Ghee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

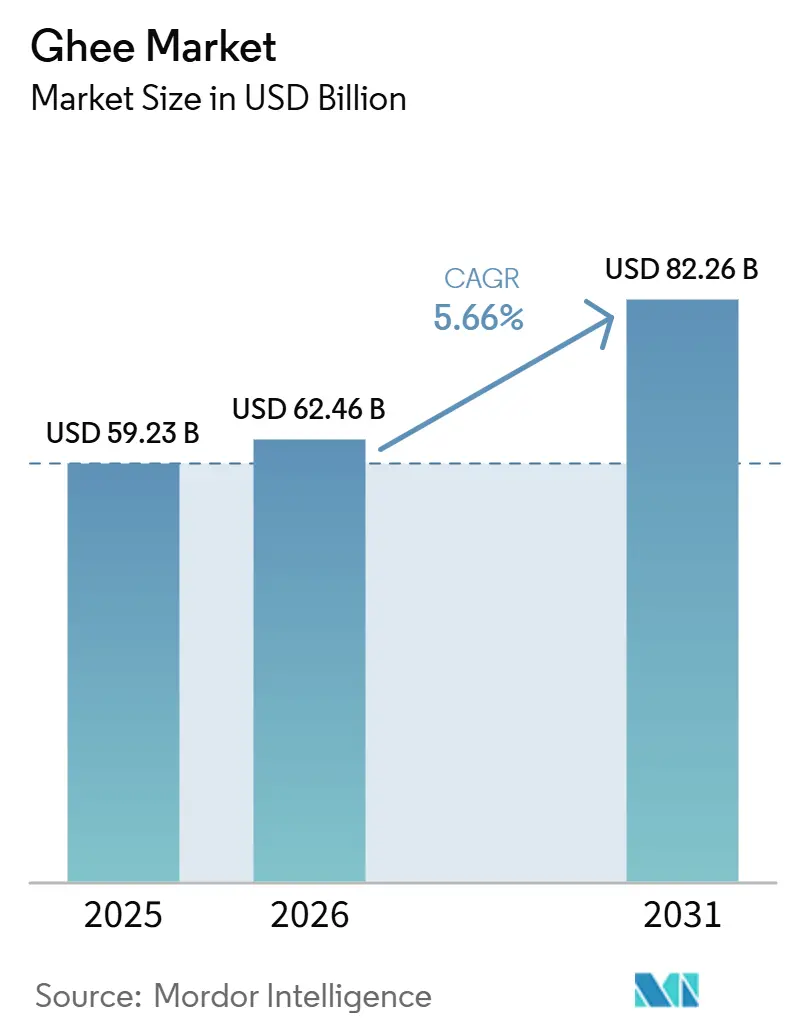

| Market Size (2026) | USD 62.46 Billion |

| Market Size (2031) | USD 82.26 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ghee Market Analysis by Mordor Intelligence

The ghee market size is expected to increase from USD 59.23 billion in 2025 to USD 62.46 billion in 2026 and reach USD 82.26 billion by 2031, growing at a CAGR of 5.66% over 2026-2031. This trajectory reflects a significant shift in consumer perception of clarified butter, which has evolved from being a niche ethnic ingredient to a versatile, health-oriented cooking fat. Ghee now competes directly with seed oils, plant-based spreads, and conventional butter. Meanwhile, North American and European markets are witnessing rising demand for premium grass-fed and A2 ghee variants, priced 30-50% higher than commodity ghee, indicating strong premiumization. This geographic divergence underscores two parallel growth drivers: traditional consumption rooted in South Asian culinary practices and diaspora demand, alongside wellness-driven adoption in Western markets. In these regions, ghee is positioned as a clean-label, high-smoke-point fat, competing with alternatives like coconut oil and avocado oil.

Key Report Takeaways

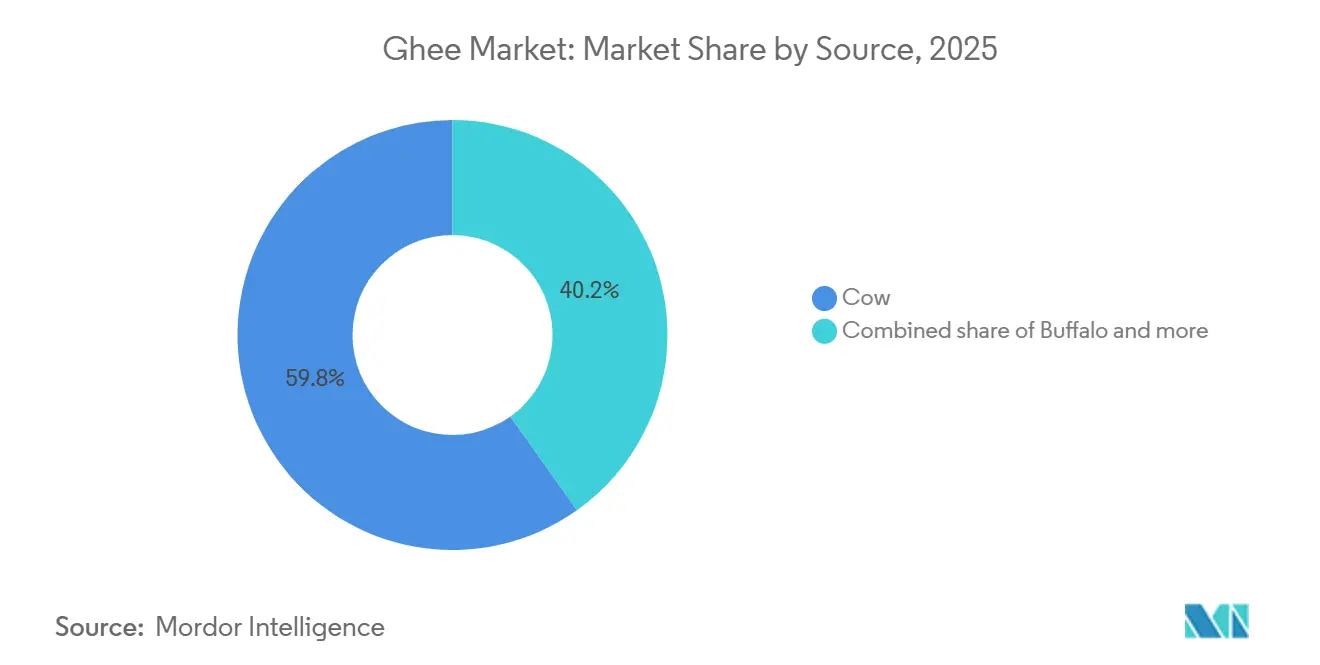

- By source, cow ghee led with 59.85% of the ghee market share in 2025, while buffalo ghee is expanding at a 7.02% CAGR through 2031.

- By nature, conventional products captured 85.49% of the ghee market in 2025; organic ghee is projected to grow at a 7.86% CAGR during 2026-2031.

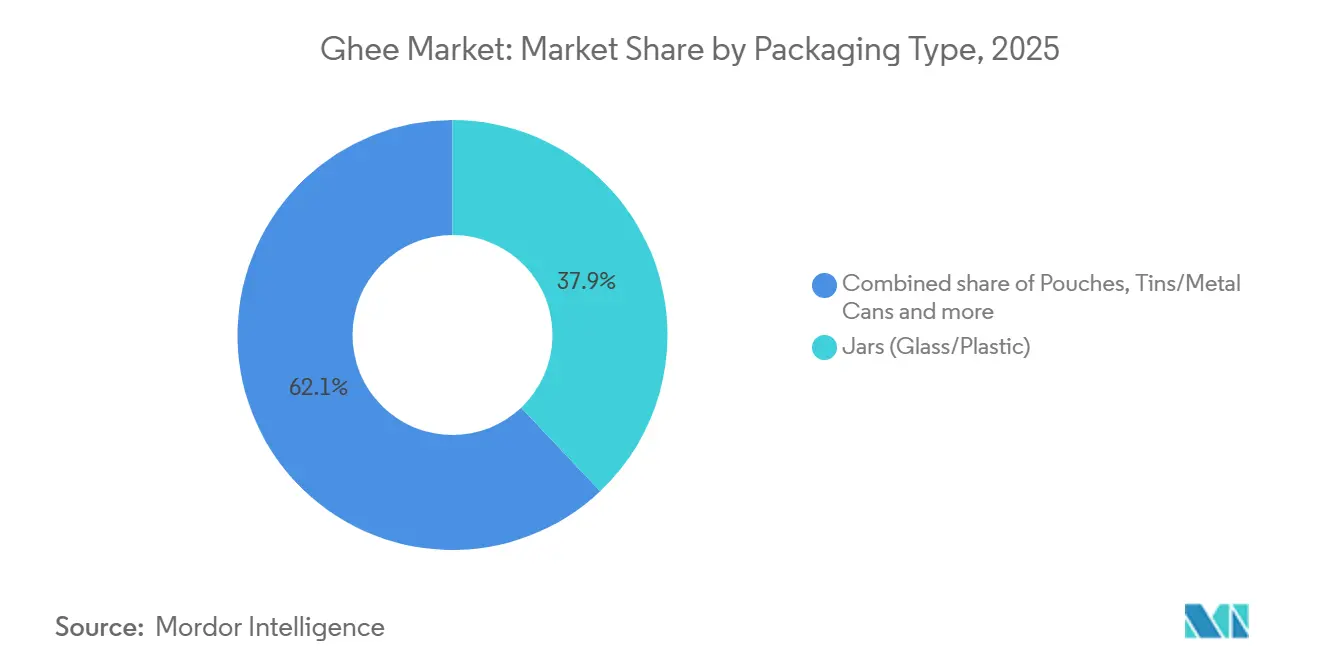

- By packaging type, jars accounted for 37.98% of 2025 sales, whereas pouches are set to post a 6.33% CAGR to 2031.

- By distribution, retail channels dominated with 68.14% share in 2025; institutional procurement is forecast to climb at a 6.71% CAGR during 2026-2031.

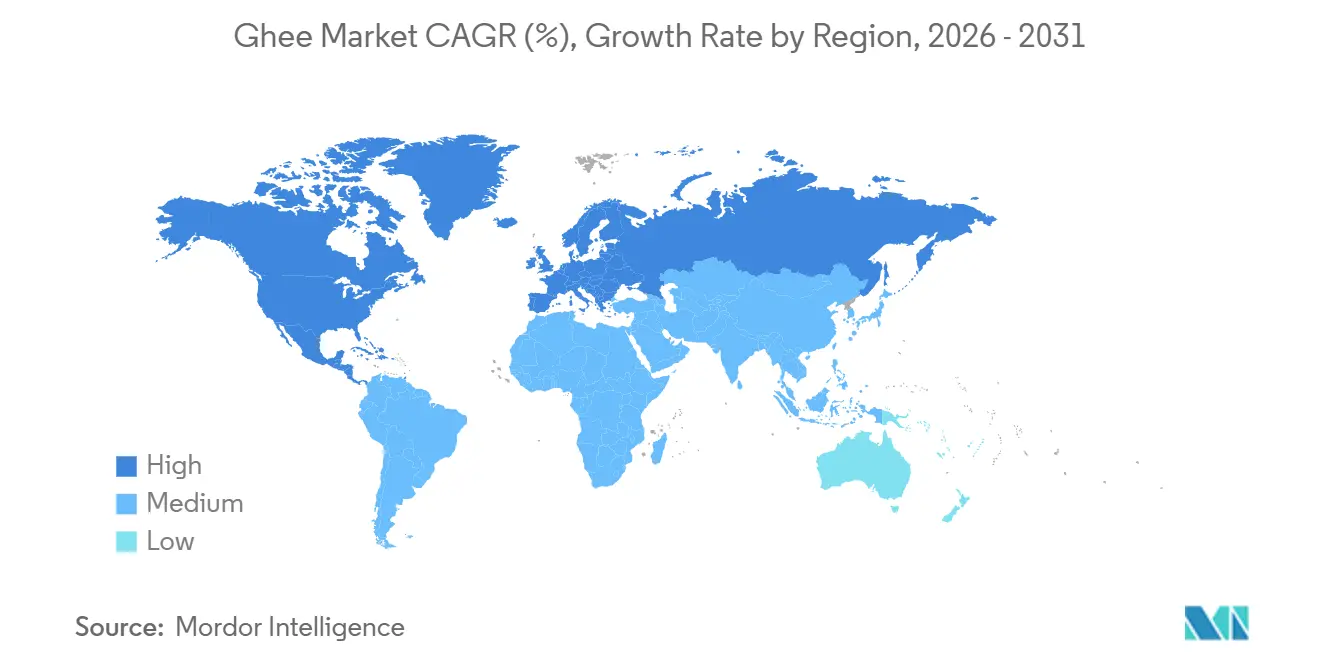

- By geography, Asia-Pacific commanded 76.53% of the ghee market in 2025, while North America is the fastest-growing region at a projected 7.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ghee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-smoke-point animal fats | +0.9% | Global, with strong uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Surge in organic, grass-fed and A2 ghee launches | +1.2% | North America, Europe, premium urban segments in India and Gulf Cooperation Council | Long term (≥ 4 years) |

| Expansion of organized retail and e-commerce channels | +1.0% | Global, led by India, North America, Gulf Cooperation Council; rapid in Tier-1/Tier-2 cities | Short term (≤ 2 years) |

| Growing adoption in specialized diets such as keto, paleo, and others | +0.8% | North America, Europe, Australia; emerging in urban India | Medium term (2-4 years) |

| Increasing awareness of digestive and therapeutic benefits | +0.7% | Global, with peer-reviewed evidence driving adoption in wellness segments | Long term (≥ 4 years) |

| Expanding applications across global cuisines | +0.6% | Global, particularly North America, Europe, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for high-smoke-point animal fats

Ghee's high smoke point of 485°F, which exceeds butter (350°F), coconut oil (350°F), and most seed oils, is increasingly appealing to professional kitchens and home cooks. This advantage allows for high-heat searing, roasting, and deep-frying without compromising flavor or producing toxic aldehydes. Institutional adoption is on the rise, with hospitality procurement guides recommending A2 Bilona ghee for banquet cooking, where prolonged heat exposure of 4-6 hours demands superior stability. Luxury hotels are now allocating dedicated monthly budgets for ghee in restaurant kitchens, reflecting a broader shift away from partially hydrogenated oils toward clean-label fats that deliver both culinary performance and health benefits. Regulatory developments further support this trend, as the U.S. Food and Drug Administration and European Food Safety Authority continue to favor dairy fats while imposing stricter regulations on industrial trans fats. This indirectly highlights ghee's ruminant trans fatty acid profile (approximately 2.4% vaccenic acid) as a preferable alternative to synthetic options.

Surge in organic, grass-fed and A2 ghee launches

Organic A2 milk sales are increasing in North America, reflecting strong consumer demand for products associated with digestibility and purity claims. Ghee producers are leveraging this trend to expand their market share. The A2 beta-casein positioning resonates with consumers who report lactose intolerance or digestive discomfort with A1 dairy, although clinical evidence remains inconclusive, and regulatory bodies caution against exaggerated health claims. Certifications such as United States Department of Agriculture Organic, European Union Organic, and India Organic are becoming essential for accessing export markets and securing premium retail placements. However, these certifications come with added compliance costs, including facility audits, traceability systems, and third-party testing, which tend to favor larger players or cooperative networks with the scale to absorb these expenses. The market is increasingly bifurcating into two segments: commodity ghee, which competes on price and volume, and premium variants, such as certified organic and A2 ghee, which command 30-50% higher price points. These premium products cater to wellness-conscious consumers who prioritize provenance, clean-label attributes, and perceived health benefits over cost.

Expansion of organized retail and e-commerce channels

Quick-commerce platforms such as Blinkit, Zepto, and Swiggy Instamart are revolutionizing dairy distribution in India's Tier-1 cities. These platforms have reduced delivery windows to 10-15 minutes, compelling manufacturers to innovate with tamper-proof, leak-resistant packaging and smaller SKUs (200g, 500g) tailored for rapid fulfillment and urban refrigerator constraints. Subscription models are also gaining popularity, offering brands recurring revenue streams and opportunities to cross-sell ghee and other value-added dairy products. Digital-first brands are outperforming traditional players in urban markets. For instance, Parag Milk Foods introduced a 20ml Gowardhan cow ghee sachet priced at INR 20, targeting first-time and value-conscious consumers by combining affordability with brand trial. Additionally, premium ghee variants, such as organic and A2-certified options, are leveraging e-commerce platforms to reach health-conscious segments willing to pay a premium for quality and provenance.

Increasing awareness of digestive and therapeutic benefits

Ghee contains butyric acid (approximately 3g per 100g in butter and ghee), a short-chain fatty acid that supports colonocyte health, strengthens intestinal barrier integrity, reduces inflammation through Histone deacetylases (HDAC) inhibition, and modulates immune signaling via GPR41, GPR43, and GPR109A receptors. In livestock, butyrate supplementation enhances rumen development, increases milk yield, and improves gut microbiota diversity, providing a biological basis for digestive health claims, though human RCTs remain limited and varied. Ayurvedic literature highlights ghee's role in promoting agni (digestive function), with modern recommendations suggesting 1-2 teaspoons daily as a finishing fat or for tadka to enhance fat-soluble nutrient absorption and support fiber-driven microbial butyrate production. Properly clarified ghee eliminates approximately 99% of lactose and casein, making it suitable for many individuals with lactose intolerance. This claim is supported by batch testing, which shows lactose levels ≤0.25% and casein/whey ≤2.5 ppm in cultured ghee. This digestibility narrative is driving consumer adoption, particularly among those seeking alternatives to plant-based butters or seed oils, and individuals experiencing bloating or inflammation associated with A1 dairy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-milk price volatility | -0.8% | Global, acute in India, Gulf Cooperation Council; climate-linked in South Asia | Short term (≤ 2 years) |

| Increasing competition from alternative fats and oils | -0.6% | North America, Europe; emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Adulteration and quality concerns | -0.5% | India, South Asia; sporadic in export markets | Short term (≤ 2 years) |

| Regulatory and quality compliance challenges | -0.4% | Global, particularly cross-border trade (India-United States, India-European Union) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-milk price volatility

Milk procurement costs surged across major Indian dairy processors in 2025, compressing gross margins and prompting retail price adjustments that could affect demand elasticity. Despite India's milk production increasing from 146.30 million tonnes in 2014-15 to 239.30 million tonnes in 2023-24, per capita availability grew only to 471g per person per day due to population growth [1]Source: Press Information Bureau of India (PIB), "National Milk Day," pib.gov.in. This limited surplus leaves the market vulnerable to seasonal or climate-driven supply shocks. Variations in feed prices have further influenced milk production economics, while seasonal supply fluctuations, weather disruptions, and global commodity market trends exacerbate input cost volatility for ghee processors. In India, the world's largest ghee market, the Office of the Economic Adviser reported that the Wholesale Price Index (WPI) of milk rose to over 192.1 in February 2026 from 180 in FY 2024, reflecting escalating raw material costs[2]Source: Office of Economic Adviser, India, "cmonthly.pdf," eaindustry.nic.in. Ghee manufacturers face a dual challenge: rising input costs and subdued ghee pricing, which limit cost pass-through and compress profit margins.

Increasing competition from alternative fats and oils

Plant-based butter alternatives, avocado oil, and coconut oil are gaining traction in North America and Europe, particularly among vegan, environmentally conscious, and health-focused consumers who view dairy fats as misaligned with sustainability or cardiovascular health objectives. Regulatory measures, such as the U.S. Food and Drug Administration's ban on partial hydrogenation and the World Health Organization's REPLACE initiative, have prompted margarine reformulations to eliminate industrial trans fats, allowing these products to be positioned as lower-saturated-fat alternatives to ghee and butter [3]Source: World Health Organization (WHO), "REPLACE Trans fat-free," who.int. Coconut oil and avocado oil compete by leveraging clean-label attributes, high smoke points (coconut ~350°F, avocado ~520°F), and plant-based appeal, though both face sustainability concerns, including deforestation for coconut plantations and the water-intensive nature of avocado farming. Ghee's competitive strategy relies on differentiation, highlighting the benign profile of ruminant trans fats, CLA content, fat-soluble vitamins (A, D, E, K), and its cultural authenticity. However, longstanding dietary guidelines cautioning against saturated fat consumption pose challenges, as ghee's 66-73% saturated fat content positions it less favorably compared to seed oils or reformulated margarines in mainstream health discussions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Buffalo Gains on Fat Yield and Regional Preference

Cow-sourced ghee accounted for 59.85% of the market share in 2025, underscoring its dominance in South and East India as well as export markets. Its lighter flavor profile and higher unsaturated fatty acid content appeal to health-conscious consumers and align with Western dietary preferences. The increasing contribution of crossbred cows, which now produce 30.8% of India's milk output, has become the single largest source of milk. This shift in raw milk composition is influencing ghee fat yields and flavor profiles, prompting dairy processors to adapt formulations to accommodate variable milk-fat percentages. Additionally, cow ghee is often marketed for its perceived health benefits, including its rich content of omega-3 fatty acids and fat-soluble vitamins, which resonate with consumers seeking functional foods.

Buffalo ghee is projected to grow at a 7.02% CAGR through 2031, driven by strong demand in North India and Middle Eastern markets. Its higher fat content (buffalo milk contains 64-67% saturated fatty acids compared to cow milk's 52-66%) results in superior yield, a richer mouthfeel, and a stronger lactic aroma, which are highly valued in traditional cooking. Buffalo ghee is often rated higher in global quality due to its pronounced lactic odor and fatty taste, making it a preferred choice for culinary applications that require robust flavors. However, cow ghee has exhibited higher acid values, indicating greater susceptibility to rancidity over time, which could influence storage and shelf-life considerations. The growing popularity of buffalo ghee is also supported by its use in premium and artisanal food products, as well as its cultural significance in traditional recipes, further solidifying its position in the market.

By Nature: Organic Certification Drives Premium Positioning

Conventional ghee retained 85.49% of market share in 2025, driven by strong demand from price-sensitive mass-market consumers and widespread distribution through cooperatives such as Amul, Mother Dairy, and Nandini, as well as private brands like Parag and Heritage. These players focus on high-volume production and affordability, ensuring accessibility to a broad consumer base. The dominance of conventional ghee is further supported by its deep-rooted cultural significance in Indian households, where it is a staple in traditional cooking and rituals. Additionally, the product benefits from established supply chains and economies of scale, which allow manufacturers to maintain competitive pricing.

Organic ghee is projected to grow at a CAGR of 7.86% through 2031, fueled by rising consumer awareness of clean-label products and the growing importance of certifications such as United States Department of Agriculture Organic, EU Organic, and India Organic. These certifications are becoming essential for accessing export markets, securing premium retail shelf space, and appealing to health-conscious urban consumers willing to pay a premium for perceived purity and environmental sustainability. However, achieving organic certification entails significant compliance costs, including facility audits, traceability systems, third-party testing, and organic feed premiums. These requirements often favor larger players or cooperative networks with the scale to absorb such costs, creating barriers to entry for smaller producers. Additionally, brands are leveraging organic and grass-fed claims to differentiate themselves in an increasingly saturated market.

By Packaging Type: Flexible Formats Gain on Sustainability and Shelf Life

Jars (plastic and glass) accounted for 37.98% of packaging share in 2025, favored for premium retail where transparency, reusability, and perceived quality justify higher unit costs, particularly for artisanal and organic brands targeting health-conscious consumers. Glass jars, in particular, are preferred for their ability to preserve product freshness and prevent contamination, making them ideal for high-value products. Innovations in jar designs, such as lightweight glass and tamper-evident closures, are further driving their adoption in the market.

Flexible pouches are forecast to grow at 6.33% CAGR through 2031, driven by innovations in sonic-sealed spouts, aseptic bag-in-box formats, and recyclable mono-materials that extend ambient shelf life without refrigeration or preservatives, enabling wider geographic distribution and reducing cold-chain dependency. Pouches are increasingly favored for their lightweight nature, cost-effectiveness, and convenience, particularly in single-serve and on-the-go formats. Their ability to accommodate advanced printing technologies also allows brands to enhance product visibility and communicate key attributes such as sustainability and nutritional benefits.

By Distribution Channel: Institutional Channels Accelerate on Premiumization

Retail channels dominated with 68.14% of market share in 2025, spanning supermarkets, hypermarkets, specialty stores, convenience stores, and online retail, reflecting ghee's transition from ethnic ingredient to mainstream cooking fat and wellness product. Quick-commerce platforms such as Blinkit, Zepto, and Swiggy Instamart are reshaping retail distribution in India's Tier-1 and 2 cities. Specialty stores and online retail cater to premium and organic segments. Supermarkets and hypermarkets provide mass-market reach. Convenience and grocery stores serve traditional and rural markets where cooperatives (Amul, Nandini, Mother Dairy) maintain dominance through extensive kirana networks and brand equity built over decades.

Institutional channels (hotels, restaurants, catering services, and food processors) are forecast to grow at a CAGR of 6.71% through 2031, driven by the increasing adoption of premium A2 Bilona ghee in hospitality kitchens. Its high smoke-point stability (250-260°C) and authentic flavor profiles make it a preferred choice for culinary applications, particularly in high-end hotels and fine-dining restaurants. Additionally, the growing trend of incorporating traditional and regional cuisines into menus has further boosted demand for ghee in institutional settings. Bulk packaging formats, such as tins and large pouches, are widely used in this segment to ensure cost efficiency and ease of handling. Food processors are also leveraging ghee as a key ingredient in ready-to-eat meals, snacks, and bakery products, aligning with consumer preferences for authentic and natural ingredients. The institutional segment's growth is further supported by partnerships between ghee manufacturers and large-scale catering services, which ensure consistent supply and quality for large-volume requirements.

Geography Analysis

Asia-Pacific held 76.53% of the market share in 2025, driven by India's position as the world's largest producer and consumer of ghee. Domestic milk production reached 248 million tonnes in 2024-25, supported by government initiatives, including the National Dairy Development Board's (NDDB) efforts to enhance milk yield and quality. Regulatory protection continues to play a significant role, as India's trade agreements with the United States and the European Union exclude dairy imports. This protection safeguards approximately 100 million milk producers from subsidized foreign competition, ensuring domestic price stability and fostering rural economic growth. Additionally, the growing popularity of traditional Ayurvedic practices in the region has further boosted ghee consumption, particularly in urban areas where health-conscious consumers are seeking natural, functional food products.

North America is forecast to grow at a 7.48% CAGR through 2031, marking the fastest growth among all regions. This growth is fueled by wellness-driven adoption, where ghee is increasingly positioned as a clean-label, high-smoke-point fat alongside alternatives like coconut oil and avocado oil. Its compatibility with ketogenic, paleo, and Whole30 diets has significantly contributed to its popularity among health-conscious consumers. Organic A2 milk sales in Northern California and the Southwest grew by 83% in 2024, reflecting a strong consumer willingness to pay premiums for products with perceived digestibility and purity claims. Furthermore, the region has seen an increase in product innovation, such as flavored ghee variants and convenient packaging formats, catering to the evolving preferences of younger demographics and busy households.

Europe exhibits moderate growth, supported by the rising demand for clean-label products and a strong preference for organic certifications. The region's specialty stores play a crucial role in distributing premium ghee products, particularly those marketed as grass-fed or sourced from A2 milk. Additionally, the growing awareness of ghee's health benefits, such as its role in improving digestion and providing essential fatty acids, has driven its adoption among health-conscious consumers. The Middle East and Africa, particularly the Gulf Cooperation Council countries, exhibit strong traditional consumption patterns alongside modern retail expansion. Ghee remains a staple in Middle Eastern cuisine, used extensively in both sweet and savory dishes.

Competitive Landscape

The global ghee market exhibits moderate fragmentation, characterized by the coexistence of regional cooperatives (Amul, Nandini, Mother Dairy), private value-added players (Parag, Heritage, Britannia), and artisanal exporters targeting niche segments. Cooperatives leverage their extensive scale and farmer networks; for instance, Amul connects 3.6 million milk producers across more than 18,500 villages in Gujarat, ensuring a steady supply chain and cost efficiency. Private players are increasingly focusing on premiumization and digital-first strategies to capture evolving consumer preferences. Additionally, the rise of private-label ghee brands in organized retail channels is intensifying competition, particularly in urban markets.

Emerging opportunities are evident in premium organic, A2, and grass-fed ghee segments, where certification, traceability, and substantiated health claims create competitive advantages against commoditized offerings. These segments are witnessing growing demand from health-conscious consumers who prioritize purity, digestibility, and ethical sourcing. Disruptors in this space include direct-to-consumer artisanal brands (Kimmus Kitchen, Authentic Urban, Nuclear Farm) that leverage social media platforms like Instagram, e-commerce, and video-verified sourcing to appeal to wellness-focused buyers. These brands are successfully capturing a niche audience willing to pay premiums for products made using traditional methods, such as the bilona process, which enhances the perceived authenticity and nutritional value of the ghee.

Technology adoption is playing a pivotal role in driving competitive differentiation within the ghee market. For example, Amul launched its "Amul AI" platform in February 2026, integrating data from 3.6 million farmers and cooperative members into a centralized system. The accompanying "Sarala" mobile app provides real-time updates on milk fat content, SNF (solids-not-fat), and daily accounts, enabling smarter procurement, quality monitoring, and yield optimization such as factors directly impacting ghee production efficiency. Packaging innovation is another critical area of focus, with brands adopting sustainable solutions such as recyclable mono-materials and reduced plastic usage to align with consumer demand for eco-friendly products. These advancements not only reduce cold-chain costs but also extend distribution reach, particularly in export markets. Regulatory compliance is becoming an increasingly significant factor in the ghee market, creating both opportunities and challenges for industry players.

Ghee Industry Leaders

-

Amul (Gujarat Co-operative Milk Marketing Federation Limited)

-

Patanjali Ayurved

-

Mother Dairy

-

Nestlé S.A.

-

VRS Foods (Paras)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Amul launched Amul AI, a digital platform integrating 3.6 million farmer and cooperative-member databases with an AI-driven "Sarala" mobile app that provides milk fat, SNF, and daily accounts to farmers, positioning it as the world's first such delivery system and a milestone in dairy sector modernization.

- September 2025: Amul reduced MRPs across more than 700 product packs to pass on GST rate-cut benefits, including a INR 40 per liter reduction in ghee price to INR 610 per liter, aiming to spur consumption and boost demand amid low per-capita dairy consumption in India.

- February 2025: Clover Sonoma launched Pasture Raised Organic A2 4% Whole Milk at USD 7.49 per unit, sourced from Jersey and Guernsey cows on California's largest organic regenerative farmland.

Global Ghee Market Report Scope

The ghee market is segmented by source, nature, packaging type, distribution channel, and geography. By source, the market is segmented into cow, buffalo, and other. By nature, the market is segmented into conventional and organic. By packaging type, the market is segmented into jars (glass/plastic), tins/metal cans, pouches, cartons/boxes, and sachets. By distribution channels, the market has been segmented into institutional (hotels, restaurants, food processors) and retail. By retail, the market has been segmented into hypermarkets/supermarkets, convenience/grocery stores, specialty stores, online retail stores, and other distribution channels. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Cow |

| Buffalo |

| Other |

| Organic |

| Conventional |

| Jars (Glass/Plastic) |

| Tins/Metal Cans |

| Pouches |

| Cartons/Boxes |

| Sachets |

| Institutional (Hotels, Restaurants, Food Processors) | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Source | Cow | |

| Buffalo | ||

| Other | ||

| By Nature | Organic | |

| Conventional | ||

| By Packaging Type | Jars (Glass/Plastic) | |

| Tins/Metal Cans | ||

| Pouches | ||

| Cartons/Boxes | ||

| Sachets | ||

| By Distribution Channel | Institutional (Hotels, Restaurants, Food Processors) | |

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the ghee market by 2031?

The ghee market is forecast to reach USD 82.26 billion by 2031 and is forecast to register a 5.66% CAGR.

Which region is expanding the quickest?

North America is projected to post the fastest regional growth at 7.48% CAGR through 2031 as keto and clean-label trends drive uptake.

How fast is organic ghee expected to grow?

The organic ghee segment is set to expand at a 7.86% CAGR through 2031, outpacing conventional ghee.

What packaging formats will dominate future sales?

Pouches are expected to outpace jars, growing at 6.33% CAGR, propelled by recyclable mono-materials and extended ambient shelf life.

Page last updated on: