Greece Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

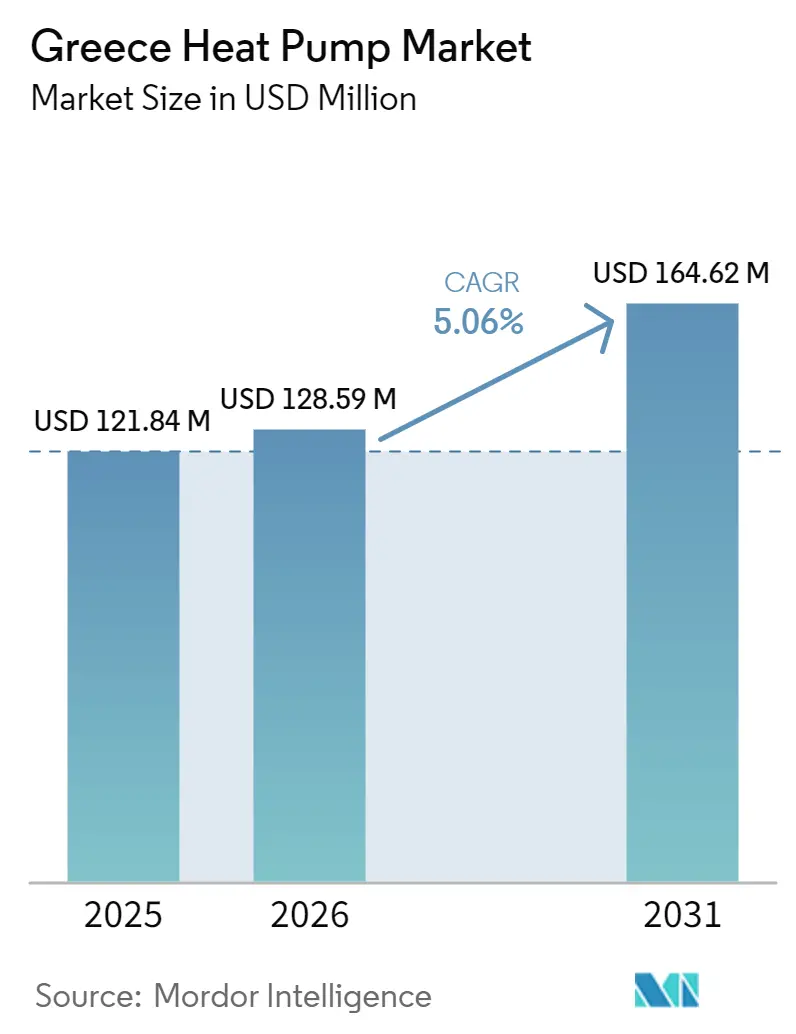

| Base Year Market Size (2025) | USD 121.84 Million |

| Market Size (2026) | USD 128.59 Million |

| Market Size (2031) | USD 164.62 Million |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Heat Pump Market Analysis by Mordor Intelligence

The Greece heat pump market size is expected to grow from USD 121.84 million in 2025 to USD 128.59 million in 2026 and is forecast to reach USD 164.62 million by 2031, growing at a CAGR of 5.06% over 2026-2031. Policy-driven electrification, generous household subsidies, and the impending phase-out of oil boilers keep demand momentum intact. Utility-backed bundled offers simplify purchasing and financing, while manufacturer investments in low-GWP refrigerant platforms anticipate the 2027 F-Gas restrictions. Installation growth is tempered by a certified-installer shortage and island-grid congestion, yet smart hybrid configurations paired with rooftop PV help smooth seasonal load swings and improve lifetime economics for households and hotels.

Key Report Takeaways

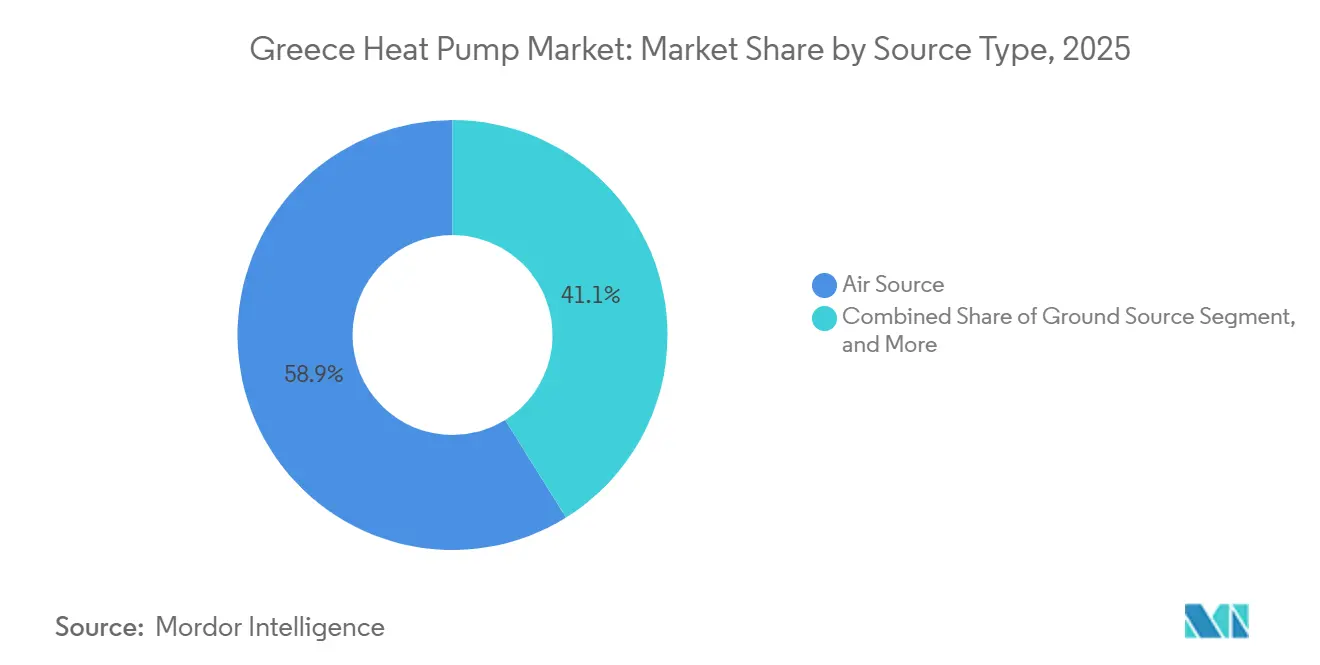

- By source type, air source systems led with 58.86% of Greece Heat Pump market share in 2025. Hybrid configurations pairing heat pumps with solar thermal or gas boilers are projected to register the fastest growth at a 6.03% CAGR through 2031.

- By technology, air-to-water technology held 48.01% share of the Greece Heat Pump market size in 2025. Ground-to-water systems are forecast to expand at a 5.82% CAGR between 2026-2031.

- By capacity, units below 10 kW commanded 43.63% capacity share in 2025, while the 50-200 kW range is projected to advance at a 5.54% CAGR.

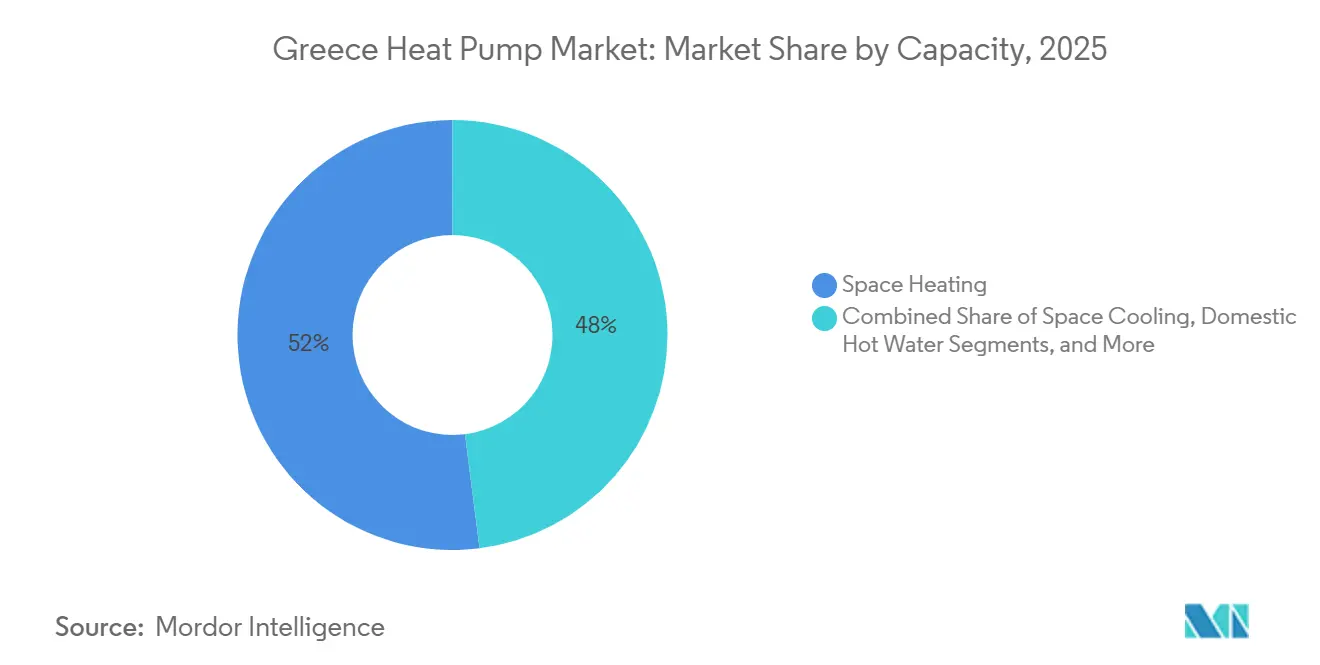

- By application, space heating dominated with 48.87% of the Greece heat pump market size in 2025, whereas industrial and process heating is set to advance at a 5.36% CAGR during the forecast window.

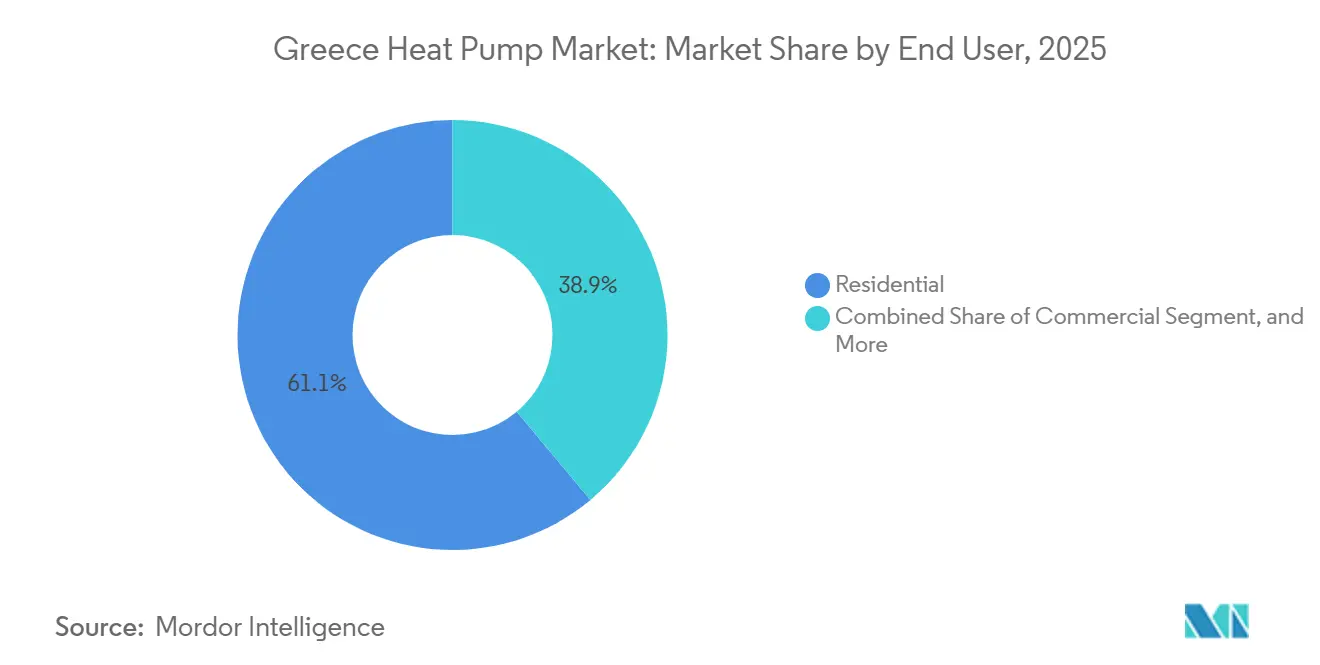

- By end user, residential end users represented 61.09% share of the Greece Heat Pump market in 2025, whereas commercial applications are poised to grow at a 5.24% CAGR to 2031.

- By installation, retrofit installations held 57.43% share of the Greece Heat Pump market size in 2025; new construction is expected to rise at a 5.49% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Greece Heat Pump Market Trends and Insights

Drivers Impact Analysi*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive Government Incentives Under "Exoikonomo" Scheme | +1.2% | National, higher uptake in Attica, Thessaloniki, rural low-income areas | Medium term (2-4 years) |

| EU Fit-for-55 Decarbonization Targets | +0.9% | Nationwide alignment with EU mandates | Long term (≥4 years) |

| Impending Ban on New Oil-Fired Boilers in Greek Islands by 2027 | +0.8% | Cyclades, Dodecanese, Ionian, North Aegean, Sporades | Short term (≤2 years) |

| Rapid Decline in Residential Electricity Tariffs Via Net-Metering | +0.7% | Regions with high rooftop PV (Crete, Attica, Peloponnese) | Short term (≤2 years) |

| Bundled PV-Heat-Pump Offers by Grid Operators | +0.5% | National, led by Public Power Corporation | Medium term (2-4 years) |

| Tourism Sector Demand for Low-Carbon HVAC in Hotels | +0.4% | Crete, Rhodes, Mykonos, Santorini, Corfu, Skiathos | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supportive Government Incentives Under "Exoikonomo" Scheme

The expanded EUR 1.6 billion (USD 1.81 billion) Exoikonomo program reimburses up to 85% of project costs for energy-poor households, removing upfront barriers to deep retrofits. A parallel replacement scheme covers 50-60% of typical change-outs, broadening access for middle-income families. Together, the two tracks underpin the target of 856,600 residential installations by 2030, equal to roughly 56,000 units per year.[1]Hellenic Republic Ministry of Environment and Energy, “National Energy and Climate Plan 2021-2030,” energy.ec.europa.eu The subsidy cadence ensures installers enjoy forward visibility, which encourages inventory planning and workforce expansion. Temporary adoption dips observed after the 2024 net-billing switch highlight the market’s sensitivity to perceived payback shifts, reinforcing the importance of stable policy frameworks.

EU Fit-for-55 Decarbonization Targets

Greece’s 2024 climate law hard-codes a 65% renewable share in total energy and 42.5% in heating and cooling by 2030. These milestones pull forward electrified heating adoption across homes, offices, and light industry.[2]European Commission Joint Research Centre, “National Climate Law Greece 2024,” climate.ec.europa.eu Parallel F-Gas revisions cap refrigerant GWP below 150 from 2027 for most small units, accelerating the rollout of R290 and R454C platforms from Daikin, Panasonic, and Viessmann. Early-mover brands gain pricing power, while installers face retraining costs to handle flammable A3 refrigerants. Access to EU Innovation and Cohesion Funds further derisks large-scale district and industrial projects.

Impending Ban on New Oil-Fired Boilers in Greek Islands by 2027

The oil-boiler prohibition on non-interconnected islands creates an unavoidable replacement cycle. Hoteliers and homeowners pivot to air-source and hybrid ground-source systems that cope with salt-laden air and high humidity. Although grid congestion limits simultaneous electrification, phased rollouts paired with on-site batteries and demand-response controls unlock steady volume growth. Manufacturers able to certify corrosion-resistant outdoor units hold a competitive edge in these coastal micro-markets.

Rapid Decline in Residential Electricity Tariffs Via Net-Metering

Greece’s move from net-metering to self-consumption has shortened heat-pump paybacks in PV-rich households. Daytime operation powered by rooftop arrays trims winter bills, especially where oil or LPG prices remain elevated. Battery coupling lifts renewable coverage above 50%, but higher evening tariffs still steer some customers toward hybrid gas backup. Overall, the tariff reform nudges households to size systems for maximum self-use rather than export, favoring variable-speed compressors and smart-cloud controls.[3]European Commission, “Greece’s Recovery and Resilience Plan,” commission.europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified Installers With F-Gas License | -0.6% | Nationwide, acute in islands and rural zones | Short term (≤2 years) |

| Island-Grid Congestion Caps Extra Electric Load | -0.5% | Cyclades, Dodecanese, Ionian, North Aegean, Sporades | Medium term (2-4 years) |

| Limited Adoption in Multifamily Blocks Due to Shared Metering | -0.4% | Athens, Thessaloniki, Patras, Heraklion | Long term (≥4 years) |

| High Seasonal Performance Factor Fluctuation in Humid Coastal Areas | -0.3% | Ionian coast and Aegean islands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Installers with F-Gas License

Only 10,600 licensed technicians serve the entire country, far below the volume needed to hit 2030 NECP targets. Training capacity is improving through manufacturer academies, yet travel time and wage premiums inflate project budgets in remote regions. The upcoming switch to R290 heightens safety requirements, extending course length and cost. Firms that build in-house crews and apprenticeship pipelines gain an execution advantage and can command premium service contracts.

Island-Grid Congestion Caps Extra Electric Load

Autonomous island grids curtailed 1,327 GWh of renewables in H1 2025, underscoring limited headroom for new electric heating loads. While the 1,000 MW Crete link eases pressure on Greece’s largest island, smaller archipelagos still face transformer and line bottlenecks. Hybrid systems with demand-response logic and behind-the-meter batteries partially solve the issue, but full resolution hinges on multi-year distribution upgrades and additional interconnections.[4]Independent Power Transmission Operator Greece, “Crete Interconnection Completion Report,” admie.gr

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Configurations Gain Traction Amid Electrification Push

Air-source units, holding 58.86% Greece Heat Pump market share in 2025, remain the default choice thanks to modest installation costs and mild winters. Water-source and ground-source alternatives thrive in geothermal pockets and premium projects, offering higher SCOP and quieter operation. Hybrid pairings that link air-source compressors with solar thermal collectors or legacy boilers are projected to grow at a 6.03% CAGR, reflecting customer desire for resiliency against tariff spikes and peak winter demand. Installers report that bundled hybrid proposals can trim annual energy outlays by 60-70% against oil heating, offsetting higher initial spend. The segment also benefits from households prioritizing self-consumption over export under net-billing rules.

A rising pool of hotel refurbishments and public-sector retrofits further institutionalizes hybrid designs. ANDRIANOS, for example, packages Viessmann or Carrier heat pumps with solar thermal arrays sourced from local collectors, achieving deep cuts in operating expenditure for island resorts. Conversely, falling PV module prices and expanding battery subsidies challenge hybrid solar-thermal economics, requiring integrators to emphasize reliability, silent operation, and hot-water comfort to justify adoption.

By Technology: Ground-to-Water Systems Emerge in Geothermal Hotspots

Air-to-water platforms represented 48.01% of Greece Heat Pump market size in 2025, valued for seamless tie-in with existing radiator circuits and domestic hot-water tanks. Air-to-air splits dominate small apartments, yet lack hot-water capability, limiting share growth. Ground-to-water systems, forecast to advance at 5.82% CAGR, win projects in Crete and Northern Greece where soil temperatures stay stable and drilling is feasible. Closed-loop boreholes deliver up to 50% operating-cost savings over comparable air-source setups, a selling point for cultural centers and university campuses seeking predictable budgets.

Technology evolution centers on natural refrigerants. Panasonic’s Aquarea L and Daikin’s Altherma 4 H employ R290 to meet 2027 GWP caps while maintaining 75 °C water supply, opening retrofit opportunities in high-temperature radiator homes. Installer training remains the gating factor, yet hydraulic-only indoor units reduce refrigerant handling, shortening learning curves. Viessmann’s modular indoor cabinets, launched in April 2025, integrate PV, battery, and cloud monitoring in factory-preplugged kits, appealing to premium builders chasing near-zero-energy codes.

By Capacity: Mid-Range Units Drive Commercial Sector Uptake

Systems below 10 kW equaled 43.63% Greece Heat Pump market share in 2025, mirroring fragmented single-family housing. The 10-50 kW cohort services multifamily blocks and small retail, offering installers volume potential once governance hurdles ease. Robust tourism pipelines spur 50-200 kW unit demand, projected at a 5.54% CAGR through 2031, as hotels retrofit central plants to meet ESG benchmarks. The 3,304 kW cooling and 4,164 kW heating installation at Benitses Beach Corfu showcases large-scale air-source feasibility in seaside climates.

Above 200 kW machines remain niche but strategic, feeding district loops and industrial processes. BDR Thermea’s stake in G.I. Holding underscores rising interest in high-capacity ammonia and R1234ze units that reach 90 °C-plus outlet temperatures for pasteurization, papermaking, and textile dyeing. Commercial installers position such projects as proof points that electrified heat can tackle medium-temperature tasks once thought gas-exclusive.

By Application: Industrial Process Heating Gains Momentum

Space heating accounted for 48.87% of 2025 demand, yet cooling co-benefits often tip payback equations in southern prefectures. Domestic hot water remains integral to air-to-water adoption, with solar-assisted storage tanks slashing immersion-heater runtime. Industrial process heating, projected to climb at 5.36% CAGR, garners attention as ammonia and high-temperature propane units spread.

ThermoDraft’s steel-mill pilots and the Nigrita geothermal-spirulina facility hint at broad potential across agri-food and light chemicals once CAPEX hurdles fall. Swimming pool conditioning, greenhouse climate control, and data-center waste-heat recovery represent emerging micro-segments. Their combined footprint is small today, yet each demonstrates the versatility of variable-speed compressor technology and the value of integrated heat-reclaim circuits in cutting overall site energy intensity.

By End User: Commercial Sector Accelerates Amid Tourism Investments

Residential buyers commanded 61.09% of 2025 shipments driven by Exoikonomo grants and PV bundling. The Greece Heat Pump industry’s commercial slice, however, is on a faster trajectory, aided by hotel chains seeking carbon-neutral branding and lower utility overheads. Metaxa Hospitality Group’s 2024 roll-out across four resorts illustrates repeatable volume potential when a corporate owner retrofits multiple properties.

Office parks, supermarkets, and public buildings follow, incentivized by Energy Performance of Buildings Directive minimum standards and the optics of climate leadership. Industrial end users progress cautiously given integration complexity, yet 90 °C outlet prototypes open new doors. Process engineers increasingly run comparative lifetime cost models that favor electrified steam generation when paired with low-tariff nighttime electricity or recovered low-grade waste heat.

By Installation: New Construction Gains Share Amid Code Tightening

Retrofits still made up 57.43% of Greece Heat Pump market size in 2025 as oil boiler change-outs dominate subsidy-eligible volumes. High-temperature R290 units such as Panasonic’s Aquarea L ease radiator compatibility, shrinking civil works and downtime. From 2026 onward, new-build penetration rises, fueled by the January 2025 oil-boiler permit ban and developer preference for compact all-in-one HVAC packs that accelerate energy-class certification

Projects like Kalamata Mediterranean Suites show that combining heat pumps, PV, and airtight envelopes can reach net-zero metrics without exotic materials. Builders also value hydraulic-only indoor modules for faster handover and reduced F-Gas paperwork. Distributors such as Schiessl Hellas, now stocking KAISAI monoblocks, court contractors with pre-filled brine loops and plug-and-play controllers that shorten commissioning cycles.

Geography Analysis

Attica, home to Athens, is the largest regional buyer thanks to high population density and installer availability, yet apartment-block governance slows collective system retrofits. Thessaloniki and Central Macedonia see stronger heating-degree days, so equipment is sized larger, improving return on investment despite slightly higher CAPEX. Peloponnese combines tourism resorts and scattered villages, making hybrid heat-pump plus solar-thermal kits attractive where roof space is ample and electricity grids are thin.

Crete’s 1,000 MW mainland interconnection completed in May 2025 cut curtailment, enabling air-source adoption alongside its long-established ground-source niche. Smaller Cycladic and Dodecanese islands still grapple with diesel-backed autonomous grids, so installers favor battery-coupled or dual-fuel designs to avoid overloading feeders. Oil-boiler bans there create a captive replacement pool once grid upgrades phase in.

Tourism hotspots such as Rhodes, Mykonos, Santorini, and Corfu accelerate commercial uptake as hotels race for green certifications. Humid coastal belts from the Ionian Sea to the northern Aegean challenge air-source defrost cycles, steering premium buyers towards ground-source or water-source alternatives. Mountainous Epirus and Western Macedonia face installer scarcity yet boast higher annual heating loads, so targeted Exoikonomo tiers channel subsidies to low-income rural households.

Competitive Landscape

Global manufacturers, including Daikin, Panasonic, Viessmann, Carrier, Mitsubishi Electric, and Ariston, control brand mindshare, while local specialists such as ANDRIANOS, MALTEZOS, Airtechnic, Inventor AG, Whelve Energy, and ThermoDraft supply project design and after-sales depth. Utility partnerships emerge as a high-leverage channel: Daikin and Public Power Corporation’s myEnergy HeatPump scheme bundles EUR 500 (USD 570) coupons with simplified financing, pulling smaller installers into pre-qualified networks.

Low-GWP readiness is the second contest. Panasonic’s EUR 320 million (USD 362 million) Czech expansion and Daikin’s R290 launch cadence position both firms for GWP 150 compliance. Viessmann’s modular indoor cabinets integrate PV and batteries, turning the heat pump into an energy hub rather than a stand-alone appliance.

Workforce bottlenecks foster vertical integration. ANDRIANOS trains in-house crews to guarantee capacity, capturing install margins and long-term maintenance revenue. Distributors such as Schiessl Hellas add KAISAI lines to hedge against brand-specific supply chain risk, while Airtechnic’s domestic factory scales complementary fan-coil and AHU output for turnkey bids. Process-heating innovators ThermoDraft and GEA court industrial clients with ammonia systems above 1 MW, carving a niche that global residential brands seldom touch.

Greece Heat Pump Industry Leaders

Daikin Industries Ltd.

Carrier Corporation

Viessmann Climate Solutions SE

Trane Technologies Plc

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ANDRIANOS and BLAUBERG showcased high-efficiency ventilation and heat-pump integrations at Climatherm Energy 2026 in Athens, highlighting multi-brand project delivery.

- January 2026: Schiessl Hellas began distributing KAISAI commercial split and monoblock heat pumps nationwide, targeting residential and light-commercial installers.

- November 2025: Ariston reported Q3 2025 revenues of EUR 668 million (USD 755 million) with 4.2% organic growth, crediting a rebound in heat-pump sales for its third straight quarterly EBIT-margin expansion.

- August 2025: Panasonic committed EUR 320 million (USD 362 million) to boost Czech heat-pump output to 1.4 million units annually by 2030, focused on R290-ready lines serving Southern Europe.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Greek heat pump market as all revenue earned inside Greece from selling, installing, and commissioning electrically driven air-source, water-source, and ground-source heat pumps that provide space heating, space cooling, or domestic hot water to homes, businesses, industry, and public buildings.

Scope exclusion: chillers used solely for industrial process cooling and VRF air-conditioning systems are not counted.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

We spoke with installers, distributors, ESCO executives, and policy officers across Athens, Thessaloniki, Crete, and selected islands. Their insights on subsidy pass-through, average selling prices, and installer capacity let us refine penetration and retrofit shares before finalizing the model.

Desk Research

We anchored the baseline with Eurostat energy balances, Hellenic Statistical Authority building permits, EHPA sales barometers, the European Commission Joint Research Centre's 2024 country fiche, and Bank of Greece macro data. Trade flows from Eurostat ComExt showed import values, while Questel patent analytics signaled technology diffusion. Company filings, public tenders, and Greek business press helped us sense-check selling prices and channel margins. Mordor analysts also dipped into D&B Hoovers and Dow Jones Factiva to benchmark vendor revenues. These examples illustrate our desk work; many additional references were reviewed for cross-validation.

Market-Sizing & Forecasting

Our team starts with dwelling stock, service-sector floor area, and new-build completions, multiplies each cohort by modeled heat-pump penetration and average selling price, then cross-checks totals with importer revenue samples. Key inputs include the electricity-to-gas price ratio, Exoikonomo grant uptake, heating degree days, renewable targets, and certified installer headcount. Multivariate regression blended with scenario analysis projects values to 2030, while supplier roll-ups fill data gaps.

Data Validation & Update Cycle

Outputs face anomaly checks against EHPA unit totals and IndexBox import values, followed by dual analyst review and manager sign-off. We refresh the model every twelve months and issue interim tweaks when subsidy budgets, energy prices, or code changes shift the market.

Why Mordor's Greece Heat Pump Baseline Earns Confidence

Published estimates often differ because firms pick different product scopes, pricing bases, and refresh cadences.

We include air-to-air units and use installer-level prices, whereas some peers rely only on customs values or unit counts, leading to lower or fragmentary figures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 122 million (2025) | Mordor Intelligence | - |

| USD 53 million (2024) | Regional Consultancy A | Excludes air-to-air units; customs prices only |

| 18 000 units (2024) | Industry Association B | Volume figure, no value or forecast |

| 40 000 units (2022) | Research Institution C | Single-year snapshot; cooling capability omitted |

Sources for external figures are IndexBox, EHPA, and the European Commission JRC. These contrasts show how Mordor Intelligence's disciplined variable selection, annual refresh, and transparent inputs give decision-makers a balanced baseline they can trust.

Key Questions Answered in the Report

What is the Greece Heat Pump market size in 2026 and how large is it expected to be by 2031?

The market is estimated at USD 128.59 million in 2026 and is projected to reach USD 164.62 million by 2031.

What CAGR is the Greece Heat Pump market projected to record between 2026-2031?

The market is forecast to grow at 5.06% annually during the 2026-2031 period.

Which source type currently dominates sales in Greece?

Air-source systems led with 58.86% market share in 2025, favored for their lower upfront cost and climate suitability.

How do government subsidies lower ownership costs for households?

Exoikonomo covers up to 85% of eligible retrofit expenses, while a separate replacement grant reimburses 50-60% of standard change-outs, sharply reducing payback times.

Why is installer availability considered a bottleneck?

Greece has just 10,600 certified F-Gas technicians, which is insufficient to meet rising installation demand, especially with new R290 safety training requirements.

What opportunities exist for heat pumps in the tourism sector?

Hotel refurbishments and new resorts are installing 50-200 kW systems to meet sustainability certifications and cut energy bills, pushing commercial CAGR to 5.24% through 2031.

Page last updated on: