Winter Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

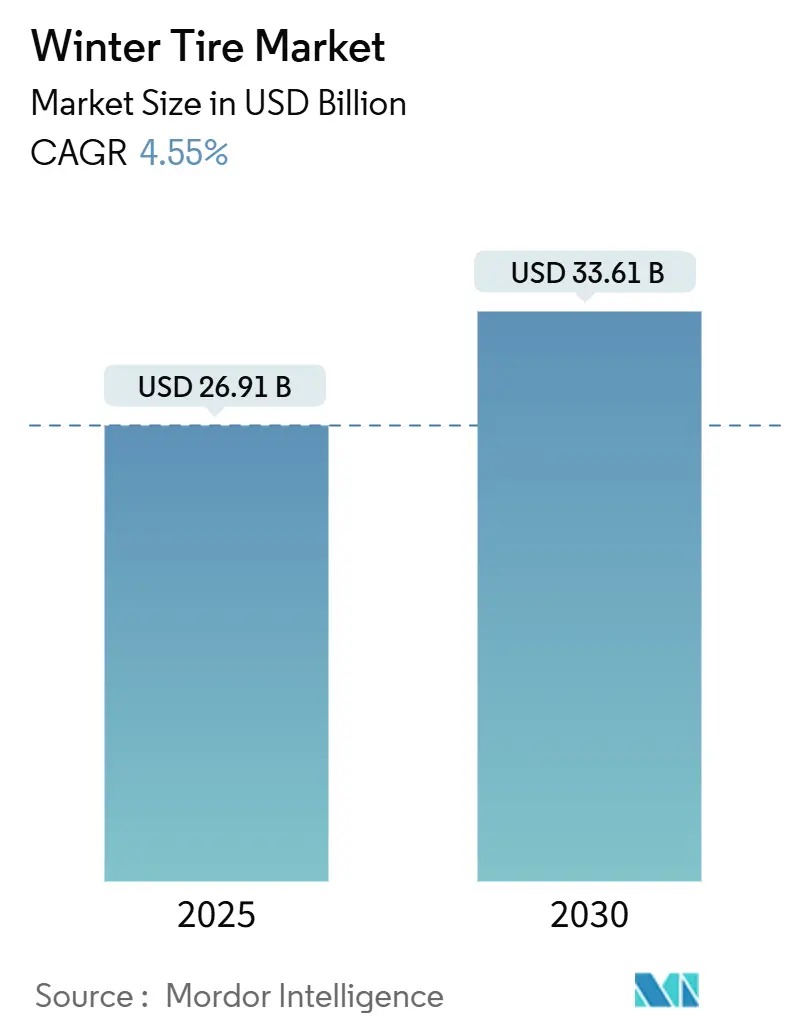

| Market Size (2025) | USD 26.91 Billion |

| Market Size (2030) | USD 33.61 Billion |

| Growth Rate (2025 - 2030) | 4.55% CAGR |

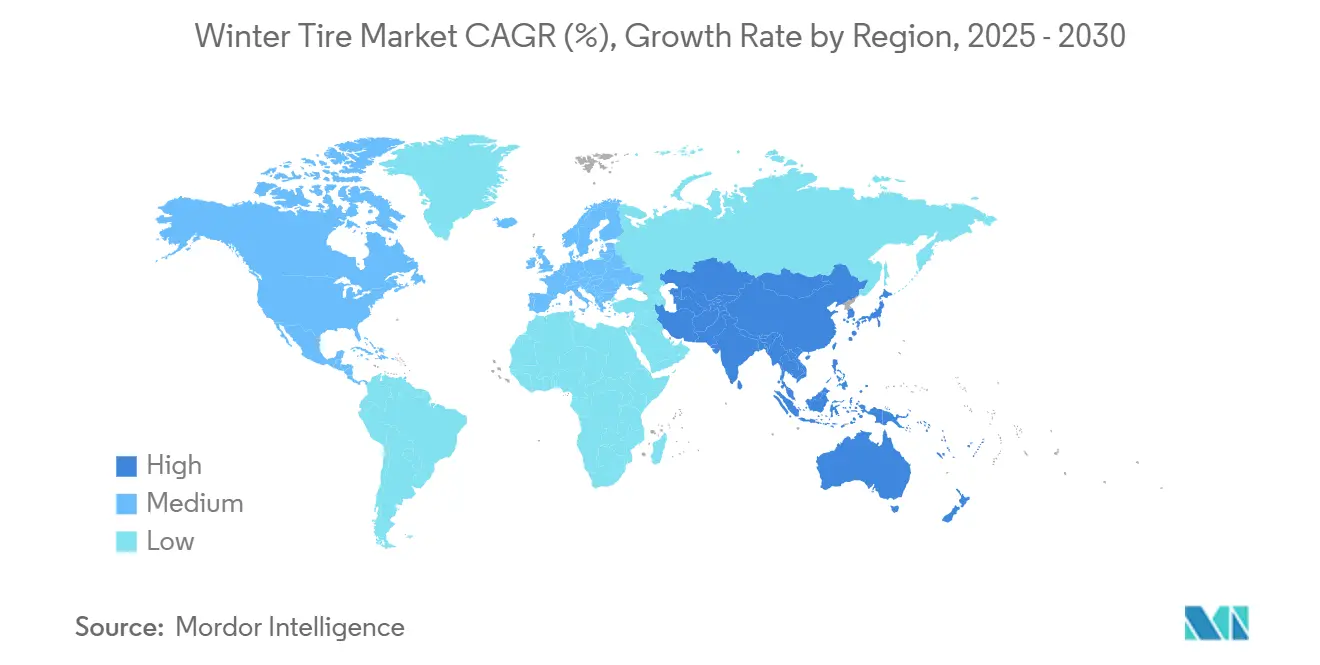

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Winter Tire Market Analysis by Mordor Intelligence

The Winter Tire Market size is estimated at USD 26.91 billion in 2025, and is expected to reach USD 33.61 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030). The growth trajectory reflects consistent regulatory adoption, compound design technology enhancements, and the ongoing shift toward electric and larger-rim vehicles. Expanding mandatory-fitment rules in Europe and selective Asia-Pacific countries underpin structural demand, while 3PMSF certification requirements keep performance thresholds high. Consumer safety focus, especially in snow-belt regions, and premiumization in SUV and crossover segments further sustain replacement cycles and average selling prices. Competitive differentiation now hinges on EV-specific low-rolling-resistance solutions, bio-based material integration, and subscription storage programs that tackle two-set ownership pain points.

Key Report Takeaways

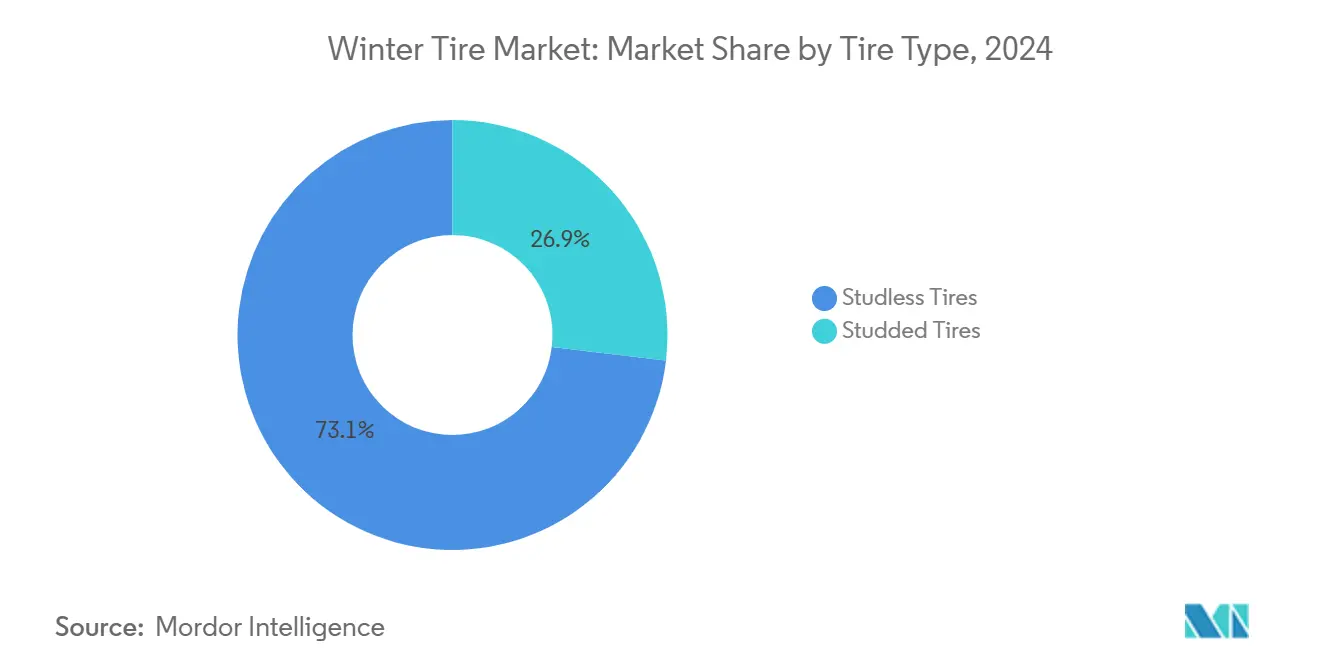

- By tire type, studless tires captured 73.12% of the winter tire market share in 2024 and are advancing at a 4.57% CAGR through 2030.

- By rim size, 12-17 inch products accounted for 54.55% share of the winter tire market size in 2024, while rim sizes above 22 inches recorded the fastest 4.64% CAGR to 2030.

- By vehicle type, passenger vehicles held a 68.83% share of the winter tire market in 2024; the same segment posted the highest 4.63% CAGR through 2030.

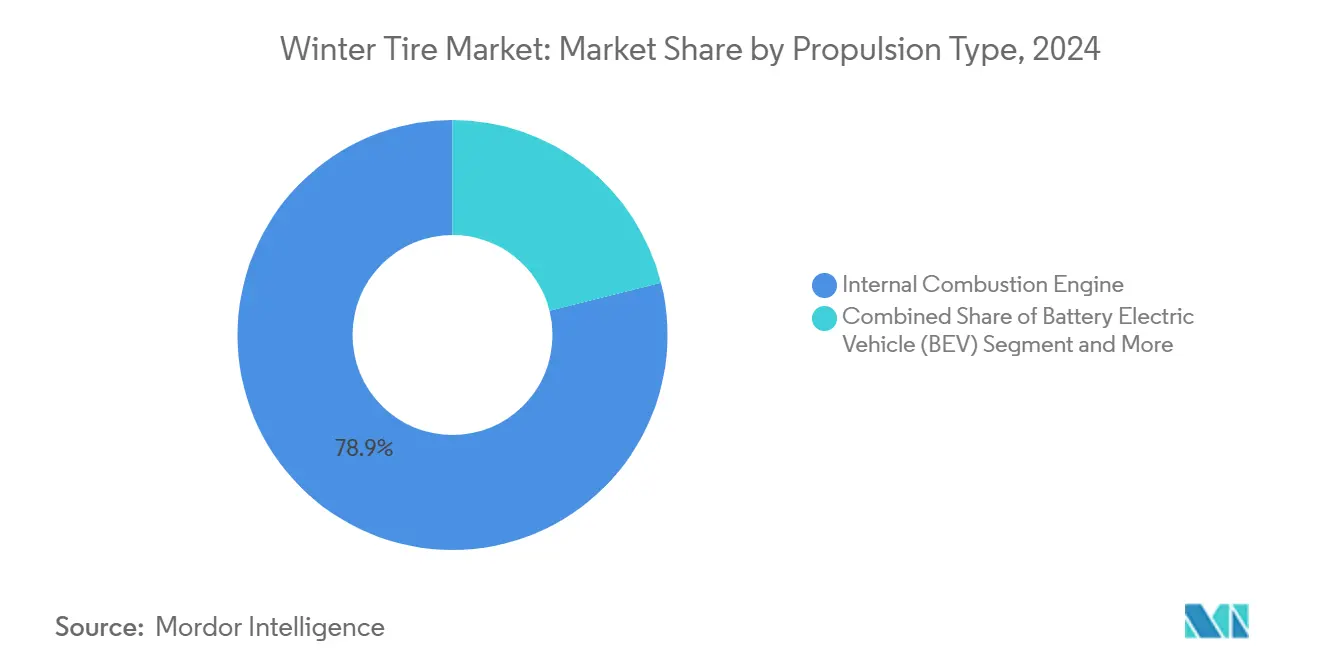

- By propulsion type, internal combustion models led with 78.91% winter tire market share in 2024, whereas battery electric vehicles grew at a 4.58% CAGR to 2030.

- By distribution channel, the aftermarket commanded a 64.57% share of the winter tire market in 2024 and is expanding at a 4.66% CAGR through 2030.

- By geography, Europe led with a 38.51% of the winter tire market share in 2024, while Asia-Pacific registers the fastest 4.61% CAGR through 2030.

Global Winter Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Winter-Tire Regulations Expansion | +0.8% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| SUV & Crossover PARC | +0.6% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Safety-Centric Consumer Behaviour | +0.5% | Europe, North America, Northern Asia-Pacific | Short term (≤ 2 years) |

| EV-Specific Low-Rolling-Resistance Winter Compounds | +0.4% | Global, led by Europe and China | Medium term (2-4 years) |

| Bio-Based Silica Rubber Compounds | +0.3% | Global, early adoption in Europe | Long term (≥ 4 years) |

| Subscription "Tire-As-A-Service" Seasonal Swap Programs | +0.2% | North America, Europe pilot markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Winter-Tire Regulations Expansion

Governments continue to broaden mandatory winter-tire laws, turning episodic demand into a predictable annual requirement. The European Union reinforces 3PMSF certification across member states, while South Korea’s inspection protocols measure grip, braking, and wear to ensure compliance[1]“Winter Tyre Regulations in EU Member States,” European Commission Directorate-General for Mobility and Transport, Europa.eu . Japan’s JATMA standard obliges half of the minimum tread depth, effectively shortening replacement intervals. Commercial operators are also affected; updated MLIT rules prohibit worn winter tires in freight fleets, translating into recurrent aftermarket volumes[2]“Vehicle Inspection Handbook 2025,” Ministry of Land, Infrastructure, Transport and Tourism, mlit.go.jp. As regulations migrate into transitional climate zones, the winter tire market enlarges beyond its traditional base.

SUV & Crossover Parc Growth Driving Larger-Size Sales

Global SUV and crossover registrations keep rising, lifting demand for 17-22 inch and 22-plus-inch winter tires that command premium pricing. Bridgestone’s Blizzak 6 targets this space with ENLITEN technology tuned for heavy vehicles, while Continental broadens its CrossContact Winter range to 22 inches[3]“Blizzak 6 Product Release,” Bridgestone Corporation, bridgestone.com. Larger-rim tires require reinforced constructions to manage higher curb weights, especially in electric SUVs. The premium segment benefits from consumers’ willingness to match high-value vehicles with branded winter solutions, supporting higher margins and revenue growth in the winter tire market.

Safety-Centric Consumer Behavior in Snow-Belt Regions

Heightened awareness of accident statistics in icy conditions convinces drivers that winter tires are essential safety equipment. Korean public campaigns cite 4.5-times higher fatality rates on untreated expressways, encouraging earlier seasonal fitment. Insurance carriers in Canada and parts of the United States now offer premium rebates for verified winter tire use, reinforcing economic incentives. Social media amplification of highway spin-outs sustains public focus, and fleet operators increasingly specify winter tires to mitigate liability risk.

EV-Specific Low-Rolling-Resistance Winter Compounds

Electric vehicles introduce torque-on-demand and higher curb weight, forcing tire makers to redesign compounds for winter grip without eroding range. Michelin codesigned a bespoke winter tire for the Porsche Macan EV that adds advanced silica while cutting rolling resistance. Pirelli’s Elect line incorporates over half of bio-based content yet maintains 3PMSF performance. Limited production volumes and complex development elevate pricing, raising the revenue ceiling for the winter tire market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance Gains In All-Season Tyres | -0.7% | Global, particularly temperate regions | Medium term (2-4 years) |

| Storage and Logistics Burden For Two-Set Ownership | -0.4% | Urban areas globally, acute in Asia-Pacific | Short term (≤ 2 years) |

| Environmental Bans On Road-Wear From Studded Tyres | -0.3% | Nordic regions, select North American markets | Medium term (2-4 years) |

| Shorter Winters Reducing Demand In Temperate Asia-Pacific | -0.2% | Temperate Asia-Pacific, expanding to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance Gains In All-Season Tyres

Premium all-season products like Goodyear Vector 4Seasons Gen-3 and Continental AllSeasonContact 2 now secure “good” winter ratings in ADAC and Auto Bild tests, shrinking the performance gap with dedicated winter tires. Urban drivers in mild climates increasingly opt for year-round fitment to avoid biannual changeovers. Japanese regulators still mandate 3PMSF tires for chain-obligatory roads, but the convenience of one-set ownership draws cost-conscious consumers, eroding replacement volumes expected by the winter tire market.

Storage & Logistics Burden For Two-Set Ownership

High-density cities lack space for off-season tires. Services such as Les Schwab’s six-month storage appeal mainly in North America, leaving most Asia-Pacific residents without practical options. Younger urban dwellers prefer the simplicity of all-season products, and subscription tire-as-a-service plans carry premiums that limit uptake. This logistical hurdle puts downward pressure on winter tire adoption in densely populated regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tire Type: Studless Technologies Drive Market Evolution

Studless products held 73.12% of the winter tire market share in 2024 and are projected to widen their lead at a 4.57% CAGR through 2030, supported by environmental rules banning studded road wear particles. This portion of the winter tire market benefits from bio-based silica blends that keep tread flexible without metal studs. In parallel, studded tires retain a foothold in Nordic territories for extreme ice, but they face mounting duty charges and shorter legal seasons, which curb adoption.

Performance gains in studless compounds are closing the historic traction differential on glare ice, encouraging regulators to phase out studs. Premium ranges from Bridgestone, Nokian, and Continental, which apply 3D siping to amplify edge density, boosting braking performance without increasing road abrasion. The resulting regulatory and performance convergence accelerates the transition to studless solutions across Europe, North America, and Northern Asia-Pacific.

By Rim Size: Premium Sizing Drives Value Creation

The 12-17 inch bracket accounted for 54.55% of the winter tire market size 2024 because it serves the global parc of compact and midsize cars. Yet rim diameters above 22 inches are slated to grow at 4.64% CAGR through 2030, reflecting the popularity of luxury SUVs and electric crossovers. These larger sizes carry higher average selling prices and require reinforced bead and sidewall designs.

Manufacturers with broad mold libraries and multi-compound expertise enjoy a volume and mix advantage in supplying larger rims. For instance, Continental’s 22-inch WinterContact range addresses EV torque peaks without sacrificing wet grip. Production scale favors top-tier suppliers, but niche brands may succeed by focusing on ultra-large sizes that demand quick design cycles and low batch runs.

By Vehicle Type: Passenger Dominance Amid Commercial Growth

Passenger cars represented 68.83% of the winter tire market share in 2024 and are forecast to advance at a 4.63% CAGR, driven by insurance incentives, broader regulations, and higher safety awareness. This category's winter tire market size rises as new drivers in China and Eastern Europe switch from all-season to dedicated winter setups. In parallel, electric models within the passenger group create incremental demand for low-rolling-resistance winter compounds that preserve driving range.

Light commercial vehicles used for e-commerce last-mile delivery need consistent winter traction to meet service-level agreements. Updated MLIT rules for vehicle inspections in Japan and European cabotage regulations prevent fleets from operating on worn winter tires and sustaining replacement cycles. Heavy trucks adopt winter tires selectively, but when mandated, the purchase volumes are significant due to multiple axles.

By Propulsion Type: Electrification Reshapes Performance Requirements

Internal combustion engines kept 78.91% of the winter tire market share in 2024, but battery electric vehicles will expand the winter tire market size for EV-optimized products to 4.58% CAGR by 2030. These tires manage higher curb weights and instant torque by pairing high-silica tread with stiffer belts. Michelin’s EV-specific winter line reduces rolling resistance by one-tenth yet preserves 3PMSF traction.

Hybrid and plug-in hybrid cars bridge the transition, requiring versatility for both combustion and electric driving cycles. Fuel-cell vehicles remain niche, but interest in cold-weather hydrogen trucking may rise, prompting the development of specialized winter tires.

By Distribution Channel: Aftermarket Strength Reflects Consumer Behavior

The aftermarket held a 64.57% of the winter tire market share in 2024, showing the strongest 4.66% CAGR to 2030. Seasonal tire changeovers drive store traffic twice yearly, giving independent retailers and chains leverage to upsell value-added services such as storage or nitrogen inflation. Consumers appreciate the wider brand selection compared with OEM dealerships, encouraging price and performance comparisons at the point of sale.

OEM channels remain linked to new vehicle shipments and warranty service intervals. However, factory-fit specifications influence buyer preferences during replacement, pushing aftermarket distributors to stock brand-original lines. Tire-as-a-service schemes aim to blur channel lines, yet uptake depends on subscription cost and geographic coverage.

Geography Analysis

Europe led the winter tire market with 38.51% of the winter tire market share in 2024, driven by universal 3PMSF rules and mature consumer awareness. Nordic countries are approaching full penetration, while Southern Europe posts the highest incremental growth as climate variability triggers policy changes. The region also pioneers low-noise regulations and particulate limits that favor studless designs.

Asia-Pacific is forecast to post a 4.61% CAGR, the fastest worldwide. China spurs demand through subsidies on EV adoption in northern provinces, translating into new SKUs for heavy, large-rim EVs. Japan’s tread-depth mandate shortens replacement intervals, and South Korea enforces multi-parameter inspections that boost quality-driven purchases. Southeast Asian mountain regions are emerging pockets as vehicle density rises.

North America shows stable, high-value demand. Canada enforces provincial mandates and insurance discounts, resulting in high penetration in Quebec and British Columbia[4]“Winter Tire Safety Campaign 2025,” Transport Canada, tc.canada.ca . The United States has fragmented uptake: northern states mirror European patterns, while southern states restrict winter tires to mountainous areas. Larger rims for pickup trucks and SUVs support a premium mix, and aftermarket distribution dominates seasonal sales.

Competitive Landscape

The winter tire market is moderately concentrated, with Bridgestone, Michelin, and Continental controlling significant global revenues. These leaders differentiate through multi-compound tread designs, advanced siping, and EV-specific lines. Bridgestone’s ENLITEN and Continental’s ContiSeal technologies combine material efficiency with puncture resistance, meeting OEM sustainability targets. Michelin collaborates with RFID specialist Beontag to introduce traceability across tire life cycles, aligning with circular economy directives.

Mid-tier players like Nokian, Hankook, and Toyo compete on niche strengths: Arctic traction, value pricing, and rapid rim-size rollouts. Patent filings around bio-based rubber and recycled steel cords intensify, signaling strategic bets on future environmental legislation. White-space entrants leverage direct-to-consumer models and subscription storage but face heavy logistics requirements.

Regional specialists capitalize on local regulations and road conditions. Giti targets China’s northern provinces with cost-effective studless tires, while Kumho focuses on South Korean fleet contracts that require certified winter performance. The race for EV compatibility and sustainability credentials is now the primary battleground for product launches through 2030.

Winter Tire Industry Leaders

Bridgestone Corporation

Michelin

Continental AG

The Goodyear Tire & Rubber Company

Nokian Tyres plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nexen Tire established a winter tire test center in Finland to enhance cold-weather development and accelerate validation for European and North American launches.

- January 2025: TireHub added Pirelli to its premium tire portfolio, expanding distribution for high-performance winter tires across North America.

- January 2025: Beontag partnered with Michelin to implement RFID tire traceability technology starting in 2025. This collaboration will improve supply chain visibility and support circular economy goals.

Global Winter Tire Market Report Scope

| Studded Tires |

| Studless Tires |

| 12 –17 inch |

| 18 –21 inch |

| Above 22 inch |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Tire Type | Studded Tires | |

| Studless Tires | ||

| By Rim Size | 12 –17 inch | |

| 18 –21 inch | ||

| Above 22 inch | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global winter tire market in 2025?

The winter tire market reached USD 26.91 billion in 2025 and will reach USD 33.61 billion by 2030.

What CAGR is expected for winter tire demand through 2030?

Aggregate demand is projected to rise at a 4.55% CAGR over the 2025-2030.

Which region holds the largest share of winter tire sales?

Europe led in 2024 with a 38.51% revenue share, driven by regulatory mandates and mature consumer adoption.

Which tire type accounts for the majority of winter tire revenue?

Studless tires dominated with 73.12% winter tire market share in 2024 due to technology advances and environmental restrictions on studs.

Why are electric vehicles influencing winter tire design?

EVs have higher curb weight and instant torque, so winter tires need low-rolling-resistance compounds and reinforced structures to preserve driving range and safety.

What channel is most important for winter tire replacements?

The aftermarket remains critical, holding 64.57% of 2024 revenue because consumers prefer seasonal changeovers and broad brand choice.

Page last updated on: