Hungary Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

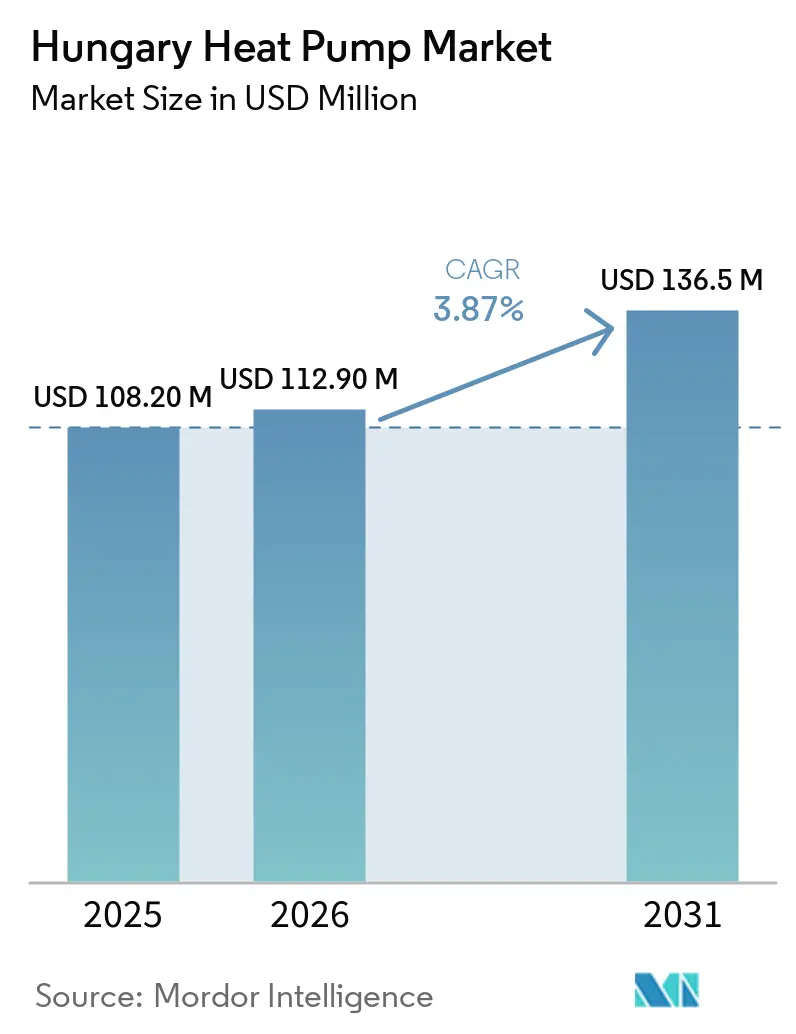

| Base Year Market Size (2025) | USD 108.20 Million |

| Market Size (2026) | USD 112.90 Million |

| Market Size (2031) | USD 136.5 Million |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Heat Pump Market Analysis by Mordor Intelligence

The Hungary heat pump market size is expected to increase from USD 108.2 million in 2025 to USD 112.9 million in 2026 and reach USD 136.5 million by 2031, growing at a CAGR of 3.87% over 2026-2031. Persistent policy support, the European Union’s decarbonization mandate, and Hungary’s region-leading low household electricity prices together underpin steady demand, yet adoption is still gated by high upfront equipment costs and a tight refrigerant phase-down timeline that pressures manufacturers to redesign products midcycle. Budapest’s dense installer base and higher disposable incomes accelerate residential retrofits, while commercial buyers gain from time-of-use tariffs that magnify savings when daytime solar generation peaks. Hardware prices are trending downward as regional factories in Hungary, Poland, and the Czech Republic reach scale, shortening payback periods and encouraging turnkey offerings that bundle financing, installation, and service. Although distribution grid bottlenecks persist in several rural corridors, the national solar build-out provides off-peak capacity that utilities can dispatch to smart heat pump fleets, anchoring long-term electricity cost stability.

Key Report Takeaways

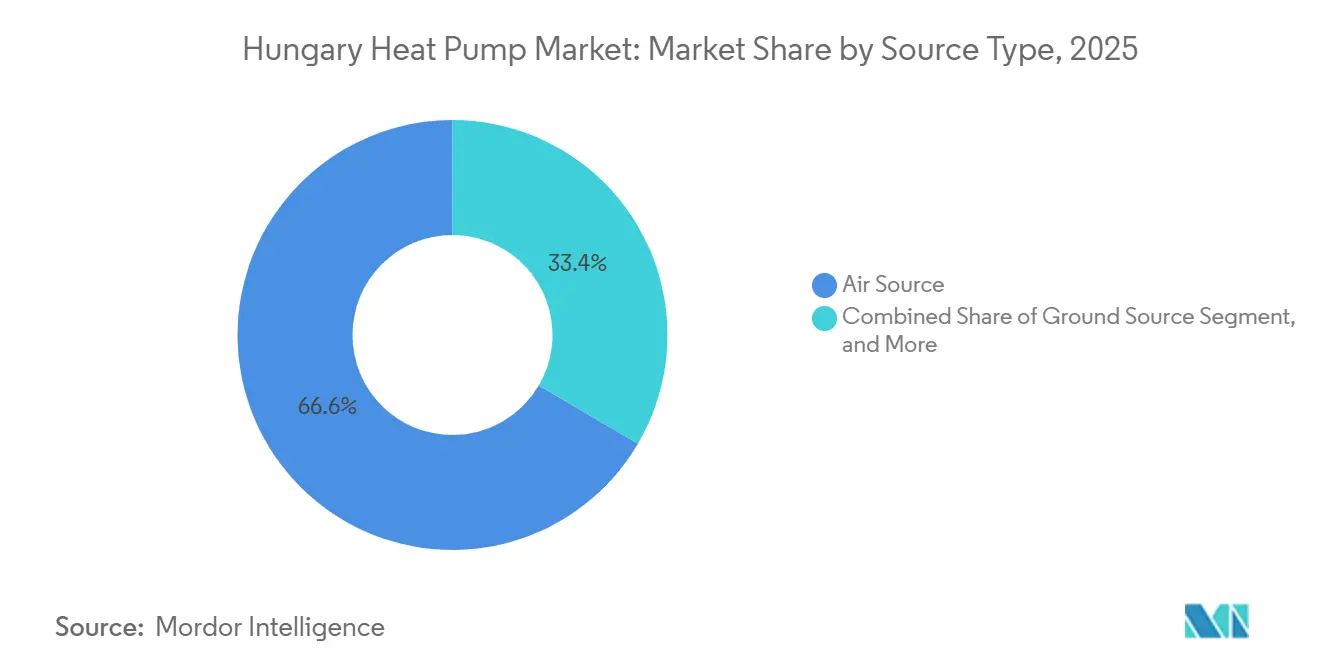

- By type, air source systems commanded 66.57% of Hungary heat pump market share in 2025 and continue to anchor revenue leadership.

- By technology, the ground-to-water configuration is projected to expand at the fastest 4.42% CAGR through 2031.

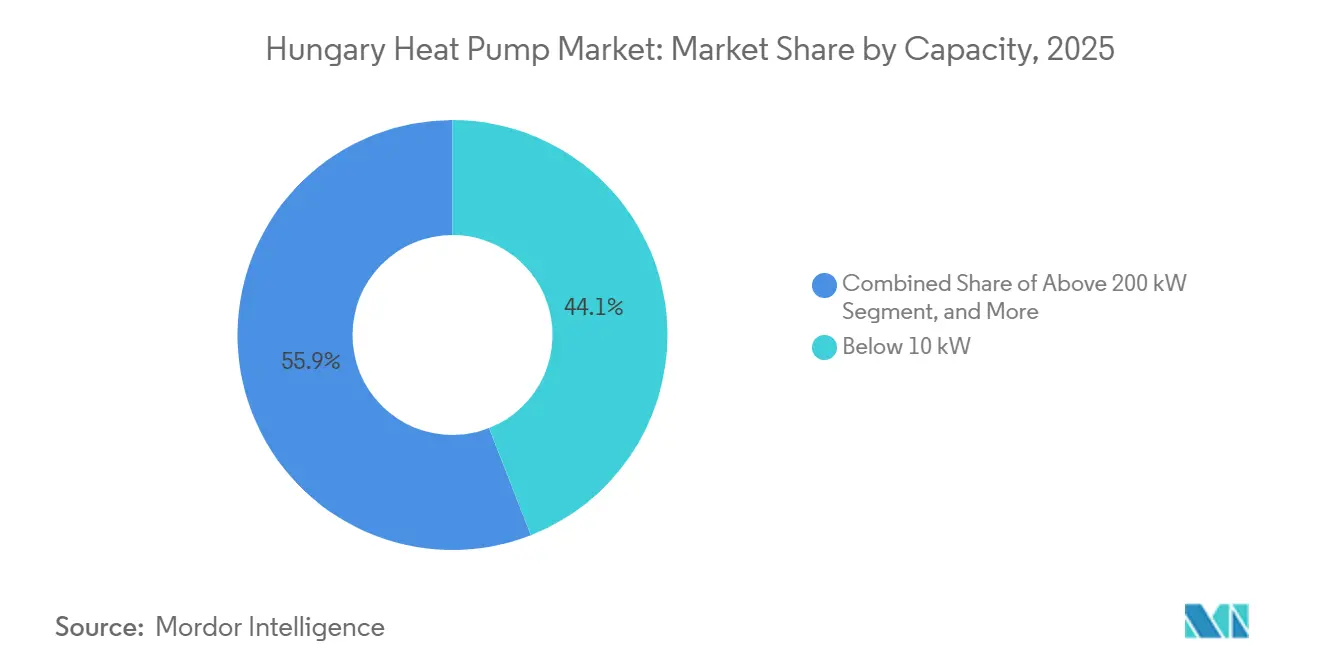

- By capacity, units rated 10-50 kilowatts are forecast to record the highest 4.51% CAGR between 2026-2031.

- By application, domestic and sanitary hot water accounted for the quickest 5.07% growth trajectory over the same horizon.

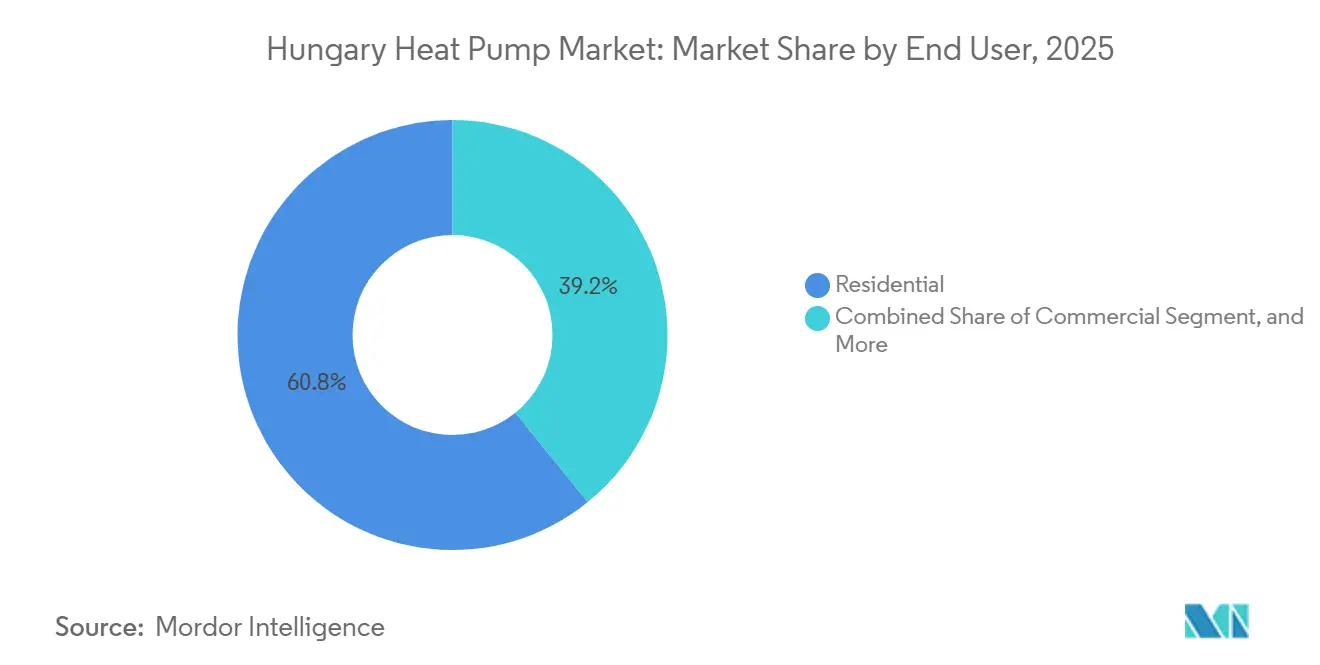

- By end user, the commercial segment is advancing at a robust 4.23% CAGR, narrowing the historical gap with residential installations.

- By installation, new-build integration increases at a 4.37% CAGR, confirming that project specifications increasingly favor electrified heating from day one.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Hungary Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive Government Incentives and Rebates | +1.2% | National, strongest in settlements under 5,000 residents | Short term (≤ 2 years) |

| EU Fit-for-55 Decarbonization Mandate | +0.9% | National, aligned with EU directives | Medium term (2-4 years) |

| Rising Energy Prices Accelerating Payback | +0.7% | National, commercial and industrial clusters | Short term (≤ 2 years) |

| Falling Heat Pump Hardware Costs | +0.5% | National, factory clusters in Central Europe | Medium term (2-4 years) |

| Surging Demand for Grid Balancing via Smart Heat Pumps | +0.3% | Solar-rich regions above 20% renewable share | Long term (≥ 4 years) |

| National HVAC Technician Upskilling Programs Expanding Installation Capacity | +0.3% | Training centers in seven major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supportive Government Incentives and Rebates

Hungary’s Otthonfelújítási Program allocated HUF 108.24 billion (USD 300.7 million) in 2024 to subsidize residential energy upgrades, offering households up to HUF 6 million (USD 16,700) in blended grants and zero-interest loans that directly lower net purchase prices.[1]Hungarian Government, “Otthonfelujitasi Támogatás,” gov.hu The Vidéki Otthonfelújítási Program extends a 50% subsidy capped at HUF 3 million (USD 8,300) to settlements with fewer than 5,000 residents, where disposable incomes are lower and awareness lags urban centers. Point-of-sale rebates under the Hitelesített Energiamegtakarítás and Takarékos Otthon schemes cut equipment invoices by 10-40%, removing liquidity constraints that typically delay retrofit commitments. An additional EUR 415 million (USD 456.5 million) channelled from the EU Recovery and Resilience Facility funds roughly 31,000 household installations, embedding electrified heating deep into Hungary’s post-pandemic stimulus.[2]European Commission, “Recovery and Resilience Facility,” europa.eu Layered together, these mechanisms compress residential payback to fewer than five heating seasons, positioning the Hungary heat pump market as the default replacement path for aging gas boilers.

EU Fit-for-55 Decarbonization Mandate

The Energy Performance of Buildings Directive phases out standalone fossil-fuel boilers in new buildings from 2030, effectively redirecting all future construction budgets toward electrified alternatives.[3]European Commission, “Energy Performance of Buildings Directive,” europa.eu Hungary’s transposition of the Renewable Energy Directive raises the renewable share in buildings to 49% by 2030, compelling utilities and developers to pair rooftop solar with heat pumps in both residential and commercial segments. Emissions trading will extend to building fuels in 2028, adding 15-25% to the operating cost of conventional gas heating and thereby widening the lifetime economic spread in favor of electric systems. The EUR 65 billion (USD 71.5 billion) Social Climate Fund earmarks targeted compensation for vulnerable households, ensuring policy equity and sustaining demand in lower-income districts. National planners target 400 megawatts of installed capacity across 100,000 systems by 2030, a near-tripling versus the 2019 baseline that illustrates the structural pull of the Fit-for-55 package.

Rising Energy Prices Accelerating Payback

Although Hungary retained the European Union’s lowest residential electricity tariff at EUR 10 (USD 11) per 100 kWh in early 2025, natural gas prices climbed 16% during the same window, widening the running-cost delta that determines homeowner economics. Solar generation surpassed 20% of national output in 2025, flattening midday wholesale prices and enabling distribution system operators to offer deep off-peak discounts that heat pump owners can harvest with thermal storage. Commercial buyers, responsible for 39.17% of 2025 revenue, increasingly treat heat pumps as hedges against volatile gas contracts, installing larger buffer tanks to maximize arbitrage across hourly tariff spreads. The International Energy Agency notes that space heating still accounts for 71% of residential energy use, magnifying savings when a fossil boiler is swapped for an electric compressor. As geopolitical risk continues to burden imported gas, the cost-saving narrative grows self-reinforcing, further sustaining Hungary heat pump market momentum.

Falling Heat Pump Hardware Costs

Qvantum’s EUR 38 million (USD 41.8 million) purchase of Electrolux’s Nyíregyháza plant, followed by an on-site R and D center in 2025, demonstrates that local manufacturing shortens supply lines and trims bill-of-materials expense.[4]Qvantum, “Qvantum Opens R and D Lab in Hungary,” qvantum.com Panasonic will commit EUR 320 million (USD 352 million) to triple Pilsen factory output to 1.4 million units annually by 2030, leveraging 80 industrial robots that lift productivity and push unit prices down 20-25%.[5]Panasonic, “Panasonic Invests EUR 320 Million in Czech Heat Pump Factory,” news.panasonic.com Bosch has earmarked over EUR 1 billion (USD 1.1 billion) for European capacity, including a new Dobromierz, Poland facility building R-290 propane platforms at lower component cost than legacy R-410A units.[6]Bosch, “Bosch Invests Over EUR 1 Billion in European Heat Pump Production,” bosch-press.com The mandated switch to natural refrigerants removes a surcharge historically embedded in high-GWP blends, and as cumulative regional volumes rise, analysts project 15-20% real hardware price erosion between 2025-2031. These trends jointly erode the capital barrier, enlarging the addressable base for the Hungary heat pump market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CapEx Versus Gas Boilers | -0.8% | Nationwide, acute in low-income rural settlements | Short term (≤ 2 years) |

| Stringent F-Gas Refrigerant Phase-Down Regulations | -0.6% | Aligned with EU Regulation 2024/573 milestones | Medium term (2-4 years) |

| Rural Distribution Grid Capacity Bottlenecks | -0.3% | Corridors such as Létavértes-Debrecen Dél | Medium term (2-4 years) |

| Limited Awareness Outside Budapest Reduces Conversion Rates | -0.2% | Settlements under 5,000 residents | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront CapEx Versus Gas Boilers

Typical 4-16 kilowatt heat pump packages retail for GBP 6,500-8,500 (USD 8,200-10,700), while a replacement gas boiler costs GBP 2,000-3,000 (USD 2,500-3,800), leaving a funding gap that subsidies only partially close. In the Bükkalja rural cluster, the median disposable income of EUR 4,750 (USD 5,225) means the differential exceeds an entire year of take-home pay, muting demand despite environmental intent. Although the Otthonfelújítási Program covers up to HUF 6 million (USD 16,700), applicants face energy audits and contractor quotes that prolong upgrade cycles by six-to-twelve months and add friction costs seldom captured in headline subsidy rates. Small enterprises share similar liquidity constraints because green financing lines remain thin, and banks often require extensive collateral for energy retrofits. As manufacturing scale drives costs lower and specialized credit products mature, this restraint will fade, yet in the immediate horizon it clips Hungary heat pump market penetration below the technically viable ceiling.

Stringent F-Gas Refrigerant Phase-Down Regulations

EU Regulation 2024/573 bans single-split systems with refrigerant GWP above 750 from 2025 and requires all self-contained units below 12 kilowatts to use GWP < 150 fluids by 2027, forcing an accelerated pivot to flammable A3 refrigerants such as R-290 propane. Manufacturers must redesign heat exchangers, compressors, and enclosure layouts to respect charge limits, incurring R and D expense and field-testing delays that temporarily constrain product availability. Installers face a mandatory certification upgrade to handle A3 fluids, and training throughput is finite despite the national vocational curriculum adding 400 hours of specialized coursework. Distributors hesitate to stock transitional R-32 or R-454B inventory that risks obsolescence when the split-system ban arrives in 2035, squeezing working capital and elongating delivery times. Until the supply chain recalibrates around propane-ready components and technician capacity scales up, the regulation exerts downward pressure on Hungary heat pump market growth even as it secures long-run climate compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Leads, Ground Source Gains in Commercial Builds

Air source units captured 66.57% of 2025 revenue within the Hungary heat pump market, reflecting modest site requirements, quicker installation timelines, and suitability for detached housing where borehole drilling often faces zoning limits. Single-fan outdoor modules drop seamlessly onto paved driveways and integrate with existing radiator circuits once flow temperatures fall to 45-55 °C, giving contractors predictable margins and homeowners minimal disruption. Ground source systems, though more capital intensive, deliver coefficients of performance above 4.0 even during sub-zero winters, a trait that appeals to office parks and retail estates seeking green building labels and 20-year life-cycle savings. Water source and hybrid variants together account for a sliver of sales, restricted by access to lakes or rivers and policy headwinds against fossil-fuel backup burners.

Regional manufacturing momentum is shaping technology preferences. Panasonic’s enlarged Pilsen plant will ship R-290 propane air-to-water models engineered for ambient lows of –15 °C, reinforcing air source volume dominance. Simultaneously, Qvantum’s Nyíregyháza research lab prototypes air source compressors calibrated for Hungary’s continental climate swings, injecting domestic know-how into export-ready designs. Commercial developers choosing between ground loops and rooftop solar-plus-air units now model 25-year present values rather than first-cost alone, a shift that lifts ground source uptake even while air source remains the Hungary heat pump market reference standard for suburban homeowners.

By Technology: Air-To-Water Dominates, Ground-To-Water Climbs Fast

Air-to-water systems accounted for 41.89% of 2025 turnover, a function of installed base compatibility since most Hungarian homes already operate hydronic radiators that can accept 50 °C supply once insulation is upgraded. Installers minimize labor by retaining pipework, adding buffer tanks, and rebalancing loops, keeping downtime short and customer satisfaction high. Ground-to-water configurations, however, register the swiftest 4.42% CAGR through 2031, fuelled by district heating substations and industrial plants that value constant thermal output and plan on multidecade horizons. Air-to-air ductless setups secure incremental cooling comfort for apartments, yet the Energy Performance of Buildings Directive tilts preference toward hydronic solutions that readily integrate with solar thermal collectors and domestic hot-water cylinders.

Factory investments underscore each trajectory. Johnson Controls is adding 1,800 square meters of test space in Aarhus to validate megawatt-scale ammonia machines destined for Nordic and Central European district grids, proving viability for dense Hungarian neighborhoods contemplating gas-to-heat-pump conversions. Meanwhile, LG’s Therma V R290 Monobloc debuted in 2025 with A+++ labels down to -15 °C, showcasing market-ready propane units that satisfy the 2027 GWP-150 ceiling. As natural-refrigerant portfolios mature, cost premiums shrink, reinforcing air-to-water’s hold on everyday retrofits while offering ground-to-water buyers an even stronger efficiency proposition, thus enlarging the Hungary heat pump market size for both segments.

By Capacity: Sub-10 Kilowatts Still Largest, 10-50 Kilowatts Accelerates

Units below 10 kilowatts represented 44.06% of 2025 demand, mapping neatly to 120-150 square-meter detached homes that dominate Hungary’s housing stock and require 6-8 kilowatts following envelope upgrades. Split-level suburban dwellings in the Budapest commuter belt often pair 8 kilowatt outdoor modules with 200 liter buffer tanks, a configuration installers can complete within two days under the Otthonfelújítási rebate timetable. The 10-50 kilowatt class grows at a compelling 4.51% CAGR through 2031 as multi-family blocks and small commercial properties phase out gas boilers, often deploying cascaded arrays of three 15 kilowatt machines to avoid costly grid service upgrades. Capacities above 50 kilowatts serve warehouses, schools, and process industries, while district heating substations employ hundreds-kilowatt machines, but these remain numerically limited despite high revenue visibility.

Strategic consolidation feeds this mid-range surge. Bosch’s USD 8 billion takeover of Johnson Controls’ residential and light commercial portfolio unifies R-454B and propane designs under one umbrella, unlocking component synergies that deflate price points in the 20-40 kilowatt sweet spot. Compliance dynamics also shape redesign cycles, because R-410A, long favored for 30 kilowatt rooftops, exceeds the 2025 GWP 750 cap, requiring rapid migration to R-32 or propane architectures. As policymakers enforce stricter split-system rules, manufacturers intensify innovation in sleeve compressors and micro-channel heat exchangers that retain footprint but halve greenhouse impact, ultimately sustaining growth across all capacity brackets of the Hungary heat pump market.

By Application: Space Heating Dominates, Domestic Hot Water Surges Ahead

Space heating applications generated 58.21% of 2025 revenue, the largest single slice of Hungary heat pump market size, because continental winters impose more than 3,000 heating degree days and legacy building envelopes still rely on high heat loads. Detached homes in Nógrád and Heves counties typically replace gas boilers with 8 kilowatt air-to-water units coupled to low-temperature radiators, while suburban developers upgrade larger villas with inverter-driven 12 kilowatt monoblocs that moderate peak draw. Industrial bakeries and beverage processors also route waste heat into hydronic loops, raising full-year capacity utilization and cushioning project economics against seasonal swings.

Domestic and sanitary hot water is the fastest growing slice, expanding at a 5.07% CAGR through 2031 as the Energy Performance of Buildings Directive compels fossil-free water heating in all new dwellings after 2030. The component’s share of Hungary heat pump market size climbs each year because rooftop photovoltaic penetration lets owners energize storage cylinders with midday surplus, flattening grid demand curves. Heat-pump-ready cylinders up to 500 liters now retail below EUR 1,200 (USD 1,320), removing a prior cost hurdle for multipurpose systems. Large apartment blocks in Budapest’s XIII district have started replacing central gas calorifiers with cascaded 35 kilowatt heat pump banks, a template that provincial municipalities plan to replicate under the Green District Heating Programme.

By End User: Residential Still Leads, Commercial Footprint Broadens

Residential customers accounted for 60.83% of 2025 installations, consolidating decades of government policy that earmarks subsidies mainly for single-family homes and small condominiums. Typical households finance upgrades through the Otthonfelújítási Program’s blended grant-and-loan structure, while independent installers bundle roof insulation and window retrofits to guarantee the mandated 30% primary-energy cut. Consumer electronics retailers in Budapest, Debrecen, and Győr increasingly stock 6-9 kilowatt monoblocs beside condensing dryers and induction cooktops, normalizing the category in daily retail traffic and enlarging brand awareness.

Commercial deployments advance at a 4.23% CAGR, closing the historical gap as office parks, hypermarkets, and logistics sheds migrate toward Science Based Targets initiative compliance. Property managers report that integrating heat pumps with building-management systems slashes HVAC operating overhead by 25-30%, a metric that resonates with asset-value appraisers and drives repeat orders. The commercial slice therefore rises steadily in Hungary heat pump market share while the absolute Hungary heat pump market size grows on both axes. Industrial end users remain a minority but adopt high-temperature ammonia machines for process water heating above 80 °C, reducing Scope 1 emissions and unlocking EU Innovation Fund support for pilot lines.

By Installation: Retrofit Rules, New Build Integration Gains Momentum

Retrofit projects held 56.12% of 2025 demand, matching a housing stock in which seven of every ten dwellings date before 2000 and carry gas boilers at end-of-life. Installers prefer compact R-290 outdoor modules that slide into prior boiler footprints and reuse domestic radiator circuits once thermostatic valves are swapped for low-temperature models, minimizing tenant disruption and drywall work. Turnkey providers such as Aira streamline complex paperwork by packaging energy audits, mechanical labor, and tax-credit filing into an online order flow that delivers a functioning system inside eight weeks, including grid notification.

New construction integration grows at 4.37% CAGR to 2031 because architects now embed ground loops or rooftop unit stubs at design stage, eliminating costly post-handover retrofits. Hungary’s zero-fossil requirement for new buildings from 2030 thereby fuels steady incremental volume, particularly in outer-ring suburbs where land plots support horizontal ground-loop fields. Developers capitalize on smart-grid readiness by wiring Modbus gateways and thermal-storage controllers during shell construction, ensuring the finished property can participate in utility demand-response pools. The forward pipeline therefore lifts new-build share of Hungary heat pump market size without eroding retrofit demand, driving a balanced workload across the installer network.

Geography Analysis

Budapest and its commuter belt remained the epicenter of demand in 2025, capturing more than one-third of Hungary heat pump market share as higher disposable incomes, dense installer coverage, and plentiful rooftop solar converge to shorten financial payback. The capital’s district heating grid complicates multi-unit conversions since central substations still burn natural gas, yet detached homes in XII and III districts replace obsolete condensing boilers with 6-12 kilowatt air source units to capitalize on generous metered tariffs. Installers note that city-center apartment associations postpone adoption until 2027, when low-GWP split units reach commercial maturity and avoid shaft ventilation retrofits.

Western border counties such as Győr-Moson-Sopron and Vas outperform national averages because cross-border technician mobility from Austria fills labor gaps and brings best-practice installation standards. Corporate campuses along the M1 motorway routinely specify cascaded 20-40 kilowatt arrays, leveraging industrial heat-recovery chillers during shoulder seasons. Meanwhile, local distributors forward-stock spare compressors and expansion valves sourced from Vienna hubs, cutting lead times that traditionally hampered rural jobs.

Eastern counties, Hajdú-Bihar, Szabolcs-Szatmár-Bereg, and Borsod-Abaúj-Zemplén, lag despite elevated rural subsidies because median incomes remain well below the national mean and residents prioritize stove upgrades or façade insulation first. Grid headroom along the Létavértes-Debrecen Dél feeder constrains new service connections, forcing queue times that dilute consumer enthusiasm. Qvantum’s plant in Nyíregyháza, however, seeds regional skills growth by hiring 400 staff and running monthly propane-safety workshops for independent installers, a policy that is expected to raise penetration curves from 2027 onward.

Competitive Landscape

Global incumbents Panasonic, Bosch, Mitsubishi Electric, LG, Samsung, and Daikin each hold single-digit slices, leaving the field fragmented and intensely contested. Panasonic’s expanded Pilsen plant, targeting 1.4 million units annually by 2030, positions the company to undercut rivals on air-to-water systems in the 6-12 kilowatt sweet spot, while Bosch’s USD 8 billion Johnson Controls acquisition unifies R-454B and propane designs under one brand umbrella. Mitsubishi Electric competes on hyper-heating inverter performance down to -25 °C ambient, a specification attractive to mountain rentals in Mátra and Börzsöny ranges, whereas LG courts retail chains with compact R-290 monoblocs that fit existing appliance aisles.

Regional specialist Qvantum leverages its Nyíregyháza base to tailor firmware for Hungarian climate cycles and harmonize bill-of-materials with local supply chains, shaving logistics overhead and securing fast-track EcoDesign approvals. GIMEK Zrt. differentiates via turnkey district-heating modules up to 250 kilowatts, sold to municipal utilities seeking to halve natural gas dependence by 2030. Vertical integrator Aira commands installer mindshare by bundling zero-interest payment plans, a move that expands the company’s revenue capture beyond hardware into lifetime service contracts and performance guarantees.

Technology roadmaps revolve chiefly around refrigerant choice. Early adopters of R-290 propane gain regulatory certainty ahead of the 2027 GWP 150 cliff and avoid costly field retrofits of transitional R-32 units. Daikin’s “Stand By Me” certification ecosystem now counts more than 3,000 technicians across Central Europe, signaling a race to lock in installer loyalty before price convergence squeezes differentiation. Given that no vendor controls above 15% of domestic shipments, Hungary heat pump market concentration remains moderate, inviting both consolidation and niche disruption through 2031.gin while easing consumer sticker shock. Technology roadmaps converge on natural-refrigerant models. Start-ups focused solely on propane circuits gain mind-share as EU F-gas quotas tighten. Large incumbents respond with R-290 product lines and training hubs; Daikin’s Budapest experience centre exemplifies the shift toward solution selling rather than unit shipping. Integrated PV-plus-battery-plus-heat-pump packages emerge as the next battleground, blurring categorical boundaries between HVAC and distributed generation.

Hungary Heat Pump Industry Leaders

Panasonic Holdings Corporation

Systemair AB

Johnson Controls International Plc

Trane Technologies Plc

Trox GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Panasonic announced a EUR 320 million (USD 352 million) expansion of its Pilsen heat pump plant, tripling floor space and automating production with 80 industrial robots to reach 1.4 million R-290 units annually by 2030.

- August 2025: Bosch completed its USD 8 billion purchase of Johnson Controls’ residential HVAC and light commercial division, integrating refrigerant R-454B know-how into Bosch’s European product pipeline.

- August 2025: Aira raised EUR 150 million (USD 165 million) to enlarge training academies and 18 regional hubs, including a Polish factory that ships to Hungary within 24 hours.

- April 2025: Qvantum opened a 45-engineer R and D laboratory at its Nyíregyháza factory to develop minus-20 °C optimized air source compressors for Central European markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Hungarian heat pump market as the yearly revenue generated from sales of factory-built air, ground, and water-source heat pump systems up to 50 kW that provide space heating, cooling, or domestic hot water to residential, commercial, and small industrial buildings. Equipment destined for mobile refrigeration, large-scale district plants, and pure chiller duty is excluded.

Scope exclusion: sales of electric resistance heaters, gas or biomass hybrid boilers, and building-integrated PV-thermal units lie outside this analysis.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview Hungarian installers, building services engineers, and energy agency officials across Budapest, Gyor, and Debrecen, then poll distributors on quarterly ASP shifts and subsidy uptake. These conversations validate demand drivers flagged in desk work and clarify installer margin structures before we lock model assumptions.

Desk Research

We begin with open-access statistical feeds such as Eurostat energy price files, the Hungarian Central Statistical Office's building stock tables, and customs codes extracted from Access2Markets. Trade group yearbooks from the European Heat Pump Association, the European Heating Industry, and the Joint Research Centre supply unit sales, stock, and policy data, while peer-reviewed articles on shallow geothermal economics ground our cost benchmarks. Company 10-Ks, investor decks, and local press releases enrich competitive mapping. Proprietary pulls from D&B Hoovers and Dow Jones Factiva give us financials and transaction news that free sources miss. The list above is illustrative; many further references, including regional patent abstracts from Questel, underpin individual data points.

Market-Sizing & Forecasting

We reconstruct 2024 revenue by applying weighted average selling prices, gathered from channel checks, to EHPA-verified unit shipments. A top-down cross-check converts household counts, gas-to-HP conversion rates, and average capacity per dwelling into a parallel demand pool, which is then reconciled with the bottom-up roll-up. Key quantitative levers include electricity-to-gas tariff ratios, renewable quota trajectories, residential renovation grant disbursements, installer headcount growth, and median heat loss of pre-1990 housing. Forecasts to 2030 employ multivariate regression where market value responds to those five drivers; scenario bounds are stress tested with expert panels. Gaps in distributor data, especially on e-commerce volumes, are bridged with conservative uptake coefficients derived from adjacent HVAC categories.

Data Validation & Update Cycle

Before release, we triangulate model outputs against independent indicators such as inverter imports and utility H-tariff enrollments, flagging variances exceeding seven percent for senior review. Reports refresh annually, with off-cycle revisions triggered by subsidy rule changes or energy price shocks; a final analyst pass ensures clients receive the latest numbers.

Why Our Hungary Heat Pump Baseline Carries Proven Credibility

Published estimates rarely align because each issuer picks different scopes, metrics, and refresh rhythms, a reality that often confuses first-time buyers. We acknowledge those divergences upfront.

Key gap drivers in Hungary stem from whether sales or installed stock are measured, if commercial projects are folded in, and how currency conversion and after-market pricing are handled. Our approach, anchored on paid ASP feeds and dual validation paths, avoids the under or over counting that surfaces when alternative publishers rely solely on shipments or single-year surveys.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 108.2 million (2025) | Mordor Intelligence | - |

| 15,432 units (2022) | Regional Consultancy A | Tracks residential unit sales only and leaves price dispersion unmodeled |

| 36,224 units stock (2022) | Industry Association B | Reports cumulative installations, omits retirements and revenue valuation |

In sum, Mordor's disciplined mix of granular pricing, dual-path volume checks, and yearly refresh cycles delivers a balanced, transparent baseline that decision makers can trace back to clear variables and readily reproduce.

Key Questions Answered in the Report

What is the projected value of the Hungary heat pump market in 2031?

The market is forecast to reach USD 136.5 million by 2031, reflecting a 3.87% CAGR from 2026-2031.

Which heat pump type currently leads adoption in Hungary?

Air source models hold 66.57% share because they carry lower installation costs and fit typical single-family plots.

Why are domestic hot-water heat pumps growing fastest?

EU building rules ban fossil-fuel water heating in new homes from 2030, driving a 5.07% CAGR in this application.

How do subsidies impact consumer payback?

Layered national and EU rebates cut upfront costs enough to bring residential payback under five heating seasons.

What refrigerant will dominate new units after 2027?

R-290 propane is emerging as the default low-GWP fluid because it satisfies the EU's GWP 150 threshold for small units.

Are grid constraints a major barrier in rural areas?

Yes, hosting-capacity limits along specific feeders delay connections, but targeted upgrades and smarter planning are under way.

Page last updated on: