Tuberculosis Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

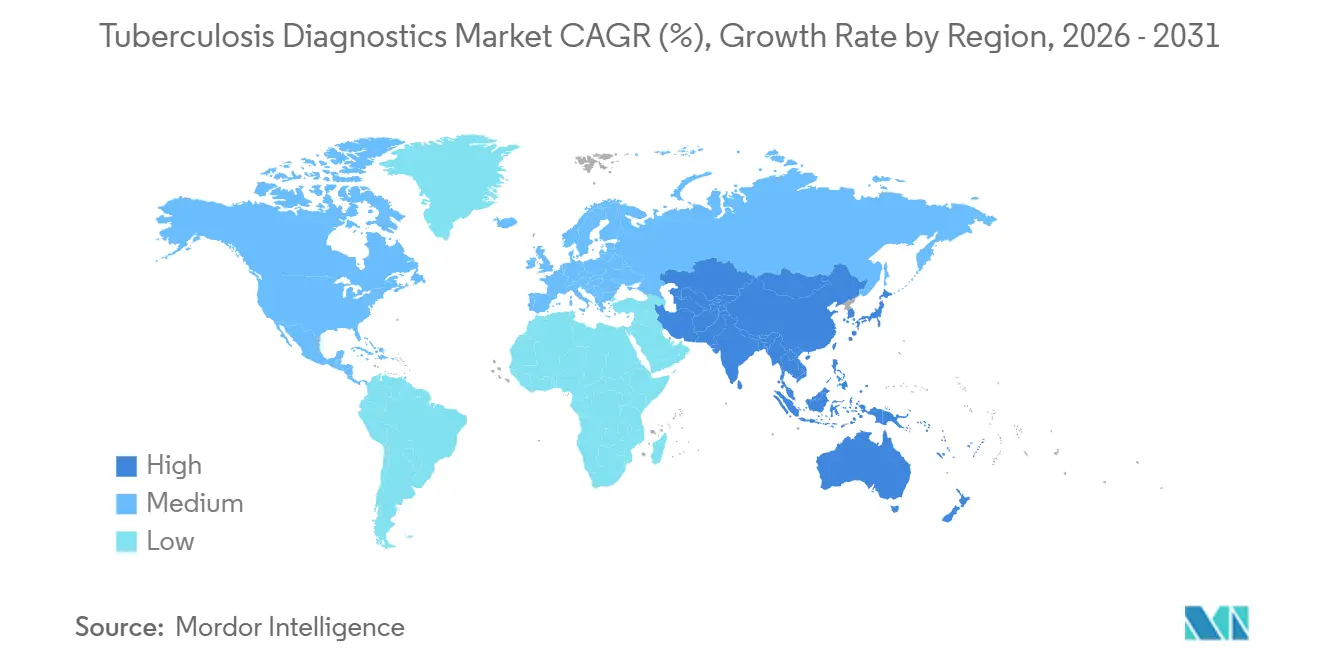

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tuberculosis Diagnostics Market Analysis by Mordor Intelligence

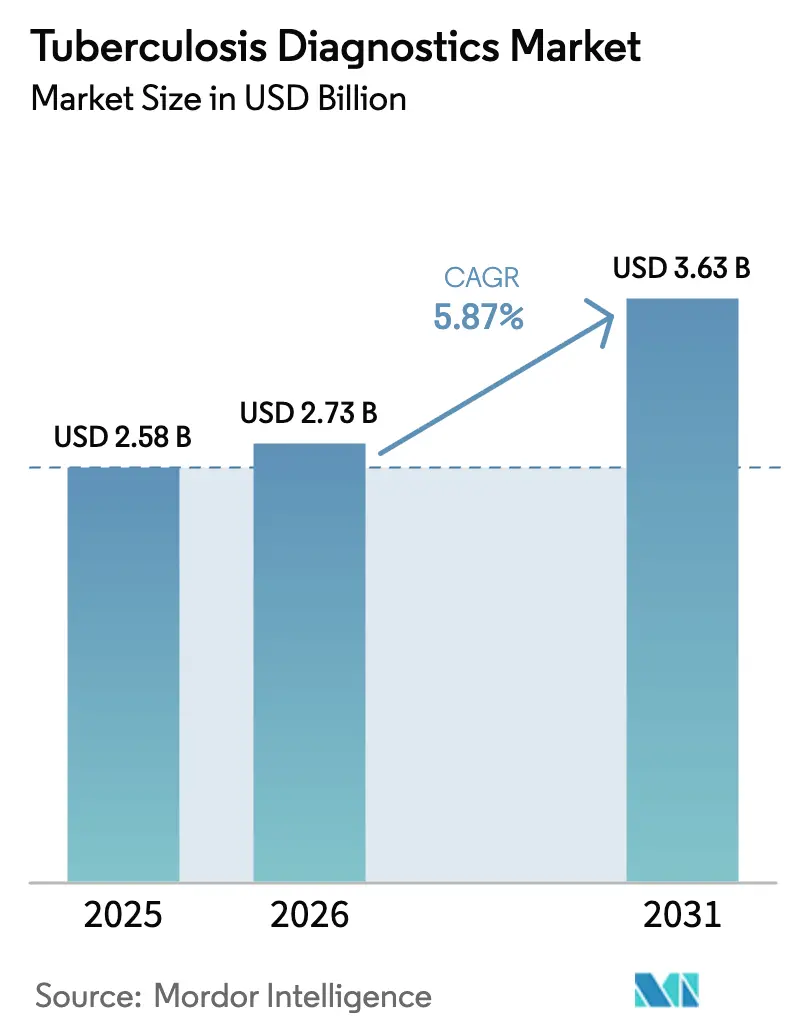

The Tuberculosis Diagnostics Market size is expected to increase from USD 2.58 billion in 2025 to USD 2.73 billion in 2026 and reach USD 3.63 billion by 2031, growing at a CAGR of 5.87% over 2026-2031.

Accelerated demand stems from the roughly 4 million tuberculosis cases that go undetected every year and from the December 2024 WHO approval of Xpert MTB/RIF Ultra. This rapid molecular test can confirm infection and drug resistance in a single visit.[1]Source: World Health Organization, “WHO announces first prequalification of a tuberculosis diagnostic test,” who.int Laboratories are abandoning weeks-long culture protocols in favor of nucleic-acid amplification platforms, which have become the centerpiece of most national testing algorithms.[2]Source: World Health Organization, “Consolidated guidelines on tuberculosis diagnosis,” who.int AI-guided digital microscopy and portable point-of-care assays, such as Tulane University’s lab-in-tube device that returns results in under an hour at a cost below USD 3, are widening access in community clinics and mobile units. Asia-Pacific is on track for the quickest expansion as high-burden countries shift from smear microscopy to molecular testing. At the same time, North America maintains the largest revenue base due to its entrenched laboratory infrastructure. Competitive intensity stays moderate: Cepheid alone has installed more than 20,000 GeneXpert systems in high-burden nations, yet cartridge supply constraints and a multibillion-dollar funding gap flagged by U.S. public-health agencies threaten to slow broader scale-up of Cepheid.

Key Report Takeaways

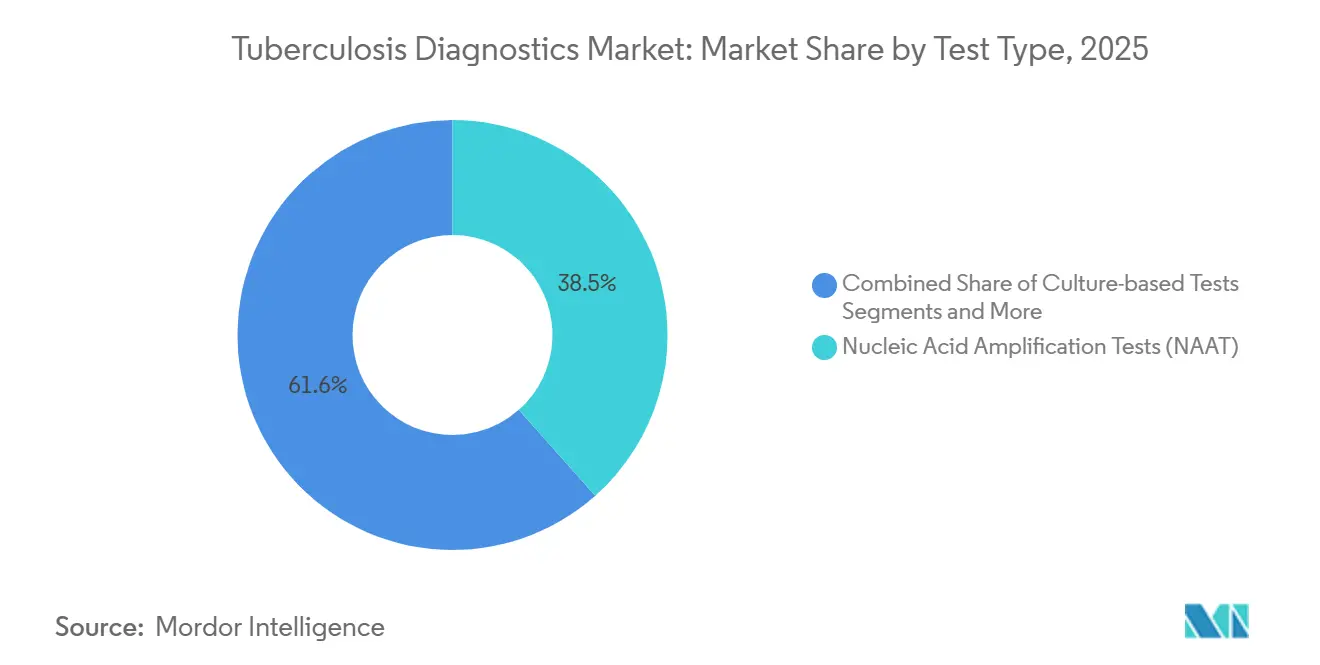

- By test type, nucleic acid amplification tests captured 38.45% of the tuberculosis diagnostics market share in 2025, while culture methods are predicted to lead growth at a 6.54% CAGR to 2031.

- By technology, molecular diagnostics commanded 45.23% share of the tuberculosis diagnostics market size in 2025, while AI-enhanced digital microscopy is projected to expand at a 7.15% CAGR through 2031.

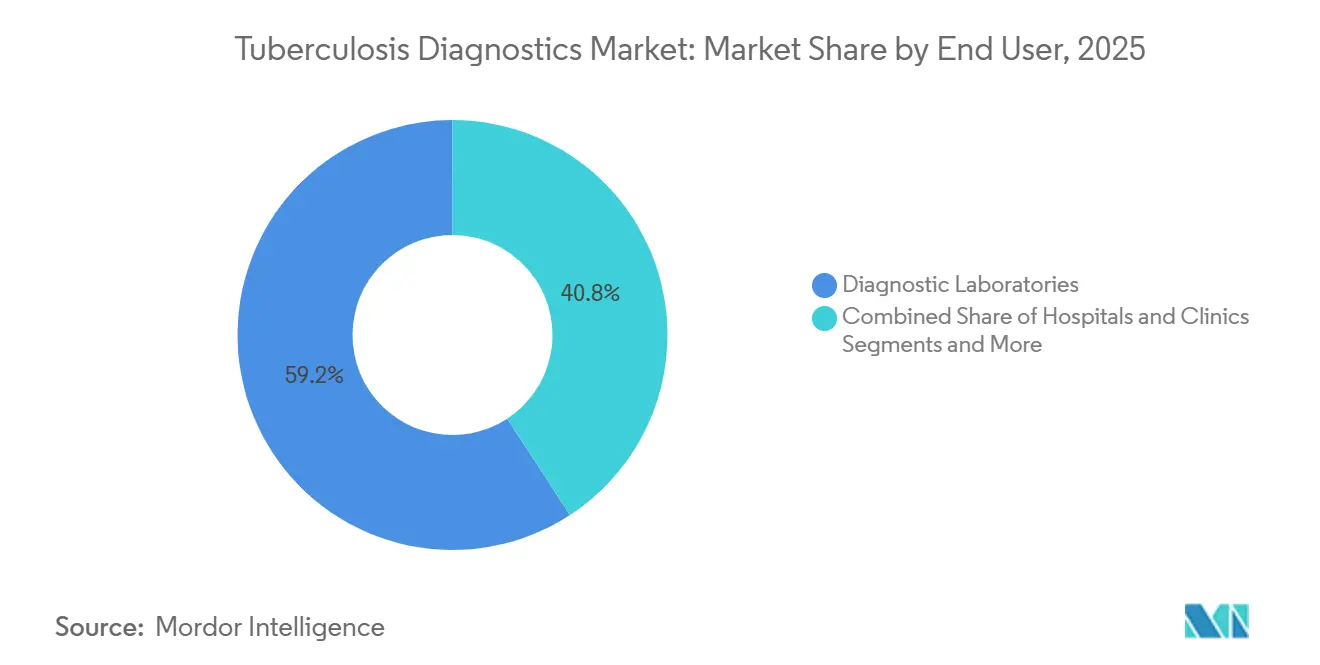

- By end user, diagnostic laboratories accounted for 59.20% of the tuberculosis diagnostics market in 2025, whereas hospitals and clinics are advancing at a 6.67% CAGR through 2031.

- By geography, North America accounted for 39.10% of the tuberculosis diagnostics market in 2025, whereas Asia-Pacific is expected to register the fastest CAGR of 6.75% over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Tuberculosis Diagnostics Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of drug-resistant TB strains | +1.2% | Global, concentrated in India, China, South Africa, Philippines | Medium term (2-4 years) |

| Who endorsement & national roll-outs of NAAT platforms | +1.5% | High-burden countries in Asia-Pacific, Sub-Saharan Africa, Eastern Europe | Short term (≤ 2 years) |

| Government funding & global health initiatives | +0.9% | Asia-Pacific, Middle East and Africa, select South America markets | Medium term (2-4 years) |

| Emergence of AI-powered microscopy & digital radiology triage | +0.8% | Asia-Pacific, Sub-Saharan Africa, with pilot adoption in North America | Long term (≥ 4 years) |

| Decentralised near-POC molecular platforms | +1.1% | Rural and peri-urban areas in India, Indonesia, Nigeria, Kenya | Medium term (2-4 years) |

| Subscription-based diagnostics-as-a-service models | +0.4% | North America, Europe, urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Drug-Resistant TB Strains

Multidrug-resistant tuberculosis cases climbed to an estimated 410,000 globally in 2025, with rifampicin-resistant strains accounting for 3.6% of new cases and 18% of previously treated cases, according to WHO surveillance data. This epidemiological shift is forcing national programs to pivot from empirical treatment to genotypic drug-susceptibility testing, which requires molecular assays capable of detecting mutations in rpoB, katG, and inhA genes within 2 hours. This technical bar only cartridge-based NAAT platforms currently meet at scale. Germany’s 5.7% multidrug-resistant incidence and Côte d’Ivoire’s 22% rifampicin resistance among retreatment cases show how resistance patterns differ by geography. Xpert MTB/XDR delivers actionable drug profiles in 90 minutes, while Abbott’s RealTime MTB RIF/INH assay achieves 94.8% sensitivity for rifampicin and 88.3% for isoniazid, letting clinicians tailor therapy promptly. Nations are also piloting targeted next-generation sequencing to comprehensively map resistance, moving diagnostic workflows from culture-dependent to molecular-first approaches.

WHO Endorsement & National Roll-Outs of NAAT Platforms

WHO’s March 2024 guideline update placed molecular rapid tests at the front of all diagnostic algorithms and introduced targeted sequencing advice for drug-resistant surveillance WHO.[3]World Health Organization, “Global Tuberculosis Report 2025,” WHO.INT India’s Initiative for Promoting Affordable and Quality TB Tests boosted Xpert uptake tenfold and cut prices by up to 50%, scaling from 56 to 211 labs in five years. Uganda: by decentralizing NAATs to district hospitals, shortened the median time to treatment initiation and increased same-day confirmations, NEJM. WHO prequalification is the de facto gatekeeper for Global Fund, USAID, and UNITAID financing; Cepheid’s Ultra assay and Eiken’s TB-LAMP together triggered USD 340 million of commitments in 1Q 2025. India’s NTEP scaled molecular capacity nationwide, while the Philippines achieved a 1,008% surge in case detection during a Truenat pilot on the Bantayan Islands, where battery-powered devices bypass erratic grid supply. The policy cascade shortens technology diffusion cycles to fewer than 24 months across Asia-Pacific, a timeline once witnessed only in high-income markets.

Emergence of AI-Powered Microscopy & Digital Radiology

A 12-country study revealed that computer-vision algorithms achieved 89% sensitivity and 97% specificity on Ziehl-Neelsen smears for USD 0.30 per test, compared to USD 10 for NAAT cartridges.[4]Nature Medicine, “AI-Enhanced Microscopy for Tuberculosis Detection: A 12-Country Validation Study,” NATURE.COM Ministries are now implementing AI microscopy as a triage layer, with flagged positive cases proceeding to confirmatory NAAT testing and negative cases exiting the process. This strategy has reduced overall molecular testing volume by 40% without compromising diagnostic yield. In 2025, Delft Imaging processed 2.3 million chest X-rays, identifying 87,000 presumptive cases that would have been missed through symptom-based screening. However, the algorithm's sensitivity drops to 72% among HIV-coinfected patients, leading to delays in regulatory approvals in South Africa and Kenya.

Decentralized Near-POC Molecular Platforms

In 2025, Molbio's Truenat, a battery-operated PCR system, secured 3,400 orders across Nigeria, Kenya, and Papua New Guinea, effectively eliminating the USD 1.20 cold-chain surcharge in rural clinics. Cepheid's Omni prototype optimized the user process by reducing steps from seven to two, resulting in a 60% decrease in error rates during trials conducted in Indonesia and Mozambique. A study published in PLOS Medicine reported an incremental cost-effectiveness of USD 280 per DALY averted when devices are located within 10 kilometers of communities, a figure well below WHO's established thresholds.

Restraints Impact Analysis of Tuberculosis Diagnostics Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost of molecular tests & cartridges | -0.9% | Low-income countries in Sub-Saharan Africa, South Asia, parts of South America | Short term (≤ 2 years) |

| Shortage of skilled laboratory infrastructure | -0.7% | Rural areas in Asia-Pacific, Sub-Saharan Africa, remote regions in South America | Medium term (2-4 years) |

| Supply-chain fragility for single-source cartridges | -0.5% | Global, acute in markets dependent on single-supplier procurement | Short term (≤ 2 years) |

| Competition from emerging non-sputum biomarkers | -0.3% | Research-intensive markets in North America, Europe, select Asia-Pacific hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Molecular Tests & Cartridges

Traditional desktop platforms can exceed USD 19,000, whereas Tulane’s lab-in-tube device costs under USD 800 and keeps per-test pricing below USD 3. Economic analyses in Brazil and India showed Diaskintest at USD 22.6 and USD 41.0 per correct case, while TSPOT.TB delivered greater effectiveness at incremental costs of USD 55-74. Cepheid’s cost-price cartridge offer narrows the gap, yet a sustainable reimbursement model remains critical for widespread adoption.

Shortage of Skilled Laboratory Infrastructure

A proficiency survey in Ethiopia revealed only 81.92% competency in smear microscopy, with performance tied to refresher training and years of experience. Sub-Saharan facilities reported 66% Xpert coverage but just 4% Line Probe Assay uptake owing to funding and workforce limitations, BMJ Global Health. WHO’s laboratory manual emphasizes quality-assured capacity building, while the CDC’s Tuberculosis Education and Training Network and the Curry International Tuberculosis Center provide ongoing webinars and hands-on coaching. Nigeria’s public-private model showed that training, along with instrument redistribution, produced a 28-fold increase in suspected referrals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Tuberculosis Diagnostics Market Segment Analysis

By Test Type:

Culture Methods Regain MomentumIn 2025, culture-based assays accounted for 38.45% of the revenue, with projections indicating a 6.54% annual growth rate. This increase is driven by WHO guidelines requiring phenotypic confirmation for all rifampicin-resistant cases. While NAAT remains the leading method for primary screening, laboratories are increasingly integrating rapid genotyping with subsequent culture testing. This dual-track workflow enables quick therapy initiation through molecular methods, while culture testing provides detailed insights to optimize treatment regimens.

Continued donor funding sustains the cost-effectiveness of smear microscopy at USD 2 per slide, particularly in regions conducting high volumes of Ziehl-Neelsen tests, such as India. However, as digital microscopy and AI algorithms achieve sensitivity levels comparable to NAAT at significantly lower reagent costs, traditional smear microscopy is gradually being relegated to peripheral triage applications.

By Technology:

AI Microscopy Emerges as Fastest-Growing ModalityIn 2025, molecular diagnostics accounted for 45.23% of revenue. However, AI-enhanced microscopy is witnessing the fastest growth rate among modalities, increasing at 7.15% annually. This growth is driven by the adoption of computer-vision software that repurposes existing optical systems. Additionally, immunoassays, particularly interferon-gamma release assays (IGRAs), play a critical role in screening latent infections within immigration and transplant groups across Europe and North America. This niche market is expected to grow at an annual rate of 4.2%, supported by stricter occupational mandates.

Culture technology remains indispensable for resistance phenotyping. When integrated with automated MGIT systems, automation has reduced turnaround times from 42 days to as few as 14 days. Consequently, the tuberculosis diagnostics industry is transitioning toward integrated algorithms that utilize AI microscopy for triage, confirm diagnoses with NAAT, and finalize therapy plans using culture profiles.

By End User:

Hospital Uptake Narrows Lab DominanceIn 2025, diagnostic laboratories accounted for 59.20% of the revenue. However, hospitals and clinics are projected to grow at a CAGR of 6.67% through 2031. This growth is driven by benchtop NAAT modules that reduce turnaround times to under two hours. Additionally, subscription models that bundle instruments, maintenance, and software into per-test fees are lowering upfront spending barriers. This approach is enabling smaller secondary hospitals to enter the tuberculosis diagnostics market.

Although academic centers and research institutes contribute less than 5% of sales, they are at the forefront of developing host-response transcriptomic tests that could advance diagnosis beyond traditional sputum methods. In 2025, a study demonstrated 83% sensitivity for a whole-blood gene-signature assay tested on 2,400 patients. This development highlights a pathway for non-sputum detection at the community level.

Geography Analysis

The Americas, EMEA and APAC Tuberculosis Diagnostics Market

North America accounted for 39.10% of the tuberculosis diagnostics market in 2025, aided by comprehensive insurance coverage and consistent CDC laboratory upgrades. Asia-Pacific is forecast to expand at a 6.75% CAGR, driven by India’s one-third share of the global burden and policy shifts from smear microscopy to NAAT. Europe posted 38,993 cases across 29 EU/EEA nations in 2024; Ukrainian refugee screening recorded 12.8 per 100,000 incidence with 26% multidrug resistance, prompting intensified entry screening. South America benefits from national Xpert scale-up; Brazil’s rollout increased notifications by 9.7% and catalyzed multisector coordination. The Middle East and Africa see uneven progress: while Nigeria’s AI-linked vans record 1.75 times higher positivity in hotspots, only 4% of labs can run Line Probe Assays. Diaskintest is cheaper than tuberculin in Brazil and India, but TSPOT.TB delivers higher accuracy at added expense, underscoring divergent procurement choices

Regulatory Landscape

Tuberculosis diagnostics are shaped by a combination of WHO policy guidance and country-level medical device regulation. WHO updated Module 3 guidance on TB diagnosis in 2024-2025, reinforcing rapid molecular testing within diagnostic algorithms and adding recommendations on sequencing for drug-resistance surveillance, which then feeds into national test menus and tender specifications in high-burden settings financed by the Global Fund, USAID, and UNITAID.

In the United States, the FDA continues to act as a key gatekeeper for both latent TB infection tests and laboratory automation workflows. This is reflected in Revvity's April 2025 FDA clearance for the Auto-Pure 2400 integrated with the T-SPOT.TB test, as well as the FDA's March 2026 proposed reclassification of Mycobacterium tuberculosis cell-mediated immunity tests. In Europe, the EU IVD Regulation (IVDR, Regulation 2017/746) places TB IVDs in Class C, which increases reliance on Notified Bodies for conformity assessment and tightens expectations around quality systems and clinical evidence for manufacturers commercializing molecular, immunoassay, and AI-enabled diagnostic solutions.

Competitive Landscape

The tuberculosis diagnostics market remains moderately concentrated. Cepheid sustains leadership by placing more than 20,000 GeneXpert units and selling cartridges at cost in 145 eligible nations. Roche stepped up through its 2024 acquisition of LumiraDx point-of-care technology and a Gates Foundation partnership to co-develop rapid TB tests. Siemens Healthineers is using AI to differentiate, exemplified by its Global Fund collaboration that embeds algorithmic chest X-ray triage in Indonesian clinics. Abbott competes with RealTime MTB-RIF/INH and has filed for expanded WHO endorsements.

Smaller entrants address affordability gaps: Tulane’s USD 3 assay targets rural outreach. Oxford Nanopore is field-testing a sequencing-based resistance panel designed for 30-minute readouts. Start-ups are piloting subscription bundles that wrap reagent costs into per-test fees, easing up-front capital barriers for small clinics. Public-private projects such as Nigeria’s 28-fold surge in referrals illustrate how distribution partnerships and training packages can quickly expand market access. Yet regulatory complexity and stringent clinical evidence expectations still favor large incumbents with global QA systems.

Tuberculosis Diagnostics Industry Leaders

Abbott Laboratories

Becton, Dickinson and Company

BioMérieux SA

Thermo Fisher Scientific Inc.

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Tuberculosis Diagnostics Market Companies Covered in this Report

- Abbott Laboratories

- Beckton Dickinson

- bioMérieux

- Danaher

- Roche

- FUJIFILM

- Hologic

- Luminex Corporation (DiaSorin)

- LumiraDx Ltd.

- Meridian Bioscience

- Molbio Diagnostics Private Limited.

- Oxford Immunotec Ltd.

- QIAGEN

- QuantuMDx Ltd.

- SD Biosensor Inc.

- Seegene

- Siemens Healthineers

- Tauns Laboratories Inc

- Thermo Fisher Scientific

Market Opportunities and Future Outlook

Decentralized testing remains a key whitespace, with programs pushing near point-of-care deployment and alternative specimen pathways. In March 2026, WHO recommended new near point-of-care TB diagnostic tools with under-one-hour turnaround. In May 2026, WHO and the Stop TB Partnership published a toolkit focused on near point-of-care and swab-based testing, which provides implementation support for shifting testing closer to community settings and reducing dependence on centralized laboratories.

Financing and implementation infrastructure also shape how much scale-up translates into higher case detection, particularly where connectivity and workflow integration affect utilization. Unitaid has highlighted an active USD 44 million investment portfolio (since 2022) aimed at improving access to TB diagnosis and reducing costs. Its May 2025 USD 15.3 million investment for drug-resistant TB testing and treatment across 16 countries, with KELIN, Partners in Health, and the Stop TB Partnership, further points to demand creation and system-strengthening alongside product procurement. Stop TB Partnership programs such as the Introducing New Tools Project broaden the adoption runway for integrated solutions that bundle ultra-portable digital X-ray, AI computer-aided detection, and targeted sequencing with deployment support.

Recent Industry Developments in Tuberculosis Diagnostics Market

- June 2026: Becton, Dickinson and Company launched the Tuberculosis (TB) Guardianship Programme in India with partners including the Indian Chest Society and USAID. The programme focuses on knowledge exchange and strengthening diagnostic practices, supporting broader adoption of standardized TB testing workflows in a high-burden market.

- April 2026: Thermo Fisher Scientific entered a definitive agreement to divest its Microbiology business to Astorg. The transaction reorganizes ownership of microbiology platforms used in infectious disease testing and can shift product focus, investment priorities, and channel strategies serving TB laboratories.

- November 2025: bioMerieux partnered with Oxford Nanopore to launch AmPORE-TB, a research-use-only sequencing solution for characterization of drug-resistant tuberculosis. The release supports sequencing-enabled workflows for resistance profiling and helps labs assess faster, more comprehensive drug-resistance surveillance approaches.

Tuberculosis Diagnostics Market Report Scope and Research Methodology

Market Definition and Coverage

This market counts the revenues generated from tests and test systems used to detect human tuberculosis infection, whether it is latent or active, across lab and point-of-care settings. The sizing covers key TB diagnostic procedures and the related consumables and instruments tied to running those tests.

Scope exclusions: Veterinary (bovine) tuberculosis testing and anti-TB drug treatments are not counted in this market sizing.

Segments Covered in This Report

- By Test Type

- Culture-based Tests

- Smear Microscopy

- Nucleic Acid Amplification Tests (NAAT)

- Interferon-Gamma Release Assays (IGRA)

- Tuberculin Skin Test (Mantoux)

- Radiographic & Imaging Tests

- Other Tests

- By Technology

- Culture-based

- Molecular Diagnostics

- Immunoassays

- Radiology / X-ray

- AI-enhanced Digital Microscopy

- Others

- By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Academic & Research Institutes

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context for TB testing, then anchoring the model to disease burden and program activity reflected in official reporting. We rely on public sources such as World Health Organization TB reports, US CDC TB surveillance summaries, and national health ministry dashboards where available.

We then supplement this with reference material such as peer-reviewed journals on diagnostic adoption and test performance, procurement and tender disclosures from public agencies, and trade statistics for relevant diagnostic inputs using an import and export shipment-level database. Company filings, investor presentations, and product documentation are also used to understand what is being sold, where it is being used, and how pricing is shifting over time. These examples are illustrative, and many other public sources were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions around test mix, typical pricing ranges, and how volumes move across public TB programs versus private care. We spoke with diagnostic lab decision makers, hospital and clinic users, distributors, and industry specialists across major regions, then used their inputs to align adoption rates and utilization patterns to operational conditions seen on the ground.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | APAC: 44% |

| Mid tier: 55% | Functional/Unit leaders: 36% | EMEA: 30% |

| Smaller Players: 17% | Managers: 48% | Americas: 26% |

Market-Sizing & Forecasting

Our model uses a top-down demand pool build, where TB incidence, screening intensity, and diagnostic algorithm pathways are translated into expected testing volumes by modality, before values are derived using observed price bands. The totals are then checked with selective bottom-up approximations like sampled ASP times volume for representative test categories, along with channel checks where coverage is available, so the market stays explainable by measurable drivers.

Inputs that are monitored include reported TB case notifications, latent TB screening activity in high-risk cohorts, molecular test placement trends, public procurement cycles, and the share shift between smear, culture, NAAT, and immunoassays. Because pricing can move with subsidies and mix changes, average selling price progression is refreshed using interview feedback and publicly visible product list pricing where it is posted.

For forecasting, we mainly use scenario analysis supported by multivariate regression on a short list of drivers that consistently influence testing, such as disease burden, funding intensity, and diagnostic algorithm upgrades. When data is thin for a sub-segment or geography, gaps are handled by applying conservative penetration ranges and utilization benchmarks that were validated in interviews, then rebalanced so regional totals stay consistent with broader demand signals.

Data Validation & Update Cycle

Estimates are validated through cross-checks between independent signals, such as TB notification trends, screening guidance updates, and public procurement behavior, before numbers are finalized. When an outlier appears, the assumptions behind volume, price, or mix are re-checked, and follow-up outreach is triggered if the variance cannot be explained from published sources.

A multi-step internal review is applied so key calculations, unit conversions, and currency treatments are verified, followed by a final consistency check across regions and test types. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is done so clients receive the latest view available at the time.

Mordor Intelligence's Tuberculosis Diagnostics Market Size Compared Against Other Published Estimates

Published market sizes for TB diagnostics can vary even when they look similar at a headline level, because the included test scope, pricing level in the channel, and the timing of the data refresh are not handled the same way. Differences also show up when some studies emphasize public program procurement while others assume a broader private testing footprint.

By tracking test mix shifts across smear, culture, NAAT, and immunoassays and refreshing manufacturer-level price bands, Mordor Intelligence keeps the total tied to diagnostic procedures rather than distributor markups or loosely defined care pathways. The remaining spread comes from how latent TB testing is counted, how imaging-related diagnostics are treated, and whether the base year uses updated notification and procurement signals or older snapshots.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.58 B (2025) | |

| Global Consultancy A | USD 2.28 B (2024) | Uses a different base year and may apply broader revenue recognition that blends channel effects with manufacturer pricing, which can lower or shift the starting point versus a procedure-linked test mix build. |

| Industry Publisher B | USD 2.40 B (2025) | Keeps a similar year but narrows modality coverage more heavily around core lab methods, which can undercount imaging-linked or newer workflow items that still contribute to diagnostic spending in some care settings. |

Taken together, the comparison shows that most of the gap is explained by what gets counted as a TB diagnostic revenue stream and how pricing is carried through the model. With clear inclusions, careful price handling, and repeatable checks against testing signals, the sizing stays easier to trace and reconcile.

Key Questions Answered in the Report

What is the projected global value of the tuberculosis diagnostics market in 2031?

The market is forecast to reach USD 3.63 billion by 2031.

Which region is growing fastest for tuberculosis testing solutions?

Asia-Pacific leads with a 6.75% CAGR through 2031 owing to large-scale molecular rollouts in India, Indonesia and the Philippines.

Why are culture methods still expanding when molecular tests are popular?

Phenotypic culture remains the gold standard for confirming resistance to new drugs, and WHO guidelines now mandate culture checks for all rifampicin-resistant cases, boosting demand.

How are subscription models changing hospital purchasing behavior?

Diagnostics-as-a-service shifts costs from capital expenditure to per-test fees, enabling smaller hospitals to install onsite NAAT modules without USD 68,000 up-front payments.

What role does AI play in lowering diagnostic costs?

AI-enhanced digital microscopy achieves near-NAAT sensitivity at USD 0.30 per test and reduces overall molecular volume by triaging smear-positive samples.

Which companies dominate the molecular cartridge segment today?

Cepheid and Roche collectively account for about 60% of the installed molecular cartridge base worldwide.

Page last updated on: