Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

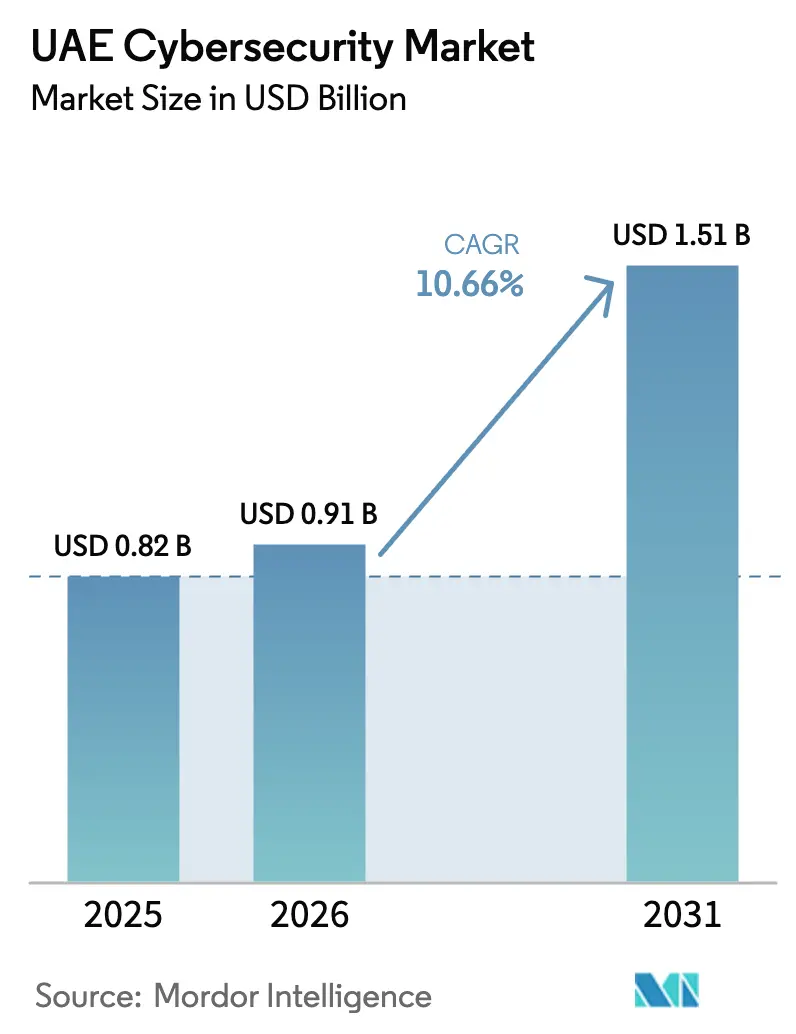

| Base Year Market Size (2025) | USD 0.82 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.51 Billion |

| Growth Rate (2026 - 2031) | 10.66% CAGR |

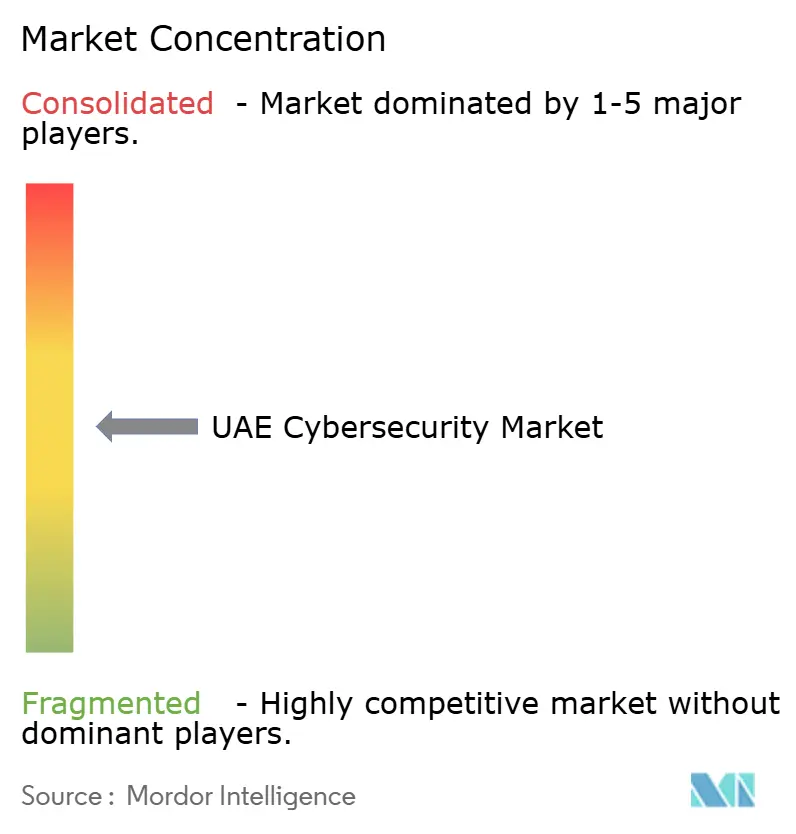

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Cybersecurity Market Analysis by Mordor Intelligence

The UAE Cybersecurity Market size was valued at USD 0.82 billion in 2025 and is estimated to grow from USD 0.91 billion in 2026 to reach USD 1.51 billion by 2031, at a CAGR of 10.66% during the forecast period (2026-2031). Heightened sovereign-data mandates, the rollout of 5G networks, and a USD 2 billion government outlay under the National Cybersecurity Strategy are accelerating procurement cycles. Domestic security operations centers are proliferating as regulators require data residency, while cloud-native architectures remain central to digital-transformation roadmaps. Vendors that can certify compliance with Version 2 of the UAE Information Assurance Standards and integrate seamlessly with hyperscale clouds are gaining ground. Competitive dynamics favor modular platforms that orchestrate endpoint, identity, and cloud-access controls on a single pane of glass, easing the skills gap that continues to strain in-house teams.

Key Report Takeaways

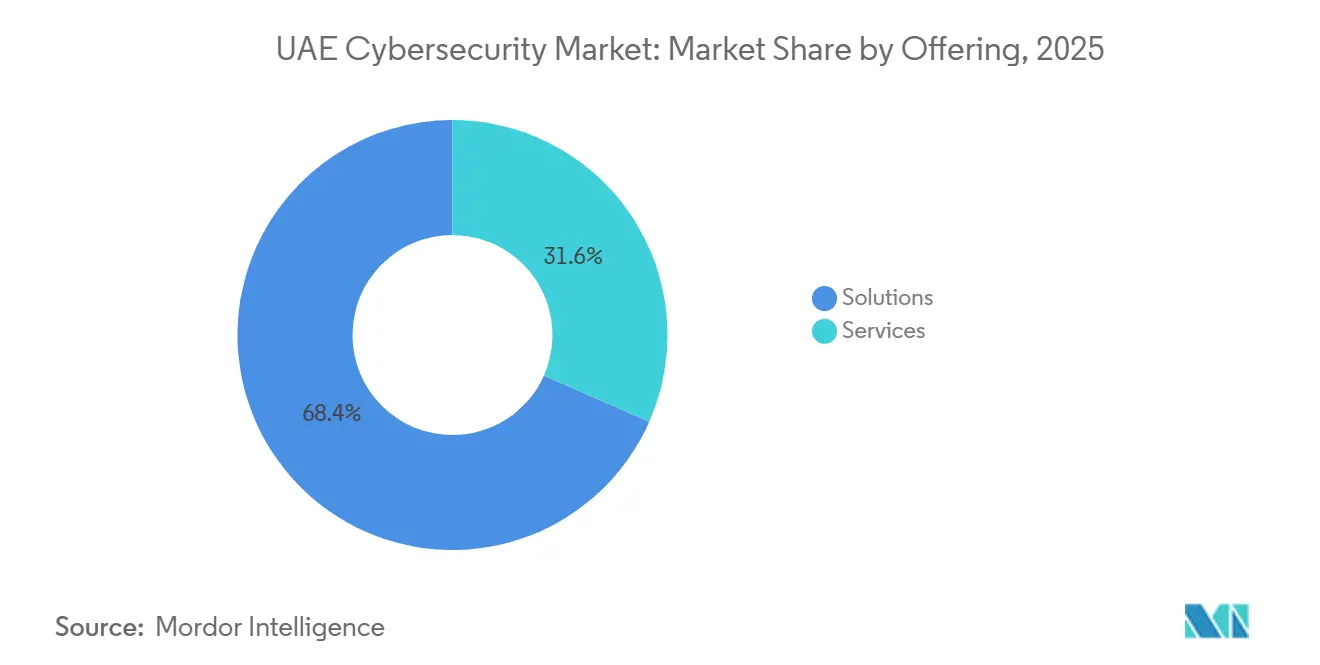

- By offering solutions, captured 68.38% of the UAE cybersecurity market revenue in 2025, whereas services are forecast to post an 11.23% CAGR through 2031, the fastest pace among offerings.

- By deployment mode, cloud deployment accounted for 63.12% of the UAE cybersecurity market share in 2025 and is advancing at an 11.16% CAGR to 2031.

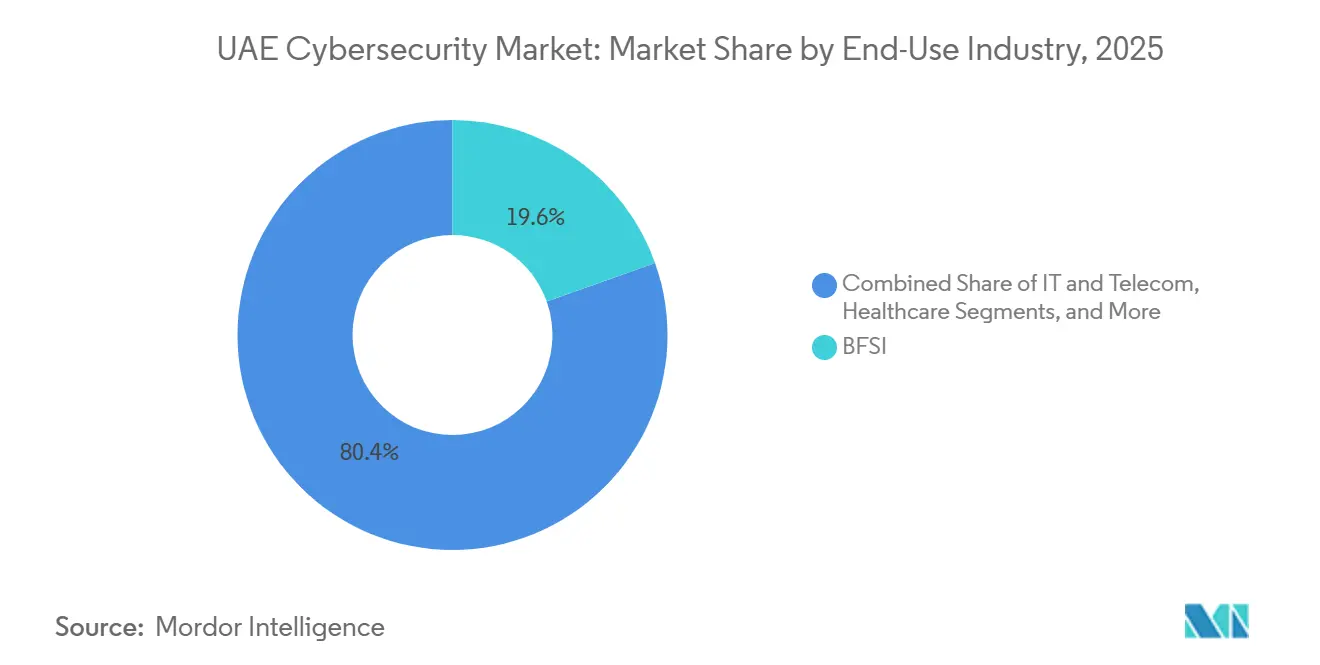

- By end-user industry, Banking, financial services, and insurance led spending, accounting for 19.56% of the UAE cybersecurity market in 2025, while healthcare is projected to grow at a 12.01% CAGR through 2031.

- By end-user enterprise size, Small and medium enterprises are expected to raise budgets at an 11.78% CAGR through 2031, narrowing the gap with large enterprises that held 67.29% of 2025 outlays.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Government Cybersecurity Spending Under UAE Vision 2031 | +2.8% | National, with concentration in Abu Dhabi and Dubai | Medium term (2-4 years) |

| Proliferation of 5G and IoT Driving Threat Surface Expansion | +2.3% | National, accelerated in smart-city zones (Dubai, Abu Dhabi, Sharjah) | Short term (≤ 2 years) |

| Mandatory Compliance With UAE Information Assurance Standards | +1.9% | National, stricter enforcement in federal entities and critical infrastructure | Medium term (2-4 years) |

| Surge in Cloud Migration Among SMEs | +1.7% | National, with higher adoption in free zones and tech hubs | Short term (≤ 2 years) |

| Growing Adoption of Cyber Insurance Among Enterprises | +0.9% | National, led by BFSI and multinational subsidiaries | Long term (≥ 4 years) |

| Initiatives to Localize Security Data Centers and SOCs | +1.1% | National, with emphasis on Abu Dhabi and Dubai sovereign zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Government Cybersecurity Spending Under UAE Vision 2031

Federal and emirate-level agencies budgeted more than USD 2 billion in 2025, financing sovereign security operations centers, workforce-development programs, and incident-response infrastructure. Mandatory migration of public workloads to IA-compliant hosting by end-2026 is compressing procurement timelines, steering contracts toward vendors with pre-certified solutions. Funds earmarked for quantum-resistant encryption, zero-trust pilots, and AI-driven anomaly detection create first-mover advantages for suppliers that co-develop reference architectures with government buyers. Regulatory linkage between ISO 27001, UAE IA conformity, and eligibility for public tenders is reinforcing security investments across non-oil sectors.

Proliferation of 5G and IoT Driving Threat Surface Expansion

Operators had deployed roughly 7,000 5G base stations by late 2025, reaching 19.4% mobile-subscriber penetration, which in turn enabled network slicing for industrial and smart-city use cases. A surge in connected sensors, drones, and wearables widened the attack surface faster than asset inventories could keep pace. Check Point counted more than 223,800 exposed UAE assets in 2024, spanning unpatched routers and industrial controllers. Vendors offering unified endpoint and IoT management, complete with behavioral analytics, are gaining traction among enterprises seeking visibility across IT and OT domains.

Mandatory Compliance With UAE Information Assurance Standards

Version 2 of the IA Standards released in 2025 tightened encryption-key management, incident-reporting deadlines, and third-party-risk assessments.[1]National Electronic Security Authority, “Information Assurance Standards Version 2,” nesa.gov.ae Critical sectors now undergo annual penetration testing by NESA-accredited providers and must localize disaster-recovery workloads within national borders, spurring hyperscale data-center build-outs by Khazna and peers. Supply-chain clauses obligate enterprises to audit software vendors, driving demand for platforms that generate software bills of materials and immutable audit trails.

Surge in Cloud Migration Among SMEs

Government cloud-first mandates pushed 80% of federal services into the cloud by 2025, establishing best practice for private-sector adoption.[2]UAE Government Digital Office, “Cloud-First Policy,” u.ae The launch of AWS and Microsoft Azure sovereign regions in 2024-2025 lowered latency to under 5 milliseconds and satisfied data-residency rules,. SMEs without in-house expertise are turning to managed-security services that bundle cloud-security-posture management and 24/7 monitoring, priced for sub-250-employee budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Emirati Cybersecurity Talent Pool | -1.4% | National, acute in specialized domains (threat intelligence, cloud security architecture) | Medium term (2-4 years) |

| High Total Cost of Ownership for Advanced Security Solutions | -1.1% | National, disproportionately affecting SMEs and micro enterprises | Short term (≤ 2 years) |

| Fragmented Regulation Across Free Zones | -0.7% | Dubai International Financial Centre, Abu Dhabi Global Market, and sector-specific free zones | Long term (≥ 4 years) |

| Limited Awareness Among Micro Enterprises | -0.5% | National, concentrated in retail, hospitality, and personal services | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Emirati Cybersecurity Talent Pool

Roughly 5,000 Emirati nationals entered private-sector cybersecurity roles during 2024-2025, yet demand for senior threat analysts still eclipses supply.[3]Ministry of Human Resources and Emiratisation, “Cybersecurity Talent Initiatives 2025,” mohre.gov.ae Salary inflation and two-year attrition cycles erode institutional knowledge, pushing organizations toward co-managed SOC models where external providers supply tier-2 and tier-3 analysts.

High Total Cost of Ownership for Advanced Security Solutions

A full security stack can consume up to 12% of an SME IT budget. Licensing that scales per user, per device, or per gigabyte, plus hardware appliances and analyst salaries, deters uptake of next-generation firewalls and XDR. Unified platforms with consumption-based pricing are easing adoption, yet many cost-sensitive businesses still view cybersecurity as a compliance checkbox.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Scale as Skills Gap Widens

Services are set to grow at an 11.23% CAGR, outpacing the overall UAE cybersecurity market, as organizations outsource threat hunting and incident response amid a persistent talent crunch. Solutions held 68.38% of revenue in 2025, reflecting investments in next-generation firewalls and endpoint detection, but operational overheads are nudging buyers toward co-managed models. The UAE cybersecurity market size for services is projected to widen as vendors like Help AG bundle Continuous Threat Exposure Management into subscription packages. Managed detection and response now anchors many contracts, converting formerly capital-intensive software into operating-expense line items that appeal to CFOs.

Professional services demand is also high, because annual audits under the IA Standards require risk assessments and penetration tests by accredited experts. As enterprises accelerate zero-trust pilots, architects capable of mapping identity, network, and data-layer controls into a single policy engine are scarce. Providers that combine consulting, deployment, and run-time operations are well placed to lift UAE cybersecurity market share in the services arena.

By Deployment Mode: Cloud Retains Primacy Under Data-Residency Rules

Cloud deployment captured 63.12% of UAE cybersecurity market share in 2025 and is advancing at an 11.16% CAGR through 2031. The UAE cybersecurity market size attributable to cloud workloads will expand as hyperscalers invest in sovereign zones, enabling customers to process security telemetry locally. On-premises architectures persist in energy and defense, yet those users still adopt cloud-native security-analytics services for non-safety-critical data.

Localization is now a differentiator. Sophos opened a UAE data center on AWS infrastructure in May 2025, and Cisco followed with a Duo MFA instance in 2024, ensuring authentication tokens remain onshore. These moves align with IA Standards clauses that prohibit cross-border flows for government workloads. As a result, cloud-access security brokers, cloud-security-posture management, and container-security tools have become staple line items in RFPs, reinforcing the centrality of cloud to the UAE cybersecurity market.

By End-Use Industry: Healthcare Accelerates, BFSI Consolidates

Healthcare is forecast to post a 12.01% CAGR, the fastest of any vertical, as telemedicine normalizes post-pandemic and encryption of electronic health records becomes mandatory.[4]Ministry of Health and Prevention, “Data Protection Healthcare 2025,” mohap.gov.ae The UAE cybersecurity market size for healthcare is rising on the back of AI governance standards released in 2024 that require security safeguards for patient-data models.

BFSI remains the largest spender with 19.56% of 2025 outlays. Central Bank directives on open-banking APIs and real-time fraud detection sustain investments in behavioral biometrics and threat-intelligence sharing. Energy, retail, and aerospace each exhibit niche requirements, prompting vendors to tailor UAE cybersecurity market offerings to sector-specific compliance frameworks.

By Enterprise Size: SMEs Close the Gap

SMEs will grow their spend at an 11.78% CAGR, aided by cloud-first economics and growing ransomware awareness. Although large enterprises commanded 67.29% of 2025 expenditure, incremental growth is tapering as their architectures mature. Unified, subscription-priced stacks that package endpoint, email, and web defenses into a single agent are resonating with cost-aware SMEs, helping them capture incremental UAE cybersecurity market share.

Micro enterprises still lag due to limited budgets and awareness, but government subsidies and freemium vendor offers are nudging adoption of basics such as multi-factor authentication and encrypted backups.

Geography Analysis

Abu Dhabi and Dubai drive the bulk of UAE cybersecurity market revenue, anchored by energy infrastructure and financial hubs. Abu Dhabi prioritizes OT security for oil, gas, and utilities, while Dubai emphasizes cloud security for banking, logistics, and tourism workloads. Sharjah, Ajman, Ras Al Khaimah, Umm Al Quwain, and Fujairah are witnessing steady uptake as SMEs digitize. Fortinet’s April 2025 MOU with the Sharjah Cyber Security Center underscores rising regional demand for training and threat intelligence.

Free-zone fragmentation complicates compliance. DIFC applies GDPR-style data-protection laws, whereas ADGM enforces separate financial-services standards. Multizone enterprises therefore favor vendors that embed jurisdiction-specific policy templates.

Regional threat vectors remain acute. IBM’s X-Force index placed the UAE fourth worldwide for cyberattacks in 2024, accounting for 10% of global events. The nation is also central to Gulf Cooperation Council threat-sharing pacts and bilateral agreements with the United States, United Kingdom, and Israel, making it a proving ground for zero-trust and quantum-safe pilots.

Competitive Landscape

The UAE cybersecurity market is moderately fragmented. Local champions such as Help AG, Injazat, and Etisalat Digital compete alongside global vendors including Cisco, Palo Alto Networks, Microsoft, CrowdStrike, and Fortinet. Local players leverage proximity to government decision‐makers, fluency in Arabic, and expertise in UAE compliance frameworks to win public-sector and critical-infrastructure projects, while international vendors contribute scale, R and D depth, and global threat-intelligence networks. Partnership models are common, Help AG’s May 2025 agreement with Etisalat Digital fuses managed-security operations with carrier infrastructure to deliver integrated monitoring and incident response. Fortinet’s October 2025 deal with Dubai Electricity and Water Authority embeds next-generation firewalls and secure SD-WAN across utility OT networks, illustrating convergence of IT and OT protection.

White-space opportunities persist in hospitality, construction, and personal services, where digital adoption is rising but security budgets trail other sectors. Disruptors are targeting these segments with cloud-delivered platforms that minimize on-premises hardware and use consumption-based pricing. Artificial-intelligence automation of threat detection and incident response is gaining favor, yet Cisco’s 2025 readiness index showed only 4% of UAE organizations fully mature across identity, network, and application domains, suggesting most enterprises still build foundational controls. Vendors that prove cuts in mean time to detect and respond through audited case studies are moving up shortlists.

Localization of data centers has become a decisive bidding factor, because IA Standards bar cross-border telemetry for government and critical-infrastructure workloads. Sophos activated a UAE telemetry hub on AWS infrastructure in 2025, and Cisco placed Duo MFA servers onshore in 2024, giving both vendors latency and compliance advantages over rivals that still backhaul data to Europe or the United States,. Mergers and minority stakes are also reshaping the field, Microsoft’s USD 1.5 billion investment in G42 in 2024 deepened collaboration on sovereign-cloud infrastructure and security research. Competitive positioning now hinges on bundling governance tooling, threat intelligence, and managed detection into SME-friendly subscriptions without sacrificing the advanced analytics demanded by large banks and energy majors. Vendors balancing global scale with local nuance are poised to capture incremental UAE cybersecurity market share.

UAE Cybersecurity Industry Leaders

DarkMatter LLC

Injazat Data Systems LLC

Help AG (Etisalat Group)

Etisalat Digital

Emirates Integrated Telecommunications Company PJSC (du)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Help AG showcased its Continuous Threat Exposure Management platform at GITEX Global 2025 and signaled expansion into Africa and South Asia.

- October 2025: Fortinet partnered with Dubai Electricity and Water Authority to deploy next-generation firewalls, secure SD-WAN, and joint SOC capabilities.

- October 2025: Cisco unveiled AI-ready Hypershield and XDR integrations for multi-cloud environments at GITEX 2025.

- May 2025: Help AG and Etisalat Digital launched an integrated managed-security partnership targeting government and critical infrastructure.

UAE Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The UAE Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How fast is spending on cyber defenses growing in the UAE?

The UAE cybersecurity market is projected to grow at a 10.66% CAGR from 2026 to 2031, rising from USD 0.91 billion to USD 1.51 billion.

Which vertical allocates the most budget?

Banking, financial services, and insurance contributed 19.56% of 2025 outlays, the largest share among end-use sectors.

Why are managed-security services gaining popularity?

A shortage of senior Emirati cybersecurity talent and the complexity of IA-standards compliance are prompting enterprises to outsource 24/7 monitoring and incident response.

What drives cloud-security demand in the Emirates?

Government cloud-first mandates, AWS and Azure sovereign regions, and data-residency clauses in the IA Standards are accelerating cloud-security adoption.

Which emirates see the highest cybersecurity investment?

Abu Dhabi emphasizes operational-technology protection for energy infrastructure, while Dubai leads spending on cloud security for finance, logistics, and tourism.

How does regulation influence vendor selection?

Compliance with Version 2 of the UAE Information Assurance Standards and on-shore data processing are now baseline requirements for winning government and critical-infrastructure contracts.

Page last updated on: