Liquid And Viscous Contract Filling Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

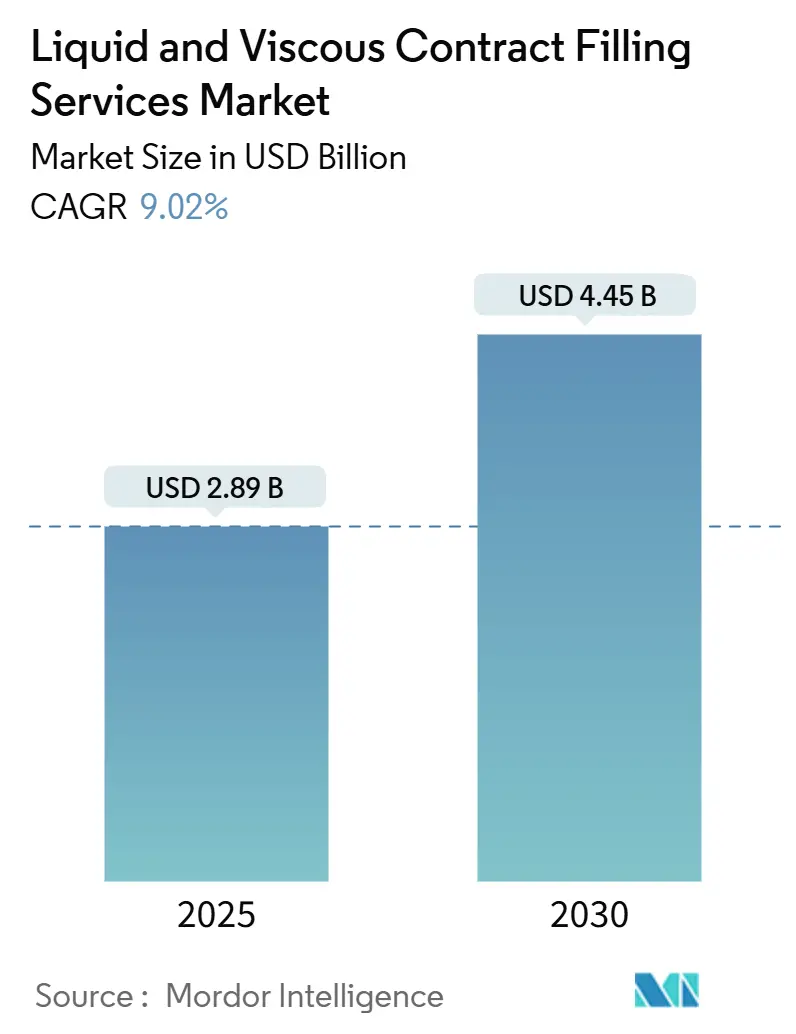

| Market Size (2025) | USD 2.89 Billion |

| Market Size (2030) | USD 4.45 Billion |

| Growth Rate (2025 - 2030) | 9.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid And Viscous Contract Filling Services Market Analysis by Mordor Intelligence

The liquid and viscous contract filling services market size is valued at USD 2.89 billion in 2025 and is projected to reach USD 4.45 billion by 2030, representing a 9.02% CAGR for the period 2025-2030. Consistent double-digit expansion reflects a mounting preference for turnkey outsourcing among consumer packaged goods companies, as well as tight regulatory demands that push brand owners toward specialized partners, and the rising complexity of high-viscosity nutritional and personal-care formulations. Production flexibility, avoidance of capital-intensive infrastructure, and access to validated aseptic environments position the liquid and viscous contract filling services market as a strategic enabler for companies that need to bring multiple stock-keeping units to market quickly. At the same time, e-commerce-driven private-label growth, sustainability-linked packaging shifts, and the embrace of net-weight piston systems for premium viscous products add further momentum to the liquid and viscous contract filling services market.

Key Report Takeaways

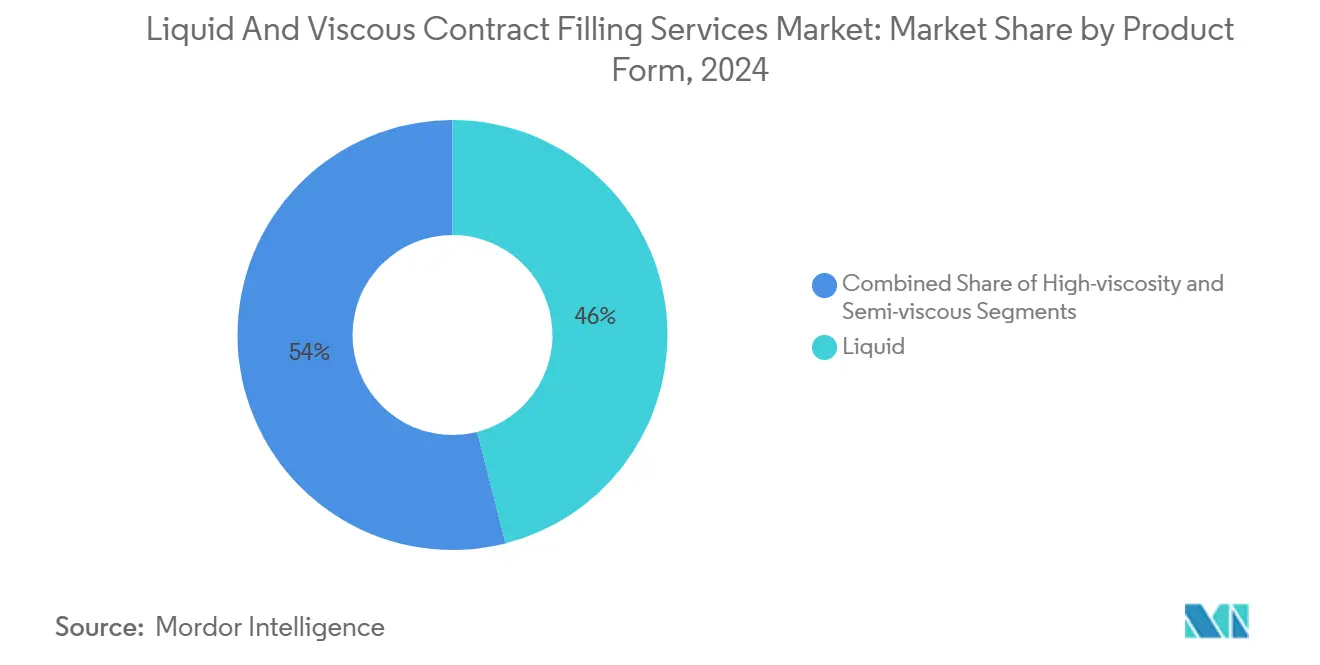

- By product form, liquids captured 46.04% of the aseptic liquid filling and packaging systems market share in 2024.

- By filling technology, the aseptic liquid filling and packaging systems market size for net-weight piston filling is forecast to advance at a 10.09% CAGR through 2030.

- By end-user industry, food and beverages captured 41.91% of the aseptic liquid filling and packaging systems market share in 2024.

- By packaging type, the aseptic liquid filling and packaging systems market size for pouches and sachets is forecast to advance at a 10.48% CAGR through 2030.

- By geography, North America captured 32.44% of the aseptic liquid filling and packaging systems market share in 2024.

Global Liquid And Viscous Contract Filling Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for turnkey outsourcing among CPG majors | +2.1% | North America and Europe | Medium term (2-4 years) |

| Growth of e-commerce private-label brands needing agile fillers | +1.8% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Stringent hygiene mandates driving investment in aseptic liquid lines | +1.5% | Regulated markets worldwide | Long term (≥ 4 years) |

| Sustainability push toward lightweight flexible pouches | +1.3% | Europe and North America expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of nutraceutical and viscous functional beverages | +1.7% | North America and Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| Near-shoring strategies of multinational F&B companies | +0.8% | North America and spillover to Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Hygiene Mandates Driving Investment in Aseptic Liquid Lines

A wave of global food-safety regulations requires aseptic processing for liquids that can support microbial growth. The United States FDA preventive-controls rule that took effect in 2024 mandates validated sanitation programs and environmental monitoring, driving brand owners without sterile infrastructure toward accredited partners.[1]“FSMA Final Rule on Preventive Controls for Human Food,” United States Food and Drug Administration, fda.gov European hazard-analysis protocols mirror that emphasis, so contract fillers with qualified aseptic suites command 20-30% pricing premiums over conventional lines. Investment in barrier isolators, clean-in-place loops, and rapid-changeover closure systems, therefore, underpins growth, especially in shelf-stable beverages and parenteral nutrition products.

Growth of E-Commerce Private-Label Brands Needing Agile Fillers

The direct-to-consumer boom increased the number of brands launching multiple SKUs in small batches. Contract fillers report 40-60% more short-run orders since 2024 as average batch sizes shrink but product variety rises.[2]Deane R., “Flexible Contract Filling: E-Commerce Drives Small Batch Demand,” Food and Beverage Packaging, foodandbeveragepackaging.com Flexible filling centers with quick-disconnect manifolds and automated wash-down shorten changeovers from hours to minutes, letting emerging labels scale without sunk capital. Agile lines configured for viscous liquids, concentrates, and emulsions are especially attractive to wellness entrepreneurs focused on premium formulations.

Sustainability Push toward Lightweight Flexible Pouches

Corporate sustainability pledges drive brand owners to redesign rigid formats. Unilever’s 2025 target to halve virgin plastic sparked a rush toward high-barrier pouches that weigh up to 70% less than comparable bottles. Contract fillers equipped with roll-stock forming, spout insertion, and retort-capable pouch lines have reported a 35-50% increase in projects since 2024. Beyond material savings, flexible formats support e-commerce by reducing breakage and dimensional weight. For fillers, pouch production commands higher margins due to the specialized sealing and nitrogen-flushing steps required to protect sensitive, viscous formulas.

Expansion of Nutraceutical and Viscous Functional Beverages

Consumer focus on immunity, cognitive health, and sports recovery fuels demand for viscous functional shots and concentrated suspensions that require gentle pumping and high-precision dosing. Approvals of new botanical extracts by U.S. and European regulators catalyze launches of omega-3 emulsions, fiber-rich smoothies, and plant-protein gels. Contract fillers able to manage shear-sensitive ingredients under chilled conditions see rising order volumes and can charge 25-40% surcharges over traditional juice filling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile food-grade commodity prices compressing filler margins | -1.2% | Worldwide, higher pressure in emerging markets | Short term (≤ 2 years) |

| Limited availability of skilled operators for high-viscosity lines | -0.8% | North America and Europe, growing in Asia-Pacific | Medium term (2-4 years) |

| Capital-intensive compliance with multi-jurisdictional regulations | -0.7% | Regulated markets | Long term (≥ 4 years) |

| Rising in-house automation by large brand owners | -0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Food-Grade Commodity Prices Compressing Filler Margins

Swinging input costs for aluminum, resins, and food-safe additives destabilize contract pricing. Aluminum averaged an 18% jump in 2024 while PET resin fluctuated 12-25%, squeezing fillers locked into fixed-price agreements. Smaller operators without bulk-purchase leverage struggle to renegotiate contracts or hedge volatility. High-viscosity jobs suffer most because they often require specialty barrier layers and processing aids that track crude-price swings and are harder to substitute.

Limited Availability of Skilled Operators for High-Viscosity Lines

Rheology-driven lines require technicians who are skilled in pressure modulation, temperature mapping, and CIP validation. Industry surveys show a 20-30% wage premium for qualified viscous-product operators and a training arc of 6-12 months to reach proficiency.[3]Miller J., “Manufacturing Skills Gap Widens in 2024,” Manufacturing.net, manufacturing.net With baby-boomer retirements accelerating, the talent gap limits rapid capacity expansions, forcing some fillers to decline projects or lengthen lead times even as demand climbs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: High-Viscosity Applications Drive Premium Growth

High-viscosity products are expected to experience the fastest expansion at a 10.29% CAGR, although liquids are projected to command the largest 2024 revenue share at 46.04%. Cross-category launches in personalized nutrition, high-protein spreads, and dense botanical blends elevate demand for shear-sensitive handling under nitrogen or vacuum. Facilities that master gentle lobe pumping, jacketed holding tanks, and servo-controlled piston filling win long-term contracts from brands seeking texture integrity and flavor protection. The liquid and viscous contract filling services market size for high-viscosity lines is forecast to widen significantly, propelled by 25-40% price premiums over standard liquid jobs. Semi-viscous offerings remain attractive when users desire creamy textures without the full rheological complexity, such as drinkable yogurts and cosmetic lotions.

Investments in modular skid systems allow production rooms to toggle between viscosity ranges with minimal downtime, guarding against customer concentration. Regulatory oversight of dietary supplements and novel foods favors fillers with validated bioburden control and allergen segregation. Consequently, the liquid and viscous contract filling services market captures revenue upside from multi-viscosity capabilities, reducing seasonality risk and maximizing equipment uptime.

By Filling Technology: Aseptic Systems Lead While Piston Filling Accelerates

Aseptic platforms accounted for 33.13% of 2024 revenue, driven by growth in batch-sterile beverages and parenteral nutrition. Their integrated high-efficiency particulate air filtration and peroxide-based decontamination protect products without high-heat exposure. Nevertheless, the net-weight piston segment is projected to grow at a 10.09% CAGR, driven by the pursuit of sub-gram dosing accuracy in premium viscous SKUs. With product costs sometimes exceeding USD 100 per liter, brand owners tolerate no giveaway, making load-cell-controlled piston systems a strategic asset. The liquid and viscous contract filling services market share for piston technology is expected to rise as nutraceutical and cosmetic innovations demand volumetric precision.

Hybrid plants roll out combinational layouts that embed clean-fill rooms adjacent to ambient gravity lines for flavored waters, raising overall asset turns. Real-time monitoring, IoT sensors, and predictive analytics reduce unplanned downtime, enhancing returns on capital equipment and bolstering customer confidence.

By End-User Industry: Nutraceuticals Surge Within Food and Beverage Dominance

Food and beverages accounted for 41.91% of 2024 demand, primarily driven by shelf-stable juices, broths, and concentrated sauces. Home and personal care doses, such as collagen shots and probiotic emulsions, exhibit an 11.21% CAGR. Formulation complexity prompts brand owners to rely on partners who are proficient in nutrient stability, oxygen exclusion, and regulatory dossiers under FDA dietary supplement rules. The liquid and viscous contract filling services market size for home and personal care clients is projected to grow rapidly as wellness adoption expands from North America and Europe to urban Asia. Home and personal care segments leverage sustainable refills and zero-waste completions, whereas pharmaceutical buyers favor cGMP-qualified fill-finish suites shared with clinical supply operations.

Synergies emerge when aseptic capabilities developed for parenteral drugs are applied to the execution of functional beverages, boosting speed-to-market and consistency of compliance. Fillers that straddle multiple regulated verticals can amortize quality system investments and cross-train staff, thereby reinforcing profit resilience.

By Packaging Type: Flexible Formats Challenge Bottle Dominance

Bottles still controlled 38.81% of 2024 shipments due to consumer habits and mature supply chains. However, pouch and sachet demand is expanding at a 10.48% CAGR as carriers aim to cut freight emissions and retail waste. Lightweight flexibles reduce transportation fuel use by up to 60% compared to glass, earning corporate buy-in for sustainability scorecards. The liquid and viscous contract filling services market size for pouches gains additional traction from e-commerce, where rigid formats incur dimensional-weight penalties. Meanwhile, jars, bag-in-box, and drums retain niche importance for food-service and industrial lubricants. Seal-integrity testing, multi-layer film qualification, and spout-insertion know-how differentiate advanced fillers.

Brand owners benefit from design freedom: irregular shapes, embedded spouts, and dispense-on-demand caps support portion control and consumer convenience. In parallel, regulatory approvals for high-barrier compostable films create new opportunities for contract fillers willing to pioneer biodegradable laminates that still endure hot-fill temperatures.

Geography Analysis

North America generated 32.44% of 2024 revenue, anchored by decades-old outsourcing contracts and tight regulatory frameworks that reward proven compliance. Recent near-shoring among multinational food majors further boosts demand for regional capacity, with Mexico serving as a manufacturing backstop under USMCA rules. Brand portfolios tend to skew toward organic, clean-label, and specialty beverages, each of which requires meticulous allergen control.

The Asia-Pacific region, projected to grow at a 10.16% CAGR, benefits from government incentives for downstream food processing, a growing middle class, and expanded logistical infrastructure. China, India, Vietnam, and Thailand attract foreign direct investment into greenfield filling plants, creating a two-way flow of knowledge transfer and local raw material integration. Domestic brands mirror Western wellness trends, propelling viscous functional drinks and cosmeceutical serums.

Europe is driving strict sustainability targets, circular economy policies, and a concentration of premium personal care brands. Germany, France, and the United Kingdom lead but must navigate post-Brexit paperwork and divergent labeling codes. Contract fillers holding ISO 22000 and BRC certifications play a pivotal role in maintaining market access and carbon-footprint transparency.

Competitive Landscape

The liquid and viscous contract filling services market is moderately fragmented, featuring a mix of global players and regional specialists. Market leaders differentiate through patented multi-viscosity valves, real-time analytics, and vertically integrated design-to-distribution solutions. Acquisitions such as Hearthside Food Solutions’ USD 120 million purchase of Midwest Packaging Solutions illustrate strategic moves to widen geographic reach and deepen functional beverage capabilities. Capital-intensive aseptic expansions, such as PCI Pharma Services’ USD 75 million Philadelphia upgrade, underscore the need for scale to achieve pharmaceutical-grade sterility.

Mid-tier fillers pursue niche leadership by specializing in high-viscosity natural cosmetics, low-acid savory sauces, or alcohol-free spirits. Automation adoption accelerates as operators deploy cobots for cap-torque inspection and vision-guided spout insertion, trimming labor cost exposure. Patent filings reveal emphasis on universal in-line clean-in-place designs that shrink downtime between allergens and viscosities. ISO 14001 and carbon-neutral certifications emerge as tie-breakers during request-for-proposal processes, especially with multinational FMCG firms aligning with Scope 3 decarbonization metrics.

Barriers to entry remain material: high upfront capex, multi-jurisdiction registrations, and the escalating skill scarcity restrain new entrants. Nonetheless, localized fillers in Southeast Asia and Eastern Europe win contracts through proximity, language fluency, and government tax incentives. Collaboration between equipment manufacturers and fillers intensifies, yielding pre-validated skids that cut commissioning time for brownfield expansions.

Liquid And Viscous Contract Filling Services Industry Leaders

Assemblies Unlimited, Inc.

BevSource, Inc.

CCI Packaging, Inc.

Co-Pak Packaging Corporation

Alpacka Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PCI Pharma Services completed a USD 75 million aseptic capacity expansion in Philadelphia, adding specialized high-viscosity injectable lines.

- October 2024: Hearthside Food Solutions acquired Midwest Packaging Solutions for USD 120 million, enlarging its functional beverage footprint.

- September 2024: Novo Nordisk partnered with Vetter Pharma on a USD 200 million GLP-1 filling line program spanning three years.

- August 2024: Co-Pak Packaging Corporation opened a new USD 45 million Texas facility dedicated to pouch filling for personal-care liquids.

Global Liquid And Viscous Contract Filling Services Market Report Scope

| Liquid |

| Semi-viscous |

| High-viscosity |

| Aseptic Liquid Filling |

| Hot Fill |

| Cold Fill |

| Net-Weight Piston Filling |

| Vacuum Gravity Filling |

| Food and Beverages |

| Home and Personal Care |

| Pharmaceuticals |

| Industrial and Chemical |

| Other End-user Industries |

| Bottles |

| Pouches and Sachets |

| Jars and Tubs |

| Bag-in-Box |

| Drums and IBCs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Form | Liquid | ||

| Semi-viscous | |||

| High-viscosity | |||

| By Filling Technology | Aseptic Liquid Filling | ||

| Hot Fill | |||

| Cold Fill | |||

| Net-Weight Piston Filling | |||

| Vacuum Gravity Filling | |||

| By End-user Industry | Food and Beverages | ||

| Home and Personal Care | |||

| Pharmaceuticals | |||

| Industrial and Chemical | |||

| Other End-user Industries | |||

| By Packaging Type | Bottles | ||

| Pouches and Sachets | |||

| Jars and Tubs | |||

| Bag-in-Box | |||

| Drums and IBCs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the liquid and viscous contract filling services market by 2030?

The liquid and viscous contract filling services market is forecast to reach USD 4.45 billion by 2030.

Which region is expected to grow fastest in liquid and viscous contract filling services?

Asia-Pacific, with an anticipated 10.16% CAGR through 2030, is the fastest-growing region.

Why are pouches gaining traction over bottles in contract filling?

Pouches weigh less, cut freight emissions, enable e-commerce sizing, and align with corporate sustainability targets, all while handling liquid and viscous products securely.

Which filling technology is seeing the highest growth rate?

Net-weight piston filling is expanding at a 10.09% CAGR because brands need sub-gram accuracy for high-value viscous formulations.

How do stringent hygiene mandates influence outsourcing decisions?

Tight FDA and EU requirements make aseptic infrastructure costly for brand owners, so many outsource to specialized fillers that already hold validated sterile environments.

What factors limit capacity expansion for viscous product filling?

Scarcity of skilled operators, extended training periods, and higher operating costs constrain how quickly fillers can add high-viscosity lines.

Page last updated on: