Dengue Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

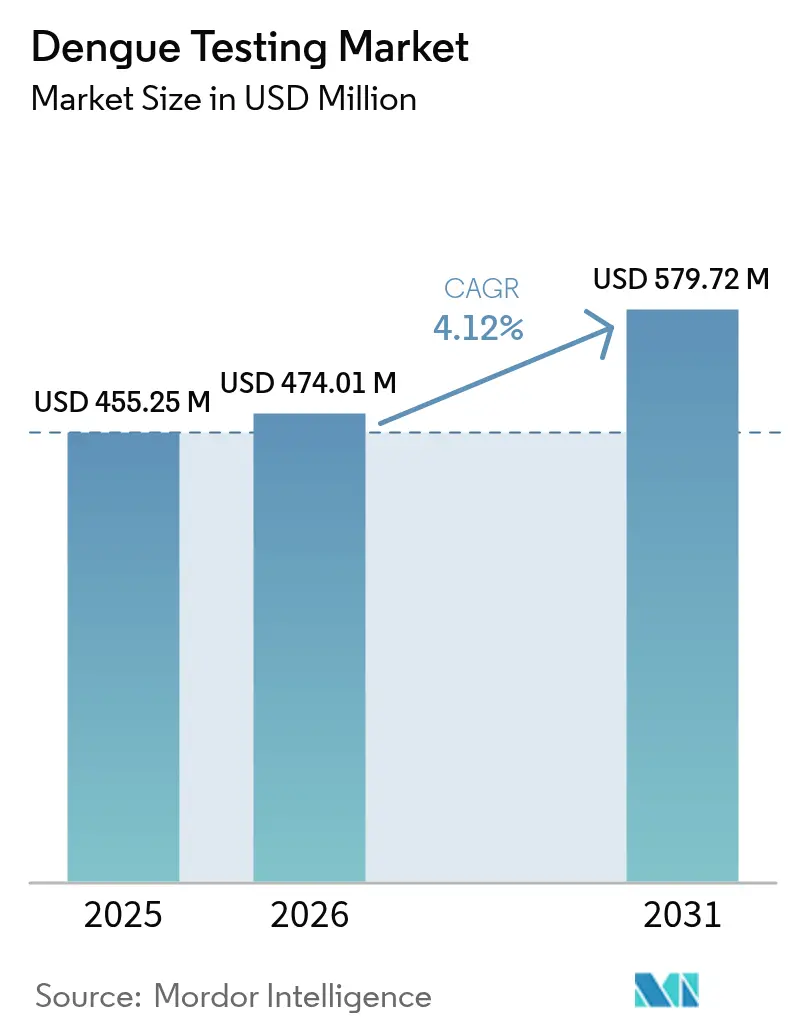

| Market Size (2026) | USD 474.01 Million |

| Market Size (2031) | USD 579.72 Million |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

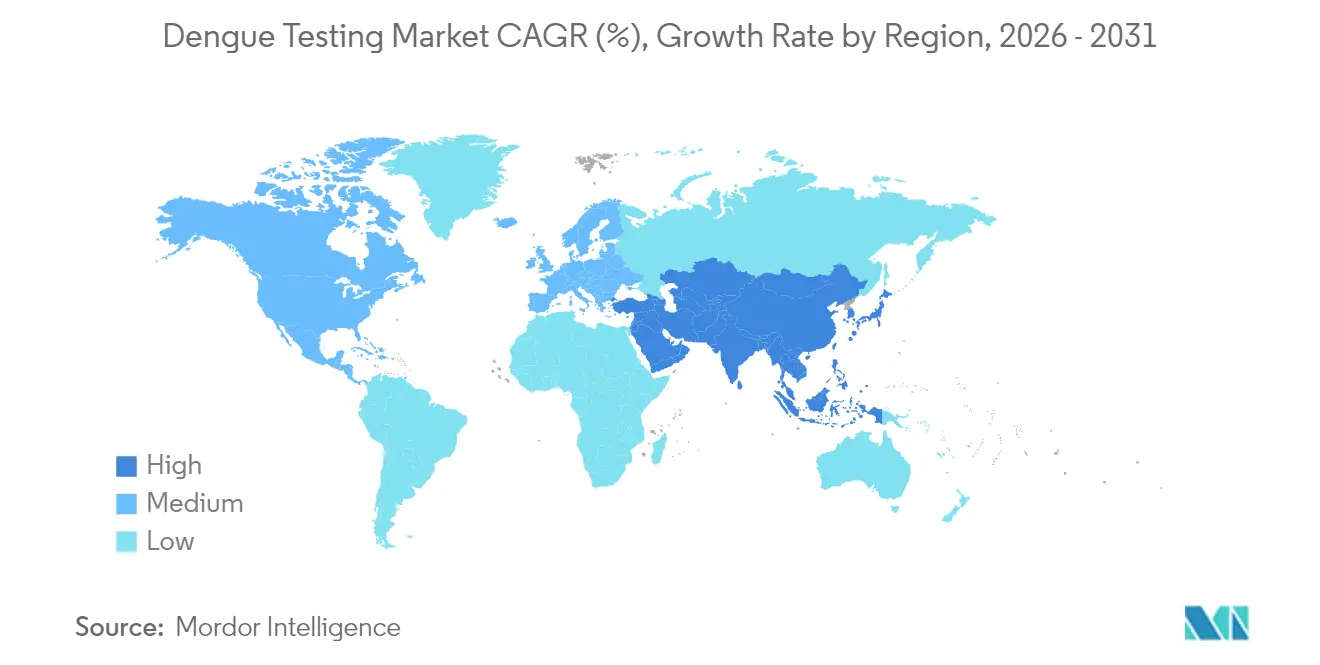

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dengue Testing Market Analysis by Mordor Intelligence

Dengue testing market size in 2026 is estimated at USD 474.01 million, growing from 2025 value of USD 455.25 million with 2031 projections showing USD 579.72 million, growing at 4.12% CAGR over 2026-2031. Heightened attention to cross-reactivity with related flaviviruses, rising temperate-zone transmission linked to climate change, and tighter regulatory oversight shape the competitive agenda. Diagnostic providers concentrate on multiplex platforms that distinguish dengue from Zika and Chikungunya, while expansion into non-endemic regions boosts demand among travel clinics and surveillance programs. Improvements in biosensor sensitivity and reagent stability strengthen point-of-care economics, even as supply-chain gaps for recombinant NS1 proteins persist. Intensifying FDA and EMA approval activity continues to reward firms able to meet stringent performance thresholds and post-market vigilance expectations.

KEy Report Takeaways

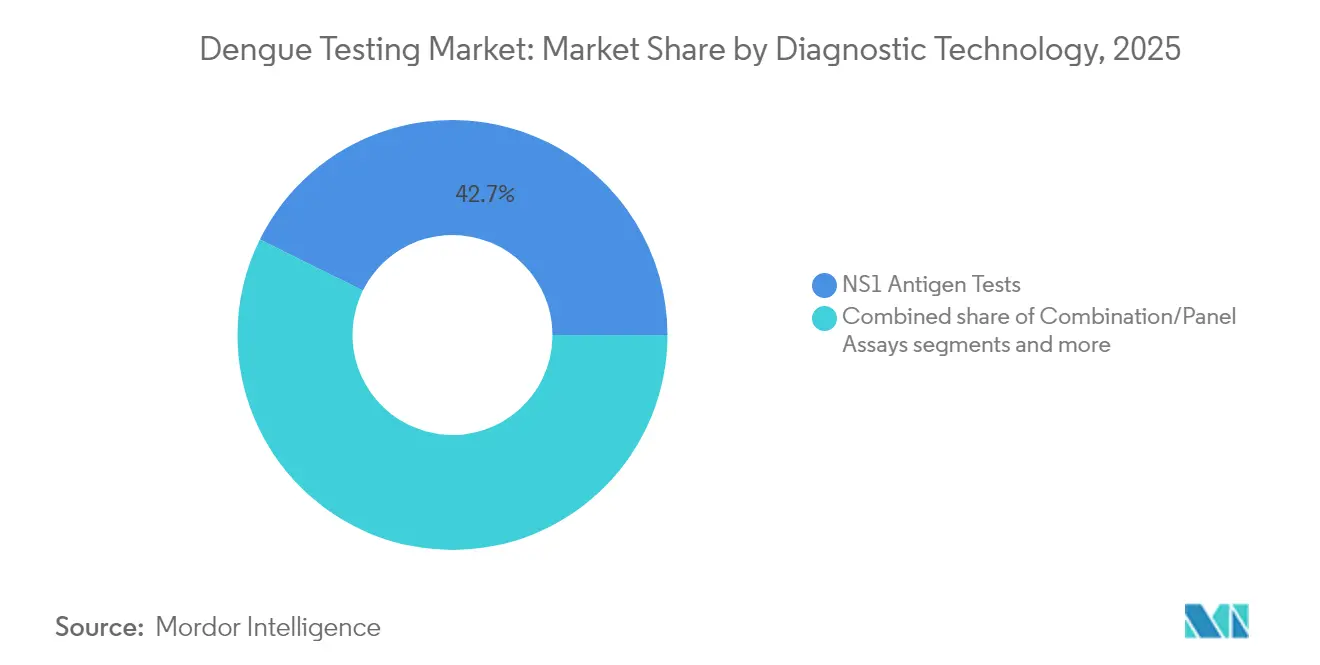

- By diagnostic technology, NS1 antigen tests held 42.68% of the dengue testing market share in 2025, Combination/panel assays are projected to grow at a 4.89% CAGR between 2026 and 2031.

- By end-user, hospitals and clinics accounted for 46.96% of revenue in 2025, whereas diagnostic laboratories are expected to expand at a 4.38% CAGR through 2031.

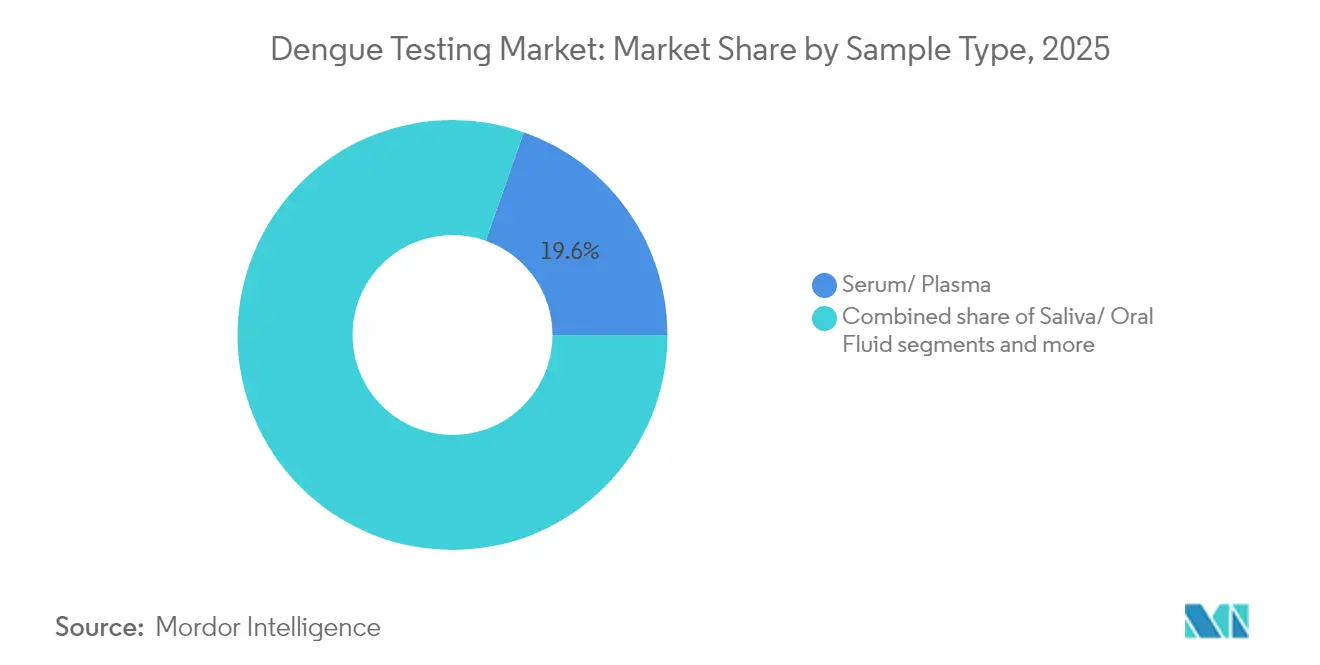

- By sample type, serum/plasma commanded 19.62% of the dengue testing market size in 2025, while saliva/oral fluid is advancing at a 4.71% CAGR to 2031.

- By geography, North America led with 24.05% revenue share in 2025; Asia-Pacific is poised for the fastest growth at a 4.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dengue Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising dengue incidence & frequent outbreaks | +1.2% | Global, with APAC and Latin America most affected | Medium term (2-4 years) |

| WHO-led push for early laboratory confirmation and surveillance | +0.8% | Global, with priority in endemic regions | Long term (≥ 4 years) |

| Adoption surge of rapid NS1 antigen point-of-care tests | +0.9% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Pre-vaccination serostatus screening mandates | +0.6% | North America, EU, and select APAC markets | Medium term (2-4 years) |

| Climate-linked vector expansion into temperate regions | +0.7% | North America, Europe, with emerging presence in higher latitudes | Long term (≥ 4 years) |

| Integration of digital outbreak-alert platforms | +0.4% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Dengue Incidence & Frequent Outbreaks

Global case counts surpassed 6.5 million in 2024, tripling historical averages and triggering widespread laboratory confirmation requirements. Securing accurate differentiation from malaria, typhoid, and other febrile illnesses became a clinical priority, pushing demand for dependable diagnostic kits. Economic losses tied to misdiagnosis encouraged hospitals to adopt rapid assays that deliver results within 48 hours. Outbreak seasonality varied by hemisphere, ensuring steady year-round test volumes. Health agencies responded with bulk-procurement frameworks that locked-in minimum purchase quantities and guaranteed supplier revenues.

WHO-Led Push for Early Laboratory Confirmation and Surveillance

Updated 2024 WHO guidance requires lab confirmation for suspected cases, converting sporadic testing into standardized fever-screening programs. Endemic nations adopted WHO-prequalified kits to meet reporting obligations under the Global Health Observatory. Integration with digital surveillance platforms accelerated transmission mapping and stock planning. This shift favored manufacturers able to provide validated performance data and electronic data-capture interfaces. Long-term demand is bolstered by donor-funded initiatives that underwrite kit costs in resource-constrained settings.

Adoption Surge of Rapid NS1 Antigen Point-of-Care Tests

Enhanced NS1 sensitivity now reaches 85-90% during the acute phase, resolving prior reliability concerns00123-4/fulltext). Results arrive in 15–20 minutes, allowing immediate triage in emergency departments. Lower per-test costs achieved through scaled production made NS1 viable for middle-income markets. The timing advantage of antigen detection during the first week of illness cemented NS1 as the frontline diagnostic in outbreak response protocols. Upgrades in reagent thermostability further extended shelf life under tropical conditions.

Pre-Vaccination Serostatus Screening Mandates (CYD-TDV & TAK-003)

IgG screening before immunization became compulsory in several jurisdictions to avoid vaccine-enhanced disease, generating predictable high-volume test orders. Population-level vaccination drives now embed diagnostics into routine schedules, encouraging labs to invest in high-throughput platforms. The cost of screening is offset by avoided hospitalizations, solidifying budget allocations for annual procurement. Companies supplying both vaccine and screening reagents enjoy cross-selling synergies that raise switching barriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variable sensitivity/specificity of many rapid kits | -0.8% | Global, particularly affecting LMIC markets | Short term (≤ 2 years) |

| Cross-reactivity with other flaviviruses muddying results | -0.6% | APAC, Latin America, and sub-Saharan Africa | Medium term (2-4 years) |

| Supply-chain fragility for recombinant NS1 reagents in LMICs | -0.4% | Sub-Saharan Africa, parts of APAC and Latin America | Medium term (2-4 years) |

| Regulatory lag for multiplex dengue-Zika-ChikV panels | -0.3% | Global, with particular impact on innovative products | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Variable Sensitivity/Specificity of Many Rapid Kits

Clinical evaluations show sensitivity ranging from 45% to 90% across brands, creating uncertainty among frontline clinicians. Substandard kits erode confidence and push procurement toward laboratory-based assays, lengthening turnaround times. LMIC regulators often lack resources for rigorous pre-market reviews, allowing inferior products into distribution. This dynamic prolongs sales cycles for high-quality suppliers that must present comparative data. Market educators now emphasize head-to-head performance studies to restore trust.

Cross-Reactivity with Other Flaviviruses Muddying Results

Serological overlap with Zika, yellow fever, and Japanese encephalitis diminishes diagnostic clarity, especially in regions where multiple viruses circulate. Confirmatory plaque-reduction neutralization assays add cost and delay, hampering timely clinical decision-making. Travelers and residents with complex exposure histories confuse interpretation of IgM/IgG results, prompting reliance on more expensive molecular methods. The added expense restricts access in low-resource settings where rapid differentiation is most critical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnostic Technology: NS1 Leadership Faces Multiplex Ascendancy

NS1 antigen assays generated 42.68% of the dengue testing market share in 2025 by providing early detection during the viraemic window when interventions yield the greatest clinical value. Yet the dengue testing market is witnessing the fastest acceleration in combination/panel assays at a 4.89% CAGR through 2031 as clinicians demand simultaneous differentiation among co-endemic viruses. The dengue testing market size for multiplex panels is projected to widen as public-health agencies standardize outbreak response algorithms on multi-pathogen detection. RT-PCR continues as the reference confirmation tool, especially for research and serotype surveillance. Biosensor-based platforms, employing electrochemical or optical readouts, promise laboratory-grade sensitivity in portable formats, creating an inflection point once regulatory approval is secured.

Emerging technology suppliers integrate artificial-intelligence modules to interpret weak signal bands, reducing reader subjectivity and improving field accuracy. Regulatory scrutiny remains intense, with FDA 510(k) clearances contingent upon robust cross-reactivity data. Successful approvals can reorder competitive hierarchies as buyers consolidate around high-performance multiplex systems.

By End-User: Laboratory Upswing Overtakes Hospital Dominance

Hospitals and clinics retained 46.96% revenue leadership in 2025, anchored by acute-care protocols that rely on rapid antigen kits for triage. Nevertheless, laboratory providers exhibit a 4.38% CAGR, outpacing traditional settings as the dengue testing market migrates toward consolidated high-throughput environments. Central laboratories achieve economies of scale in serostatus screening, critical for vaccination programs. Integration with laboratory information systems simplifies electronic reporting obligations and supports reimbursement claims. The dengue testing industry records nascent but growing interest in self-testing, catalyzed by pandemic-driven consumer familiarity with at-home diagnostics. Regulatory pathways for home use remain stringent; however, early European approvals suggest eventual diffusion into additional markets.

By Sample Type: Saliva Spurs Non-Invasive Expansion

Serum/plasma maintained a 19.62% share in 2025 due to entrenched clinical protocols and assay validation history. The dengue testing market now observes momentum in saliva/oral fluid, clocking a 4.71% CAGR on patient comfort and simplified collection. Innovations in stabilizing buffers preserve viral proteins, rendering salivary results comparable to blood-based methods within the acute window. Whole blood retains value in point-of-care settings where finger-stick convenience speeds frontline decision-making. Dried blood spots fulfill logistical needs for remote areas lacking cold-chain infrastructure, though longer processing times limit emergency uses.

Geography Analysis

North America delivered 24.05% of global revenue in 2025, supported by robust insurance coverage and travel-screening programs that extend beyond endemic zones. U.S. states such as Florida implemented routine Aedes surveillance, driving continual procurement of multiplex kits. Canada’s demand centers on major airports and urban hospitals, while Mexico’s endemic burden secures government tenders for both rapid and laboratory assays. The dengue testing market size in North America benefits from early adoption of digital reporting mandates, incentivizing integrated analyzer connectivity.

Asia-Pacific records the highest regional growth at a 4.79% CAGR through 2031, propelled by India’s national vector-borne disease strategies and China’s urban health reforms. Thailand and Vietnam sustain elevated per-capita test rates due to hyperendemic transmission, whereas Singapore deploys airport-based rapid screening for incoming travelers. South Korea prioritizes imported case detection, leveraging centralized labs to manage seasonal spikes. Australia’s northern territories maintain steady demand, with preparedness budgets funding diagnostic stockpiles against potential southward vector spread.

South America advances on the back of Brazil’s dominant spend and Argentina’s expanding lab capacity. Brazil’s experience handling concurrent dengue, Zika, and Chikungunya epidemics underpins aggressive multiplex adoption. Europe registers moderated growth, concentrated around Mediterranean countries where Aedes albopictus establishes seasonal footholds. The Middle East and Africa present a heterogeneous picture: Gulf Cooperation Council members focus on travel-related testing, while sub-Saharan nations grapple with supply constraints that hamper widespread deployment despite high disease incidence.

Regulatory Landscape

Dengue IVDs face tightening performance and quality expectations, especially around cross-reactivity and claims for early acute detection. In the United States, the FDA classifies dengue virus nucleic acid amplification test (NAAT) reagents and dengue virus serological reagents as Class II devices subject to special controls, which reinforces requirements for analytical and clinical validation and labeling controls when differentiating dengue from other flaviviruses.

During the 2024-2025 dengue emergency context, WHO activated a Dengue Expert Review Panel for Diagnostics (May 2025) to support procurement decisions for non-prequalified IVDs, adding an evidence-based gate for suppliers competing for outbreak-funded tenders. At the same time, US policy attention to laboratory developed tests increased with a staged phaseout beginning May 6, 2025, and FDA finalized emergency-related IVD enforcement guidance in September 2025, raising expectations for validation, risk mitigation, and post-market oversight versus approaches that relied on discretionary pathways.

Value Chain Analysis

The dengue testing value chain begins with sourcing critical biological and material inputs, including recombinant dengue proteins (such as NS1), monoclonal antibodies, nitrocellulose membranes, and colloidal gold or other signal chemistries. It then moves through assay design, validation, and ISO 13485-aligned manufacturing (including CE-IVDR aligned systems for European commercialization). WHO diagnostic algorithms tied to days post symptom onset shape product positioning and portfolio mix, linking acute-phase demand to NAAT and NS1 antigen detection and later-stage testing to IgM/IgG serology, while reference and surveillance laboratories use molecular workflows for confirmation and serotype monitoring.

Downstream, manufacturers distribute finished kits through clinical distributors and public tenders for hospitals, clinics, and centralized diagnostic laboratories, where stability and packaging (moisture-proof foil, desiccants, and temperature-controlled logistics) weigh heavily in endemic and tropical environments. Bottlenecks often appear around reagent supply consistency, particularly recombinant NS1, along with distribution conditions in LMIC settings. This raises the importance of validated shelf-life claims, temperature monitoring practices, and local registration pathways for tender eligibility.

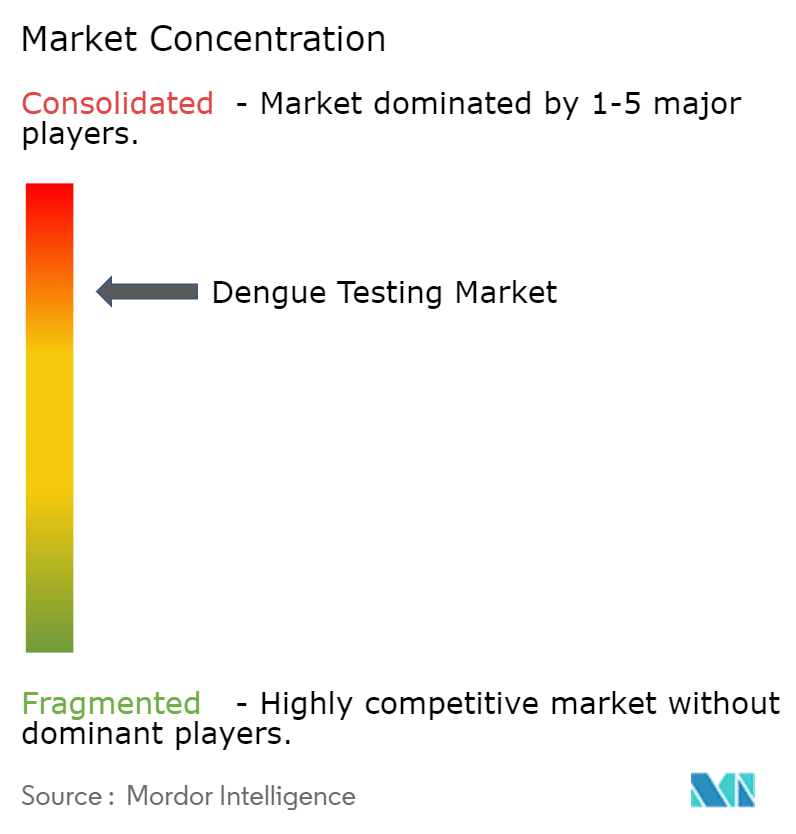

Competitive Landscape

The dengue testing market remains moderately fragmented, with no single supplier exceeding a dominant threshold. Abbott leverages a global logistics footprint to distribute upgraded NS1 assays, while Roche’s cobas platform secures high-throughput laboratory contracts through automation advantages. bioMérieux augmented its rapid test line by acquiring GenBody, enhancing reach across Southeast Asia. Thermo Fisher targets the research niche with multiplex RT-PCR kits capable of serotype quantification.

Patent clustering around NS1 monoclonal antibodies and microfluidic cartridge designs shapes competitive maneuvering. Firms with established ISO 13485 systems and proven temperature-stable reagents win tenders that require stringent quality documentation. White-space opportunities persist in home testing and AI-enabled interpretation, though lengthy regulatory routes deter smaller players lacking capital reserves.

Dengue Testing Industry Leaders

Thermo Fisher Scientific Inc.

InBios International, Inc.

NovaTec Immundiagnostica GmbH

F. Hoffmann-La Roche Ltd.

Abbott

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Procurement and clinical practice are shifting toward standardized, stage-based testing pathways, creating openings for suppliers that align product claims and instructions with WHO laboratory-testing algorithms (updated interim guidance in April 2025) and arboviral clinical management guidance released in 2025. These documents increase demand for complete testing menus across acute and convalescent windows, supporting paired offerings such as NS1 antigen plus IgM/IgG serology and automated laboratory workflows that can handle outbreak-driven surges without extending turnaround time.

Emergency procurement mechanisms provide a practical route to scale in outbreak periods, with the WHO Dengue Expert Review Panel for Diagnostics (May 2025) acting as an evidence filter for non-prequalified IVDs considered in donor and public-sector purchases. In parallel, endemic-market tenders continue alongside climate-linked spread into temperate regions and travel-clinic screening, expanding the addressable testing footprint. This environment supports multiplex differentiation (dengue versus Zika and chikungunya), connectivity-enabled reporting, and higher-throughput immunoassay placements in laboratories that already run integrated analyzer platforms.

Recent Industry Developments

- February 2026: InBios updated regulatory-status and product specifications across its dengue diagnostics portfolio on its company product pages, reinforcing positioning of NS1 ELISA and rapid formats used by laboratories and frontline settings. This strengthens buyer clarity on intended use, as regulators and procurement agencies scrutinize labeling, performance claims, and cross-reactivity evidence.

- October 2025: Roche received a CE mark for the Elecsys Dengue Ag test, a fully automated immunoassay for NS1 antigen detection in human serum and plasma. The assay was validated for use on cobas e 801 and cobas e 402 platforms with an 18-minute turnaround time, supporting higher-throughput acute-phase dengue testing in routine clinical laboratories.

- May 2024: WHO supported procurement of diagnostic products and related laboratory items used for the diagnosis and management of diseases including dengue infections. This backing reinforced public-sector purchasing channels and helped anchor test availability during periods of heightened outbreak response needs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is counted as the value of dengue diagnostic testing products and testing services used to detect dengue infection, across routine clinical diagnosis and outbreak-driven testing. It covers testing done in labs and near-patient settings, where results are used for patient care or public health action.

Scope exclusions: We exclude dengue vaccines, vector control programs, and general fever workups that do not include a dengue-specific test.

Segmentation Overview

- By Diagnostic Technology (Value)

- NS1 Antigen Tests

- IgM/IgG Serology ELISA

- RT-PCR Molecular Tests

- Combination/Panel Assays

- Novel Biosensor-based Tests

- By End-User (Value)

- Hospitals & Clinics

- Diagnostic Laboratories

- Home Care / Self-Testing

- Others

- By Sample Type (Value)

- Serum / Plasma

- Whole Blood (Finger-stick / Venous)

- Saliva / Oral Fluid

- Others (Urine, Dried-Blood-Spot)

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Rest of APAC

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base demand context and the dengue testing pathway, so the market model stays tied to real testing volumes and practical use. We referred to public health reporting and surveillance updates such as those from the World Health Organization (WHO), the US CDC, and country health ministry dashboards where outbreak counts and testing advisories are published.

To translate demand signals into spending, we also reviewed regulatory and product information from the US FDA, peer-reviewed studies indexed in sources such as PubMed that discuss test performance and use patterns, and trade and customs statistics that indicate diagnostics imports and exports in high-burden countries. Company annual reports, investor presentations, and reputable press were used to check product mix shifts and geographic focus. A paid subscription database was used only for company financials and for patent landscaping to confirm technology direction. These sources are illustrative, and other public references were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on how dengue testing is actually ordered, which test types are selected by stage of illness, and how budgets move during outbreaks. We spoke with a mix of test manufacturers, distributors, diagnostic lab leaders, hospital procurement teams, and clinicians across APAC, EMEA, and the Americas, then used follow-up checks to close gaps on pricing ranges, utilization, and channel markups.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 37% |

| Mid tier: 47% | Functional/Unit leaders: 27% | EMEA: 37% |

| Smaller Players: 16% | Managers: 59% | Americas: 26% |

Market-Sizing & Forecasting

For sizing, we start with a top-down demand pool build where dengue incidence trends and suspected case loads are translated into likely testing volumes by care setting, then priced using a realistic mix of test types. Because ordering patterns change through the illness window, the model separates early triage use (for example, NS1 and rapid formats) from later confirmation use (for example, serology and RT-PCR), and totals are built up at region level before being rolled to the global number.

To keep the output practical, we corroborate totals using selective bottom-up approximations, such as sampled price points by channel, lab menu checks, and supplier shipment signals where visible in public disclosures. Inputs tracked as model variables include dengue case seasonality by region, test positivity and repeat testing practices during outbreaks, the share of testing done in centralized labs versus point of care, average selling price movement by technology, and changes in screening and surveillance intensity driven by public health advisories. Forecasts are built using scenario analysis supported by a simple multivariate regression overlay, with main drivers including disease burden indicators and testing access signals. The growth path is then adjusted based on what interviewees expect in procurement cycles and platform adoption. Where bottom-up evidence is patchy in smaller countries, we use proxy ratios from similar burden markets and then re-check the implied spend per suspected case for reasonableness.

Data Validation & Update Cycle

Validation is done in steps so that a single input does not over-push the final number. We compare outputs against independent signals such as outbreak alerts, diagnostic import movement where available, and the implied testing intensity per reported dengue burden, then review any unusual jumps again before sign-off.

If a gap is found, assumptions are revisited and, when needed, respondents are re-contacted to confirm whether it is a real market shift or a data timing issue. Reports are refreshed annually, with interim updates triggered by material events such as large outbreaks, major guideline changes, or pricing shocks, and a final analyst pass is completed right before delivery so clients receive the latest view.

Mordor Intelligence's Dengue Testing Market Sizing Compared With Other Published Estimates

Published sizes for dengue testing often do not line up, and the gaps usually come from differences in study definitions of what counts as dengue testing and what year is treated as the anchor. Differences also show up when one model relies more on shipment-style signals and another relies more on surveillance and testing behavior in care settings.

Some published figures include broader infectious disease panels, add adjacent fever testing, or assume a faster shift to higher-priced molecular formats across all regions. In the Mordor Intelligence build, only dengue-specific diagnostic technologies and related testing services are counted, and the mix is constrained using interview-validated shares for NS1, serology, and RT-PCR by region and by setting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 474.01 M (2026) | |

| Industry Publisher A | USD 612.53 M (2024) | Uses a different base year and often bundles centralized testing service spend and broader product formats under a single 2024 value, which can lift the total if outbreak year volumes are treated as normal demand. |

| Research House B | USD 775.80 M (2026) | Reported 2026 value is higher, which can happen when wider product buckets such as multiplex and confirmatory tests are included more aggressively and when higher molecular adoption is assumed across emerging markets without the same level of channel and utilization checks. |

Overall, the spread is mostly explained by timing and what is counted inside the testing basket, followed by how quickly pricing and technology mix are allowed to move. Our approach stays traceable to burden-led testing volumes and a realistic test mix, so buyers can reproduce the logic and challenge inputs without needing hidden data.

Key Questions Answered in the Report

How big is the dengue testing market in 2026?

The market stands at USD 474.01 million in 2026 and is projected to reach USD 579.72 million by 2031.

Which diagnostic technology leads current revenue?

NS1 antigen assays command 42.68% of 2025 revenue thanks to early detection advantages.

Which region grows fastest through 2031?

Asia-Pacific is forecast to expand at a 4.79% CAGR, driven by expanding surveillance and disease burden.

Why are multiplex panels gaining traction?

They simultaneously distinguish dengue from Zika and Chikungunya, meeting public-health mandates in co-endemic regions.

What factor most limits rapid test adoption?

Variable sensitivity and specificity across brands undermine clinician confidence, especially in lower-resource markets.

How does climate change affect testing demand?

Warming temperatures extend Aedes aegypti habitats into temperate zones, prompting new surveillance programs and sustained test volumes.

Page last updated on: