Truffle Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

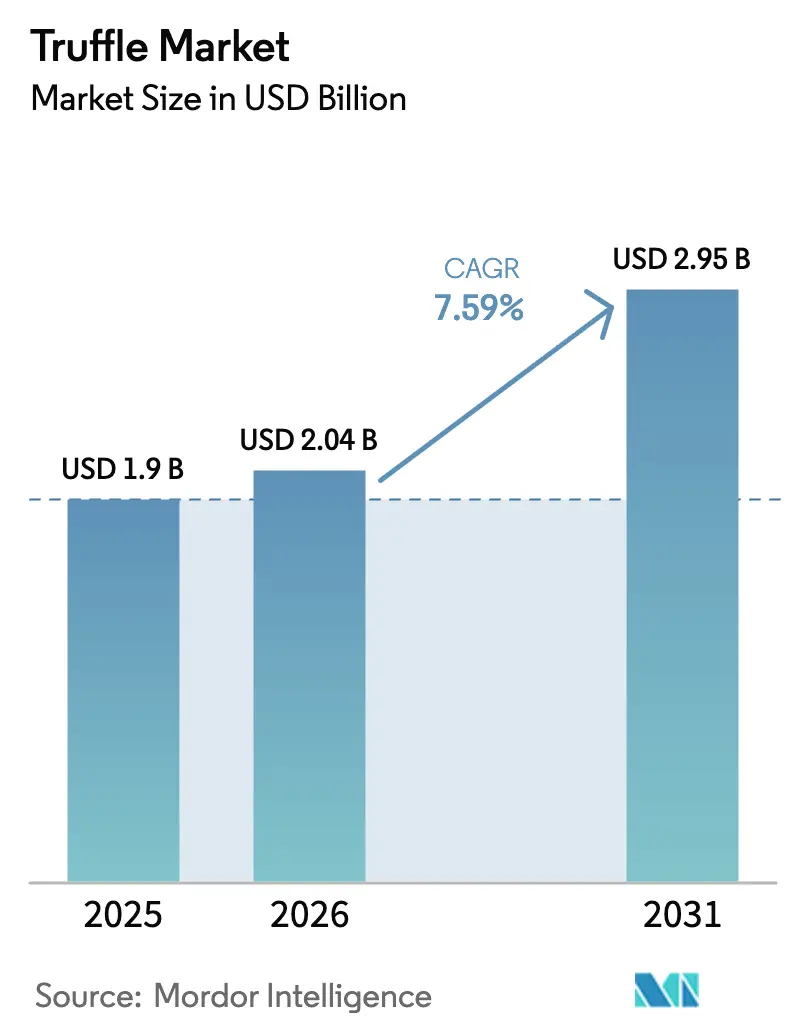

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.95 Billion |

| Growth Rate (2026 - 2031) | 7.59% CAGR |

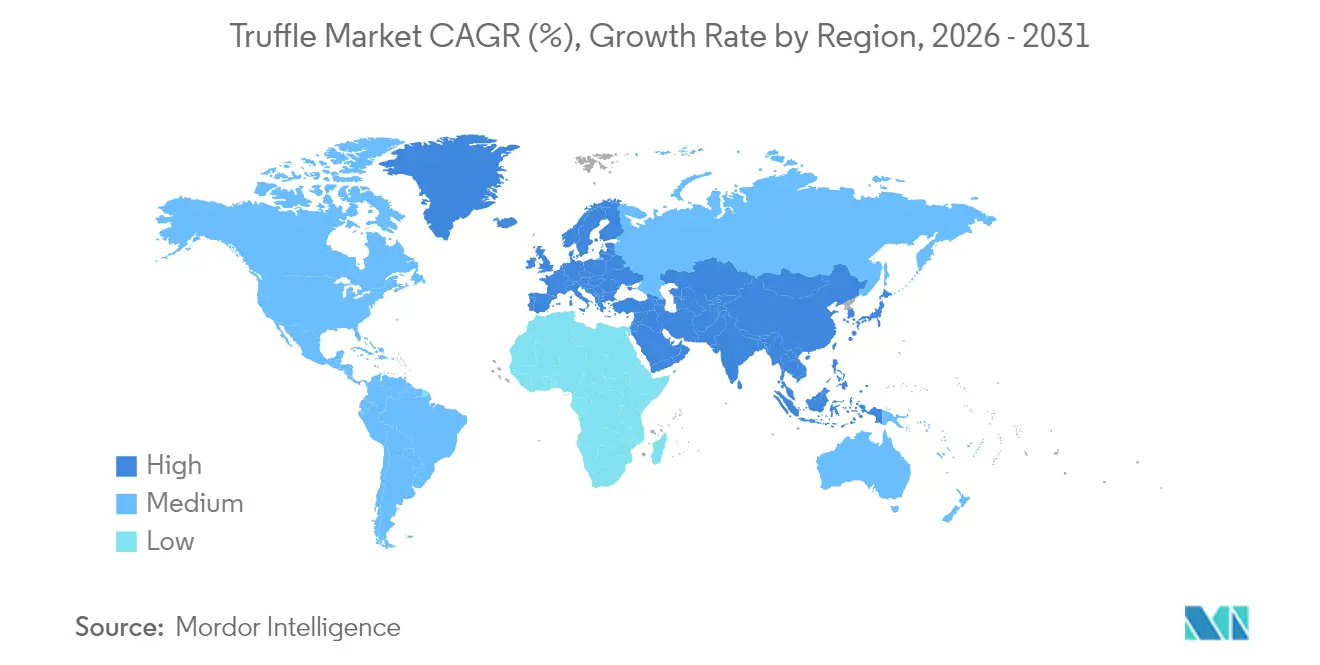

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

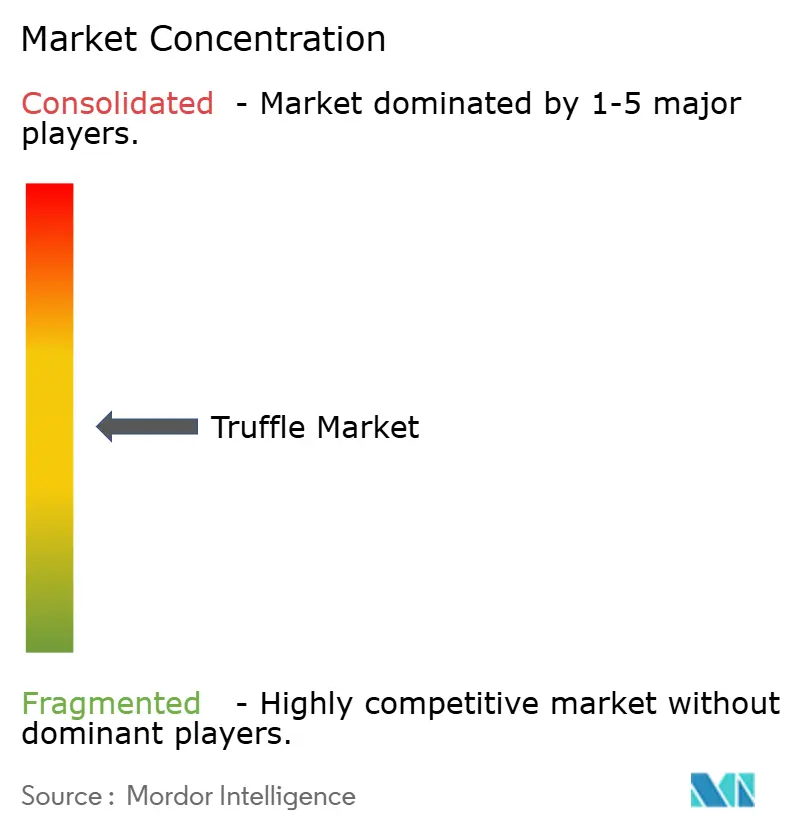

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Truffle Market Analysis by Mordor Intelligence

The truffle market size was valued at USD 1.90 billion in 2025 and estimated to grow from USD 2.04 billion in 2026 to reach USD 2.95 billion by 2031, at a CAGR of 7.59% during the forecast period (2026-2031). Rising commercial orcharding in North America and Australia, coupled with year-round supply enabled by Southern Hemisphere harvests, is giving the truffle market resilience even as other premium food categories slow. Climate stress in Mediterranean Europe is pushing buyers to diversify sourcing, which strengthens the negotiating position of newer growers while tempering historical price spikes. Processing technologies that extend shelf life and unlock value for lower-grade tubers are opening the truffle market to mainstream consumers through sauces, oils, and ready-to-eat snacks. Retail democratization follows, with specialty grocers and e-commerce platforms making fresh and processed truffles visible to home cooks who once saw them only on chef-driven menus. Established European brands are responding by investing in distribution centers closer to growth regions, signaling that global logistics is now as critical as terroir to the truffle market.

Key Report Takeaways

- By product type, black truffles led with 47.30% truffle market share in 2025; Chinese truffles are forecast to expand at a 7.66% CAGR through 2031.

- By form, fresh truffles accounted for a 55.05% share of the truffle market size in 2025, while processed formats are projected to grow at a 6.63% CAGR between 2026-2031.

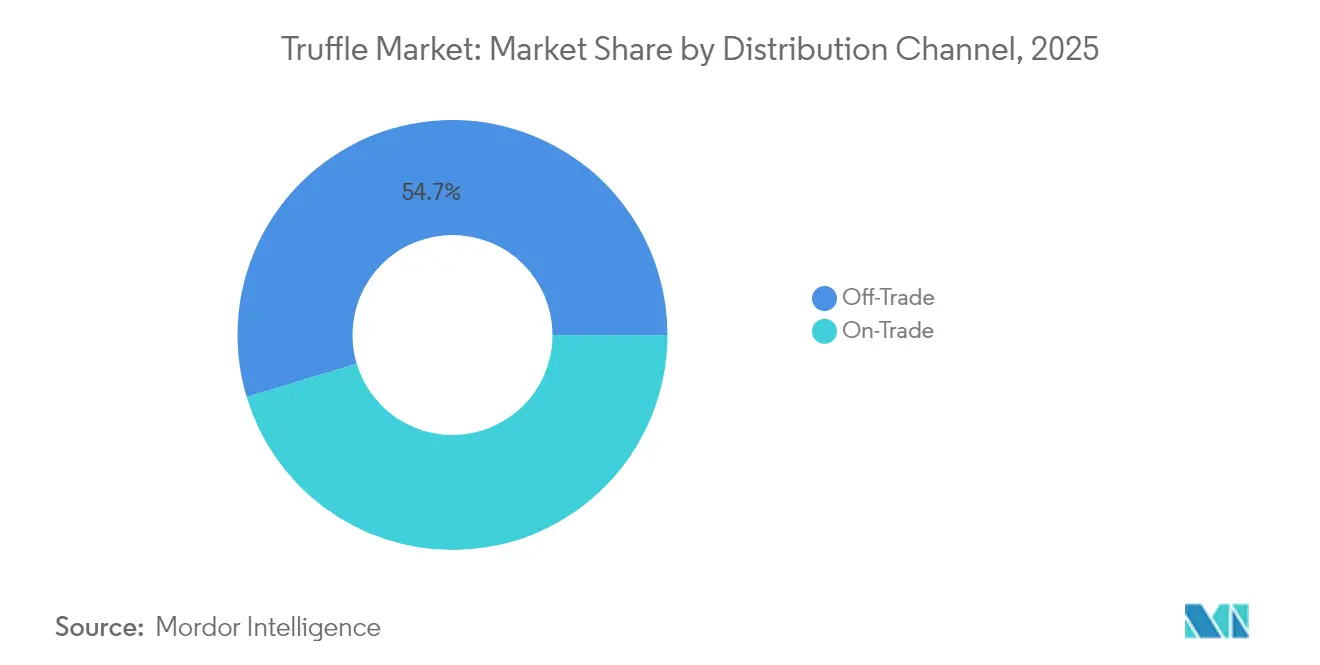

- By distribution channel, off-trade captured 54.65% of the truffle market share in 2025 and is expected to advance at a 7.32% CAGR to 2031.

- By geography, Europe retained 42.72% of the truffle market share in 2025, whereas Asia-Pacific is poised to record the fastest 9.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Truffle Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding gourmet cuisine culture & premium ingredient demand | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid growth of truffle-infused packaged foods & condiments | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Commercial truffle orcharding spreading beyond Europe | +1.2% | North America, Australia, Asia-Pacific | Long term (≥ 4 years) |

| Growth in Foodservice Sector | +1.0% | Global, urban centers priority | Medium term (2-4 years) |

| Sustainability and Ethical Sourcing | +0.8% | Europe, North America | Long term (≥ 4 years) |

| Advancements in Cultivation Techniques | +0.7% | Global, technology-adopting regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Gourmet Cuisine Culture and Premium Ingredient Demand

The growing popularity of gourmet cuisine through social media and celebrity chefs increases consumer demand for premium ingredients, particularly truffles. Restaurants incorporate truffle dishes as signature menu items, with retail prices ranging from USD 800 to USD 1,000 per pound. This market evolution has transformed truffles from exclusive luxury items into more accessible ingredients through smaller portions and processed products. The North American Truffle Growers Association conducts educational programs to help consumers distinguish between authentic truffles and synthetic alternatives, addressing previous market confusion. Oregon's reputation for truffle production demonstrates how regions can establish culinary identities around premium local ingredients. These developments expand demand beyond traditional European markets while maintaining premium price points.

Rapid Growth of Truffle-Infused Packaged Foods and Condiments

Advancements in processing technologies allow truffles to be incorporated into shelf-stable products, expanding their market reach beyond fresh consumption. The use of supercritical carbon dioxide extraction and β-cyclodextrin encapsulation preserves truffle aroma compounds, enabling year-round availability and addressing seasonal limitations. These processing methods create opportunities for lower-grade truffles while maintaining their authentic flavors. Sabatino's 40% expansion of distribution capacity through its Connecticut facility indicates growing demand for processed truffle products. The facility's automation and sustainability initiatives demonstrate the industry's shift toward efficient production methods. Processed truffle products increase market accessibility while generating higher profit margins compared to fresh truffle sales.

Commercial Truffle Orcharding Spreading Beyond Europe

Scientific cultivation methods are now supplanting traditional foraging, leading to more predictable supply chains across various regions. The North American Truffle Growers Association, representing over 200 member farms, employs mycorrhizal inoculation techniques, with cultivation cycles spanning 8-10 years. North American yields currently average 15 kg per hectare, trailing significantly behind European benchmarks, suggesting a considerable potential for enhancement through refined agronomic practices. While climate change poses threats to traditional Mediterranean production zones, it simultaneously opens doors for cultivation in regions once deemed unsuitable. With over 200 truffle farms, Australia showcases a successful adaptation in the Southern Hemisphere, directing most of its exports to European and Asian markets during off-seasons. The identification of two new North American truffle species, Tuber canirevelatum and Tuber cumberlandense, paves the way for broader cultivation, leveraging native varieties that are better suited to local conditions.

Growth in Foodservice Sector

Post-pandemic, the restaurant industry is increasingly turning to premium ingredients, not just to elevate their menu offerings but also to command higher price points. Truffles, once a luxury reserved for high-end establishments, are now making their way into casual dining spots, thanks to processed formats that allow for more cost-effective menu integration. The foodservice channel not only ensures consistent volume but also bolsters commercial cultivation expansion, offering producers a reliable revenue stream. In a nod to cross-industry innovation, Maker's Mark distillery is venturing into truffle-infused whiskey, harnessing the unique Tuber cumberlandense species for this novel product. This move, diversifying truffles' use beyond their traditional culinary realm, not only broadens market opportunities but also carves out a distinct premium brand identity. Additionally, owing to the rising tourism, the demand for various cuisines is increasing among consumers. According to the Office for National Statistics data from 2023[1]Office for National Statistics, "Inbound Tourism in the United Kingdom", www.ons.gov.uk, 38 million overseas residents visited the United Kingdom. As foodservice outlets increasingly adopt truffle flavors, they pave the way for a burgeoning retail market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price volatility & affordability barrier | -1.5% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Climate-change-driven yield uncertainty | -1.2% | Mediterranean Europe, expanding globally | Long term (≥ 4 years) |

| Regulatory and Certification Barriers | -0.8% | Europe, North America | Medium term (2-4 years) |

| Limited Shelf Life | -0.6% | Global, supply chain dependent | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Price Volatility & Affordability Barrier

Périgord black truffles command prices as high as USD 2,345.7 per kilogram during peak demand, underscoring the affordability challenges hindering their mainstream adoption. These truffles are highly sought after due to their unique flavor profile and limited availability, which further drives up their value. Similarly, Portuguese summer truffles fluctuate between USD 29.32 and USD 703.71 per kilogram, with prices swayed by regional availability and quality. This price volatility is largely attributed to weather-dependent yields, seasonal harvesting, and limited storage, which together shorten selling windows. The unpredictable nature of truffle yields, influenced by climatic conditions, adds another layer of complexity to pricing. While commercial cultivation endeavors seek to stabilize supply, the 8-10 year development cycles pose a challenge, delaying any immediate market impact. As a result of this price sensitivity, the market's expansion is largely confined to affluent consumers, limiting volume growth even amidst robust demand. However, ongoing research and technological advancements in truffle farming may offer long-term solutions to address these challenges and broaden market accessibility.

Climate-Change-Driven Yield Uncertainty

Climate stress is increasingly impacting Mediterranean truffle production, with summer precipitation patterns playing a crucial role in winter harvest outcomes. An analysis of Spanish black truffle production highlights a pronounced sensitivity to climate factors. As wild populations dwindle, cultivated truffles now account for 80-90% of Spain's national output. Unpredictable drought conditions lead to reduced yields, disrupting the supply chain and influencing global pricing and availability. Although climate change presents cultivation opportunities in northern regions, established production areas grapple with heightened uncertainty. While the industry's strategy of geographic diversification offers some risk mitigation, the transition periods introduce market instability. Additionally, the rising demand for truffles in international markets further exacerbates supply chain challenges, as producers struggle to meet growing consumer expectations. Investments in advanced irrigation techniques and climate-resilient cultivation practices are emerging as potential solutions to stabilize production and address these challenges effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chinese Truffles Drive Volume Growth

Chinese truffles represent the fastest-growing product segment at 7.66% CAGR through 2031, despite black truffles maintaining 47.30% market share in 2025. This growth trajectory reflects China's transformation from domestic pig feed usage to international export prominence, with 2024 exports reaching record levels of 32.5 tonnes. Yunnan province dominates Chinese production, leveraging favorable climate conditions and established cultivation infrastructure. White truffles command premium pricing but face cultivation challenges that limit supply expansion, while Burgundy truffles occupy mid-market positioning with moderate growth potential.

The discovery of Tuber indicum's varying chemical composition across Chinese regions creates quality differentiation opportunities, with Qujing specimens demonstrating superior antioxidant properties and flavor compounds. This geographic variation enables premium positioning for specific regional products while supporting broader market expansion through diverse price points. North American species discoveries add cultivation diversity, with Tuber canirevelatum and Tuber cumberlandense offering aromatic profiles comparable to European varieties while adapted to local growing conditions.

By Form: Processing Innovation Creates Shelf-Stable Value

Fresh tubers held 55.05% of market share in 2025, reflecting enduring chef preference for shaved delicacies. Yet mild thermal processing at 63 °C now stretches usable life to 160 days, letting wholesalers ship pallets rather than courier packets. When combined with CO₂ extraction, processors capture aromas once lost to oxidation, giving table sauces an authenticity that lifts price premiums. Pack sizes range from 30-g single-use jars to 5-kg foodservice buckets, broadening addressable occasions. That versatility feeds the 6.63% CAGR expected for processed items and helps smooth seasonal cash flow for growers who formerly depended on eight-week windows.

By 2031, the processed Truffles are forecast to grow at a CAGR of 6.63%, reshaping how the truffle market balances luxury cues with convenience demands. Suppliers increasingly bundle fresh, frozen, and ambient options into the same shipment, a strategy that gives chefs menu flexibility and reduces spoilage risk. Retailers capitalize by merchandising truffle chips beside wine pairings, educating newcomers while capturing impulse purchases. With each cycle, processed SKUs strengthen consumer familiarity, which in turn lifts traffic for fresh counter sales, reinforcing the virtuous circle that sustains the broader truffle market.

By Distribution Channel: Off-Trade Broadens Consumer Access

Off-trade outlets owned 54.65% of the truffle market share in 2025 and are expected to reach a CAGR of 7.32% in 2031, thanks to rapid onboarding by high-end supermarkets, specialty e-tailers, and gourmet subscription boxes. Shelf-stable spreads and freeze-dried crumble fit ambient aisles, reducing shrink relative to fresh. Retailers leverage truffle SKUs as basket builders, pairing them with premium cheese and charcuterie for aspirational home entertaining. E-commerce eliminates geography as a barrier, letting Appalachian foragers sell side-by-side with Périgord estates in curated online marketplaces, a dynamic that injects new storytellers into the global truffle market narrative.

On-trade continues to set taste trends, but its share erodes as at-home cooks replicate restaurant experiences. Chefs still dominate peak-season bidding for Grade Extra noir, ensuring that flagship restaurants remain critical opinion leaders. However, growth now stems from households experimenting with truffle aioli on weeknight burgers, validating that wider availability does not dilute exclusivity; rather, it raises baseline expectations and pulls more consumers into the truffle market funnel.

Geography Analysis

Europe accounted for 42.72% of global revenue in 2025, underpinned by Spain’s 80–90% cultivated share and stringent EU-wide geographical indication rules that protect terroir claims, according to the European Commission data from 2024. Producers in Aragón have installed precision irrigation to offset drought, but cost pressures intensify as water scarcity rises. Northern experiments, including the United Kingdom’s inaugural Périgord harvest, demonstrate that climate adaptation is already migrating center-of-gravity northward, foreshadowing a more dispersed European production base that still anchors the premium reference price for the truffle market.

Asia-Pacific is advancing at a 9.64% CAGR, fueled by China’s 32.5-tonne export leap and Australia’s counter-seasonal shipments that backfill European gaps. Manjimup festivals galvanize domestic tourism and export marketing simultaneously, entrenching Australia as a trusted second-half supplier. According to the Observatory of Economic Complexity data from 2023, Australia imported USD 417 thousand worth of Truffles from Italy, Spain, China, and Croatia. Japanese labs trial controlled-environment chambers for white truffle mycorrhization; if successful, they could decouple Asia’s future supply from soil constraints altogether, a shift that would sharply enlarge truffle market capacity in the world’s most densely populated luxury-goods region.

North America hosts more than 200 orchards aligned with the North American Truffle Growers Association, yet average yields remain one-quarter of French benchmarks, underscoring vast headroom for agronomic gains. Discovery of native species gives the continent a path to build indigenous branding narratives rather than recycling European prestige. State extension services in Oregon, Tennessee and North Carolina now co-fund inoculation greenhouses, signaling policy recognition that truffle market revenues can diversify farm economies. Expanded scientific collaboration across universities promises cultivar breakthroughs that could let North America meet domestic demand internally by the latter half of the decade.

Competitive Landscape

The truffle market exhibits middle-tier concentration with legacy European houses Urbani Tartufi, Sabatino Tartufi, and La Maison Plantin retaining brand authority through centuries-old provenance claims. Their strategy centers on vertical integration: owning orchards, processing rooms, and last-mile distribution. Sabatino’s new Connecticut hub shortens freight times to U.S. coasts and embeds automated cold-chain tracking that documents humidity adherence crate-by-crate, a transparency play aimed at younger, ethics-focused buyers.

Australian players such as The Truffle & Wine Co. leverage Southern Hemisphere seasonality to negotiate premium slots with European wholesalers during the northern off-season, while independent North American orchards pool volumes through cooperative marketing alliances that mimic New World wine consortia. Technology startups supply IoT probes that measure soil carbon flux and mycorrhizal vigor, data that growers use to woo investors seeking ESG-compliant agriculture. Intellectual property emerges around inoculation strains, giving early movers the chance to license genetics and earn royalties, a novel revenue layer within the truffle market.

Regulatory tides also shape competition. The USDA’s latest organic mushroom standards point to a probable similar pathway for truffles; once enacted, certified organic status could command price premiums that narrow the heritage advantage enjoyed by European incumbents. Firms racing to align agronomy with potential rules may seize first-mover claims that re-rank the competitive hierarchy. Meanwhile, marketing spend pivots toward educational content that teaches consumers how to distinguish authentic tubers from synthetic flavor oils, reflecting industry-wide commitment to trust as the cornerstone of sustained truffle market expansion.

Truffle Industry Leaders

-

Urbani Tartufi

-

Sabatino Tartufi

-

La Maison Plantin

-

TruffleHunter Ltd.

-

Australian Truffle Traders

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: La Rustichella, a global luxury truffle brand hailing from Italy, is poised to unveil a new range of products, all 100% certified organic. This new lineup, expanding the brand's already vast portfolio, features organic truffle oil, organic truffle pâté, and organic truffle carpaccio, all tailored for foodservice channels.

- September 2024: Be Truffle brand launched a range of truffle products. The collection includes 32 high-quality truffle-inspired products. The products include mayonnaise, ketchup, Sweet Chili, and others.

- April 2024: Sorrentina launched a new black truffle hot sauce. the product is made from black truffles and fresh red chilis. The product is gluten-free and vegan and can be consumed with products like pizza, pasta, and others.

- May 2023: Hunter and Ganther brand launched a limited edition White Truffle Mayonnaise. The product is made from avocado oil, white truffle oil, pink Himalayan salt, and other ingredients.

Global Truffle Market Report Scope

| Black Truffle |

| White Truffle |

| Burgendy Truffle |

| Chinese Black Truffle |

| Others |

| Fresh |

| Processed (Oils, Pastes, Sauces, Powders) |

| Others (Dried, Frozen) |

| On-Trade |

| Off-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Black Truffle | |

| White Truffle | ||

| Burgendy Truffle | ||

| Chinese Black Truffle | ||

| Others | ||

| Form | Fresh | |

| Processed (Oils, Pastes, Sauces, Powders) | ||

| Others (Dried, Frozen) | ||

| Distribution Channels | On-Trade | |

| Off-Trade | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the truffle market in 2026?

The truffle market stands at USD 2.04 billion in 2026 and is projected to reach USD 2.95 billion by 2031 at a 7.59% CAGR.

Which region is growing fastest in the global truffle market?

Asia-Pacific is the fastest-growing region, expected to post a 9.64% CAGR between 2026 and 2031, powered by rising Chinese exports and Australian counter-seasonal supply.

What product type leads the truffle market?

Black truffles retain leadership with a 47.30% share in 2025, reflecting enduring chef preference and established European heritage.

How are processed truffle products impacting market expansion?

Shelf-stable oils, sauces and powders are widening consumer access, enabling processed formats to log a 6.63% CAGR and bring truffle flavor into mainstream retail.

Page last updated on: