Tubeless Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

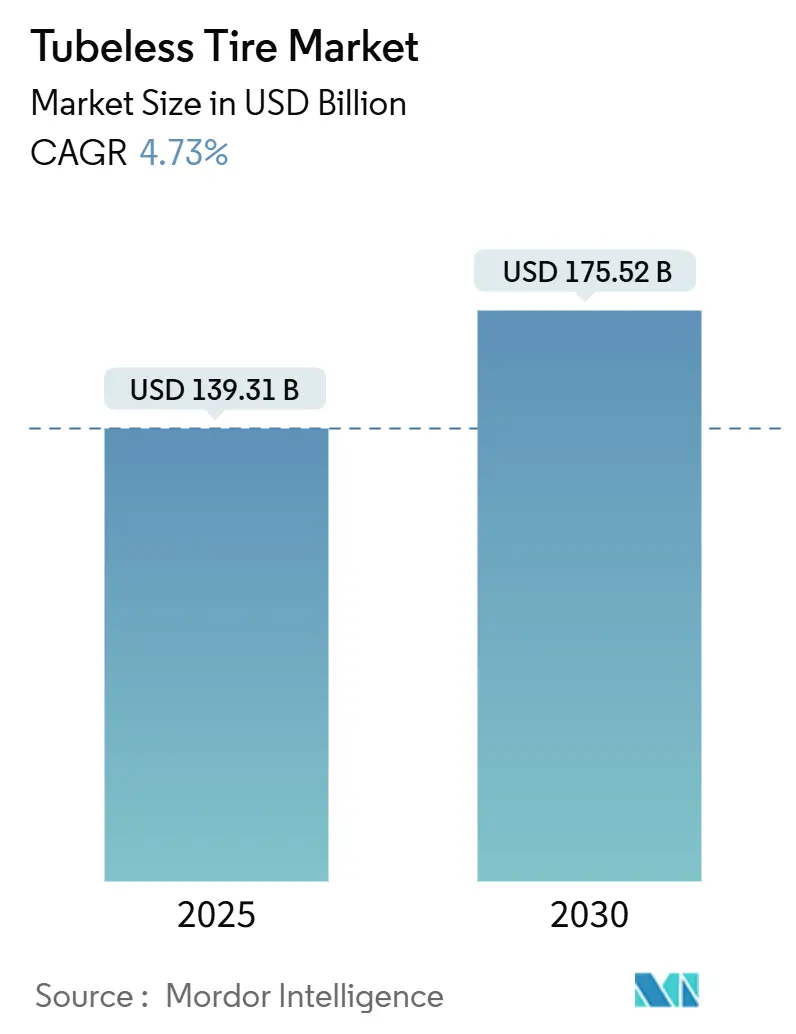

| Market Size (2025) | USD 139.31 Billion |

| Market Size (2030) | USD 175.52 Billion |

| Growth Rate (2025 - 2030) | 4.73% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

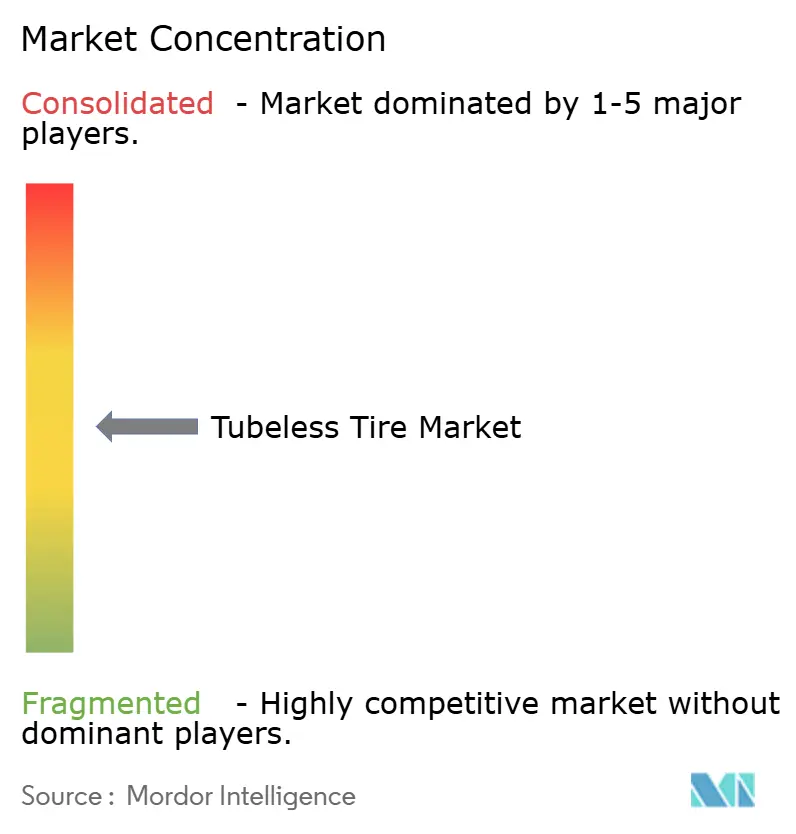

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tubeless Tire Market Analysis by Mordor Intelligence

The Tubeless Tire Market size is estimated at USD 139.31 billion in 2025, and is expected to reach USD 175.52 billion by 2030, at a CAGR of 4.73% during the forecast period (2025-2030). Supported by rapid EV penetration, stricter tire-safety regulations, and large-scale OEM adoption. Strong aftermarket replacement demand, technology investments in self-sealing compounds, and persistent raw-material cost swings shape the competitive landscape. At the same time, Asia-Pacific’s production scale and South America’s growth momentum set the regional cadence. OEM fitment preferences, TPMS mandates, and evolving ride-hailing logistics reinforce structural demand shifts toward premium radial constructions that cut downtime and improve fuel efficiency. Advanced silica, nano-compounds, and air-loss mitigation technologies offer incremental performance gains, and integrated tire-monitoring systems provide data-driven maintenance advantages for fleets.

Key Report Takeaways

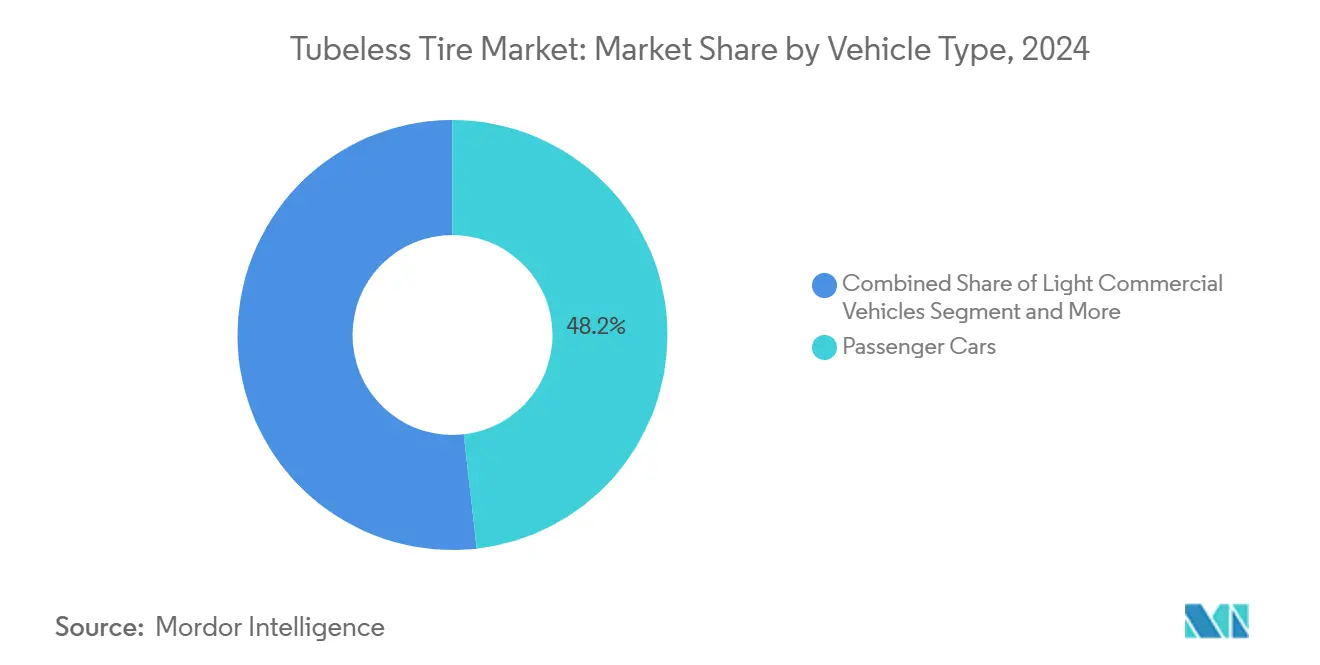

- By vehicle type, passenger cars led with a 48.17% share of the tubeless tire market in 2024, while light commercial vehicles are expected to grow at a CAGR of 4.75% during the forecast period (2025-2030).

- By design, radial tires commanded 87.31% share of the tubeless tire market in 2024 and are expected to grow at a 4.77% CAGR during the forecast period (2025-2030).

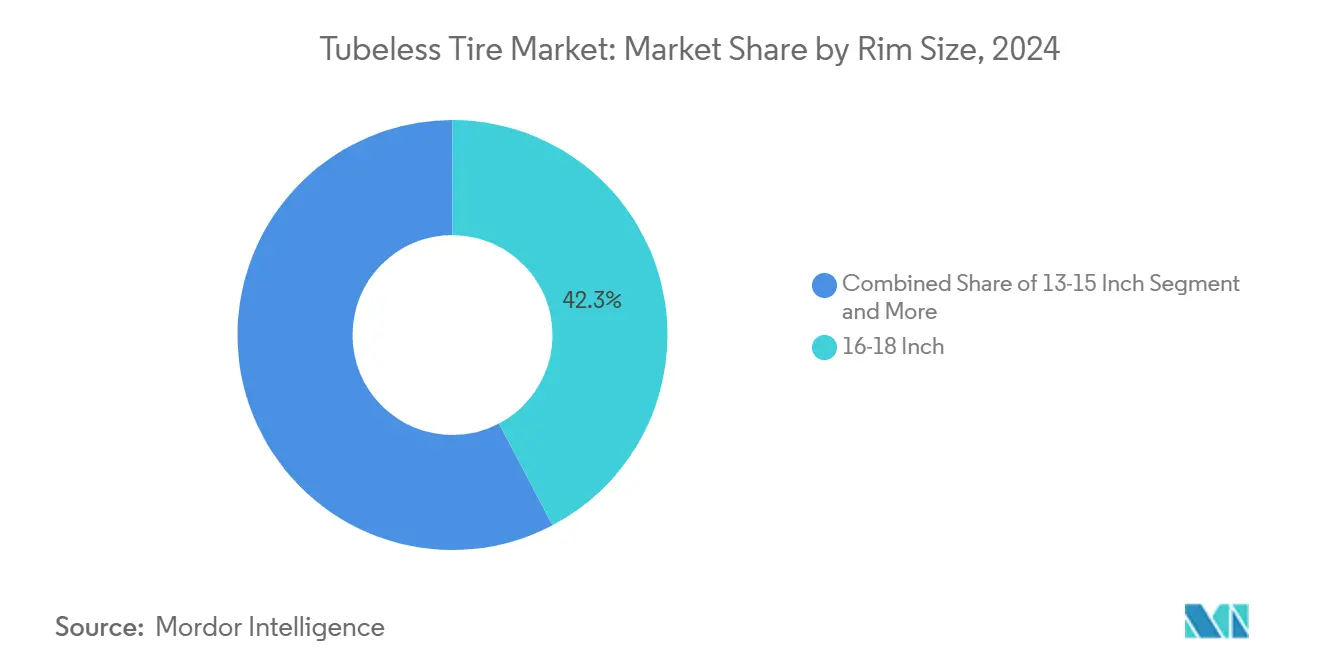

- By rim size, 16-18-inch models captured 42.27% share in 2024; rims above 21 inches are forecast to expand at a 4.84% CAGR during the forecast period (2025-2030).

- By sales channel, the aftermarket held 67.73% of the tubeless tire market share in 2024, while the OEM channel shows the fastest growth at 4.78% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific accounted for 39.81% share of the tubeless tire market in 2024; South America is positioned to post the strongest 4.81% CAGR during the forecast period (2025-2030).

Global Tubeless Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory TPMS and Tire-Safety Regulations | +1.2% | North America and EU core, expanding to Asia Pacific | Short term (≤ 2 years) |

| Surge In Electric-Vehicle (EV) Sales | +1.0% | Global, led by China, EU, and California | Medium term (2-4 years) |

| Growing Preference For Low-Maintenance Tires | +0.8% | Global, with strong adoption in North America and Europe | Medium term (2-4 years) |

| Expansion Of Ride-Hailing And Last-Mile Fleets | +0.6% | Urban centers globally, concentrated in Asia Pacific and North America | Long term (≥ 4 years) |

| Advanced Silica & Nano-Compound Adoption | +0.4% | Premium segments globally | Long term (≥ 4 years) |

| Emerging Air-Loss Self-Sealing Technologies | +0.3% | Premium markets in developed economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory TPMS & Tire-Safety Regulations

The U.S. Federal Motor Vehicle Safety Standard 138 mandates tire-pressure monitoring on all light vehicles, cutting instances of severe underinflation by more than half and aligning with European TPMS mandates that link compliance to stricter labelling on rolling resistance and wet-grip performance [1]“FMVSS 138 Regulatory Impact Analysis,” National Highway Traffic Safety Administration, nhtsa.gov. Tubeless architectures naturally retain pressure more consistently than tube-type alternatives, enabling easier regulatory compliance and improving CO2 emissions through lower rolling resistance. As regulators in Japan, India, and ASEAN harmonise with UNECE standards, OEMs globally specify tubeless radials to meet safety and sustainability criteria without costly redesigns.

Surge In Electric-Vehicle (EV) Sales

EV drivetrain torque and battery weight demand tires with higher load indices and optimized rolling resistance. Pirelli’s ELECT line delivers one-fifths rolling-resistance reduction and a 10% range boost, illustrating how radial tubeless construction satisfies EV range and NVH requirements. Michelin now supplies one-third of OE tires for U.S. EVs, demonstrating OEM reliance on specialized tubeless platforms. As EV adoption accelerates in China and Europe, tubeless tire market demand scales through OEM channels and premium aftermarket segments alike.

Growing Preference For Low-Maintenance Tires

Fleet operators adopt tubeless designs to cut roadside interventions and reduce cost per mile, lowering emergency service calls by up to one-third when real-time tire monitoring platforms such as Goodyear Fleet Central are deployed [2]“Fleet Central Predictive Maintenance Case Study,” Goodyear, goodyear.com . Simplified puncture repair and the absence of tubes minimise downtime, which is critical for ride-hailing and logistics fleets facing labour shortages and rising wage costs. Integration with route-optimisation software multiplies efficiency gains that tube-type tyres cannot replicate. As mileage rates and urban traffic density increase, the operational ROI of tubeless solutions strengthens, translating into higher penetration in medium and light commercial segments across North America and Western Europe.

Expansion Of Ride-Hailing And Last-Mile Fleets

Urban commercial fleets switching to tubeless tires report one-fourth fewer service interruptions, strengthening the business case for mass migration away from tubes. Revel and Uber’s EV charging collaboration underscores the intertwining of electrification and tubeless tire uptake. High trip densities in ride-hailing and delivery fleets amplify the durability advantages of radial tubeless designs, especially where potholes and debris elevate puncture risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Upfront Cost | -0.9% | Price-sensitive markets in developing economies | Short term (≤ 2 years) |

| Counterfeit & Gray-Market Tire Proliferation | -0.7% | Southeast Asia, Africa, Latin America | Medium term (2-4 years) |

| Raw-Material Price Volatility | -0.6% | Global, with acute impact on cost-sensitive segments | Short term (≤ 2 years) |

| Limited Fitment In Off-Highway Legacy Fleets | -0.2% | Agricultural and construction sectors globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost Vs Tube-Type Tires

Self-sealing tubeless models cost slightly more than tube-type alternatives, constraining adoption in price-sensitive markets despite lower lifetime operating costs. Manufacturing complexity tied to advanced innerliner compounds raises capex needs, making scale critical to lowering unit costs. Rural buyers in India and Africa still favor tube-type tires when up-front affordability trumps total cost considerations, keeping localized tube-type production viable in certain niches.

Counterfeit & Grey-Market Tire Proliferation

Counterfeit automotive parts cause highly in annual losses, with more than four-fifths of bogus items sourced from China, according to the EU Intellectual Property Office. Vietnam seized multiple fake automotive parts in 2024, many unsafe tire units that erode consumer trust in legitimate tubeless offerings. Online marketplaces mask seller identities, flooding developing markets with substandard products and depressing prices, undermining brand equity for premium tire makers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Adoption

Passenger cars maintained the largest share of the tubeless tire market at 48.17% in 2024, but their growth plateaued in mature economies where replacement cycles lengthened. Light commercial vehicles are expected to be the fastest-growing segment at 4.75% CAGR during the forecast period (2025-2030), reflecting e-commerce-driven mileage spikes and the operational advantages of radial tubeless tires in reducing downtime.

Fleet digitization intensifies demand for integrated TPMS solutions, and OEMs respond by factory-fitting tubeless radials to new van and pickup models. Cost-of-service economics favor tubeless platforms in ride-hailing and delivery use cases, prompting regional policy incentives for low-maintenance commercial fleets. Passenger car retrofits remain robust, especially for rim upgrades from 16 inch to 18 inch, sustaining aftermarket sales as vehicle parc ages.

By Design: Radial Dominance Accelerates

Radial construction secured 87.31% of the tubeless tire market share in 2024 and is expected to expand at a 4.77% CAGR during the forecast period (2025-2030), as OEMs phase out bias ply in favor of superior heat dissipation and fuel efficiency. Bias ply retains niche relevance in mining and forestry vehicles where sidewall flexibility and puncture resistance outweigh speed requirements.

Advanced belt-angle optimization and aramid reinforcement bolster radial carcass strength, enabling higher load indices crucial for electric SUVs and pickups. Material innovations such as renewable lignin-based fillers trim carbon footprints, aligning with ESG mandates and enhancing life-cycle assessments. Bias-radial market transition timelines shorten as emerging economies leapfrog legacy technologies, mirroring smartphone adoption curves.

By Rim Size: Premium Segments Lead Growth

In 2024, 16-18 inch models dominate the tubeless tire market with a 42.27% share. Meanwhile, rims exceeding 21 inches are projected to expand at a 4.84% CAGR during the forecast period, driven by luxury automakers' emphasis on aesthetics and cornering stability. The 19-21 inch segment serves as a bridge between mainstream and performance categories, reaping benefits from mid-cycle refreshes in crossover vehicles.

Manufacturers employ aerodynamic simulations and lightweight cord-compound integrations to optimize EV range, mitigating counter-rotating mass penalties in large-diameter wheels. Premium pricing on 22- to 24-inch tires bolsters manufacturers' gross margins, helping them navigate commodity rubber price fluctuations. As demand concentrates in high-value regions like the U.S., China, and the luxury markets of the Middle East, dedicated production lines for large rims are scaling up to meet this demand.

By Sales Channel: OEM Growth Outpaces Aftermarket

In 2024, the Aftermarket segment dominates the Tubeless Tire Market, holding a 67.73% share. Meanwhile, the OEM segment is poised for a growth spurt, projected to expand at a 4.78% CAGR during the forecast period. This uptick underscores a notable trend: automakers are increasingly opting for factory-fitted tubeless solutions. These come bundled with vehicle-integrated TPMS. As electrification gains momentum, it's not just the evolving vehicles. There's a pronounced collaboration between OEMs and tire manufacturers. A case in point: TDK's smart-sensor suites are now seamlessly embedded into original equipment (OE) radials. These advanced sensors directly relay critical temperature, load, and wear data to the vehicle's Advanced Driver Assistance Systems (ADAS).

Intensified brand-to-consumer engagement through dealership networks narrows the information advantage that independent retail once held. Digital service ecosystems provide predictive tire-replacement alerts, linking customers to OEM channels for authentic replacements and reinforcing brand loyalty. The aftermarket counters through tier-three low-cost imports but faces regulatory scrutiny and counterfeiting crackdowns.

Geography Analysis

In 2024, Asia-Pacific commanded a dominant 39.81% share of the tubeless tire market, driven by China's robust vehicle output and India's production-linked incentives for auto suppliers, establishing a strong domestic foundation for the market's expansion[3]“Automotive Production 2024,” China Ministry of Industry and Information Technology, miit.gov.cn. Regional export capacity is buoyed by RCEP tariff advantages, and multinationals such as Goodyear invest a huge amount in Kunshan expansions to meet global demand.

South America is set to lead the momentum, with projections indicating a 4.81% CAGR growth rate through 2030. This surge is attributed to a rebound in Brazil's production and a USD 6 billion commitment from Stellantis, bolstering OEM output. The rising popularity of pickups and SUVs drives demand for larger rim sizes and higher-margin tubeless radials. Concurrently, increased infrastructure spending is spurring upgrades in commercial fleets. Moreover, import substitution policies in Argentina and Colombia provide added incentives for domestic tire investments.

North America and Europe remain mature, growth‐limited regions where regulations, not volume, drive innovation. The Middle East and Africa show selective gains in urban corridors such as Riyadh and Lagos. At the same time, rural segments continue to favour tube-type bias ply due to service infrastructure constraints.

Competitive Landscape

Global leadership rests with Bridgestone, Michelin, Goodyear, Continental, and Hankook, holding a significant share of the market, indicating moderate industry concentration. These firms leverage proprietary compound chemistries, vertical integration of synthetic rubber, and global distribution to sustain scale advantages. Total disclosed capex in 2024 underlines aggressive expansion agendas oriented toward premium EV-specific tire lines, smart-sensor integration, and sustainable material R&D [4]“Sustainability Report 2025,” Bridgestone Corporation, bridgestone.com .

Strategic alliances reshape competition: TDK-Goodyear’s SightLine sensor integration embeds tire data into ADAS architectures; Bridgestone-Versalis closed-loop recycling targets circularity; Sumitomo-Mitsubishi Chemical’s carbon-black recycle addresses Scope three emissions. Tier-two players such as Sailun and Yokohama differentiate on regional price leadership and niche motorsport sponsorships. At the same time, Chinese entrants exploit domestic subsidies to undercut global pricing—heightening anti-dumping scrutiny in the EU and U.S.

Counterfeit and grey-market influx dilutes price discipline, prompting brand protection investments, serial-number RFID tagging, and customs liaisons. Raw-material volatility amplifies cost pressures, advantaging integrated producers with diversified feedstock. The competitive narrative increasingly pivots on ESG credentials and digital service ecosystems rather than tread pattern alone, demanding continuous innovation to defend share.

Tubeless Tire Industry Leaders

Bridgestone Corporation

Goodyear Tire & Rubber Company

Continental AG

Pirelli & C. S.p.A

Yokohama Rubber Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Continental introduced the Grand Prix TR, a road tire that combines affordability with tubeless-ready capabilities. Targeted at cyclists seeking a reliable tire for training, commuting, and extended rides, the Grand Prix TR finds its place in Continental's endurance segment.

- June 2024: JK Tyre & Industries unveiled a new range of tyres for the transportation sector, including four Truck and bus Radial variants: JETWAY JUM XM, JETWAY JUC XM, JETSTEEL JDC XD, and JETWAY JUXe for electric buses. The JETWAY JUM XM, a next-generation tubeless tire with a 4-Star Rating and an RRc value of 4.9 KN/n, is the most energy-efficient, offering improved fuel economy and cost optimization.

Global Tubeless Tire Market Report Scope

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Medium Commercial Vehicles (MCV) |

| Heavy Commercial Vehicles (HCV) |

| Radial |

| Bias |

| 13-15 Inch |

| 16-18 Inch |

| 19-21 Inch |

| Above 21 Inch |

| OEMs |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Medium Commercial Vehicles (MCV) | ||

| Heavy Commercial Vehicles (HCV) | ||

| By Design | Radial | |

| Bias | ||

| By Rim Size | 13-15 Inch | |

| 16-18 Inch | ||

| 19-21 Inch | ||

| Above 21 Inch | ||

| By Sales Channel | OEMs | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the tubeless tire market?

The tubeless tire market size stands at USD 139.31 billion in 2025.

How fast is global revenue expected to grow?

Revenue is projected to rise at a 4.73% CAGR, reaching USD 175.52 billion by 2030.

Which region commands the highest share?

Asia-Pacific controls 39.81% of worldwide sales, driven by large-scale vehicle production.

Which rim size bracket is expanding the quickest?

Rim diameters above 21 inch show the fastest 4.84% CAGR through 2030 due to premium vehicle demand.

Why are OEM channels gaining momentum?

Automakers integrate TPMS and EV-optimized radials at the factory, pushing OEM shipments to a 4.78% CAGR.

What is a key threat to legitimate tire brands?

Counterfeit and gray-market tires erode pricing power and raise safety risks, especially in Southeast Asia.

Page last updated on: