Form-Fill-Seal (FFS) Packaging Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

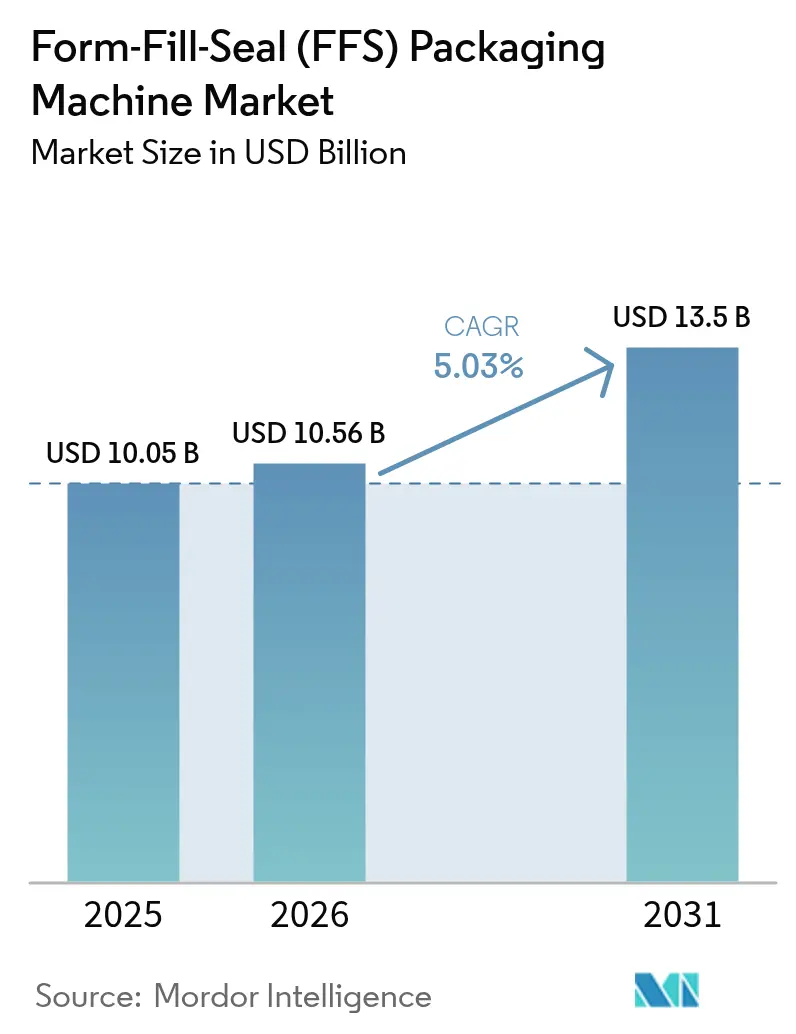

| Market Size (2026) | USD 10.56 Billion |

| Market Size (2031) | USD 13.5 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

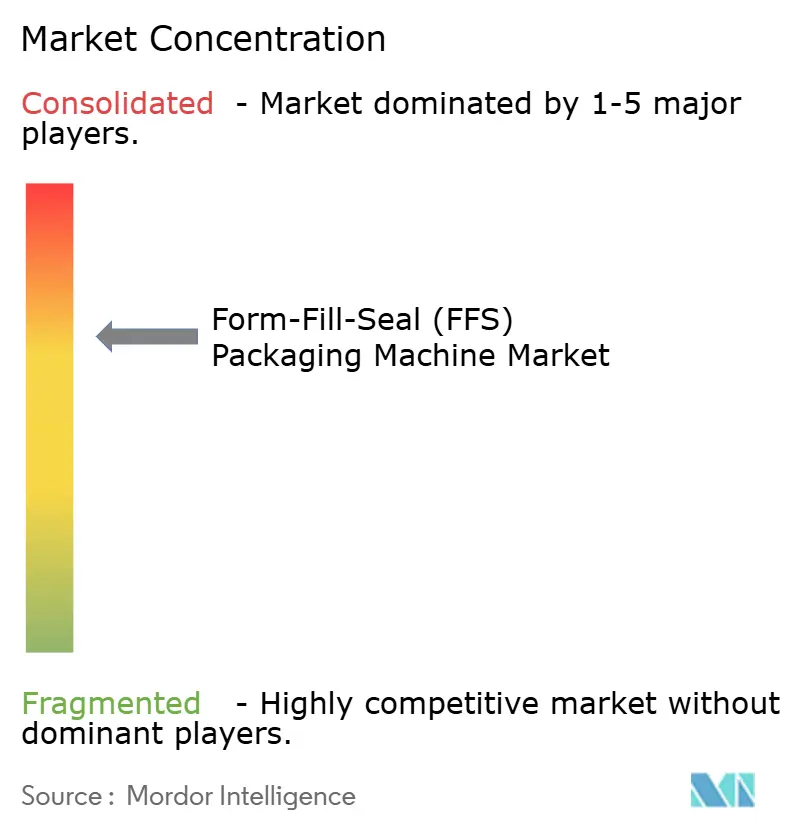

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Form-Fill-Seal (FFS) Packaging Machine Market Analysis by Mordor Intelligence

The form fill seal packaging machine market size is expected to grow from USD 10.05 billion in 2025 to USD 10.56 billion in 2026 and is forecast to reach USD 13.5 billion by 2031 at 5.03% CAGR over 2026-2031. Automation upgrades, regulatory pressure for aseptic processing, and sustainability mandates are reshaping investment priorities across pharmaceuticals, food, and emerging end-user segments. Edge-AI predictive maintenance modules have reduced unplanned downtime by up to 40%, improving total cost of ownership and accelerating replacement demand for legacy equipment. Meanwhile, tighter Extended Producer Responsibility rules in Europe are catalyzing a rapid shift toward recyclable mono-material films, altering equipment specifications and tooling requirements. Competitive intensity remains moderate as OEMs differentiate through digital features rather than price, while regional supply chains buffer currency volatility and input-cost swings.

Key Report Takeaways

- By equipment type, vertical form-fill-seal systems led with 57.83% of the form fill seal packaging machine market share in 2025; horizontal systems are projected to expand at a 6.58% CAGR through 2031.

- By automation level, fully-automatic units commanded 71.85% revenue share of the form fill seal packaging machine market in 2025, while the same segment is pacing a 6.05% CAGR to 2031 on the back of labor shortages and higher compliance demand.

- By material compatibility, polyethylene films accounted for 41.74% share of the form fill seal packaging machine market size in 2025; bioplastic and compostable films are set to grow at a 6.74% CAGR during 2026-2031 as sustainability rules tighten.

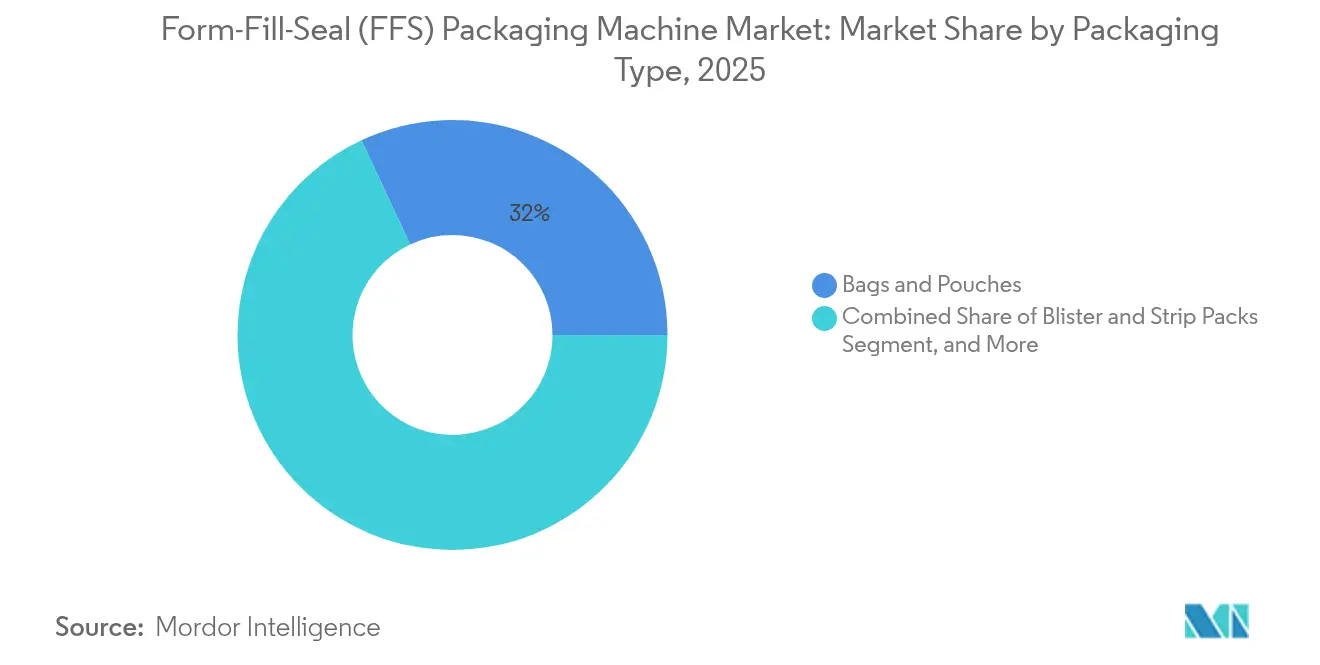

- By packaging type, bags and pouches held 31.96% of the form fill seal packaging machine market size in 2025, whereas blister and strip packs are moving ahead at a 6.62% CAGR to 2031 on rising demand for unit-dose integrity.

- By end-user industry, food and beverage applications represented 27.91% of the form fill seal packaging machine market in 2025, while pharmaceuticals and biologics are forecast to register the fastest 6.66% CAGR to 2031 as sterile formats scale.

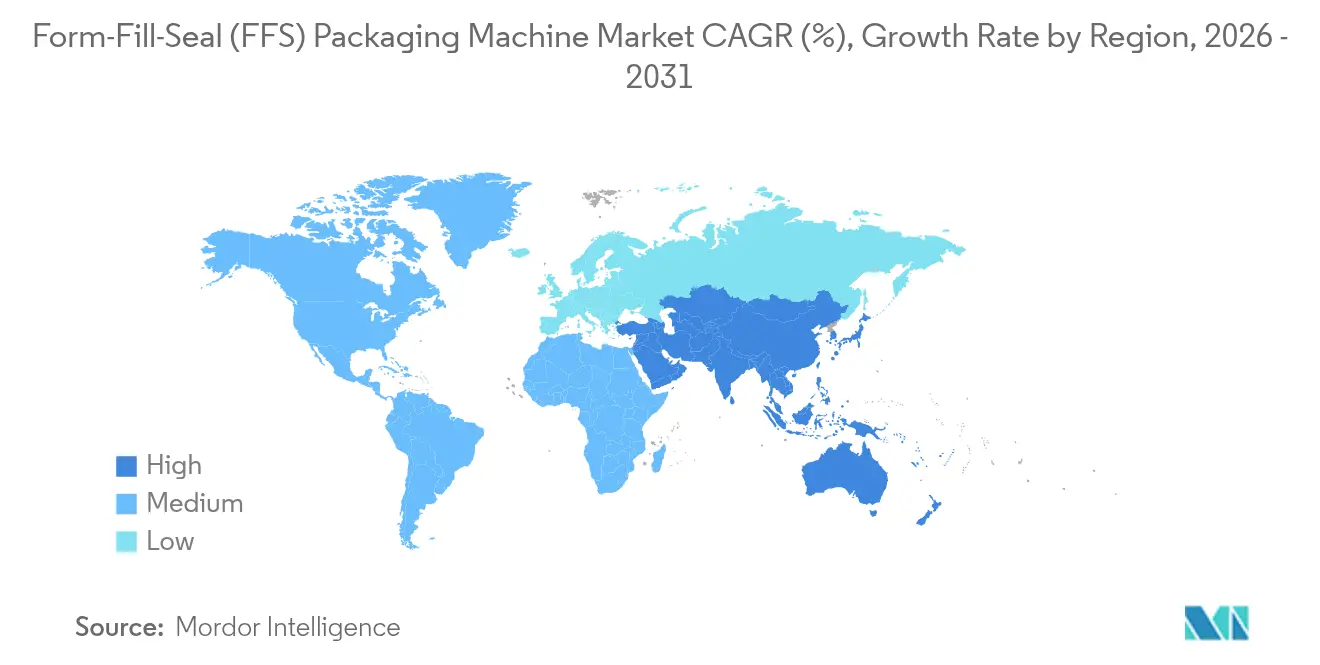

- By geography, Asia-Pacific retained the largest 39.75% slice of the form fill seal packaging machine market in 2025; Middle East and Africa emerge as the fastest-growing cluster at 7.25% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Form-Fill-Seal (FFS) Packaging Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for aseptic packaging in biologics and cell-gene therapy | +0.8% | North America and Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth of pet-food and veterinary nutraceutical brands | +0.6% | Global with strength in North America and Europe | Short term (≤ 2 years) |

| Sustainability-driven shift toward recyclable mono-material films | +0.7% | Europe leading, North America and Asia-Pacific following | Long term (≥ 4 years) |

| Surge in low-acidity ready-to-drink coffee launches | +0.4% | Global, urban markets | Short term (≤ 2 years) |

| Edge-AI enabled predictive maintenance modules | +0.5% | Developed markets first, emerging markets adoption | Medium term (2-4 years) |

| FMCG on-demand customization (late-stage differentiation) | +0.3% | Global, premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Aseptic Packaging in Biologics and Cell-Gene Therapy

Pharmaceutical manufacturers are scaling form fill seal systems that maintain sterility for highly sensitive biologics and cell-gene therapies. Ready-to-use containers lower contamination risks by 50% compared with conventional filling approaches, trimming batch rework and scrap. Syntegon’s SynTiso liquid line processes 600 containers per minute using contactless transport and real-time particle monitoring, demonstrating how OEMs embed European Annex 1 updates into machine design. The capital shift first gained traction in North America and Europe but is now spreading to Asian contract manufacturing hubs as regulatory convergence accelerates. These installations typically pair isolator technology with inline vision inspection, shortening validation cycles and easing FDA and EMA audit readiness. Heightened biologic throughput is translating into repeat orders for higher-speed systems, strengthening aftermarket parts and service backlogs for leading suppliers.

Growth of Pet-Food and Veterinary Nutraceutical Brands

Pet-humanization trends have sparked premium and therapeutic pet-food launches requiring portion-controlled pouches that preserve flavor volatiles and active nutraceutical ingredients. Specialty nutraceutical packs mandate child-resistant closures and tamper evidence, which favor servo-driven horizontal form fill seal configurations for precision dosing and seal integrity. Frequent recipe changes force manufacturers to seek equipment that enables tool-less changeovers and recipe upload through HMI presets, shaving downtime in short-run production. North American and European co-packers are spearheading this demand, but similar patterns are emerging in Brazil, South Korea, and urban India as disposable income and pet adoption rise. OEMs have responded by bundling recipe-management software with remote support contracts that guarantee uptime during seasonal demand peaks. Resultant volume growth is elevating installed-base renewals as converters upgrade from semi-automatic lines to fully-automatic platforms with integrated leak detection.

Sustainability-Driven Shift Toward Recyclable Mono-Material Films

European Extended Producer Responsibility statutes have turbocharged interest in mono-polyolefin laminates that can enter existing curbside recycling streams. Flexible sealing-jaw research shows these films seal at lower temperatures, reducing energy use and preserving barrier performance. Equipment retrofits now focus on specialized forming collars and multi-zone heaters that compensate for narrower thermal windows. Brand owners in personal care and snacks are moving fully to mono-material structures by 2027, forcing contract packagers on both sides of the Atlantic to re-qualify every SKU. The learning-curve effect is encouraging collaborative trials between film suppliers and machinery OEMs that shorten time to commercial scale. By aligning with global recyclability guidelines, converters also future-proof investments against prospective carbon taxes on multilayers, multiplying replacement orders within the existing installed base.

Edge-AI Enabled Predictive Maintenance Reduces Downtime

Embedded sensors and edge analytics are migrating from pilot projects to standard specifications on premium form fill seal models, allowing continuous vibration, temperature, and torque monitoring. Machine-learning algorithms benchmark live data against historical baselines, signaling bearing wear or misalignment hours before catastrophic failure. Users report up to 40% cuts in unplanned stoppages and 15% drop in spare-parts inventory, strengthening the business case for full automation. Cloud-connected dashboards provide OEM technicians with diagnostic readouts, facilitating remote fixes and reducing technician dispatch costs. Early adopters are typically pharmaceutical and high-volume snack players, yet OEMs now offer subscription-based models to mid-tier packers, democratizing access to predictive insights. The technology’s spread supports longer amortization cycles and premium service revenue, nudging OEM competition toward software ecosystems rather than hardware alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneconomical for low-density products | -0.4% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Skilled-labor shortage for advanced servo systems | -0.6% | Developed markets spreading to emerging economies | Short term (≤ 2 years) |

| Volatility in polymer-resin prices | -0.5% | Global, supply-chain dependent | Short term (≤ 2 years) |

| Rising carbon-tax regimes on multilayer films | -0.3% | Europe leading, expanding globally | Medium term |

| Source: Mordor Intelligence | |||

Uneconomical for Low-Density Products

Form fill seal systems face unfavorable economics when handling powders or extruded snacks with bulk densities below 0.3 g/cm³, as film consumption per unit weight rises sharply. Material expenditure can surpass 15% of product value, eroding margin in price-sensitive developing markets. Carton and woven-sack alternatives sometimes deliver lower cost-per-kilogram despite reduced shelf appeal, prompting regional brand owners to delay capex for form fill seal lines. OEMs are tackling the barrier by introducing tubular designs that eliminate side seams and optimize vertical pitch, yet adoption remains tepid where resin prices and currency fluctuations squeeze EBIT. Consequently, the restraint exerts a long-run drag on aggregate equipment replacement in emerging economies reliant on low-density staples.

Skilled-Labor Shortage for Advanced Servo Systems

Vacancy rates above 25% for mechatronics technicians continue to plague high-automation plants across North America and Western Europe, delaying commissioning schedules and inflating maintenance budgets. Workforce gaps widen as legacy mechanics retire and vocational programs lag in digital curriculum. Advanced form fill seal platforms now integrate augmented-reality overlays and guided maintenance apps, but these aids cannot fully offset scarce human expertise for servo tuning and PLC troubleshooting. OEMs run regional academies and virtual-twin simulators to accelerate training; however, poaching among co-packers sustains churn. The constraint keeps some mid-market firms on semi-automatic setups longer than planned, tempering near-term unit growth despite favorable ROI models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: VFFS Dominance Faces HFFS Challenge

Vertical systems controlled 57.83% of the form fill seal packaging machine market in 2025, leveraging versatility for granular foods, powders, and industrial products. The form fill seal packaging machine market size for horizontal machines is projected to climb at a faster 6.58% CAGR to 2031 as pharmaceutical and high-barrier snack applications prefer their flat web geometry for even heat distribution. Finite-element-optimized forming collars have improved VFFS seal quality, mitigating product-in-seal defects and sustaining leadership. Yet HFFS configurations enable cleaner product paths and contactless transport that align with Annex 1 revisions, prompting premium drug-filler segments to migrate. Multinational brands often keep a dual-fleet strategy, deploying VFFS for mainstream SKUs while reserving HFFS for value-added formats.

Adoption choices pivot on hygiene class, pack style, and line-speed targets rather than pure cost. HFFS reels usually carry higher barrier coatings, enabling shelf-life parity at thinner gauges and partially neutralizing material-cost disadvantages. Cross-training operators across both formats remains a challenge, nudging OEMs toward common HMI frameworks that lower learning curves. Consequently, the VFFS stronghold will erode slightly through 2031, although absolute shipments rise in line with expanding sachet demand in Asia.

By Automation Level: Full Automation Gains Ground

Fully-automatic lines captured 71.85% revenue in 2025 as labor scarcity and stricter hygiene requirements tilted purchasing decisions toward touchless operation. This segment will outpace the broader form fill seal packaging machine market at a 6.05% CAGR, fueled by edge-AI diagnostics that guarantee uptime contracts. Semi-automatic lines persist in specialty runs and developing-nation SMEs where capex constraints and small lot sizes dominate. However, modular control architectures now offer staged upgrades, allowing users to retrofit weighers, pick-and-place robots, and servo axes without wholesale replacement.

IoT dashboards supply OEE metrics that plant managers leverage to justify continuous-improvement bonuses, anchoring management buy-in. Moreover, e-commerce sizing constraints favor dimensional consistency achievable only with closed-loop motion control, further nudging migration upward. Nonetheless, a residual serviceable market for manual loading and bagging continues in bulk agricultural produce where product variability challenges camera-based inspection.

By Material Compatibility: Bioplastics Challenge PE

Polyethylene retained 41.74% share in 2025, anchored by global resin availability and established heat-seal windows. The form fill seal packaging machine market size linked to bioplastic films is set to expand at 6.74% CAGR through 2031 as legislation mandates recyclable or compostable solutions. Mono-polyolefin and paper-based laminates necessitate revamped forming sets and multi-zone sealing bars, spurring retrofit revenue. Early adopter case studies in snack and personal-care SKUs document 5-10°C lower seal temperatures that reduce energy consumption and shrink bag distortion risk.

Still, supply continuity for certified compostable resins lags demand, posing risk for launch timelines. Equipment makers are forming consortia with film extruders and converters to co-develop sealing-profile libraries, shortening factory-acceptance testing. Down-gauging now intersects with sustainability goals, but excessive thinning threatens barrier integrity, underscoring the importance of precision heater profiling enabled by servo pressure controls.

By Packaging Type: Specialized Formats Accelerate

Bags and pouches delivered 31.96% of segment revenue in 2025, favored for cereal, confectionery, and fertilizer packs that reward film-to-product ratios. Blister and strip packs, though smaller in base, will register a 6.62% CAGR as biologics, probiotics, and high-value functional foods adopt unit-dose regimens. Stick packs and sachets bridge convenience and precise dosing, commanding incremental line speeds above 400 packs per minute on new servo-axis designs. Aseptic bottles and ampoules increasingly emerge from form fill seal platforms that thermoform barrier polypropylene, sterilize in-line, and cut containers in a single pass, bypassing downstream depalletizing.

Sustainability overlays further push innovation in tray and lid stock, with paper fiber trays heat-sealed by low-gauge PE lidding films now tested for yogurt and dairy desserts. CGI-driven design tools help converters simulate corner fold-over stress, minimizing crack propagation in recyclable paper-poly structures. Accordingly, packaging-type diversification acts as a durable driver for line extensions.

By End-User Industry: Pharmaceuticals Surge Ahead

Food and beverage maintained 27.91% share in 2025, underpinned by continuous demand for staples and impulse snacks. Pharmaceuticals and biologics will expand at a 6.66% CAGR to 2031, boosting the form fill seal packaging machine market share of sterile formats as contract development and manufacturing organizations scale high-potency pipelines. Veterinary nutraceuticals and premium pet-foods carve double-digit gains, absorbing flexible-foil costs through premium retail pricing. Home and personal-care players eye dissolvable-strip formats for concentrated cleansers, routing capex toward multi-lane stick-pack lines.

Industrial bulk goods, including construction chemicals and seed coatings, gravitate toward heavy-duty gusseted bags where multi-pass heat sealing ensures drop-impact resistance. That variety of end-use cases underscores the platform’s adaptability, reinforcing OEM service diversity from sterilizable stainless-steel modules to ruggedized IP-rated enclosures.

Geography Analysis

Asia-Pacific retained the largest 39.75% slice of the form fill seal packaging machine market in 2025, propelled by rising urban consumption and export-oriented manufacturing bases across China, India, and Vietnam. Policy incentives for localized pharma production in India and tax benefits for automation in China catalyze fresh capacity, while growing snack exports from Thailand and Indonesia add mid-speed line demand. Domestic film extrusion clusters enable fast supply loops, tempering currency risk on imported consumables.

North America and Europe uphold technology leadership through high-precision and sustainable packaging agendas. Both regions engage in replacement, not green-field, cycles: U.S. operators invest in edge-AI retrofits and robotics to offset labor turnover, whereas European plants allocate capex to mono-material compatibility and energy-efficient heaters. Their mature regulatory frameworks accelerate Annex 1-compliant isolators and real-time release testing, locking in premium margins for specialized OEMs.

Middle East and Africa emerge as the fastest-growing cluster at 7.25% CAGR to 2031 as regional pharma hubs in Saudi Arabia, Egypt, and South Africa localize generic production. Infrastructure upgrades in cold-chain logistics draw additional demand for aseptic pouching lines, while rising disposable income supports packaged snacks and RTD coffee launches. Equipment suppliers win orders through turnkey support, including operator training and after-sales stocking, to counter limited local skill pools. Collectively, geographic diversification cushions cyclical swings, granting the form fill seal packaging machine market a balanced global growth runway.

Competitive Landscape

The form fill seal packaging machine market hosts a mid-level concentration where the top five OEMs control roughly 55-60% of global revenue. European manufacturers such as Syntegon, IMA, and Marchesini dominate pharmaceutical and aseptic niches with GMP-certified stainless-steel portfolios. U.S.-based ProMach and Barry-Wehmiller emphasize modular integration and robust aftermarket services, anchoring North American share. Chinese producers, including Foshan Coretamp, win high-volume snack and condiment orders by bundling entry-level automation at attractive price points.

Strategic trajectories revolve around digitalization, with leading firms rolling out subscription-based analytics platforms that bundle predictive maintenance and parts-inventory optimization. Patent filings in forming collar geometry and sealing-bar micro-texture exhibit mechanical innovation, yet competitive edges increasingly rest on software ecosystems that elevate overall equipment effectiveness metrics. M&A activity trends toward vertical-integration plays, such as film suppliers acquiring machinery builders to offer closed-loop trials for recyclable structures.

Regional after-sales footprints turn into key differentiators as spare-parts lead times influence OEE. Italian OEMs leverage regional partnerships to stage critical spares in Dubai and Singapore, minimizing customs delays. Meanwhile, U.S. firms cultivate cloud-based digital twins that enable line-simulation studies for SKU changeovers, shortening project cycles. As a result, technology capabilities rather than sheer scale decide market leadership, sustaining moderate concentration.

Form-Fill-Seal (FFS) Packaging Machine Industry Leaders

Syntegon Technology GmbH

ProMach Inc.

SACMI Imola S.C.

Winpak Ltd.

Mespack S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Syntegon launched the SynTiso liquid pharmaceutical filling line concept at Pharmatag 2025, integrating contactless suspended transport and real-time particle monitoring for 600 containers per minute throughput.

- April 2025: Graphic Packaging International and Mother Parkers Tea and Coffee introduced Boardio paperboard canisters that cut inbound truck volume 94% and reduce plastic by 50% versus composite bags.

- March 2025: WEPACK 2025 in Shanghai expanded to 140,000 m² and 1,500 exhibitors, spotlighting intelligent and sustainable packaging across seven co-located shows.

- December 2024: Westrock Coffee installed three automated RTD lines in Conway, Arkansas, including a PET ESL line for six-month refrigerated shelf life.

Global Form-Fill-Seal (FFS) Packaging Machine Market Report Scope

Form-fill-seal (FFS) machines are a type of packaging machinery that completes the entire packaging process, including forming, filling, and sealing, in a single operation. These machines primarily come in two variants: vertical form-fill-seal (VFFS) and horizontal form-fill-seal (HFFS). The latter encompasses a range of horizontal machines, including flow-wrappers, sachet machines, blister pack machines, four-side seal machines, and thermoform fill and seal machines. FFS machines work by pulling packaging material from a roll, shaping it, and then sealing it. Subsequently, the formed bags or packs are filled, sealed, and finally separated.

The form-fill-seal (FFS) packaging machine market is segmented by equipment type (vertical form-fill-seal equipment and horizontal form-fill-seal equipment) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Vertical Form-Fill-Seal (VFFS) |

| Horizontal Form-Fill-Seal (HFFS) |

| Fully-Automatic |

| Semi-Automatic |

| Polyethylene (PE) Films |

| Polypropylene (PP) Films |

| Bioplastic and Compostable Films |

| Aluminum-Laminate and Barrier Films |

| Bags and Pouches |

| Sachets and Stick Packs |

| Aseptic Bottles and Ampoules |

| Blister and Strip Packs |

| Other Packaging Types |

| Food and Beverage |

| Pharmaceuticals and Biologics |

| Pet Food and Veterinary |

| Home and Personal Care |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Equipment Type | Vertical Form-Fill-Seal (VFFS) | ||

| Horizontal Form-Fill-Seal (HFFS) | |||

| By Automation Level | Fully-Automatic | ||

| Semi-Automatic | |||

| By Material Compatibility | Polyethylene (PE) Films | ||

| Polypropylene (PP) Films | |||

| Bioplastic and Compostable Films | |||

| Aluminum-Laminate and Barrier Films | |||

| By Packaging Type | Bags and Pouches | ||

| Sachets and Stick Packs | |||

| Aseptic Bottles and Ampoules | |||

| Blister and Strip Packs | |||

| Other Packaging Types | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceuticals and Biologics | |||

| Pet Food and Veterinary | |||

| Home and Personal Care | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the form fill seal packaging machine market in 2026?

It is valued at USD 10.56 billion and projected to reach USD 13.5 billion by 2031.

What is driving new equipment orders in pharmaceuticals?

Sterile manufacturing for biologics and cell-gene therapies requires Annex 1-compliant lines, lifting demand for aseptic form fill seal machines.

Which region is expanding fastest?

Middle East and Africa are forecast to grow at 7.25% CAGR through 2031 on rising pharma and consumer-goods capacity.

Which region has the biggest share in Form-Fill-Seal Packaging Machine Market?

In 2025, the Asia-Pacific accounts for the largest market share in Form-Fill-Seal Packaging Machine Market.

How are sustainability goals affecting material choices?

Brand owners are shifting from multilayer barrier films to recyclable mono-polyolefin or paper laminates, prompting machine retrofits for new sealing profiles.

What role does edge-AI play in maintenance?

Embedded analytics cut unplanned downtime by up to 40%, enhancing OEE and lowering total cost of ownership for automated lines.

Why is labor availability a restraint?

Technician shortages for advanced servo systems delay commissioning and raise maintenance costs, particularly in North America and Europe.

Page last updated on: