Razor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.06 Billion |

| Market Size (2031) | USD 14.05 Billion |

| Growth Rate (2026 - 2031) | 3.90% CAGR |

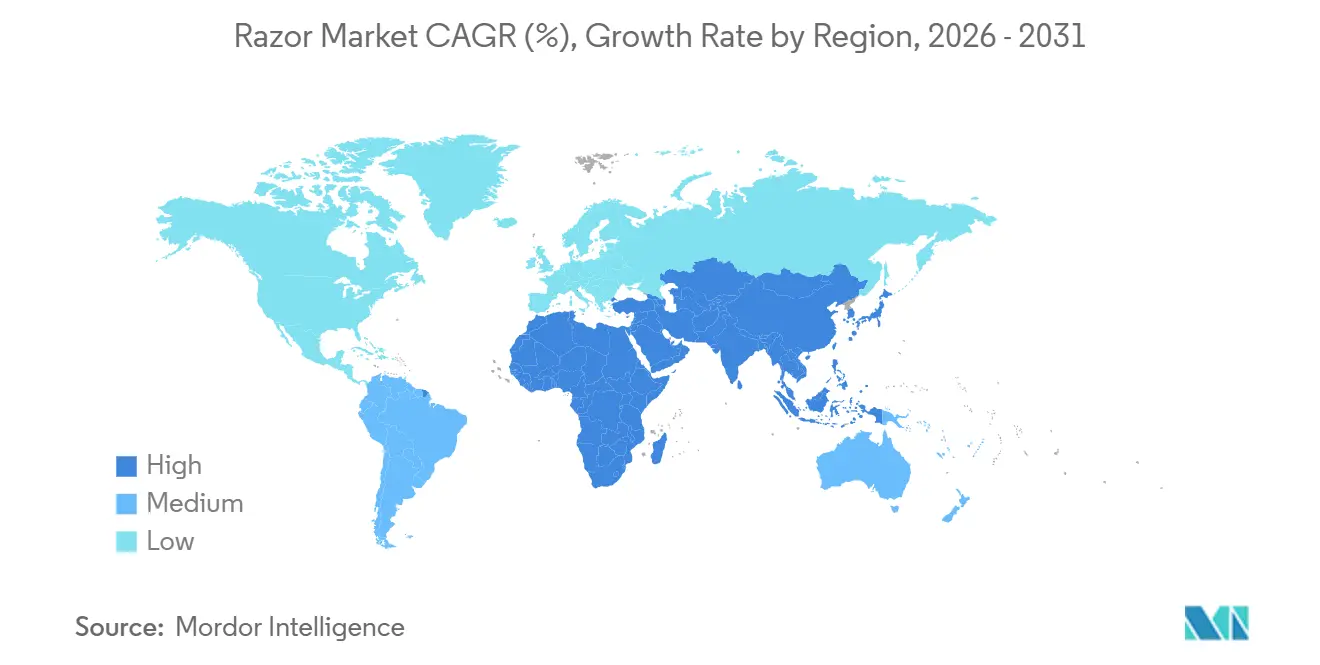

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Razor Market Analysis by Mordor Intelligence

The razor market size is projected to expand from USD 11.62 billion in 2025 and USD 12.06 billion in 2026 to USD 14.05 billion by 2031, registering a 3.9% CAGR between 2026 and 2031. This steady expansion is increasingly driven by premiumization, the rapid adoption of e-commerce subscription models, and deeper penetration across emerging markets. Rising disposable incomes and a growing middle-class population in Asia-Pacific continue to anchor global demand, while developed markets are witnessing a shift toward higher-value products rather than volume growth. Sustainability considerations are becoming central to product development, as regulatory pressures and consumer preferences accelerate the adoption of eco-friendly materials, refillable formats, and reduced plastic usage. While traditional constraints such as beard fashion trends and the increasing use of electric grooming devices continue to moderate demand in mature markets, ongoing innovation in product design and materials is helping manufacturers maintain pricing power and extend product life cycles.

Key Report Takeaways

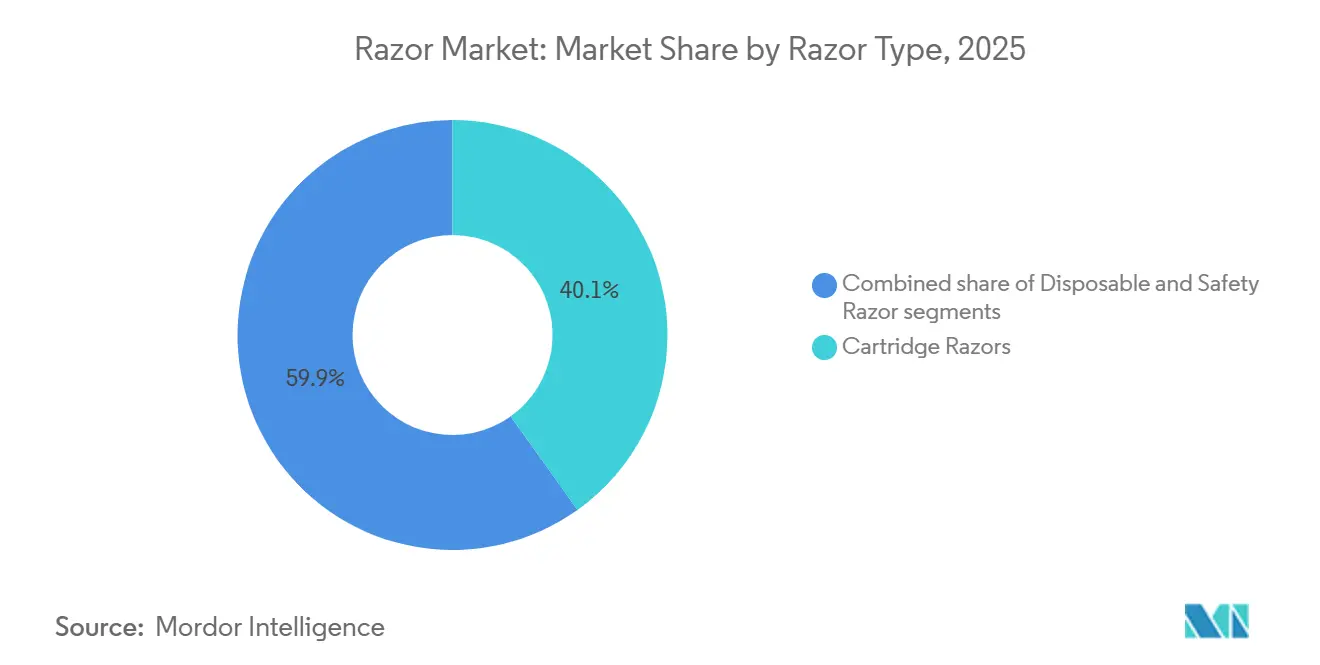

- By razor type, cartridge razors led with 40.12% revenue in 2025 and are forecast to expand at a 4.16% CAGR through 2031.

- By end-user, men accounted for 68.95% of the razor market share in 2025, whereas women are poised for the fastest 4.60% CAGR through 2031.

- By price range, mass products represented 70.30% of 2025 sales; premium lines are projected to grow at a 4.85% CAGR during 2026-2031.

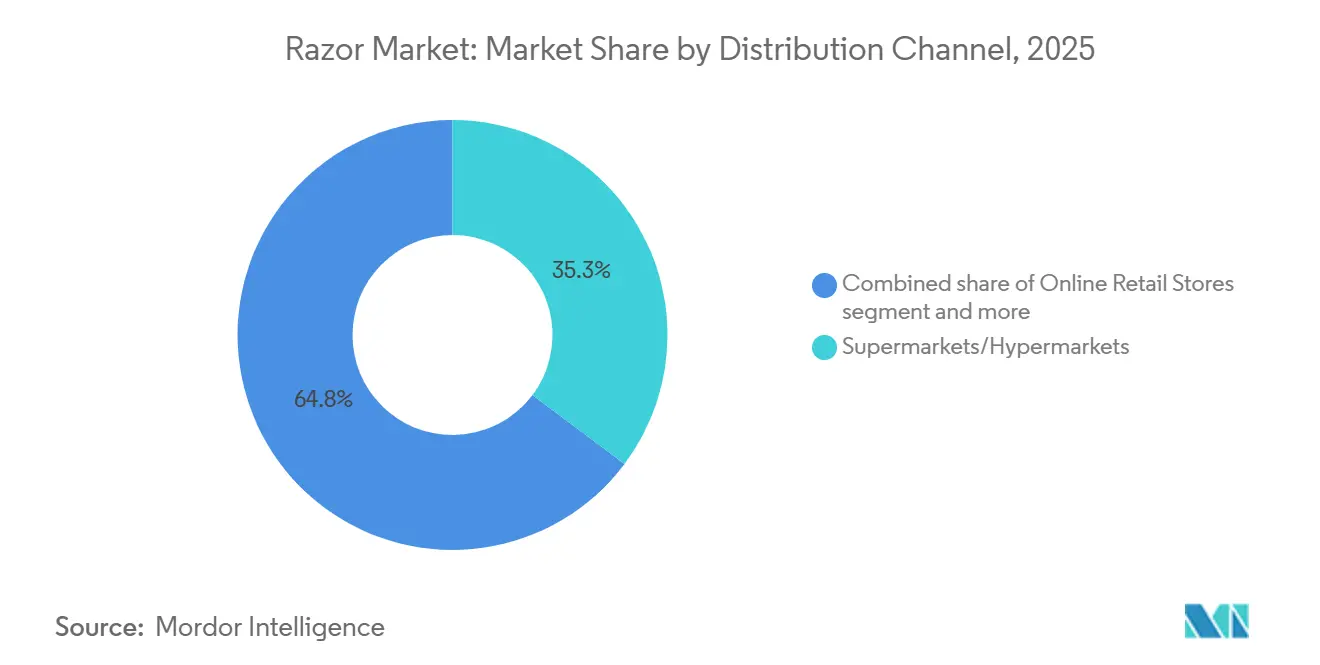

- By distribution channel, supermarkets and hypermarkets held 35.25% of 2025 turnover, yet online retailers are rising at a 5.70% CAGR during 2026-2031.

- By geography, Asia-Pacific commanded 35.30% of 2025 revenue and is expected to post a 4.90% CAGR through 2031, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Razor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Male Grooming and Personal Care Adoption | +0.8% | Global, with strongest impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Rapid Growth of Direct-to-Consumer Subscription Models | +0.6% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Increasing Consumer Shift Toward Sustainable and Eco-Friendly Products | +0.5% | Europe, North America, APAC premium segments | Long term (≥ 4 years) |

| Rising Demand for Dermatologically Tested and Sensitive-Skin Solutions | +0.4% | Global, with premium positioning in developed markets | Medium term (2-4 years) |

| Continuous Product Innovation and Technology Integration | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Accelerating Participation of Female Consumers in Grooming Products | +0.5% | Global, with fastest growth in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Male Grooming and Personal Care Adoption

The growing emphasis on male grooming continues to reshape global razor market dynamics, as shaving becomes increasingly embedded within broader personal care and lifestyle routines rather than remaining a basic hygiene activity. This shift is especially evident in Asia-Pacific, where rapid urbanization and rising disposable incomes are fostering demand for higher-quality grooming products. According to the National Bureau of Statistics of China, the country’s per capita disposable income reached CNY 41,314 in 2024, reflecting a steady rise in consumer purchasing power and lifestyle spending [1]Source: National Bureau of Statistics of China, "Statistical Communiqué on the 2024 National Economic and Social Development", stats.gov.cn. In developed markets like Japan, steady growth in men’s skincare is reinforcing adjacent demand for premium shaving systems, particularly those integrated with pre- and post-shave care solutions. This evolution is further supported by younger consumers, especially those aged 18–34, who increasingly associate grooming with personal branding and social presentation. As a result, they are more inclined to adopt subscription-based models and higher-end multi-blade systems tailored for skin sensitivity. Collectively, these trends are encouraging manufacturers to reposition razors as value-added, lifestyle-oriented products, enabling premium pricing strategies and stronger customer retention.

Rapid Growth of Direct-to-Consumer (DTC) Subscription Models

The subscription economy is fundamentally transforming the razor industry by shifting competitive advantage toward direct-to-consumer (DTC) models that prioritize convenience, recurring revenue, and customer lifetime value. Subscription-based offerings enable both emerging entrants and incumbent players to build stronger consumer relationships through personalized assortments, automated replenishment, and data-driven product innovation. Both startups and established players use subscriptions to secure recurring revenue and drive product innovation. This shift is supported by growing global internet access; by 2023, over 5.4 billion people, two-thirds of the global population, were online, according to the International Telecommunication Union (ITU) [2]Source: International Telecommunication Union, "Facts and Figures 2023: Almost universal connectivity but still a digital divide", itu.int. However, subscriber retention remains a key challenge, as consumers increasingly expect flexibility, pricing transparency, and alignment with evolving preferences. To address this, established players are adopting hybrid go-to-market models that integrate subscription services with traditional retail channels, while offering customizable plans and frictionless user experiences. Overall, the shift toward subscription-driven commerce is redefining competitive dynamics in the razor market, with success increasingly dependent on a brand’s ability to deliver convenience, personalization, and continuous engagement alongside product performance.

Increasing Consumer Shift Toward Sustainable and Eco-Friendly Products

Driven by rising environmental awareness, the demand for sustainable shaving solutions is accelerating, making sustainability a baseline expectation rather than a differentiator. A growing share of consumers is actively reconsidering brand choices based on environmental impact, with a majority indicating willingness to switch to products offering greener packaging and reduced plastic usage. This shift is further reflected in the gradual adoption of safety razors and other low-waste alternatives aimed at minimizing disposable plastic consumption. Regulatory developments are reinforcing this transition, particularly in Europe, where evolving frameworks such as the EU’s Packaging and Packaging Waste Regulation are set to restrict certain forms of single-use packaging by 2030. These measures are compelling manufacturers to rethink product design, accelerating the shift toward refillable cartridge systems, durable metal handles, and biobased materials that align with circular economy principles. Similarly, increasing scrutiny around microplastics and their potential environmental and health implications is expected to further influence regulatory direction and consumer preferences. As a result, markets, particularly in Europe, are witnessing strong momentum toward zero-waste and low-impact grooming solutions.

Rising Demand for Dermatologically Tested and Sensitive-Skin Solutions

As consumers become increasingly discerning about personal care, razors are evolving to prioritize skin health alongside core shaving performance. A significant proportion of regular shavers report experiencing skin sensitivity, reinforcing the need for products that minimize irritation, razor burn, and ingrown hairs. A 2025 epidemiological study conducted on over 600 adults in Thailand revealed that a significant 86.9% reported having sensitive skin. Among them, 57.5% faced moderate to severe sensitivity [3]Source: National Library of Medicine (NLM), "Sensitive Skin in Thais: Prevalence, Clinical Characteristics, and Diagnostic Cutoff Scores", ncbi.nlm.nih.gov. Leading brands are responding with targeted innovations. For instance, Procter & Gamble’s Gillette SkinGuard Sensitive incorporates specialized guard technology to reduce blade contact with the skin, thereby lowering irritation and improving comfort for sensitive users. In the women’s segment, product development is increasingly focused on sensitive areas, with solutions tailored for underarm and bikini use, incorporating dermatologically and gynecologically tested formulations. Limited-edition collaborations and design-led variations are also being leveraged to drive repeat purchases while maintaining core product performance. At the regulatory level, tightening standards around product safety and biocompatibility, supported by frameworks such as ISO 10993 and increasing oversight from health authorities, are elevating the importance of clinical validation. As a result, brands that can substantiate skin-safe claims through rigorous testing and expert endorsement are better positioned to build consumer trust, justify premium pricing, and differentiate in an increasingly competitive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Popularity of Beard and Low-Shave Grooming Trends | -0.4% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Substitution Threat from Electric Grooming Devices and Laser Treatments | -0.5% | Developed markets, expanding to urban areas in emerging economies | Long term (≥ 4 years) |

| Regulatory Pressures on Single-Use Plastics and Disposable Products | -0.3% | Europe leading, with global regulatory spillover expected | Long term (≥ 4 years) |

| Pricing Pressures Due to Scrutiny on Gender-Based Premiums | -0.2% | North America and Europe, with regulatory attention increasing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Popularity of Beard and Low-Shave Grooming Trends

The growing cultural acceptance of facial hair continues to act as a structural restraint on the traditional razor market, as beard and stubble styles gain widespread acceptance across age groups and regions. This shift reflects evolving aesthetic preferences, particularly among younger consumers, where facial hair is increasingly associated with personal identity and style. Over the past decade, this trend has contributed to a measurable decline in shaving frequency, with razor usage volumes experiencing moderate contraction as consumers move away from daily clean-shave routines. Similarly, alternative grooming solutions have gained prominence, with beard trimmers now accounting for a substantial share of male electric grooming sales. Seasonal and cultural movements such as “Movember” further reinforce this trend, significantly boosting demand for beard-care products and normalizing facial hair among younger demographics. In parallel, barbershops are experiencing a notable resurgence, redirecting a portion of consumer spending from at-home shaving products toward professional grooming services and curated beard maintenance. Brands that successfully adapt by addressing hybrid grooming needs and expanding into beard care ecosystems are better positioned to mitigate volume pressures and sustain long-term relevance in the evolving razor market.

Substitution Threat from Electric Grooming Devices and Laser Treatments

Alternative hair removal technologies, including electric shavers and laser-based solutions, are increasingly constraining growth in the traditional razor market, particularly in developed regions. A significant share of male consumers has already adopted electric grooming devices, driven by advancements in motor efficiency, AI-assisted performance, and self-cleaning systems that enhance convenience and reduce preparation time. These innovations are narrowing the performance gap with manual razors while offering a faster and more user-friendly grooming experience. The shift is further reinforced by evolving consumer needs, particularly among individuals experiencing hair loss, where specialized electric head shavers are gaining traction due to their speed and ease of use. Despite these competitive pressures, wet shaving continues to maintain an advantage in terms of closeness of shave and lower per-use cost. However, the convenience gap is steadily narrowing, placing a structural ceiling on cartridge razor volume growth. This dynamic is particularly evident among younger, tech-savvy consumers who prioritize time efficiency and multifunctionality in grooming routines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Razor Type: Cartridge Systems Retain Lead Through Multi-Blade Innovation

Cartridge razors continue to dominate the global razor market, accounting for approximately 40.12% share in 2025, and are projected to expand at a ~4.2% CAGR through 2031, reinforcing their leadership position. This sustained growth reflects strong consumer preference for premium, multi-blade shaving systems that deliver enhanced comfort and performance. Leading product lines integrate advanced features such as multi-blade configurations, lubricating guards, and precision coatings to reduce irritation while improving shave quality. The segment also benefits from a built-in recurring revenue model, as proprietary cartridge systems encourage repeat purchases and customer lock-in, supporting stable and predictable cash flows for manufacturers. Continuous R&D investments, focused on improving blade longevity, skin protection, and material innovation, are further enabling brands to justify premium pricing and sustain value growth.

In contrast, disposable razors continue to serve price-sensitive consumers and travel-use cases but are facing increasing structural pressure. Growing environmental concerns, particularly around plastic waste and microplastics, alongside tightening regulatory frameworks, are challenging the long-term viability of single-use products. As a result, demand growth in this segment is moderating, with consumers gradually shifting toward more sustainable alternatives.

Safety razors, while representing a smaller share of the overall market, are emerging as a high-growth niche segment driven by environmentally conscious consumers and traditional grooming enthusiasts. Their appeal lies in durability, reduced long-term cost through low-priced replacement blades, and minimal plastic usage. This segment is further supported by the rise of boutique manufacturers and specialty brands that emphasize craftsmanship, customization, and sustainability.

By End User: Women Propel Future Growth

Men continue to dominate razor consumption, generated 68.95% of demand in 2025, supported by established shaving routines and broader product availability. However, the women’s segment is emerging as the fastest-growing category, accelerating at a 4.60% CAGR to 2031, driven by evolving beauty standards, rising disposable incomes in emerging markets, and increasing awareness of personal grooming. Female consumers also exhibit a higher willingness to pay for premium products, particularly those addressing specific needs such as sensitive skin, multi-functional use, and ergonomic design.

The women’s segment is facing growing scrutiny over gender-based pricing disparities, commonly referred to as the “pink tax,” where similar products are priced at a premium. This has prompted regulatory attention in certain markets and is encouraging brands to adopt more transparent and value-driven pricing strategies. The male segment, while dominant, is undergoing structural shifts due to changing grooming habits. The rising popularity of beard and stubble styles has reduced shaving frequency, redirecting demand toward alternative grooming products such as trimmers, beard oils, and styling tools. In addition, increasing adoption of electric grooming devices and laser-based solutions, particularly in developed markets, is intensifying competitive pressure on traditional razors.

By Price Range: Premium Stakes Rise on Sustainability and Skin Science

Mass market products command 70.30% share in 2025, reflecting the price-sensitive nature of razor purchases and the importance of accessibility in driving volume sales. However, premium segments are growing faster at 4.85% CAGR through 2031, indicating successful brand differentiation through technological innovation and superior user experiences. This growth pattern underscores a clear market bifurcation, where consumers are increasingly gravitating toward either value-oriented offerings or premium, performance-driven experiences, leaving mid-tier positioning under pressure. Premium growth is being propelled by advanced product innovations, including heated razors, enhanced lubrication systems, and high-durability materials, which enable brands to justify elevated price points and strengthen margin profiles.

The premium segment is further supported by the introduction of high-end systems featuring lifetime durability, precision engineering, and clinically validated performance claims. Certification labels, such as biobased material ratings and dermatologist endorsements, are playing a critical role in reinforcing perceived product value and building consumer trust. These factors, combined with strong branding and innovation pipelines, are allowing premium products to command significant pricing power.

By Distribution Channel: Online Acceleration Reshapes Retail

Traditional supermarkets and hypermarkets maintain 35.25% market share in 2025, but online retail channels are experiencing rapid growth at 5.07% CAGR through 2031, driven by subscription models and direct-to-consumer strategies that bypass traditional retail markups. This growth is driven by the success of direct-to-consumer (DTC) models, where brands leverage subscription-based offerings to build long-term customer relationships and enhance lifetime value. Subscription platforms are particularly effective in the razor category, given predictable replacement cycles, with average retention periods extending beyond a year. These models provide convenience for consumers while enabling companies to secure recurring revenue streams and gather valuable first-party data for continuous product optimization. Incumbent players are responding by adopting omnichannel strategies, integrating brand-owned websites, major e-commerce marketplaces, and traditional retail partnerships to maximize reach and maintain competitiveness.

Convenience stores and pharmacies remain relevant for impulse purchases and health-oriented positioning, especially for dermatologist-endorsed products. However, ongoing improvements in logistics, bundled pricing strategies, and the growing preference for convenience are expected to further shift demand toward online platforms. While challenges such as high customer acquisition costs and subscriber churn persist, the long-term trajectory indicates a continued redistribution of market share from offline to digital channels.

Geography Analysis

Asia-Pacific remains the largest and fastest-growing region in the global razor market, accounting for a significant share of total revenue and exceeding USD 4.1 billion in 2025, with projections to surpass USD 5.4 billion by 2031. This growth is driven by strong demographic fundamentals, rapid urbanization, and rising disposable incomes across key markets such as China and India. Increasing digital adoption is further accelerating demand, with consumers shifting toward multi-blade systems and subscription-based purchasing models through e-commerce platforms. In India, expanding male grooming expenditure, supported by workplace norms favoring clean-shaven appearances, is reinforcing razor demand as a core category. Meanwhile, in China, large-scale online retail events are boosting premium product visibility, while Japan’s emphasis on precision and quality is supporting the uptake of high-end cartridge systems and locally developed innovations.

North America represents a mature but high-value market characterized by strong brand loyalty and deep product penetration. While unit growth is stabilizing due to the popularity of beard styles and increasing adoption of electric grooming alternatives, value growth continues through premiumization and ongoing product innovation. The region remains a global innovation hub, with leading players investing in R&D, digital marketing, and advanced product development.

Europe is defined by stringent regulatory oversight and strong sustainability mandates, which are accelerating the transition toward eco-friendly materials, solvent-free manufacturing processes, and reduced plastic usage. This has led to increasing traction for safety razors, metal handles, and refillable systems, particularly in environmentally conscious markets such as Scandinavia. While Western Europe remains relatively saturated, Eastern Europe presents growth opportunities driven by rising incomes and improving e-commerce infrastructure.

South America, the Middle East, and Africa continue to represent developing markets with long-term growth potential. These regions benefit from expanding urban populations, increasing grooming awareness, and gradual improvements in digital and retail infrastructure. However, growth remains uneven due to economic volatility, pricing sensitivity, and distribution challenges. As e-commerce penetration improves and younger consumers adopt modern grooming habits, global and regional players are strengthening their presence through localized strategies and adaptive pricing models.

Competitive Landscape

The global razor market remains highly consolidated, with legacy players such as Procter & Gamble (Gillette) and Edgewell Personal Care maintaining dominant positions through extensive product portfolios, entrenched retail partnerships, and global distribution networks. Gillette, in particular, commands a substantial share of global market value, supported by a strong intellectual property portfolio and long-standing retailer relationships, which enable prominent shelf placement. Edgewell, through its Schick brand, continues to hold a secondary position, strengthened by its integration of digitally native capabilities and omnichannel reach.

The competitive landscape is evolving as new entrants and niche players leverage agility, targeted branding, and direct-to-consumer (DTC) models to address shifting consumer preferences. The rise of subscription-based platforms and data-driven marketing has reshaped traditional retail dynamics, enabling brands to build closer customer relationships and enhance lifetime value. Established players have responded by adopting hybrid go-to-market strategies and pursuing acquisitions to strengthen their digital capabilities and maintain competitive relevance.

Strategically, leading players are diversifying beyond traditional shaving into adjacent categories such as skincare, beard grooming, and women’s personal care to capture a broader share of consumer spending. Sustainability, inclusive design, and transparency are emerging as key differentiation levers, particularly among younger consumers who prioritize ethical and environmentally responsible products.

Razor Industry Leaders

-

The Procter & Gamble Company

-

Edgewell Personal Care Company

-

Dorco Co., Ltd.

-

Societe Bic S.A.

-

Feather Safety Razor co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Procter & Gamble Company announced the acquisition of a South Boston site for approximately USD 1 billion to develop a new global headquarters and R&D center for its Gillette brand, alongside a planned expansion of manufacturing operations in Andover, reinforcing its long-term investment in innovation and operational capacity.

- March 2026: Gillette Venus, in collaboration with Rifle Paper Co., introduced its fourth limited-edition collection at Target, featuring a Pubic Hair & Skin Razor equipped with dermatologist-tested anti-irritation technology, highlighting the brand’s focus on premium, skin-sensitive innovations and lifestyle-driven product offerings.

- February 2026: BIC launched the Flex 5 Trim & Shave, a hybrid grooming device combining a detachable trimmer with a five-blade cartridge, distributed via Walmart and Amazon. This marks BIC’s first entry into 2-in-1 wet-shave solutions, targeting consumers seeking convenience and multifunctional grooming tools.

- February 2025: BIC launched the Flex 5 Sensitive razor, featuring a lubricating strip infused with aloe, vitamin E, and licorice. Manufactured in Athens, the product was introduced to the U.S. market through Walmart and Amazon, reinforcing BIC’s focus on skin-friendly innovations for sensitive-shave consumers.

Global Razor Market Report Scope

The razor market comprises a range of grooming tools designed for hair removal, including manual razors and electric shaving devices, used across facial and body grooming routines. The global razor market is analyzed across multiple dimensions, including razor type, end-user, price range, distribution channel, and geography. By product type, the market is segmented into cartridge razors, disposable razors, and safety razors. By End-User, the market is divided into men and women. By price range, it is categorized into mass and premium products. Distribution channels include supermarkets/hypermarkets, convenience/grocery stores, online retail, and other channels such as specialty stores and direct-to-consumer platforms. Geographically, the study covers key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

For each segment, market sizing and forecasts are provided in terms of value (USD billion).

| Cartridge Razors |

| Disposable Razors |

| Safety Razors |

| Men |

| Women |

| Premium |

| Mass |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Razor Type | Cartridge Razors | |

| Disposable Razors | ||

| Safety Razors | ||

| By End-User | Men | |

| Women | ||

| By Price Range | Premium | |

| Mass | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the razor market?

The razor market was valued at USD 11.62 billion in 2026 and is forecast to reach USD 14.05 billion by 2031 at a 3.90% CAGR.

Which product segment is growing the fastest?

Cartridge systems are projected to expand at a 4.16% CAGR through 2031, buoyed by premium innovations such as heated handles and exfoliating bars.

Why are online channels important for razor sales?

Online stores are expanding at a 5.70% CAGR because subscriptions automate refills, enhance convenience, and provide brands with direct customer feedback.

How is sustainability influencing new razor launches?

EU plastics regulation and consumer eco-awareness have accelerated the adoption of stainless-steel safety handles, recyclable packaging, and manufacturer take-back schemes.

What impact does beard fashion have on blade demand?

Beard and stubble styles reduce daily shaving frequency, trimming blade volumes but simultaneously creating opportunities for beard maintenance tools and oils.

Page last updated on: