regulations. Against this backdrop, white-space opportunities persist in edge nodes for autonomous-vehicle telemetry, 5G open-RAN testbeds, and secure enclaves for quantum-safe encryption keys.

United Arab Emirates Hyperscale Data Center Industry Leaders

Khazna Data Centers

Equinix Inc.

Amazon Web Services

Microsoft Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: OpenAI partnered with UAE authorities to develop a 5 GW AI campus in Abu Dhabi, slated for 1 GW first-phase completion in 2026.

- April 2025: Du and Microsoft signed an AED 2 billion hyperscale data center agreement to anchor Dubai’s sovereign AI region

- March 2025: ADQ teamed with Energy Capital Partners, allocating over USD 25 billion toward power projects dedicated to data-center growth.

- February 2025: Khazna launched construction of a 100 MW AI-optimised site in Ajman, targeting handover in Q3 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Arab Emirates hyperscale data center market as the annual revenue that operators earn from facilities engineered to support cloud-scale loads above 25 MW, built with fully redundant electrical paths, software-defined automation, and expansion blocks repeatable across multiple halls. Capacity additions measured in megawatts of critical IT load are converted to revenue using prevailing wholesale colocation price bands, then summed with self-build service income.

Scope exclusion: Enterprise server rooms, edge micro sites below 1 MW, and non-compute telecom shelters remain outside this assessment.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Unit

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning Services

- Design and Engineering

- Fire/Security Systems

- DCIM / BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT Services

- Telecom

- Government

- BFSI

- Media and Entertainment

- Manufacturing

- E-Commerce

- Other End Users

- By Data Center Size

- Large (Less than equal to 25 MW)

- Massive (Greater than 25 MW and less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Desk Research

Analysts compiled foundational metrics from open sources such as the UAE Federal Competitiveness & Statistics Center, the Telecommunications & Digital Government Regulatory Authority, Dubai Electricity & Water Authority tariff filings, and Uptime Institute certification logs, which together clarify demand drivers, power pricing, and tier adoption. Complementary insights were drawn from central bank payment data, Emirates Customs shipment records for IT hardware, and investor presentations disclosed on ADX. Paid intelligence from D&B Hoovers and Dow Jones Factiva enriched company-level revenue splits and project pipelines. These sources, while pivotal, are illustrative; many additional public and subscriber materials supported data gathering, sense-checking, and clarification.

Primary Research

We interviewed regional facility operators, utility planners, hyperscale cloud architects, and specialist contractors spanning Abu Dhabi, Dubai, and Sharjah. Their feedback validated load-growth assumptions, typical lease-up periods, liquid-cooling adoption timelines, and forecast rack densities, thereby filling information gaps left by published statistics.

Market-Sizing & Forecasting

A top-down build transforms national power-demand projections into a hyperscale-only revenue pool by applying penetration rates for large-block leasing and self-build share; selective bottom-up cross-checks (sampled average selling price × commissioned MW) temper the totals. Key variables include new utility-grade substation approvals, land-bank absorption, average 42 kW rack density progression, PPA electricity tariffs, and AI-related GPU deployment ratios. Forecasts through 2031 rely on multivariate regression that links those drivers to annual commissioned megawatts, with coefficients fine-tuned through primary-expert consensus. Data gaps in supplier roll-ups are bridged using conservative midpoint estimates that are subsequently validated against historical variance bands.

Data Validation & Update Cycle

Outputs pass three-layer reviews: automated outlier scans, peer comparison against independent capacity trackers, and senior-analyst sign-off. Models refresh every twelve months, with mid-cycle updates triggered by material events such as multi-gigawatt campus announcements. A final pre-publication sweep ensures clients receive the latest view.

Why Our United Arab Emirates Hyperscale Data Center Baseline Stands Apart

Published estimates often diverge because firms pick different facility types, revenue hooks, currency bases, and refresh cadences.

Key gap drivers here stem from whether enterprise and retail colocation halls sit inside scope, if numbers reflect installed capital versus service revenue, and how aggressively future AI rack densities are priced into forecasts. Mordor's disciplined, annually refreshed approach anchors on realized service income from >=25 MW campuses, tempered by operator-verified ASPs, which yields a balanced baseline for decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.15 B (2025) | Mordor Intelligence | - |

| USD 1.26 B (2024) | Regional Consultancy A | Includes enterprise & retail colocation; investment metric blended with service revenue |

| USD 2.65 B (2029) | Trade Journal B | Captures cumulative capital spend, not annual operator income; scope spans all facility tiers |

Taken together, the comparison shows that when scope alignment and revenue-only framing are enforced, our figure remains the most transparent and repeatable baseline, grounded in operator disclosures, validated demand markers, and a methodology clients can readily audit.

Key Questions Answered in the Report

What is the growth outlook for the United Arab Emirates hyperscale data center market?

The United Arab Emirates hyperscale data center market is forecast to expand from USD 1.16 billion in 2025 to USD 5.97 billion by 2031 at a 31.42% CAGR.

Which emirate is attracting most hyperscale investment?

Abu Dhabi is leading capacity additions, driven by the 5 GW Stargate UAE campus and strong government backing.

Why are AI workloads reshaping facility design?

AI model training requires rack densities above 100 kW, pushing operators to adopt liquid-cooling, 2N power and mega-scale campuses for efficiency.

How are sustainability goals addressed?

Operators secure long-term solar and nuclear PPAs, deploy district-cooling heat-reuse and transition to water-efficient liquid-cooling architectures.

What are the key restraints on market growth?

Shortages of Uptime-accredited engineers and limited freshwater for evaporative cooling are the main near-term challenges.

Which segments are growing fastest?

Hyperscaler self-build facilities, liquid-cooling systems and mega sites (>60 MW) each exceed 30% projected CAGR to 2030 within the United Arab Emirates hyperscale data center market.

Page last updated on: