China Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

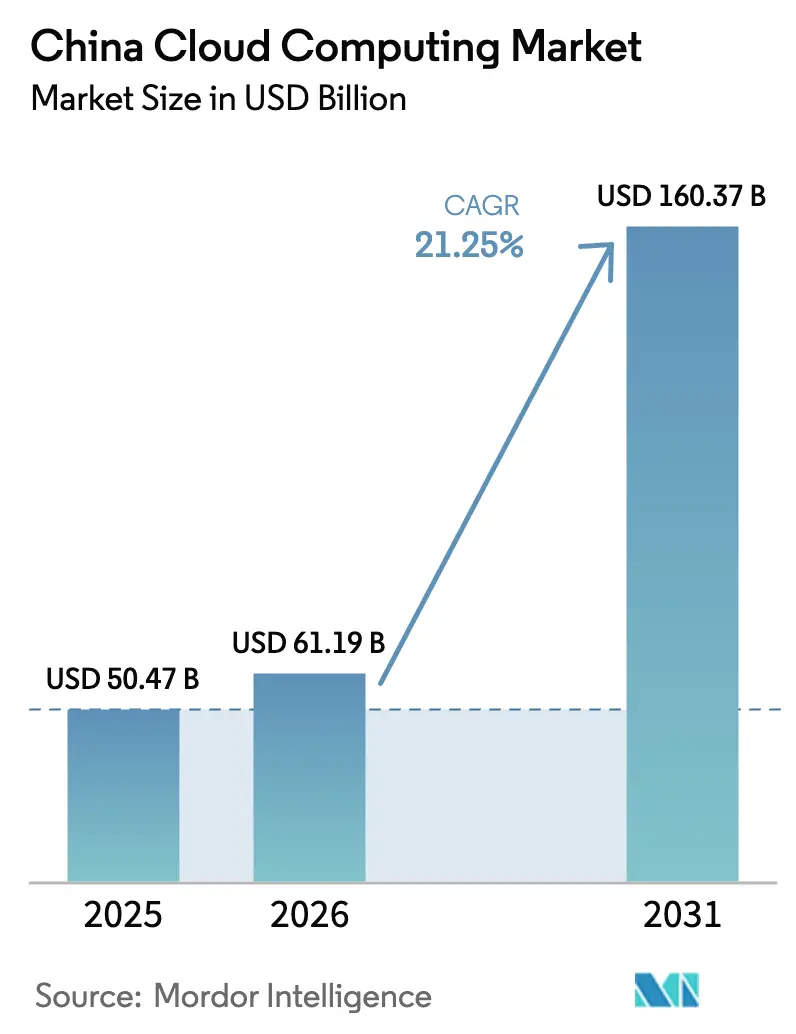

| Base Year Market Size (2025) | USD 50.47 Billion |

| Market Size (2026) | USD 61.19 Billion |

| Market Size (2031) | USD 160.37 Billion |

| Growth Rate (2026 - 2031) | 21.25% CAGR |

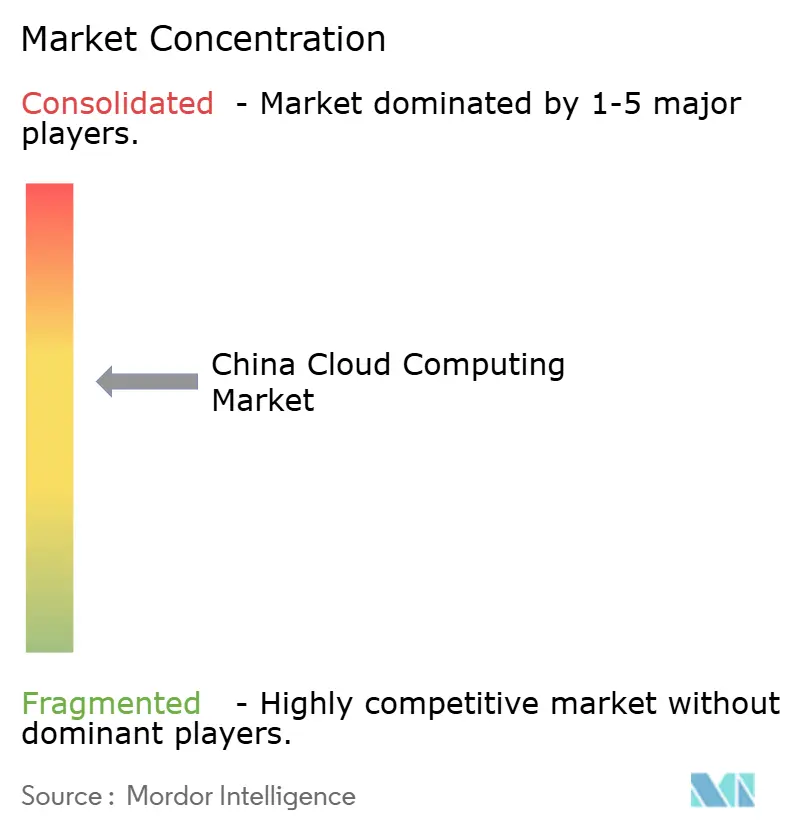

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Cloud Computing Market Analysis by Mordor Intelligence

China Cloud Computing Market size market size in 2026 is estimated at USD 61.19 billion, growing from 2025 value of USD 50.47 billion with 2031 projections showing USD 160.37 billion, growing at 21.25% CAGR over 2026-2031. Accelerated state-backed digital transformation, surging demand for AI-native workloads, and large-scale investments in renewable-powered data centers underpin this expansion, positioning China as the world’s fastest-growing cloud region. Public cloud still dominates the deployment mix, yet hybrid and multi-cloud strategies are scaling quickly as enterprises pursue sovereignty-compliant solutions while tapping public-cloud elasticity. Energy-intensive data center build-outs have pushed national electricity consumption for cloud infrastructure up 31% year-on-year, intensifying demand for efficient power and cooling systems. The Eastern Data, Western Computing program is re-shaping geographic distribution by shifting high-density workloads toward renewable-rich western provinces, thereby alleviating grid strain in coastal cities and lowering carbon footprints. Competitive intensity is rising as telecom-backed providers double revenue, triggering price wars that hasten enterprise adoption but compress vendor margins. Meanwhile, January 2025 data-security regulations are tightening compliance demands and steering customers toward domestic vendors.

Key Report Takeaways

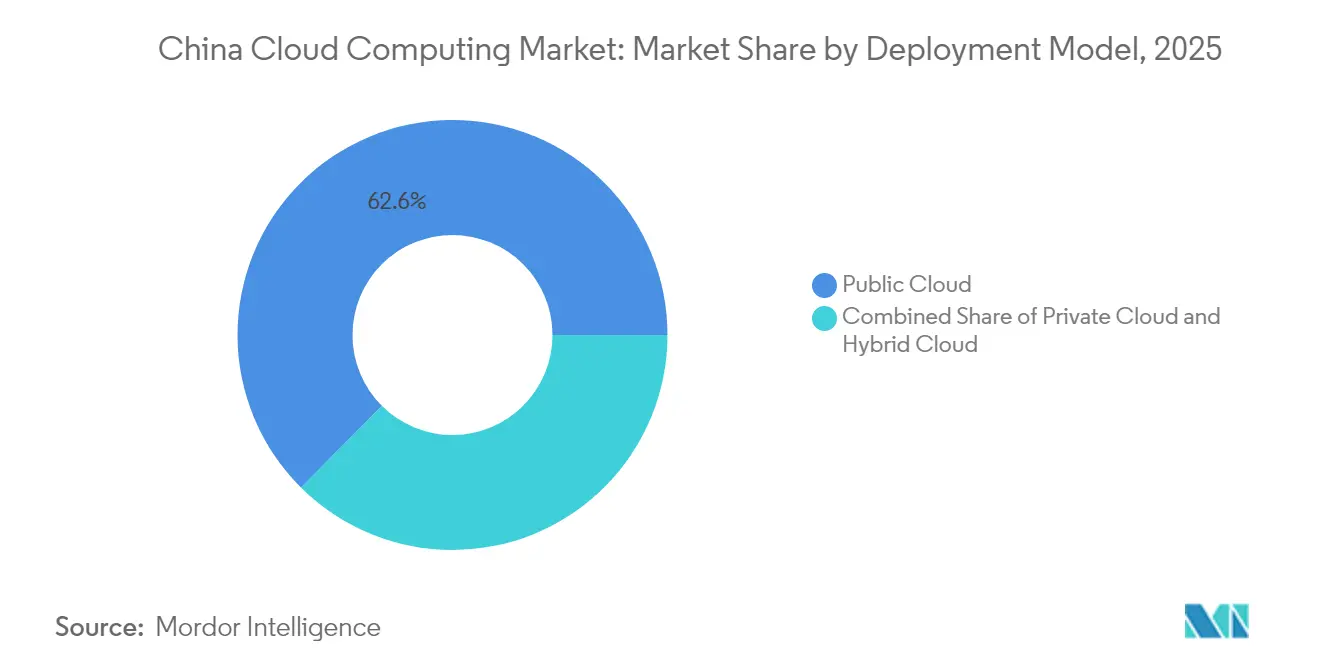

- By deployment model, Public Cloud led with 62.55% revenue share in 2025, while Hybrid/Multi-Cloud is forecast to expand at a 24.2% CAGR through 2031.

- By service model, Infrastructure-as-a-Service accounted for 67.40% of the China cloud computing market share in 2025; Platform-as-a-Service is projected to grow at 30.7% CAGR to 2031.

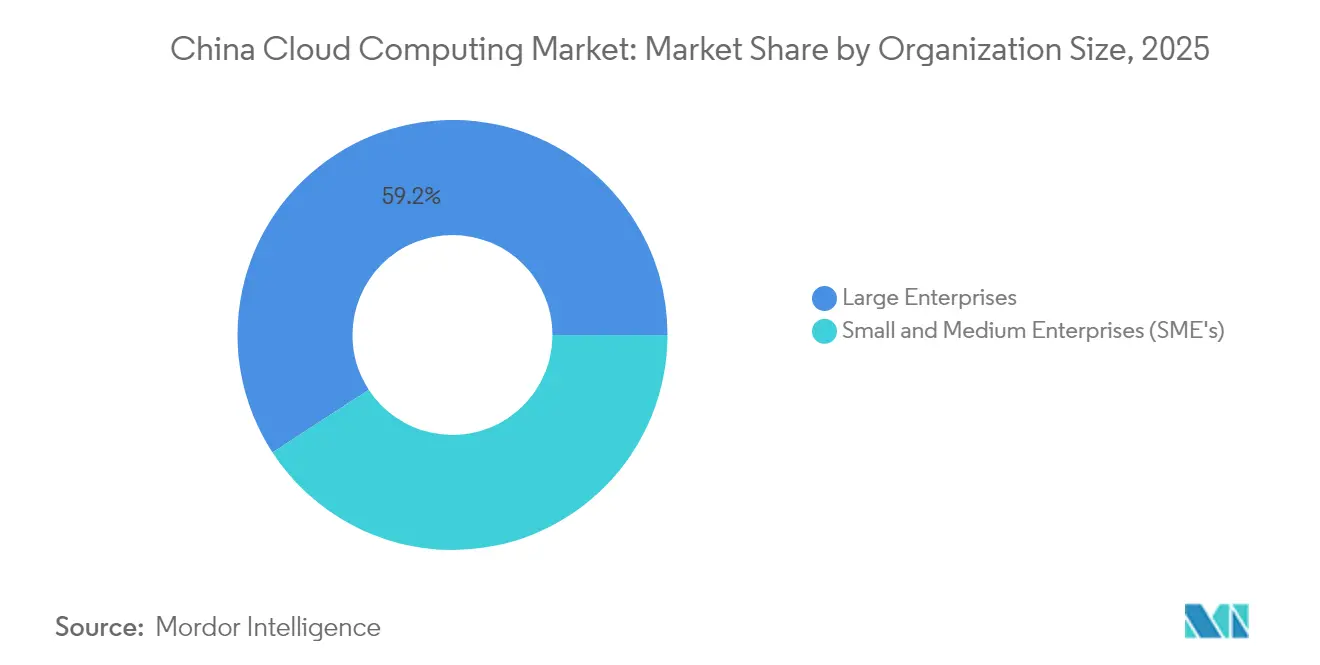

- By organization size, Large Enterprises held 59.20% of the China cloud computing market size in 2025; the SME segment is advancing at a 23.8% CAGR between 2026-2031.

- By end-user industry, Internet & Tech captured 25.20% of 2025 revenues, while Industrial Manufacturing is set to expand at a 27.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China participates in a competitive field that extends beyond its own borders. The market landscape in the global cloud computing industry outlined by Mordor Intelligence covers that wider structure.

China Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Digital-Transformation Spend by SOEs and Municipalities | +4.2% | Nationwide, especially tier-1 cities | Medium term (2-4 years) |

| AI-Native Workloads Demanding Elastic GPU Clouds | +6.8% | East and North China, spreading inland | Short term (≤2 years) |

| State-Backed “Eastern Data, Western Computing” Hub Build-Out | +3.5% | Central and West China, benefits felt country-wide | Long term (≥4 years) |

| Industrial-Internet Pilots in Discrete and Process Manufacturing | +2.9% | Coastal manufacturing belts, expanding nationwide | Medium term (2-4 years) |

| Cloud price wars lowering total cost for late adopters | +2.1% | Nationwide, stronger pull in tier-2/3 cities | Short term (≤2 years) |

| Carbon-peaking goals steering builds toward green data centers | +1.5% | Nationwide, most active in renewable-rich west | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital-Transformation Spend by SOEs and Municipalities

State-owned enterprises and city governments are moving core workloads to the cloud as part of Beijing’s digital-economy mandate, pushing cloud platforms from basic IT upgrades toward AI-powered smart-city use cases.[1]National Development and Reform Commission, “2024 NDRC Report,” npcobserver.com Hybrid architectures that meet sovereignty rules yet scale AI services are preferred, and procurement rules often require suppliers to run on approved domestic clouds. Ripple effects are evident across supply chains as SOEs ask vendors to join shared cloud ecosystems, widening the China cloud computing market beyond early adopters. Municipal platforms increasingly deploy AI for traffic optimization, urban management, and citizen-service chatbots, deepening demand for low-latency GPU clusters. This driver boosts subscription stickiness and opens vertical-solution revenue for providers targeting public administration.

AI-Native Workloads Demanding Elastic GPU Clouds

China filed 38,000 generative-AI patents between 2014-2023, outpacing the United States almost sixfold.[2]World Intellectual Property Organization, “China-Based Inventors Filing Most GenAI Patents,” wipo.int Training and inference of large language models now dominate cloud resource requirements, sending ByteDance, Alibaba, and others on multibillion-dollar GPU shopping sprees. Cost-saving pivots to domestic accelerators such as Huawei’s Ascend line highlight sovereign-chip strategies that reduce dependency on imported hardware. Providers respond with dedicated AI clusters including Huawei’s 2 000-PFLOPS Cloud Matrix in Tibet that democratize model access for SMEs and spur rapid workload migration to cloud-hosted inference services.

State-Backed “Eastern Data, Western Computing” Hub Build-Out

Beijing’s megaproject links eight national computing hubs and ten data-center clusters, funneling RMB 400-500 billion of capital to renewable-rich western provinces.[3]South China Morning Post, “Ant Group’s Use of Local GPUs Cuts Training Costs,” scmp.com The strategy raises national computing capacity 50% by 2025 and cuts carbon intensity by relocating heavy workloads away from coastal grids. Gansu’s Qingyang park already hosts 300+ AI firms in a 17 000 mu estate. Ultra-low-latency backbones like the 8 080-mile CENI fiber network ensure real-time data transfer, enabling enterprises in Shanghai or Shenzhen to tap western GPU farms seamlessly.

Industrial-Internet Pilots in Discrete and Process Manufacturing

Manufacturers from Midea to Foxconn are rebuilding production lines on cloud-native stacks that mesh IoT, edge gateways, and analytics platforms.[4]Tencent News, “Midea’s Digital Transformation Roadmap,” news.qq.com Cloud-enabled predictive maintenance and digital twins deliver measurable quality gains, while Huawei’s Pangu 5.5 models boost pipeline inspections and defect detection across 30+ industries. Hybrid designs let factories keep latency-sensitive controls on-premises and offload heavy analytics to regional clouds, driving sticky demand for specialized industrial PaaS suites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tougher cybersecurity and data-locality rules | -3.8% | Nationwide, strictest in finance and government | Short term (≤2 years) |

| High migration costs and downtime risks for legacy systems | -2.4% | Nationwide, harder on traditional industries | Medium term (2-4 years) |

| Shortage of cloud-native DevSecOps talent | -1.9% | Nationwide, most acute in tier-2/3 cities | Medium term (2-4 years) |

| Margin-squeezing price battles slowing provider CAPEX | -1.6% | Nationwide, hits all major vendors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Evolving Multi-Layer Cybersecurity and Data-Locality Regulations

The Network Data Security Management Regulations effective January 2025 impose tiered obligations on firms handling “important data,” heightening compliance complexity and slowing migrations for banks and insurers. Cross-border transfer approvals remain cumbersome, nudging multinationals toward multiple regional clouds rather than one global instance. Domestic providers gain relative advantage through localized compliance expertise, yet all vendors face higher audit and reporting overheads. Hybrid architectures that keep sensitive datasets on-premises are becoming the default mitigation, moderating broader cloud-growth velocity.

Enterprise Cloud-Migration Cost and Downtime Concerns

Legacy ERP refactoring, staff retraining, and potential production downtime raise switching costs for traditional manufacturers, causing staggered rollouts and extended pilots. Limited DevSecOps talent inflates consulting fees, while fluctuating price discounts prompt wait-and-see strategies among cost-conscious SOEs. These factors collectively temper near-term migration volume even as long-term demand remains intact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Drive Sovereignty Balance

Hybrid and multi-cloud solutions, expanding at a 24.2% CAGR, reflect enterprise strategies to satisfy data-locality mandates while exploiting public-cloud scalability. Although Public Cloud held 62.55% share in 2025, the China cloud computing market is witnessing rapid workload re-allocation to hybrid stacks anchored by on-premises or private instances for classified data. Financial services and government agencies lead adoption with sovereign-cloud blueprints, while manufacturers deploy edge-connected private clouds for latency-critical controls. Telecom operators bundle 5G and cloud to enable distributed AI and real-time analytics at plant floors, strengthening hybrid appeal. Vendor lock-in fears further prompt multi-cloud procurement, e.g., banks splitting core and digital-bank workloads across Alibaba and Tencent to diversify risk. Eastern Data, Western Computing amplifies this shift by allowing sensitive data to reside in western sovereign clusters and lighter workloads to stay near coastal users. Edge nodes located in industrial parks complement central clouds, creating a continuum of compute tiers that define the next phase of the China cloud computing market.

Hybrid demand is also propelled by steep discounts from newly aggressive telecom clouds challenging the Big-Three tech incumbents. Bundled connectivity plus cloud services deliver measurable opex savings for tier-2/3 city clients, encouraging first-time migrations. At the same time, public-cloud providers counter with sovereign zones inside their campuses, offering “trusted computing” enclaves that pass regulator scrutiny. These innovations are widening the overall China cloud computing market, reinforcing hybrid’s status as the architecture of choice through 2031.

By Service Model: PaaS Acceleration Reflects AI Integration

Infrastructure-as-a-Service retained 67.40% dominance in 2025, yet Platform-as-a-Service is sprinting ahead with a 30.7% CAGR, signaling maturation of enterprise cloud usage. The China cloud computing market size for PaaS is scaling on the back of AI model studios, container orchestration, and low-code development suites that shorten time-to-value. Alibaba Cloud’s Model Studio, already adopted by 300 000 customers, typifies this trend. Baidu AI Cloud’s 18.1 million-strong ERNIE developer base underscores the gravity of AI-native PaaS ecosystems. Domestic AI accelerators integrated into PaaS stacks are lowering total ownership costs, enticing price-sensitive SMEs. Software-as-a-Service growth remains moderate because large enterprises favor customizable in-house builds over standardized SaaS packages.

Demand migrations from raw compute to managed AI platforms deepen vendor lock-in but also raise average revenue per user, bolstering profitability despite headline price wars. Container-native tooling embedded in PaaS offerings eases multi-cloud portability, supporting enterprise efforts to avoid single-vendor dependence. Consequently, PaaS will keep enlarging its slice of the China cloud computing market while IaaS growth decelerates off a larger base.

By Organization Size: SME Democratization Accelerates Adoption

Large Enterprises accounted for 59.20% of 2025 revenues, yet SMEs, advancing at 23.8% CAGR, represent the fastest-growing customer cohort. Subsidized government programs and aggressive vendor discounts are putting advanced analytics, AI APIs, and e-commerce back-end services within reach of micro-enterprises. Falling entry-level pricing and simplified management dashboards cut the learning curve for non-technical owners. Digital China’s 62.7% jump in cloud-services revenue exemplifies specialized providers capitalizing on SME demand. Promotional “starter bundles” pairing 5G connectivity with basic cloud seats are especially popular among retail and professional-services firms in tier-3 cities. This democratization embeds cloud into the core of China’s 30 million small businesses, diversifying the China cloud computing market beyond large enterprises and stabilizing long-term growth.

By End-User Industry: Manufacturing Transformation Leads Growth

Internet and Tech maintained 25.20% revenue share in 2025 due to the inherent cloud-native DNA of platforms like e-commerce and gaming, yet Industrial Manufacturing is accelerating at a 27.6% CAGR, becoming the prime catalyst for incremental workloads. Smart-factory pilots leverage AI-enabled visual inspection and predictive maintenance hosted on regional clouds, generating surging data volumes that require elastic storage and GPU resources. AIBank and other financial firms expand cloud usage for risk scoring and customer analytics, illustrating BFSI’s catch-up acceleration. Healthcare adoption is also brisk, evidenced by Ant Group’s AI-powered AQ health app that scales diagnostics across regions. Cross-sector convergence of AI, IoT, and 5G multiplies data-intensive scenarios, securing a broad demand base for the China cloud computing market.

Geography Analysis

East China remains the largest regional node, fueled by Shanghai’s financial sector, Jiangsu’s industrial corridors, and Zhejiang’s e-commerce giants. Deep talent pools and mature fiber networks support latency-critical blockchain trading systems and omnichannel retail platforms. Provincial incentives, such as Wuhu’s cloud-cluster subsidies, continue to attract additional data-center builds, reinforcing coastal dominance for mission-critical low-latency services.

North and Northeast China benefit from cooler climates that trim cooling opex and from policy-driven AI compute targets set by Beijing’s municipal government. The confluence of research universities and central-government agencies creates steady demand for sovereign-cloud compliance capabilities. Telecom carriers leverage abundant wind power from Inner Mongolia to offer carbon-neutral cloud packages tailored to state agencies.

Central and West China, energized by Eastern Data, Western Computing, represent the fastest growth frontier. Renewable electricity discounts, lower land costs, and dedicated fiber links attract AI model-training clusters. Tibet’s high-altitude data center leverages natural cooling to deliver 2 000 PFLOPS, underscoring the region’s rising strategic value. Economic spillovers include job creation in high-skill sectors and the emergence of new provincial innovation hubs.

Mordor Intelligence provides coverage of the cloud computing market across other key regional markets, including Asia, South America, and North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to South Korea, Japan, Brazil, United States, Israel, and Canada incorporating local coverage and market participation, as required.

Competitive Landscape

Alibaba Cloud (36%), Huawei Cloud (19%), and Tencent Cloud (15%) collectively hold roughly 70% of revenue, yielding a moderately concentrated yet fiercely contested market. Telco-affiliated entrants China Telecom, China Mobile, and China Unicom doubled cloud turnover to RMB 70 billion in 2024, eroding incumbents’ margins while expanding overall addressable workloads. Strategic bifurcation is emerging: private tech firms differentiate via AI-native PaaS and cross-border e-commerce capabilities; state-owned entities emphasize compliance-first hybrid solutions. Domestic AI chip integration has become a key battleground, with Huawei bundling Ascend accelerators and Pangu models to cut inference costs by 30% over NVIDIA-based offerings. Patent races intensify competitiveness: Chinese firms filed 38 000 Gen-AI patents versus 6 276 from US counterparts.

Edge-computing niches, industry-specific vertical clouds, and hybrid-management platforms remain whitespace areas attracting venture funding. DeepSeek’s low-cost AI model services signpost potential disruptors, prompting established providers to integrate third-party models rapidly. Foreign players AWS China and Microsoft Azure (21Vianet) operate via joint ventures, focusing on multinational clients that require global-standard architectures yet must comply with China’s localization rules.

China Cloud Computing Industry Leaders

Alibaba Cloud Internationa (Aliyun)

Tencent Cloud

Huawei Software Technologies Co., Ltd.

Baidu Cloud (Baidu, Inc.)

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Huawei open-sourced two Pangu models to accelerate global Ascend adoption.

- June 2025: Baidu announced plans to open-source its ERNIE model, widening developer access.

- June 2025: Alibaba unveiled a USD 52 billion global infrastructure plan to export Chinese AI worldwide.

- May 2025: Huawei released Pangu 5.5 AI models with 718 billion parameters.

China Cloud Computing Market Report Scope

Cloud computing delivers computing services via the internet, encompassing servers, storage, databases, networking, software, analytics, and intelligence. This approach fosters quicker innovation, adaptable resources, and economies of scale. Typically, customers pay solely for the cloud services they utilize, leading to reduced operational costs, more efficient infrastructure management, and the ability to scale in line with evolving business needs.

China cloud computing market report is segmented by type (public cloud [ IaaS, Paas, Saas], private cloud, hybrid cloud), and by organization size (SMEs, large enterprises), and by end-user industries (manufacturing, education, retail, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and others including utilities, media & entertainment, etc.). The market sizes and forecasts are provided in terms of value (USD) for all segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| IaaS |

| PaaS |

| SaaS |

| Large Enterprises |

| Small and Medium Enterprises (SME's) |

| Manufacturing |

| BFSI |

| Healthcare and Life-Sciences |

| Retail and e-Commerce |

| Transportation and Logistics |

| Telecom and IT Services |

| Others |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | IaaS |

| PaaS | |

| SaaS | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SME's) | |

| By End-User Industry | Manufacturing |

| BFSI | |

| Healthcare and Life-Sciences | |

| Retail and e-Commerce | |

| Transportation and Logistics | |

| Telecom and IT Services | |

| Others |

Key Questions Answered in the Report

What is the current size of the China cloud computing market?

The market is valued at USD 61.19 billion in 2026 and is forecast to grow to USD 160.37 billion by 2031.

Which deployment model is growing fastest in China?

Hybrid/Multi-Cloud leads growth with a projected 24.2% CAGR through 2031 as enterprises balance sovereignty with scalability.

Why are GPUs critical to China’s cloud growth?

AI-native workloads such as large language models require elastic GPU clusters, driving billion-dollar hardware investments and specialized cloud services.

Which region is expanding cloud infrastructure the quickest?

Central and West China shows the fastest regional growth at a 27.2% CAGR, fueled by the Eastern Data, Western Computing initiative and renewable energy advantages.

How strict are China’s data-locality rules for cloud users?

January 2025 regulations mandate enhanced classification and reporting for firms handling “important data,” pushing many enterprises toward hybrid architectures for compliance.

Who are the leading cloud providers in China?

Alibaba Cloud holds 36% market share, followed by Huawei Cloud at 19% and Tencent Cloud at 15%, together accounting for around 70% of market revenue.

Page last updated on: