Electric Vehicle Tires Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 12.62 Billion |

| Market Size (2031) | USD 25.70 Billion |

| Growth Rate (2026 - 2031) | 15.28% CAGR |

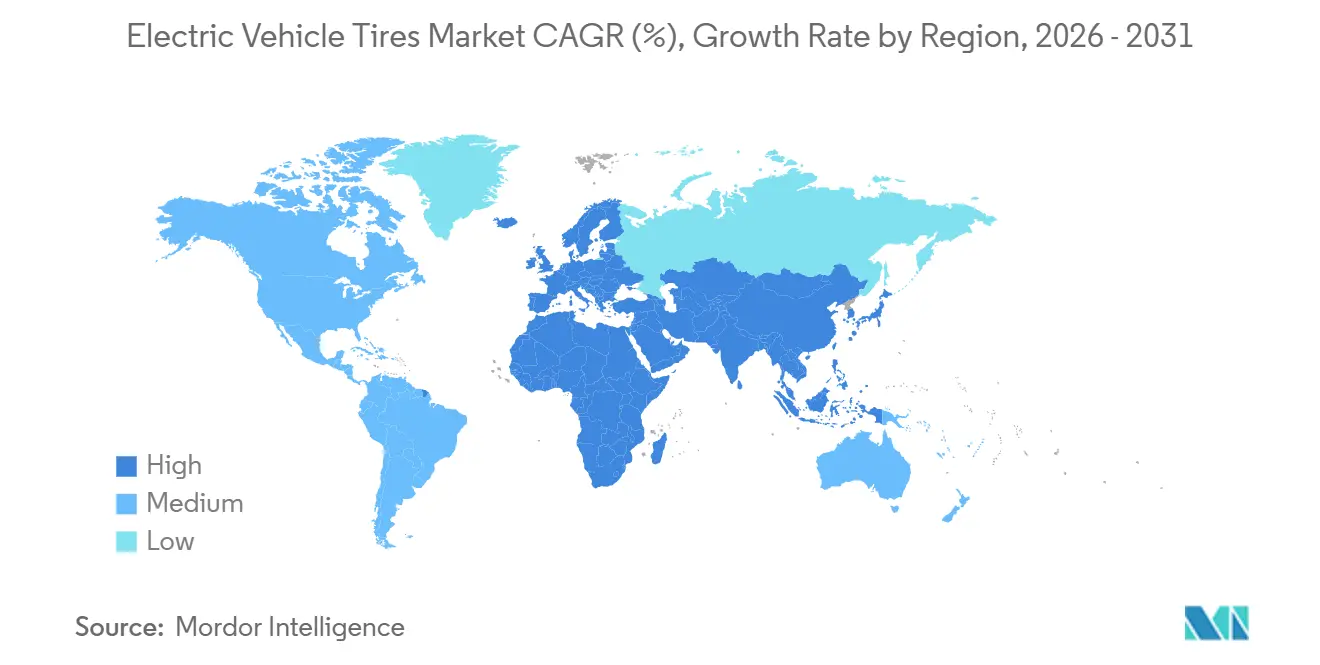

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Tires Market Analysis by Mordor Intelligence

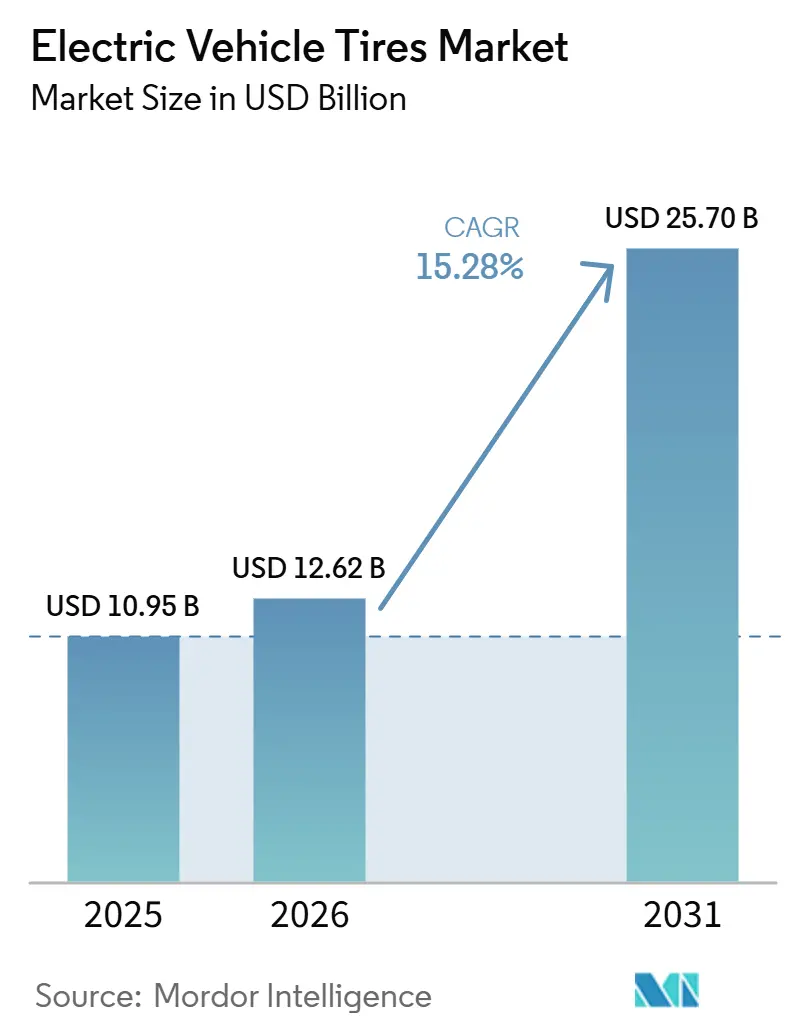

The electric vehicle tires market size is expected to be USD 10.95 billion in 2025, USD 12.62 billion in 2026, and reach USD 25.70 billion by 2031, growing at a CAGR of 15.28% from 2026 to 2031. As electric vehicle (EV) production surges and preferences shift towards heavier architectures and larger rims, demand is broadening. Concurrently, regulatory emphasis on rolling resistance and noise is steering the industry towards the adoption of premium compounds. Original Equipment Manufacturers (OEMs) are increasingly sourcing low-rolling-resistance designs to enhance driving range. This trend is not only solidifying relationships with the top tire suppliers but also consolidating the electric-vehicle tire market. Meanwhile, volatility in raw materials and impending restrictions on 6PPD are driving a swift pivot towards renewable feedstocks. This shift comes as natural rubber prices have fluctuated significantly. In the Middle East and Africa, rapid unit expansion is underway, spurred by infrastructure rollouts aligned with government zero-emission mandates. Yet, the Asia-Pacific region, led by China's expansive production capabilities, continues to dominate in scale. Today, competitive differentiation hinges on reducing wear, integrating sensors, and leveraging direct-to-consumer channels. Premium brands are dedicating a notable portion of their sales to R&D investments as part of their strategic focus.

Key Report Takeaways

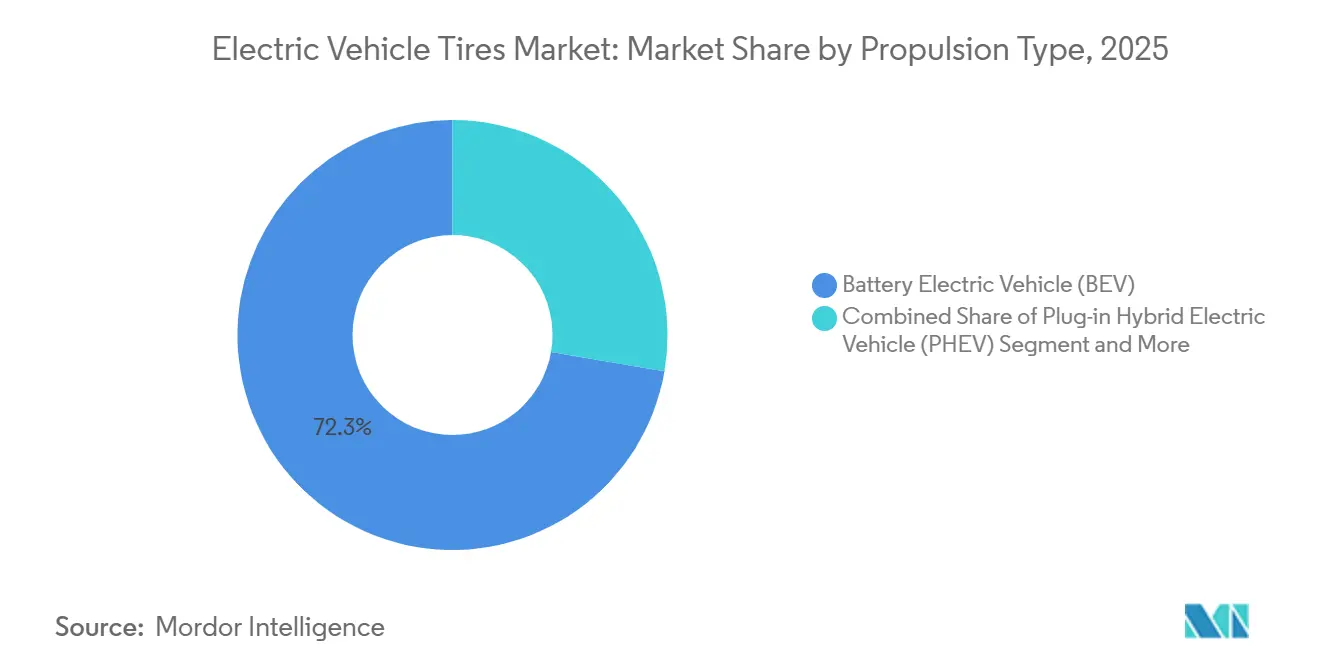

- By propulsion type, Battery Electric Vehicles (BEVs) held a 72.34% share in 2025, while Fuel-Cell Electric Vehicles (FCEVs) are projected to expand at a 17.12% CAGR through 2031.

- By vehicle type, passenger cars accounted for 64.18% of sales in 2025, whereas heavy commercial vehicles are forecast to post a 16.06% CAGR through 2031.

- By application, on-road usage captured 76.44% of demand in 2025, and off-road tires are advancing at a 15.87% CAGR over the forecast window.

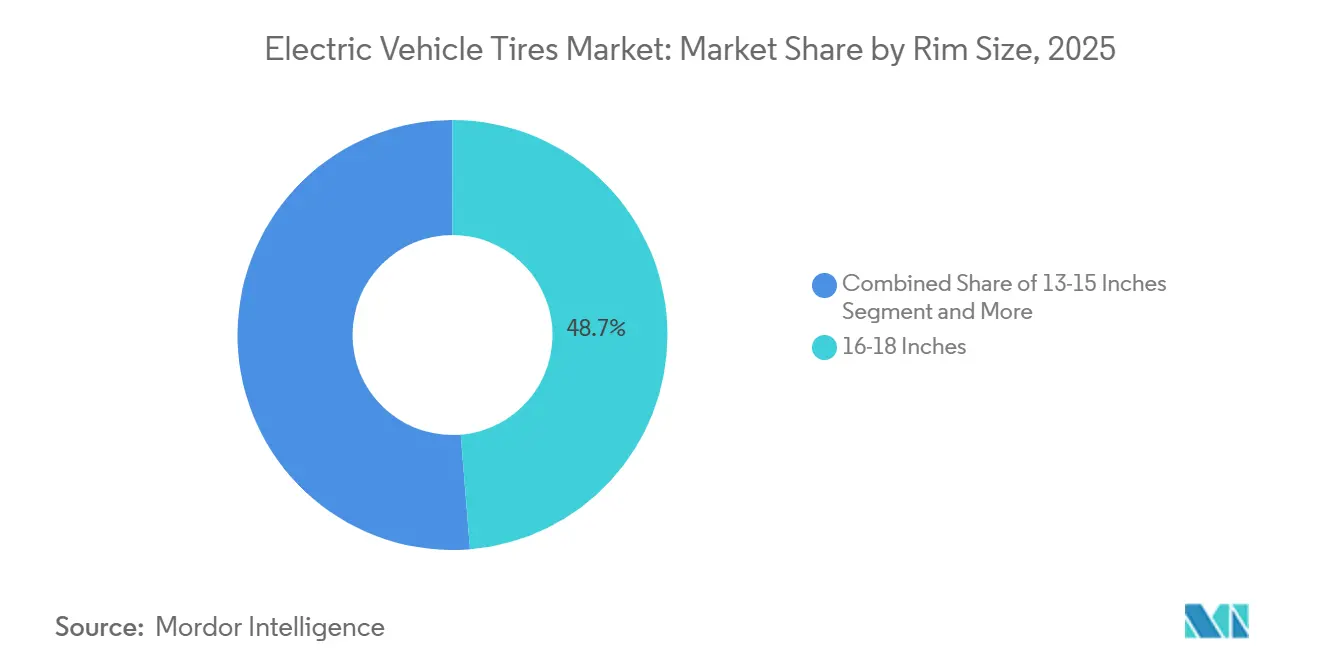

- By rim size, the 16-18-inch category held a 48.71% share in 2025, while tires above 21 inches are set to grow at a 16.84% CAGR through 2031.

- By sales channel, the OEM route controlled 59.33% of volumes in 2025, yet the aftermarket is expanding at a 15.41% CAGR as replacement cycles shorten.

- By geography, Asia-Pacific dominated with 54.63% share in 2025, whereas the Middle East and Africa are projected to record a 15.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Vehicle Tires Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Global EV Production | +4.5% | Global, led by China, Europe, North America | Medium term (2-4 years) |

| OEM Focus on Range-Boosting Tires | +3.2% | Global premium markets | Long term (≥ 4 years) |

| Accelerated EV Tire-Wear Boosts Demand | +2.8% | Mature EV markets | Short term (≤ 2 years) |

| Stricter Tire Regulations Impact Design | +1.8% | Europe and expanding regions | Medium term (2-4 years) |

| OEM Warranty for High-Load Tires | +1.5% | Commercial vehicle hubs | Long term (≥ 4 years) |

| Smart-Sensor Tires Unlock Revenue Streams | +1.2% | Premium markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Global EV Production and Sales

Global electric vehicle (EV) production has seen significant growth, with China contributing the largest share and Europe following. The International Energy Agency forecasts that EVs will dominate new passenger-car registrations in the coming years, driving long-term growth in the electric vehicle tires market. Assembly plants require five tires per vehicle, including spares, which directly translates production increases into higher tire demand. Recent production trends indicate short-term inventory adjustments. Despite this, original equipment manufacturers (OEMs) are narrowing their supplier lists. Notably, Continental now serves most of the high-volume EV producers, improving its economic scale. As production hubs expand in regions like Southeast Asia and Mexico, logistics are becoming increasingly complex. This shift provides a competitive advantage to global suppliers with localized curing facilities.

OEM Focus on Range-Boosting Low-Rolling-Resistance Tires

Rolling resistance accounts for as much as 30% of highway energy draw, making tire selection a prime lever in easing range anxiety. Continental’s EcoContact 7 received an A label under EU Regulation 2020/740, achieving a 15% reduction in rolling resistance compared to its predecessor [1]“Tire Technology Innovations 2026,”, Continental AG, continental.com. Michelin responded with the Primacy 5 Energy, launched in March 2026, delivering up to a 10% range uplift through silica-rich tread chemistry [2]“Primacy 5 Energy Technical Sheet,”, Michelin, michelin.com. The EU label program has effectively reduced energy consumption and is projected to continue saving energy over time. Meanwhile, in the U.S., the NHTSA has identified ROLL10 and ROLL20 technologies as cost-effective solutions for meeting Corporate Average Fuel Economy targets. These policies sustain high computational modeling budgets and encourage suppliers to focus on compound optimization, ensuring tread depth does not compromise grip or longevity.

Accelerated EV Tire-Wear Boosting Replacement Demand

Electric vehicles (EVs) experience quicker wear and tear due to their instant torque and the weight of their batteries, leading to more frequent replacements than in internal combustion engine (ICE) vehicles. Capitalizing on this trend, premium suppliers are pricing EV-specific SKUs higher than traditional ones. Continental's EcoContact 6, designed to extend tire life, effectively reduces ownership costs. Additionally, with many new EV models featuring larger rims, the tighter sidewalls are subject to increased wear, driving up aftermarket demand.

Stricter Tire Energy-Label and Noise Regulations

UNECE Regulation 117 Revision 6 Amendment 2 mandates abrasion testing for C1 passenger tires, emphasizing convoy tests aligned with regenerative braking levels. Simultaneously, EU Regulation 2020/740 mandates transparency in rolling resistance and noise ratings. Notably, A-rated products consume less energy than their G-rated counterparts. Japan has adopted a similar labeling approach, and China is piloting its efficiency ratings, broadening the global compliance landscape. Continental has achieved significant progress in the use of renewable and recycled materials, outpacing future targets. In contrast, smaller firms face funding challenges for compound redesigns and investments in indoor drums, driving consolidation in the electric vehicle tires market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -2.5% | Asia-Pacific production hubs | Short term (≤ 2 years) |

| High R&D, Tooling Costs | -1.8% | Global, smaller manufacturers most exposed | Medium term (2-4 years) |

| Synthetic Rubber Sustainability Scrutiny | -1.2% | Europe and North America | Medium term (2-4 years) |

| Absence of Unified EV-Tire Certification | -0.8% | Multi-regional | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility and Supply-Chain Risk

Natural rubber prices reached their highest level in over a year due to storms in Southeast Asia disrupting latex flows and a shift in plantations towards palm oil, which reduced available acreage. Continuous supply deficits have created a demand-supply imbalance, putting pressure on profit margins. Meanwhile, synthetic rubber prices, closely tied to crude oil volatility, have fluctuated significantly. Indian producers, with crude-linked inputs accounting for a substantial portion of their costs, experienced margin declines as oil prices rose. This volatility has prompted them to adopt hedging strategies and diversify their feedstock. In response to such commodity fluctuations, Continental has set a target to increase its renewable content to buffer against market swings.

High R&D and Tooling Cost for EV-Specific Compounds

Continental has allocated significant resources for tire R&D, while Michelin, with a dedicated team, consistently invests heavily, outpacing mid-tier rivals. Establishing a line for electric vehicle tires often demands substantial investment in custom molds, especially as rim diameters increase. The USTMA predicts a challenging timeline to replace 6PPD, necessitating a costly dual-line phase for an extended period. Smaller Asian brands, lacking OEM endorsements, find it hard to recoup such investments. This limitation nudges them towards price-sensitive segments or partnerships with local automakers. As a result, consolidation is set to accelerate, heightening entry barriers and centralizing intellectual property among the top five brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Fuel Cells Drive Future Growth

Battery Electric Vehicles (BEVs) dominated the electric vehicle tires market with a 72.34% share in 2025, reflecting their prevalence in passenger and light-commercial applications. Fuel-Cell Electric Vehicles (FCEVs) are forecast to grow at a 17.12% CAGR through 2031 as Japan and South Korea subsidize hydrogen dispensing corridors.

Honda's CR-V e:FCEV showcases design nuances, utilizing tires to handle a curb weight, with hydrogen tanks positioned behind the axle. While tire supply for Battery Electric Vehicles (BEVs) is scalable globally, the limited volume of Fuel Cell Electric Vehicles (FCEVs) hasn't justified specialized tooling. This constraint nudges suppliers to adapt BEV casings with minor chemical modifications. Yet, if infrastructure advancements keep pace, the electric vehicle tires market, driven by FCEVs, could present a prime opportunity for premium brands to delve into hydrogen-compatible compounds. While a lag in ISO cohesion poses challenges for global homologation, UNECE's convoy alignment rule marks progress in standardizing rolling-resistance and abrasion benchmarks across all electrified drivetrains.

By Vehicle Type: Commercial Vehicles Accelerate Electrification

Passenger cars accounted for 64.18% of revenues in 2025, yet heavy commercial vehicles are expected to expand at a 16.06% CAGR, lifting their market share amid EU demands for a 45% CO₂ cut by 2030.

Continental’s Conti Efficient Pro demonstrates the engineering leap needed to support tractors weighing 30% more than diesel peers without eroding efficiency. Light commercial vans are also being rapidly adopted as e-commerce leaders pursue carbon-neutral logistics, with Amazon, DHL, and UPS specifying electric drivetrains across Europe and North America. Higher rim diameters (18-20 inches) and load indices intensify heat build-up, but premium pricing—USD 400-800 per tire—offsets lower unit volumes. While passenger-car growth is moderating in early-adopter markets, crossovers and SUVs anchor replacement demand, keeping the electric vehicle tires market resilient across cycles.

By Application: Off-Road Electrification Gains Momentum

On-road deployments represented 76.44% of 2025 demand, but off-road niches are advancing at a 15.87% CAGR through 2031 as mines and quarries decarbonize.

Sandvik's Toro LH518iB loader, equipped with hefty L-5S tires, manages a substantial operating weight. This underscores a design focus on compound reinforcement and cut resistance over merely prioritizing low rolling resistance. Meanwhile, electric haul trucks, such as SANY's SKT105E, boast a commendable tire lifespan. However, suppliers mandate on-site payload validation to uphold warranty commitments. While agricultural electrification lags, hindered by battery-swap logistics, equipment in vineyards and orchards is reaping early benefits. Collectively, these advancements are bolstering the electric vehicle tires market, especially in specialized SKUs, with average selling prices exceeding USD 5,000 per set.

By Rim Size: Premium Segments Drive Innovation

The 16-18-inch class retained 48.71% of revenue share in 2025, reflecting compact and mid-size BEV volumes, yet rims above 21 inches are projected to surge at a 16.84% CAGR as luxury SUVs and pickups proliferate.

Continental, responding to rising Indian demand for both premium imports and domestic flagships, has invested significantly to upgrade its Modipuram plant to increase tire production. Michelin’s Pilot Sport Energy, designed for performance EVs, focuses on larger sizes, combining top-rated rolling resistance with reinforced bead bundles. While larger rims, priced at a premium per tire, require more raw materials, the stronger margins they offer offset any volume dilution. Given aesthetic preferences and the need for regenerative-braking clearance, the electric vehicle tire industry is poised to increasingly favor oversized formats. This trend is particularly pronounced in North America and China, regions witnessing the highest adoption of pickups.

By Sales Channel: Aftermarket Momentum Builds

OEM fitments controlled 59.33% of shipments in 2025, but the aftermarket is growing at a 15.41% CAGR as EV owners cycle through replacements every 15,000-30,000 miles.

Independent dealers and e-commerce platforms are broadening choices and driving competitive pricing. This shift has prompted premium brands to unveil direct storefronts and forge mobile install partnerships. Subscription models, which package tires with maintenance, are redefining conventional channel boundaries. However, the aftermarket enjoys a heftier per-unit margin by sidestepping OEM volume rebates. In India, replacement sales account for an important share of the tire market, a segment expected to grow as electrification spreads beyond major cities. Consequently, the market for electric vehicle tires is set to reach channel parity, aligning with the evolution of wear-sensitive EV platforms.

Geography Analysis

Asia-Pacific, anchored by China, secured 54.63% of the electric vehicle tires market in 2025. Domestic production of tire units has significantly increased, energizing the market. To navigate trade frictions, Chinese firms like Zhongce, Giti, and Sailun are expanding their overseas curing capacities. However, with domestic inventories on the rise, they're feeling the squeeze of rising prices. As India's EV sales continue to grow, Bridgestone has invested in its Pune facility, while Continental has allocated funds for new production lines. MRF is catering to Tata, Mahindra, and a host of emerging two-wheeler initiatives. Meanwhile, JK Tire has partnered with EKA Mobility, integrating advanced connected sensors into commercial EV casings [3]“Partnership with EKA Mobility 2024,”, JK Tyre & Industries, jktyre.com.

North America and Europe, together accounting for a significant share of the market, play a pivotal role in the premium A-rated segment. This is especially true as EU labeling standards and California’s Advanced Clean Trucks regulation elevate performance benchmarks. To align with EU microplastic mandates and U.S. 6PPD restrictions, suppliers are increasingly incorporating recycled rubber and bio-based fillers into their roadmaps. This shift is also leading to tighter qualification cycles and extended lead times.

The Middle East and Africa, though small, are forecast to post the fastest CAGR of 15.74% through 2031, as the UAE and Saudi Arabia allocate sovereign funds to charging networks and mandate zero-emission quotas. Elevated ambient temperatures above 50 °C hasten oxidation, forcing compound tweaks that favor ozone-resistant polymers. South America lags but gains momentum via Brazilian tax waivers for local BEV assembly by Chinese OEMs, although infrastructure and affordability still curb near-term upside. Together, these regional vectors keep the electric vehicle tires market diversified across economic cycles and regulatory regimes.

Competitive Landscape

Leading the electric vehicle tire market, Michelin, Bridgestone, Continental AG, Goodyear, and Pirelli hold dominant shares of global OEM supply contracts. Continental boasts partnerships with many of the top EV assemblers, enabling efficient tooling amortization across vast volumes. Meanwhile, Michelin has secured contracts with several of China's top premium BEVs. Premium brands are setting themselves apart with innovations like silica-rich compounds, smart sensors, and direct-to-consumer portals, capitalizing on the aftermarket. Notable R&D achievements include Michelin’s Primacy Energy, which boosts range, and Continental’s EcoContact, which reduces wear per kilometer.

Mid-tier and regional brands are aggressively pursuing cost leadership by leveraging local distribution channels to dominate price-sensitive markets. Yokohama's recent OE accolade from BYD underscores a shift, hinting at Chinese automakers' growing acceptance of foreign suppliers seeking global recognition. In India, tire giants Apollo, MRF, and CEAT are eyeing the burgeoning aftermarket, with MRF seeing a notable uptick in exports that now constitute a substantial portion of its overall volume. In the fiscal year 2024-25, MRF's export turnover reached INR 2,307 crores, marking a robust 23% increase from the INR 1,874 crores recorded in the prior year. All three are channeling investments into connected-tire telemetry to enhance fleet adoption.

Incumbent firms benefit from navigating regulatory intricacies: UNECE’s abrasion mandate demands test tracks and drum rigs, resources often out of reach for smaller players. While Chinese manufacturers are establishing overseas bases to sidestep tariffs, European clients remain wary, particularly regarding quality issues with oversized rims. Additionally, premium firms are adeptly navigating raw-material shocks, leveraging recycled polymers to sustain double-digit margins, even amidst inflationary pressures.

Electric Vehicle Tires Industry Leaders

Michelin

Bridgestone Corporation

Goodyear Tire and Rubber Company

Pirelli & C S.p.A.

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Continental AG (Continental) has secured approval from Porsche for its SportContact 6, CrossContact RX, and WinterContact TS 860 S tires. These tires, sized between 20 and 22 inches, are set to equip the Macan all-electric SUV across various countries. Notably, the SportContact 6, hailing from the ultra-ultra-high-performance (UUHP) segment, boasts remarkable grip and top-tier safety, even at exhilarating speeds of 350 km/h.

- November 2025: Continental AG (Continental) has equipped the Hyundai IONIQ 9, an all-electric SUV, with its PremiumContact C tires. The chosen tire size is 285/45R21 113V XL FR, tailored for warm-season use on heavy SUVs and crossover vehicles.

Global Electric Vehicle Tires Market Report Scope

The electric vehicle tires market report is segmented by propulsion type (battery electric vehicle (BEV), plug-in hybrid electric vehicle (PHEV), hybrid electric vehicle (HEV), and fuel-cell electric vehicle (FCEV)), vehicle type (passenger cars, light commercial vehicles (LCVs), heavy commercial vehicles (HCVs), and buses and coaches), application (on-road and off-road), rim size (13-15 inches, 16-18 inches, 19-21 inches, and above 21 inches), sales channel, and geography. The market forecasts are provided in terms of value (USD) and volume (units).

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Heavy Commercial Vehicles (HCVs) |

| Buses and Coaches |

| On-Road |

| Off-Road |

| 13-15 Inches |

| 16-18 Inches |

| 19-21 Inches |

| Above 21 Inches |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Propulsion Type | Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Heavy Commercial Vehicles (HCVs) | ||

| Buses and Coaches | ||

| By Application | On-Road | |

| Off-Road | ||

| By Rim Size | 13-15 Inches | |

| 16-18 Inches | ||

| 19-21 Inches | ||

| Above 21 Inches | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the electric vehicle tires market by 2031?

The electric vehicle tires market is forecast to reach USD 25.70 billion by 2031, expanding at a 15.28% CAGR over 2026-2031.

Which rim-size category is growing fastest in electric vehicle tires?

Tires larger than 21 inches are expected to rise at a 16.84% CAGR as luxury SUVs and pickups dominate new EV launches.

Which region currently leads global demand for electric vehicle tires?

Asia-Pacific holds 54.63% of global demand, supported by China’s sizable EV manufacturing base and India’s rapid sales growth.

How are raw-material costs impacting the electric vehicle tires market?

Natural rubber hit 205 US cents/kg in Feb 2026, part of a multi-year deficit that has trimmed tire-maker margins by up to 300 basis points .

Why is aftermarket demand accelerating for electric vehicle tires?

Aftermarket sales are experiencing significant growth, driven by EVs that wear tires faster than their ICE counterparts, resulting in shorter replacement cycles.

Page last updated on: