Vietnam Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

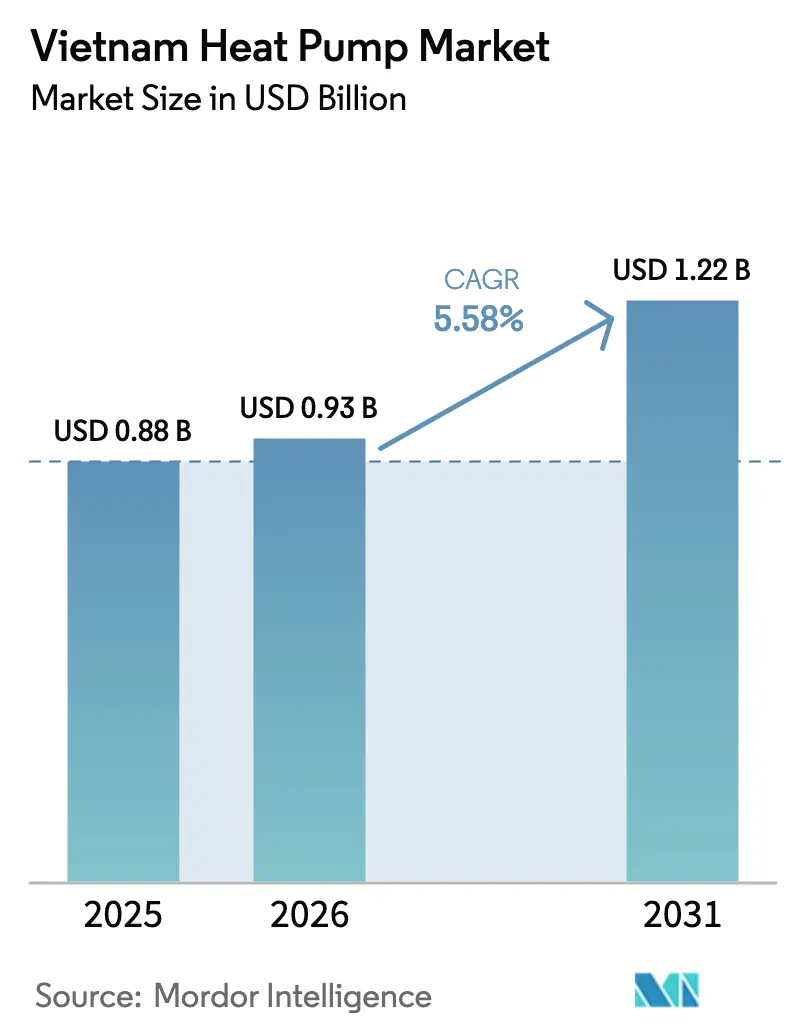

| Base Year Market Size (2025) | USD 0.88 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.22 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Heat Pump Market Analysis by Mordor Intelligence

The Vietnam heat pump market size was valued at USD 0.88 billion in 2025 and estimated to grow from USD 0.93 billion in 2026 to reach USD 1.22 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031). Rising policy support for low-carbon cooling, rapid urban high-rise construction, and concessional green financing are lifting demand, even as upfront cost sensitivities and technician shortages restrain faster adoption. Air-source configurations dominate because of Vietnam’s warm climate and simpler installation, yet hybrid and ground-source systems are gaining traction in industrial retrofits, aquaculture, and data-center waste-heat recovery projects. The impending 2029 refrigerant ban is set to trigger a sizable compliance-driven replacement cycle, while the two-part electricity tariff rolling out in 2026 encourages load-shifting strategies that favor high-efficiency heat pumps over resistance heating. Against this backdrop, residential buyers remain the largest customer group, but industrial users are emerging as the fastest-growing segment as they prepare for Vietnam’s mandatory carbon market.

Key Report Takeaways

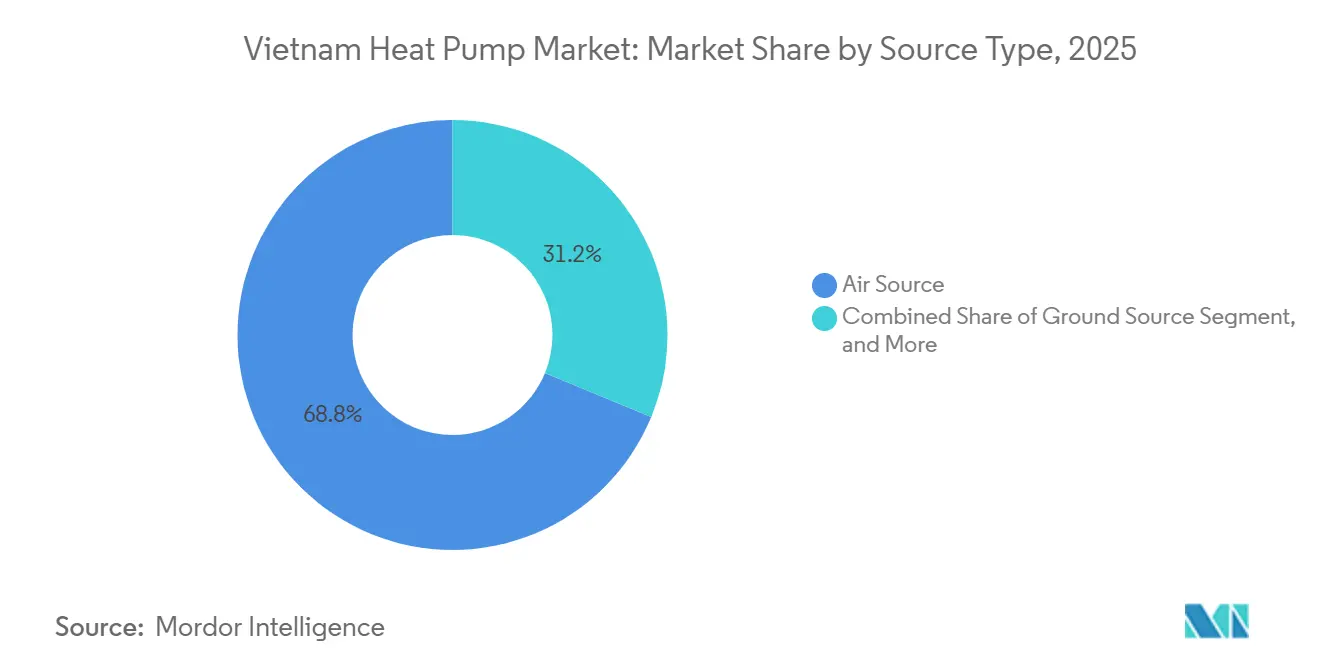

- By type, air-source systems led with 68.78% of the Vietnam heat pump market share in 2025, while hybrid units are projected to expand at a 7.13% CAGR through 2031.

- By technology, air-to-water solutions accounted for 60.31% of the Vietnam heat pump market size in 2025; ground-to-water options are advancing at a 6.47% CAGR to 2031.

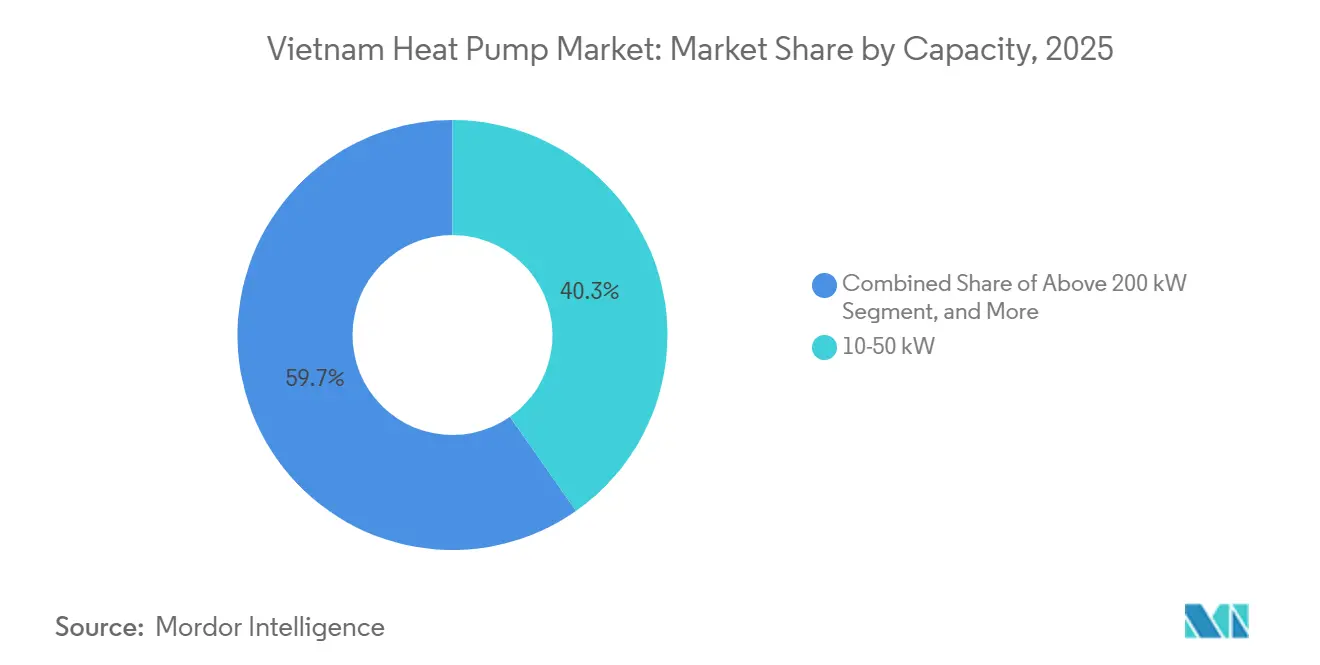

- By capacity, 10-50 kW models captured 40.26% of 2025 demand, whereas systems above 200 kW are forecast to grow at a 6.02% CAGR.

- By application, space cooling held a 44.12% share in 2025; industrial and process heating is poised for a 5.83% CAGR through 2031.

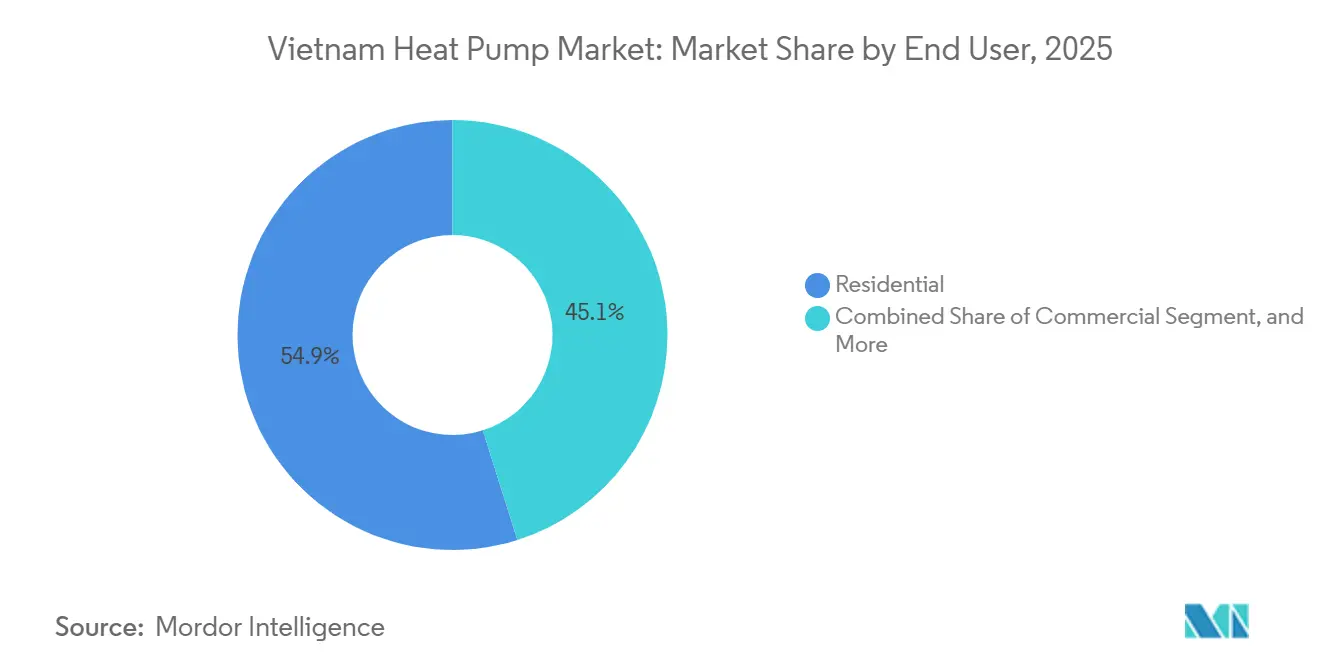

- By end user, the residential segment dominated with 54.89% of the Vietnam heat pump market share in 2025, yet industrial buyers are on track for a 5.71% CAGR.

- By installation, new projects represented 60.37% of 2025 activity, while retrofit deployments are set to rise at a 5.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Roll-Out of Government Subsidies and Zero-Interest Green Loans | +1.2% | National (early gains in Hanoi, Ho Chi Minh City, Da Nang) | Short term (≤ 2 years) |

| Mandatory Phase-Out of Inefficient Electric Water Heaters in Urban Areas | +0.9% | Tier-1 and tier-2 cities | Medium term (2-4 years) |

| Rapid Residential High-Rise Construction Boom in Tier-1 Cities | +0.8% | Hanoi, Ho Chi Minh City, Da Nang | Short term (≤ 2 years) |

| Rising Demand for Low-Carbon Aquaculture Heating Systems | +0.5% | Mekong Delta provinces | Medium term (2-4 years) |

| Heat-Pump Integration in Hyperscale Data-Center Waste-Heat Recovery | +0.7% | Ho Chi Minh City, Hanoi, Binh Duong, Dong Nai | Medium term (2-4 years) |

| Impending Ban on R22 Refrigerant Driving Retrofit Demand | +0.6% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Roll-out of Government Subsidies and Zero-Interest Green Loans

Cheaper capital is beginning to reshape buying behavior, especially among small hotel chains and condominium associations that historically delayed high-efficiency upgrades. As commercial lenders embed the 2% interest subsidy in their green-loan products, monthly installments for a mid-rise hot-water plant fall below the cash savings from lower electricity use, creating immediate positive cash flow for borrowers.[1]Thuy Dung, “Green and ESG projects to enjoy 2% loan support,” Vietnam Government News, bao chinhphu.vn Installation contractors report that order backlogs for R32 air-to-water units in Ho Chi Minh City doubled between January and March 2026, a shift they attribute to buyers racing to lock in concessional terms before any quota caps are reached. Manufacturers are responding by offering “loan-ready” packages that bundle equipment, monitoring software, and pre-filled application documents, reducing transaction friction for end users who lack experience with green-finance paperwork. Over the next two years, this policy-driven liquidity is expected to narrow the payback gap between heat pumps and gas heaters to less than three years for many commercial sites, firmly anchoring demand in the short term.

Mandatory Phase-Out of Inefficient Electric Water Heaters in Urban Areas

Compliance deadlines embedded in QCVN 25:2025 are forcing property managers to audit appliance fleets and draft multi-year replacement schedules. Because municipal inspectors now review energy-certificate logs during routine safety checks, owners of older resistance heaters are exposed to fines as well as higher electricity bills, accelerating their decision to switch technologies.[2]LuatVietnam, “Roadmap to restrict the production and import of equipment containing controlled substances,” luatvietnam.net Retail chains in Hanoi have already removed low-efficiency storage heaters from shelves, replacing them with inverter-driven heat-pump models that meet the 2025 minimum-performance threshold. Insurance firms are also signaling that non-compliant equipment could void fire-risk coverage, adding a financial stick to the regulatory carrot. As enforcement radiates from tier-1 to tier-2 cities, a rolling wave of demand is expected to cascade through the distribution channel, sustaining double-digit shipment growth through 2029.

Rapid Residential High-Rise Construction Boom in Tier-1 Cities

Developers chasing premium unit pricing now advertise heat-pump hot-water systems alongside rooftop gardens and smart-home controls, using lower utility costs as a selling point to young professional buyers. The tiered tariff introduced in 2025 has made these claims credible, because households in the top two consumption brackets pay nearly twice the average retail rate during summer peaks. Construction lenders increasingly require energy-performance models as part of loan covenants, and projects that miss green benchmarks face higher interest spreads, nudging builders toward heat-pump specifications. Equipment vendors are therefore partnering with general contractors to lock in design-phase commitments, rather than relying on post-tender retrofits that are harder to secure. With more than 200 new towers slated for groundbreaking across Hanoi and Ho Chi Minh City through 2028, this pull-through mechanism supports a stable multi-year revenue pipeline.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Installation complexity and high upfront cost | -1.2% | National, strongest in rural zones | Short term (≤ 2 years) |

| Limited public awareness | -0.9% | Rural and small-city areas | Medium term (2–4 years) |

| Technician shortage and slow training throughput | -0.7% | High-growth urban centers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Low-Carbon Aquaculture Heating Systems

Export-oriented shrimp and pangasius farms are under pressure to document Scope 1 reductions to retain buyer contracts in Europe and North America, where carbon-adjustment fees loom. Early pilots show that water-source heat pumps can lift larval survival rates by 6-8 percentage points while trimming diesel usage, an operational win that resonates with farm managers.[3]United Nations Environment Programme, “Life Cycle Refrigerant Management,” ozone.unep.org Climate-linked insurance policies now offer premium discounts for electrified hatcheries, further sweetening the value proposition. Provincial authorities, keen to safeguard a USD 10 billion seafood export sector, are co-financing demonstration plants to showcase cost savings to smaller operators. As carbon-credit spot prices rise ahead of the 2028 market launch, farms that bank verified reductions via heat-pump projects will gain a tradable revenue stream that enhances project economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Equipment and Installation Cost | -0.8% | National, acute in rural and tier-2/tier-3 cities | Short term (≤ 2 years) |

| Shortage of Certified Heat-Pump Technicians | -0.6% | Provinces outside Hanoi, Ho Chi Minh City, Da Nang | Medium term (2-4 years) |

| Limited Available Land for Ground-Source Loop Fields | -0.3% | Urban cores of Hanoi, Ho Chi Minh City, Da Nang | Long term (≥ 4 years) |

| Industrial Natural-Gas Tariff Advantage over Electricity Prices | -0.5% | Binh Duong, Dong Nai, Ba Ria-Vung Tau | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Equipment and Installation Cost

Despite policy support, the cash price of a 200-liter residential heat-pump water heater still exceeds the annual income of many rural households, muting diffusion outside major urban centers. Import duties on compressors and electronic expansion valves add 7-10% to invoice values, and logistics surcharges pushed up freight costs by 12% year-on-year in early 2026. Dealers therefore focus promotional budgets on upper-middle-income districts where credit-card penetration and mortgage refinancing options can offset sticker shock. Without a broader consumer-subsidy scheme or a mass-leasing model, market penetration in tier-3 cities is likely to remain below 5% through 2027. Consequently, manufacturers face a delicate balance between volume aspirations and the need to preserve margins amid persistent price sensitivity.

Shortage of Certified Heat-Pump Technicians

Only 2,100 technicians had attained the new refrigerant-handling certificate by March 2026, far short of the 8,000-person target for 2034. This talent gap inflates labor quotes, especially for ground-source projects that require specialized drilling oversight and complex commissioning protocols.[4]Department of Climate Change, “National Cooling Action Plan: Policy Brief,” energytransitionpartnership.org Several large hotel chains have postponed retrofit programs because bid prices climbed 15-20% after contractors factored in travel and per-diem costs for certified crews. Vocational colleges outside Hanoi and Ho Chi Minh City struggle to attract instructors, as private sector pay scales lure experienced trainers back into the field. Until technician density improves, installation lead times in secondary provinces will stay at six to eight weeks, elongating project cycles and dampening adoption momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air-Source Dominance Sustained While Hybrid Units Gain Ground

Air-source systems accounted for 68.78% of the Vietnam heat pump market share in 2025, underpinned by favorable ambient temperatures, widespread dealer networks, and lower installation complexity. Hybrid designs pairing heat pumps with gas or biomass boilers are set for a 7.13% CAGR as commercial and industrial users hedge against peak-hour electricity prices and grid instability. The Vietnam heat pump market size for water-source solutions remains modest, yet pilots in coastal resorts and aquaculture hint at long-term niche expansion. Ground-source uptake is inhibited by urban land scarcity and drilling costs, restricting deployments to data-center campuses and greenfield industrial parks where vertical boreholes can be planned from the outset.

Developers in Hanoi and Ho Chi Minh City increasingly pre-install R32-charged air-source units that meet 2029 refrigerant rules, cutting retrofit headaches for residents. Meanwhile, manufacturers fine-tune outdoor coils and inverter drives for humid, 35-40 °C summer conditions, sustaining seasonal performance factors above 4.5 even at partial load. These advances reinforce air-source hegemony, yet rising industrial electrification and refrigerant phase-outs are opening beachheads for ground- and water-source configurations in specialized applications.

By Technology: Air-to-Water Retains Leadership, Ground-to-Water Accelerates

Air-to-water equipment captured 60.31% of the Vietnam heat pump market size in 2025 as hotels, hospitals, and condominiums prioritized domestic hot water and radiant floor loops. The Vietnam heat pump market share for ground-to-water units will rise as data centers pursue waste-heat recovery and Mekong Delta hatcheries deploy geothermal loops to stabilize water temperatures during extreme weather events. Air-to-air split units dominate southern provinces for cooling but seldom run in heating mode, curbing their incremental contribution. Water-to-water machines serve district cooling schemes in urban redevelopment zones, where central chilled-water plants integrate heat-recovery chillers to deliver process or sanitary hot water without extra electrical input.

Developers of data-center campuses in Binh Duong are piloting dual-temperature hydronic loops that let ground-to-water heat pumps scavenge 30 °C server exhaust and elevate it to 60 °C process water without auxiliary boosters. Aquaculture operators, meanwhile, favor sealed-loop pond coils linked to modular water-to-water units, citing corrosion resistance and stable COPs during monsoon season. Equipment makers are responding with factory-prefabricated skid modules that compress design timelines from months to weeks, an advantage for fast-track projects racing to meet export certification audits. As monitoring platforms aggregate field data, financiers gain confidence in long-term performance, unlocking cheaper debt that narrows the cost differential with mainstream air-to-water systems.

By Capacity: Mid-Range Units Prevail, Large-Scale Systems Outpace Growth

Units rated 10-50 kW represented 40.26% of shipments in 2025 thanks to widespread use in light commercial spaces and multi-family towers. Larger-than-200 kW installations are projected to expand at 6.02% CAGR, driven by dyeing mills, food processors, and urban district cooling networks seeking to curtail fossil-fuel dependence. Below-10 kW models remain price-sensitive, with uptake tied to consumer awareness campaigns and promotions from electric utilities. Mid-size 50-200 kW modules serve hotels and clinics that value modular scalability and redundancy during maintenance cycles.

Textile dye houses in Dong Nai have begun clustering multiple 300 kW heat-pump modules around shared thermal-storage tanks, achieving redundancy and shaving capacity charges by up to 18%. Municipal redevelopment authorities in Ho Chi Minh City specify 1 MW central plants for district cooling rings that serve mixed-use blocks, signaling an appetite for even higher tonnage over the forecast window. Below-10 kW models could gain traction if appliance retailers secure vendor financing that lets homeowners amortize costs within utility bills, a pay-as-you-save concept now under pilot review. These dynamics suggest the sales mix will slowly tilt toward both extremes, compact residential units for individual dwellings and mega-scale arrays for industrial and civic infrastructure, while the 10-50 kW band maintains its stronghold in small businesses and high-rise cores.

By Application: Cooling Dominates Today, Industrial Heating Climbs Fast

Space cooling delivered 44.12% of revenue in 2025 as climate change lengthens peak-temperature periods and drives air-conditioning penetration. Industrial and process heating is forecast for a 5.83% CAGR as exporters prepare for carbon pricing and investors favor electrified production lines. Domestic hot water remains a staple in hospitality and healthcare, where heat-pump boilers deliver 2-3× higher coefficients of performance than electric heaters while cutting peak-demand charges under time-of-use tariffs. Space heating stays niche, concentrated in northern provinces experiencing winter lows below 15 °C.

Food processors experimenting with low-temperature blanching use cascade heat-pump lines that deliver 80 °C hot water alongside 5 °C chilled water, eliminating separate boiler and chiller assets. Hospitals in Hanoi are integrating air-to-water units with heat-recovery ventilators to pre-condition fresh air, cutting HVAC electrical loads by an estimated 22% in preliminary audits. In the agritech sector, greenhouse operators report that reversible systems curb humidity swings, reducing fungal outbreaks and pesticide use, an ancillary benefit included in ESG scorecards. These multi-service applications reinforce the shift from single-purpose cooling toward versatile heat-pump platforms that optimize thermal flows across diverse operating envelopes.

By End User: Residential Leads, Industrial Users Catch Up

Residential customers commanded 54.89% of 2025 volumes, benefitting from mortgage-backed green building certifications that reward developers for energy-efficient common-area systems. The industrial customer base is set for a 5.71% CAGR, propelled by two-part tariffs and the 2028 launch of Vietnam’s carbon market, which will monetize Scope 1 emissions reductions from process electrification. Commercial facilities, notably hotels and retail, sit between the two in size and growth, using bundled HVAC-controls retrofits to meet corporate ESG targets while leveraging concessional finance.

Industrial buyers are negotiating performance-based service contracts that guarantee uptime and energy savings, a prerequisite for board approvals now that carbon-compliance costs are becoming material. Residential adoption in tier-1 cities is further lifted by developers bundling heat-pump hot-water systems into homeowner association fees, smoothing repayment across 10-year building-maintenance cycles. In the commercial segment, international hotel chains embed digital twins to track real-time COPs and trigger predictive maintenance alerts, maximizing guest-comfort scores while meeting global sustainability pledges. This service-centric approach elevates post-sale value creation, shifting competitive focus from hardware margins to lifecycle performance differentiation.

By Installation: New Builds Dominate but Retrofit Wave Approaches

New projects delivered 60.37% of 2025 shipments as tower cranes filled Hanoi and Ho Chi Minh City skylines. Retrofitting, however, is forecast for a 5.66% CAGR because the 2029 ban on HFC-410A and HFC-407C renders thousands of legacy units non-compliant. Flexible loan terms from the Environment Protection Fund make retrofit economics more palatable, especially when combined with refrigerant-recovery credits under the evolving lifecycle-management regime. Manufacturers offering swap-out packages that wrap financing, certified installation, and old-gas destruction stand to capture an outsized share of this pipeline.

Facilities planning retrofit projects are increasingly opting for “plug-and-play” outdoor monobloc units that minimize downtime by avoiding refrigerant pipe runs through occupied spaces. Service firms sweeten proposals with refrigerant buy-back prices tied to verified destruction credits, offsetting part of the equipment outlay and satisfying corporate ESG disclosures. Building-automation retrofits often couple heat-pump swaps with smart meters and occupancy-based controls, achieving compound paybacks that clear internal hurdle rates within five years. Given the 2029 refrigerant cliff, forward-planning landlords are staging replacements floor by floor to spread capital draws, creating a predictable retrofit pipeline for suppliers through 2031.

Geography Analysis

Ho Chi Minh City remains the single largest pocket of demand, reflecting its economic heft, dense high-rise stock, and aggressive enforcement of energy-efficiency ordinances. Developers there integrate central heat pump plants in premium mixed-use complexes to lower tenant utility bills and secure green certifications linked to preferential property tax rates. Hanoi follows closely, buoyed by governmental facility upgrades and a burgeoning data-center cluster primed for waste-heat recovery installations. Da Nang, Vietnam’s leading coastal city, records double-digit growth by embedding air-to-water systems in new resorts that seek to slash utility costs while marketing sustainability credentials to international tourists.

The Mekong Delta shows rising potential as aquaculture firms retrofit water-source loops to curb diesel usage, aided by international financing tied to carbon-border compliance. Provinces such as Can Tho and Ben Tre partner with Japanese agencies to pilot ground-source loops that stabilize hatchery temperatures, thereby improving larval survival metrics. In industrial corridors like Binh Duong and Dong Nai, customers weigh heat pumps against competitively priced pipeline natural gas. Yet the two-part tariff’s capacity charge tilts the calculus in favor of electrified heating when paired with off-peak storage.

Northern provinces gain from grid reinforcement projects approved for 2026, which alleviate transmission bottlenecks and bolster voltage stability. Cooler winters there open small but growing windows for space-heating heat pump sales, and municipal procurement of efficient public-sector buildings sets demonstrative precedents that ripple into private construction contracts.

Competitive Landscape

Competition in the Vietnam heat pump market is fragmented, with Japanese, European, and Chinese players jostling for share. Daikin, Panasonic, and Mitsubishi Electric leverage Indonesian and Indian plants to control costs and shorten lead times, while Chinese vendors such as Midea, Gree, and PHNIX undercut pricing in entry-level tiers. Daikin’s December 2025 agreement to acquire Anh Nguyen widens its service moat by bundling HVAC hardware with building-automation competencies, a proposition appealing to factories and hotels confronting the two-part tariff regime.

Price competition intensified in 2025 as ASEAN channel inventories swelled, driving Daikin’s regional sales nine percent lower year-on-year. Brands responding with localized R290 product lines and extended warranties have partially defended margins. Retrofit-oriented portfolios that package refrigerant recovery, financing, and performance contracts are emerging differentiators ahead of the 2029 refrigerant ban.

High-capacity opportunities cluster around hyperscale data-center builds by Viettel, ST Telemedia, and CMC Telecom, where vendors able to design integrated waste-heat capture, hydronic distribution, and demand-response algorithms gain an advantage. Conversely, the Mekong Delta’s aquaculture niche remains underserved, offering room for specialists with corrosion-resistant heat exchangers and remote-monitoring suites adapted to coastal conditions.

Vietnam Heat Pump Industry Leaders

Stiebel Eltron GmbH & Co. KG

Viessmann Climate Solutions SE

Glen Dimplex Group

PHNIX Eco-Energy Solution Ltd.

Vaillant Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Vietnam Environment Protection Fund officially launched 10-year loans at 2.6% for energy-saving technologies, broadening access for small enterprises.

- December 2025: Daikin signed an agreement to acquire Anh Nguyen Trading Technical Service, aimed at expanding bundled HVAC and controls solutions, with closing expected in Q1 FY2026.

- November 2025: The Ministry of Industry and Trade approved the 2026 national power system operating plan, outlining consumption scenarios up to 368 billion kWh to secure grid reliability.

- October 2025: Vietnam Electricity began piloting a two-component tariff combining capacity and energy charges for large industrial consumers, paving the way for nationwide rollout in 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Vietnam heat pump market as every air, water, and ground-source unit shipped into or assembled within the country for space heating, space cooling, or domestic hot-water use across residential, commercial, industrial, and institutional sites.

Scope exclusion: window air-conditioners with reverse-cycle features and large process chillers are outside the count.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed installers, distributors, hotel facility heads, and policy officers; their insights on average selling prices, retrofit ratios, and incentive uptake let us validate and fine-tune secondary findings.

Desk Research

We extracted baseline volumes from customs code HS 8418/8419 filings, dwelling-stock figures from the General Statistics Office, and tariff tables published by the Ministry of Industry and Trade. Broader context came from IRENA heat-roadmap papers, ASEAN Center for Energy outlooks, and peer-reviewed degree-day analyses. Paid slices from D&B Hoovers and Dow Jones Factiva supplied revenue splits and contract news. Many other public sources were checked to confirm trends.

Market-Sizing & Forecasting

We build a top-down model that starts with dwelling and floor-area pools, applies technology-penetration curves, and multiplies by verified ASPs. Bottom-up supplier roll-ups and channel checks test the totals. Key inputs include new-build completions, power-tariff shifts, cooling degree-days, import shipment counts, and subsidy claim rates. Multivariate regression, supported by expert scenarios, drives the 2025-2030 outlook, and gaps in supplier data are filled with conservative ASEAN analogs.

Data Validation & Update Cycle

Outputs face variance checks against trade flows and historical adoption before two-level analyst review. Our team refreshes figures every twelve months, adds interim updates after major tariff or policy moves, and performs a final sweep before release.

Why Mordor's Vietnam Heat Pump Baseline Commands Trust

Published numbers vary because scopes, price assumptions, and refresh cadences differ. Mordor defines a clear product boundary, uses live customs data, and updates annually, whereas other studies often blend reverse-cycle AC sets or hold static ASPs.

The comparison shows that Mordor's disciplined scope selection, live variable tracking, and timely refresh deliver the most balanced and reproducible baseline for Vietnam's decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.90 B (2025) | Mordor Intelligence | - |

| USD 1.49 B (2024) | Global Consultancy A | Counts industrial chillers, fixed ASP |

| USD 0.26 B (2024) | Trade Journal B | Omits commercial retrofits, older tariff base |

The comparison shows that Mordor's disciplined scope selection, live variable tracking, and timely refresh deliver the most balanced and reproducible baseline for Vietnam's decision-makers.

Key Questions Answered in the Report

How big is the Vietnam heat pump market size expected to be by 2031?

It is forecast to reach USD 1.22 billion by 2031, advancing at a 5.58% CAGR from 2026.

Which heat pump configuration is most popular with Vietnamese residential builders?

Air-source, air-to-water units remain the first choice because they are easier to install and suit the countrys warm climate while complying with upcoming refrigerant rules.

Why are industrial companies in Vietnam considering large-capacity heat pumps?

Two-part electricity tariffs starting in 2026 and the 2028 carbon market launch make electrified, off-peak load-shifting solutions financially attractive compared with gas boilers.

What is driving retrofit demand ahead of 2029?

The Ministry of Natural Resources and Environment will ban imports of HFC-410A and HFC-407C units from January 2029, forcing owners of legacy systems to replace or upgrade them.

How do green-loan programs affect payback periods for heat pump projects?

Interest-rate subsidies of 2% and concessional loans at 2.6% cut financing costs, reducing typical residential and commercial payback times to roughly five to six years.

Where is ground-source technology seeing early adoption in Vietnam?

Hyperscale data centers near Ho Chi Minh City and shrimp hatcheries in the Mekong Delta are piloting geothermal loops to capture waste heat or stabilize water temperatures.

Page last updated on: