United Arab Emirates (UAE) Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

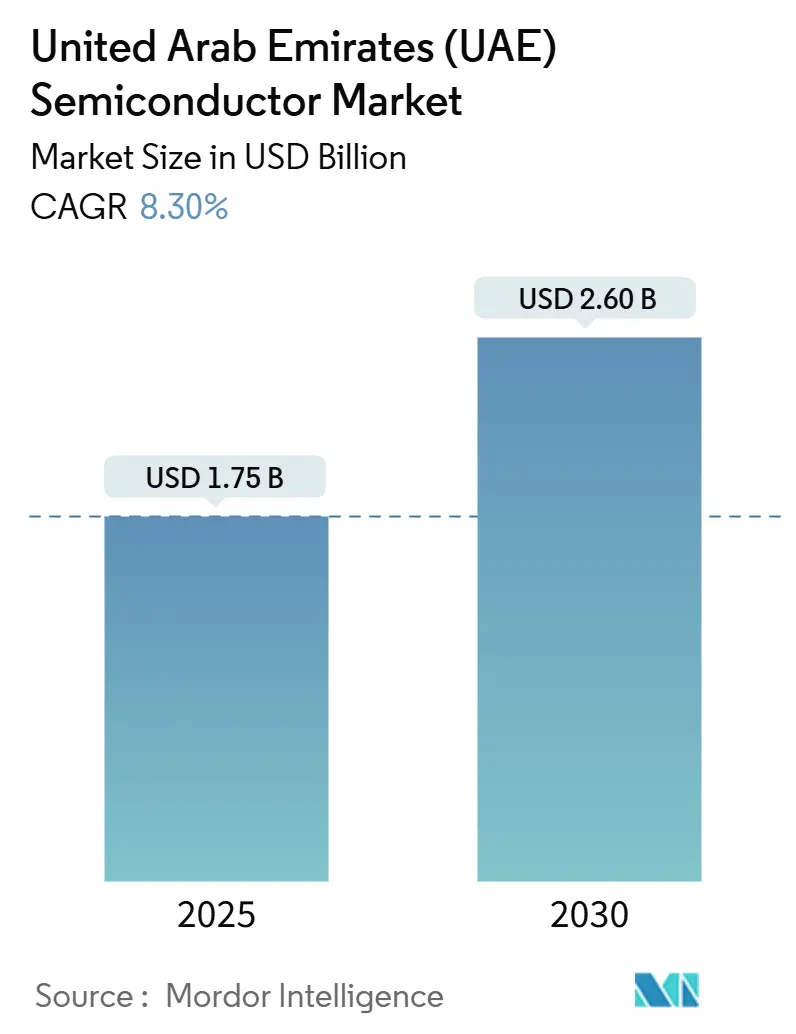

| Market Size (2025) | USD 1.75 Billion |

| Market Size (2030) | USD 2.60 Billion |

| Growth Rate (2025 - 2030) | 8.30% CAGR |

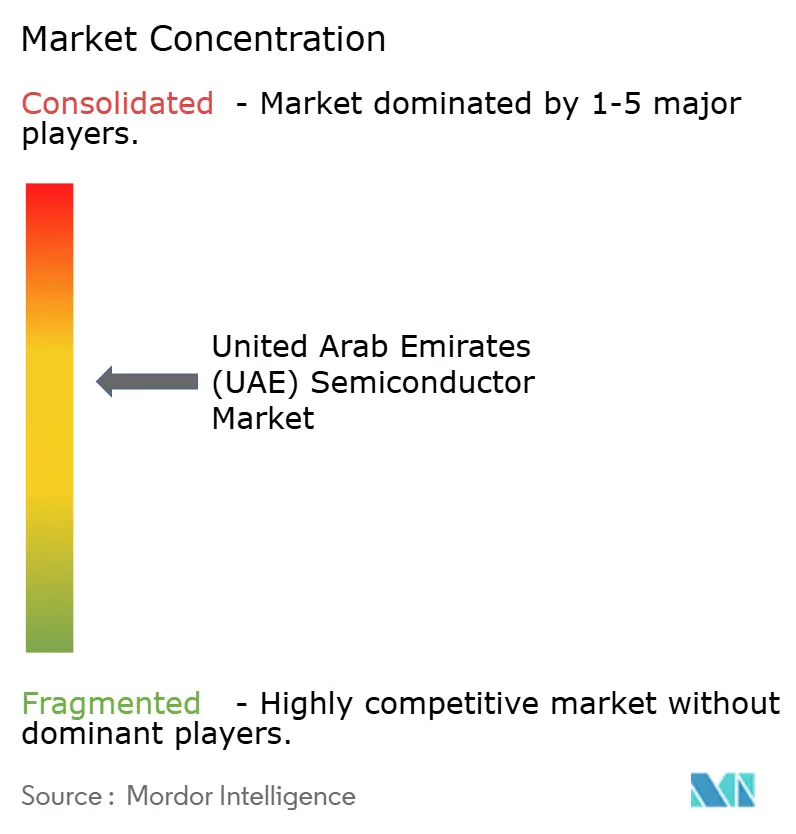

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates (UAE) Semiconductor Market Analysis by Mordor Intelligence

The United Arab Emirates Semiconductor Market size is estimated at USD 1.75 billion in 2025, and is expected to reach USD 2.60 billion by 2030, at a CAGR of 8.30% during the forecast period (2025-2030). This trajectory reflects the government’s push to shift the national economy from hydrocarbons toward knowledge industries, anchored by large-scale AI data-center buildouts, 5G-Advanced rollouts, and renewed advanced-node manufacturing incentives. Sustained investment from sovereign funds and long-term agreements with U.S. chip suppliers ensure a reliable flow of advanced GPUs, memory, and RF components, mitigating previous import-license risks. National broadband plans are driving optical-transceiver and RF-front-end demand, while ambitious EV adoption targets translate into surging orders for power-management and sensor devices. Entry barriers persist, however, as the Emirates contends with water scarcity, imported specialty gases, and fierce global competition for semiconductor talent.

Key Report Takeaways

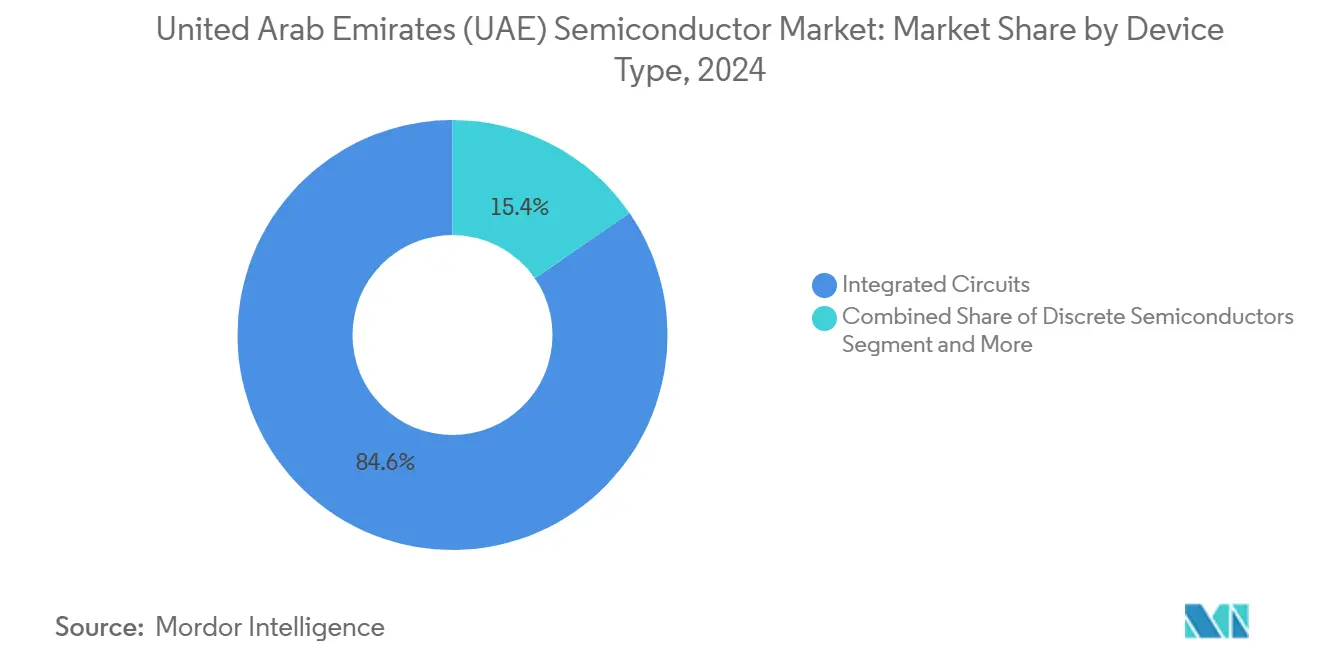

- By device type, Integrated Circuits held 84.6% of the UAE semiconductor market share in 2024, while Sensors and MEMS are advancing at a 9.7% CAGR through 2030.

- By business model, the IDM segment accounted for a 68.3% share of the UAE semiconductor market size in 2024; Design/Fabless vendors are projected to expand at a 9% CAGR to 2030.

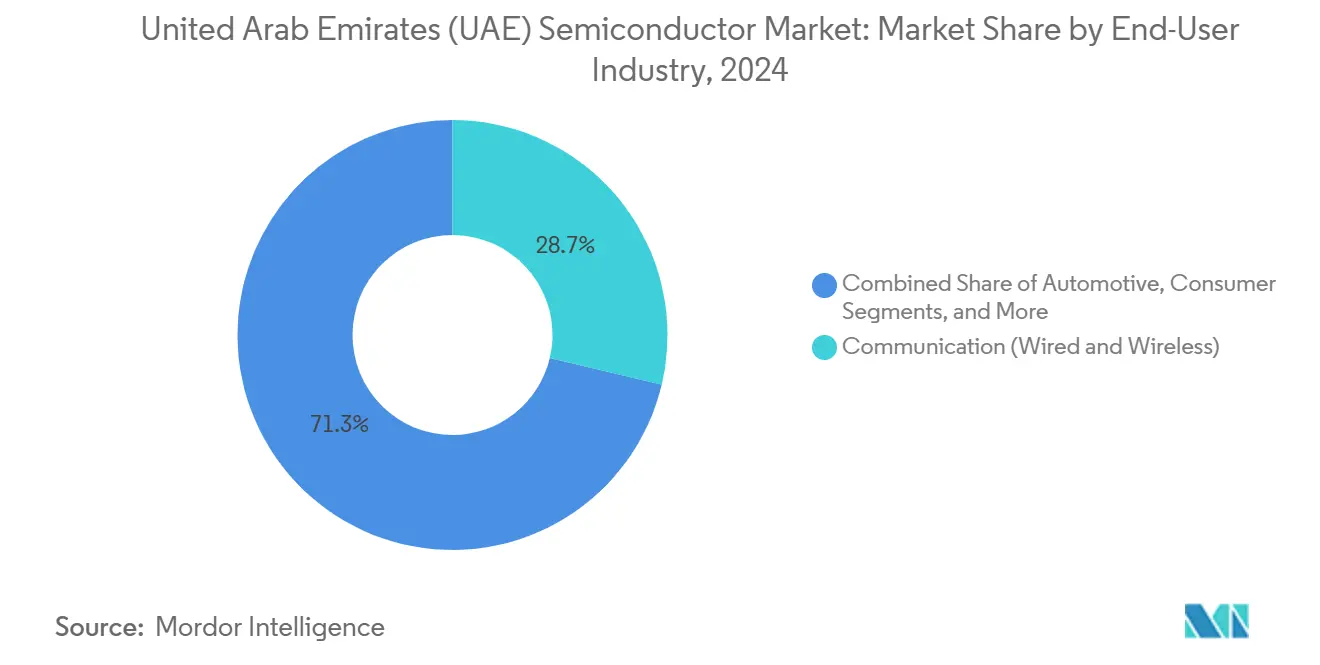

- By end-user industry, communication applications captured 28.71% revenue share of the UAE semiconductor market in 2024, whereas artificial-intelligence applications are forecast to grow at a 9.6% CAGR through 2030.

United Arab Emirates (UAE) Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Govt push for advanced-node manufacturing incentives | +1.2% | Dubai Silicon Oasis, Abu Dhabi | Medium term (2-4 years) |

| Surge in domestic AI/edge-computing hardware demand | +1.8% | Abu Dhabi AI campus, nationwide | Short term (≤2 years) |

| Rapid 5G and FTTx rollout | +1.1% | Dubai, Abu Dhabi | Short term (≤2 years) |

| Electrification of transport and smart mobility | +0.9% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Niche aerospace-defense offset programs | +0.6% | Defense industrial zones | Long term (≥4 years) |

| Semiconductor design-IP clusters | +0.8% | Dubai Silicon Oasis | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government push for advanced node manufacturing incentives

A 180 billion AED industrial package under “Make it in the Emirates” earmarks tax holidays, 100% foreign ownership, and streamlined IP protection to lure foundry investments, tilting policy from chip importation toward selective wafer-fab and advanced-packaging activities. [1]UAE Ministry of Industry & Advanced Technology, “Make it in the Emirates,” moiat.gov.ae Dubai Silicon Oasis has already updated its land-lease regulations to prioritize semiconductor tenants and fast-track environmental clearances. Export-control clauses embedded in new patent rules assure U.S. licensors that sensitive defense-grade IP will remain protected, lowering compliance friction for dual-use technologies. Preliminary site-selection talks with TSMC and Samsung indicate interest in small-volume pilot lines, though water-recycling investment and skilled-labor pipelines remain prerequisites. The net effect is a targeted uplift in design-for-manufacturing know-how rather than a wholesale relocation of mega-fabs to the desert.

Surge in domestic AI/edge-computing hardware demand

The Stargate UAE campus will deploy roughly 100,000 Nvidia GB300 GPUs, giving Abu Dhabi one of the world’s top-five AI compute capacities once fully operational in 2026. G42’s adoption of Qualcomm Cloud AI 100 accelerators demonstrates the pivot toward specialized inference chips for sovereign public-sector workloads, from border-control analytics to Arabic-language LLM deployments. Local cloud providers bundle GPU leasing with national-security-grade SLAs, ensuring near-captive demand for high-margin accelerators. Beyond hyperscale, edge-AI modules power traffic-management systems in Dubai’s Smart City corridors, requiring ruggedized SOCs capable of handling 65 °C ambient temperatures without active liquid cooling. The resulting bill-of-materials mix skews heavily toward advanced nodes (≤5 nm), raising ASPs and cushioning suppliers from commodity-price swings.

Rapid 5G and FTTx rollout driving RF and optical components

Operators e& and du reached 30.5 Gbps in field tests using 5G-Advanced carrier aggregation, a milestone that forces continuous upgrades of RF front-end modules and gallium-nitride power amplifiers. Commercial VoNR services launched in 2025 require low-latency envelope-tracking ICs to preserve handset battery life while sustaining millimeter-wave links. Nationwide fiber penetration surpasses 93%, boosting demand for silicon-photonics transceivers as operators future-proof backhaul for 6G readiness. Planned 6G testbeds before 2030 will require terahertz silicon-germanium mixers, widening addressable revenue pools for compound-semiconductor vendors. Such predictable multi-year capex cycles underpin baseline volume commitments for front-end suppliers.

Electrification of transport and smart-mobility projects

Dubai targets 42,000 EV registrations by 2030 and has earmarked concessions for 1,000 smart chargers, each equipped with silicon-carbide MOSFETs and isolated gate drivers for grid resiliency. Abu Dhabi’s Department of Energy mandates OCPP-compliant charging stations, elevating demand for secure microcontrollers and connectivity chipsets that support over-the-air firmware updates. Automotive OEMs offer Level 2+ ADAS packages, each vehicle embedding up to USD 550 in semiconductor content—double 2022 figures—thanks to radar, lidar, and sensor-fusion processors. Pilot robo-taxi corridors on Yas Island employ Nvidia DRIVE Orin SOCs, while Hyperloop cargo pods under feasibility study will rely on high-temperature-rated IGBTs for linear-motor propulsion. Growing appetite for energy-efficient power devices strengthens revenue diversification for analog and power-discrete suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited wafer-fab water and energy optimization | -1.4% | Potential fab sites | Medium term (2-4 years) |

| Dependence on imported specialty gases and substrates | -0.8% | Nationwide | Short term (≤2 years) |

| Talent attraction gaps vs. Asian hubs | -1.1% | Nationwide | Long term (≥4 years) |

| IP-protection concerns in cross-border JVs | -0.5% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited wafer-fab water and energy optimization challenges

Producing a single 300 mm wafer can consume 2,000 gallons of ultrapure water; a high-volume fab may demand 10 million gallons daily, straining the UAE’s desalination-centric supply—already earmarked for domestic and agricultural use. [2]Staff Writer, “Thirsty Chip Facilities Under Scrutiny in Water-Stressed Areas,” fdiintelligence.com Data-center cooling will add 426 billion liters annually across the Gulf by 2030, heightening resource competition. Although closed-loop recycling allows fabs to reuse up to 98% of process water, capital investment tops USD 200 million per mid-node line, complicating ROI for potential entrants. Power-quality constraints also loom; voltage sags beyond ±2% can scrap lots worth USD 20 million, necessitating redundant sub-stations and on-site gas turbines, which inflate overheads for would-be foundry investors. The downside risk deters greenfield mega-fab commitments, channeling investment toward design, assembly, and advanced-testing niches instead.

Talent attraction gaps versus mature Asian hubs

The global semiconductor industry needs 1 million additional skilled professionals by 2030, yet only 3% of the pipeline currently prefers relocation to the Middle East, citing limited academic ecosystems and career-progression clarity. Average total compensation for a senior process engineer in Taiwan is 14% lower than in Dubai after tax, but subsidized housing and stock-option upside at Asian giants offset the gap. Qualcomm’s Abu Dhabi engineering hub illustrates progress, yet it focuses on AI inference rather than core process-integration R&D. Without tier-one microelectronics graduate programs, local universities struggle to feed the talent funnel, pushing companies toward costly expatriate packages that erode margin headroom. Workforce constraints rank among the top-three concerns cited by prospective fab partners in ongoing feasibility assessments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits dominate value capture

Integrated Circuits generated 84.6% of 2024 revenue, underscoring the UAE semiconductor market’s orientation toward AI accelerators, server CPUs, and high-bandwidth DRAM clusters that anchor cloud infrastructure. [3]SoftBank Group, “Global Tech Alliance Launches Stargate UAE,” softbankgroup.com Annual hyperscale GPU orders alone exceeded 40,000 in 2025, translating to nearly USD 1 billion in silicon value and anchoring the UAE semiconductor market size at the high end of the ASP spectrum. Memory and logic ICs ride the same wave, as sovereign-cloud providers expand sovereign LLM capacity. By contrast, discrete power devices contribute less than 5% of shipments but enjoy a volume uptick from EV-charger rollouts, elevating compound annual revenue by high single digits. Sensor and MEMS volumes are smaller but outpace all other categories at a 9.7% CAGR, powered by edge-AI cameras and smart-meter deployments across municipal grids. Optoetronics, particularly photonic integrated circuits (PICs) and vertical-cavity surface-emitting lasers (VCSELs), ride the fiber-optic boom accompanying nationwide FTTx upgrades. While PIC uptake remains in early innings, operators’ preference for single-vendor coherent optics under long-term maintenance agreements positions the category for steady double-digit growth over the forecast horizon.

Strong average selling prices and a skew toward advanced nodes keep gross margins near 47%, well above global commodity averages, even though volume expansion is modest. This high-value mix explains why the UAE semiconductor market continues to punch above its shipment weight in regional revenue comparisons. Suppliers strategically introduce their newest nodes in the country to lock in premium early-adopter contracts, reinforcing the Integrated Circuits segment’s revenue dominance.

By Business Model: IDM leadership persists as fabless momentum builds

IDM companies captured 68.3% revenue in 2024, aided by GlobalFoundries’ preferential status with multiple state entities and Samsung’s heavy DRAM and NAND share within hyperscale data-center procurements. End users value one-stop vertical control for mission-critical chips that power national security workloads. Furthermore, local public-cloud tenders frequently require in-country failure-analysis labs—capabilities more common among IDMs—cementing their supply-chain primacy.

Fabless and design-only vendors are nonetheless gaining ground, advancing at a 9% CAGR through 2030. Qualcomm’s Abu Dhabi engineering center illustrates how localized ASIC design for edge-computing and industrial IoT allows fabless houses to undercut traditional IDMs on time-to-market while banking on offshore manufacturing scale. Start-up clusters inside Dubai Silicon Oasis offer subsidized EDA toolchains and tape-out grants, cutting first-silicon costs by up to 35%. The UAE semiconductor market size for design services could exceed USD 150 million by 2030 if these incubators successfully graduate 30+ fabless start-ups, signaling a subtle but meaningful power shift from manufacturing to design leadership.

By End-User Industry: Communication hardware still largest as AI rockets ahead

Communication infrastructure commanded 28.71% of 2024 revenue, driven by RF-front-end ASICs, base-station power amplifiers, and coherent optical modules feeding the national 5G-Advanced rollout. Mobile-edge computing nodes installed at 5G sites incorporate AI inference accelerators for real-time video analytics, making communication and AI demand increasingly intertwined. Procurement cycles are predictable here, with multi-year frame agreements tying suppliers to carrier roadmaps, ensuring stable baseline volumes.

Artificial-intelligence workloads represent the fastest-growing end-user segment at an 9.6% CAGR, having already overtaken industrial automation in 2025 as the second-largest revenue generator. Government mandates to host sovereign LLMs inside national borders guarantee at least 200 petaflops of incremental compute capacity annually through 2028. Edge-AI deployments in customs, healthcare triage, and urban planning widen the aperture beyond data centers, diversifying semiconductor demand to include low-power NPUs and secure enclave microcontrollers.

Industrial and energy verticals continue to rely on rugged microcontrollers, power devices, and industrial Ethernet PHYs for oil-field digitization and refinery automation. However, their share inches downward as AI and mobility projects capture larger slices of public funding. Consumer electronics remain the smallest slice owing to a limited domestic OEM base, yet premium smartphone imports indirectly buoy RF component shipments because many devices are distributed via UAE logistics hubs before re-export to Africa and South Asia.

Geography Analysis

Dubai and Abu Dhabi jointly account for almost 80% of UAE semiconductor consumption. Dubai’s mature telecoms sector, financial-services data centers, and free-trade zones concentrate RF, storage, and networking orders. Revenue expansion here runs parallel to incremental 5G densification, municipal smart-grid rollouts, and fintech server deployments. The Dubai Silicon Oasis cluster has grown into the de facto design-services hub, hosting more than 120 semiconductor and EDA firms, including front-office operations for Intel Foundry Services and Synopsys license support.

Abu Dhabi’s footprint is anchored by the Stargate campus and GlobalFoundries’ historic stakes. AI hyperscale racks slated for delivery in 2026 will alone demand more than two million server DIMMs and 15,000 coherent optical transceivers, underpinning a step-change in demand for high-bandwidth DRAM and advanced IC substrates. The emirate’s abundant gas-fired power plants supply baseload capacity for energy-hungry GPU clusters, giving Abu Dhabi a structural cost advantage over neighboring technology hubs.

Northern Emirates—Sharjah, Ras Al-Khaimah, and Fujairah—play support roles, offering industrial land for PCB assembly and regional distribution warehouses. While their semiconductor spending is modest, free-zone tax incentives attract logistics firms that shorten delivery lead times for import-dependent fabs across the Gulf. Over time, these emirates may morph into ancillary OSAT (outsourced semiconductor assembly and test) locations, capitalizing on lower real-estate costs.

Regionally, the UAE competes directly with Saudi Arabia’s USD 266 million semiconductor-hub initiative unveiled in 2024, which targets 50 design start-ups by 2030. Saudi Arabia’s deeper domestic market and vast PIF funding represent credible competition for high-profile joint ventures, but the UAE’s earlier infrastructure and regulatory head start lend it a first-mover advantage. Qatar and Oman lag further behind, focusing mostly on system integration. Consequently, the UAE semiconductor market retains its role as the regional gateway, funneling Asian-manufactured silicon into Middle-East deployments while layering on design validation, system integration, and high-margin value-adds.

Competitive Landscape

Global competition remains moderate, with no firm owning more than 20% of total UAE semiconductor revenue. GlobalFoundries leverages sovereign backing to supply secure ASICs for defense and telecoms, while Intel secures high-margin CPU deals for cloud and enterprise workloads through its Gulf subsidiary. Samsung dominates memory share, especially in HBMe silicon feeding GPU clusters, and partners with Etisalat’s data-center division for high-density SSD deployments.

Qualcomm supplies Snapdragon X80-based RF modules for 5G CPEs and collaborates with e& on private-network edge-AI gateways. [4]Qualcomm Press Office, “Qualcomm and e& Collaborate on AI at the Edge,” qualcomm.com Nvidia, though fabless, wields outsized influence because every hyperscale announcement in the country to date banks on its GPU roadmap. Analog Devices, Infineon, and STMicroelectronics jostle for automotive-SiC and industrial-power sockets, each announcing regional customer-support centers to meet stringent IEC and GCC grid-code requirements.

Strategic moves skew toward joint-innovation labs and long-term supply commitments rather than greenfield fabs. Microsoft’s AED 2 billion hyperscale facility with du bundles Azure cloud with sovereign-data compliance, illustrating the ecosystem approach: compute platform plus connectivity plus local integration. Suppliers increasingly co-locate field-app engineering teams inside customer campuses, shortening design-win cycles and raising switching costs for rivals.

Vendor white-space opportunities persist in power-efficient edge-AI accelerators, automotive functional-safety MCUs, and silicon photonics for <200-m data-center links. Success will depend on ecosystem alignment: tapping into UAE R&D grants, integrating with home-grown AI stacks, and addressing Arabic NLP requirements. Companies able to overlay software, services, and local warranty-support layers on top of hardware stand to capture sticky annuity streams.

United Arab Emirates (UAE) Semiconductor Industry Leaders

GlobalFoundries Inc.

Intel Semiconductor Gulf LLC

Samsung Gulf Electronics FZE

NXP Semiconductors Middle East FZ-LLC

STMicroelectronics NV (Dubai Branch)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TSMC restarted exploratory talks with U.S. negotiators over a potential Arizona-scale fab in the UAE, signaling a possible entry into MENA manufacturing.

- May 2025: The U.S.–UAE export framework granted licenses for 500,000 Nvidia H100 and GB300 GPUs over five years, the Gulf’s biggest advanced-chip agreement to date.

- May 2025: Qualcomm inaugurated a global engineering center in Abu Dhabi to spearhead AI, industrial IoT, and data-center silicon solutions.

- May 2025: The Stargate UAE consortium (G42, OpenAI, Oracle, Nvidia, SoftBank, Cisco) broke ground on a 1 GW AI compute cluster slated for 2026 completion.

- April 2025: du and Microsoft committed AED 2 billion to a hyperscale data-center venture supporting sovereign-cloud workloads in Dubai.

- March 2025: UAE pledged USD 1.4 trillion in U.S. investments over the next decade, including USD 25 billion for energy infrastructure and data centers with semiconductor tie-ins.

United Arab Emirates (UAE) Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design/Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design/Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

What CAGR is forecast for UAE semiconductor revenue through 2030?

The market is expected to grow at a 8.30% CAGR, lifting revenue from USD 1.75 billion in 2025 to USD 2.60 billion by 2030.

Which device category generates the largest share of UAE semiconductor sales?

Integrated Circuits account for 84.6% of 2024 revenue, thanks to strong demand for AI accelerators and memory.

Why are IDMs still dominant in the Emirates?

Vertical control over manufacturing, secure supply lines, and local failure-analysis labs give IDMs 68.3% revenue share.

What is driving the fastest growth in end-user demand?

Artificial-intelligence applications are expanding at an 9.6% CAGR due to hyperscale compute clusters and edge-AI rollouts.

Which geographic hub sees the bulk of future chip demand?

Abu Dhabi leads upcoming growth as its Stargate campus ramps GPU deployment and attracts adjacent data-center investments.

What key obstacle limits large-scale wafer fabs in the UAE?

Water scarcity and the capital cost of advanced recycling systems pose significant barriers to mega-fab economics.

Page last updated on: