Vertical Form Fill Seal Automation For Liquid Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

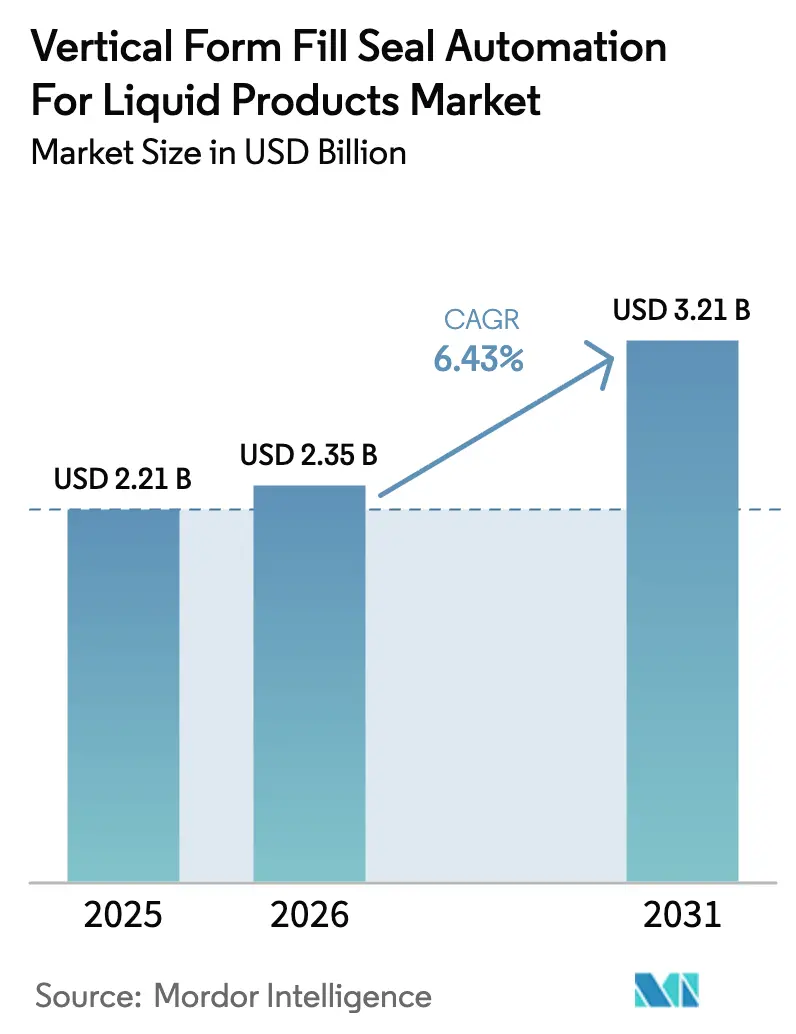

| Market Size (2026) | USD 2.35 Billion |

| Market Size (2031) | USD 3.21 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

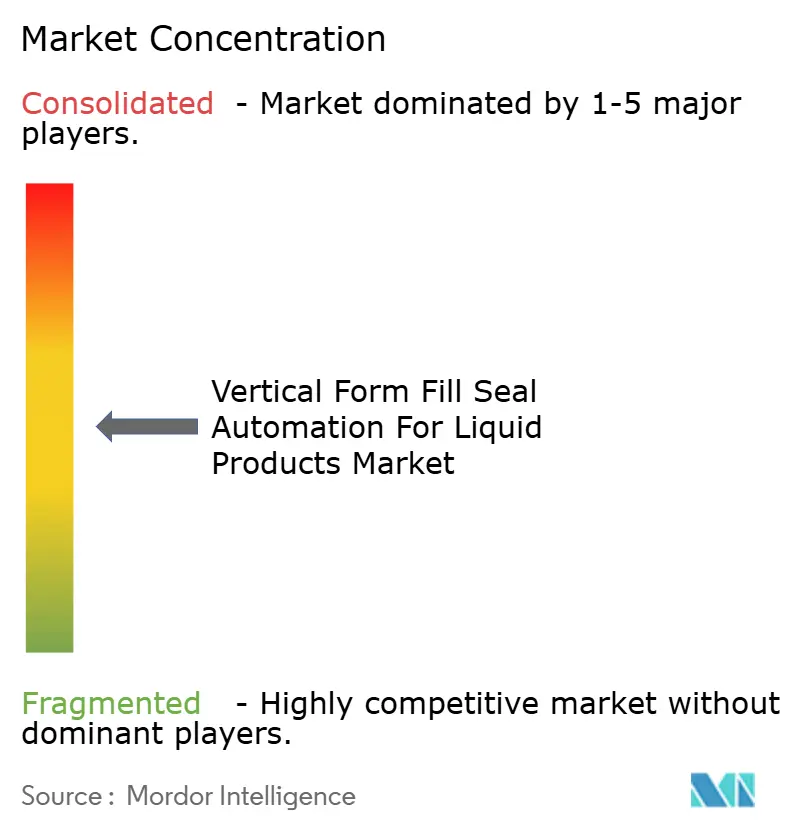

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vertical Form Fill Seal Automation For Liquid Products Market Analysis by Mordor Intelligence

The Vertical Form Fill Seal Automation For Liquid Products Market size was valued at USD 2.21 billion in 2025 and estimated to grow from USD 2.35 billion in 2026 to reach USD 3.21 billion by 2031, at a CAGR of 6.43% during the forecast period (2026-2031). Demand accelerates as brand owners automate filling and sealing lines to offset global labor shortages, comply with stricter hygiene rules, and satisfy consumers who favor single-serve packs for dairy, beverages, sauces, and health products. Asia-Pacific leads adoption thanks to lower operating costs, a deep contract-packing base, and rapid supermarket penetration across emerging economies. Suppliers also benefit from government incentives that localize food and pharmaceutical value chains, a strategic priority following pandemic-era disruptions. In mature regions, technology upgrades rather than greenfield installations propel growth-particularly around aseptic dosing, digital twin monitoring, and recyclable mono-material films that meet new sustainability mandates. Competition remains moderate because several mid-sized machinery builders coexist beside diversified packaging groups; partnerships and small acquisitions help both sides combine servo hardware, robotics, and cloud software more quickly.

Key Report Takeaways

- By machine type, intermittent motion systems held 45.38% of vertical form fill seal automation for liquid products market share in 2025, while aseptic VFFS units are forecast to expand at an 11.23% CAGR through 2031.

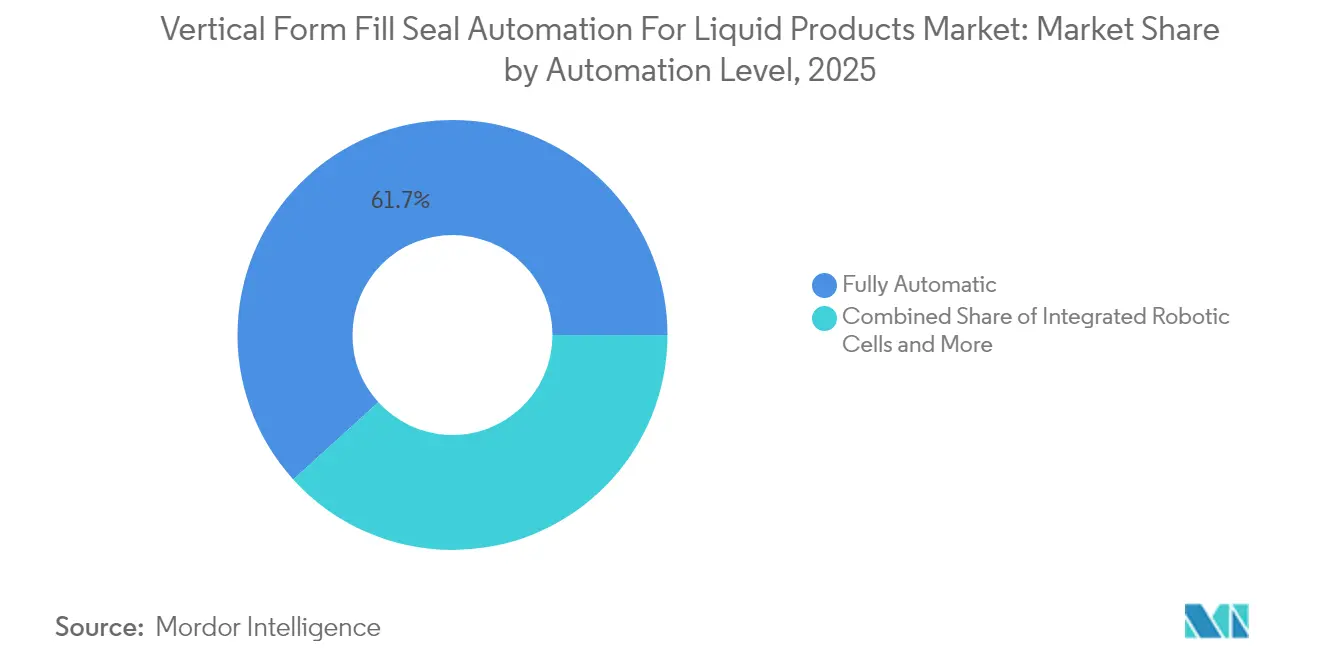

- By automation level, fully automatic lines accounted for 61.72% of the vertical form fill seal automation for liquid products market size in 2025; integrated robotic cells post the fastest projected CAGR at 13.34% through 2031.

- By filling technology, gravity fill captured 37.61% of the vertical form fill seal automation for liquid products market size in 2025, whereas aseptic fill will lift at a 11.98% CAGR to 2031.

- By packaging material, polyethylene films led with 40.77% revenue share in 2025; biodegradable films are on course for a 12.47% CAGR, the segment-high pace to 2031.

- By end-use, dairy products dominated with 29.62% share of the vertical form fill seal automation for liquid products market size in 2025, but pharmaceuticals and nutraceuticals head for a 11.56% CAGR through 2031.

- By geography, Asia-Pacific commanded 34.12% share in 2025, while the Middle East is projected to log the fastest 10.31% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vertical Form Fill Seal Automation For Liquid Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift toward Single-Serve Liquid Portions | +1.2% | North America and Europe first, global later | Medium term (2-4 years) |

| Growth of Aseptic Filling to Reduce Cold-Chain Costs | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| SKU Proliferation in Functional Beverage Space | +0.9% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Push for Recyclable Mono-Material Films | +0.8% | European Union primary, North America following | Long term (≥ 4 years) |

| Digital Twin-Enabled OEE Optimization | +0.7% | Global, led by advanced manufacturing hubs | Medium term (2-4 years) |

| Rising Demand from Contract Packers in Emerging Asia | +0.6% | Asia-Pacific, notably China and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Single-Serve Liquid Portions

Growing interest in portion control drives brand owners to pack yogurts, functional drinks, and condiments in 30-100 ml units consumers can carry on the go. Smaller fill volumes demand tighter volumetric accuracy, faster sealing jaws, and advanced motion control to keep throughput above 150 packs per minute. Aseptic variants gain particular traction because they drop preservatives yet secure shelf stability, a key message for clean-label shoppers. Major beverage fillers funded new VFFS lines in 2024 to secure single-serve capability across Europe and Oceania.[1]Shamil Ramazanov, “TNA Solutions to Demonstrate How Automation in the Production Line Can Ease Labor Shortages at SNAXPO 2025,” PotatoPro, potatopro.com Brands without such flexibility risk losing shelf facings to rivals able to switch pouch sizes overnight.

Growth of Aseptic Filling to Reduce Cold-Chain Costs

Aseptic dosing lets liquid products travel and store at ambient temperatures, removing refrigerated truck fees that can reach 18% of total logistics spend in emerging economies. Producers in Southeast Asia now distribute dairy-based nutrition shakes to inland regions where cold rooms are scarce, growing revenue without building expensive infrastructure. Equipment suppliers integrate sterile chambers, in-line hydrogen peroxide tunnels, and non-contact fillers into a single chassis, cutting floor space by 20%.[2]“Layout 1,” Innovations in Food Processing and Packaging, innovationsfood.com Regulatory authorities in India and the Gulf recognize aseptic packaging as compliant with HACCP, widening adoption.

SKU Proliferation in Functional Beverage Space

Functional beverage launches jumped throughout 2024 as start-ups marketed immunity, collagen, and plant-protein drinks. Contract packers face ten or more recipes per day, each with different viscosity and foaming behavior. Modern VFFS lines employ recipe-driven servo pumps and ultrasonic cold seals that eliminate the 15-minute heat-bar warm-up common on older equipment, yielding first-bag quality immediately after changeover. Downtime savings exceed USD 30,000 per hour on high-volume fillers, a compelling economic argument for automation investment.

Regulatory Push for Recyclable Mono-Material Films

European rules set minimum recycled content and restrict multilayer laminates because they hinder mechanical recycling. Film suppliers now co-extrude polyethylene layers with EVOH barrier while VFFS builders optimize sealing temperatures to compensate for narrower heat windows. Early adopters secure compliance before enforcement and win contracts from retailers championing circular-economy goals. Successful pilot projects show 100% recyclable pouches survive drop tests at 4 m and reach speeds of 300 pouches per minute without seal failure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX Versus Horizontal Alternatives | -1.4% | Global, strongest for small and medium firms | Short term (≤ 2 years) |

| Volatility in Polymer Film Prices | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Shortage of Skilled Maintenance Technicians | -0.7% | North America and Europe | Medium term (2-4 years) |

| Clean-in-Place Validation Complexity for Multi-Viscosity Lines | -0.5% | Global, concentrated in pharma applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX Versus Horizontal Alternatives

An entry-level intermittent VFFS liquid system can cost 25%-40% more than a horizontal pouch filler once ancillary conveyors, fillers, and inspection units are added. Small contract packers often defer upgrades even though they struggle to recruit line operators, citing multi-year payback horizons. Industry surveys taken in 2025 again show 78% of packagers list capital affordability as the main hurdle to wider automation.[3]Casey Flanagan, “The Packaging Workforce: Hiring, Retention, and Training in a Changing Industry,” Packaging World, packworld.com Banks and leasing companies have begun offering outcome-based finance, but acceptance remains slow.

Volatility in Polymer Film Prices

Resin markets swung sharply after Red Sea shipping disruptions lifted freight rates and limited raw-material availability. LDPE film spiked by 4.1% and HDPE by 2.3% in Q1 2024, squeezing converters that quote long-term contracts in local currency. Contract packers honor fixed service rates, so sudden material hikes eat margins until indexed clauses reset. Some producers expanded safety stocks to three months, tying up working capital and risking obsolescence if barrier-film formulations change.[4]"Supply chain disruptions drive up prices of European flexible packaging materials in first quarter of 2024,” FlexPack Europe, flexpack-europe.org Frequent price swings complicate volume forecasts and delay machinery purchases dependent on stable cost models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Aseptic Systems Strengthen Position

Intermittent motion units delivered 45.38% vertical form fill seal automation for liquid products market share in 2025 and remain popular where 60-120 packs per minute suffice. Their simpler drivetrains, wash-down frames, and lower spare-part inventories fit cheese sauces, flavored milk, and table sauces. Continuous motion models push beyond 180 packs per minute but yield lower flexibility for varied bag sizes. Rotary architectures fill niche jobs that require multi-lane dosing or shaped pouches, yet their complexity limits wide uptake. The premium story emerges from aseptic VFFS, set to clock 11.23% CAGR, because sterile configurations sidestep cold-chain costs in pharmaceuticals and nutraceuticals. SIG introduced a combi platform that integrates decontamination, clean-room airflow, and servo-driven mandrels on one skid, proving operators can switch from dairy to oral electrolyte solutions without breaking sterility.

Demand for aseptic systems also shapes service business. Validation, filter integrity testing, and remote performance monitoring add annuity revenue for suppliers, locking in customers for ten-year service contracts. Over time, this life-cycle income partly offsets the hefty upfront price tag, helping vendors defend market presence.

By Filling Technology: Sterile Dosing Outpaces Gravity

Gravity fill accounted for 37.61% of the vertical form fill seal automation for liquid products market size in 2025, favored for water-like fluids and low-acid juices. Yet aseptic fill delivers a 11.98% CAGR through 2031 as vaccine diluents, probiotic shots, and ready-to-drink coffee migrate into ambient pipelines. Sterile systems rely on magnetic flow meters and servo pistons that regulate volumes within ±0.2 ml even at 200 CPM. Piston and peristaltic options capture high-viscosity creams, cleansing gels, and nutraceutical pastes where shear sensitivity matters. Vacuum fill retains relevance for foamy or oxygen-sensitive beverages but requires intricate vent management that elevates maintenance time.

Regulators now permit low-acid protein shakes filled aseptically at 95 °C holding to bypass refrigerated storage, slashing logistics bills by double digits in tropical climates. Servicing such lines demands deeper operator skills; thus, vendors bundle augmented-reality assistance into the machine price to shorten technician travel.

By Packaging Material: Sustainable Films Accelerate

Polyethylene remained the workhorse in 2025 with 40.77% share thanks to favorable cost, seal strength, and chemical resistance. However, biodegradable and paper-based alternatives will capture incremental volume as their 12.47% CAGR shows. EU eco-design laws outlaw certain composite laminates by 2030, making mono-material solutions attractive to multinational food brands. Film extruders extend EVOH or mineral barriers while limiting layers to two, a threshold recyclers can handle. Manufacturers pilot volumetric dosing of milk cloned in labs into paper laminate pouches, proving that heat-seal bonds stay secure during 40 °C shipping lanes.

Multilayer barrier films, though harder to recycle, retain niches in oncology drugs and disinfectant refills that require aluminum foil to block oxygen. Polypropylene, albeit costlier, serves retort applications where pouches endure 121 °C sterilization. Across all materials, sensors track temperature and dwell times, automatically adjusting jaw pressure to avoid seal burn or micro-leaks when thinner gauges run.

By Automation Level: Robotics Close the Skills Gap

Fully automatic lines recorded 61.72% share in 2025, but integrated robotic cells-involving pick-and-place arms, vision-guided reject stations, and automated spout inserters climb at 13.34% CAGR. Robots ensure that one operator can supervise five simultaneous lines, a response to the global shortage of maintenance technicians. Camera feedback loops verify pour-spout torque and tamper-evident cap alignment, reducing human error. Semi-automatic configurations still appeal to boutique producers, yet rising minimum wages erode their cost advantage quickly.

Digital twin software packages simulate pouch forming and fill turbulence before a batch runs, trimming setup waste by 30%. Savings convince contract packers bidding on short batches for social-media-driven beverage launches. Vendors note aftermarket service revenues grow 12% annually as buyers sign cloud subscriptions for remote condition-based maintenance.

By End-Use Industry: Pharmaceuticals Lift Value Density

Pharmaceuticals and nutraceuticals enjoy a 11.56% CAGR as liquid vitamins, rehydration salts, and pediatric suspensions migrate into lightweight pouches. The high regulatory bar locks out generics until they partner with automation suppliers offering validation documents. Dairy products, despite a commanding 29.62% share, post mid-single-digit gains as mature markets approach saturation. Still, recent lactose-free and high-protein innovations inject modest volume growth.

Beverage marketers push single-serve sports drinks and cold brew coffee that need nitrogen-flush systems to protect flavor, stimulating VFFS investment. Sauces, dressings, and condiments require wider jaws and flapper nozzles to pass particulates up to 6 mm, a technical challenge that vendors now solve with servo-timed agitation. Personal care lotions lean on piston fillers with CIP systems so changeovers from fragranced to hypoallergenic formulas do not trigger cross-contamination. Finally, industrial and household chemicals demand anti-static film and explosion-proof drives, carving a small but profitable niche.

Geography Analysis

Asia-Pacific anchored 34.12% of sales in 2025, bolstered by its dense co-packing networks and government schemes that refund up to 30% of capex for food-processing automation. China’s coastal clusters integrate film extrusion, filling, and secondary packaging in shared campuses to cut transit times. India mirrors the trend as state programs allow 100% accelerated depreciation on machinery installed before 2026, spurring dairies to leapfrog to servo-driven aseptic platforms. Southeast Asian plants export ambient coconut water pouches, advancing the region’s leadership.

The Middle East, led by the United Arab Emirates and Saudi Arabia, records the fastest 10.31% CAGR. Sovereign funds channel billions into agro-industrial parks where water bottlers and long-life milk fillers co-locate with logistic hubs, lowering finished-goods freight costs. Local firms previously reliant on imports now source laminate film, caps, and spare parts domestically, enhancing resilience after pandemic-era shipping delays.

North America and Europe remain vital but mature arenas. Here, the vertical form fill seal automation for liquid products market grows as firms retrofit legacy lines to run recyclable films, adopt cloud OEE dashboards, and install robotic case packers. Replacement demand spikes every seven to nine years, aligned with corporate carbon targets that require lighter packaging. South America shows upside in Brazil, where dairy processors upgrade to raise chilled-milk shelf life to 21 days, and in Argentina, where craft breweries adopt pouch formats for home delivery. Exchange-rate swings and inflation, however, temper capex in the region.

Competitive Landscape

Competition is moderate because no single vendor exceeds a 15% slice of global revenue. Legacy players such as Tetra Pak, Syntegon, and SIG leverage established service networks, but nimble specialists like Triangle Package Machinery innovate quickly in servo sealing and ultrasonic welding. Start-ups focusing on AI-based vision systems partner with machine builders to retrofit inspection into installed bases, creating joint value without full acquisitions.

Strategic moves concentrate on digital services. Syntegon introduced Synexio cloud modules that rank energy consumption per SKU and nudge operators to reduce idle time. TNA Solutions demonstrated a line where one operator oversees five baggers by using predictive algorithms to dispatch maintenance tasks 30 minutes before a stoppage. Larger groups also buy robotics integrators to widen scope. The trend suggests future leadership hinges less on hardware patents and more on data-driven uptime guarantees, carbon dashboards, and pay-per-output contracts.

Sustainability credentials now influence tenders. Machinery able to run 100% recyclable polyethylene wins European bids where retailers scrutinize life-cycle analysis. Vendors supply seal-bar inserts, lower-temperature films, and remote firmware updates so customers comply without downtimes. Those that cannot demonstrate quick adaptation risk commoditization in price-focused segments.

Vertical Form Fill Seal Automation For Liquid Products Industry Leaders

-

Tetra Pak International S.A.

-

SIG Group AG

-

Syntegon Technology GmbH

-

KHS GmbH

-

Nichrome India Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TNA Solutions displayed robag 3e units at SNAXPO 2025 that let one technician manage five lines at up to 250 bags per minute.

- February 2025: Syntegon launched SVX Agile, a VFFS system rated for 100% recyclable mono-material at 300 pouches per minute, featuring a new cross-seal drive.

- January 2025: Circle Packaging unveiled V24Sti with advanced servo control and built-in vision inspection aimed at pharmaceutical users.

- December 2024: Matrix Packaging introduced MVC-300L liquid VFFS with ultrasonic sealing that eliminates heat-bar warm-up time, trimming changeovers.

Global Vertical Form Fill Seal Automation For Liquid Products Market Report Scope

The Vertical Form Fill Seal Automation for Liquid Products Market Report is Segmented by Machine Type (Intermittent Motion VFFS, Continuous Motion VFFS, Aseptic VFFS, Rotary VFFS), Filling Technology (Gravity Fill, Piston Fill, Peristaltic Pump Fill, Vacuum Fill, Aseptic Fill), Packaging Material (Polyethylene Films, Polypropylene Films, Multilayer Barrier Films, Paper Laminates, Biodegradable Films), Automation Level (Fully Automatic Systems, Semi-automatic Systems, Integrated Robotic Cells), End-use Industry (Dairy Products, Beverages, Sauces and Condiments, Personal Care and Cosmetics, Pharmaceuticals and Nutraceuticals, Industrial and Household Chemicals), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Intermittent Motion VFFS |

| Continuous Motion VFFS |

| Aseptic VFFS |

| Rotary VFFS |

| Gravity Fill |

| Piston Fill |

| Peristaltic Pump Fill |

| Vacuum Fill |

| Aseptic Fill |

| Polyethylene Films (LDPE/HDPE) |

| Polypropylene Films |

| Multilayer Barrier Films (EVOH, Nylon) |

| Paper Laminates |

| Biodegradable Films (PLA, PHA) |

| Fully Automatic Systems |

| Semi-automatic Systems |

| Integrated Robotic Cells |

| Dairy Products |

| Beverages (Juices, Water) |

| Sauces, Dressings and Condiments |

| Personal Care and Cosmetics |

| Pharmaceuticals and Nutraceuticals |

| Industrial and Household Chemicals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Intermittent Motion VFFS | ||

| Continuous Motion VFFS | |||

| Aseptic VFFS | |||

| Rotary VFFS | |||

| By Filling Technology | Gravity Fill | ||

| Piston Fill | |||

| Peristaltic Pump Fill | |||

| Vacuum Fill | |||

| Aseptic Fill | |||

| By Packaging Material | Polyethylene Films (LDPE/HDPE) | ||

| Polypropylene Films | |||

| Multilayer Barrier Films (EVOH, Nylon) | |||

| Paper Laminates | |||

| Biodegradable Films (PLA, PHA) | |||

| By Automation Level | Fully Automatic Systems | ||

| Semi-automatic Systems | |||

| Integrated Robotic Cells | |||

| By End-use Industry | Dairy Products | ||

| Beverages (Juices, Water) | |||

| Sauces, Dressings and Condiments | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals and Nutraceuticals | |||

| Industrial and Household Chemicals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the vertical form fill seal automation for liquid products market?

The market is valued at USD 2.35 billion in 2026.

How fast is the vertical form fill seal automation for liquid products market expected to grow?

It is forecast to post a 6.43% CAGR and reach USD 3.21 billion by 2031.

Which region holds the largest share of installations?

Asia-Pacific leads with 34.12% share, driven by contract packing expansion and local incentives.

Which machine segment will grow the quickest through 2031?

Aseptic vertical form fill seal systems are projected to register an 11.23% CAGR because they eliminate cold-chain costs.

Why are biodegradable films attracting interest among liquid product packagers?

EU recycling rules push mono-material solutions, and biodegradable films meet compliance while supporting brand sustainability goals.

How are companies dealing with the shortage of skilled maintenance technicians?

Integrated robotic cells and cloud-based predictive maintenance allow one operator to monitor multiple lines, reducing the need for specialized staff.

Page last updated on: