Canada Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

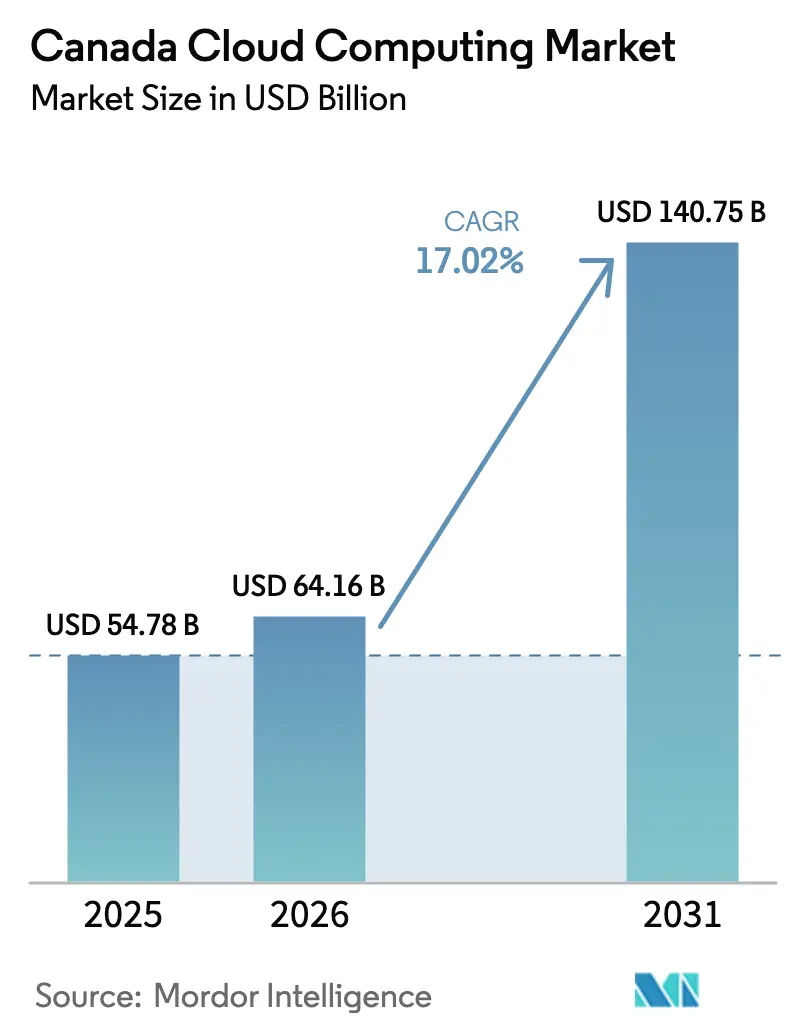

| Base Year Market Size (2025) | USD 54.78 Billion |

| Market Size (2026) | USD 64.16 Billion |

| Market Size (2031) | USD 140.75 Billion |

| Growth Rate (2026 - 2031) | 17.02% CAGR |

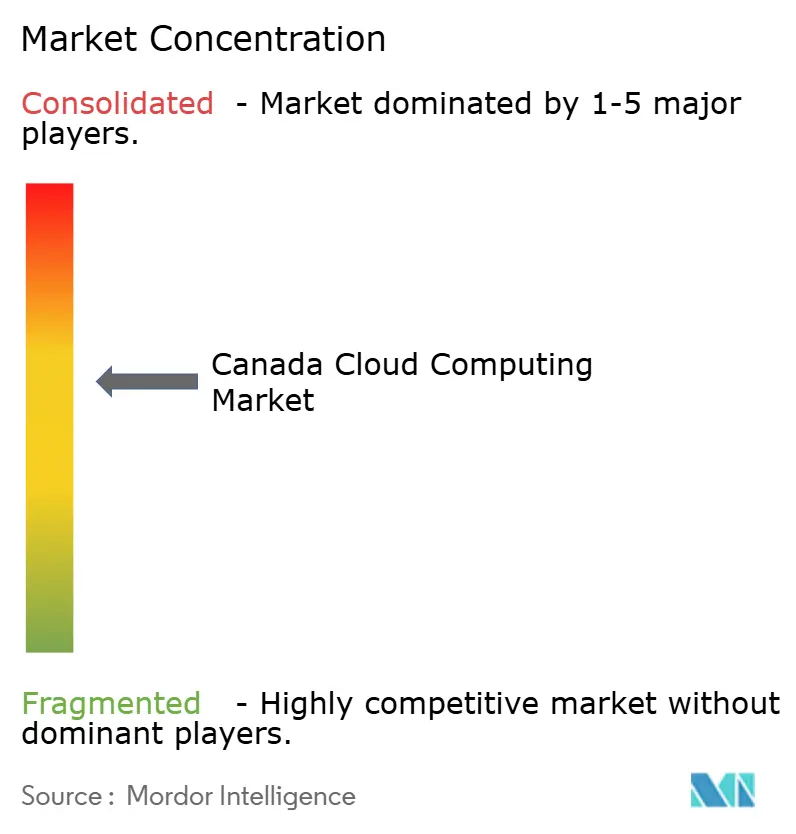

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Cloud Computing Market Analysis by Mordor Intelligence

Canada Cloud Computing Market size in 2026 is estimated at USD 64.16 billion, growing from 2025 value of USD 54.78 billion with 2031 projections showing USD 140.75 billion, growing at 17.02% CAGR over 2026-2031. Mandatory digital-first programs, a USD 2.4 billion federal AI compute plan, and sustained provincial incentives for sovereign data centres are driving large-scale migration to public, private, and hybrid clouds.[1]Innovation, Science and Economic Development Canada, “Canadian Sovereign AI Compute Strategy,” ised-isde.canada.ca Growing AI and machine-learning workloads, combined with permanent remote-hybrid work, are accelerating demand for hyperscale GPU capacity and low-latency collaboration platforms. Ontario anchors national cloud spend, yet Alberta’s clean-energy advantage is fuelling the fastest datacentre buildout, signalling geographic diversification of cloud assets. Continued skills shortages in cloud engineering and AI specialisations remain a material brake on growth despite targeted immigration streams for STEM talent.

Key Report Takeaways

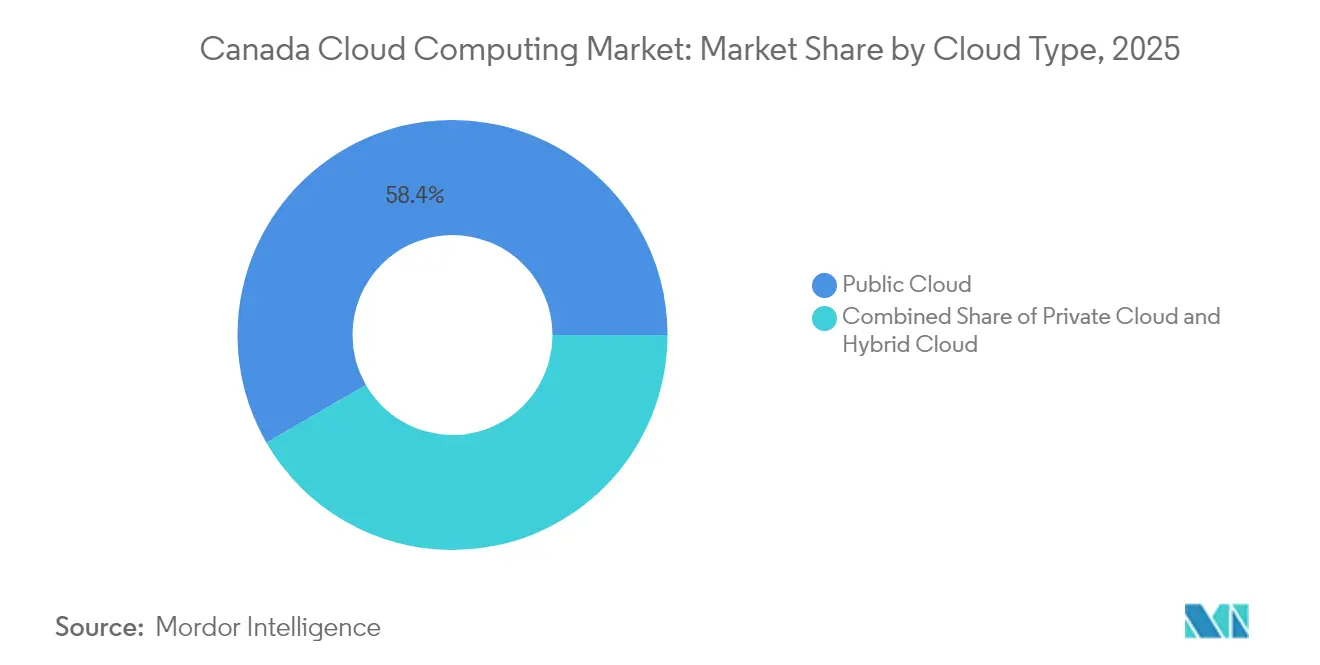

- By cloud type, public cloud led with 58.35% revenue share in 2025, while hybrid cloud is projected to expand at a 19.94% CAGR through 2031.

- By service model, SaaS captured 46.05% of the segment in 2025; IaaS is forecast to grow at 21.38% CAGR to 2031.

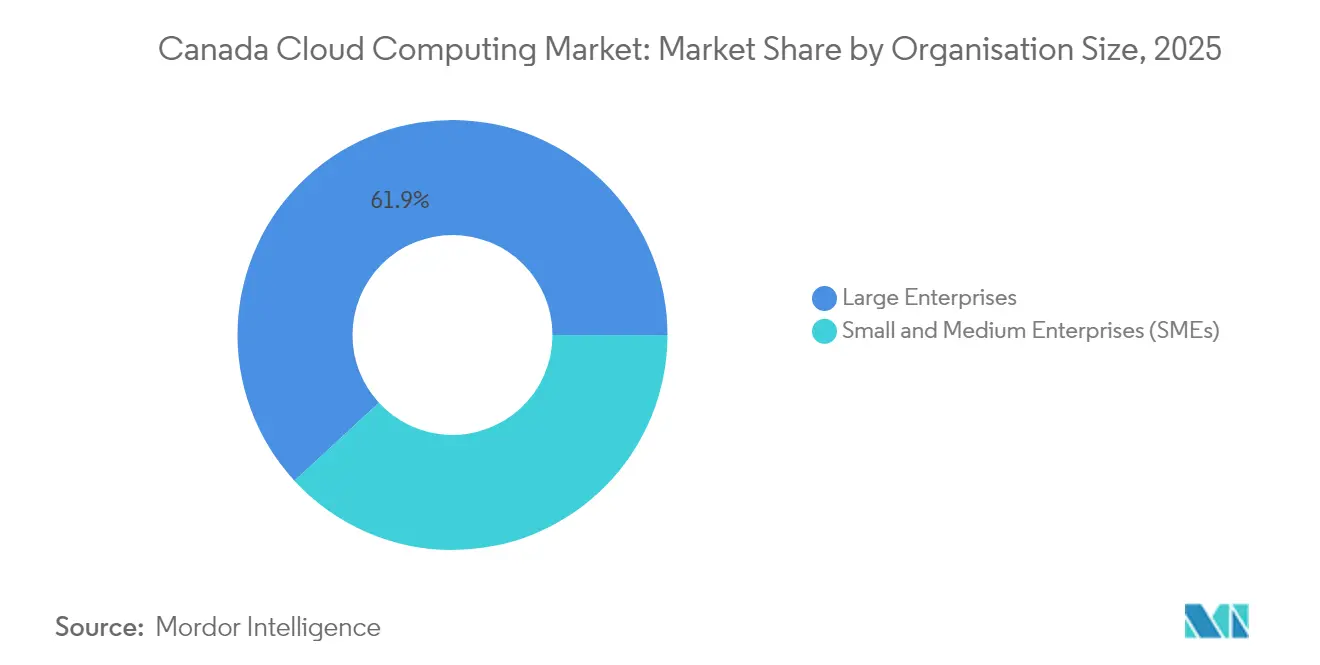

- By organisation size, large enterprises held 61.85% of the Canada cloud computing market share in 2025, whereas SMEs record the highest projected CAGR at 17.92% through 2031.

- By end-user industry, BFSI accounted for 23.65% share of the Canada cloud computing market size in 2025; healthcare and life sciences advances at a 20.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Canada representing one among them. The global report on cloud computing market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Canada Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise-wide digital transformation momentum | +4.2% | National, strongest in Ontario and Quebec | Medium term (2–4 years) |

| Shift to permanent remote-hybrid work | +3.1% | National, led by major urban centres | Short term (≤2 years) |

| Green data-centre incentives from federal and provincial programs | +2.8% | Alberta, British Columbia, Quebec | Long term (≥4 years) |

| Rising AI/ML workloads needing hyperscale GPUs | +5.4% | Alberta, Ontario, British Columbia | Medium term (2–4 years) |

| Increasing demand for francophone SaaS localisation | +1.8% | Quebec, extending to New Brunswick | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Robust Shift Toward Enterprise-Wide Digital Transformation

Canada’s transformation agenda now ties cloud adoption to measurable service-delivery gains such as the federal target to halve processing times for priority services.[2]Benjamin Alarie, “Make Canadian Government Services AI-First,” buildcanada.com Full subscription of the Canada Digital Adoption Program shows that 160,000 SMEs view cloud migration as the fastest path to competitiveness. Large incumbents including Bell Canada re-positioned from connectivity to AI-enabled solutions, illustrating that digital capability is replacing cost efficiency as the core differentiator. Manufacturing SMEs are embedding sustainability metrics into digital roadmaps because 63% of sectoral employment depends on technology adoption that also meets environmental goals. As a result, the Canada cloud computing market is moving from discretionary IT spending to a foundational element of business resilience and revenue generation.

Permanent Remote-Hybrid Workforce Paradigm

Hybrid work has pushed agencies to cloud-first architectures that support distributed collaboration while meeting strict cybersecurity rules.[3]Treasury Board of Canada Secretariat, “Canada’s Digital Ambition 2023-24,” tbs-sct.canada.ca Partnerships such as Microsoft-Seneca Polytechnic show education using Azure AI to weave cloud into curricula rather than treating it as peripheral infrastructure. Federal HR systems migrated to Ceridian Dayforce SaaS, proving that complex payroll environments can modernise securely in multi-tenant cloud. Organisations now demand low-latency services, layered security, and compliance tooling to make remote work sustainable beyond the pandemic window. Consequently, the Canada cloud computing market is seeing rising demand for integrated collaboration stacks and zero-trust architectures that scale seamlessly as workforces remain location-agnostic.

Federal & Provincial Green-Data-Centre Incentives

Alberta’s Wonder Valley AI Data Centre Park, a USD 70 billion project with 7.5 GW capacity, exemplifies alignment of clean energy resources with AI compute demand.[4]Major Projects Alberta, “Wonder Valley AI Data Centre Park,” majorprojects.alberta.ca The federal USD 160 billion net-zero investment roadmap strengthens renewable build-outs that lower operating costs for hydro and geothermal-powered facilities. Utilities such as Hydro One and BC Hydro are advancing smart-grid and virtual power plant programs that accommodate cloud-scale loads while reducing carbon intensity. This confluence makes sustainability a purchasing criterion, influencing hyperscaler region selection and catalysing hybrid deployments anchored in green provinces. Hence, clean-energy policy is increasingly intertwined with Canada cloud computing market expansion.

Surge in AI/ML Workload Demand for Hyperscale GPUs

Bell’s 500 MW AI Fabric network, Canada’s largest sovereign compute cluster, signals rapid build-out of GPU-rich infrastructure dedicated to AI training and inference. Ottawa’s USD 2.4 billion Sovereign AI Compute Strategy directly tackles the country’s absence of G7-class supercomputers, funnelling USD 300 million into an access fund for businesses. Data-center electricity demand is projected to rise 160% by 2030 as training cycles double energy use roughly every nine months. Alberta’s phased connection plan offers 1,200 MW grid capacity earmarked for AI-centric facilities, confirming provincial commitment to address power bottlenecks. These factors make AI-ready infrastructure the fastest growing revenue pool in the Canada cloud computing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex data-residency regulations across jurisdictions | –2.9% | National, highest complexity in Quebec and Alberta | Long term (≥4 years) |

| Shortage of cloud skills and specialised talent | –3.7% | National, centred in major urban hubs | Medium term (2–4 years) |

| Rising electricity and cooling costs in key provinces | –1.6% | Ontario, Quebec; Alberta relatively resilient | Short term (≤2 years) |

| Vendor lock-in risk under sovereign resilience mandates | –2.1% | National, acute in government and regulated sectors | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Complex Federal-Provincial Data-Residency Regulations

Overlapping rules between federal PIPEDA and provincial privacy acts force multi-jurisdictional architectures, raising compliance cost and design complexity. Government cloud guardrails for Protected B workloads stipulate baseline controls within 30 days of account creation, influencing provider onboarding workflows. Cross-border data transfer friction linked to U.S. Patriot Act concerns adds an extra compliance layer for multinational firms. These issues push enterprises toward hybrid strategies but can slow decision cycles and inflate total cost of ownership in the Canada cloud computing market.

Acute Cloud-Skills & Talent Shortage

Government reports cite persistent shortages in cloud infrastructure, security, and AI engineering, prompting targeted STEM immigration streams and national reskilling programs. The Cloud Skills Adoption pilot seeks to plug immediate gaps, yet demand for quantum-ready, edge, and AI-integrated cloud services outstrips supply. Enterprises increasingly rely on managed services, which solves short-term skill deficits but may lock customers into vendor-controlled environments and raise long-run switching costs. The talent gap therefore applies downward pressure on the projected growth trajectory of the Canada cloud computing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cloud Type: Hybrid Architectures Drive Sovereignty Balance

Hybrid deployments recorded the fastest 19.94% CAGR as firms balanced global scalability and domestic data sovereignty mandates, while public cloud still delivered 58.35% revenue in 2025. The Canada cloud computing market size for hybrid solutions is projected to expand sharply as regulated entities layer private zones over hyperscaler regions. Telecommunications carriers exploit fibre and tower footprints to launch hybrid offerings that segment sensitive versus elastic workloads. In parallel, sovereign clouds operated by Bell and eStruxture are winning mandates that require strict jurisdictional control. Demand for workload portability and multi-cloud optimisation positions hybrid as the de-facto default over pure public or private strategies.

Private cloud retains traction for high-security workloads in defence and crown corporations. Yet the shifting regulatory environment, combined with AI compute intensity, is coaxing those users toward hybrid extensions rather than full on-prem refresh cycles. The interplay of compliance, performance, and cost is reshaping provider roadmaps and keeps the phrase Canada cloud computing market at the forefront of board-level discussions.

By Service Model: Infrastructure Acceleration Supports AI Workloads

SaaS captured 46.05% revenue in 2025, yet IaaS is accelerating at 21.38% CAGR as enterprises seek GPU clusters and high-throughput networking for model training. The Canada cloud computing market size for high-performance IaaS is forecast to more than double by 2031 as federal grants subsidise compute-intensive research. PaaS gains traction in DevOps pipelines, though its growth pace lags IaaS because AI workloads still favour direct infrastructure control. Function-as-a-Service uptake rises in telco edge deployments where event-driven microservices power 5G applications.

Hyperscalers integrate vertical AI accelerators, while telcos bundle managed Kubernetes and networking to capture mid-market demand. Such differentiation underlines how service-model choices are becoming workload-specific rather than blanket decisions, reinforcing the heterogeneity of the Canada cloud computing market.

By Organisation Size: SME Growth Accelerates Through Government Support

Large enterprises held 61.85% revenue share, leveraging sophisticated hybrid stacks and multi-cloud governance frameworks. However SMEs expand at 17.92% CAGR thanks to grants up to USD 15,000 and interest-free loans through the CDAP program. Simplified portals, pay-as-you-grow tariffs, and bundled security services reduce adoption friction. Providers localise onboarding content, recognising linguistic diversity across the Canada cloud computing industry.

SMEs initially consume SaaS for accounting and e-commerce, but rising familiarity triggers migration to IaaS and PaaS for analytics and AI use cases. This bottom-up expansion diversifies revenue streams and mitigates reliance on a handful of large enterprise contracts in the Canada cloud computing market.

By End-User Industry: Healthcare Transformation Drives Fastest Growth

BFSI kept its 23.65% revenue lead in 2025, reliant on low-latency trading platforms and stringent compliance controls. Healthcare and life sciences, growing 20.92% CAGR, benefit from interconnected EHR systems reaching 93% clinician adoption in Ontario. Cloud-enabled digital twins, remote monitoring for 16,000 patients, and AI-supported diagnostics push demand for secure, HIPAA-aligned environments. The segment’s outsized growth keeps the Canada cloud computing market share for healthcare rising each year.

Manufacturing leverages cloud-powered Industry 4.0, while government digital ambitions generate steady SaaS consumption. Telecom operators themselves are heavyweight buyers of cloud to support 5G core and edge nodes, highlighting virtuous self-consumption within the Canada cloud computing market.

Geography Analysis

Ontario anchors the Canada cloud computing market through its concentration of banks, insurers, federal agencies, and a mature provider ecosystem that demands low-latency, high-compliance cloud zones. Toronto’s financial district pushes hybrid architectures geared toward real-time analytics, expanding spend on multi-region disaster recovery strategies. Healthcare cloud uptake in the province surged as remote monitoring programs managed tens of thousands of patients, proving that clinical workloads can run securely in the public cloud while meeting privacy statutes.

Alberta’s rapid 19.18% CAGR reflects deliberate provincial policy aligning energy abundance with AI infrastructure needs. The province’s USD 70 billion Wonder Valley park and a 1.8 GW Pembina-Kineticor power plant underscore a pivot from hydrocarbons to digital energy exports. AESO’s phased connection plan further validates that grid planning is now cloud-centric. Private investors such as eStruxture commit USD 750 million to new Calgary capacity, signalling confidence in Alberta’s long-term role in the Canada cloud computing market.

Quebec leverages hydro power and localisation mandates to capture francophone-focused workloads. Provincial subsidies for French digital content create a specialised SaaS sub-segment requiring local data processing and support. British Columbia benefits from Asia-Pacific latency corridors, with Bell’s AI Fabric network using hydroelectricity to deliver sovereign AI compute at scale. Smaller provinces pursue niche opportunities in agriculture tech and maritime logistics, gradually lifting national coverage. Together these dynamics sustain diversified geographic demand, reinforcing the resilience of the Canada cloud computing market against regional policy or energy shocks.

Mordor Intelligence provides coverage of the cloud computing market across other key regional markets, including North America, Europe, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, Brazil, France, China, United Kingdom, and Germany incorporating local coverage and market participation, as required.

Competitive Landscape

Competition in the Canada cloud computing market is moderate, led by hyperscalers AWS, Microsoft, and Google, each operating multiple Canadian regions with dedicated compliance certifications. Domestic telcos are closing capability gaps by converting fibre, spectrum, and colo assets into cloud platforms. Bell’s USD 500 million AI Fabric places 500 MW sovereign GPU capacity across six B.C. sites, representing the boldest challenge yet to hyperscaler AI dominance. Telus and Rogers pursue Open RAN and edge cloud strategies to monetise 5G traffic by bundling compute with connectivity.

White-space opportunities revolve around industry-specific compliance. Healthcare cloud remains underserved due to privacy nuance, opening room for niche providers offering turnkey, HIPAA-aligned platforms. Francophone SaaS localisation similarly differentiates regional vendors able to embed cultural and legislative requirements into product design. Integration with AI accelerators is another battleground: Microsoft’s work with BMO on Azure OpenAI underwriting shows how cloud-native AI services can cement long-term enterprise stickiness.

Edge computing specialists and GPU-as-a-service startups add competitive pressure, offering pay-per-minute training cycles without full cloud migration. Energy utilities are also entering the field by pairing smart-grid services with on-prem cloud appliances, especially in regions targeting net-zero data centres. Consequently, success in the Canada cloud computing market now hinges on a mix of sovereign capacity, regulatory fluency, and vertical AI solution depth rather than pure scale economics.

Canada Cloud Computing Industry Leaders

Amazon Web Services, Inc

Google LLC

Microsoft Corporation

IBM Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bell Canada launched Bell AI Fabric, a USD 500 million program establishing 500 MW hydro-powered AI data centres in British Columbia.

- March 2025: Ottawa unveiled the Canadian Sovereign AI Compute Strategy with USD 2.4 billion over five years, including a USD 300 million access fund for businesses.

- March 2025: Pembina and Kineticor formed a JV to build a 1.8 GW natural-gas facility dedicated to data centre power in Alberta.

- February 2025: Bell and Nokia expanded a 5G alliance to include cloud and Open RAN deployments nationwide.

Canada Cloud Computing Market Report Scope

Cloud computing is the supply of computing services over the internet, including servers, storage, databases, networking, software, analytics, and intelligence to provide quicker innovation, adaptable resources, and scale economies. Customers usually only pay for their cloud services, which helps save operational costs, run infrastructure more effectively, and scale as business requirements change.

The Canadian cloud computing market is segmented by type (public cloud [IaaS, PaaS, and SaaS], private cloud, and hybrid cloud), organization size (SMEs and large enterprises), and by end-user industries (manufacturing, education, retail, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and other end-user industries (utilities, media & entertainment, etc.). The market sizes and forecasts are provided in terms of value in USD for all segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| IaaS |

| PaaS |

| SaaS |

| FaaS / Serverless |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing |

| Telecom and IT |

| Government and Public Sector |

| Energy and Utilities |

| Education |

| Media and Entertainment |

| Others |

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Cloud Type | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | IaaS |

| PaaS | |

| SaaS | |

| FaaS / Serverless | |

| By Organisation Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-user Industry | BFSI |

| Healthcare and Life Sciences | |

| Manufacturing | |

| Telecom and IT | |

| Government and Public Sector | |

| Energy and Utilities | |

| Education | |

| Media and Entertainment | |

| Others | |

| By Province | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Key Questions Answered in the Report

What is the current value of the Canada cloud computing market?

The market is valued at USD 64.16 billion in 2026 and is projected to reach USD 140.75 billion by 2031.

Which cloud type is growing fastest in Canada?

Hybrid cloud leads growth with a 19.94% CAGR as enterprises balance global scalability with data-residency rules.

Why is Alberta attracting hyperscale data centres?

Alberta offers abundant low-cost energy, a USD 100 billion provincial AI infrastructure plan, and grid connection programs tailored to data-centre loads.

How is government policy influencing cloud adoption among SMEs?

The Canada Digital Adoption Program provides grants and loans that lower the cost of migration, driving an 17.92% CAGR in SME cloud spending.

Which industry vertical shows the highest cloud growth rate?

Healthcare and life sciences expand at 20.92% CAGR due to electronic health records, remote monitoring, and AI-enabled diagnostics.

Page last updated on: