Tube Filling And Sealing Contract Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

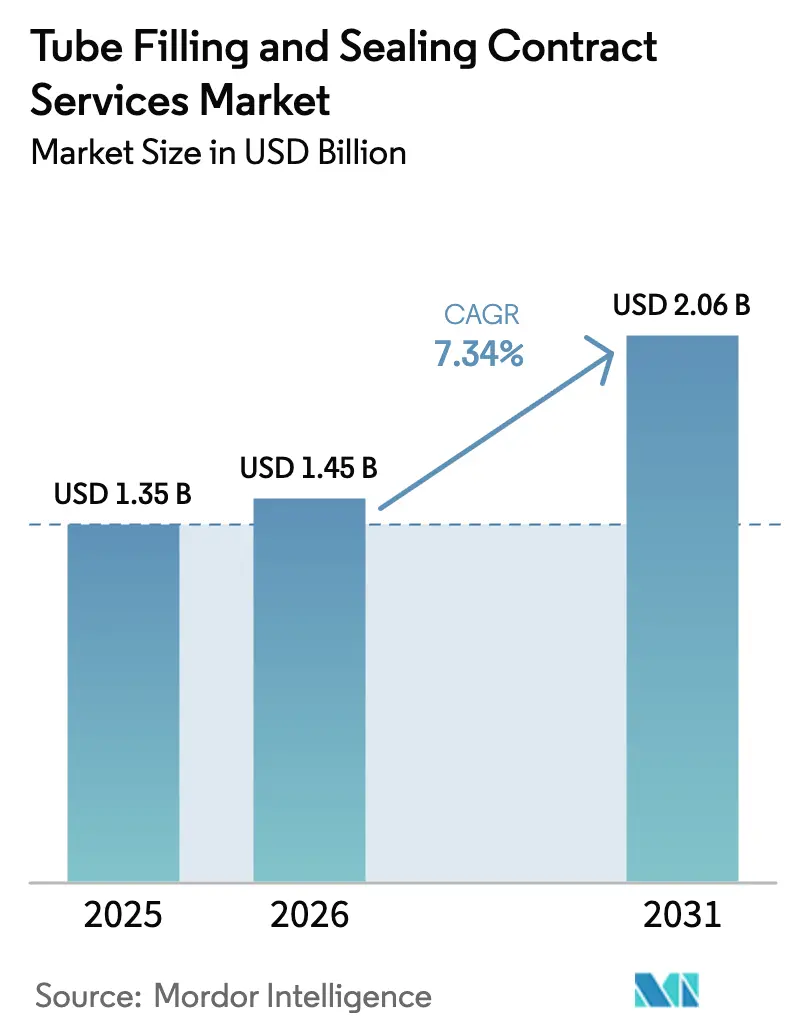

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 2.06 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tube Filling And Sealing Contract Services Market Analysis by Mordor Intelligence

The Tube Filling and Sealing Contract Services market size is expected to grow from USD 1.35 billion in 2025 to USD 1.45 billion in 2026 and is forecast to reach USD 2.06 billion by 2031 at 7.34% CAGR over 2026-2031. Across the forecast horizon, demand growth is underpinned by pharmaceutical companies outsourcing complex sterile packaging tasks, personal care brands premiumizing high-margin SKUs, and consumer goods firms upgrading to compliant, flexible production lines. Industry 4.0 automation is reducing minimum order quantities, enabling agile, on-demand production, and helping converters offset raw material volatility through real-time quality controls. Regulatory pressure to demonstrate both sterility and environmental stewardship is driving twin investment waves in aseptic technologies and recyclable laminate or aluminum tubes, respectively. The rising adoption of unit-dose packaging in dermatology, pain management, and oral gel therapies is further expanding the serviceable addressable market for sub-5 mL fills. Meanwhile, the sustained cost advantage of India and China is intensifying the shift of global packaging volume toward Asia-Pacific contract sites.

Key Report Takeaways

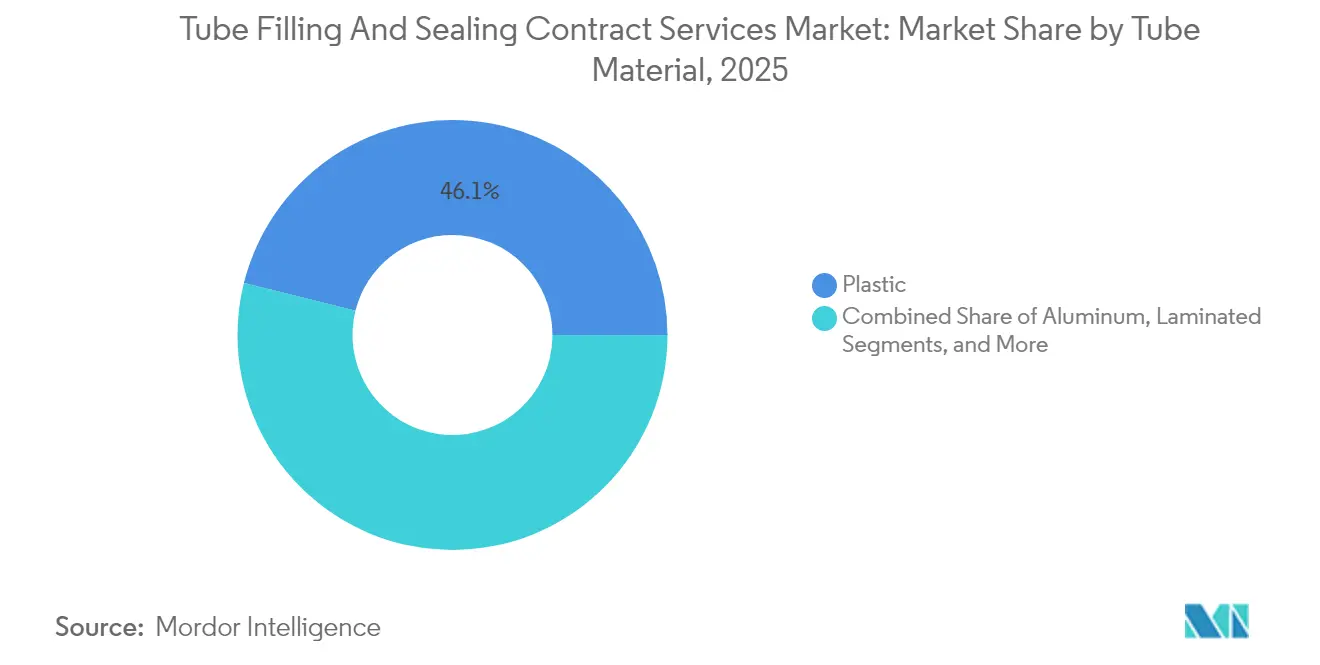

- By tube material, plastic tubes captured 46.12% of the Tube Filling and Sealing Contract Services Market share in 2025.

- By filling technology, Tube Filling and Sealing Contract Services Market size for ultrasonic-seal systems is projected to grow at 8.88% CAGR between 2026-2031.

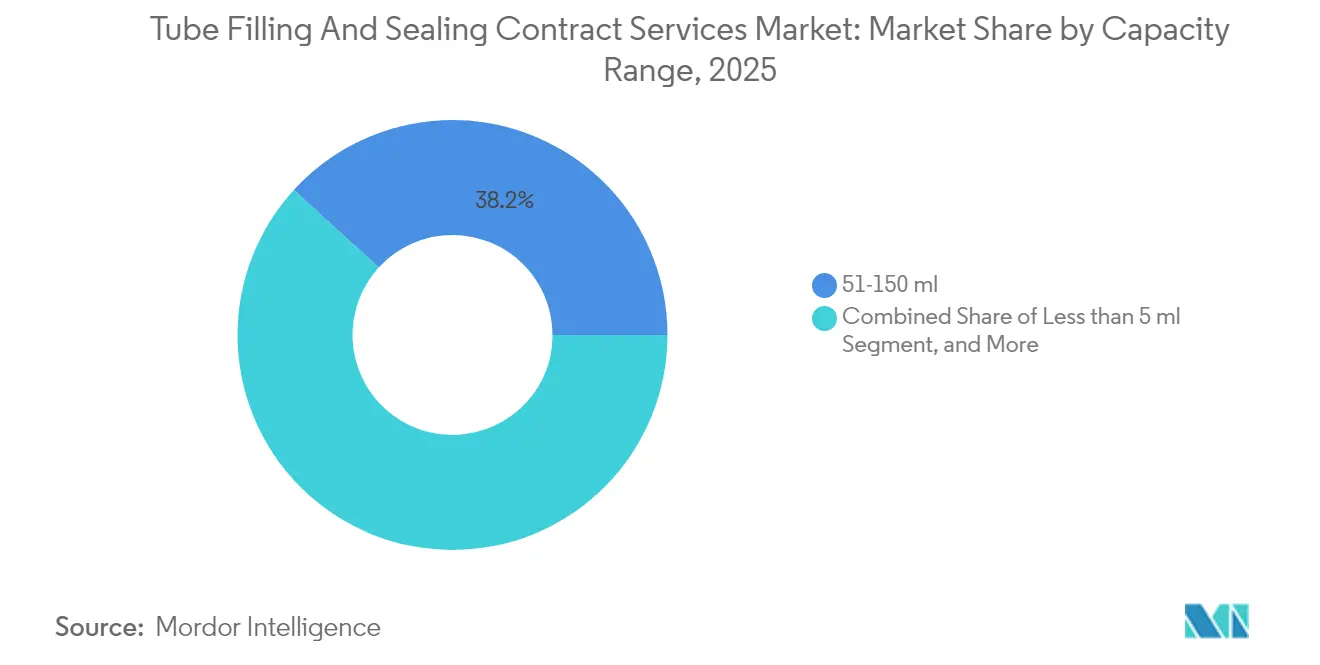

- By capacity range, the 51-150 ml band captured 38.21% of the Tube Filling and Sealing Contract Services Market share in 2025.

- By end-use, Tube Filling and Sealing Contract Services Market size for personal care and cosmetics is projected to grow at 9.61% CAGR between 2026-2031.

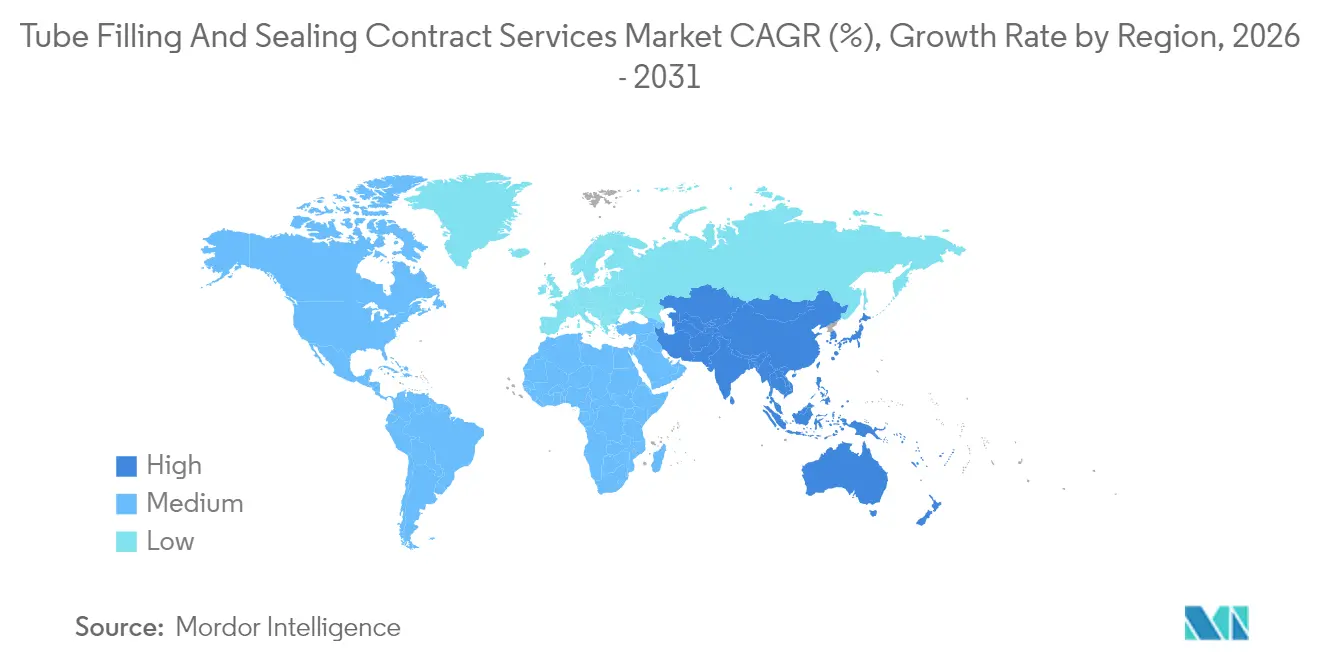

- By geography, North America captured 32.10% of the Tube Filling and Sealing Contract Services Market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tube Filling And Sealing Contract Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Single-Dose Topical and Oral Gels | +1.2% | Global, concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of Outsourced Pharma Manufacturing in Emerging Asia | +1.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Rise of Cosmetic Sachet-to-Tube Conversions | +0.9% | Global, early gains in Asia-Pacific urban markets | Short term (≤ 2 years) |

| Shift Toward Recyclable Laminate and Aluminum Tubes | +1.1% | Europe and North America leading, expanding globally | Medium term (2-4 years) |

| On-Demand Production Enabled by Industry 4.0 Lines | +1.3% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Regional SKU Proliferation in OTC Products | +0.7% | North America and Europe primary, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Single-Dose Topical and Oral Gels

Clinical preference for unit-dose formats is reshaping packaging specifications as dermatology and pain-relief molecules trend toward highly potent actives that require precise dosing. Contract packagers have seen a 40% rise in sub-5 mL job orders since 2024, with specialty pharma firms prioritizing sterility and accuracy for patient safety. FDA guidance that encourages the use of unit-dose containers for potent APIs accelerates vendor qualification cycles. As more indications shift to outpatient self-administration, single-use tubes also improve adherence and limit cross-contamination. The Tube Filling and Sealing Contract Services market benefits directly, capturing new revenue from low-volume, high-margin jobs. Equipment makers have responded by releasing micro-dose fillers capable of ±0.1 ml accuracy, which widens the capability gap between automated vendors and manual in-house operations.

Expansion of Outsourced Pharma Manufacturing in Emerging Asia

Asia-Pacific contract packagers sit at the intersection of large-scale generic drug production and favorable operating costs. Regional outsourcing value reached USD 45 billion in 2025, with tube-based secondary packaging growing as multinationals localize supply chains. Harmonized International Council for Harmonisation (ICH) standards in China reduce regulatory friction, prompting Western license holders to position late-stage fills in Shenzhen and Suzhou. India channeled USD 2.1 billion of FDI into new facilities in 2025, with 15% of the investment targeting tube filling lines that meet U.S. and EU audit criteria. Volume migration lowers cost-per-unit for sterile tubes by 18%, enabling brand owners to maintain gross margins when list prices are constrained. This structural shift ensures sustained mid-single-digit gains for the Tube Filling and Sealing Contract Services market throughout the decade.

On-Demand Production Enabled by Industry 4.0 Lines

Sensors, vision systems, and edge analytics now track fill weight, seal quality, and particulate counts in real-time, reducing batch reject rates by 30% and decreasing minimum order quantities by 60%. These gains unlock agile supply models where converters can switch formulations in under 15 minutes on servo-driven platforms. Pharmaceutical sponsors capitalize on lower safety stock levels, while indie cosmetic brands can validate niche SKUs without prohibitive setup fees. As more job quotes embed predictive maintenance data, buyers perceive lower operational risk and shift volume from manual lines. Continuous verification also streamlines FDA and EMA audits, supporting premium service fees that lift average selling prices for qualified providers.

Shift Toward Recyclable Laminate and Aluminum Tubes

Sustainability mandates from global consumer-goods majors dictate a rapid pivot to fully recyclable structures. Unilever’s 100% recyclable packaging goal for 2025 prompted contract packagers to invest USD 180 million in new laminate and aluminum lines in 2025.[1]Unilever, “Sustainable Packaging Progress Report 2025,” Unilever.comEuropean rules enforcing 30% recycled content by 2030 further pressure pharmaceutical and cosmetic owners to phase out non-compliant substrates. Early adopters currently command a 25% price premium, yet rising throughput is narrowing this differential. As raw-material certification frameworks mature, aluminum offers an extended shelf life without compromising recyclability, which is vital for oxygen-sensitive ointments. Over the medium term, the Tube Filling and Sealing Contract Services market sees higher capex but also thicker order backlogs tied to ESG-driven procurement policies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Pressure from Raw-Material Price Volatility | -0.8% | Global, acute impact in emerging markets | Short term (≤ 2 years) |

| Limited Availability of Pharma-Grade Clean-Room Capacity | -1.1% | Global, concentrated in established pharma hubs | Medium term (2-4 years) |

| High Validation Cost for Biologic-Grade Filling | -0.6% | North America and Europe primary impact | Long term (≥ 4 years) |

| Regulatory Delays for Novel Barrier-Film Substrates | -0.4% | Global, varying regional timelines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin Pressure from Raw-Material Price Volatility

Aluminum spot prices soared 35% on the London Metal Exchange in 2025, while resin contracts fluctuated by 22%, squeezing converters that operate under multi-month pharmaceutical agreements.[2]London Metal Exchange, “Aluminum Price Volatility and Industrial Impact Analysis,” LME.com Large CMOs (contract manufacturing organizations) hedge through long-dated swaps, but family-owned specialists often endure immediate margin erosion. Quarterly price-adjustment clauses help partially offset volatility, yet buyers resist surcharges on low-margin generics. Tighter spreads compel vendors to seek efficiency gains through the use of downgauged laminates and scrap-reduction analytics. Persistent volatility could cap upside for the Tube Filling and Sealing Contract Services market until commodity cycles stabilize.

Limited Availability of Pharma-Grade Clean-Room Capacity

Global ISO Class 7 rooms operated at 87% utilization in 2025, a level that constrains incremental aseptic-fill work. Construction costs have increased by 40% since 2024, primarily due to ventilation upgrades and staffing shortages for validation engineers. Lead times range from 12 to 18 months, delaying program launches for biologic APIs that require segregated Class-C corridors. Sponsors have begun dual-sourcing to mitigate capacity risk, but redundancy is limited because only a subset of CMOs pass FDA pre-approval inspections. The bottleneck raises slot-auction pricing, nudging formulators to weigh lyophilization or alternative containers that bypass sterile tubes. Until the clean-room build cycle catches up, capacity scarcity remains the single largest brake on the Tube Filling and Sealing Contract Services market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tube Material: Sustainability Upshift Drives Laminated Gains

Plastic retained a 46.12% share in 2025 due to cost-effectiveness across OTC creams and mainstream cosmetics. The Tube Filling and Sealing Contract Services market share for laminated structures is increasing due to EU recycling directives, with laminated tubes poised to grow at a 9.01% CAGR through 2031. Sustainability clauses are increasingly specifying multi-layer laminates with aluminum barriers that are thin enough for induction sorting yet robust enough to ensure peroxide-free shelf life.

Pharmaceutical sponsors that must protect oxygen-labile actives view laminated composites as a viable alternative to full aluminum, reducing the gross packaging cost by 18%. Laminated uptake also benefits from brand owners seeking metallic aesthetics without full-body foils. The Tube Filling and Sealing Contract Services market absorbs the transition smoothly because existing ultrasonic sealers can handle both HDPE and laminate formats with minimal tooling adjustments.

By Filling Technology: Aseptic Dominance with Ultrasonic Momentum

Aseptic filling contributed 41.18% of 2025 revenue and is expected to maintain its leadership position due to sterility mandates in topical antibiotics and ophthalmic gels. Ultrasonic sealing, however, records the sharpest 8.88% CAGR as its clean, low-heat process reduces char residue and micro-leak risk.

Adopters report a 30% cycle-time savings when pairing ultrasonic jaws with servo dribble fillers, enabling three SKU changeovers per shift instead of two. The Tube Filling and Sealing Contract Services market size for ultrasonic applications is expected to increase from USD 0.46 billion in 2025 to approximately USD 0.77 billion by 2031. Sponsors also prefer its lower energy draw, dovetailing with corporate sustainability scorecards.

By Capacity Range: Mini-Dose Lines Outpace Mid-Volume Workhorses

Mid-range 51-150 ml tubes, anchored by 38.21% of 2025 shipments, aligned with dermatology creams and mainstream shampoos. Sub-5 ml units, while small in tonnage, are growing at an 8.52% CAGR because high-potency APIs favor single-use delivery. CMOs have invested in no-drip micro-dose nozzles with a tolerance of ±0.1 ml, meeting FDA specifications for dose accuracy.

Profitability per linear foot of tubing is 40% higher than mid-range formats, supporting above-market margins. Going forward, the Tube Filling and Sealing Contract Services market size for sub-5 mL products is expected to expand the fastest as orphan drugs and premium cosmetic ampules proliferate.

By End-use Industry: Pharma Commands Wallet Share, Cosmetics Delivers Pace

Pharmaceuticals provided 52.05% of 2025 sales, leveraging stringent GMP and validation hurdles that favor specialist CMOs. Meanwhile, the personal care and cosmetics sector posts a 9.61% CAGR to 2031, driven by premium skin-care launches and influencer-driven demand for travel-friendly packaging.

Tube Filling and Sealing Contract Services market stakeholders are increasingly bundling formulation tweaks with packaging jobs to capture holistic value from independent brands. In the food and beverage industry, condiment pouches converting to mini-tubes support modest gains, but barrier concerns restrict the segment. Household chemicals stay volume-relevant for bleach gels but face competitive price ceilings that constrain margin potential.

Geography Analysis

North America accounted for 32.10% of 2025 revenue, driven by an FDA-regulated ecosystem that prioritizes traceability and rapid technical service. Capacity expansions in the United States and Canada in 2025 focus on ultrasonic retrofits and advanced vision inspection, reflecting a pivot toward high-potency, low-volume pharmaceutical work.

Europe maintains a robust presence in the premium cosmetics and Rx dermatology sectors, with Germany and France hosting several pilot plants utilizing recycled laminate materials. Regional sustainability statutes accelerate aluminum uptake and have spurred USD 50.85 million in capex for greener lines. The Tube Filling and Sealing Contract Services market size in Europe is expected to increase steadily, despite wage inflation, as ECM (external contract manufacturing) fees capture ESG (Environmental, Social, and Governance) premiums.

Asia-Pacific is the clear high-velocity frontier, charting a 9.43% CAGR to 2031 as contract service providers integrate into wider finishing complexes that include serialization and cold-chain kitting. India’s pharmaceutical exports hit USD 25 billion in 2025, with contract packaging forming 18% of value. [3]Asian Development Bank, “Pharmaceutical Manufacturing Investment Trends in Asia-Pacific,” ADB.org Chinese CMOs leverage regulatory convergence to funnel generic ointment business away from saturated Western plants. Southeast Asian nations such as Vietnam and Indonesia attract mid-tier cosmetics with duty-free regional distribution.

Competitive Landscape

The competitive arena features a blend of global CMOs with multi-continent footprints and regional specialists focused on niche formulations. The five largest players collectively hold approximately 38% of sector revenue, indicating moderate concentration. Scale confers purchasing leverage for aluminum and resin, while local champions thrive on flexible scheduling and white-glove regulatory support.

Automation investment remains the prime battleground. Catalent expanded its Singapore aseptic suite with ultrasonic modules that shorten release cycles for orphan drugs. Fareva’s acquisition of a North Carolina plant strengthens biopharma coverage in the U.S. southeast, providing redundant clean rooms essential for pandemic-era risk mitigation. Albea leverages its laminate heritage to upsell recyclable tubes tied to corporate ESG mandates, winning long-term contracts with beauty conglomerates.

Price competition intensifies in high-volume OTC segments where barrier requirements are moderate and switching costs are low. In contrast, biologic-grade projects erect high regulatory walls: ISO Class 5 isolators and 100% in-line vision verification raise capital thresholds beyond the reach of smaller entrants. Digital twins, augmented-reality maintenance, and cloud batch records differentiate advanced providers, accelerating vendor consolidation as smaller firms struggle to fund upgrades.

Tube Filling And Sealing Contract Services Industry Leaders

Silgan Holdings Inc.

Sonic Packaging Industries Inc.

LF of America Corp.

Unette Corporation

Dalton Chemical Laboratories Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Catalent Pharma Solutions completed a USD 85 million expansion in Singapore that lifts small-volume aseptic capacity by 40%.

- September 2025: Fareva Group acquired a North Carolina tube-filling plant for USD 120 million, adding validated clean-rooms for biologics.

- August 2025: Albea Contract Manufacturing launched a EUR 45 million (USD 50.85 million) recyclable laminate line in France.

- July 2025: Unicep Packaging implemented Industry 4.0 upgrades that trimmed changeover time by 50%.

Global Tube Filling And Sealing Contract Services Market Report Scope

| Plastic |

| Aluminum |

| Laminated |

| Metal |

| Hot-Fill |

| Aseptic-Fill |

| Vacuum-Fill |

| Ultrasonic-Seal |

| Less than 5 ml |

| 6-50 ml |

| 51-150 ml |

| More than 151 ml |

| Food and Beverage |

| Pharmaceuticals |

| Household and Institutional Care |

| Personal Care and Cosmetics |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Tube Material | Plastic | ||

| Aluminum | |||

| Laminated | |||

| Metal | |||

| By Filling Technology | Hot-Fill | ||

| Aseptic-Fill | |||

| Vacuum-Fill | |||

| Ultrasonic-Seal | |||

| By Capacity Range | Less than 5 ml | ||

| 6-50 ml | |||

| 51-150 ml | |||

| More than 151 ml | |||

| By End-use Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Household and Institutional Care | |||

| Personal Care and Cosmetics | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Tube Filling and Sealing Contract Services market in 2026?

The Tube Filling and Sealing Contract Services market size is expected to reach USD 1.45 billion by 2026.

What is the forecast for CAGR through 2031?

Aggregate revenue is expected to rise at a 7.34% CAGR by 2031.

Which tube material grows fastest by 2031?

Laminated tubes post the highest 9.01% CAGR, propelled by sustainability mandates.

Why is Asia-Pacific the fastest growing region?

Multinational firms tap cost-efficient, ICH-aligned plants in India and China, leading to a 9.43% regional CAGR.

What technology offers the quickest growth?

Ultrasonic sealing expands at 8.88% CAGR because it delivers superior seal integrity with lower heat exposure.

What restrains short-term growth?

Raw-material volatility, notably in aluminum and resins, compresses margins and moderates’ expansion.

Page last updated on: