Connected Tires Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

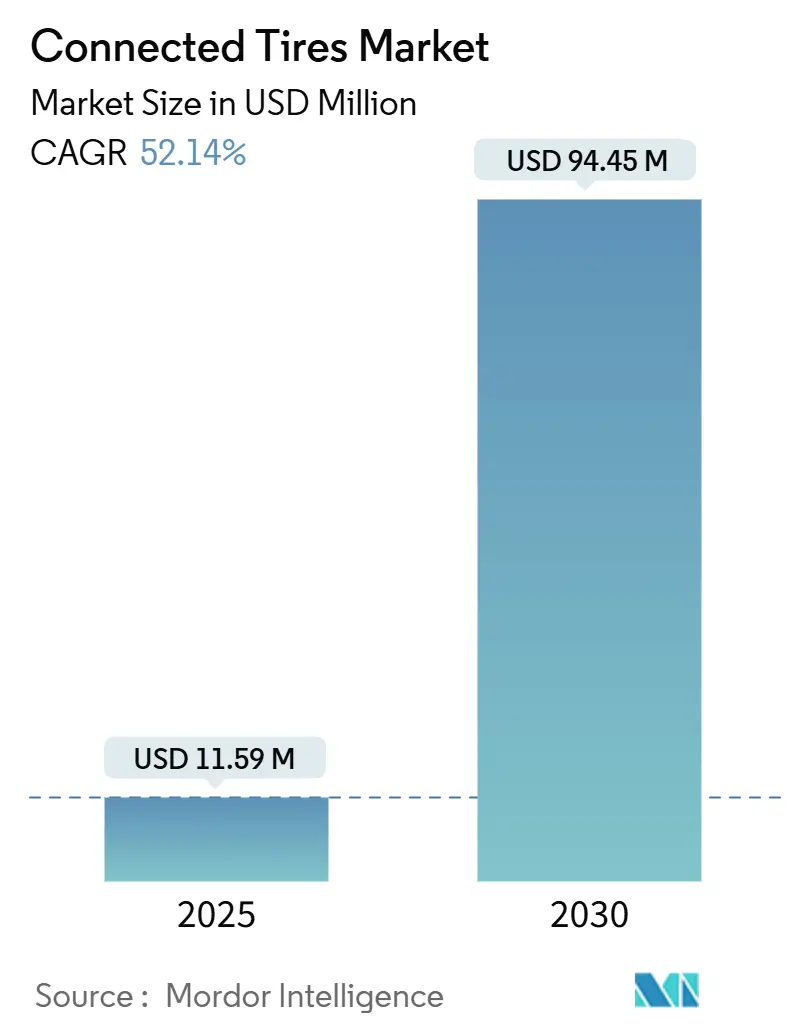

| Market Size (2025) | USD 11.59 Million |

| Market Size (2030) | USD 94.45 Million |

| Growth Rate (2025 - 2030) | 52.14% CAGR |

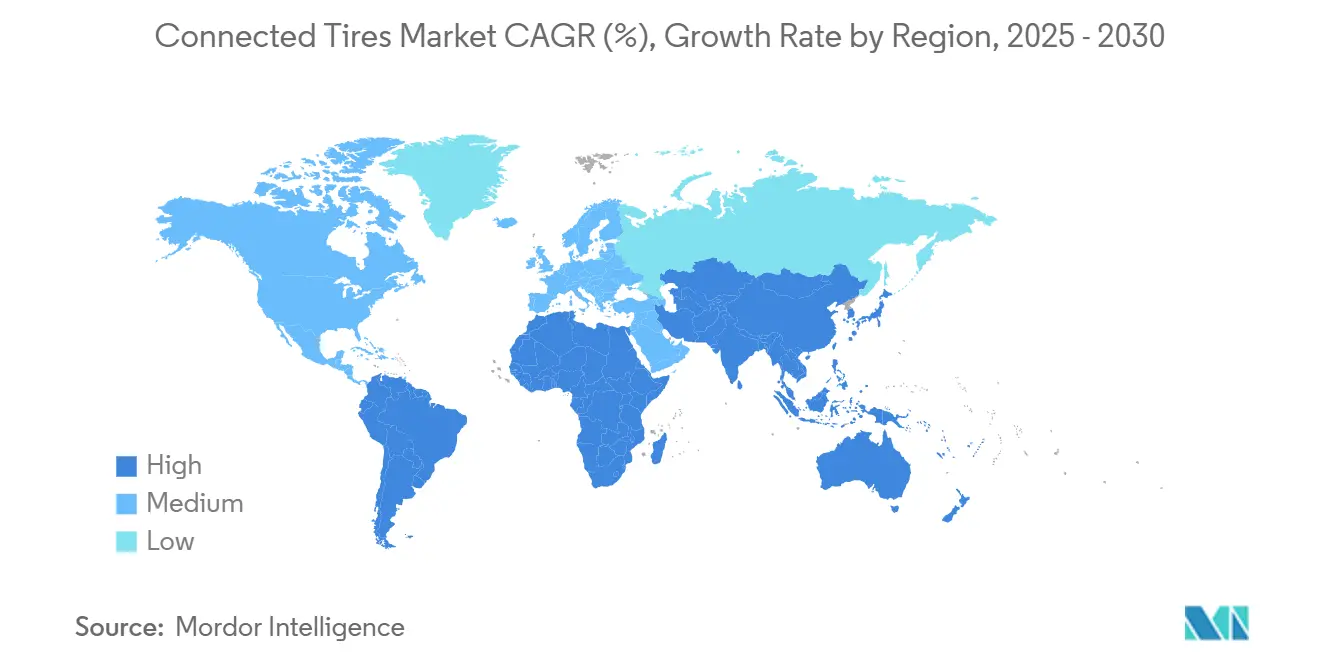

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Tires Market Analysis by Mordor Intelligence

The Connected Tires Market size is estimated at USD 11.59 million in 2025, and is expected to reach USD 94.45 million by 2030, at a CAGR of 52.14% during the forecast period (2025-2030). This projection highlights how the connected tires market is moving beyond pilot programs toward large-scale automotive deployment, propelled by tightening safety regulations, accelerating electric-vehicle sales, and growing fleet digitization demands. Rising OEM integration, rapid sensor-price declines, and data-driven service models further reinforce growth prospects. Strong replacement-tire demand, especially in regions with aging vehicle fleets, also supports adoption, while ecosystem partnerships between tire makers, sensor suppliers, and telematics providers create new revenue pathways. However, short product lifecycles for electronics, cybersecurity compliance costs, and a still-fragmented standards landscape temper near-term margins.

Key Report Takeaways

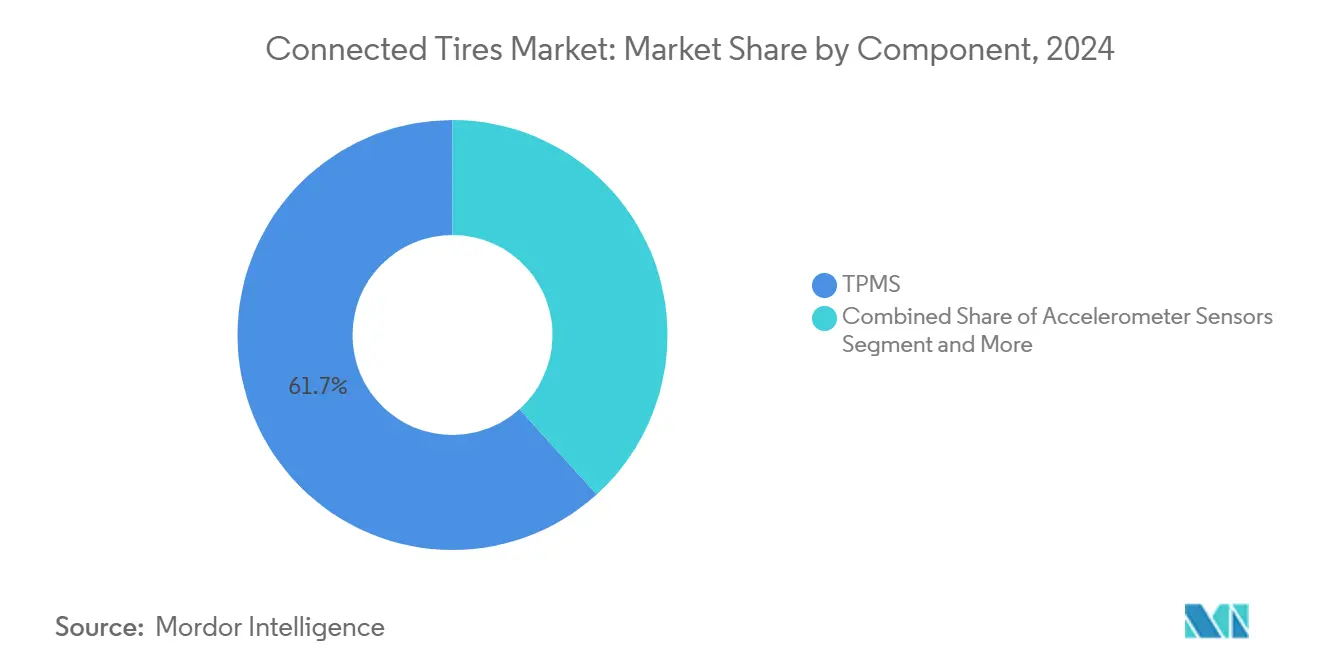

- By component, TPMS led the connected tires market with 61.73% of the share in 2024; RFID chips are forecast to post the highest 52.16% CAGR through 2030.

- By connectivity technology, Bluetooth held 36.78% of the connected tires market share in 2024; cellular 4G/5G connectivity is forecast to advance at a 52.19% CAGR to 2030.

- By rim size, the 18–22 inch segment commanded 56.23% of the connected tires market share in 2024; above-22 inch tires are poised to grow fastest at a 52.17% CAGR through 2030.

- By propulsion type, internal-combustion vehicles captured 66.71% of the connected tires market share in 2024; battery electric vehicles will expand at a 52.31% CAGR over the forecast period.

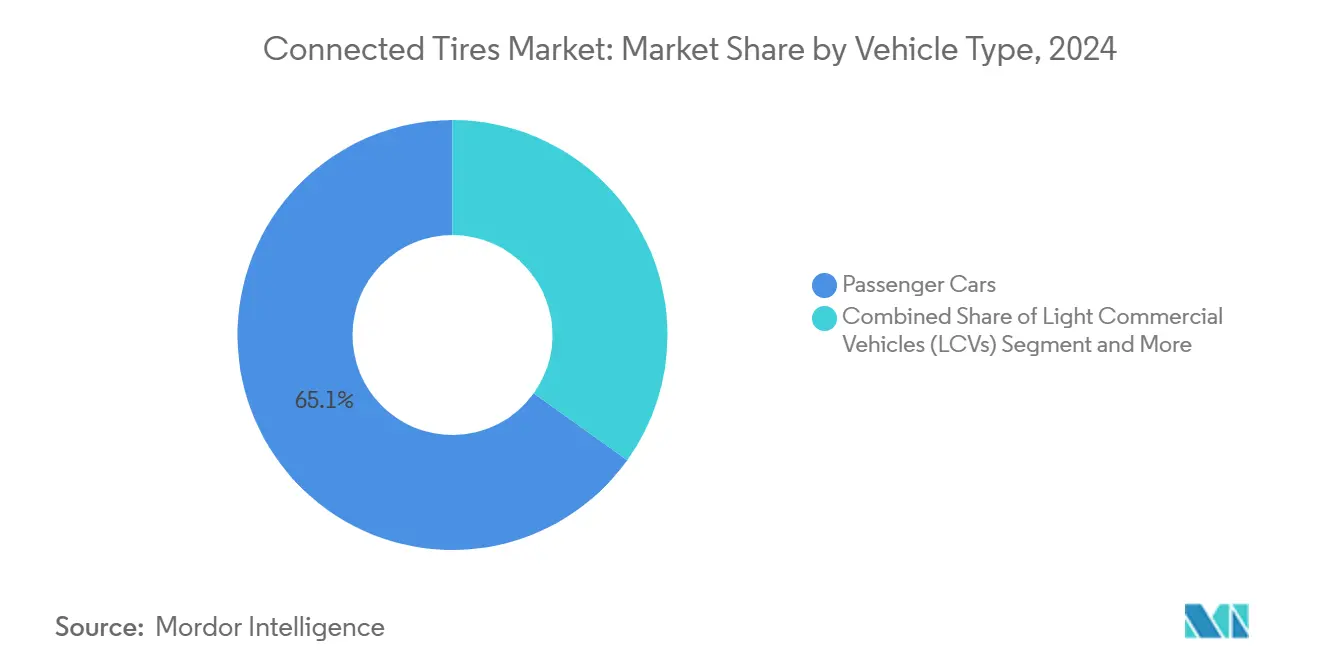

- By vehicle type, passenger cars held 65.11% of the connected tires market share in 2024, yet heavy commercial vehicles are rising fastest at a 52.23% CAGR to 2030.

- By sales channel, OEM fitment dominated with 83.24% of the connected tires market share in 2024 and is projected to lead growth at a 52.26% CAGR through 2030.

- By geography, Asia-Pacific captured 39.85% revenue share of the connected tires market in 2024, while South America is projected to advance at a 52.28% CAGR over the same period.

Global Connected Tires Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Driven Demand | +12.5% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Fleet Focus On Predictive Maintenance | +9.8% | North America and EU commercial corridors | Medium term (2-4 years) |

| Regulatory Mandates | +8.2% | Global, with the EU and North America leading | Short term (≤ 2 years) |

| OEM Shift To Mileage-Based "Tire-As-A-Service" | +7.3% | North America and Europe fleet markets | Medium term (2-4 years) |

| Integration With In-Wheel Motor Torque-Vectoring | +6.1% | Premium vehicle segments globally | Long term (≥ 4 years) |

| Airless/SMA Tires | +4.7% | Global, early adoption in specialized applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Driven Demand For Load-Bearing Smart Tires

Electric vehicles weigh one-fifth more than their internal combustion counterparts and deliver instant torque that accelerates tread wear by the same margin. Battery-electric models, need intelligent tires to monitor load, temperature, and wear in real time to curb rolling resistance and maximize range. Embedded sensors that feed vehicle energy-management systems are becoming standard on new EV platforms across China, Europe, and the United States[1]Goodyear, “SightLine Intelligent Tire Solution,” goodyear.com.

Fleet Focus On Predictive Maintenance & Uptime

North American and European fleet operators increasingly view connected tires as core to uptime strategies. Watsontown Trucking recorded fewer annual labor hours on pre-trip inspections and a minimal drop in roadside incidents after deploying Bridgestone Fleet Care, saving a huge amount in operating costs[2]“Fleet Care Case Study—Watsontown Trucking,” Bridgestone, bridgestone.com . Heavy commercial vehicles showcase how telematics-ready tires trim fuel use, cut emergency call-outs, and boost asset utilization.

Regulatory Mandates For Tpms Adoption

New European Union rules effective 2024 now oblige TPMS installation on light commercial vehicles, joining existing passenger-car requirements. The United States continues to enforce TREAD Act compliance, keeping TPMS fitment non-negotiable for all new light vehicles. These directives lay the groundwork for seamless upgrades to connected tire functions such as real-time tread-wear alerts and remote pressure diagnostics while ushering in cybersecurity and data-privacy norms governing tire-to-infrastructure messaging.

OEM Shift To Mileage-Based “Tire-As-A-Service”

Major fleets now buy uptime rather than rubber. Subscription models bundle tires, sensors, cloud analytics, and replacement into cents-per-mile contracts that shift performance risk back to vendors. Bridgestone and Michelin have trialed pay-per-kilometer programs in Europe, cementing a recurring revenue path for the connected tires industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sensor-Package Cost | -4.8% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Fragmented Connectivity Standards | -3.2% | Global, with regional variation in standards adoption | Medium term (2-4 years) |

| Cyber-Security Liability At The Tire Edge | -2.1% | North America and EU, with regulatory compliance focus | Medium term (2-4 years) |

| Data-Ownership Disputes Slow Ecosystem Uptake | -1.7% | Global, with varying data protection regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Sensor-Package Cost & Harsh-Duty Reliability

Tire-mounted electronics must survive -40 °C to +125 °C swings, centrifugal forces above 1,000 G, and constant flexing for up to seven years. Automotive-grade ASICs, battery chemistries, and hermetic seals drive unit costs that still deter entry-level vehicle segments, limiting immediate aftermarket volumes.

Fragmented Connectivity Standards & Interfaces

Bluetooth accounts for two-fifths of installed systems, yet fleets favor 4G/5G links, the fastest-growing segment at a robust CAGR. The parallel adoption of Wi-Fi and nascent V2X protocols forces OEMs and tire makers to juggle multiple stacks, complicating cross-brand analytics and slowing large-scale deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: RFID chips drive digital transformation

The connected tires market size for TPMS reached 61.73% of total revenue in 2024. TPMS dominance stems from its regulatory pedigree and mature cost curve. RFID expands at a 52.16% CAGR because tags enable cradle-to-grave identification, warranty tracking, and automated warehouse workflows. Michelin’s Gen 4 tags, manufactured under license by Murata beginning January 2025, exemplify scale-ready innovation. Over the forecast period, RFID value capture will intensify as cloud platforms monetize tire-usage data for predictive modeling. TPMS will still anchor baseline safety compliance, yet hybrid TPMS-RFID modules will become common as OEMs seek single-package solutions.

In parallel, accelerometer and strain-gauge sensors are emerging. Bridgestone’s Smart Strain unit quantifies sidewall deflection independent of speed, while Continental leverages vertical-axis accelerometers to map road roughness. These capabilities elevate tires from passive components to real-time road-state probes. As autonomous-driving stacks crave high-fidelity surface information, multi-sensor hubs will migrate from premium to volume segments, powering incremental growth above baseline TPMS revenues.

By Connectivity Technology: Cellular networks enable fleet scale

Bluetooth-enabled tires dominated the connected tires in 2024 with 36.78% market share, owing to low bill-of-materials costs and easy smartphone integration. Yet the segment’s growth is slowing as fleets demand continuous remote visibility that short-range links cannot provide. Cellular 4G/5G solutions, projected to expand at 52.19% CAGR, unlock over-the-air firmware updates, edge analytics, and real-time alerts across national corridors. Partnerships with mobile-network operators help tire makers bundle data plans into the purchase price, lowering adoption friction. V2X remains nascent but strategic, allowing tires to broadcast grip levels to nearby vehicles and infrastructure for cooperative safety scenarios by 2030.

Wi-Fi retains a niche in depot analytics where high-bandwidth uploads archive gigabytes of tread-temperature and wear images during overnight parking. Combined multi-radio architectures are likely to balance cost, power draw, and coverage to serve private motorists and industrial fleets.

By Rim Size: Large diameters drive premium adoption

Tires mounted on 18-22 inch rims held 56.23% of the connected tire market share in 2024, mirroring growth in the crossover, premium sedan, and light-van categories. Connected functionality aligns well with customer expectations for high-tech safety features and is easier to package within wider tire cavities.

Above-22-inch products—covering performance SUVs, luxury EVs, and heavy trucks—are projected to rise at a 52.17% CAGR. Higher unit prices justify sensor integration, and thick carcasses better protect electronics from shock. Conversely, 12-17-inch economy tires remain price-sensitive; adoption will lag until hardware costs drop.

By Propulsion Type: Electric vehicles accelerate sensor integration

Internal combustion models retained 66.71% of the connected tire market share in 2024, yet their growth plateaus as electrification speeds ahead. Battery EVs, sprinting at a 52.31% CAGR, experience heavier curb weights and aggressive torque maps that chew through tread faster.

OEMs, therefore, specify advanced load and temperature monitoring to preserve range and warranty margins. Plug-in hybrids follow a similar rationale but at lower volumes. Fuel-cell vehicles, though niche, value continuous inflation data to protect costly composite wheels, presenting specialized opportunities.

By Vehicle Type: Commercial fleets drive advanced applications

Passenger cars generated 65.11% of the connected tire market share in 2024, reflecting sheer unit volumes and mandated TPMS fitment. Still, heavy commercial trucks are the fastest-growing slice, up 52.23% CAGR, because predictive maintenance reduces downtime costs per roadside failure.

Connected tires feed fleet-management dashboards with wear forecasts, enabling just-in-time replacements and lowering total mileage cost. Buses, coaches, and light-commercial vans also see quick uptake as urban-delivery operators chase uptime and insurance reductions tied to monitored safety compliance.

By Sales Channel: OEM integration dominates market development

OEM programs accounted for 83.24% of the connected tire market share in 2024, and are rising at a 52.26% CAGR as automakers embed sensors during assembly, guaranteeing compatibility with in-vehicle networks. Deep co-design between tire and ECU engineering teams ensures secure data pathways and pressure-loss alerts on factory instrument clusters.

Aftermarket kits struggle with installation complexity and fragmented head-unit interfaces, but retrofit demand persists in fleets seeking uniform dashboards across mixed-brand assets. Over 2025-2030, falling hardware prices and standardization efforts may open broader do-it-yourself consumer channels.

Geography Analysis

In 2024, the Asia-Pacific region held 39.85% of the connected tire market share due to China’s manufacturing heft and Japan’s sensor miniaturization prowess. Government EV incentives and aggressive safety rules push local OEMs to bundle connected tires as a factory standard. South Korea’s electronics giants supply SOCs and power-management ICs, ensuring regional self-sufficiency.

Meanwhile, North America's connected tires market size benefits from extensive trucking corridors where predictive maintenance demonstrates quick ROI. Federal TPMS mandates since 2008 create a mature baseline, encouraging upgrades to telematics-ready versions. Europe follows a similar pattern but adds carbon-emissions pressure, stimulating tire-efficiency analytics.

South America, while smaller, posts the highest 52.28% CAGR as Brazil and Argentina modernize logistics and adopt telematics to navigate long-haul routes. Local retread industries see connected sensors as a way to certify casing health, boosting acceptance. The Middle East and Africa remain exploratory but leverage connected tires for harsh-climate monitoring and off-road safety in mining and oil operations.

Competitive Landscape

Market concentration is moderate. Bridgestone, Michelin, Continental, Goodyear, and Pirelli command the majority of market share, reinforced by long-standing OEM supply contracts. Each invests in proprietary cloud platforms that convert tire-generated datasets into uptime guarantees.

Goodyear collaborates with ZF to feed tire friction metrics into chassis-control software, while its pact with TDK supplies piezoelectric MEMS for next-gen strain sensing[3]“TDK Partnership for Advanced Sensors,” Goodyear, goodyear.com . Continental acquires niche sensor firms to close capability gaps. Michelin scales digital-fleet services in Europe, bundling AI-driven maintenance advice with subscription pricing.

Component suppliers such as Sensata, NXP Semiconductors, and DENSO provide ASICs, batteries, and radios, maintaining bargaining power through automotive-grade certifications. Start-ups like NIRA Dynamics and Revvo focus on edge analytics algorithms, partnering with tier-one tire makers seeking rapid software innovation without costly in-house builds. White-space openings persist in aftermarket retrofits, off-highway equipment, and localized data analytics layers for developing markets.

Connected Tires Industry Leaders

Bridgestone Corporation

Michelin

Continental AG

Goodyear

Pirelli

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hankook Tire launched SmartFlex AL51, a premium truck and bus tire featuring SmaTEC technology targeting five performance areas: safety, mileage, chip-and-cut resistance, retreadability, and braking. The tire has a Grade 2 rolling resistance rating and an 111% improvement in rolling resistance performance versus previous products.

- January 2025: Goodyear and TNO demonstrated advanced vehicle integration capabilities in automatic emergency braking systems for tire intelligence. This shows crash mitigation effectiveness up to 80 kph in wet conditions through real-time tire and road condition data integration.

- January 2025: Goodyear agreed to sell the Dunlop brand to Sumitomo Rubber Industries for USD 701 million, including trademarks and intellectual property for Europe, North America, and Oceania. Transition arrangements will extend through 2026, and five-year off-take agreements will be in place for a minimum of 4.5 million tires annually.

Global Connected Tires Market Report Scope

| TPMS |

| Accelerometer Sensors |

| Strain-Gauge Sensors |

| RFID Chips |

| Bluetooth |

| Cellular (4G/5G) |

| Wi-Fi |

| V2X |

| 12–17 Inches |

| 18–22 Inches |

| Above 22 Inches |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid EV (PHEV) |

| Hybrid EV (HEV) |

| Fuel Cell EV (FCEV) |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Heavy Commercial Vehicles (HCVs) |

| Buses & Coaches |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East & Africa |

| By Component | TPMS | |

| Accelerometer Sensors | ||

| Strain-Gauge Sensors | ||

| RFID Chips | ||

| By Connectivity Technology | Bluetooth | |

| Cellular (4G/5G) | ||

| Wi-Fi | ||

| V2X | ||

| By Rim Size | 12–17 Inches | |

| 18–22 Inches | ||

| Above 22 Inches | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid EV (PHEV) | ||

| Hybrid EV (HEV) | ||

| Fuel Cell EV (FCEV) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Heavy Commercial Vehicles (HCVs) | ||

| Buses & Coaches | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the forecast dollar value for connected tires worldwide by 2030?

The connected tires market is projected to reach USD 94.45 million by 2030, reflecting a 52.14% CAGR over 2025-2030.

Which region will grow fastest through 2030?

South America shows the highest 52.28% CAGR as infrastructure upgrades and fleet telematics adoption accelerate.

Why are electric vehicles important to connected tire demand?

EVs weigh more and deliver instant torque, so real-time load and wear monitoring helps preserve range and extend tire life, driving sensor integration.

How dominant is OEM fitment versus aftermarket retrofits?

OEM channels account for 83.24% of 2024 shipments and remain the fastest-growing as sensors are embedded during vehicle assembly.

Which component segment is expanding most quickly?

RFID chips for lifetime tracking and supply-chain visibility are increasing at a 52.16% CAGR over 2025-2030.

What cost barriers hinder wider adoption?

High automotive-grade sensor costs and harsh-duty reliability requirements limit uptake in price-sensitive car segments.

Page last updated on: