Italy Heat Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.19 Billion |

| Market Size (2030) | USD 1.52 Billion |

| Growth Rate (2025 - 2030) | 4.94% CAGR |

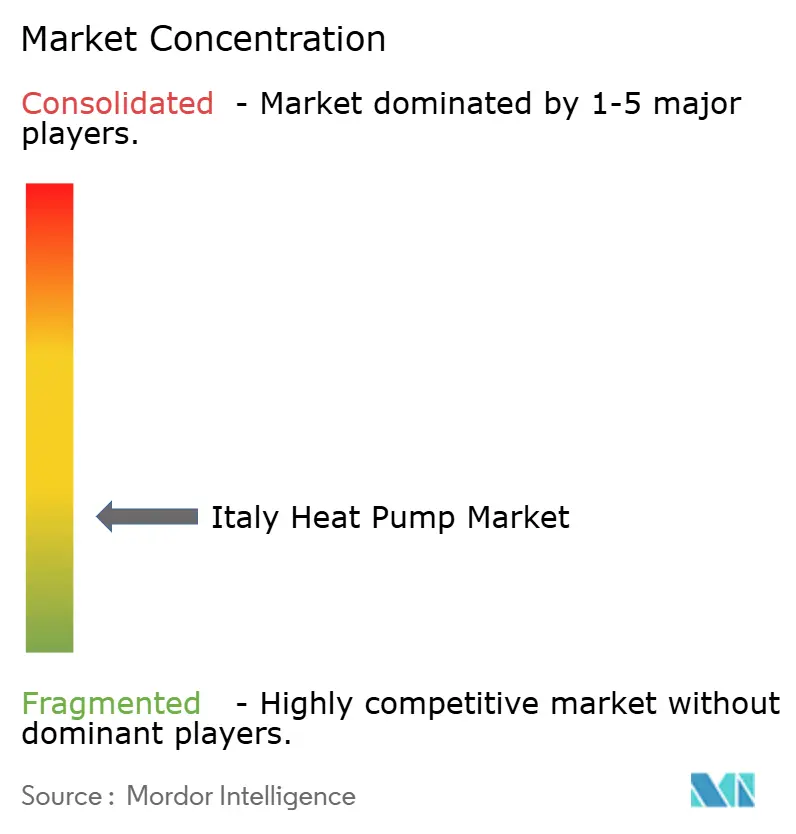

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Heat Pump Market Analysis by Mordor Intelligence

The Italy heat pump market reached USD 1.19 billion in 2025 and is projected to expand to USD 1.52 billion by 2030 at a 4.94% CAGR, reflecting a transition from subsidy-fuelled expansion to steadier, policy-supported growth. Key demand drivers include the Ecobonus tax credits, a widening preference for electrified heating, and accelerating adoption of natural-refrigerant designs. Hybrid/exhaust-air units are widening the addressable base by lowering peak grid demand, while e-commerce channels shorten lead times for standard residential systems. Manufacturers that align with the revised F-Gas Regulation and integrate digital controls are winning specification in both retrofit and new-build projects. Grid reinforcement, installer shortages outside the North, and tighter acoustic limits in heritage districts still temper near-term volumes, yet structural tailwinds tied to the EU Fit-for-55 package underpin long-run opportunity for the Italy heat pump market.

Key Report Takeaways

- By type, air-source systems held 82% Italy heat pump market share in 2024; hybrid/exhaust-air units are forecast to grow at a 6.40% CAGR through 2030.

- By rated capacity, sub-10 kW models commanded 61% of the Italy heat pump market, while units above 100 kW are set to post a 6.30% CAGR to 2030.

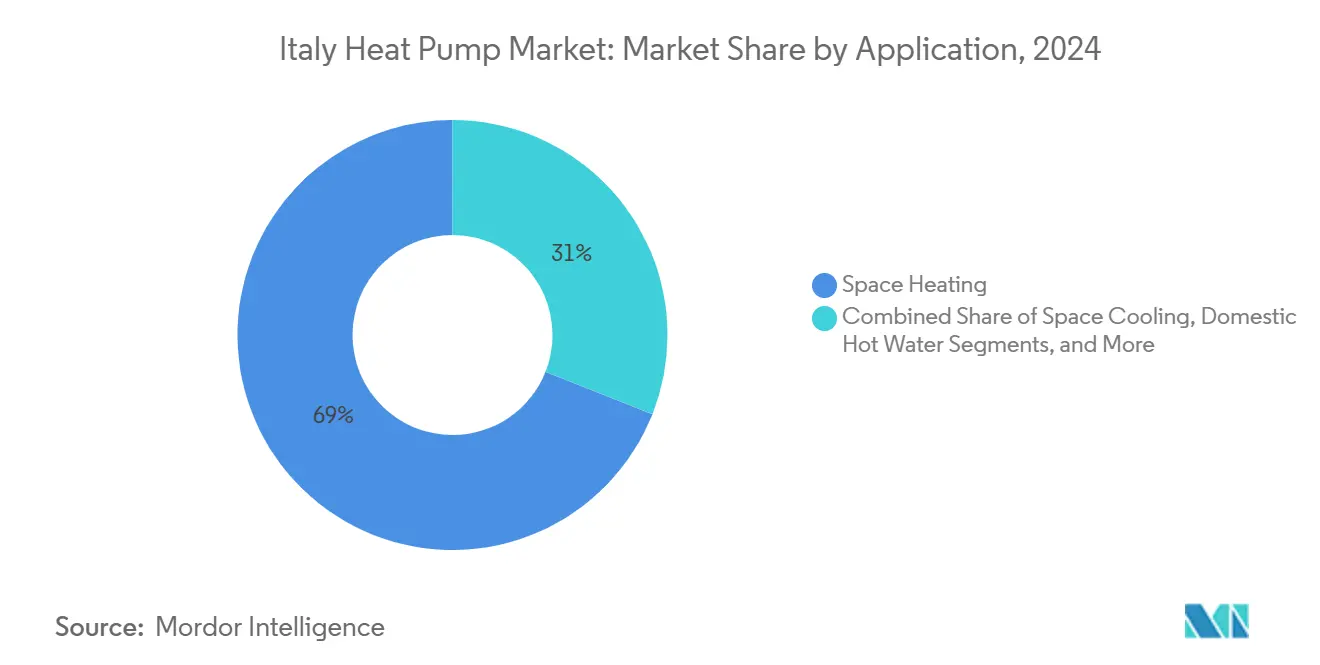

- By application, space heating led with 69% revenue in 2024; space cooling is projected to advance at a 5.70% CAGR.

- By end-user, the residential segment accounted for 56% of the Italy heat pump market; industrial users will rise fastest at an 6% CAGR.

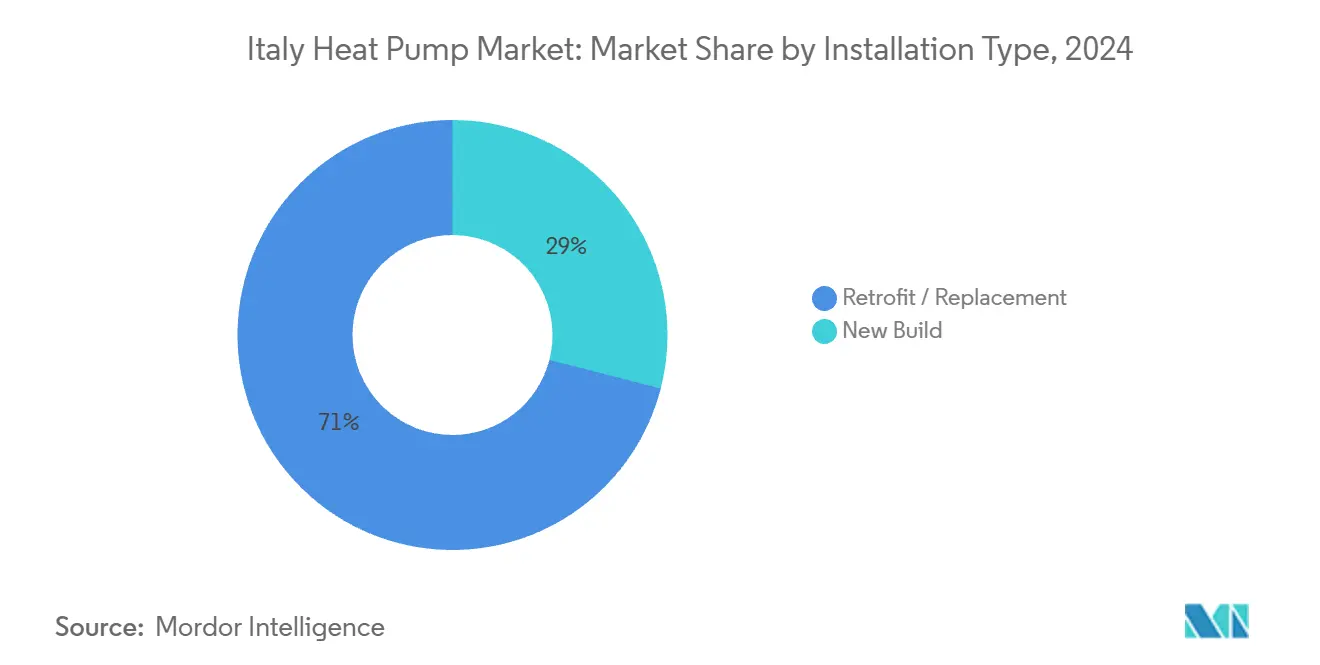

- By installation type, retrofits captured 71% share in 2024; new-build deployments are expected to expand at 5.60% CAGR to 2030.

- By sales channel, distributor / installer network captured 68% share in 2024; E-commerce is forecast to grow at a 6.50% CAGR.

Italy Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heat-pump-ready district-heating tenders | +1.2% | Urban North and Central | Medium term (2-4 years) |

| Recovery-plan grants for residential retrofits | +1.5% | Nationwide, strongest in North | Short term (≤2 years) |

| Data-center waste-heat projects | +0.9% | Industrial corridors | Medium term (2-4 years) |

| EU Fit-for-55 subsidy extension | +0.7% | Nationwide | Long term (≥4 years) |

| F-Gas phase-down to natural refrigerants | +0.6% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recovery-plan grants for residential retrofits

The Superbonus scheme ignited rapid uptake, financing nearly 500,000 energy renovations by mid-2024. Even after rates fall to 50% in 2025, market momentum persists as consumer awareness and installer capacity are now firmly in place. Retrofit economics remain attractive versus gas boiler replacement, particularly as electricity tariffs stabilise and carbon levies on methane tighten policy risk. The Italy heat pump market therefore shifts from incentive-led spikes toward recurring, mortgage-linked funding streams that reward high-efficiency upgrades.

Heat-pump-ready district-heating tenders by municipal utilities

Cities such as Milan in Italy are tendering large air-to-water units to decarbonise district loops, enlarging several addressable capacity above 10 MWth per contract. Tender guidelines now specify propane or CO₂ refrigerants, driving suppliers to fast-track compliant designs. Volume-based procurement also lifts local assembly demand, reinforcing the Italy heat pump market’s supply-chain depth.

Demand from data-center waste-heat reuse projects

Northern industrial zones link low-grade server waste heat with municipal grids, deploying reversible heat pumps to elevate temperature for neighbouring buildings. The European Commission frames such integration as core to energy-system coupling, positioning Italy as a test bed for replicable circular-heat models.[1]ARANER, “Heat Pump Grants: How to Access European and Local Funds,” araner.com These projects anchor the Italy heat pump market in the broader digital-infrastructure narrative, unlocking industrial energy-service revenue streams.

EU Fit-for-55 heat-pump subsidies extension

Long-dated regulatory clarity under Fit-for-55 deters new gas-boiler investment and channels capital into electrified systems.[2]Regulatory Assistance Project, “The Perfect Fit: Shaping Fit for 55 to Drive a Heat Pump Market,” stiftung-mercator.de As part of its "Fit for 55" initiative, the EU is rolling out a suite of measures, including subsidies and incentives, to hasten the adoption of heat pumps. These efforts align with the EU's ambitious goal of slashing greenhouse gas emissions by 55% come 2030. Manufacturers scale Italian plants accordingly, confident that rising carbon costs and energy-tax revisions sustain demand beyond the current budget horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent refrigerant and safety codes | −0.8% | Dense urban zones | Short term (≤2 years) |

| Long grid-connection lead times | −0.6% | Rural Southern regions | Rural and Southern regions |

| Skilled-installer shortage outside North | −0.5% | Central, South and Islands | Central, South and Islands |

| Tighter acoustic limits in heritage areas | −0.4% | Historic centers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent refrigerant and safety codes

The shift from HFCs (Hydrofluorocarbons) to propane triggers additional ventilation, leak-detection, and zoning requirements, elevating installed costs in multi-storey dwellings. [3]Environmental Investigation Agency, “Pumping Up the Potential,” eia-international.org Smaller OEMs (original equipment manufacturers) struggle with certification, nudging the Italy heat pump market toward larger, compliance-ready brands. To comply with regulations, heat pumps utilizing low-GWP or natural gas refrigerants necessitate specialized components and safety features, such as explosion-proof designs for flammable refrigerants. Consequently, these systems incur higher product and installation costs than their conventional counterparts.

Long lead-times for grid connection upgrades

Surging retrofit demand strains ageing low-voltage feeders, with wait-times hitting six months in parts of Puglia and Calabria. Developers increasingly specify hybrid systems to shave peak demand until reinforcement arrives. Many older buildings in Italy feature outdated or undersized electrical systems. Upgrading the internal wiring and external grid connection can be both costly and time-consuming, especially in historic or rural areas. As a result, property owners might forgo adopting heat pumps if it necessitates grid upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Air-Source Dominates Despite Diversification

Air-source units generated 82% of market share. Milder winters south of Florence ensure seasonal performance factor stability, anchoring volume growth in both retrofit apartments and villa conversions. The Italy heat pump market demand attributed to hybrid/exhaust-air designs is poised to witness significant growth, as they replace combi-boilers without major electrical upgrades. Ground-source systems remain favoured in new commercial complexes where borehole drilling is feasible, keeping a specialist niche alive. Water-source models, while limited in footprint, gain relevance along Adriatic marinas where seawater intake moderates winter capacity drops. Across all formats, natural-refrigerant re-engineering catalyses design refresh cycles, accelerating product substitution.

Continued public procurement for district loops amplifies large air-to-water shipments, while hotel chains in Veneto adopt water-loop heat pumps to cut peak demand charges. OEMs integrate cloud-based control to track real-world coefficient of performance, providing data to justify energy-service contracts. These usage analytics strengthen after-sales revenue, deepening manufacturer-installer alliances within the Italy heat pump market.

By Rated Capacity: Small Units Lead in Volume, Large in Growth

Sub-10 kW models represented 61% of the Italy heat pump market size in 2024 owing to apartment retrofits supported by 50% Ecobonus relief. Demand aligns with radiator-based systems upgraded with low-temperature emitters. Units above 100 kW, though just 4% of shipments, will expand at 6.30% CAGR on the back of industrial electrification incentives. Textile and food SMEs in Emilia-Romagna retrofit process heaters below 80 °C, exploiting the Transizione 5.0 tax-credit ladder that rises to 45% for deep-energy cuts.[4]Ministry for Ecological Transition, “Strategy for Energy Retrofitting of National Building Stock,” energy.ec.europa.eu Mid-range 20-50 kW systems pick up in mixed-use office blocks where VRF and hydronic loops intersect, fostering multipurpose heating and cooling profiles.

OEM capacity scaling in Veneto and Friuli shortens lead times for >100 kW skids, encouraging EPC contractors to pre-specify Italian-made equipment. The Italy heat pump market thereby re-balances from single-family dependence toward diversified industrial baseloads, smoothing policy cycles.

By Application: Space Heating Dominates, Cooling Accelerates

Space heating contributed to 69% of the market share. Rising methane tariffs after the 2024 market reform nudge condominium assemblies to vote for common-area hydronic upgrades, planting multiyear demand. The Italy heat pump market size for cooling will outpace heating through 2030 at 5.70% CAGR as heatwaves stretch into October, amplifying dual-service payback. Domestic hot-water remains resilient owing to mandatory legionella safeguards in hospitality and healthcare. Process heat for wineries in Piedmont adopts cascade systems that lift outlet temperatures to 80 °C, widening the “other” slice of the Italy heat pump market.

Seasonal switching logic embedded in smart thermostats lowers operational cost, reinforcing consumer confidence. PV-coupled storage combos cut summer self-consumption payback to eight years in Sicily, anchoring demand for reversible air-source models.

By End-User Vertical: Residential Leads, Industrial Rises

The residential sector secured 56% of total value, cementing its role as the prime volume engine. Yet industrial adoption will rise 6% CAGR as process electrification policies intersect with corporate decarbonisation pledges. SMEs opting for modular skid units expand average deal sizes and lengthen service contracts. Commercial offices lean on VRF-to-hydronic hybrids to monetise both heating and cooling within the same capital budget. Institutional upgrades funded under PREPAC ensure steady baseline demand, particularly for schools meeting the 3% annual efficiency mandate.

Broader energy-service framing converts one-off sales into multi-year performance-based agreements, integrating O&M revenue into the Italy heat pump market.

By Installation Type: Retrofits Dominate, New-Build Accelerates

Retrofits generated 71% of Italy heat pump market share as ageing masonry stock pairs naturally with mono-bloc units. Acoustic baffles and facade colour-matching meet UNESCO guidelines, enabling installs even in historic cores. New-build penetration will climb at 5.60% CAGR as nZEB codes mandate <45 kWh/m² annual primary-energy demand, effectively prescribing heat pumps for compliance. Builders favour integrated rooftop PV-heat-pump packages to hit Class A energy labels, securing premium sale prices.

As developers adopt platform-based pre-plumbed shafts, lead-times shrink, and standardisation allows bulk e-commerce procurement of 6 kW monoblocs. This process modernises the Italy heat pump market supply chain, stitching together manufacturing, logistics, and on-site commissioning.

By Sales Channel: Installers Crucial, E-Commerce Disrupts

Installer networks handled 68% of share in 2024, reflecting the country’s dense fabric of small HVAC firms that navigate permitting and grid liaison. Direct OEM sales target supermarkets and factories where bespoke engineering warrants manufacturer oversight.

Online platforms are forecast to grow 6.50% CAGR, propelled by AI-based load-sizing tools that deliver fixed-price offers within hours. Consumer acceptance rises as five-year performance warranties offset perceived risk. Marketplace ecosystems bundle financing, PV, and maintenance, embedding recurring revenue in the Italy heat pump market.

Geography Analysis

Northern Italy accounted for major revenue in 2024 as Lombardy’s dense housing stock and higher disposable incomes fostered early adoption. Milan’s 2025 Heat Pump Technologies fair spotlighted district-scale integration, amplifying municipal tenders. Piedmont leverages ample installer density, easing labour constraints that hamper southern regions.

Central regions report balanced heating-cooling loads, allowing reversible units to achieve year-round utilisation. Heritage zoning in Florence and Rome imposes facade and noise restrictions; acoustic blankets and split-condenser configurations maintain project viability while slightly inflating capex. Grid bottlenecks are less acute than in the south, sustaining smoother installation timelines.

The Islands of Sicily and Sardinia witnesses significant growth, fuelled by high solar yields that slash operating costs for PV-coupled systems. However, restrictive curbs on new renewable projects could withhold 400 MW of planned capacity, highlighting the critical link between electricity supply and the Italy heat pump market. Rural Calabrian provinces face the longest grid-upgrade queues, compelling installers to promote hybrid units that trim peak-draw until reinforcement is complete. A South Tyrol study showed levelised heat costs of 104 EUR/MWh (USD 117.5/MWh), rivalling subsidised gas, demonstrating viability even in alpine conditions when coupled with targeted renewables.

Competitive Landscape

The Italy heat pump market remains fragmented. Domestic players Ariston, Clivet, and Riello leverage local familiarity and after-sales support, while global groups Daikin, Mitsubishi Electric, and Bosch bring R&D expertise. Midea's USD 67.8 million Feltre plant will reduce lead times from five months to one month, tightening competition on delivery performance. Ariston’s Q1 2025 rebound validates its balanced portfolio strategy across water-heating and climate comfort.

The innovation focus shifts to R290 designs and smart grid integration. Daikin’s forthcoming CO2 VRV range targets heritage sites wary of flammable refrigerants. CAREL’s high-efficiency inverters debut at ISH 2025, enhancing seasonal performance and appealing to installers tasked with minimizing fuse upgrades.

Channel power is tilting toward e-commerce newcomers bundling PV, batteries, and heat pumps under single-click finance, pressuring traditional wholesalers to add digital storefronts. Overall, price pressure coexists with a premium tier that commands markups for natural refrigerants and predictive maintenance, thereby preserving margin diversity within the Italian heat pump market.

Italy Heat Pump Industry Leaders

-

Daikin Industries Ltd.

-

Carrier Corporation

-

Viessmann Climate Solutions SE

-

Trane Technologies Plc

-

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UL Solutions has launched a new laboratory in Italy, bolstering its European HVAC testing capabilities. This move comes in response to the burgeoning heat pump market and evolving regulations. The Italian facility offers heat pump manufacturers cutting-edge testing services, efficient regulatory compliance assistance, and evaluations focused on sustainable heat pump performance tailored for the European landscape.

- April 2025: Ariston launched 15 kW+ Nuos commercial water-heater heat pumps, expanding into mid-scale hospitality retrofits. Businesses, particularly commercial spaces, are set to benefit from this expansion, as it focuses on delivering energy-efficient hot water solutions, catering to those eager to upgrade their systems.

- March 2025: Thermocold, an Italian specialist in heating and cooling, has launched new air-to-water heat pumps tailored for residential, commercial, and industrial applications. The iMEX HP R454B model utilizes R454B refrigerant, noted for its global warming potential (GWP) of 466. These units can achieve a leaving water temperature of 45°C even when the outdoor temperature drops to -15°C. Additionally, during summer months, they can heat water up to 60°C when outdoor air temperatures range between 5°C and 35°C.

- January 2025: Italian manufacturer Clivet boasts that its Large Evo PL heat pump achieves a seasonal coefficient of performance of up to 4.17. The system can deliver water temperatures of up to 60°C and, when stacked in series, can reach a maximum system capacity of 1,660 kW.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Italian heat-pump market as revenue generated from factory-built air, water, and ground-source units (reversible and non-reversible) up to industrial capacities that are sold for space heating, cooling, and sanitary hot water across residential, commercial, industrial, and institutional premises.

Scope exclusion: portable spot coolers, chillers, and purely cooling-only minisplits are omitted to avoid double counting.

Segmentation Overview

-

By Pump Type

- Air-Source

- Water-Source

- Ground-Source (Geothermal)

- Other Pump Types (Hybrid, Exhaust-Air)

-

By Rated Capacity (kW)

- < 10 kW

- 10-20 kW

- 20-50 kW

- 50-100 kW

- > 100 kW

-

By Application

- Space Heating

- Space Cooling

- Domestic / Sanitary Hot Water

- Other Applications (Pool Heating, Process Heating, and Cooling)

-

By End-User Vertical

- Residential

- Commercial

- Industrial

- Institutional

-

By Installation Type

- New Build

- Retrofit / Replacement

-

By Sales Channel

- Direct (OEM to End-User)

- Distributor / Installer Network

- E-Commerce

Detailed Research Methodology and Data Validation

Primary Research

Interviews were conducted with HVAC wholesalers, energy-service companies, and regional building-code officials across Lombardy, Veneto, Lazio, and Sicily. Discussions clarified real-world subsidy utilization, installer mark-ups, and seasonal demand swings, enabling us to calibrate penetration assumptions and discount headline shipment spikes tied to one-off tax incentives.

Desk Research

Our analysts first mapped public datasets such as Eurostat building-energy files, Gestore dei Servizi Energetici (GSE) renewable-heat balances, and customs codes for HS 8418 and 8415 shipments. They then reviewed trade-association dashboards from EHPA, Assoclima, and Assotermica that track unit sales and installed stock. Policy texts (Ecobonus decrees, Green Homes Directive drafts) and peer-reviewed Italian retrofit case studies supplied regulatory and performance benchmarks. To price the value pool, we compared average selling prices disclosed in installer surveys with price corridors seen in listed OEM filings and D&B Hoovers snapshots. Select paywalled feeds, including Dow Jones Factiva for deal activity and Questel for refrigerant-patent volumes, added competitive and technology depth. The sources noted are illustrative; many additional materials informed validation.

Market-Sizing and Forecasting

We built a top-down demand pool by reconstructing yearly dwelling-stock renovations and new-build completions, applying heat-pump adoption ratios derived from permit data. Results were pressure-tested with a bottom-up check using sampled ASP times units from six leading distributors. Key variables include: Ecobonus incentive rates, residential electricity-to-gas price ratio, median system capacity per household, and replacement cycle length for legacy boilers. A multivariate regression model links these indicators to annual sales before an ARIMA overlay projects the 2025 to 2030 trajectory. Gaps in distributor disclosure were bridged by triangulating EHPA unit totals with customs import values.

Data Validation and Update Cycle

Outputs pass two analyst reviews, variance tests against Eurostat energy balances and anomaly flags on price/volume outliers, before sign-off. Models refresh every twelve months, with interim revisions triggered by policy amendments or greater than 10 percent swings in quarterly EHPA sales.

Why Mordor's Italy Heat Pump Baseline Earns Decision-Maker Trust

Published figures often diverge because firms mix cooling-only splits, assume uniform ASPs, or stretch forecasts without adjusting for subsidy tapering.

Our disciplined scope, yearly refresh cadence, and policy-sensitive variables anchor a dependable reference point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.19 B (2025) | Mordor Intelligence | - |

| USD 2.26 B (2024) | Global Consultancy A | Includes heat-pump water heaters and minisplits; single ASP applied nationwide |

| USD 1.55 B (2024) | Industry Study B | Extrapolates 2022 shipment spike forward; limited price validation |

These contrasts show that when incentive-driven surges fade or segment boundaries blur, Mordor's scenario-tested model offers the balanced, transparent baseline executives can replicate and stress-test for strategic planning.

Key Questions Answered in the Report

What is the current size of the Italy heat pump market and its growth outlook?

The market was valued at USD 1.19 billion in 2025 and is projected to reach USD 1.52 billion by 2030, reflecting a 5.02% CAGR.

Which heat-pump technology holds the largest share in Italy?

Air-source units led with 82% market share in 2024 because their lower installation cost and milder Italian climate conditions support high seasonal efficiency.

What regional market leads in installations?

The North-West region—covering Lombardy, Piedmont, Liguria, and Valle d’Aosta—accounted for 34% of national revenue in 2024, supported by dense housing stock and a broad installer base.

How have government incentives changed for residential retrofits?

From 2025, Ecobonus tax deductions cover 50% of heat-pump costs for primary residences (down from earlier higher Superbonus levels), yet retrofit economics remain favourable due to rising gas prices and stronger consumer awareness.

Page last updated on: