United Arab Emirates Cloud Accounting Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

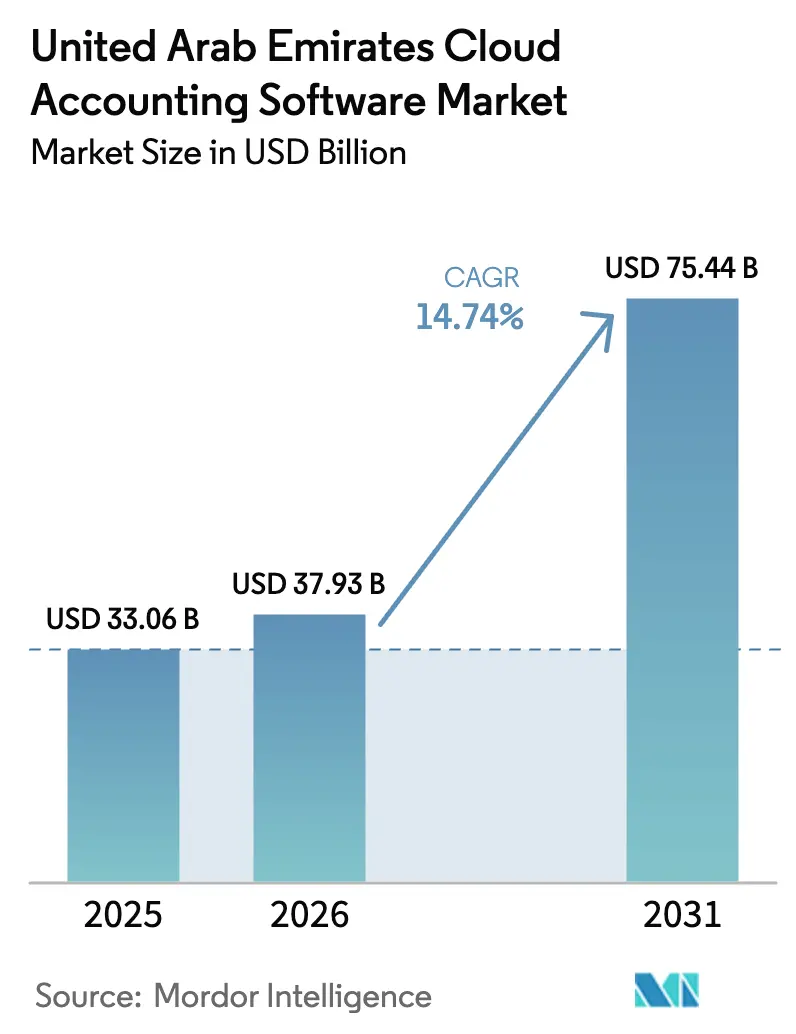

| Base Year Market Size (2025) | USD 33.06 Billion |

| Market Size (2026) | USD 37.93 Billion |

| Market Size (2031) | USD 75.44 Billion |

| Growth Rate (2026 - 2031) | 14.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Cloud Accounting Software Market Analysis by Mordor Intelligence

The United Arab Emirates Cloud Accounting Software Market size is projected to be USD 33.06 billion in 2025, USD 37.93 billion in 2026, and reach USD 75.44 billion by 2031, growing at a CAGR of 14.74% from 2026 to 2031. Demand is climbing because three regulatory measures the Federal Tax Authority’s mandatory e-invoicing program, the Central Bank of the UAE’s Open Finance Regulation, and sovereign-cloud data-residency rules are compressing digital-transformation timetables across every major vertical. Vendors able to deliver accredited e-invoicing, out-of-the-box API connectivity to licensed financial institutions, and in-country hosting are seizing design-in wins while procurement cycles remain open. Small and medium enterprises still dominate installed base numbers, yet large conglomerates are accelerating hybrid deployments to reconcile global enterprise-resource-planning (ERP) environments with local data-sovereignty obligations. The interplay between policy deadlines and hyperscale investment is positioning the Emirates as a regional test bed for compliance-native, API-first finance stacks.

Key Report Takeaways

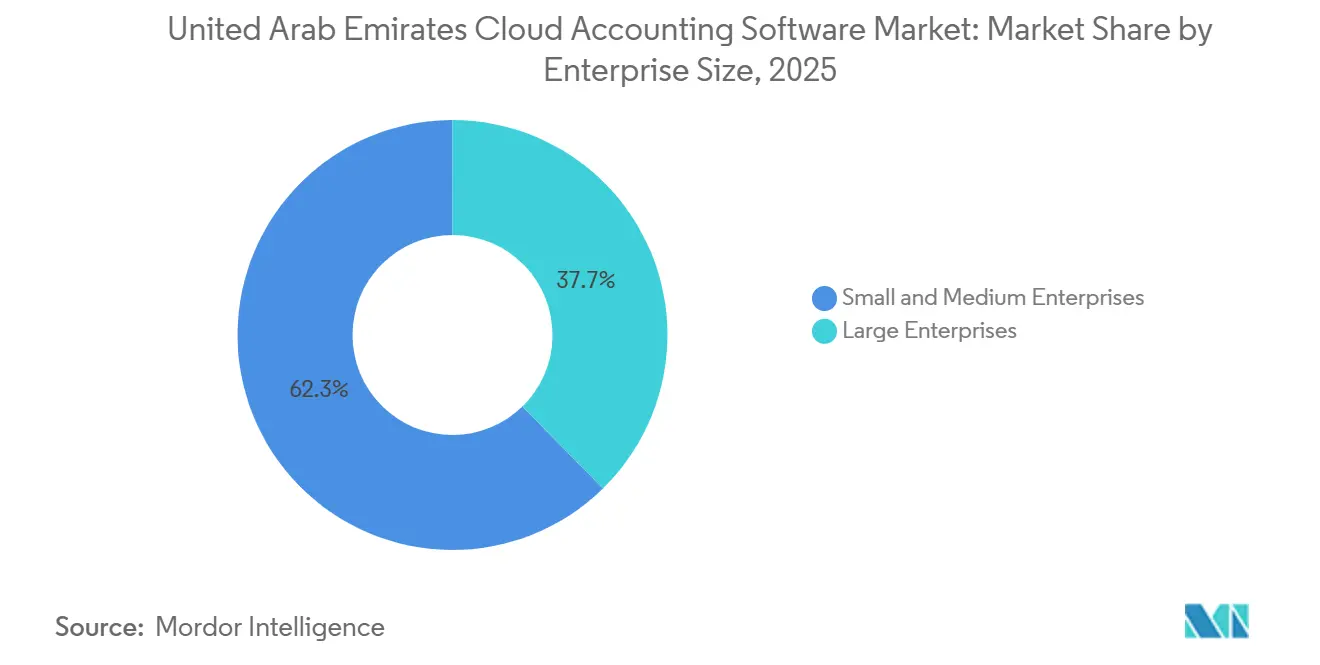

- By size of enterprise, small and medium enterprises led with 62.34% revenue share in 2025; large enterprises are projected to deliver the fastest 15.68% CAGR through 2031.

- By industry vertical, banking, financial services and insurance held 27.51% of the United Arab Emirates cloud accounting software market share in 2025, while energy, oil and gas is on track to expand at a 15.16% CAGR to 2031.

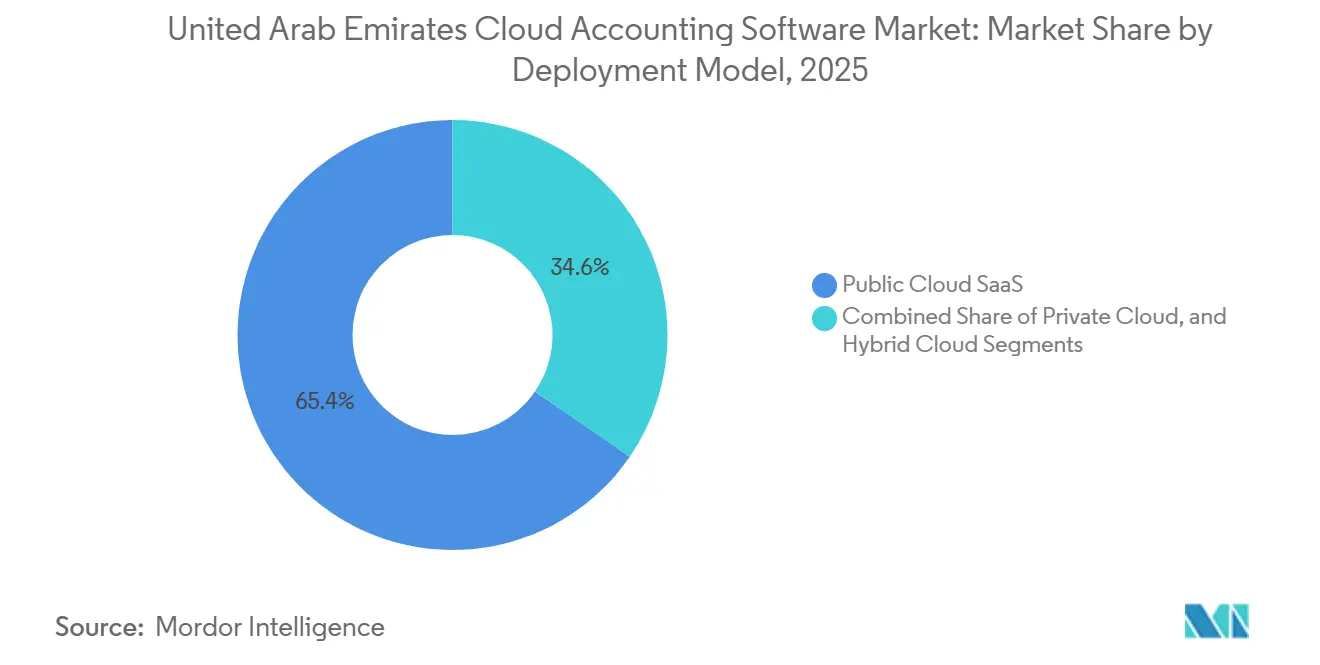

- By deployment model, public cloud software-as-a-service accounted for 65.42% share of the United Arab Emirates cloud accounting software market size in 2025, but hybrid cloud is advancing at a 14.97% CAGR over 2026-2031.

- By application, invoicing and billing captured 31.73% share in 2025 and inventory and order management is expected to grow at a 15.71% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Cloud Accounting Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory E-Invoicing Compliance Wave | +4.2% | National, early adoption in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Demand to Improve Financial-Process Efficiency | +3.1% | National, strongest in BFSI and retail | Medium term (2-4 years) |

| Real-Time Payments Rail Driving Embedded Accounting | +2.8% | National, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Growing Automation of Accounting Practices | +2.3% | National, higher penetration in large enterprises | Long term (≥ 4 years) |

| FinTech Sandboxes Enabling API-First Integrations | +1.6% | Dubai (DIFC), Abu Dhabi (ADGM) | Long term (≥ 4 years) |

| Rise in Demand for Subscription Models | +1.4% | National, particularly among SMEs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory E-Invoicing Compliance Wave

The Federal Tax Authority piloted structured e-invoicing in July 2026 and will mandate full adoption for firms exceeding AED 50 million turnover by January 2027, pushing enterprises toward PEPPOL-compliant five-corner models that legacy desktop products cannot handle.[1]Federal Tax Authority, “E-Invoicing,” TAX.GOV.AE A ten-year digital-document-retention rule further tilts economics toward cloud subscriptions because on-premises storage requires capital expenditure and disaster-recovery duplication. ClearTax and Taxilla earned Accredited Service Provider status early, providing out-of-the-box integrations that shorten implementation cycles. With procurement backlogs expected after mid-2026, organizations are fast-tracking selections to avoid non-compliance penalties, channeling bookings to vendors already certified.

Demand to Improve Financial-Process Efficiency

Boards listed on the Dubai Financial Market and Abu Dhabi Securities Exchange now expect monthly instead of quarterly closes, forcing finance teams to automate reconciliations, intercompany eliminations and multi-currency restatements. Cloud platforms provide machine-learning anomaly detection and rule-driven journal posting, compressing close cycles while eliminating manual spreadsheets. The UAE National AI Strategy offers priority access to sovereign-cloud infrastructure for early adopters, giving pilot users a cost advantage. Together, governance expectations and policy incentives are transforming automation from discretionary to mission-critical.

Real-Time Payments Rail Driving Embedded Accounting

The Central Bank’s Instant Payment Platform clears transactions in under ten seconds, creating demand for ledgers that automatically ingest confirmations and reconcile receivables. Open Finance rules oblige banks to expose standardized APIs, allowing accounting vendors to embed payment initiation and account aggregation at negligible incremental cost. Retailers now display invoice settlement status in checkout flows, while enterprises holding digital-asset reserves need mark-to-market valuation modules in the same ledger. Vendors that conform to ISO 20022 and pre-integrate with the central API hub are winning digitally native accounts.

Growing Automation of Accounting Practices

Artificial-intelligence adoption in the Dubai International Financial Centre jumped to 52% of regulated firms in 2025, with 79% utilizing AI for internal operations, including finance. Tools ranging from duplicate-invoice detection to dynamic cash-flow forecasting are mitigating the Emirates’ shortage of certified accountants. Tally Prime 7.0, launched in December 2025, added bilingual interfaces and automated VAT reconciliation that cut month-end closes by 40% during pilots. For SMEs, automation is not optional; it substitutes for unavailable talent while improving control environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Sovereign-Cloud Residency Fees for SMEs | -1.8% | National, most acute in Sharjah and the Northern Emirates | Short term (≤ 2 years) |

| Data-Security and Privacy Concerns | -1.5% | National, especially BFSI and healthcare | Medium term (2-4 years) |

| Integration Complexity with Legacy Systems | -1.2% | Dubai and Abu Dhabi large enterprises | Medium term (2-4 years) |

| Lack of Skilled In-House Personnel | -0.9% | National, more pronounced outside Dubai and Abu Dhabi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Sovereign-Cloud Residency Fees for SMEs

The National Cloud Security Policy mandates in-country hosting for sensitive data, but sovereign regions operated by Microsoft, Oracle and others cost roughly 30% more than global cloud lists.[2]Microsoft Azure, “Sovereign Cloud Solutions,” AZURE.MICROSOFT.COM Micro-enterprises in Sharjah and the Northern Emirates, already facing higher financing costs, sometimes postpone migration or split workloads across cheaper international regions, introducing latency and compliance risk. Federal programs promise cloud credits for one million SMEs by 2030, yet opaque eligibility slows uptake, muting near-term conversion.

Data-Security and Privacy Concerns

The Central Bank’s Cloud Computing Rulebook requires annual third-party audits, encryption in transit and at rest, plus multi-factor authentication for financial-sector deployments. High-profile ransomware events have driven risk committees to favor vendors with ISO 27001 and SOC 2 Type II attestations. Absence of a finalized federal data-protection law leaves cross-border-transfer liability unclear, nudging BFSI and healthcare buyers toward private or hybrid clouds while prolonging sales cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: Hybrid Architectures Catalyze Large-Enterprise Upswing

Large enterprises represented a smaller installed base but are forecast to grow at 15.68% CAGR, outpacing the overall United Arab Emirates cloud accounting software market. Consolidated groups and government-linked companies need multi-entity eliminations, IFRS alignment and integration with procurement, inventory and HR modules. The United Arab Emirates cloud accounting software market size for large-enterprise deployments is expected to jump from USD 0.01 billion in 2026 to USD 0.03 billion in 2031. Demand centers on hybrid frameworks where sensitive HR and tax data sit on-premises while analytics workloads run in hyperscale clouds, balancing sovereignty and scale. ADNOC’s USD 1.5 billion digital program illustrates the trend, mixing Azure analytics with private-cloud data stores.

Small and medium enterprises currently anchor 62.34% share thanks to 557,000 registered SMEs and cloud-credit subsidies under the National SME Programme. Lightweight packages such as Zoho Books and Wafeq provide Arabic-English interfaces, VAT automation and subscription pricing below AED 40 (USD 10.89) per month, aligning with tight budgets. However, SMEs occasionally struggle with premium sovereign-cloud tariffs, slowing full adoption in outlying emirates. Vendors therefore maintain tiered product lines low-touch SaaS for SMEs and extensible suites for complex conglomerates to optimize coverage across customer sizes.

By Industry Vertical: Energy Accelerates, BFSI Holds Leadership

Banking, financial services and insurance captured 27.51% of 2025 revenue as incumbent banks and digital-only challengers rolled out API-ready ledgers to satisfy Open Finance mandates. Yet the energy, oil and gas vertical, spurred by joint-venture accounting and production-sharing obligations, will record the fastest 15.16% CAGR through 2031. The United Arab Emirates cloud accounting software market share for energy is projected to surpass 12% by the end of the forecast window. ADNOC’s roll-out of Dynamics 365 Finance across 500 service stations underscores real-time margin analysis ambitions.

Retail and e-commerce companies are embedding inventory and payments data into unified ledgers as omnichannel sales surge. Noon’s AWS-based architecture integrates stock visibility and multi-currency settlement, demonstrating the operational gains from tightly linked accounting and logistics workflows.[3]Amazon Web Services, “Noon Case Study,” AWS.AMAZON.COM Real estate developers, construction contractors and healthcare providers form a long-tail opportunity where project accounting, escrow management or medical-billing integrations remain under-served by horizontal suites.

By Deployment Model: Hybrid Cloud Narrows the Gap

Public cloud SaaS commanded 65.42% of 2025 spend because SMEs value zero infrastructure. Nevertheless, hybrid architectures are climbing at a 14.97% CAGR as regulated entities route sensitive records through in-country nodes while exploiting public cloud for burst analytics.

The United Arab Emirates cloud accounting software market size attributed to hybrid deployments is set to double between 2026 and 2031. Oracle’s Alloy sovereign cloud enables Fusion applications to run inside local data centers, while Azure Arc unifies governance across on-premises and multi-cloud assets. This dual-zone approach satisfies the Central Bank’s tiered risk guidance and remains the default path for large banks, energy companies and healthcare systems.

By Application: Inventory and Order Management Leads Growth Curve

Invoicing and billing still retain the largest 31.73% slice thanks to mandatory e-invoicing rollouts. However, inventory and order management solutions will post a rapid 15.71% CAGR as omnichannel merchants embed real-time stock validation into checkout flows.

United Arab Emirates cloud accounting software market size for inventory modules could exceed USD 0.02 billion by 2031. Tally Prime’s expiry-batch alerts and Zoho Books’ predictive reorder points demonstrate vertical innovation. Payroll and HR applications remain essential because the UAE’s labor code requires complex gratuity calculations for expatriates, while tax-management modules enjoy a cyclical lift ahead of the 2027 compliance deadline.

Geography Analysis

Dubai retained 44.63% revenue share in 2025, driven by free-zone headquarters, venture funding density and mature broadband. Abu Dhabi follows, with government-linked entities prioritizing hybrid and private cloud deployments to satisfy sovereign-data statutes. The remainder of the federation Fujairah, Umm Al Quwain, Ajman and emerging industrial corridors will collectively grow at 15.67% CAGR. United Arab Emirates cloud accounting software market share for non-Dubai emirates is expected to reach 33% by 2031.

Federal fiber initiatives, such as Etisalat’s Gigabit coverage expansion, lower infrastructure barriers in peripheral emirates. Zoho’s AED 17 million (USD 4.63 million) wallet-credit scheme with the Umm Al Quwain Chamber accelerated uptake by regional SMEs, illustrating how targeted subsidies translate into subscription growth. Meanwhile, Sharjah manufacturers adopt hybrid ledgers to balance lower operating margins against data-residency costs.

Dubai remains the showcase for innovation. The annual GITEX expo spotlighted partnerships between telecom operator du and Dubai SME, bundling AI accounting assistants with sovereign hosting for 5,000 pilot customers. Though absolute spending leadership should remain with Dubai and Abu Dhabi, faster percentage growth in other emirates will gradually rebalance regional demand.

Competitive Landscape

Competition is moderately fragmented. Global suites Microsoft Dynamics 365, Oracle NetSuite, SAP S/4HANA Cloud, Zoho Books and Xero compete with Arabic-first vendors Wafeq, Tally Solutions and Focus Softnet. The five largest providers captured about 40% of 2025 billings, while 30-plus niche players address micro-segments such as Islamic banking or fleet-management accounting. Tally Solutions reported 70,000 UAE customers by end-2025 after releasing bilingual Tally Prime 7.0 with automated tax reconciliation. Zoho grew local revenue 50% in 2024, expanding its reseller base 40% to penetrate underserved northern emirates.[4]Zoho Corporation, “UAE Market Expansion Announcements,” ZOHO.COM

Vendor strategies converge around securing Federal Tax Authority accreditation, embedding Central Bank API connectivity and adding generative-AI commentary features. Microsoft and SAP each pledged USD 1 billion-plus UAE investments, expanding data-center footprints and channel ecosystems. Oracle’s sovereign-cloud alliance and Xero’s Stripe and Barclays integrations underline a broader play: bundle payments and real-time reconciliation to raise switching costs.

White-space remains in vertical extensions oil-and-gas joint-venture accounting, construction progress billing and Islamic finance. Start-ups such as ReconcileOS unbundle reconciliation and sell automation overlays at AED 599 per month, targeting enterprises hesitant to rip out legacy ERP cores. As regulations compress decision timelines, market concentration is trending upward, yet the long-tail of localized modules ensures plurality of offerings for the foreseeable future.

United Arab Emirates Cloud Accounting Software Industry Leaders

Intuit Inc.

Sage Group plc

Oracle Corporation

Odoo S.A.

Xero Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tally Solutions launched Tally Prime 7.0 with bilingual interfaces, automated VAT and corporate-tax reconciliation and support for the UAE’s new currency symbol.

- October 2025: du and Dubai SME introduced an AI-powered business-platform bundle with sovereign cloud hosting for 5,000 companies, scaling federation-wide in 2026.

- April 2025: Tally Solutions released Tally Prime 6.0, adding enhanced bank reconciliation and UAE-based data centers.

- October 2024: AWS and e& agreed to invest USD 1 billion to scale cloud infrastructure across the UAE and the Middle East, improving latency for SaaS accounting workloads.

United Arab Emirates Cloud Accounting Software Market Report Scope

Cloud accounting software refers to accounting software that is hosted on remote servers and accessed over the Internet. It allows businesses to manage their financial records, perform accounting tasks, and store financial data securely in the cloud rather than on a local computer or server. The Cloud accounting software offers several advantages, including real-time collaboration, automatic updates, and the ability to access financial data from anywhere with an internet connection.

The United Arab Emirates Cloud Accounting Software Market Report is Segmented by Size of Enterprise (Small and Medium Enterprises, Large Enterprises), Industry Vertical (BFSI, IT and Telecom, Retail and E-Commerce, Energy Oil and Gas, Real Estate and Construction, Other Industry Verticals), Deployment Model (Public Cloud SaaS, Private Cloud, Hybrid Cloud), Application (Invoicing and Billing, Payroll and HR, Inventory and Order Management, Tax and Compliance Management, Financial Reporting and Analytics), and Geography (Dubai, Abu Dhabi, Sharjah and Northern Emirates, Rest of United Arab Emirates). The Market Forecasts are Provided in Terms of Value (USD).

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| IT and Telecom |

| Retail and E-Commerce |

| Energy, Oil and Gas |

| Real Estate and Construction |

| Other Industry Verticals |

| Public Cloud SaaS |

| Private Cloud |

| Hybrid Cloud |

| Invoicing and Billing |

| Payroll and HR |

| Inventory and Order Management |

| Tax and Compliance Management |

| Financial Reporting and Analytics |

| By Size of Enterprise | Small and Medium Enterprises |

| Large Enterprises | |

| By Industry Vertical | BFSI |

| IT and Telecom | |

| Retail and E-Commerce | |

| Energy, Oil and Gas | |

| Real Estate and Construction | |

| Other Industry Verticals | |

| By Deployment Model | Public Cloud SaaS |

| Private Cloud | |

| Hybrid Cloud | |

| By Application | Invoicing and Billing |

| Payroll and HR | |

| Inventory and Order Management | |

| Tax and Compliance Management | |

| Financial Reporting and Analytics |

Key Questions Answered in the Report

How quickly will large corporations in the UAE migrate to cloud accounting?

Large enterprises are forecast to expand adoption at a 15.68% CAGR between 2026 and 2031, propelled by hybrid architectures that meet data-sovereignty rules while integrating global ERPs.

Which regulatory deadline influences most near-term purchase decisions?

The Federal Tax Authority will mandate structured e-invoicing for companies above AED 50 million (USD 13.61 million) turnover in January 2027, compressing purchasing cycles into an 18-month window.

Why are inventory modules growing faster than invoicing tools?

Omnichannel retailers want real-time stock visibility at checkout, driving a 15.71% CAGR for inventory and order-management applications through 2031.

What deployment model dominates among SMEs?

Public cloud SaaS leads because it eliminates infrastructure costs, capturing 65.42% of 2025 spend, though hybrid options are gaining as compliance demands rise.

Which emirate provides the highest revenue opportunity today?

Dubai contributes 44.6% of current revenue thanks to its concentration of free-zone headquarters, finance hubs and mature broadband networks.

How will sovereign-cloud fees impact micro-enterprises?

Hosting premiums of about 30% over global rates deter some SMEs, especially in the Northern Emirates, from fully migrating until subsidy programs become easier to access.

Page last updated on: