Estonia Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

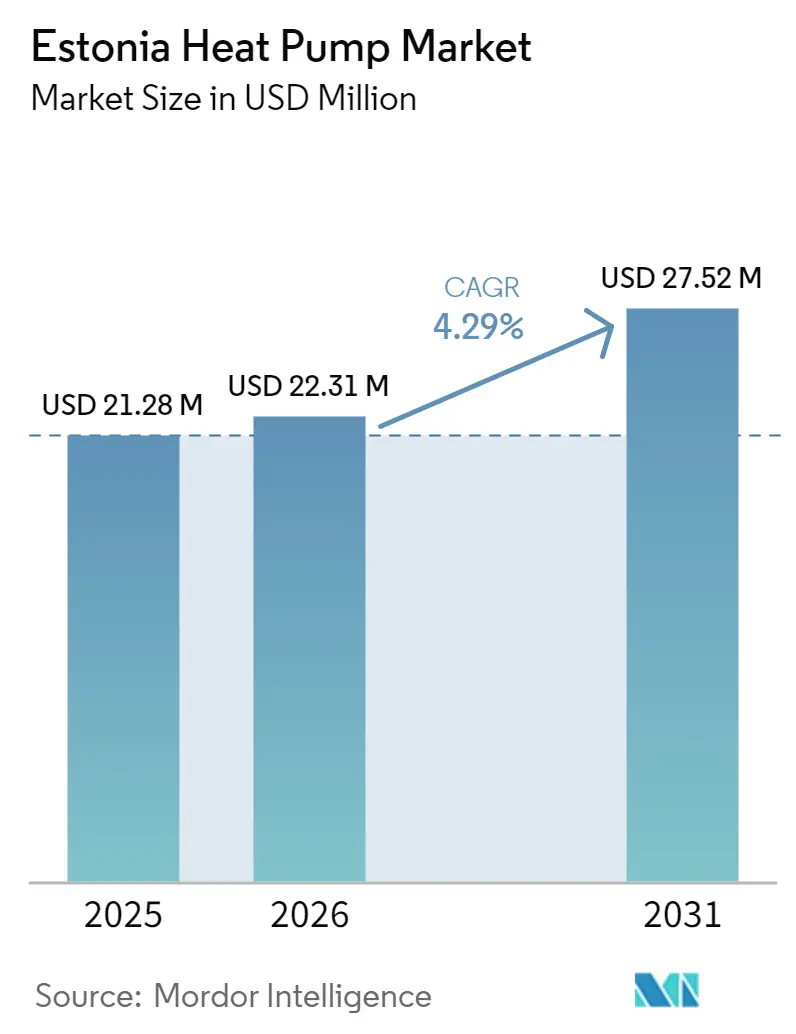

| Base Year Market Size (2025) | USD 21.28 Million |

| Market Size (2026) | USD 22.31 Million |

| Market Size (2031) | USD 27.52 Million |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Estonia Heat Pump Market Analysis by Mordor Intelligence

The Estonia heat pump market size is projected to expand from USD 21.28 million in 2025 and USD 22.31 million in 2026 to USD 27.52 million by 2031, registering a CAGR of 4.29% between 2026 and 2031. Estonia already records Europe’s highest per-capita penetration, yet fresh growth stems from district-heating electrification, commercial retrofits, and industrial process heating. Utility-scale wastewater and seawater projects in Tallinn, stronger electricity-to-gas price advantages, and the 2025 tightening of building-energy rules are shifting demand from small residential units toward mid-scale and high-temperature systems. Domestic prefab timber-module exporters that embed factory-installed units are carving an export-driven niche, while F-gas rules are accelerating the transition toward propane and ammonia refrigerants. Hybrid solutions that blend biomass or gas with air-source technology are bridging rural fuel-cost realities until grid upgrades catch up.

Key Report Takeaways

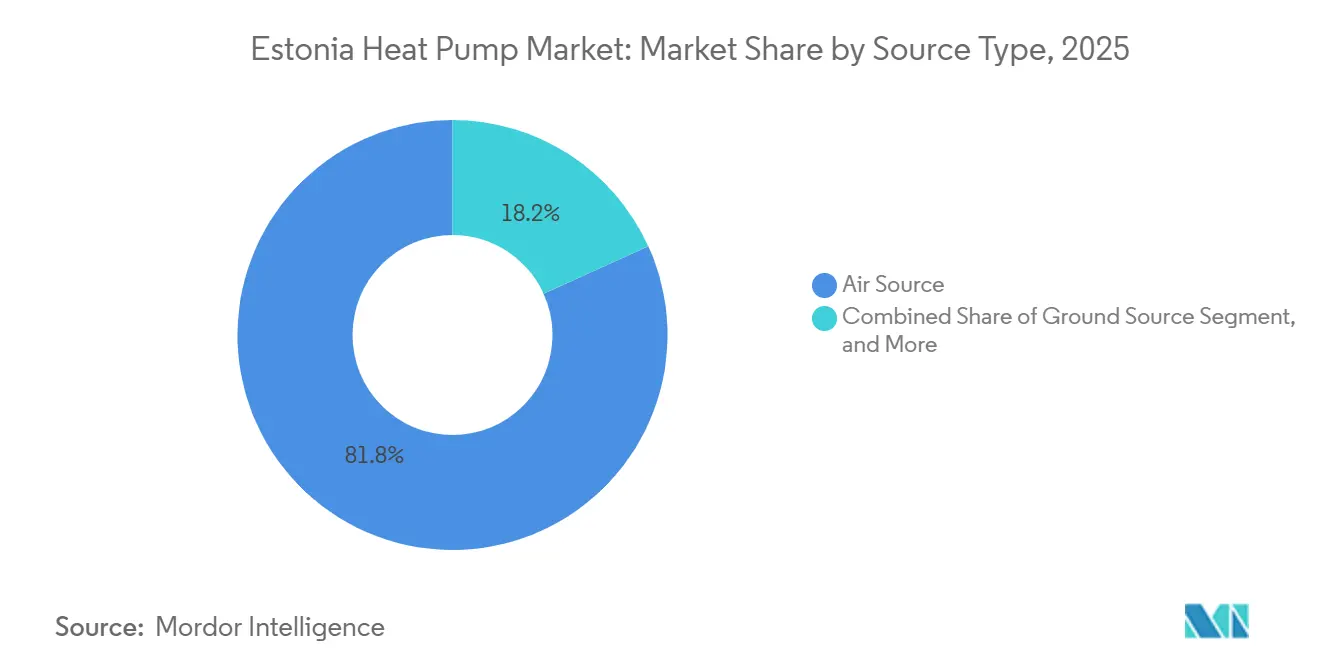

- By source type, air source systems led with 81.78% of the Estonia heat pump market share in 2025; hybrid configurations integrating biomass or gas backups are forecast to grow at a 5.24% CAGR through 2031.

- By technology, air-to-air units captured 58.31% revenue in 2025, while ground-to-water installations are projected to expand at a 4.96% CAGR over 2026-2031.

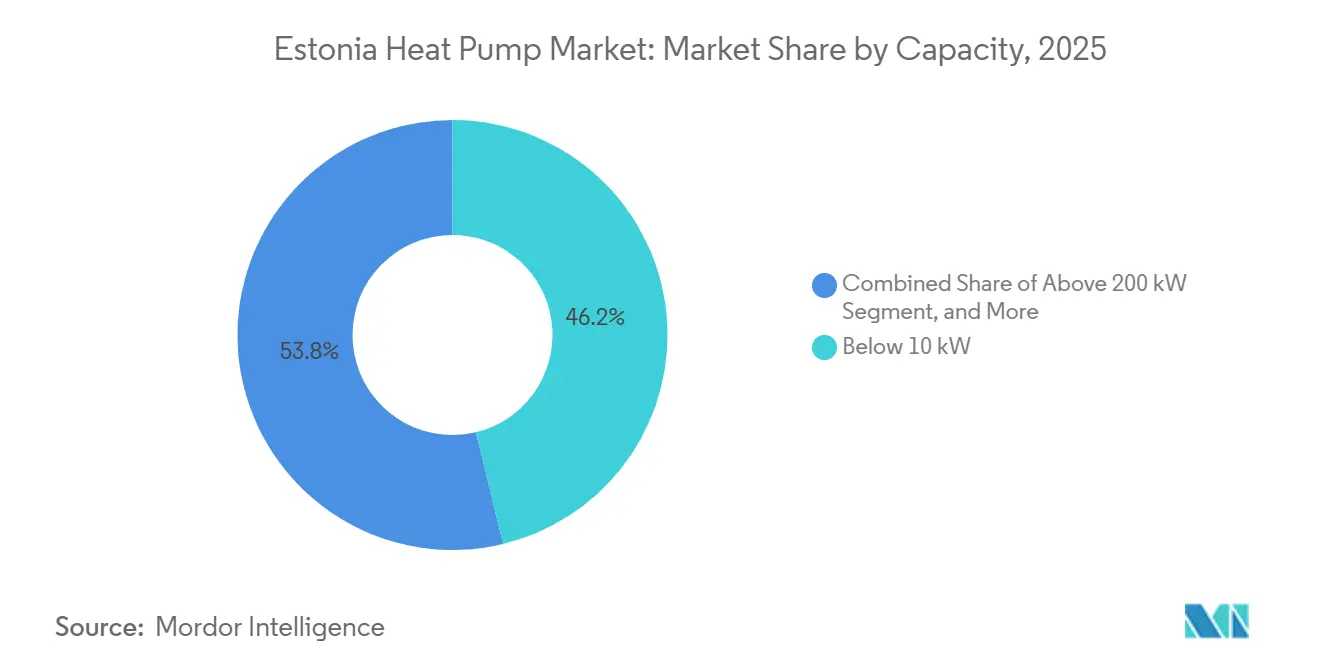

- By capacity, below-10 kW units accounted for 46.23% of the Estonia heat pump market size in 2025, whereas the 50-200 kW mid-scale bracket is advancing at a 4.72% CAGR to 2031.

- By application, space heating dominated with 55.42% share in 2025; industrial and process heating is the fastest-growing use case at a 4.86% CAGR to 2031.

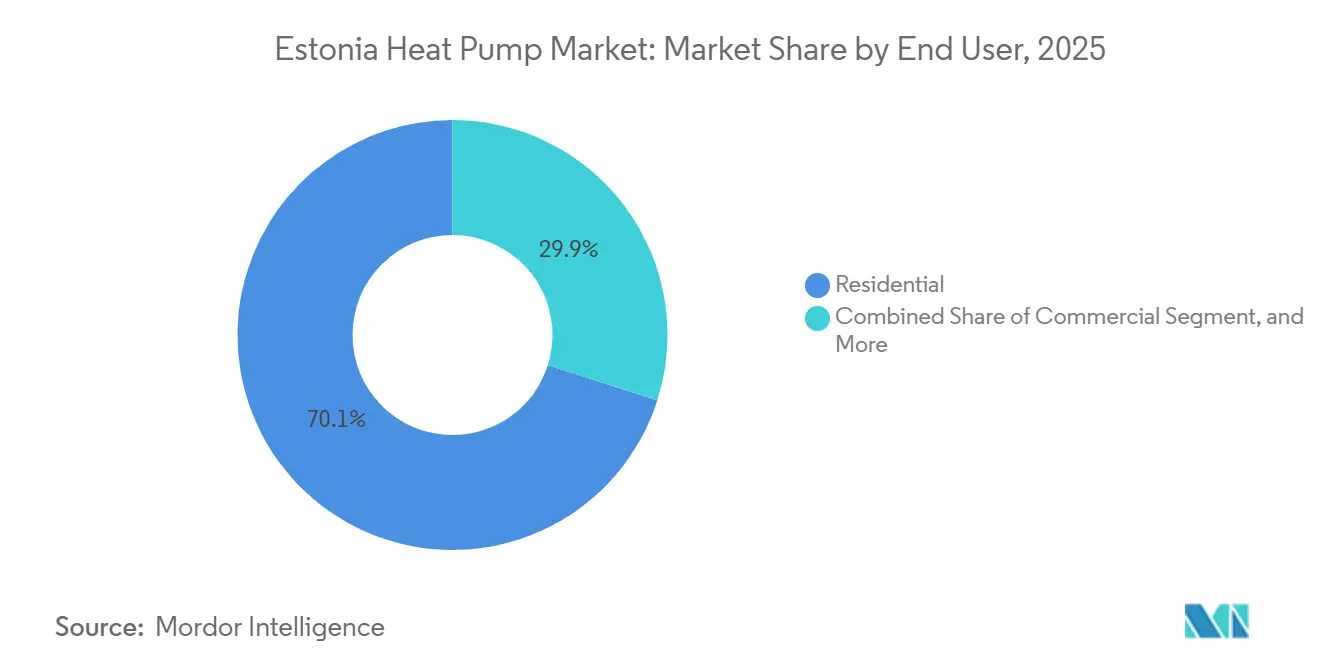

- By end user, residential customers held 70.09% revenue in 2025, yet the industrial segment is set to rise at a 4.87% CAGR through 2031.

- By installation, retrofit projects formed 63.27% of 2025 demand, but new-construction integrations are increasing at a 4.43% CAGR on the back of nearly-zero-energy mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Estonia Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive Government Incentives and EU Climate Funding | +1.2% | Tallinn, Tartu, Pärnu urban cores | Medium term (2-4 years) |

| Rapidly Rising Electricity-Gas Price Differential | +1.0% | District-heating zones nationwide | Short term (≤ 2 years) |

| Fit For 55 Decarbonization Mandates Accelerating Retrofits | +0.8% | National public-building stock | Long term (≥ 4 years) |

| Availability of Low-GWP Refrigerants and F-Gas Compliance | +0.5% | Commercial and industrial segments | Medium term (2-4 years) |

| Surge in Prefab Timber Modular Exports | +0.4% | Tallinn and Pärnu manufacturing hubs | Medium term (2-4 years) |

| Smart Grid Pilots Enabling Dynamic Tariffs | +0.3% | Pilot zones in Tallinn and Tartu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supportive Government Incentives and EU Climate Funding

In 2025 the Ministry of Climate earmarked EUR 28 million (USD 31.6 million) for home renovations, EUR 15.9 million (USD 18.0 million) for heating upgrades, and EUR 22.5 million (USD 25.4 million) for district networks. Grants covering up to 50% of equipment cost shorten residential paybacks from a decade to roughly six years. Municipal procurement rules in Tallinn oblige public buildings to use renewable heating, creating predictable tenders that stabilize installer revenue. Urban households exhaust subsidy windows within weeks, yet rural counties underspend because certified labor and three-phase connections remain scarce. This uneven drawdown fragments supply chains and limits bulk-purchase discounts, tempering the driver’s full impact on the Estonia heat pump market.[1]Ministry of Climate, “National Energy and Climate Plan 2030,” envir.ee

Rapidly Rising Electricity-Gas Price Differential

Gas prices jumped 23.9% in the first half of 2025, while wind-rich electricity traded at one-third that cost in January 2026.[2]Eurostat, “Natural Gas Price Statistics,” ec.europa.eu Ground-source units with seasonal COP 5 now deliver heat at EUR 0.018 kWh⁻¹, 72% below condensing boilers. District-heating firms pair large ammonia machines with 1.1 GWh thermal storage to buy power off-peak and sell heat on-peak, trimming delivered costs by another 14-24%.[3]Energy Storage News, “Estonia Unveils 1.1 GWh Heat Storage,” ess-news.com The spread continues to widen as offshore-wind interconnectors ramp up, keeping the advantage in favor of electrification. Investors therefore prioritize projects with hour-by-hour tariff optimization software to lock in predictable margins.

EU Fit-for-55 decarbonization targets accelerating retrofits

The recast Energy Performance of Buildings Directive took effect locally in June 2025, tightening primary-energy ceilings and nudging heating setpoints from 21 °C to 21.5 °C.[4]Riigi Teataja, “Minimum Requirements for Energy Performance,” riigiteataja.ee Heat pumps gain compliance credits because harvested renewable energy lowers the final primary-energy factor. Apartment associations in Tallinn bundle 50-unit retrofits to share grid-upgrade costs, shifting bargaining power from individual owners to collective buyers. Contractors secure bank financing on the strength of these multi-building contracts, allowing longer payment terms that ease cash flow. As codes tighten again after 2028, early adopters avoid future retrofit surcharges, further motivating take-up in the Estonia heat pump market.

Smart-grid-ready heat pumps linked to district-heating pilots

EU rules ban high-GWP blends such as R410A in new split systems from 2027. Suppliers pivot to propane and ammonia; Thermia’s R452B-charged Calibra Eco posted a seasonal COP 5.96 in Estonian trials. GEA’s ammonia compressors now raise 26-38 °C process heat to 82-95 °C for district networks, proving industrial viability.[5]RefIndustry, “GEA Installs Ammonia Heat Pumps at Utilitas Väo,” refindustry.com Installers invest in new safety training, widening the skilled-labor gap in the short term but future-proofing inventories. Early movers secure regulatory certainty and marketing leverage as consumers grow wary of stranded refrigerant assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Versus Legacy Biomass Boilers | -0.9% | Võru, Valga, Ida-Viru rural counties | Short term (≤ 2 years) |

| Skilled-Labor Bottleneck for Certified Installers | -0.7% | National, acute outside Tallinn | Medium term (2-4 years) |

| Grid Capacity Constraints in Rural Networks | -0.5% | Dispersed rural areas | Long term (≥ 4 years) |

| Strict Upcoming Noise-Emission Bylaws | -0.3% | Tallinn and Tartu historic cores | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Legacy Biomass Boilers

Residential air-to-water systems cost EUR 12,000-18,000 (USD 13,800-20,700), triple the price of pellet boilers that dominate forested regions. Half the country’s heating fuel is locally sourced biomass, anchoring a political coalition that resists subsidy reallocation away from timber interests.[6]Statistics Estonia, “Energy Statistics,” stat.ee Even a EUR 6,000 (USD 6,900) grant leaves six-to-nine-year paybacks where single-phase grids cap COP performance. Rural households therefore postpone heat-pump adoption until electricity-biomass spreads widen or carbon charges bite harder. This restraint caps near-term penetration in counties where wood supply remains abundant.

Skilled-Labor Bottleneck For Certified Installers

Only 120-150 EQF-level technicians graduate annually, well below the 300-plus target set in the National Energy and Climate Plan. Installation fees rose 20% in Tallinn during 2025, while lead times stretched to 12 weeks in Tartu and Narva. Some owners risk uncertified crews, voiding warranties and increasing callback costs that tarnish market reputation. Larger integrators recruit abroad, yet language barriers slow on-site coordination. Prolonged labor scarcity therefore tempers the growth trajectory of the Estonia heat pump market through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Setups Unlock New Rural Demand

Air-source units delivered 81.78% of 2025 revenue, confirming their dominance in the Estonia heat pump market share. Rural municipalities are now pairing those outdoor units with existing pellet or gas boilers, creating hybrid systems that are growing at a 5.24% CAGR through 2031. The blend lets homeowners hedge fuel-price swings while keeping comfort during deep-winter cold snaps. Water- and ground-source models together held roughly 17% of sales, but their higher efficiency often fails to offset drilling or water-intake costs in single-family retrofits. Utility-scale ammonia machines such as the 24 MW installation at Väo show how biomass CHP operators can recover low-grade flue heat and send it into district loops.

Prefab timber-module exporters have become surprise influencers. They preinstall compact air-source units on factory floors, cut on-site labor to half a day, and ship turn-key houses to Scandinavia. That practice pushes volume discounts back through the supply chain and keeps air-source pricing ahead of ground-loop alternatives. Borehole drilling, at EUR 8,000-12,000 for 150 m depths, remains a hard cost barrier outside large commercial lots. Permitting for groundwater extraction also slows water-source expansion, leaving hybrids to bridge Estonia’s biomass legacy and electric future.

By Technology: Ground-to-Water Rises With District Heating

Air-to-air systems captured 58.31% revenue in 2025 thanks to low upfront cost and built-in summer cooling. Air-to-water units followed, favored in radiator retrofits but still pricier by EUR 3,000-5,000 (EUR 3,450-5,760). Ground-to-water solutions are the fastest climber at a 4.96% CAGR, because district-heating companies need seasonal COP values above 5 to justify capital outlays. Thermia’s R452B-charged Calibra Eco logged a seasonal COP of 5.96 during 2025 field tests.

Regulatory quirks add nuance. New codes allow slightly higher heat-loss coefficients in buildings that specify air-to-water units, trimming insulation budgets and nudging small developers toward that technology even when lifetime efficiency favors ground loops. Water-to-water machines remain a niche tied to industrial waste-heat streams such as dairies and data centers. Propane-charged air-to-air models that sustain 100% capacity at -20 °C keep coastal buyers from considering deeper boreholes. Overall, shifting refrigerant rules and public-utility decarbonization goals position ground-to-water technology as the strategic play for high-load sites.

By Capacity: 50-200 kW Equipment Becomes Retrofit Sweet Spot

Units below 10 kW held 46.23% of 2025 shipments, reflecting years of residential adoption. The Estonia heat pump market size for these small systems is now plateauing, so suppliers chase mid-scale projects. Equipment rated 50-200 kW commands only about 13% of revenue today, yet it is scaling at a 4.72% CAGR because apartment associations and municipal owners can split costs across dozens of tenants. EnergySave’s cascade-ready monoblocs, stackable to 1.44 MW, lead this trend by replacing bespoke engineering with catalog-order simplicity.

Above-200 kW orders remain lumpy, driven by single district-heating tenders such as the 110 MW Paljassaare project. At the other end, the 10-50 kW band benefits from new near-zero-energy villas and small hotels, but competition is fierce and margins thin. Mid-scale integrators therefore emphasize remote monitoring contracts and performance guarantees to lock in service revenue. In saturated suburban districts the next growth lever will be replacing 2000-era first-generation units with today’s higher-COP models, again favoring modular mid-scale designs.

By Application: Process Heating Overtakes Cooling As Growth Driver

Space heating still generated 55.42% of 2025 turnover, a logical outcome in a country with more than 5,000 heating degree-days. Yet industrial and process heating is advancing at a 4.86% CAGR, a pace that will narrow the share gap by 2031. Food processors, timber kilns, and chemical reactors can now tap ammonia machines delivering 95 °C supply water and earn sub-five-year paybacks because natural gas prices jumped 23.9% in early 2025.

Cooling accounts for just below 12% of demand, but the 2025 rule change that lowered indoor setpoints to 26 °C is lifting reversible heat-pump installations in office towers and data centers. Domestic hot-water supply stays stable around 17% share, usually bundled with space heating. Agricultural drying and district-loop supply round out the smaller niches, each sensitive to site-specific waste-heat streams and feed-in tariffs.

By End User: Industry Jumps Ahead As Gas Loses Favor

Residential buyers still produced 70.09% of 2025 revenue, but saturation is visible in urban detached homes. The industrial slice, roughly 9% today, is expanding at a 4.87% CAGR as dairies and timber mills electrify boilers. E-Piim’s 6 MW installation in Paide proves the model, capturing waste refrigeration heat and cutting water use by 23,000 m³ a year.

Commercial uptake lags because landlord-tenant split incentives mute direct savings. Hotels and schools, where owners pay the energy bill, continue upgrading, but multitenant offices often defer large retrofits. Policy makers eye carbon-based property taxes to close that loophole. For now, the industrial user class holds the clearest upside, helped by zero-GWP refrigerants that future-proof capital spending.

By Installation: New-Build Integrations Narrow Retrofit Lead

Retrofits kept a 63.27% share in 2025, servicing Estonia’s Soviet-era apartment stock, yet new construction is rising at a 4.43% CAGR. Factory-installed units in exported timber modules shift market timing from post-occupancy upgrades to the design phase, locking in sales months earlier. In Tallinn’s Lasnamäe district, bundled 50-unit retrofits illustrate how collective decisions overcome the split-incentive hurdle.

Grid-connection delays remain the wild card. Developers sometimes install temporary resistance heaters while waiting eight weeks for three-phase service, then swap in heat pumps, adding EUR 2,000-3,000 (USD 2,300-3,450) per dwelling. As grid upgrades accelerate, the Estonia heat pump market share for new-build projects is set to close within ten percentage points of retrofits by decade-end. Forward-looking installers pre-book transformer capacity to keep that timetable on track.

Geography Analysis

Tallinn and Harju County produced about 58% of 2025 installations thanks to dense district-heating pipes and a concentration of 70% of the nation’s certified installers. Utilitas’s 110 MW Paljassaare wastewater plant, due online in winter 2026, will cover one-fifth of the capital’s heat load and push fossil share below 10%. Fast permitting and abundant three-phase capacity shorten urban lead times to six weeks, reinforcing a virtuous cycle of supplier clustering.

Tartu contributes roughly 17% of demand. The city’s Energy 2030 roadmap targets fossil-free district heating by the decade’s end, but smaller population limits economies of scale, so contractors travel from Tallinn, adding EUR 800-1,200 (USD 920-1,380) to project budgets. Pilot boreholes confirm viable ground-source potential, yet high drilling costs slow mass rollout. Pärnu and Saaremaa support a niche of reversible air-source units that serve holiday homes and spa hotels. Installations peak in summer when builders retrofit for the tourist season, and sandy soils favor easy outdoor-unit placement. Ida-Viru’s industrial corridor lags because ageing Soviet-era grids need EUR 50-80 million of upgrades before large electric loads can connect; only 26% of requested rural-network funding was secured in 2025.

Rural Võru and Valga counties, where pellets cost EUR 250-300 (USD 285-340) t⁻¹, show the slowest uptake. Paybacks exceed eight years, and many feeders lack three-phase service, so households stick with legacy boilers despite subsidies. Noise bylaws further constrain growth in Tallinn Old Town and Tartu Toomemägi, where outdoor units need EUR 500-800 (USD 570-920) wooden enclosures and strategic placement to meet the 40 dB night limit, nudging owners toward costlier ground-source alternatives .

Competitive Landscape

The market is moderately fragmented; no brand tops 15% revenue, and the combined share of the five largest equipment suppliers sits well under 50%. Global names Viessmann, Mitsubishi Electric, Ariston, NIBE, and Trane fill distributor showrooms, but local integrators Soojuskeskus, Sunergia, and Gaspal control on-site decisions through turnkey service bundles. That installer-led dynamic means catalog breadth, financing options, and after-sales response trump pure hardware efficiency in winning bids.

Utility-scale orders are reshaping vendor hierarchies. Friotherm won the EUR 100 million (USD 115) Paljassaare tender with four 110 MW centrifugal machines that will cover 20% of Tallinn’s district heat from 2026. GEA followed by supplying ammonia screw compressors at Väo, leveraging refrigeration pedigree and zero-GWP credentials to edge out traditional HVAC brands. Those wins highlight a divide: residential specialists face mature demand, while industrial refrigeration firms pivot into megawatt-scale district-heating conversions.

Mid-scale commercial retrofits create a different battleground. EnergySave markets cascade-ready R410A monoblocs scalable to 1.44 MW, pitching lower engineering overhead to apartment associations. Systemair bundles heat recovery ventilation, photovoltaic inverters, and cloud monitoring into one procurement, seeking recurring software subscriptions. Domestic producer Gapsal competes on Nordic-climate tuning and five-year warranties, but limited factory scale keeps prices above Asian imports. With refrigerant phase-downs looming, suppliers that move fastest to propane and ammonia portfolios gain a regulatory head start, while laggards risk inventory write-offs and lost distributor shelf space.

Estonia Heat Pump Industry Leaders

Viessmann Climate Solutions SE

Ariston Holding N.V.

Nilan A/S

Trane Technologies Plc

Systemair AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Utilitas commissioned a 1.1 GWh hot-water storage tank in Tallinn that lets ammonia heat pumps exploit off-peak wind power.

- November 2025: Construction progressed on Utilitas’s 110 MW wastewater-and-seawater heat-pump plant in Paljassaare, expected to meet 20% of Tallinn’s district-heating load from winter 2026.

- June 2025: GEA delivered four high-efficiency ammonia compressors to the Väo biomass CHP site, achieving COP 4-plus performance during the first heating season.

- May 2025: Ground broke on Estonia’s first 110 MW wastewater heat-pump facility, supplied by Friotherm, with EUR 100 million (USD 115 million) financing in place.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Estonian heat pump market as the annual revenue generated from the sale and installation of electrically-driven air-source, water-source, ground-source, hybrid, and exhaust-air heat pumps sized below 1 MW for space heating, space cooling, sanitary hot water, and selected low-temperature industrial loads. According to Mordor Intelligence, this market was worth USD 21.3 million in 2025.

We exclude pure chillers, air-conditioning splits, and second-hand units that are re-imported into Estonia.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

We interviewed Estonian wholesalers, certified installers in Harjumaa, utility engineers at Utilitas, and municipal retrofit program officers. Their insights on average selling prices, rebate uptake rates, and seasonal installation capacity bridged data gaps and challenged early assumptions before we locked the model.

Desk Research

We began by pulling baseline demand signals from open sources such as Eurostat trade codes 841861 and 841869, the Estonian Environment Agency's building energy statistics, the European Heat Pump Association's sales dashboards, and policy papers from the Ministry of Economic Affairs and Communications. Company filings, tender notices on Tenders Info, and patent counts from Questel added competitive color, while D&B Hoovers supplied historical revenue for key installers. A second pass gathered electricity-to-gas retail price spreads, district heating tariff bulletins, and national retrofit grant ledgers that inform payback calculations. The sources named illustrate the wider evidence pool; many additional references were tapped for triangulation and clarifications.

A follow-up scan of paid databases (Dow Jones Factiva for news flow and Marklines for OEM product launches) helped our analysts tie market inflections to corporate moves, ensuring that our desk work stayed current.

Market-Sizing and Forecasting

We used a top-down construction that starts with customs import volumes, converts them with weighted average selling prices, and then adjusts for locally produced units and re-exports. Targeted bottom-up checks (sampled OEM shipments times installer margins) validated those totals. Key variables inside our workbook include heat pump stock per 1,000 households, annual residential retrofit permits, electricity versus gas price differential, rebate budget absorption, and district heating carbon intensity. Multivariate regression links these drivers to historical sales and projects demand through 2030, while scenario analysis stress tests price shock and policy delay cases. When bottom-up estimates diverge by over five percent, we rerun price bands before finalizing the curve.

Data Validation and Update Cycle

Every quarter, our analysts rerun anomaly scans that flag sharp volume or price swings; flagged series trigger call-backs to at least two prior respondents. The full report is refreshed annually, and a fast-track update is issued whenever major subsidy rules or grid tariff revisions surface.

Why Our Estonia Heat Pump Baseline Commands Reliability

Published numbers differ because firms treat refurb sales, ASP evolution, and currency bases in unique ways. We openly document our scope, refresh cadence, and driver set, which lets clients track each assumption.

Benchmark of Current-Year Market Values

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.3 M (2025) | Mordor Intelligence | - |

| USD 15 M (2024) | Regional Consultancy A | Omits hybrid and exhaust-air units; uses list instead of transacted prices |

| EUR 6 M (2016) | Trade Journal B | Historical customs only, no retrofit channel or price inflation adjustment |

The comparison shows estimates shrink when hybrid systems, current ASPs, and retrofit demand are overlooked. By blending transparent scope choices with live primary checks, Mordor Intelligence delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the projected size of the Estonia heat pump market by 2031?

The market is forecast to reach USD 27.52 million in 2031, up from USD 22.31 million in 2026.

What share of Estonian residential heating is already served by heat pumps?

By the end of 2025, 34% of households had units installed, equal to 29.3 systems per 1,000 dwellings.

How fast are hybrid air-source systems expected to expand through 2031?

Hybrid configurations that combine air-source technology with biomass or gas backups are projected to grow at a 5.24% CAGR from 2026-2031.

Which capacity band is seeing the quickest uptake among commercial building owners?

Mid-scale 50-200 kW systems, common in apartment blocks and municipal facilities, are advancing at a 4.72% CAGR over the same period.

Why are high-temperature ammonia units gaining traction in Estonian process plants?

Ammonia refrigerant has zero global-warming potential and can reach 95 °C, letting food, timber, and chemical sites replace gas boilers with 3-5-year paybacks.

What is the main obstacle to faster rural adoption outside Tallinn and Tartu?

Limited three-phase grid capacity, paired with higher upfront costs versus pellet boilers, stretches rural paybacks to eight or more years.

Page last updated on: