Influenza Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 1.92 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Influenza Diagnostics Market Analysis by Mordor Intelligence

The influenza diagnostics market size was valued at USD 1.82 billion in 2025 and estimated to grow from USD 1.92 billion in 2026 to reach USD 2.54 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). This healthy trajectory follows the market’s transition from pandemic-era volatility toward routine, technology-led respiratory disease management. Growth is anchored by wider adoption of molecular platforms that offer higher accuracy than legacy rapid antigen tests, steady government funding for surveillance infrastructure, and rising consumer demand for at-home and point-of-care (POC) solutions. Vendors are consolidating to combine molecular accuracy with near-patient speed, while AI-enabled software is shortening laboratory turnaround times and improving quality control. Regional dynamics further shape demand: North America leads on installed base and reimbursement clarity, whereas Asia Pacific records the fastest uptake thanks to ongoing investment in public-health laboratories.

Key Report Takeaways

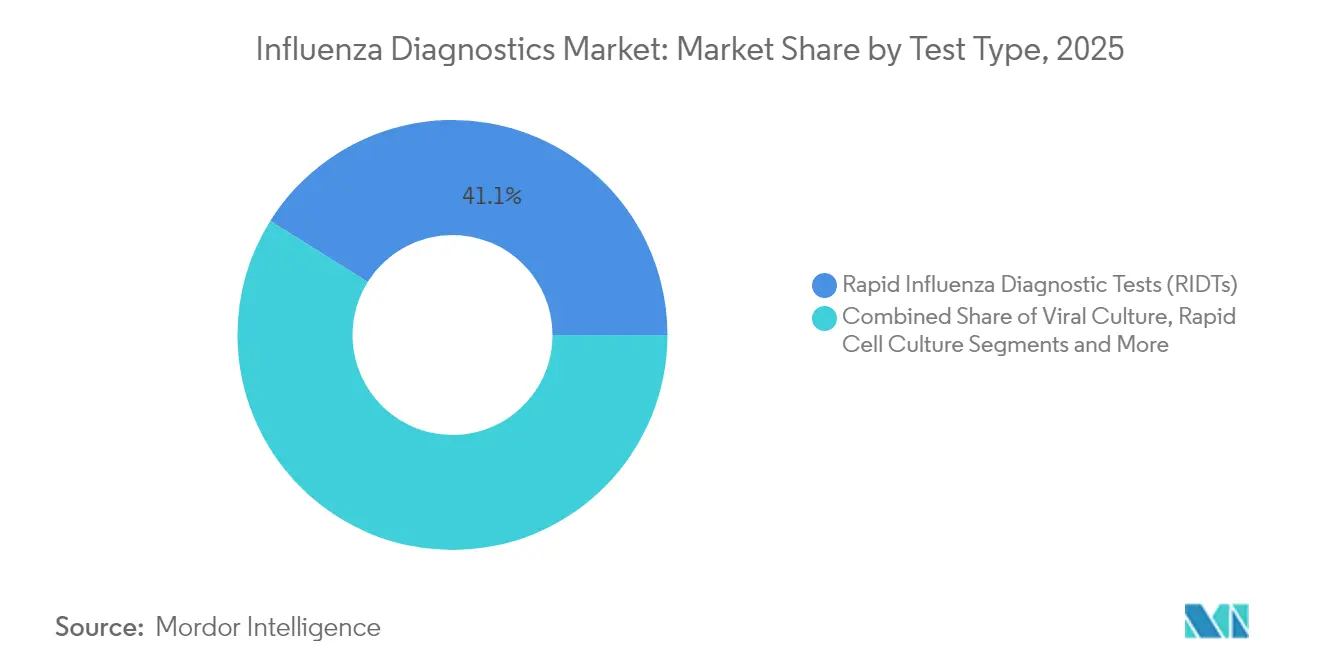

- By test type, rapid influenza diagnostic tests captured 41.10% of the influenza diagnostics market share in 2025, whereas CRISPR-based assays are projected to expand at a 9.28% CAGR through 2031.

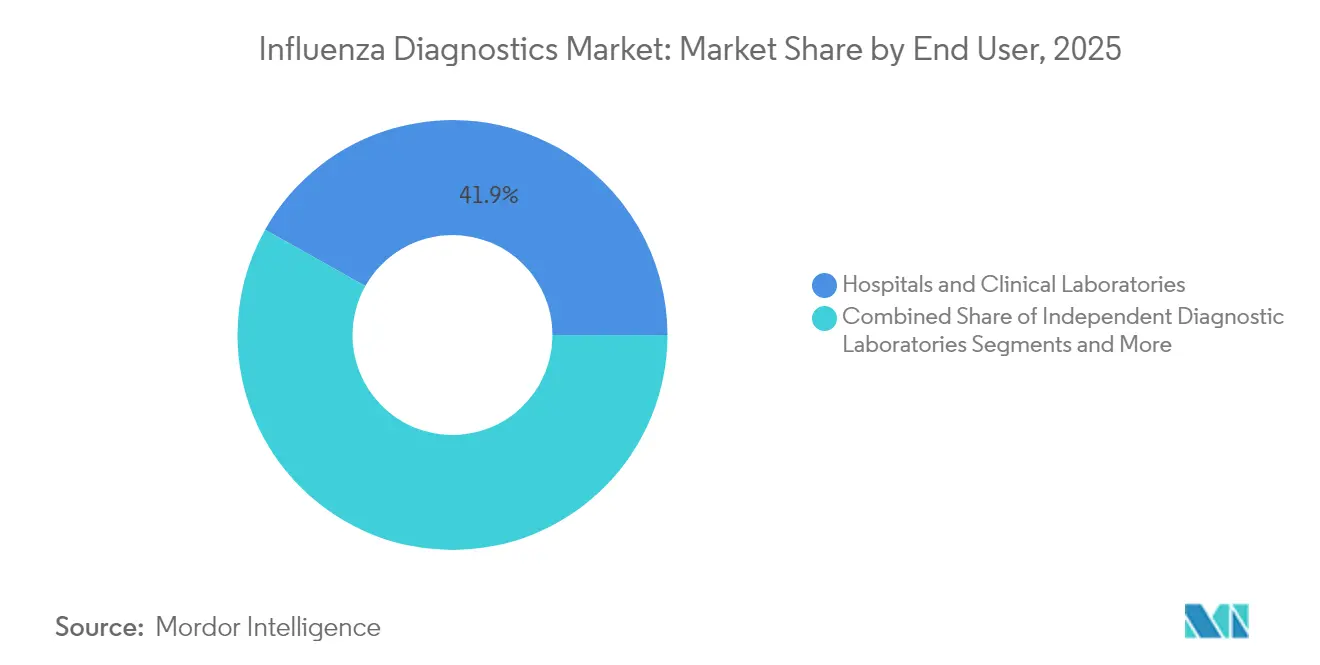

- By end user, hospitals and clinical laboratories held 41.85% of the market in 2025; point-of-care settings record the highest forecast CAGR at 9.12% to 2031.

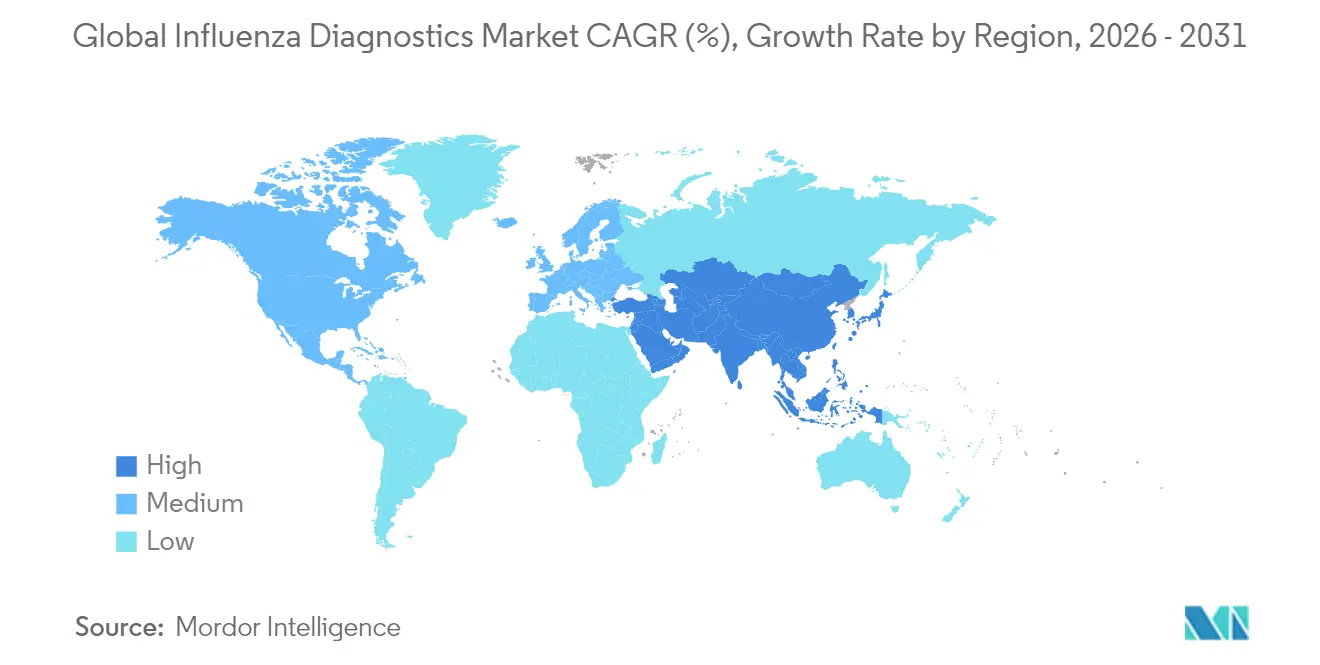

- By geography, North America commanded 37.25% revenue share in 2025; Asia Pacific is anticipated to grow at an 7.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Influenza Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence & Severity Of Seasonal And Zoonotic Influenza Outbreaks | +1.20% | Global, with heightened impact in Asia Pacific and North America | Medium term (2-4 years) |

| Growing Adoption Of Rapid Point-Of-Care (POC) Tests In Outpatient Settings | +0.90% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Government-Funded Surveillance Programs & Pandemic Preparedness Budgets | +0.80% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| AI-Powered Result-Interpretation Software Boosting Molecular Workflow Throughput | +0.70% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Commercialization Of Combo SARS-CoV-2/Flu Multiplex Panels Expanding Installed Base | +0.60% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Increasing Integration Of Telehealth With Home-Based Flu Testing Kits | +0.50% | North America & EU, gradual APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence & Severity of Seasonal and Zoonotic Influenza Outbreaks

A resurgence in seasonal influenza activity has intensified global diagnostic demand, with the CDC logging 39,053 laboratory-confirmed hospitalizations during the 2024-2025 season, the highest rate since 2010-2011.[1]Centers for Disease Control and Prevention, “Weekly Flu Season Update,” cdc.govConcurrently, highly pathogenic H5N1 outbreaks generated 38 human cases in California among dairy workers, prompting expanded livestock surveillance. New kits, such as Singapore’s Steadfast assay, differentiate highly and low pathogenic strains within three hours, enhancing outbreak response. These events push health systems to retain emergency-level testing capacity year-round, sustaining procurement of high-accuracy molecular platforms.

Growing Adoption of Rapid Point-of-Care Tests in Outpatient Settings

Hospital studies from the University of Southampton showed that POC influenza testing cuts result time to under one hour, enabling faster antiviral initiation and shorter patient stays. Platforms now include molecular options like Abbott’s ID NOW, which returns influenza A/B results in 13 minutes with 96.3% sensitivity. AI-enhanced readers further reduce interpretation time to two minutes.[2]Baozhang Li, “TIMESAVER: Rapid Deep-Learning Interpretation of Lateral-Flow Assays,” Nature Communications, nature.com Lower transport costs and same-visit treatment support economic arguments for widespread POC deployment in clinics and retail health sites.

Government-Funded Surveillance Programs & Pandemic-Preparedness Budgets

Post-COVID lessons spurred higher allocations, with the U.S. Department of Health and Human Services earmarking USD 172 million for influenza preparedness in FY 2025. The CDC now partners with commercial labs such as Quest Diagnostics and Labcorp to expand avian influenza testing capacity. Meanwhile, WHO achieved full national influenza center coverage across 11 South-East Asian countries in 2024, a milestone that elevates baseline demand for standardized diagnostic kits. These programs stabilize procurement cycles and set performance benchmarks that steer private-sector R&D.

AI-Powered Result-Interpretation Software Boosting Molecular Workflow Throughput

Machine-learning pipelines now classify viral sequences and flag mutations faster than manual processes, increasing laboratory throughput without new hardware.[3]Hannah R. Meredith, “Machine-Learning Pipeline Accelerates Virus Detection and SNP Discovery,” PubMed Central, ncbi.nlm.nih.govBugSeq’s collaboration with BARDA brings AI-driven reporting to clinical metagenomics, underpinning pathogen-agnostic surveillance. TIMESAVER, a deep-learning algorithm, lifted the sensitivity of lateral-flow assays for influenza A/B to 93.8% while slashing read time to two minutes. Laboratories deploying such tools improve quality-control consistency and can flex capacity during seasonal peaks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variable Sensitivity & False-Negative Rate Of RIDTs | -0.80% | Global, particularly impacting resource-limited settings | Short term (≤ 2 years) |

| High Capital & Running Cost Of Molecular Diagnostic Platforms | -0.60% | APAC and emerging markets, moderate impact in developed regions | Medium term (2-4 years) |

| Regulatory Uncertainty For CRISPR-Based Influenza Assays | -0.40% | Global, with varying regional approval timelines | Long term (≥ 4 years) |

| Supply Chain Disruptions Affecting Critical Reagents For PCR Assays | -0.50% | Global, with heightened impact during geopolitical tensions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Variable Sensitivity & False-Negative Rate of RIDTs

Many RIDTs miss early infections when viral load is low; studies place false-negative rates above 30% for certain commercial kits. The Panbio COVID-19/Flu A&B panel delivered only 80.8% sensitivity for influenza. WHO’s 2024 guidance now recommends nucleic-acid tests for severe or high-risk cases. Clinics have introduced confirmatory PCR workflows that erase the speed advantage of RIDTs, curbing segment expansion.

High Capital & Running Cost of Molecular Diagnostic Platforms

Comprehensive systems like Roche’s Cobas 6800 require significant capital plus service contracts beyond many mid-size hospitals’ budgets. Reagents, maintenance, and skilled labor keep operating expenses elevated; supply-chain shocks further lift logistics outlays, which reached nearly 20% of revenue for device makers in 2024. In lower-income markets, limited reimbursement for syndromic panels slows adoption despite clinical advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: CRISPR Innovation Challenges Traditional Dominance

Rapid formats remained dominant with a 41.10% revenue share, yet the influenza diagnostics market is repositioning as clinicians prioritize sensitivity and multiplexing. CRISPR assays show 9.28% CAGR by 2031, led by the Broad Institute’s SHINE test that discriminates subtypes in 15 minutes. Molecular panels that bundle influenza A/B, RSV, and SARS-CoV-2 deliver operational efficiency for emergency departments. The influenza diagnostics market size for CRISPR platforms is forecast to expand fastest among all modalities, driven by simplified workflows and shrinking instrument footprints. Direct fluorescent antibody and viral culture testing continue to serve research niches where strain typing or antiviral susceptibility is required, but they no longer influence mainstream purchasing decisions.

Molecular diagnostics, including RT-PCR and isothermal formats, see accelerated uptake as AI tools streamline result interpretation. Multiplex CRISPR-Cas13a strips achieved 100% concordance with RT-qPCR while removing amplification steps. Hospitals prefer syndromic panels that differentiate overlapping respiratory symptoms within a single sample, whereas retail clinics adopt CLIA-waived molecular cartridges for rapid walk-in encounters. This convergence of accuracy and speed positions molecular solutions to erode RIDT leadership as capital barriers abate.

By End User: Hospital Consolidation Versus POC Expansion

Hospitals and clinical laboratories generated 41.85% of 2025 revenue by leveraging high-throughput instruments and in-house microbiology expertise. Consolidation among health systems concentrates purchasing power, allowing bulk reagent contracts that stabilize supply. Point-of-care venues, however, exhibit the highest 9.12% CAGR as physicians require immediate answers for treatment during a single visit. The influenza diagnostics market share held by pharmacies and urgent-care centers continues to climb as retailers like CVS deploy 3-in-1 combo tests across 1,600 sites.

Independent diagnostic laboratories maintain relevance by servicing outpatient clinics and specialist practices, but face referral declines where hospitals move tests in-house. Home testing forms an emerging sub-segment after the FDA cleared the first OTC combo flu/COVID assay in 2024. Across all settings, the influenza diagnostics industry leverages telehealth connections to relay results directly into electronic health records, supporting antiviral e-prescriptions without extra clinic visits. Source: https://www.mordorintelligence.com/industry-reports/global-influenza-diagnostics-market

Geography Analysis

North America’s leadership stems from comprehensive surveillance systems and mature reimbursement models. The CDC coordinates eight regional surveillance hubs spanning 125 countries, yet maintains its largest testing footprint domestically. The influenza diagnostics market size in North America benefits from Thermo Fisher Scientific’s USD 2 billion investment to expand domestic manufacturing, aimed at insulating supply chains. Retail pharmacies integrate CLIA-waived molecular cartridges for same-visit care, while health insurers increasingly reimburse home-collection kits, broadening consumer access.

Asia Pacific posts the fastest 7.78% CAGR owing to rapid laboratory build-outs and government funding. WHO’s milestone of 11 fully operational national influenza centers across South-East Asia evidences this progress. Japan updated quality-management regulations to align with ISO 13485:2016, smoothing approval pathways for foreign assay developers. China and India funnel vaccine-related mRNA investments into diagnostics, fostering locally made CRISPR cartridges for regional distribution.

Europe remains influential through the In Vitro Diagnostic Regulation (IVDR), which raises conformity-assessment requirements from 15% to nearly 90% of assays. Transition extensions granted in 2024 prevent immediate supply shortages but raise compliance costs that could shift R&D to fewer, higher-value tests. Middle East & Africa and South America pursue capacity growth via multilateral aid and public-private partnerships; the OECD urges diversified sourcing to mitigate logistic shocks experienced during the pandemic. This uneven readiness shapes divergent adoption curves, yet shared emphasis on respiratory surveillance sustains global demand for robust assays. Source: https://www.mordorintelligence.com/industry-reports/global-influenza-diagnostics-market

Competitive Landscape

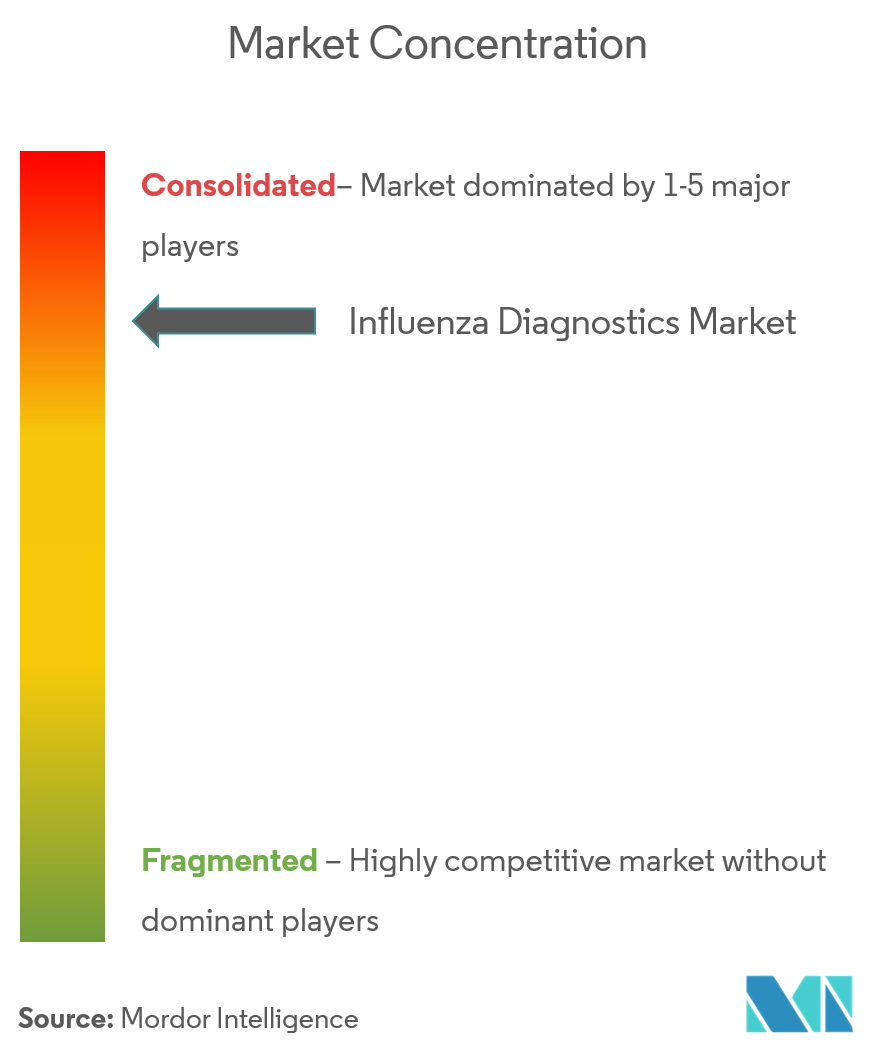

The influenza diagnostics market shows moderate consolidation: the top five firms account for nearly 60% of global revenue, yet nimble innovators still capture white-space niches. Roche’s USD 295 million purchase of LumiraDx’s POC technology underscores strategic moves to unite molecular accuracy with handheld convenience. bioMérieux’s EUR 111 million acquisition of SpinChip brings 10-minute whole-blood immunoassays into its stable. Abbott and QuidelOrtho continue to iterate CLIA-waived combo tests covering influenza A/B, RSV, and SARS-CoV-2 for retail settings where throughput and simplicity supersede broader panels.

Emergent competitors differentiate on CRISPR or AI capabilities. The Broad Institute’s paper-strip SHINE assay promises molecular-grade sensitivity in 15 minutes without instrumentation. BugSeq integrates AI reporting with nanopore sequencing for pathogen-agnostic detection. Supply-chain resilience now factors into competitive advantage; Thermo Fisher’s four-year plan earmarks USD 1.5 billion to boost domestic production, responding to PCR reagent shortages experienced in 2024. As reimbursement shifts toward bundled respiratory panels, platform versatility and cost-per-reportable outcome will dictate future market share allocations. Source: https://www.mordorintelligence.com/industry-reports/global-influenza-diagnostics-market

Influenza Diagnostics Industry Leaders

Becton, Dickinson and Company

F. Hoffmann-La Roche Ltd

Thermo Fisher Scientific

Abbott Laboratories

QuidelOrtho Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thermo Fisher Scientific announced plans to divest parts of its diagnostics business for approximately USD 4 billion, including its microbiology division that generates USD 1.4 billion in annual sales

- June 2025: Illumina agreed to acquire SomaLogic for USD 350 million to fast-track multiomics biomarker discovery.

- April 2025: HealthTrackRx and the CDC unveiled a rapid H5N1 PCR test to strengthen outbreak readiness.

- April 2025: Thermo Fisher Scientific committed USD 2 billion for U.S. manufacturing and R&D expansion over four years.

- February 2025: Bio-Rad Laboratories offered to acquire Stilla Technologies to bolster digital PCR offerings.

Global Influenza Diagnostics Market Report Scope

Influenza, also known as flu, is a highly contagious infectious disease caused by a virus. This is an infection of the respiratory passages, which causes fever and severe aches. The influenza diagnostic market includes the tests that are conducted for the diagnosis of influenza cases. As per the scope of this report, only the test kits and reagents used for the diagnosis of influenza have been considered for calculating the total market size. The Influenza Diagnostics Market is segmented by Test Type (Traditional Diagnostic Test and Molecular Diagnostic Assay), End User (Hospital, Laboratories, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across significant regions globally. The report offers the value (USD million) for the above segments.

| Traditional Diagnostic Tests | Rapid Influenza Diagnostic Tests (RIDTs) |

| Direct Fluorescent Antibody (DFA) Tests | |

| Viral Culture | |

| Rapid Cell Culture | |

| Molecular Diagnostic Tests | Reverse-Transcriptase PCR (RT-PCR) |

| Loop-Mediated Isothermal Amplification (LAMP) | |

| Nicking-Enzyme Amplification Reaction (NEAR) | |

| CRISPR-based Assays | |

| Syndromic Multiplex PCR Panels |

| Hospitals & Clinical Laboratories |

| Independent Diagnostic Laboratories |

| Point-of-Care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Traditional Diagnostic Tests | Rapid Influenza Diagnostic Tests (RIDTs) |

| Direct Fluorescent Antibody (DFA) Tests | ||

| Viral Culture | ||

| Rapid Cell Culture | ||

| Molecular Diagnostic Tests | Reverse-Transcriptase PCR (RT-PCR) | |

| Loop-Mediated Isothermal Amplification (LAMP) | ||

| Nicking-Enzyme Amplification Reaction (NEAR) | ||

| CRISPR-based Assays | ||

| Syndromic Multiplex PCR Panels | ||

| By End User | Hospitals & Clinical Laboratories | |

| Independent Diagnostic Laboratories | ||

| Point-of-Care Settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the influenza diagnostics market?

The influenza diagnostics market size reached USD 1.92 billion in 2026.

How fast is the influenza diagnostics market projected to grow?

It is forecast to expand at a 5.72% CAGR from 2026 to 2031.

Which region holds the largest share of global influenza testing revenue?

North America led with 37.25% market share in 2025.

Why are CRISPR-based assays gaining traction in influenza testing?

CRISPR platforms combine molecular-level accuracy with rapid, equipment-light workflows that match point-of-care needs.

What restrains broader molecular platform adoption in emerging markets?

High equipment costs, ongoing reagent expenses, and specialized staffing requirements limit uptake outside well-funded health systems.

How are AI tools transforming influenza diagnostics?

AI pipelines accelerate result interpretation, increase sensitivity, and automate quality checks, boosting laboratory throughput during seasonal peaks.

Page last updated on: