OTR Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 26.17 Billion |

| Market Size (2030) | USD 32.81 Billion |

| Growth Rate (2025 - 2030) | 4.63% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

OTR Tire Market Analysis by Mordor Intelligence

The OTR Tire Market size is estimated at USD 26.17 billion in 2025, and is expected to reach USD 32.81 billion by 2030, at a CAGR of 4.63% during the forecast period (2025-2030). Elevated infrastructure spending, a rebound in mining capital expenditure, and rapid mechanization across emerging economies anchor this expansion. The electrification of haulage fleets in large open-pit mines is another structural catalyst illustrated by Fortescue’s order for 475 zero-emission trucks. Tire makers continue funneling capital into capacity: Bridgestone alone committed to enlarging its Kitakyushu plant for premium mining and construction tires. Heightened demand intersects with the tightening natural rubber supply, pushing producers to diversify sourcing and accelerate research into bio-based alternatives. At the same time, tire-as-a-service (TaaS) contracts bundled with telematics are redefining aftermarket economics, reducing downtime for fleet operators and deepening loyalty to premium brands.

Key Report Takeaways

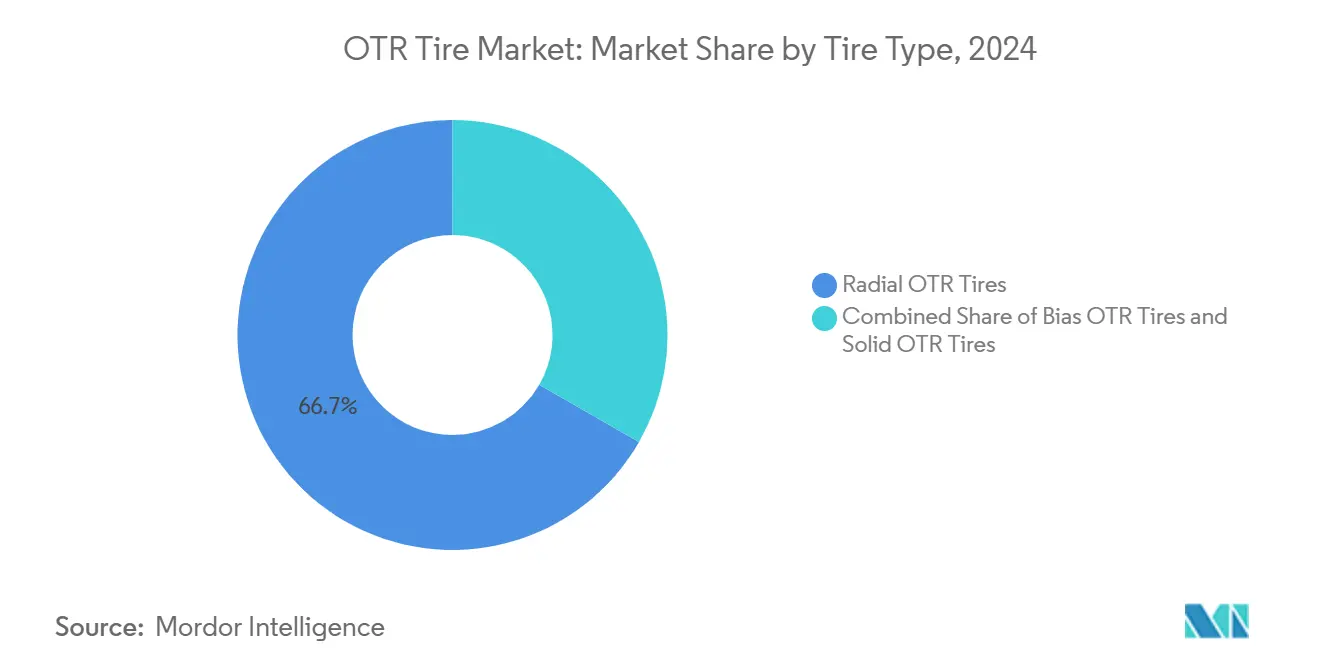

- By tire type, radial products captured 66.71% of the OTR tire market share in 2024; solid tires are forecast to compound at a 4.65% CAGR through 2030.

- By equipment type, earthmovers held 24.52% of the off the road tire market share in 2024, while loaders and dozers are projected to grow at a 4.78% CAGR.

- By rim size, less than 31-inch wheels accounted for 38.73% of the OTR tire market share in 2024; the 41–45-inch range is poised to expand at a 4.66% CAGR.

- By application, construction led with 37.18% of the off the road tire market share in 2024, whereas port equipment is advancing at a 4.77% CAGR.

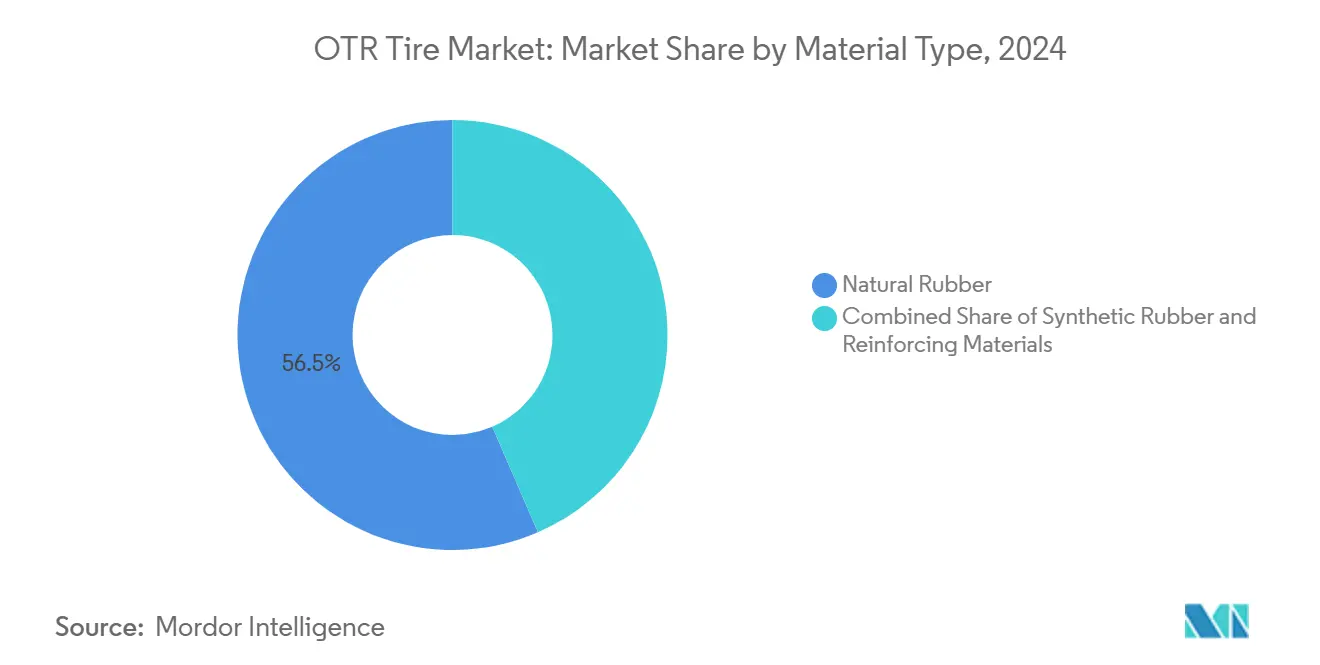

- By material, natural rubber represented 56.47% of the OTR tire market share in 2024; the reinforcing materials segment is set for a 4.75% CAGR.

- By distribution channel, the aftermarket dominated with 73.27% of the off the road tire market share in 2024, rising at a 4.68% CAGR.

- By geography, Asia Pacific commanded 38.33% of the OTR tire market share in 2024, while the Middle East & Africa is projected to grow at a 4.71% CAGR through 2030.

Global OTR Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Megaproject Pipeline | +1.2% | Global, concentrated in MEA, Asia Pacific | Long term (≥ 4 years) |

| Commodity Super-Cycle Reviving Large-Scale Mining Capex | +1.0% | Global, led by Australia, Chile, South Africa | Medium term (2-4 years) |

| Accelerating Mechanization | +0.8% | Asia Pacific core, spill-over to Africa, Latin America | Medium term (2-4 years) |

| OEM Shift To Telematics-Enabled Tire-As-A-Service Contracts | +0.6% | North America and EU, expanding to Asia Pacific | Short term (≤ 2 years) |

| Electrification Of Underground Mining Vehicles | +0.5% | Global, led by Australia, Canada, South Africa | Medium term (2-4 years) |

| Surge In Demand For Low-Profile Metric Tires | +0.4% | Global, concentrated in North America, EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Megaproject Pipeline

Multi-billion-dollar transport, energy, and utility ventures underpin a steady pull for heavy equipment and thus for the off-the-road (OTR) tire market. Saudi Arabia’s 2025 construction outlay grows exponentially, channeling two-fifths into Riyadh province’s giga-projects[1]“Saudi Arabia Budget 2025,” Ministry of Finance, mof.gov.sa. The UAE maintains a massive pipeline spanning metro extensions, solar parks, and smart-city districts[2]“UAE Infrastructure Outlook,” Ministry of Energy & Infrastructure, moei.gov.ae. Such multi-year programs keep earthmovers and dump trucks in near-continuous service, translating to predictable replacement cycles as projects move from greenfield to maintenance phases, demand shifts from OE fitments to the aftermarket. Because these projects cluster in hot, abrasive environments, premium compounds with superior heat dissipation enjoy pricing power and deepen brand differentiation.

Commodity Super-Cycle Reviving Large-Scale Mining Capex

Battery-electric vehicles, solar panels, and grid storage technologies revive appetite for copper, lithium, nickel, and rare-earth elements. Miners have responded: autonomous haul truck fleets at Chilean copper pits now exceed 360 units, each fitted with 3-meter-diameter tires priced upward of USD 50,000 per piece. Epiroc notes that two-third of its revenue already comes from service and parts, affirming sustained consumables demand[3]“Q1 2025 Presentation,” Epiroc Investor Relations, epiroc.com. Electrified haulage increases torque and regenerative-braking heat load, pushing tire makers to redesign compounds and steel-belt layouts. Elevated duty cycles shorten replacement intervals, enlarging the premium slice of the off the road tire market.

Accelerating Mechanization in Emerging-Market Agriculture

India sold almost 9 lakh tractors in 2024 , a record that signals how farm mechanization is reshaping rural equipment fleets. Government subsidies, higher MSPs, and favorable monsoons point to 1 million domestic tractor sales by 2026. Similar patterns surface in Indonesia and sub-Saharan Africa, where labor shortages elevate demand for higher-horsepower tractors. Each high-power tractor consumes more durable tires and a lifting unit value. Farmers increasingly specify radial and VF constructions to reduce soil compaction and fuel burn, propelling premiumization inside the OTR tire market. Subsidized credit schemes shorten replacement cycles, anchoring long-run aftermarket volumes.

OEM Shift to Telematics-Enabled Tire-as-a-Service Contracts

Goodyear’s TaaS program slashed U.S. last-mile fleet breakdowns by four-fifths and eliminated customer-owned tire inventory. By bundling sensors, analytics, and round-the-clock service, TaaS converts capital expense into predictable operating fees a value proposition resonating with large fleets. Continental’s integration of ContiConnect with Samsara extends these benefits to mixed equipment yards, creating fleet-wide visibility. As predictive alerts avert catastrophic failures, fleets are more willing to adopt premium tires that maximize carcass life, strengthening pricing power for technology-enabled suppliers and cementing long-term contracts that stabilize production planning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Natural-Rubber | -0.9% | Global, acute in Asia-dependent supply chains | Short term (≤ 2 years) |

| Supply-Chain Fragility | -0.5% | Global, concentrated in specialized equipment | Medium term (2-4 years) |

| Rising Competition From Retread and Tire-Leasing Specialists | -0.4% | North America, EU, mature Asia Pacific markets | Medium term (2-4 years) |

| Tightening Particulate-Emission Rules | -0.3% | Global, strict enforcement in North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural Rubber & Petro-Chemical Prices Squeezing Margins

Spot natural-rubber prices climbed one-fifth quarter-on-quarter in early 2025 as Thai and Indonesian plantations faced flood-induced yield losses. India ran a 550,000-tonne deficit, raising import costs for domestic tire makers like Apollo Tyres. Because OTR casings contain higher natural-rubber ratios than passenger tires, margin exposure is acute. Producers hedge through long-term offtake agreements and pivot to synthetic blends, but face parallel spikes in petrochemical feedstocks. R&D budgets now tilt toward bio-rubber and recycled compounds to buffer volatility. Yet, near-term cost pass-through remains constrained by fleet budgets, compressing EBITDA margins across the off the road tire market.

Supply-Chain Fragility for Large OTR Tire Molds & Curing Presses

Only a handful of machinery companies fabricate molds exceeding 4 meters in diameter, creating choke points. Ocean freight disruptions through the Red Sea and container shortages lengthen lead times, delaying capacity ramps for new-size introductions. Announced general rate increases on Asia–Europe lanes elevate landed costs for presses destined for greenfield plants. Some manufacturers raise safety-stock targets for critical spares, while others explore near-shoring partnerships to dilute single-source risk. High interest rates increase the hurdle rate for fresh capacity, potentially slowing supply growth against steady demand, which could inflate average selling prices within the off-the-road (OTR) tire market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tire Type: Radial Dominance Meets Solid Innovation

Radial constructions controlled 66.71% of the OTR tire market 2024, driven by superior heat management, longer tread life, and lower rolling resistance. Premium mines and mega-projects standardize radials to optimize fuel burn and reduce lifecycle cost. Solid tires, though only a niche in revenue terms, are expanding at a 4.65% CAGR as operators in scrap yards and underground mines prize puncture immunity over ride comfort. Goodyear’s hydrothermal recycling process, designed to source recovered carbon black from spent casings, exemplifies how sustainability overlays product development. Press-on solid bands, once confined to slow-moving forklifts, now appear on high-capacity wheel loaders thanks to dual-durometer cores that ease vibration. In parallel, bias designs persist in low-speed, low-budget jobs where acquisition price trumps total cost considerations, particularly in some African infrastructure projects funded by state budgets.

The strategic pitch among vendors is shifting from tread depth to data. Sensors embedded in radial products stream temperature and load profiles back to dashboards, granting fleet managers granular visibility into operating abuse. Consequently, premium radials with integrated IoT routinely command double-digit price premiums yet still lower total cost per operating hour. Solid-tire producers reply by touting zero downtime and simplified logistics no compressed-air tools required on site. This divergent value proposition sustains healthy rivalry inside the OTR tire market while opening cross-selling gateways as mixed fleets seek optimized fitments across duty cycles.

By Equipment Type: Earthmover Leadership Amid Loader Growth

Earthmovers generated 24.52% of the OTR tire market share in 2024, underscoring their centrality to mega civil works and open-pit mines. Each 250-ton truck consumes six ultra-large tires whose combined price tops USD 300,000 per change-out, making earthmovers a value-dense anchor for suppliers. In contrast, loader and dozer fitments are forecast to expand at a 4.78% CAGR as governments fast-track road repairs and port-side dredging. Caterpillar’s preview of an autonomous-ready Cat 775 showcases how drivetrain electrification is rewriting torque curves and, by extension, tire stress profiles. Vendors now co-design carcass geometry with OEMs to accommodate regenerative braking loads.

Forklifts and graders remain stalwarts of warehouse and road-finishing operations, respectively. Still, neither delivers the SKU complexity of the “Others” bucket terminal tractors, reach stackers, and material handlers used in logistics hubs. Automation here is advancing rapidly: APM Terminals ordered 240 electrified units across six countries, lifting port-equipment tire demand. Each new autonomous machine tends to run longer shifts, cycling through tires sooner, which magnifies aftermarket share within the broader OTR tire market.

By Rim Size: Compact Equipment Drives Mid-Size Growth

Wheels of less than 31 inches held 38.73% of the OTR tire share in 2024 because compact loaders, skid steers, and forklifts populate construction sites and warehouses worldwide. These segments prize maneuverability, and the corresponding tire dimensions remain highly standardized, allowing manufacturers to leverage scale for cost efficiency. Mid-range 41–45-inch rims are climbing at a 4.66% CAGR, reflecting the rise of medium excavators and articulated dump trucks that bridge the gap between compact and ultra-large machines. Metric low-profile sizes introduced on 29-inch rims improve ground stability, aligning with OEM calls for lower centers of gravity. Each step up in rim diameter lifts unit price and intensifies the pull on steel-cord supply chains as bead diameters widen.

Above 45 inches, ultra-class mining haulage remains a specialized niche but exerts outsized influence on profit pools: margins on these SKUs can exceed a quarter. Production capacity for such mammoth molds is scarce, reinforcing earlier supply-chain fragility. Vendors respond through modular die technology that allows incremental dimension changes without a complete mold replacement, compressing lead time and capital outlay. As fleets modernize, the center of gravity in rim-size distribution will keep drifting upward, lifting the premium mix inside the OTR tire market size over the forecast horizon.

By Industry Application: Construction Leadership Faces Port Surge

Construction consumed 37.18% of the OTR tire market share in 2024, reflecting ongoing beltways in India, solar farms in China, and high-rise clusters in the Gulf. Yet port operations are poised to outpace all other verticals with a 4.77% CAGR as global container trade rebounds and automation widens quay-side uptime windows. Suape in Brazil is launching Latin America’s first all-electric terminal, deploying reach stackers and yard tractors that require high-load-index tires engineered for instant torque. Mining remains a perennial heavyweight thanks to the commodity up-cycle, while agriculture supplies a steady pull driven by tractor sales in South Asia and emerging African markets.

Industrial users, steel mills, waste processors, and pulp-and-paper mills generate demand for specialized profiles that must resist high temperatures, chemicals, or metal debris. Vendors exploit this diversity by tailoring compounds with ozone stabilizers or fire-retardant ingredients, unlocking premium pricing. Cross-industry fleets often negotiate master supply agreements, encouraging manufacturers to harmonize pattern names and casing geometries across applications, simplifying inventory management and solidifying loyalty in an increasingly data-driven OTR tire market.

By Material Type: Natural Rubber Dominance Amid Reinforcement Innovation

Natural rubber delivered 56.47% of the OTR tire market share in 2024 revenue due to its unmatched tear resistance and heat dissipation vital for 50-ton axle loads in scorching mines. However, supply disruptions stimulate research into dandelion-based latex and recycled crumb. Continental now operates a CO₂-neutral plant in Lousado that blends dandelion-derived polymers into select OTR SKUs. Reinforcing materials, including steel cord, aramid, and hybrid composites, are advancing at a 4.75% CAGR as mines demand higher cut resistance and lower downtime. High-tenacity steel ropes with brass coating extend carcass life, while aramid overlays lighten the casing without sacrificing strength.

Synthetic rubber offers more consistent quality but faces its own petrochemical price headwinds. Rubber recyclers like Tyromer supply devulcanized crumb to Apollo Tyres, supporting a two-fifth recycled-content target by 2030. Such initiatives dovetail with ESG targets at mining majors, boosting the eco-label adoption. Suppliers that master material flexibility can mitigate raw-material shocks, safeguard margins, and differentiate in an increasingly sustainability-centric OTR tire market.

By Distribution Channel: Aftermarket Supremacy Sustains Growth

At 73.27% share, the aftermarket is the undisputed revenue engine of the OTR tire market, underpinned by three or more tire changes across a heavy machine’s life. It is also projected to grow at a robust CAGR of 4.68%. Bridgestone’s global field-engineering web of 130 service points illustrates how on-site support fortifies brand stickiness. AI-driven dashboards predict lug wear and schedule pit-lane swaps, slashing unplanned downtime. Digital storefronts further erode geographic barriers: Michelin’s acquisition of Tyroola in Australia exemplifies the push to merge e-commerce with brick-and-mortar networks.

OEM channels remain crucial for spec-in wins on new platforms but face inherent volume limitations tied to equipment sales cycles. TaaS blurs channel lines by embedding tire provisioning within holistic uptime contracts, migrating a portion of aftermarket revenue into subscription buckets. As fleets outsource risk to providers offering guaranteed cost per hour, loyalty is expected to tighten around data-enabled suppliers, reinforcing premium stratification within the OTR tire market.

Geography Analysis

Asia-Pacific held a 38.33% of the off the road tire market share in 2024, fueled by China’s construction juggernaut, India’s tractor boom, and Australia’s copper and iron-ore mines. Bridgestone’s expansion in India and a new satellite technology center in Pune underscore sustained regional investment. Southeast Asia diversifies manufacturing footprints away from China, generating incremental OE and aftermarket volumes. Energy-transition minerals in Western Australia keep ultra-class dump trucks running at high utilization, anchoring demand for 57-inch tires that weigh over 3 tons each.

The Middle East & Africa is the fastest climber, forecast at a 4.71% CAGR. Saudi Arabia’s massive pipeline covering NEOM, The Line, and the Red Sea resort complex demands continuous earthmoving and aggregate haulage. The UAE invests heavily in metro extensions, solar parks, and green-hydrogen plants, and expands its equipment fleets. In Africa, South Africa’s platinum mines and Zambia’s copper belt sustain premium OTR orders, while port upgrades from Lagos to Mombasa boost 41-45-inch rim-size uptake.

North America advances steadily on the back of the U.S. Infrastructure Investment and Jobs Act, which earmarks funding for roads and bridges, supporting replacement orders for graders and pavers. South America’s Andean copper and lithium ventures underpin robust demand despite political volatility, and Europe focuses on circular-economy mandates, steering procurement toward high-recycled-content tires. Collectively, these mature regions mix modest volume growth with higher ASPs, cushioning overall profitability in the global off the road tire market.

Mordor Intelligence provides coverage of the otr tire market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The market is moderately concentrated, the top five players hold a significant share, implying keen rivalry but room for regional specialists. Yokohama’s acquisition of Goodyear’s OTR business closed in February 2025, giving it immediate access to North American mining accounts. CEAT’s purchase of Camso broadens its SKU map in snow and agro-industrial niches. Bridgestone’s MASTERCORE line, now deployed in 100 mines, leverages proprietary steel cord to raise carcass life by a minimum.

White-space innovation centers on electrification-ready casings and predictive analytics platforms. BKT pilots blockchain tags for carcass traceability from the factory to the mine site. Continental is divesting ContiTech to sharpen its focus on tires, freeing capex for R&D in renewable materials.

Chinese entrants such as ZC Rubber invest heavily in a Mexican greenfield plant to skirt U.S. tariffs, putting incumbents under cost pressure. With a considerable amount of announced capex across the cohort, the race is on to blend sustainability, connectivity, and localized production into a compelling proposition for fleet managers navigating tight operating margins.

OTR Tire Industry Leaders

Bridgestone Corporation

Michelin

Continental AG

The Goodyear Tire & Rubber Company

Nokian Tyres plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Continental AG announced plans to spin off ContiTech, transforming itself into a pure-play tire manufacturer.

- February 2025: Yokohama Rubber finalized the USD 905 million purchase of Goodyear’s global OTR business.

Global OTR Tire Market Report Scope

| Radial OTR Tires |

| Bias OTR Tires |

| Solid OTR Tires |

| Earthmovers |

| Loaders & Dozers |

| Dump Trucks |

| Tractors |

| Forklifts |

| Graders |

| Others |

| Below 31 Inches |

| 31–40 Inches |

| 41–45 Inches |

| Above 45 Inches |

| Construction |

| Mining |

| Agriculture |

| Industrial |

| Port Operations |

| Others |

| Natural Rubber |

| Synthetic Rubber |

| Reinforcing Materials |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Tire Type | Radial OTR Tires | |

| Bias OTR Tires | ||

| Solid OTR Tires | ||

| By Equipment Type | Earthmovers | |

| Loaders & Dozers | ||

| Dump Trucks | ||

| Tractors | ||

| Forklifts | ||

| Graders | ||

| Others | ||

| By Rim Size | Below 31 Inches | |

| 31–40 Inches | ||

| 41–45 Inches | ||

| Above 45 Inches | ||

| By Industry / Application | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | ||

| Port Operations | ||

| Others | ||

| By Material Type | Natural Rubber | |

| Synthetic Rubber | ||

| Reinforcing Materials | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global OTR tire market in 2030?

The market is forecast to reach USD 32.81 billion by 2030, reflecting a 4.63% CAGR from 2025.

Which region is expanding the fastest for OTR tires?

The Middle East & Africa is the fastest-growing region, advancing at 4.71% CAGR through 2030 on giga-scale infrastructure and mining projects.

Why do radial OTR tires dominate equipment fitments?

Radials offer superior heat management, longer tread life, and lower rolling resistance, securing 66.71% share in 2024 across heavy mining and construction fleets.

How is tire-as-a-service changing procurement strategies?

TaaS bundles premium tires with telematics and maintenance, shifting costs from capital to operating budgets while cutting emergency breakdowns.

What impact does natural rubber volatility have on tire producers?

A 20% spike in rubber prices compressed margins in 2025, prompting manufacturers to hedge supply, explore bio-alternatives, and raise recycled content.

Which equipment category delivers the highest revenue in OTR tires?

Earthmovers hold the crown, accounting for 24.52% of 2024 revenue due to the high value of ultra-large haul-truck tires.

Page last updated on: