UAE Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

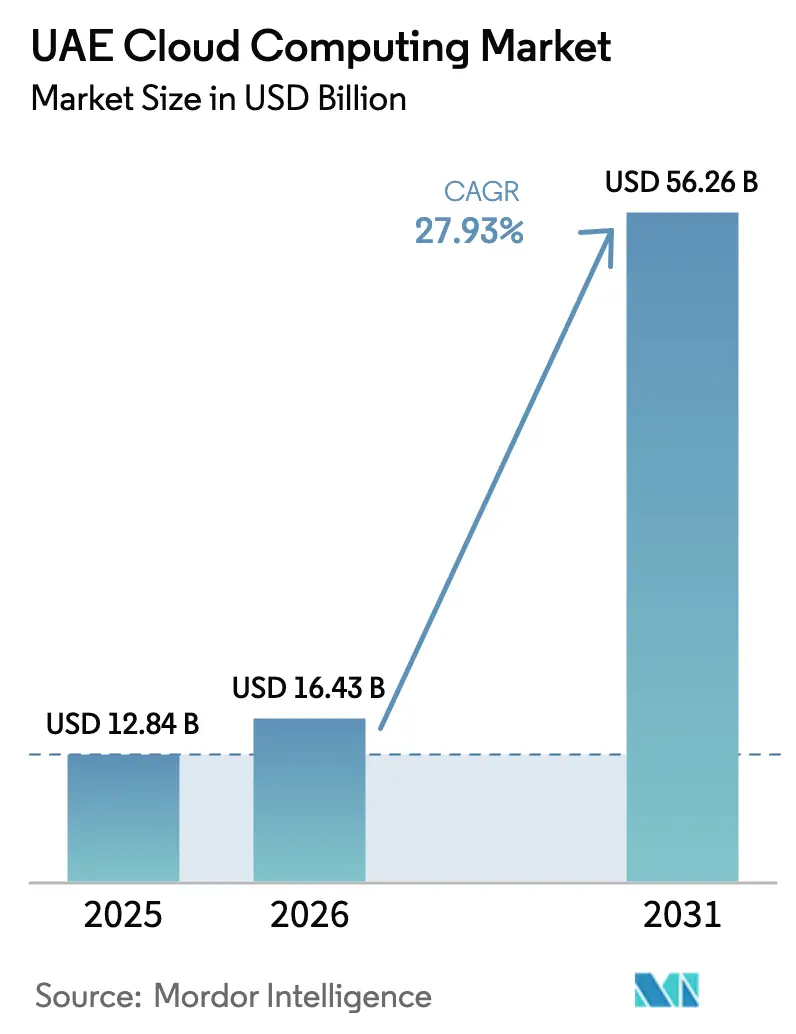

| Base Year Market Size (2025) | USD 12.84 Billion |

| Market Size (2026) | USD 16.43 Billion |

| Market Size (2031) | USD 56.26 Billion |

| Growth Rate (2026 - 2031) | 27.93% CAGR |

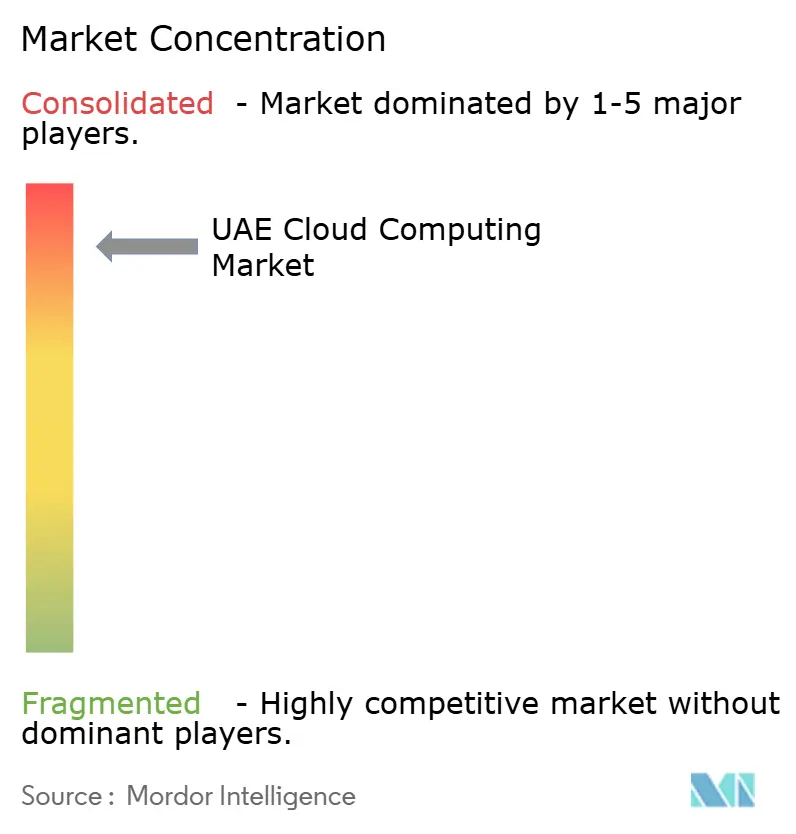

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Cloud Computing Market Analysis by Mordor Intelligence

The UAE cloud computing market size in 2026 is estimated at USD 16.43 billion, growing from 2025 value of USD 12.84 billion with 2031 projections showing USD 56.26 billion, growing at 27.93% CAGR over 2026-2031. Momentum stems from mandatory sovereign-cloud frameworks, aggressive AI infrastructure roll-outs, and energy-linked cost advantages that attract global hyperscalers. More than USD 10 billion in fresh capacity commitments from AWS, Microsoft, Oracle, Huawei, and STC have cut service latency to sub-10 milliseconds for domestic traffic and expanded the SKU catalogue, encouraging large banks, retailers, and ministries to decommission aging hardware. Cheap solar-nuclear power and 99% internet penetration amplify the commercial logic for migrating compute-heavy analytics and large language model (LLM) training into local zones. Cloud-first mandates worth AED 13 billion (USD 3.54 billion) anchor predictable public-sector consumption, while 5G-Advanced networks enable edge workloads for autonomous transport, smart utilities, and video streaming. The combination creates a self-reinforcing ecosystem in which capital, policy, and talent converge, accelerating workload migration into the UAE cloud computing market.

Key Report Takeaways

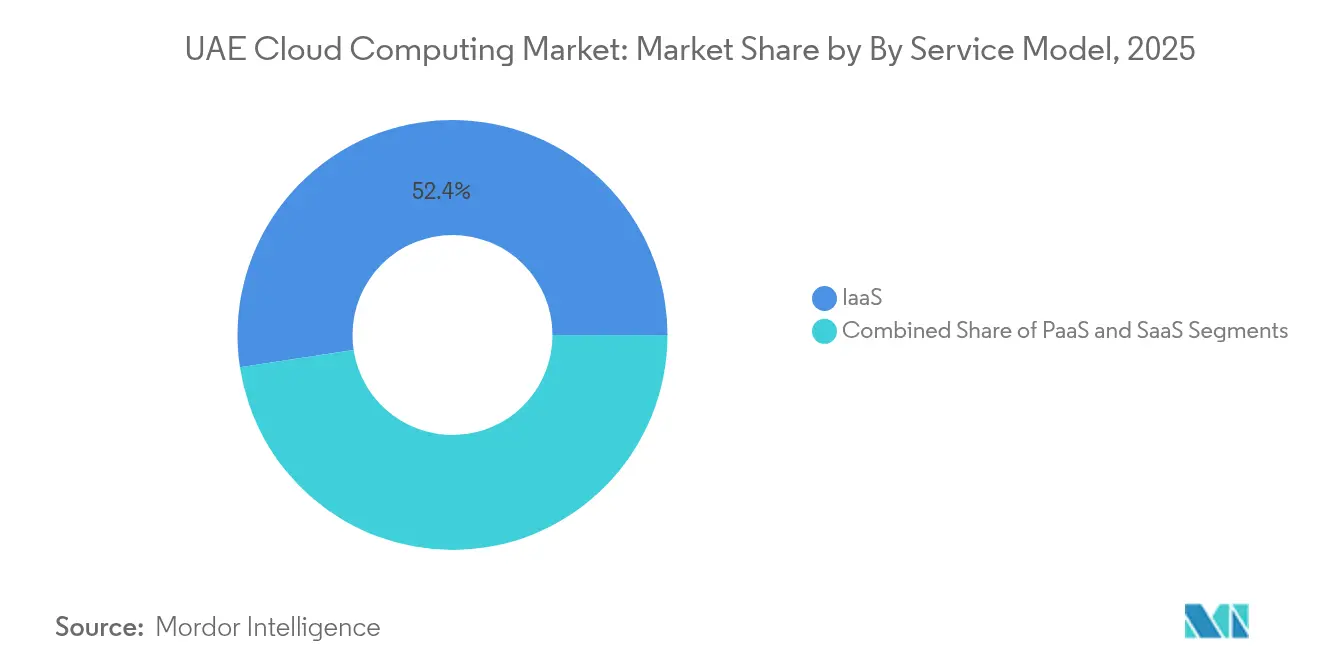

- By service category, Infrastructure-as-a-Service captured 52.40% of UAE cloud computing market share in 2025, whereas Platform-as-a-Service is forecast to outpace all other models at a 29.62% CAGR through 2031.

- By deployment type, the public-cloud segment accounted for 63.20% of UAE cloud computing market size in 2025; hybrid architectures will expand at a 31.45% CAGR, the fastest rate among all deployment options.

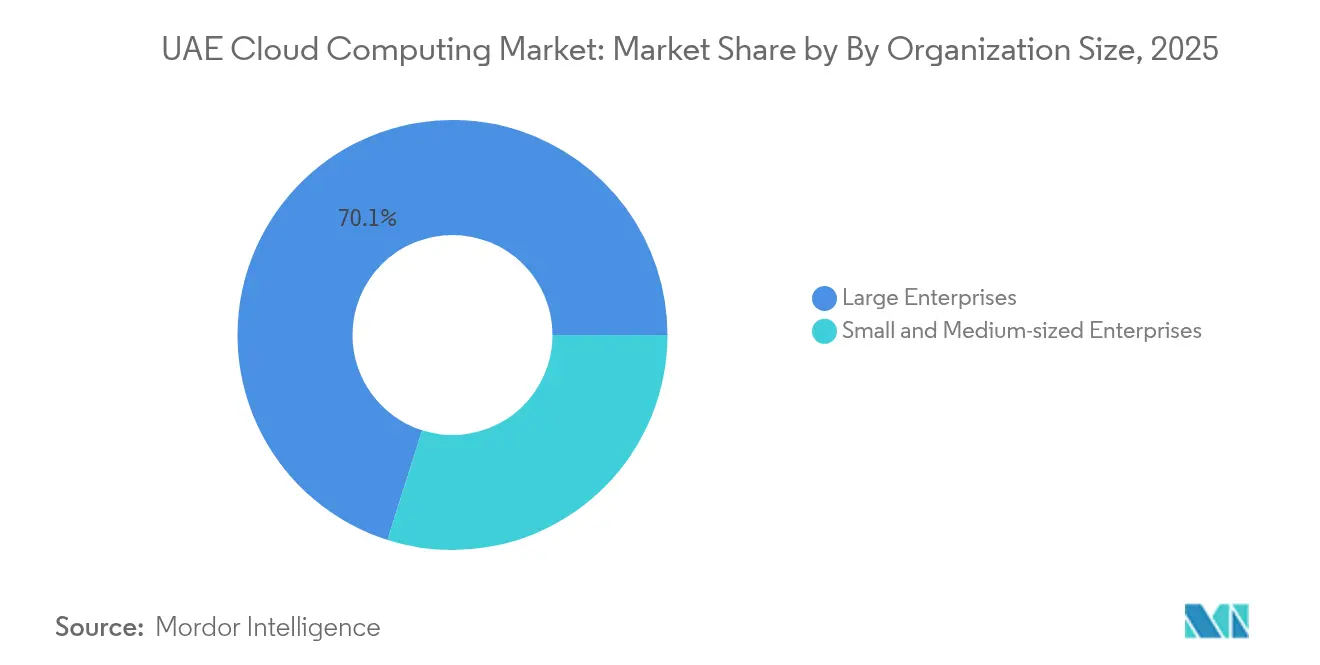

- By organisation size, large enterprises controlled 70.10% revenue in 2025, but SMEs represent the growth engine with a 30.05% CAGR projected to 2031.

- By vertical, BFSI led with 21.60% share of UAE cloud computing market size in 2025, while healthcare posts the highest forecast CAGR of 29.74% through 2031.

- AWS, Microsoft, Oracle, and G42 collectively surpassed 54.40% revenue share in 2025, underlining moderate consolidation within the UAE cloud computing market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's cloud computing market share coverage captures this comparative structure.

UAE Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Robust shift toward "cloud-first" government digital-economy mandates | +4.2% | National, with Abu Dhabi and Dubai leadership | Medium term (2-4 years) |

| Sovereign-cloud and data-residency rules boosting local hyperscale build-outs | +5.1% | National, with emphasis on free zones | Short term (≤ 2 years) |

| 5G-Advanced rollout triggering edge and multi-cloud spend | +3.8% | National coverage with urban concentration | Short term (≤ 2 years) |

| AI/LLM training workloads favouring UAE due to cheap solar-nuclear power | +6.3% | Abu Dhabi and Dubai focus areas | Long term (≥ 4 years) |

| "Green-cloud" procurement incentives for net-zero data centres | +2.1% | National, with renewable energy zones | Medium term (2-4 years) |

| 99% internet penetration and 5G-led bandwidth boom | +2.8% | National coverage with complete urban saturation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Shift Toward “Cloud-First” Government Digital-Economy Mandates

Abu Dhabi’s AED 13 billion Digital Strategy 2025-2027 requires every ministry to migrate 100% of mission-critical workloads to sovereign clouds, while Dubai stipulates cloud-native architectures for new Smart City services. The policy standardises procurement via TDRA’s IaaS catalogue, compressing tender cycles from quarters to weeks and ensuring sustained baseline throughput for providers. More than 200 AI use cases—from traffic-flow optimisation to e-court transcription—are scheduled, each demanding GPU-enabled clusters and compliant data-pipelines. Private contractors that integrate with federal APIs must therefore adopt compatible architectures, expanding addressable demand across the entire UAE cloud computing market.[1]UAE Government, “The UAE Digital Government Strategy 2025,” u.ae

Sovereign-Cloud and Data-Residency Rules Boosting Local Hyperscale Build-Outs

Federal Decree Law 45 of 2021 codifies data-residency while permitting controlled cross-border replication, triggering region launches by AWS, Azure, and Oracle that collectively exceed USD 10 billion. The AWS–e& USD 1 billion alliance delivers sovereign partitions, and Microsoft’s USD 1.5 billion stake in G42 underwrites AI-optimised sovereign regions. Capital intensity raises barriers for smaller entrants, nudging the UAE cloud computing market toward partner-driven consolidation and expanding multi-zone availability for enterprise failover.

5G-Advanced Rollout Triggering Edge and Multi-Cloud Spend

Nationwide 5G-Advanced coverage lowers round-trip latency below 10 ms, enabling mission-critical edge workloads in autonomous vehicles and smart-grid sensors. Du’s AED 2 billion hyperscale pact with Microsoft embeds edge micro-zones that cache content and run containerised workloads at the network edge. Firms now orchestrate data placement across core, regional, and edge layers, fuelling demand for orchestration platforms that manage multi-cloud and edge nodes seamlessly inside the UAE cloud computing market.

AI/LLM Training Workloads Favouring UAE Due to Cheap Solar-Nuclear Power

DEWA’s mixed solar-nuclear generation keeps power prices predictable and carbon intensity low, ideal for 24/7 GPU clusters that train trillion-parameter models. Stargate UAE, a 5 GW AI campus backed by SoftBank, OpenAI, Oracle, and NVIDIA, will house one of the world’s densest AI compute fabrics. Access to 500,000 NVIDIA chips annually positions the UAE as an attractive arbitration point for firms seeking lower power costs than Europe and faster provisioning than the United States, reinforcing the competitive edge of the UAE cloud computing market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Talent crunch in cloud-native and FinOps skill sets | -2.1% | National, with acute shortages in specialized roles | Long term (≥ 4 years) |

| Rising utility-scale power-availability bottlenecks for hyperscalers | -1.8% | Abu Dhabi and Dubai data center zones | Medium term (2-4 years) |

| Data-sovereignty overlap between Federal and Emirate-level regulators | -1.4% | National, with varying emirate interpretations | Medium term (2-4 years) |

| Vendor lock-in concerns among state-owned enterprises | -1.2% | Government and state-owned enterprise focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Talent Crunch in Cloud-Native and FinOps Skill Sets

Oracle’s pledge to train 350,000 professionals is significant yet insufficient, as demand grows faster than supply, particularly for FinOps and AI-ops engineers. Salary premiums reach 40%, and SMEs often pause projects due to unavailable senior architects. Dependence on overseas consultants inflates project TCO, delaying complex hybrid deployments inside the UAE cloud computing market.[2]“Oracle to train 350,000 people in AI and advanced digital technologies across the Middle East,” Zawya, zawya.com

Rising Utility-Scale Power-Availability Bottlenecks for Hyperscalers

While national generation capacity climbed 5.49% during 2024, 100 MW data halls cluster in a handful of industrial zones, straining substations and lengthening lead times for new grid interconnects. Operators negotiate multiyear power reservations, driving up real-estate costs and forcing some expansions into less optimal sites with higher latency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Category: IaaS Foundation Enables PaaS Acceleration

Infrastructure-as-a-Service contributed USD 6.73 billion in 2025, reflecting 52.40% UAE cloud computing market share as agencies retire on-premises mainframes. TDRA credits let ministries test workloads risk-free, accelerating IaaS uptake. Platform-as-a-Service, starting from USD 2.06 billion in 2025, is on course for 29.62% CAGR. Standardised PaaS menus priced at AED 30-161 monthly lure start-ups and dev-ops teams with serverless runtimes and CI/CD pipelines. Software-as-a-Service adoption expands as HR, ERP, and CRM move into multitenant environments, especially within manufacturing where Google Workspace saved Al Shirawi 30% on IT operations.

By Cloud Deployment Model: Public Cloud Dominance Amid Hybrid Acceleration

Public-cloud services delivered USD 8.11 billion in 2025, equal to 63.20% of UAE cloud computing market share. Larger availability zones, sovereign partitions, and cost-efficient PaaS bundles lower barriers for ministries and retailers alike. Hybrid cloud, though smaller today, is projected to exceed USD 16.28 billion by 2031 owing to a 31.45% CAGR as banks, utilities, and health-care providers adopt “local data, global scale” architectures. Private cloud remains pivotal for latency-sensitive trading systems and confidential citizen records but grows more slowly because standardized sovereign public services now satisfy most compliance templates.

By Organization Size: SME Revolution Transforms Market Dynamics

Large enterprises produced 70.10% of 2025 billings through complex multi-cloud estates and reserved-instance contracts. Yet SMEs will add more absolute net new revenue between 2026 and 2031 because their 30.05% CAGR outpaces all other segments. Programs such as AWS Connected Community, Dubai’s noon SME accelerator, and government MGX funds subsidise migration assessments and voucher schemes, injecting fresh users into the UAE cloud computing market. SaaS-first preferences among SMEs mean providers must bundle security, billing, and compliance in a single pane.

By End-User Industry: BFSI Leadership Amid Healthcare Transformation

Banks sustain 21.60% revenue thanks to real-time payments and open-banking APIs that demand elastic capacity. First Abu Dhabi Bank now processes over 90% of interactions through digital channels hosted on AWS and Azure clusters. Healthcare accelerates at 29.74% CAGR as AI radiology and tele-ICU platforms rely on sovereign GPU clouds built under the Oracle-Cleveland Clinic-G42 alliance. Manufacturing, retail, logistics, and education each expand at mid-twenties percentages, enabled by IoT telemetry, omnichannel commerce, and distance-learning portals. Utilities modernise SCADA and demand-response analytics, leveraging cloud-native microservices to balance renewable generation.

Geography Analysis

Abu Dhabi captures disproportionate sovereign and AI workloads due to its AED 13 billion digital programme and proximity to the Barakah nuclear plant, which supplies baseload power for GPU farms. Microsoft-G42 sovereign regions sit within the capital’s Mafraq corridor, providing ministries sub-5 ms latency. Dubai hosts the majority of commercial SaaS and content-delivery traffic, using its optical landing stations and free-zone incentives to attract global ISVs. The emirate’s du-Microsoft edge network embeds micro-zones inside 5G towers, facilitating AR/VR consumer experiences.

Ajman, Ras Al Khaimah, and Sharjah are next-tier beneficiaries. Khazna’s 100 MW AI-optimised campus in Ajman decentralises capacity, mitigating grid pressure in Dubai and providing regional redundancy. Cross-border spill-overs occur as Kuwaiti, Omani, and African SaaS vendors colocate in UAE POPs to satisfy latency SLAs without building domestic regions. Harmonising GCC data-protection rules further lowers expansion frictions, enabling UAE operators to export sovereign-cloud blueprints alongside managed services to neighbouring markets.

Analysis of the cloud computing market by Mordor Intelligence spans multiple other regional evaluations across South America, North America, and Europe, supported by country-level insights for Spain, France, Brazil, Canada, Japan, and China, wherein local market conditions keep varying from one country to another.

Competitive Landscape

AWS retains first-mover status through its e& alliance, combining telco last-mile reach with hyperscale economics. Microsoft fast-tracks parity by embedding Azure OpenAI services inside G42 sovereign clusters, offering GPU quotas unavailable in other EMEA regions. Oracle’s USD 30 billion annual G42 deal funnels customers seeking HPC-in-database advantages and end-to-end AI pipelines. Google leverages Anthos and low-carbon branding but trails in in-country zones. Huawei Cloud inks government security contracts yet faces advanced-chip supply friction.

Core42 emerges from the G42-Injazat-Inception merger, pitching confidential compute atop AMD EPYC processors for regulated verticals. Du and STC pivot to platform brokers, bundling fintech APIs with managed Kubernetes and FinOps dashboards. New niche entrants exploit vertical white spaces—such as med-tech cloud or defence-grade SaaS—though capital hurdles remain high because sovereign-cloud compliance demands minimum dual-availability-zone presence within the UAE cloud computing market.

UAE Cloud Computing Industry Leaders

Amazon.com Inc.

Microsoft Corporation

Google LLC

Oracle Corporation

Alibaba Group Holding Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: OpenAI, Oracle, NVIDIA, Cisco, and SoftBank launched Stargate UAE, a 5 GW AI cluster slated to go live in 2026.

- April 2025: du inked a AED 2 billion (USD 544 million) hyperscale data-center pact with Microsoft to accelerate Dubai’s AI-cloud ambitions.

- March 2025: ADQ partnered with ECP on USD 25 billion data-center energy projects to bolster regional AI infrastructure.

- January 2025: e& and AWS finalized a USD 1 billion six-year alliance to drive nationwide cloud adoption and upskill local talent.

UAE Cloud Computing Market Report Scope

Cloud computing delivers computing services via the internet, encompassing servers, storage, databases, networking, software, analytics, and intelligence. This approach fosters quicker innovation, adaptable resources, and economies of scale. Typically, customers pay solely for the cloud services they utilize, leading to reduced operational costs, more efficient infrastructure management, and the ability to scale in line with evolving business needs.

The UAE cloud computing market report is segmented by type (public cloud [ IaaS, Paas, Saas], private cloud, hybrid cloud), and by organization size (SMEs, large enterprises), and by end-user industries (manufacturing, education, retail, transportation, and logistics, healthcare, BFSI, telecom and IT, government and public sector, and others including utilities, media & entertainment, etc.). The market sizes and forecasts are provided in terms of value (USD) for all segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| BFSI |

| Government and Public Sector |

| Healthcare |

| Retail and E-commerce |

| Telecom and IT Services |

| Manufacturing |

| Transportation and Logistics |

| Education |

| Others (Utilities, Media and Entertainment) |

| ERP / Core Enterprise Apps |

| AI / ML and Data-analytics |

| IoT and Edge Computing |

| Disaster-Recovery / BCDR |

| Content and Media Streaming |

| By Cloud Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Category | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| By Organisation Size | Small and Medium-sized Enterprises |

| Large Enterprises | |

| By End-user Industry | BFSI |

| Government and Public Sector | |

| Healthcare | |

| Retail and E-commerce | |

| Telecom and IT Services | |

| Manufacturing | |

| Transportation and Logistics | |

| Education | |

| Others (Utilities, Media and Entertainment) | |

| By Workload / Use-case | ERP / Core Enterprise Apps |

| AI / ML and Data-analytics | |

| IoT and Edge Computing | |

| Disaster-Recovery / BCDR | |

| Content and Media Streaming |

Key Questions Answered in the Report

What is the projected value of the UAE cloud computing market by 2031?

The market is expected to reach USD 56.26 billion by 2031 at a 27.93% CAGR.

Which deployment model is growing fastest?

Hybrid cloud leads with a 31.45% CAGR as firms balance compliance and flexibility.

Why are AI workloads clustering in the UAE?

Access to 500,000 NVIDIA GPUs and low-cost solar-nuclear power make the UAE cost-effective for large-scale training.

How significant is the SME segment?

SMEs post a 30.05% CAGR thanks to subsidised migration vouchers and SaaS-first adoption pathways.

What share does BFSI hold in the market?

BFSI accounted for 21.60% of revenue in 2025, driven by real-time payment and regulatory digitalisation.

What are the key restraints hindering growth?

A talent shortage in cloud-native skills, power-availability constraints for hyperscalers, overlapping data-sovereignty rules, and vendor lock-in concerns are the main challenges impacting market momentum.

Page last updated on: